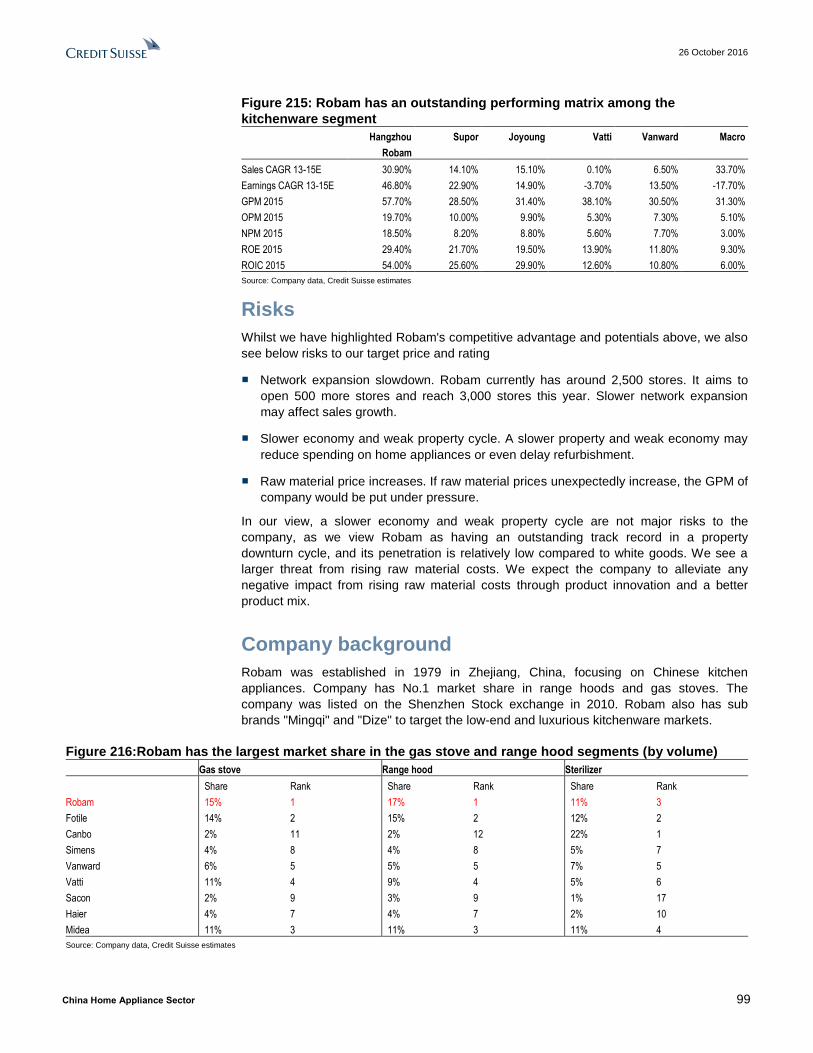

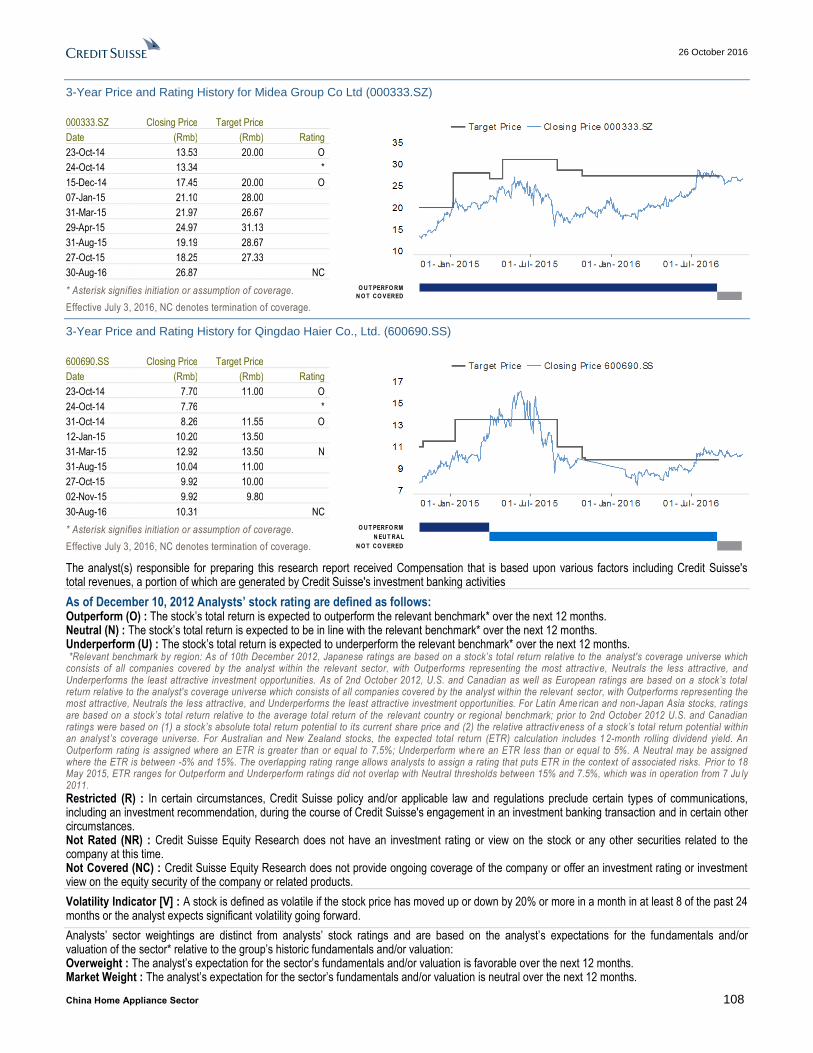

china home appliance sector

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

26 October 2016 Asia Pacific/Hong Kong

Equity Research Consumer Discretionary

China Home Appliance Sector Research Analysts

Raymond Ching

852 2101 7852

Carey Shi

852 2101 7729

ASSUMING COVERAGE

Riding on consumption upgrade and industry consolidation ■ We assume coverage on China's home appliances sector. We forecast

5% sector growth for 2016-18, up from 2% in 2014-15 driven by the end of the air conditioning (AC) price war, product mix enhancement, rising replacement need and strong property cycle starting from 2H15 (delay of 9-12 months). By category, white goods is a mature segment with 3-5% growth. Kitchenware is at a growing stage with a 9% CAGR, supported by low penetration and trade-up. In this report, we initiate on four white goods brands – Midea (OUTPERFORM, TPRmb34.50), Gree (OUTPERFORM, TP Rmb28), QD Haier (OUTPERFORM, TP Rmb12.30), Haier Electronics (NEUTRAL, TP HK$13.40) – and two kitchenware brands – Hangzhou Robam (OUTPERFORM, TP Rmb50.30) and Joyoung (NEUTRAL, TP Rmb21.50).

■ AC rebounds, kitchenware has the fastest growth. AC inventory issues have largely been resolved, and we expect a double-digit sales recovery in 2H16/1H17, which should act as a key share price catalyst for market leaders Gree and Midea. Kitchenware has the highest potential as consumers are trading up. Segment leaders, including Robam, would gain market share with their strong branding and differentiated products.

■ White goods giants eyeing global. With overseas M&As and strong export sales driven by RMB depreciation, we expect overseas sales of QD Haier, Midea and Gree to reach 45%/55%25% in 2017E. Toshiba and GEA acquisitions will help Midea and QD Haier tap into Japan and the US markets while cross-selling their brands to China. KUKA acquisition should enhance Midea's automation and tap into the fast growing robotic market.

■ Our top picks (OUTPERFORMs) are Midea, Robam and Gree. We like Midea for its strongest earnings prospect among white goods players and well-diversified product category, Robam for its strongest momentum as it is the market share taker in the fast-growing imbedded kitchenware segment. We like Gree for its cheap valuation, high dividend yield and accelerated earnings growth on AC restocking. Risks to our rating and TP include consumption trends change, adverse pricing competition and volatile raw material prices.

Figure 1: CAGR forecast for 2016-18

Source: AVC, CMM, IOL, Company data, Credit Suisse estimates

9%

6%

5%

5%

3%

2%

1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Kitctenware Life smallappliances

AC Water heater Washer Fridge TV

26 October 2016

China Home Appliance Sector 2

Focus charts and tables

Figure 2: Industry growth driven by urbanisation Figure 3: Industry is trading up

Source: AVC,CMM,IOL, Credit Suisse estimates Source: NBS,AVC, r Credit Suisse estimates

Figure 4: We expect margin expansion for most of

our coverage companies Figure 5: AC inventory issues almost solved

Source: Credit Suisse estimates Source: AVC, IOL, Credit Suisse estimates

Figure 6: White goods sector trading at 11x P/E Figure 7: Kitchenware sector trading at 19x P/E

Source: Bloomberg, Credit Suisse estimates Source: Bloomberg, Credit Suisse estimates

Figure 8: TP and highlights

Company Name CS Ticker Rating Last Price TP Upside Mkt Cap Trd vol CAGR P/E P/E PEG P/B ROE DY

/Downside US$mn US$ mn 16-18E 2016E 2017E 2017E 2017E 2017E 2017E

Qingdao Haier 600690.SS O 10.3 12.3 19.6% 9,141 40 15.0% 12.4 10.8 0.9 2.0 19% 2%

Midea Group 000333.SZ O 26.8 34.5 28.7% 25,075 128 14.8% 11.7 10.1 0.8 2.4 24% 4%

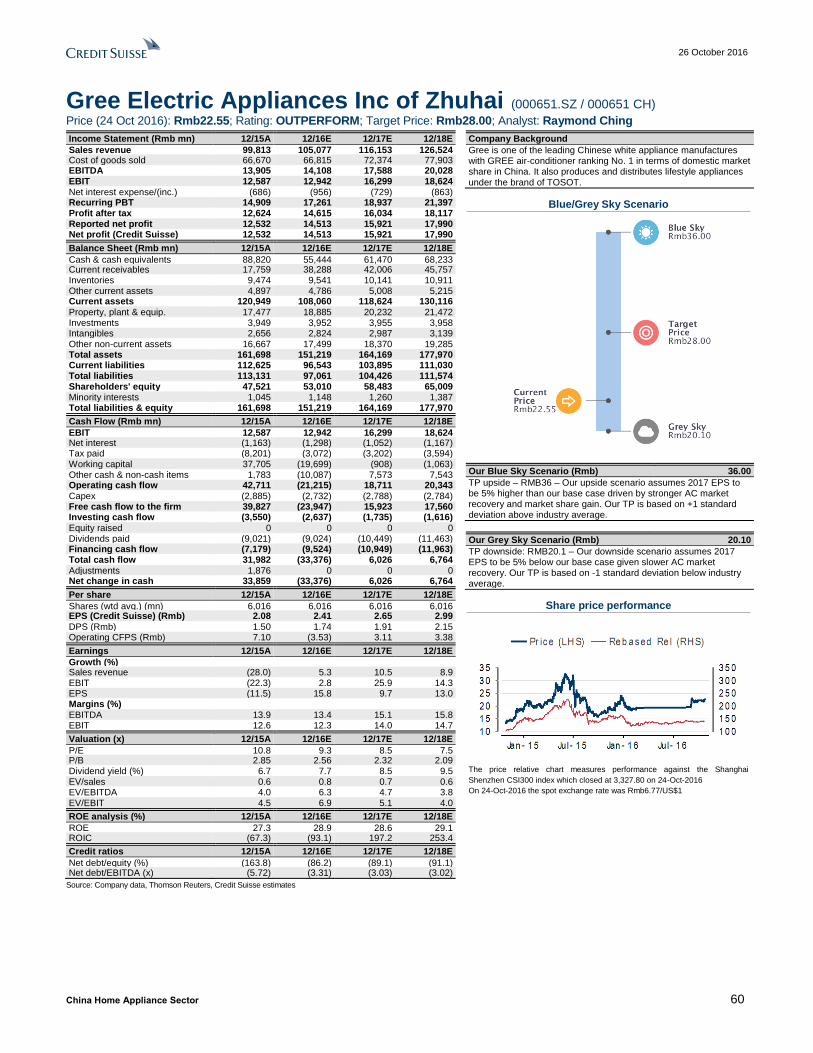

Gree Electric 000651.SZ O 23.0 28.0 21.6% 19,892 138 11.3% 9.5 8.7 0.8 2.4 27% 8%

Haier Electronic 1169.HK N 12.5 13.4 7.0% 4,464 6 10.3% 11.5 10.4 1.1 2.0 15% 1%

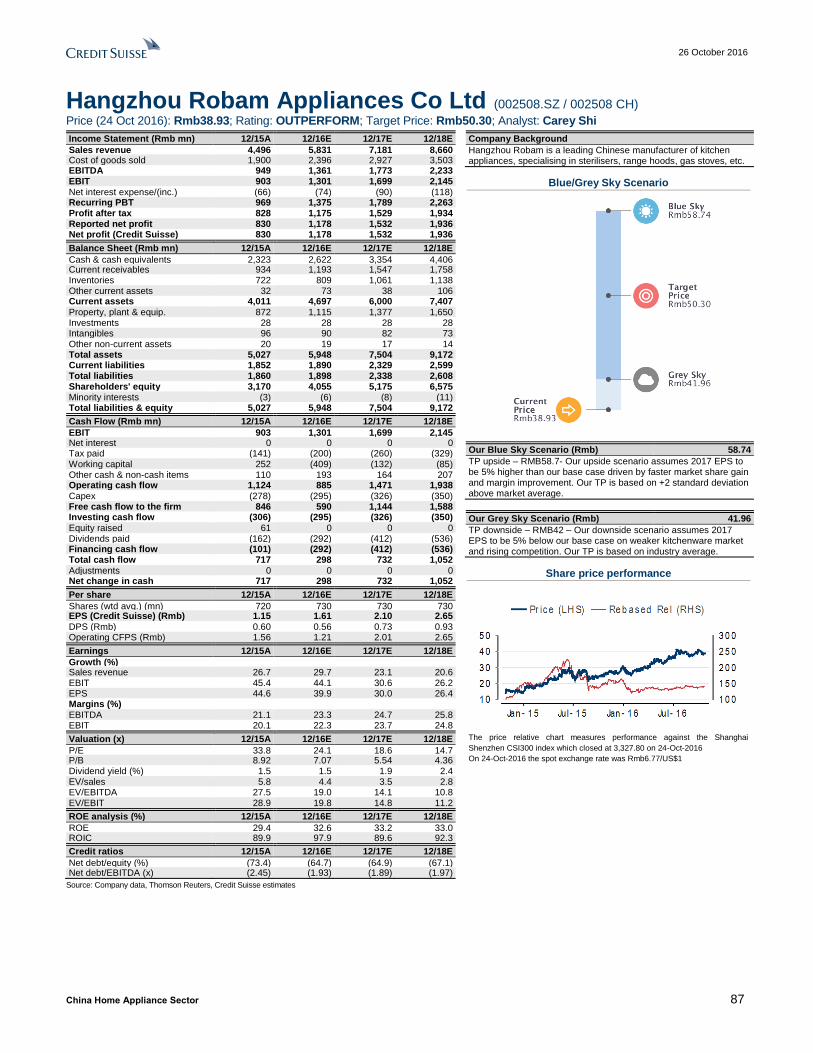

Robam 002508.SZ O 38.6 50.3 30.3% 4,135 25 28.2% 23.9 18.4 0.8 5.5 30% 2%

Joyoung Co 002242.SZ N 19.9 21.5 8.0% 2,266 15 11.5% 22.1 19.7 1.9 4.0 20% 4%

Source: Company data, Credit Suisse estimates price is as of Oct 25, 2016 market close

The authors of this report wish to acknowledge the contribution made by Yvonne Wu, an employee of

Evalueserve, a third-party provider of offshore research services to Credit Suisse

0

20

40

60

80

100

120

140

Color TV Air Conditioner Refrigerator WashingMachine

Water heater

Urban Rural

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2012 2013 2014 2015 6M16AC Washer Fridge Gas stove Range hood Sterilizer

Rmb

0%

5%

10%

15%

20%

25%

Midea Gree QD Haier Haier Elec Robam Joyoung

2016 NPM 2018E NPM

30

40

26

-

5

10

15

20

25

30

35

40

45

2014 Jul 2015 Jul 2016 Jul

mn units

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

Jan10

Apr10

Jul10

Oct10

Jan11

Apr11

Jul11

Oct11

Jan12

Apr12

Jul12

Oct12

Jan13

Apr13

Jul13

Oct13

Jan14

Apr14

Jul14

Oct14

Jan15

Apr15

Jul15

Oct15

Jan16

Apr16

Jul16

Mean: 11

Std: 2.3

Mean

Mean +2 std

Mean -2 std

Mean +1 std

Mean -1 std

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan10

Apr10

Jul10

Oct10

Jan11

Apr11

Jul11

Oct11

Jan12

Apr12

Jul12

Oct12

Jan13

Apr13

Jul13

Oct13

Jan14

Apr14

Jul14

Oct14

Jan15

Apr15

Jul15

Oct15

Jan16

Apr16

Jul16

Mean: 19.3Std: 4.3

Mean -1 std

Mean

Mean +1 std

Mean -2 std

Mean +2 std

26 October 2016

China Home Appliance Sector 3

Riding on consumption upgrade and industry consolidation

Growth: Kitchenware > small appliance > white goods

We expect the home appliance sector growth to accelerate to 5% over 2016-18, faster

than +2% in 2014/15, thanks to the end of the AC price war as channel inventory improves

along with rising replacement needs as sales during 2008-13 driven by government

subsidies program will enter into replacement cycle (normal replacement at 8-10 years for

large appliance). The strong property cycle starting in 2H15 will partially boost sales

demand. We expect the traditional white goods to post stable growth, while we see

strong potential in kitchenware and small appliances categories.

White goods sector: A relatively mature market

White goods segment is at a mature stage. We expect AC, water heater, washing machine

and refrigerator growing at 5%, 5%, 3%, 2% CAGR, respectively. AC and water heater

should have stronger outlook as these two categories are still under penetrated.

Consumption upgrade and replacement needs will be the key drivers. The strong property

market starting in 2H15 will be positive to the sector in 2H16/1H17. Nevertheless,

correlation between property and home appliance sales is gradually diminishing, as

replacement demand is picking up and many new home sales are driven by investment

purpose. In the near term, we see double-digit AC sales growth at the manufacturing

end, which should be key share price catalyst for market leaders Gree and Midea.

White goods giants eyeing global

White goods giants are expanding to overseas through M&As and switching from OEM

(original equipment manufacturer) to OBM (original brand manufacturer). Toshiba and

GEA acquisitions will help Midea and QD Haier tap into Japan and the US markets while

cross-selling their brands to China. KUKA acquisition would enhance Midea's automation

and tap into the fast growing robotic market. Strong R&D capability and RMB depreciation

will strengthen brand image and drive better OBM sales. We forecast overseas to account

for 45%/55%/25% of QD Haier, Midea and Gree in 2017E from 21%/40%/15% in 2015.

Kitchenware: A fast-growing segment

Kitchenware market is at a growing stage. We expect the industry to witnessed a 9%

CAGR over 2016-18 backed by: (1) low penetration rate of 30-40% versus white goods at

70-90%, (2) rising demand driven by aging population and two child policy and (3) upgrade

to better brands and products with more functionality as the Chinese has higher standard

of living. At imbedded kitchenware, consumers are trading up to premium brands such as

Robam and Fotile. At small kitchen appliances, growth is driven by specialisation and

product category expansion. Midea, Joyoung and Supor are the key market players.

Top picks: Midea, Robam, and Gree

With this sector report, we initiate and assume coverage on the four white goods

companies—Midea, Gree QD Haier, Haier Electronic (NEUTRAL) and two kitchenware

companies—Robam (OUTPERFORM) and Joyoung (NEUTRAL). Our top picks are

Midea, Robam and Gree. We like Midea for its strongest earnings outlook at 14.8%

CAGR (0.8 PEG) and well-diversified product categories, Robam for its 28% earnings

CAGR over 2016-18 backed by market share gain in the fast growing kitchenware

segment, and Gree for its attractive valuation at 10.5x P/E (5x ex-cash P/E) along with

accelerating earnings growth of 11.3% 2016-18 CAGR. We rate Joyoung and Haier

Electronic at NEUTRAL as their earnings outlook and valuation are not attractive enough.

26 O

cto

be

r 201

6

Ch

ina H

om

e A

pp

lian

ce

Sec

tor

4

Figure 9: Valuation table

Company Name CS Ticker Price Market Cap Rating TP GPM GPM OPM OPM NPM NPM ROE ROE CAGR P/E PEG P/B

2016E 2017E 2016E 2017E 2016E 2017E 2016E 2017E 16-18E 2017E 2017E 2017E

White good

Qingdao Haier 600690.SS 10.28 9,141 O 12.3 28.8% 29.7% 7.0% 6.7% 4.4% 4.2% 19.1% 18.8% 15% 10.8 0.7 2.0

Hisense Kelon 000921.SZ 11.39 1,893 NC na 24.0% 24.6% 4.8% 5.6% 4.6% 5.3% 24.5% 25.4% 22% 15.6 0.7 3.2

Midea Group Co 000333.SZ 26.8 25,075 O 34.5 29.5% 32.7% 9.5% 10.4% 9.6% 9.9% 24.2% 23.8% 15% 10.1 0.7 2.4

Guangdong Homa 002668.SZ 78.22 1,797 NC na 33.1% 32.2% 8.4% 8.3% 6.2% 6.1% 13.5% 12.6% 18% 30.1 1.7 5.9

Hefei Meiling 000521.SZ 7.02 999 NC na 21.0% 21.4% 2.5% 2.9% 2.0% 2.2% 6.5% 7.3% 20% 21.6 1.1 1.7

Haier Electronic 1169.HK 12.46 4,464 N 13.4 16.7% 16.7% 5.1% 5.3% 4.3% 4.4% 15.3% 14.7% 10% 10.4 1.0 2.0

Whirlpool Chin-A 600983.SS 11.56 1,279 NC na 33.5% 33.7% 6.2% 6.8% 5.9% 6.2% 8.3% 9.1% 24% 19.8 0.8 1.9

Wuxi Little Sw 000418.SZ 34 2,797 NC na 27.1% 27.5% 9.7% 9.9% 7.3% 7.4% 20.0% 20.8% 23% 15.2 0.7 3.6

Gree Electric 000651.SZ 23.03 19,892 O 28.0 36.4% 37.7% 12.3% 14.0% 13.8% 13.7% 27.4% 27.2% 11% 8.7 0.8 2.4

Average 27.8% 28.5% 7.3% 7.8% 6.5% 6.6% 17.6% 17.7% 14% 11.1 0.7 2.2

Kitchenware

Hangzhou Robam 002508.SZ 38.59 4,135 O 50.3 58.9% 59.2% 22.3% 23.7% 20.2% 21.3% 29.0% 29.6% 28% 18.4 0.7 5.5

Zhejiang Supor 002032.SZ 37.26 3,444 NC na 30.0% 30.3% 11.3% 11.8% 9.0% 9.5% 20.3% 20.2% 18% 18.4 1.0 4.5

Joyoung Co 002242.SZ 19.91 2,266 N 21.5 31.9% 31.6% 11.4% 11.1% 9.0% 8.9% 20.2% 20.5% 12% 19.7 1.7 4.0

Guangdong Xinb 002705.SZ 17.34 1,500 NC na 20.1% 20.8% 7.4% 8.5% 5.8% 6.6% 15.6% 17.7% 26% 19.0 0.7 3.5

Zhejiang Meida 002677.SZ 12.62 1,170 NC na 54.3% 56.4% 36.1% 37.7% 31.4% 32.6% 17.9% 20.6% 31% 28.4 0.9 6.7

Vatti Corp Ltd 002035.SZ 25.92 1,383 NC na 42.0% 42.3% 8.1% 9.1% 7.0% 7.7% 17.9% 19.5% 34% 23.5 0.7 5.3

Guangdong Vanward 002543.SZ 17.85 1,130 NC na 33.5% 33.8% 8.9% 9.2% 7.8% 8.0% 12.3% 12.9% 17% 18.2 1.1 2.6

Average 38.7% 39.2% 15.1% 15.9% 12.9% 13.5% 19.0% 20.1% 24% 20.78 1.0 4.6

Note O = Outperform, NC= Not covered. Source: Reuters, Bloomberg estimates for NC companies, Credit Suisse estimates for rated companies

26 October 2016

China Home Appliance Sector 5

Table of contents

Riding on consumption upgrade and industry consolidation 1

Focus charts and tables 2

Riding on consumption upgrade and industry consolidation 3

Growth: Kitchenware > small appliance > white goods 6

White goods: A relatively mature market 8

China white goods giants eyeing global 24

Top picks: Midea, Robam and Gree 36

China Home Appliance Sector through HOLT Lens™ 40

Midea Group Co Ltd (000333.SZ / 000333 CH) 43

Gree Electric Appliances Inc of Zhuhai (000651.SZ / 000651 CH) 59

Qingdao Haier Co., Ltd. (600690.SS / 600690 CH) 72

Haier Electronics Group Co., Ltd. (1169.HK / 1169 HK) 82

Hangzhou Robam Appliances Co Ltd (002508.SZ / 002508 CH) 86

Market share taker in a fast growing industry 86

Joyoung Co Ltd (002242.SZ / 002242 CH) 101

26 October 2016

China Home Appliance Sector 6

Growth: Kitchenware > small appliance > white goods We expect home appliance sector growth to accelerate to 5% over 2016-18 from 2% in

2014-15 led by: (1) the end of the AC price war after inventory overhang issue was

resolved, (2) product mix enhancement and (3) rising replacement demand, as consumer

electronics purchased in 2008-13 during the government subsidies program are entering

into the replacement phase. In addition, the strong property cycle starting from 2H15 will

partially boost sales demand in 2H16 and 1H17, considering the 9-12 months delay effect.

China home appliance sector is made up of multiple categories (see figure 2) and each is

at a different development stage. Overall, when comparing to the developed markets such

as the US, Western Europe and Japan, we still see room for penetration as China’s

urbanisation rate is only 56% versus over 75% for the developed markets.

By category, traditional white goods sector (air conditioning, refrigerator and washing

machines) has entered into a mature stage with stable growth. Traditional TVs are in a

declining stage as consumers are watching media through portable devices such as smart

phones and personal laptops (we have not initiated coverage on TV segment at present).

In contrast, kitchenware and small appliances are in the growing stage supported by new

features and specialisation. Household robots, kitchen waste processor and other

innovative products are in introduction period with huge potential upside, in our view.

Figures 2 and 3 below summarise the growth of major electronic categories as well as

their development cycles.

We expect kitchenware companies including Robam to deliver stronger earnings outlook

than the white goods companies, but we believe that has also reflected in a higher

valuations of kitchenware and small appliance companies.

Figure 10: Home appliances industry growth cycle

Source: Credit Suisse research

Introduction period Growing period Mature period Declining period

Household

robotics

Kitchen-waste

processor

Small

kitctenware

Life small appliances White goods

Traditional TV

Fan

Embedded

kitchenware

26 October 2016

China Home Appliance Sector 7

Figure 11:CAGR forecast for 2016-18

Source: AVC, CMM, IOL, Company data, Credit Suisse estimates

Figure 12: Home appliance sector is expected to

grow at 5% CAGR over 2016-18

Figure 13: TV/AC/Kitchenware are the three biggest

segments in the China market

Source: CMM, Credit Suisse estimates

Source: CMM, Credit Suisse estimates

9%

6%

5%

5%

3%

2%

1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Kitctenware Life smallappliances

AC Water heater Washer Fridge TV

8,001

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Rmb 100 mnAC

20%

Washer7%

Fridge13%

Kitctenware17%

Life small appliances

7%

TV22%

Water heater14%

26 October 2016

China Home Appliance Sector 8

White goods: A relatively mature market China white goods sector is a relatively mature market. We see the industry growing at 3-

5% CAGR over 2016-18 driven by: (1) urbanization, (2) new home sales and (3) product

upgrade/replacement. Based on industry estimate, each factor contributes 25-35%,

20-25%, and 35-45%, respectively.

1) Urbanization drives penetration

In China, the penetration rate for urban area for most appliances are close to the level of

the developed countries, which is more than or close to 100%, and thus volume growth is

capped (see figure 5). We believe urban market growth will be mainly driven by mix and

replacement (average white goods replacement cycle in China is around eight years).

However, AC is a special segment where China's urban area still lags that of developed

countries. China's average AC penetration rate is only 85% versus Hong Kong, Japan,

Taiwan at 223%/147%/135%. Given AC penetration can go up to 200-300% (e.g. two to

three ACs per household), we see room for solid volume growth even in urban areas. In

contrast, we believe washing machine and refrigerator growth in urban areas to be driven

by replacement demand.

We see large growth potential in rural areas of China as the penetration of AC, washing

machine and refrigerator is only at 76%, 14%, and 11%, respectively. We see room for

their penetration rates to catch up to urban area rates during urbanization progress as

income increases.

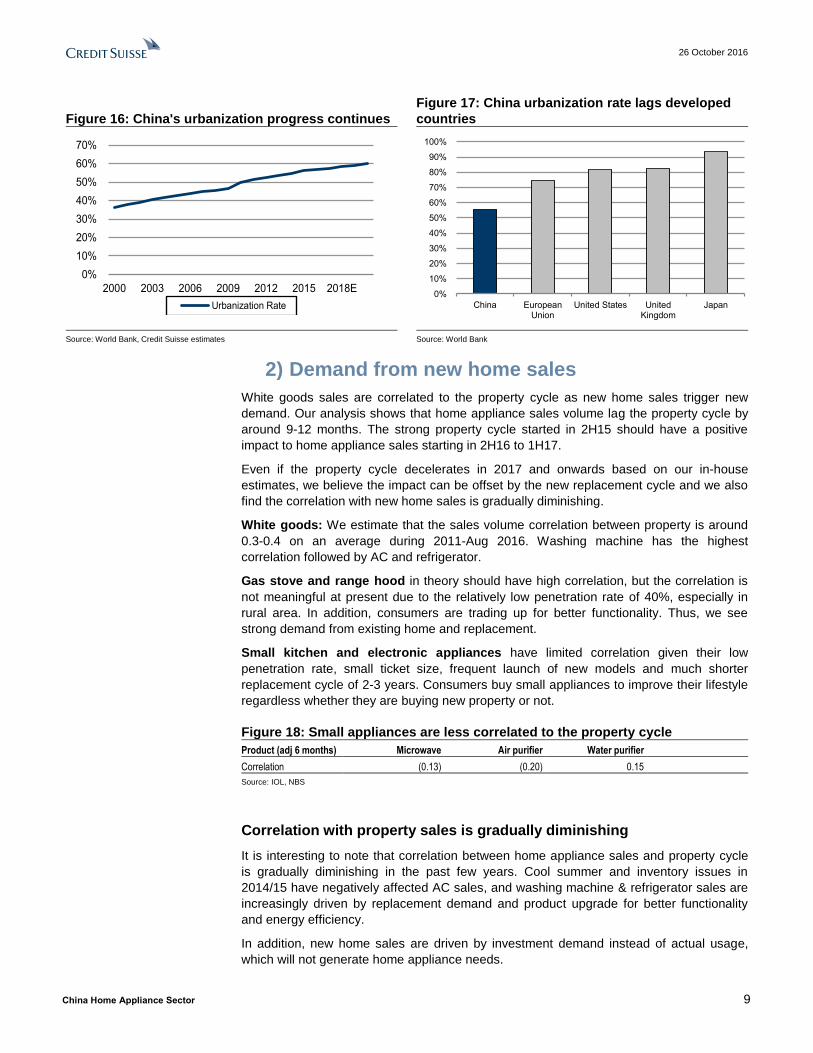

Overall, urbanization rate in China is only 56% in 2015—it is expected that urbanization

rate will increase to 60% by 2020 based on government target. Rising urbanization and

penetration in rural area will be one of the key drivers of white goods' segment growth.

Figure 14: Rural area home appliances are still

underpenetrated Figure 15: AC penetration can go up to 200-300%

Source: NBS, AVC, Credit Suisse Source: Euromonitor

0

20

40

60

80

100

120

140

Color TV Air Conditioner Refrigerator WashingMachine

Water heater

Urban Rural

85

135147

223

0

50

100

150

200

250

China Taiwan Japan Hong Kong

%

26 October 2016

China Home Appliance Sector 9

Figure 16: China's urbanization progress continues

Figure 17: China urbanization rate lags developed

countries

Source: World Bank, Credit Suisse estimates Source: World Bank

2) Demand from new home sales

White goods sales are correlated to the property cycle as new home sales trigger new

demand. Our analysis shows that home appliance sales volume lag the property cycle by

around 9-12 months. The strong property cycle started in 2H15 should have a positive

impact to home appliance sales starting in 2H16 to 1H17.

Even if the property cycle decelerates in 2017 and onwards based on our in-house

estimates, we believe the impact can be offset by the new replacement cycle and we also

find the correlation with new home sales is gradually diminishing.

White goods: We estimate that the sales volume correlation between property is around

0.3-0.4 on an average during 2011-Aug 2016. Washing machine has the highest

correlation followed by AC and refrigerator.

Gas stove and range hood in theory should have high correlation, but the correlation is

not meaningful at present due to the relatively low penetration rate of 40%, especially in

rural area. In addition, consumers are trading up for better functionality. Thus, we see

strong demand from existing home and replacement.

Small kitchen and electronic appliances have limited correlation given their low

penetration rate, small ticket size, frequent launch of new models and much shorter

replacement cycle of 2-3 years. Consumers buy small appliances to improve their lifestyle

regardless whether they are buying new property or not.

Figure 18: Small appliances are less correlated to the property cycle

Product (adj 6 months) Microwave Air purifier Water purifier

Correlation (0.13) (0.20) 0.15

Source: IOL, NBS

Correlation with property sales is gradually diminishing

It is interesting to note that correlation between home appliance sales and property cycle

is gradually diminishing in the past few years. Cool summer and inventory issues in

2014/15 have negatively affected AC sales, and washing machine & refrigerator sales are

increasingly driven by replacement demand and product upgrade for better functionality

and energy efficiency.

In addition, new home sales are driven by investment demand instead of actual usage,

which will not generate home appliance needs.

0%

10%

20%

30%

40%

50%

60%

70%

2000 2003 2006 2009 2012 2015 2018E

Urbanization Rate0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China EuropeanUnion

United States UnitedKingdom

Japan

26 October 2016

China Home Appliance Sector 10

Property sales picked up since 2H15, with sales volume rising by 8% in 2H15 and 27%

YTD; we expect it will trigger better white goods sentiment in 2H16/1H17 taking into

account the 9-12 months lagging effect.

Figure 19: Property market will pick up in 2016E and

slow down in 2017/18E

Figure 20: White goods have diminishing

correlation with property market

Source: NBS, Credit Suisse estimates Source: NBS,IOL Credit Suisse estimates

After the strong momentum in 2H15 and 2016E, our property team is turning more

conservative into 2017E/2018E with projected sales volume to decline by 0.9%/3.5%. We

agree that would have a slightly negative effect to white goods companies in 2H17/2018E

and onwards. Nevertheless, we are not overly concerned, especially for leading white

goods companies given the following:

Correlation is only 0.3 in the past and is on a diminishing trend

A large percentage of property, especially in Tier 1-3 cities are for investment

purpose, which do not generate home appliance sales.

Home appliance segment is entering a replacement cycle starting 2017. The

normal replacement cycle is around eight to ten years—many home appliances

that were bought between 2007 and 2013 triggered by government subsidy

programs are now entering the replacement cycle. The aggregate sales during

2007 to 2013 amounted to Rmb4,800 bn, which is 6.8 times larger than the

annual industry sales of Rmb700 bn, and it's expected to release new demand

gradually.

The strong white goods sales driven by RMB depreciation, stronger Chinese branding and technology should offset a potential domestic sales weakness.

Replacement cycle is shortening as consumers trade up on high-end products

with better functionality and energy efficiency. Many consumers nowadays

replace their home appliance before it is broken/non-functional.

Leading white goods companies are gaining market shares as consumers' trade

up to better brands and quality. We see market consolidation toward the

top 5 companies.

Through M&As and developing own brand sales in foreign market, overseas sales

now accounts for an increasing percentage of the leading white goods companies'

sales. Midea, Gree and QD Haier have strong present in the SE. Asia which is a

growing market.

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

200

400

600

800

1,000

1,200

1,400

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017E

China residential property sold (mn sqm) -LHS YoY change-RHS

mn sqr

-50%

-30%

-10%

10%

30%

50%

70%

1/2012 7/2012 1/2013 7/2013 1/2014 7/2014 1/2015 7/2015 1/2016 7/2016

Property sales YoY AC sales YoY WM sales YoY Fridge sales YoY

26 October 2016

China Home Appliance Sector 11

3) Consumption upgrade drives ASP growth

We see white goods and kitchenware ASP growing at 3%/5% CAGR for the next three

years, compared to 2%/6% CAGR in the past few years. Consumers are trading up for

better functionality, smart features and energy efficiency.

In our view, the consumption upgrade trend will continue and kitchenware will continue to

outgrow white goods as trade-up to high-end brands is more obvious. Among domestic

players, we prefer high-end kitchenware brands such as Robam. Consumers are willing to

pay a premium to buy stylish products, as they see imbedded kitchenware (e.g., range

hood and stove) as part of the renovation.

We also like QD Haier and Midea as they have the broadest smart product offerings (see

table 21), which is one of the key driver of industry ASP growth. Gree has less upside due

to single product category, where it is hard to create a smart eco system and its AC selling

price is already at a 15% premium due to its strong branding.

Figure 21: Home appliances sector is trading up with steady ASP increase

Source: CMM, Credit Suisse estimates

Product mix enhancement

Over the last two years, we see product upgrades in AC/washer/refrigerator in terms of

functionality. Better product mix will engine ASP growth. For example, consumers now buy

AC with low noise, larger size and front load washers, and multiple-door refrigerators for

better food management. The below chart summarise the product mix change in various

key appliance categories.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2012 2013 2014 2015 6M16

AC Washer Fridge Gas stove Range hood Sterilizer

Rmb

26 October 2016

China Home Appliance Sector 12

Figure 22: Inverter AC increased from 57% to 63%

Figure 23: Large size washer increased from 16% to

39%

Source: CMM Source: CMM

Figure 24: Front-load washer increased from 32% to

41%

Figure 25: Multi-door refrigerator increased from 8%

to 18%

Source: CMM Source: CMM

Smart home market—early stage with huge potential

The smart home appliances market is at Rmb90bn, representing 13% of total industry

sales. We expect total smart home market size to double by 2018 with a 26% CAGR due

to low penetration rate. On an average, smart appliances have 20% premium over normal

products. Rising smart appliance will drive industry ASP growth.

Penetration in China is low at 6%/12%/16% for refrigerator, washing machines and AC.

Smart kitchenware penetration is almost zero. CMM expects smart refrigerator/washing

machines/AC penetration to reach 20%/45%/55% in 2020. For Haier, the leading smart

appliances manufacturer only has 15% smart products sales in 2015. We believe the 26%

CAGR is achievable with reference to 78% penetration rate for smart TVs.

57%63%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 7M16Inverter non-inverter

16%

39%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 7M16

>8KG 7-7.9KG 6-6.9KG 5-5.9KG <4.9KG

32%41%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 7M16

Front load Tumbling box Double cylinder Single cylinder

8%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 7M16

side by side multiple door 3 door 2 door single door

26 October 2016

China Home Appliance Sector 13

Figure 26: Smart home market will grow at a fast

pace

Figure 27: Smart home appliances have low

penetration rate

Source: Haier.com, Credit Suisse estimates Source: AVC, CMM

We conducted a channel check and found that for a similar model, products with smart

features are priced at around 15-25% price premium over non-smart products. That said,

consumer preference to smart products will increase ASP for 2% for the next three years.

Figure 28: Retail price for smart and non-smart products

Product Smart price Non-smart price Premium for smart

function

AC Inverter /3rd grade efficiency 3,466 2,932 18.2%

Refrigerator Two door/530L/non-inverter 3,499 3,099 12.9%

Washing machine 7KG/drum type/non-inverter 1898 1498 26.7%

Source: Tmall, GOME, JD

Midea/Haier leading the trend in smart products

Midea and Haier are the leading domestic players with integrated smart appliances

platform. They are the initial domestic brands to develop integrated smart system back in

2014 (U+ for Haier and M+ for Midea), and they offer the largest smart product categories.

90

180

0

20

40

60

80

100

120

140

160

180

200

2015 2020E

26%

Rmb bn

4% 6%

20%

5%

12%

45%

8%

16%

55%

73%78%

93%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 1H16 2020E

Fridge WM AC TV

26 October 2016

China Home Appliance Sector 14

Figure 29: Haier and Midea have broadest smart product categories

Haier Midea TCL Gree Xiaomi Roban Joyoung Skyworth LeTV

Air conditioner Y Y Y Y Y

Air purifier Y Y Y Y Y

Cordless home appliance Y Y

Game Console Y

Refrigerator Y Y Y Y

Smartphone Y Y Y Y

Oven Y Y

Washing machine Y Y

Water heater Y Y

TV Y Y Y Y Y

Robot vacuum cleaner Y Y Y Y

Plug Y

Rice cooker Y Y Y

Kitchen Y

Hood Y

Soymilk machine

Source: Company data, Credit Suisse estimates

Until today, both companies have partnered with Ali, Huawei, Wechat, JD, etc., as well as

international giants including Apple. Midea has also led in Xiaomi with 1.288% stock

offering while Haier has partnered with Meizu.

Amongst white goods leaders, Gree is less active on smart application due to product

concentration. It has partnered with Ali and JD to develop smart ACs. In 2013, the firm

also launched its own Gree smart phone to enlarge its smart product categories. However,

sales of Gree smart phone are way below management and market expectations.

No new government subsidy program at present

We see no new government subsidy program to trigger sales at present. In Nov 2015, the

government launched a new program known as "Energy Top Runner". This program

chose the most energy efficient products and awarded them "Top Runner". It is a

reputational reward rather than monetary benefits.

The passing of government subsides during 2007-13 resulted in a strong 10% sales

CAGR during the period. These subsides partly front loaded the market demand but also

increased penetration, especially in rural areas. This to some extent explained in the

slower market growth in 2014/15 after the program ended. We believe the market should

normalise in 2H16 and onwards.

In 2016, National Development and Reform Commission published a target that by 2020,

two-level efficiency home appliances need to take up at least 50%. Up to August 2016,

two-level efficiency penetration was 32% for AC. Channel check suggests that one-level

efficiency and two-level efficiency are 35% and 15% more expensive than three-level

efficiency ACs , which implies 4% ASP for ACs.

In our view, large brands such as Midea, Haier, and Gree with high production standards

and large R&D investments will benefit from energy-efficiency trends.

26 October 2016

China Home Appliance Sector 15

Figure 30: Government subsidy programs

Time Subsidy Program Applicable products Size

Dec 2007 - Jan 2013 Home appliance to rural (家电下乡) TV, white goods, mobile phone, PC Cumulative sales over Rmb 720bn and sales

volume of ~300mn units

Jun 2009 - Dec 2011 Old for new program (以旧换新) TV, white goods, PC stimulated over Rmb340bn home appliances

consumption

June 2009 - May 2011 Energy saving subsidy (节能惠民) AC, auto, light, motor, etc. stimulated over Rmb70bn home appliances

consumption

June 2012 - May 2013 New energy saving subsidy (新节能惠民) TV, white goods, water heater stimulated over Rmb250bn home appliances

consumption

Nov 2015 - current Top runner (领跑者) White goods that meet the most stringent

energy saving standards

NA

Source: Company data, Credit Suisse estimates

Figure 31: Room to grow for energy-efficient

products

Figure 32: One-level and two-level efficient products

have 35% and 15% price premium

Source: NDRC, CMM Source: CMM,

50%

32%

0%

10%

20%

30%

40%

50%

60%

Government target Current penetration 0

20

40

60

80

100

120

140

160

3-level efficiency 2-level efficiency 1-level efficiency

price index

26 October 2016

China Home Appliance Sector 16

AC: The worst is over, manufacturing sales picking up

With the inventory overhang situation largely over and central AC demand picking up, we

believe the AC sector is ready for a 5% CAGR over 2016-18 at the retail level. Based on

the Jul-Sep IOL data, China domestic AC shipments increased 16%/23%/37% from a low

base versus 32%/10% decline in 1H16 and 2015. Our discussions with major AC

manufacturers suggest a strong expected rebound in AC manufacturing sales in 2H16 and

1H17 driven by low base and solid retail demand.

Market highly concentrated led by Gree

Currently, the market size of AC is around Rmb137 bn, which is 175% and 57% larger

than washing machines and refrigerators, respectively. The market is highly concentrated,

with top three leaders taking 68% share. By value, Gree is the No.1 player with 33%

market share, followed by Midea at 25% and Haier at 11%.

Domestic and foreign brands are priced at similar levels, which to some extent reflect

refined technique and well-established brand image for domestic players. Among domestic

players, Gree has the largest price premium due to strong branding.

Figure 33: AC market size growth

Figure 34: Market breakdown by retail volume

(8M16)

Source:IOL, Credit Suisse estimates Source: CMM

Figure 35: Market break down by retail value (8M16)

Figure 36: Gree has 15% price premium due to

branding

Source: CMM Source: CMM

-12%

-6%

0%

6%

12%

18%

24%

30%

36%

42%

0

20

40

60

80

100

120

140

160

2009 2010 2011 2012 2013 2014 2015

AC market size (LHS) YoY chg (RHS)

Rmb bn

Error! Use the Home tab to apply Report Date to the text that you want

to appear here.

Gree29%

Midea24%

Haier10%

Hisense6%

Aux5%

TCL4%

Chigo5%

Whirpool3%

Others14%

Gree33%

Midea25%

Haier11%

Hisense6%

Aux4%

TCL2%Chigo

3%

Whirpool2%

Others14%

178

115 105 102 102 100 100 95

86 77 73 73

60 49

0

20

40

60

80

100

120

140

160

180

200

Misubishi

Gree

Haier

Foreign

Midea

Industry

Dom

estic

Hisense

Aux

Kelon

Chigo

Whirlpool

TC

L

Electrolux

26 October 2016

China Home Appliance Sector 17

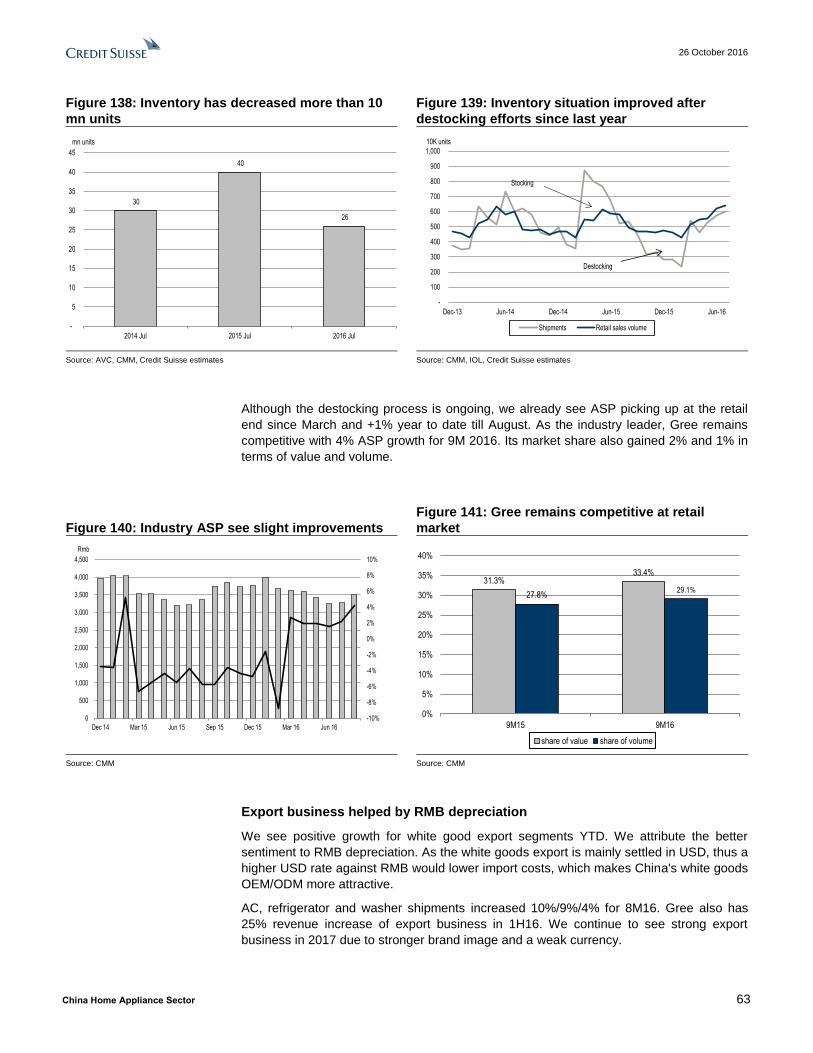

Destocking has largely completed

With record-breaking hot weather in summer 2016 and the aggressive destocking by

leading players since 2Q15, we believe AC inventory level should see significant

improvement after August. Current inventory level is around 26 mn units, compared to 40

mn units a year ago (down 35% YoY and also 10% below the end of summer inventory

level in 2014). Companies are trying to reduce to three-month inventory versus four-/five-

month now, which we believe will take another one to two quarters to achieve.

AC domestic sales volume grew 16%/23%/37% over July-Sep, after 13 months of

consecutive decline. Surging sales brought down more than 10 mn units of inventory

between August 2015 and July 2016.

Companies continue to rationalise their inventory level by reducing shipments to

distributors and shortening production cycle. We believe the destocking process will

continue to help new product sales and increase ASP and margin subsequently.

Figure 37: AC sales surged in June/July this year

Figure 38: Inventory has decreased more than 10mn

units

Source: IOL Source: CMM, IOL, Credit Suisse estimates

Figure 39: Channel inventory problem has improved significantly from 2H15 to

1H16

Source: IOL, CMM, Credit Suisse estimates

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

100

200

300

400

500

600

700

800

900

1,000

Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Oct 15 Jan 16 Apr 16 Jul 16

Domestic shipments YoY change

mn units

30

40

26

-

5

10

15

20

25

30

35

40

45

2014 Jul 2015 Jul 2016 Jul

mn units

-

100

200

300

400

500

600

700

800

900

1,000

Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16

Shipments Retail sales volume

10K units

Destocking

Stocking

CMM, IOL, Credit Suisse estimates

26 October 2016

China Home Appliance Sector 18

Central AC—domestic brands catching up

Central AC market is around Rmb69 bn. We expect central AC to witness a 7% CAGR in

the next three years, slightly faster than household ACs. Domestic leading brands such as

Midea, QD Haier and Gree should enjoy faster growth due to market share gains.

Foreign brands still dominate the market at this stage, but domestic brands are capturing

market share rapidly. We see the domestic brand share increasing gradually from 34% in

2014 to 45% in 1H16.

A central AC has more elegant display than a traditional one and does a better job in

matching overall in-house decoration. It is also more energy-efficient, which coincides with

the consumption trend and government guidance. Individual housing, commercial areas

including offices, shopping malls, subways, etc., can use central ACs.

Daikin, Midea and Gree are the leading brands with 18%, 17% and 16% market share,

respectively. We expect the central AC business to outgrow the residential business for

Midea and Gree's, as the central AC business has high entry barrier and requires strong

reputation.

Figure 40: Midea, Daikin, Gree led central AC market Figure 41: Domestic brands gaining market share

Source: IOL Source: Aircon.con

Washing machine/refrigerator—stable growth driven

by replacement needs and export sales

Washing machine and refrigerator are mature segments with less growth potential due to

high penetration. Segment growth will be mainly driven by replacement needs and export

sales. We expect replacement needs to increase starting from 2017, as sales boosted by

government subsidies programs in 2007-13 will enter into the replacement cycle. Strong

export sales is another growth driver, as domestic brands are stronger and develop better

sales channels overseas. We see washer/refrigerator record 4%/9% export sales growth

YTD.

QD Haier is No.1 in both segments, with 27%/28% market share in washer/refrigerator.

We expect its leading position to remain, backed by mid-to-high end position in the context

of consumer trade-up and strong presence in smart appliance. Starting in late 2015, QD

Haier also launched more SKUs with price below Rmb2,000 for washer/refrigerator to take

shares of customers who are more price sensitive.

Daikin+McQuay18%

QD Haier7%

Midea17%

Gree16%

York5%

Carrier4%

Hitachi8%

Others25%

34%

45%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2011 1H16

26 October 2016

China Home Appliance Sector 19

Figure 42: Washing machine market share (8M16 in

value) Figure 43: Refrigerator market share (8M16 in value)

Source: CMM Source: CMM

Figure 44: Refrigerator has 9% export growth YTD

(volume)

Figure 45: Washer has 4% export growth YTD

(volume)

Source: IOL Source: IOL

Haier27%

Little Swan17%

Midea5%

Siemens14%

Sanyo6%

Panasonic8%

Hisense2%

Samsung5%

Others16%

Haier28%

Midea11%

Rongsheng11%

Meiling9%

Hisense4%

Siemens12%

Xinfei2%

Electrolux1%

Others22%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

50

100

150

200

250

300

350

Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Oct 15 Jan 16 Apr 16 Jul 16

Sales volumn YoY

10k units

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

20

40

60

80

100

120

140

160

180

Jul 14 Oct 14 Jan 15 Apr 15 Jul 15 Oct 15 Jan 16 Apr 16 Jul 16

Export sales volume (LHS) YoY (RHS)

10k units

26 October 2016

China Home Appliance Sector 20

Upgrade drives GPM, raw material is controllable

In general, home appliance companies' GPM has been rising in the past few years driven

by higher ASP from stronger branding and product mix enhancement, cheaper raw

material costs, efficiency enhancement and economies of scale. Among the key

categories, kitchenware saw the highest margin expansion driven by consumption

upgrade, followed by AC, refrigerator, and washing machine.

Raw material cost accounts for about 70% of COGS for white goods. Major raw materials

include plastic, steel, copper, and aluminum. Comparing prices in 2013 versus now,

copper/aluminum, cold-rolled steel, stainless steel and polypropylene have decreased by

28%, 12%, 26%, 23%, and 43%, respectively. We see a slight raw material price increase

since 2016, but still within the historical low range.

We conducted a sensitivity analysis on the raw material hike impact to white goods GPM

and summarised on the table below. Overall, we believe that raw material is a controllable

risk. In the worst case scenario, where all raw material prices go up together (which in our

view is highly unlikely based on historical trend), we estimate that a 1% ASP increase can

offset a 2% increase in overall raw material prices (see figure 48).

As the white goods market is highly concentrated and all major players are listed

companies, we expect the white goods companies to likely raise prices to pass through

cost pressure to end consumers.

Overall, we expect the industry ASP to increase by 3% per annum driven by the positive

factors that we discussed above. We continue to see industry GPM to slightly increase

going forward and raw material should be a controllable risk, in our view.

Figure 46: GPM of our coverage companies

Company Ticker 2013 2014 2015 2016E 2017E 2018E

Midea 000333.SZ 23% 25% 25% 30% 33% 33%

Gree 000651.SZ 23% 25% 25% 30% 33% 33%

QD Haier 600690.SS 25% 27% 28% 29% 30% 30%

Haier Electronics 1169.HK 15% 15% 16% 17% 17% 17%

Robam 002508.SZ 54% 57% 58% 60% 60% 60%

Joyoung 002242.SZ 34% 33% 32% 33% 32% 32%

Source: Company data, Credit Suisse estimates

Figure 47: GPM sensitivity to the change in raw materials and ASP

Gross margin chg (%)

Factor change AC Washing machine Refrigerator

Plastic -0.07 -0.11 -0.18

Copper -0.17 -0.04 -0.11

Steel -0.15 -0.32 -0.18

Labor -0.08 -0.09 -0.09

ASP 0.68 0.7 0.71

Source: Company data, Credit Suisse estimates

26 October 2016

China Home Appliance Sector 21

Figure 48: AC COGS breakdown Figure 49: Washing machine COGS breakdown

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 50: Refrigerator COGS breakdown Figure 51: Copper/aluminum price trend

Source: Company data, Credit Suisse estimates Source: CEIC

Figure 52: Steel and plastic price trend Figure 53: Raw material price YoY change

Source: CEIC, Thomson Reuters Datastream Source: CEIC, Thomson Reuters Datastream

Steel22%

Plastics10%

Copper25%

Labour12%

Others31%

Steel44%

Plastics15%

Copper6%

Labor13%

Others22%

Copper15%

Steel25%

Plastics25%

Labor13%

Others22%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2011 2012 2013 2014 2015 2016

Copper aluminum

Rmb/ton

0

5,000

10,000

15,000

20,000

25,000

30,000

2011 2012 2013 2014 2015 2016

Stainless steel Cold rolled steel Polypropylene

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

2012 2013 2014 2015 2016

Copper YoY Aluminum YoY Polypropylene YoY

Stainless steel YoY Cold rolled steel YoY

26 October 2016

China Home Appliance Sector 22

Slight margin premium over international brands is sustainable

Compared to the global brands, China white goods sector GPM/OPM was 28%/7%,

compared to 27%/6% for the international players. In our view, the slight margin premium

for the domestic brands is attributed to: (1) almost 100% in-house production, (2)

economies of scale and (3) stronger bargaining power against the channel operators.

Domestic brands manufacture almost 100% in-house and they also do OEM/ODM for

international companies. Meanwhile, their production scales are also larger than many

international brands which lead to stronger raw material power and production efficiency.

On the channel front, for domestic players only 20% of sales are contributed to chain

channels (such as Gome and Suning), while the rest of the sales go towards distributors

and e-commerce platform. In contrast, chain channel is the dominating channel for

international brands, where channel players have stronger bargaining power. This partly

explains the slightly lower OPM for the international brands.

Based on our discussions with industry players, OPM for e-commerce, traditional

distribution and key accounts (chains stores such as Gome and Suning) are similar, while

kitchenware companies generate higher OPM from e-commerce channel as they are self-

operated. Looking forward, we expect e-commerce and traditional channels to be growing

faster than key accounts channel as: (1) the young generation tends to shop online and (2)

e-commerce is under-penetrated in rural areas. We believe the channel changes are

neutral to white goods companies but are positive to kitchenware players as higher sales

mix from e-commerce will increase group GPM.

Export margin is expanding

We expect overseas sales to contribute a larger percentage to white goods companies'

revenue and have higher margin going forward. Majority of the revenue increase is driven

by acquisitions of international brands, which makes similar margin to the existing

business. We see room for margin expansion from sourcing and production synergies. For

the pure export business, their NPM is around half of the domestic business, but their

GPM has been improving from 2012 to 1H16. We expect the rising trend to be sustainable

because of: (1) higher sales mix from better margin OBM model (from ODM/OEM) as

Chinese brands are having stronger brand image globally, (2) RMB depreciation which

also boosted export GPM as export prices are mainly settled in USD and (3) overall export

ASP which has been rising as Chinese players' quality and technology are

becoming better.

26 October 2016

China Home Appliance Sector 23

Figure 54: Chinese companies have slight margin

premium over international brands

Figure 55: Export GPM is expanding for domestic

white goods players

Source: Bloomberg, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Note: 1H2016 data for QD Haier is not available. 2015 leap for QD Haier is mainly due to revenue calculation method change

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

GPM OPM NPM

China International

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2012 2013 2014 2015 6M2016

Gree Midea Haier

26 October 2016

China Home Appliance Sector 24

China white goods giants eyeing global With overseas M&A, asset injection from parent companies, and increasing OBM shares,

overseas markets are increasingly becoming important for Chinese white goods giants. In

2015, overseas market accounted for 21%, 40%, and 15% of QD Haier, Midea and Gree,

respectively, and we expect it to expand to 45%/55%/25% in 2017.

At present, we see limited overseas exposure in kitchenware brands due to different

dietary habits. Meanwhile, the kitchenware companies are relatively smaller versus the

white goods giants with less capex for overseas acquisitions.

While overseas GPM is much lower than domestic market at present, we expect overseas

gross margin to trend upwards due to better pricing power, channel expansion, and brand

building. With recent overseas acquisitions e.g. Toshiba, KUKA and GE, we expect more

synergies will kick in and further boost export sales and margin in the future. We will

provide more details in our company discussions.

Figure 56: White goods export sales share picked

up since 2015 Figure 57: Leading brands export share increases

Source: IOL Source: Company data, Credit Suisse estimates

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2011 2012 2013 2014 2015 8M2016

AC Washing machines Fridge

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2010 2011 2012 2013 2014 2015 6M2016

Gree Midea QD Haier

26 October 2016

China Home Appliance Sector 25

Figure 58: Export margin improved for Midea, Gree, and QD Haier

Source: Company data

Note: 1H2016 data for QD Haier is not available. 2015 leap for QD Haier is mainly due to revenue calculation method change

From OEM to OBM

Looking forward, home appliance companies will focus on expanding their own branding

business overseas as their technology and R&D are now comparable or exceeded

international companies after many years of development. Meanwhile, companies can also

leverage on their overseas acquisitions' channel to launch their brands.

In 1H16, overseas accounted for 30% of the leading white goods companies sales, of

which around 30% were own brand sales (OBM) with the rest being ODM and OEM. Haier

was the exceptional case with all its overseas sales coming from the OBM business. Its

core markets are SE. Asia and African countries.

At present, OBM does not have a huge margin advantage over ODM and OEM as Chinese

brands have relatively low brand premium in overseas market. However, OBM is crucial for

brand establishment and beneficial for higher margin in the long run.

Figure 59: Midea has the highest overseas revenue share

(1H16) Overseas revenue % GM of export business * OEM% of export sales

Midea 43.8% 24.8% 1/3

Gree 24.2% 21.2% 1/3

QD Haier 28.7% 17.3% All own brand sales

Joyoung 1.9% 24.2% All own brand sales

Robam 1% na na

Source: Company data, Credit Suisse estimates

Overseas volume growth driven by M&A

Besides overseas OBM and ODM, almost all major domestic brands have initiated M&A to

expand their overseas business. We see good export business upside as cost synergies

will kick in through sharing R&D/sourcing and product offering expansion. By acquiring

local brands, domestic manufacturers are able to utilize local production landscape and

leverage sales network of acquired brands.

Midea acquired Toshiba's white goods section in early 2016, which will increase Midea's

turnover by 5-10% going forward. QD Haier acquired GE appliances in January 2016,

which will increase its turnover by 25-45% starting from 2H16. We expect two to three

years for these international brands to be fully integrated into parent-co and realise

maximum synergies. The below table summarises the recent overseas acquisitions.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2012 2013 2014 2015 6M2016

Gree Midea Haier

26 O

cto

be

r 201

6

Ch

ina H

om

e A

pp

lian

ce

Sec

tor

26

Figure 60: Recent domestic brands M&A

Ticker Time Target Sector Consideration Financing Current Stage

600060 CH 7/31/2015 100% of Sharp Mexico TV USD 23.7M; Sharp Mexico 2014 net assets

around RMB345.32M to use "sharp" brand

and all its channel resources in America

Internal resources Completed

000333 CH 3/17/2016 80.1% of Toshiba White goods Sector

(Japan)

Appliances JPY53.7B for 40 yrs trademark authorisation

rights & over 5K patents

Internal resource & debt

financing

Completed in June, Financial statements

consolidated in 1H16

5/26/2016 KUKA (Germany) Robotics EUR115/shr, 35% premium to stock price;

EUR 3.7B if transaction complete

Internal resource & debt

financing

Pending reviews; deal will complete in March

2017 at the latest; 81.04% agreed to sell

+13.51% original stake=94.55% share in total if

complete

6/21/2016 80% of Clivet (Italy) Central AC specific consideration not disclosed; 2015

Clivet sales is EUR120M -3% of European

chillers

No disclosure Definitive agreement assigned, pending anti-

monopoly reviews; expect to complete before

2016 YE

600690 CH 1/14/2016 GE Appliances Sector (US) Appliances USD 5.58bn, 10x EV/EBITDA internal resources & USD3.3B

loan from Chinese development

bank

Conducting audit on target assets; board

meeting/US/Mexica competition premerger office

approved

7/28/2011 White goods section in Japan and

Indonesia of Sanyo (Japan)

Home Appliances JPY 10B No disclosure Completed, was injected to QD Haier in 2015

9/10/2011 80% of Fisher& Paykel (New Zealand) Home appliances 9.87 NZD; 12.56x EV/EBITDA, 1.53x P/B No disclosure Completed, plan to inject assets to QD Haier in

2020

751 HK 6/10/2014 Sinoprima (South Africa) TV/ display monitor Rmb30M for net asset negative Rmb62M net

asset

No disclosure Completed

5/7/2015 METZ (Germany) partial asset

including LCD/LED TV sections

TV no disclosure No disclosure Completed

9/25/2015 Toshiba Appliances no specific number for 5% of Toshiba Nanhai

& Toshiba Shenzhen companies

No disclosure Completed

12/21/2015 Toshiba Consumer Products

Indonesia factory

TV/Washing machines USD25M-30M, no specific disclosure No disclosure Completed on May 16, 2016, but Midea acquired

Toshiba white goods sector later so co-operation

with Toshiba may not continue

00810 CH 7/21/2015 Strong Media (Europe) TV set up boxes EUR 30M Offshore bank financing Completed

2317 TW started in 2012

and completed

in 2016

Sharp (Japan) TV JPY 88B (about USD3.5B) for 66% of Sharp No disclosure Completed in March 2016

300172 CH 7/26/2016 Vizio (US) Smart TV USD2B No disclosure Completed

1070 HK 3/31/2014 90% Stake of Sanyo Mexico Electronic products USD15.22M Internal resource Completed

Source: Company data, Credit Suisse

26 October 2016

China Home Appliance Sector 27

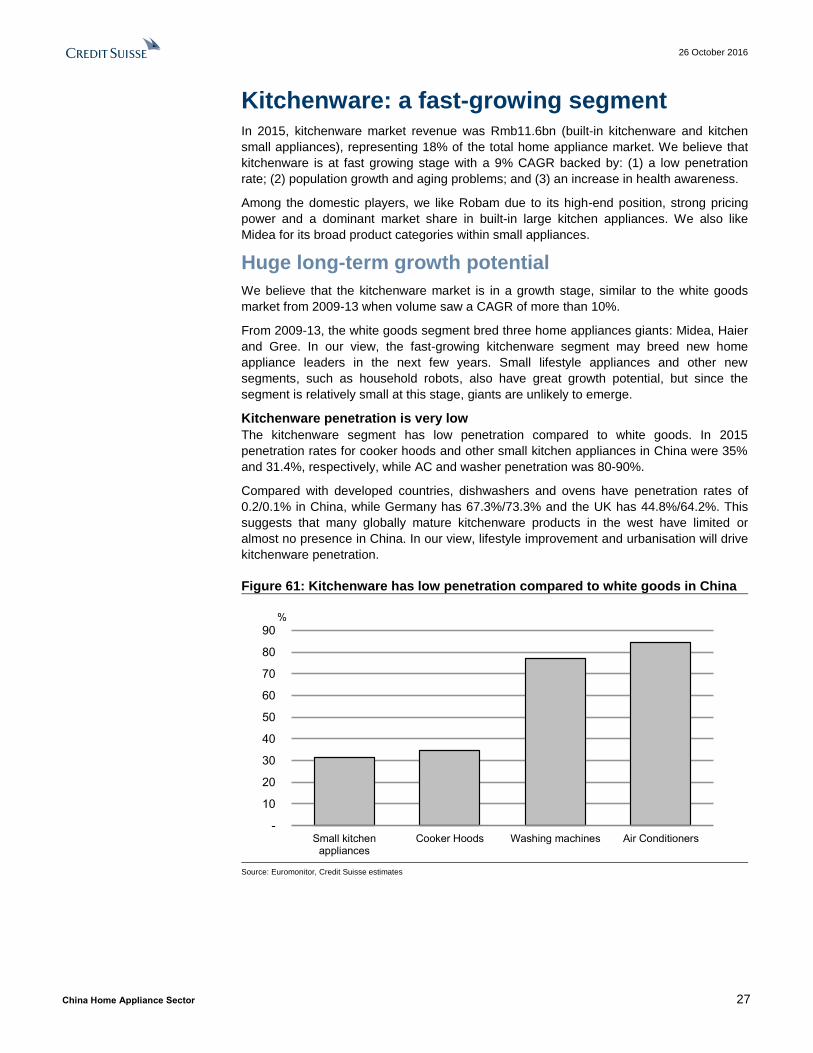

Kitchenware: a fast-growing segment In 2015, kitchenware market revenue was Rmb11.6bn (built-in kitchenware and kitchen

small appliances), representing 18% of the total home appliance market. We believe that

kitchenware is at fast growing stage with a 9% CAGR backed by: (1) a low penetration

rate; (2) population growth and aging problems; and (3) an increase in health awareness.

Among the domestic players, we like Robam due to its high-end position, strong pricing

power and a dominant market share in built-in large kitchen appliances. We also like

Midea for its broad product categories within small appliances.

Huge long-term growth potential

We believe that the kitchenware market is in a growth stage, similar to the white goods

market from 2009-13 when volume saw a CAGR of more than 10%.

From 2009-13, the white goods segment bred three home appliances giants: Midea, Haier

and Gree. In our view, the fast-growing kitchenware segment may breed new home

appliance leaders in the next few years. Small lifestyle appliances and other new

segments, such as household robots, also have great growth potential, but since the

segment is relatively small at this stage, giants are unlikely to emerge.

Kitchenware penetration is very low

The kitchenware segment has low penetration compared to white goods. In 2015

penetration rates for cooker hoods and other small kitchen appliances in China were 35%

and 31.4%, respectively, while AC and washer penetration was 80-90%.

Compared with developed countries, dishwashers and ovens have penetration rates of

0.2/0.1% in China, while Germany has 67.3%/73.3% and the UK has 44.8%/64.2%. This

suggests that many globally mature kitchenware products in the west have limited or

almost no presence in China. In our view, lifestyle improvement and urbanisation will drive

kitchenware penetration.

Figure 61: Kitchenware has low penetration compared to white goods in China

Source: Euromonitor, Credit Suisse estimates

-

10

20

30

40

50

60

70

80

90

Small kitchenappliances

Cooker Hoods Washing machines Air Conditioners

%

26 October 2016

China Home Appliance Sector 28

Figure 62: China kitchenware penetration lags developed countries

2015 penetration rate

(%)

China US France Japan Germany UK

Dishwashers 0.2 63.1 44.9 18.7 67.3 44.8

Ovens 0.1 10.3 38.1 3.5 73.3 64.2

Microwaves 22.8 84.9 86.2 84.5 71.8 91.5

Food processor 24.9 170 124.3 29.5 103 98.3

Coffee Machines 0.1 154.6 103.6 7.6 95.6 50

Source: Euromonitor

Aging population and two child policy drive kitchenware demand

In our view, the two-child policy and aging problems will contribute to kitchenware sector

growth. Babies and elderly require additional care due to food safety issues in China. We

expect new-born babies and the aging population to require more in-home cooking thus

benefiting kitchenware sales.

According to our in-house estimates, the two-child policy will bring an additional 3-5 mn

babies from 2017 onwards, assuming an annual application rate of 5-10% for the currently

eligible 60 mn couples. This means a population boost of 17-33% from the current 16.5

mn new-born babies per year from 2017 onwards.

China's population is aging. In 2015, people aged over 65 years old amounted to 144 mn,

10.5% of the total population. We expect this number to see a CAGR of 5.1% over the

next five years and reach 180 mn in 2020, representing 13% of the total population.

Figure 63: We expect 3-5 mn new babies starting

from 2017E

Figure 64: We expect the elderly population to see a

5.1% CAGR from 2016-20

Source: NBS, Credit Suisse estimates Source: NBS, Credit Suisse estimates

Rising health cautiousness

According to a Boston Consulting Group survey, Chinese consumers have very strong

health awareness, with 73% willing to pay a premium for healthier products, which is 12%

more than the global average.

With increasing food safety issues, in the 2016 BCG survey food safety is the top choice

among all other factors that interviewees were unsatisfied with. Therefore, we see robust

growth of health-related appliances, such as blenders, that can break food cells and slow-

speed juicers that can better maintain fruit nutrition. We see continuous growth in the

kitchenware segment, especially small appliances.

14

15

16

17

18

19

20

21

22

23

2010 2011 2012 2013 2014 2015 2016E 2017E

Born under one-child policy additional babies

mnn

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

People above 65 years old Growth % of total population

13%mn

26 October 2016

China Home Appliance Sector 29

Figure 65: Chinese consumers have high health awareness

Source: BCG

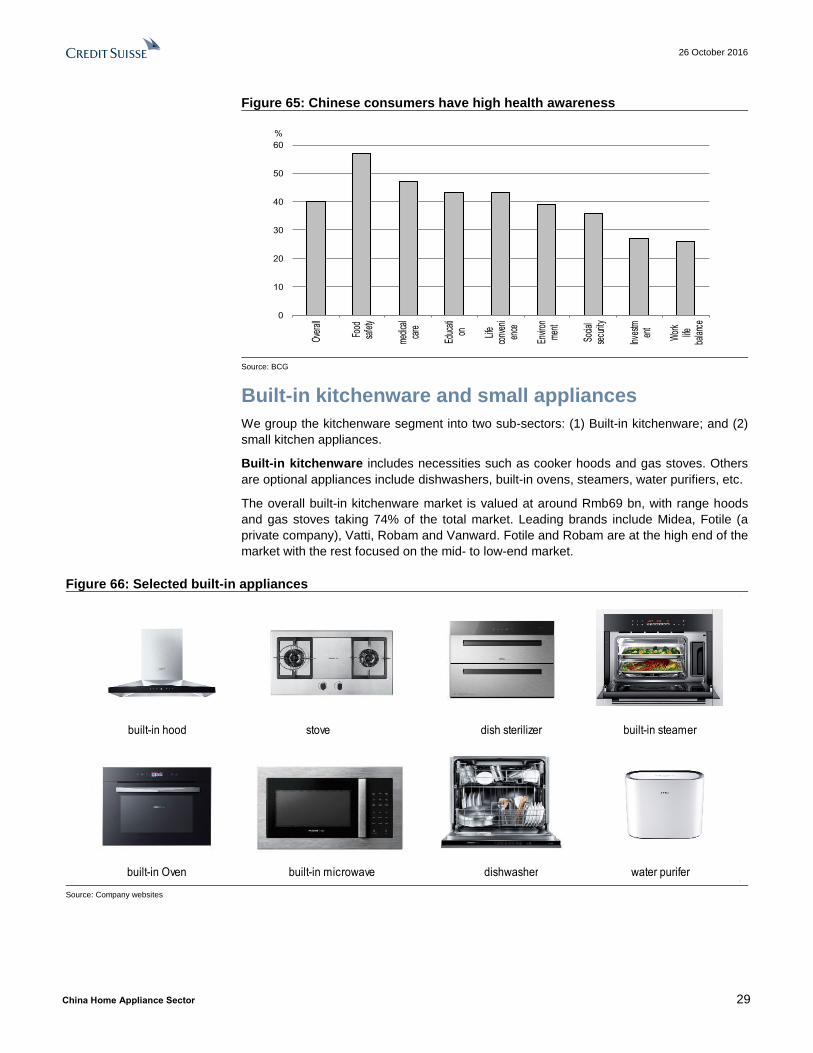

Built-in kitchenware and small appliances

We group the kitchenware segment into two sub-sectors: (1) Built-in kitchenware; and (2)

small kitchen appliances.

Built-in kitchenware includes necessities such as cooker hoods and gas stoves. Others

are optional appliances include dishwashers, built-in ovens, steamers, water purifiers, etc.

The overall built-in kitchenware market is valued at around Rmb69 bn, with range hoods

and gas stoves taking 74% of the total market. Leading brands include Midea, Fotile (a

private company), Vatti, Robam and Vanward. Fotile and Robam are at the high end of the

market with the rest focused on the mid- to low-end market.

Figure 66: Selected built-in appliances

Source: Company websites

0

10

20

30

40

50

60

Ove

rall

Food

safe

ty

med

ical

care

Educ

ati

on Life

conv

eni

ence

Envir

onm

ent

Socia

lse

curit

y

Inve

stmen

t

Wor

klife

bala

nce

%

built-in hood stove dish sterilizer built-in steamer

built-in Oven built-in microwave dishwasher water purifer

26 October 2016

China Home Appliance Sector 30

Figure 67: Built-in kitchenware market

breakdown(value)

Figure 68: Built-in kitchenware market breakdown

(shipments)

Source: CMM Source: Euromonitior

Figure 69: Range hood market brand share(8M16

value)

Figure 70: Gas stove market brand share

(8M16value)

Source: CMM Source: CMM

Small kitchen appliances feature much more selection. The market size is around

Rmb47 bn. Popular appliances include necessities, such as rice cookers and water

heaters, which constitute around 45% of total small appliances. The rest are noodle

machines, soybean makers, juicers, bread makers, etc. Leading brands include Midea,

Supor, Joyoung and Donlim.

By volume, Euromonitor expects small kitchen appliance will to experience a 5% CAGR

from 2016-18E. Given average selling price (ASP) increases, we expect the market size to

see a 9% CAGR.

dishwasher1%

microwave10%

gas stove28%

range hood46%

sterilizer9%

oven6%

2,000 1,900

1,026

787

400

20

-

500

1,000

1,500

2,000

2,500

range hood gas stove microwave oven sterilizer dishwasher

10k units

Robam31%

Fotile28%

Midea12%

Vatti11%

Vanward4%

Macro4%

Siemens6%

Sacon4%

Robam23%

Fotile22%

Midea7%

Vatti12%

Vanward4%

Macro3%

Siemens5%

Others24%

26 October 2016

China Home Appliance Sector 31

Figure 71: Selected kitchen small appliances

Source: Company websites

Figure 72: Small kitchen appliance breakdown by

value Figure 73: Small appliance brand share

Source: CMM, Credit Suisse Source: CMM, Credit Suisse

Figure 74: selected kitchen small appliances brand share

Rice cooker Electric

kettle

Pressure

cooker

Induction

cooker

Soymilk

machine

Electric pot Juicer Blender Baking pan

Midea 41% 30% 42% 46% 21% 26% 24% 31% 40%

Joyoung 27% 21% 28% 19% 14% 11% 16% 7% 21%

Supor 14% 20% 19% 21% 62% 11% 44% 49% 16%

Others 18% 29% 11% 14% 3% 52% 16% 13% 23%

Source: Company data, CMM

deep fryer coffee machine soybean machine water heater

rice cooker induction cooker pressure cooker electric pot

Rice cooker32%

Induction cooker16%

Pressure cooker13%

soymilk maker12%

juicer9%

electric kettle8%

Blender5%

coffee machine3%

Others2%

OUTPERFORM

Midea41%

Joyoung27%

Supor14%

Others18%

26 October 2016

China Home Appliance Sector 32

Consumers are trading up

We expect ASPs to see a 5% CAGR from 2016-18E as consumers trade up to high-end

functional products We see more room for ASP increases in kitchenware than the

traditional white goods segment due to more new model launches and more obvious

market consolidation. In short, kitchenware is still in a growing phase.

Kitchenware ASPs have surged 20-30% in the past four years. In the built-in-kitchenware

segment, consumers are more inclined to buy high-end products with high air flow rates,

low noise and modern appearance. In the small appliance segment, we see major

upgrade progress in rice cookers from non-induction heating (IH) to IH due to rising

requirements by Chinese for food quality.

The high-end market is expected to benefit most from this trend. Premium brands Fotile

and Robam expanded their market share from 25% in 2008 to more than 40% in 2015. We

continue to see market share gains from high-end brands and prefer Robam.

Figure 75: Kitchenware ASPs have been rising

steadily from 2012

Figure 76: High-end brand market share has

increased

Source: CMM, Credit Suisse estimates Source: CMM

Range hoods: European style and high air flow rates

We see rising interest in European-style hoods with large air flows. European-style hoods

are stylish with a modern appearance. The market share increased to 48% in 2016 from

42% in 2012. Moreover, European-style range hoods have a 16% price premium.

Due to different cooking habits, Chinese families have a greater demand for higher air flow

rates, or suction power, than Western families. Usually a 15-17m3/min air flow rate is

enough for a normal Chinese family. As consumers have higher living standards, we see

the market shares of range hoods with above 17m3/min suction power rising to 40% in

2016 from 15% in 2012. Given their stronger functionality, they are priced at a 25%

premium over the market average.

-

500

1,000

1,500

2,000

2,500

3,000

2012 2013 2014 2015 6M2016

Gas stove Range hood Sterilizer

Rmb

28%

48%

25%

43%

0%

10%

20%

30%

40%

50%

60%

2008 2015

Range hood total share Gas stove total share

26 October 2016

China Home Appliance Sector 33

Figure 77: European-style range hoods are the most popular

Source: Company website

Figure 78: Rising interest in European-style range

hoods

Figure 79: Large suction powered range hoods rise

rapidly

Source: CMM Source: CMM

Figure 80: High-end products have ~20% premium over the industry average

Suction power Price Price premium Style Price Price premium

Industry average 2,853 0% Industry average 2,853 0%

<13 m3/min 1,134 -60% Flat 1,261 -56%

13-14.9 m3/min 1,610 -44% Deep cover 954 -67%

15-16.9 m3/min 2,984 5% Inclined 2,804 -2%

>17 m3/min 3,529 24% European 3,322 16%

Source: CMM

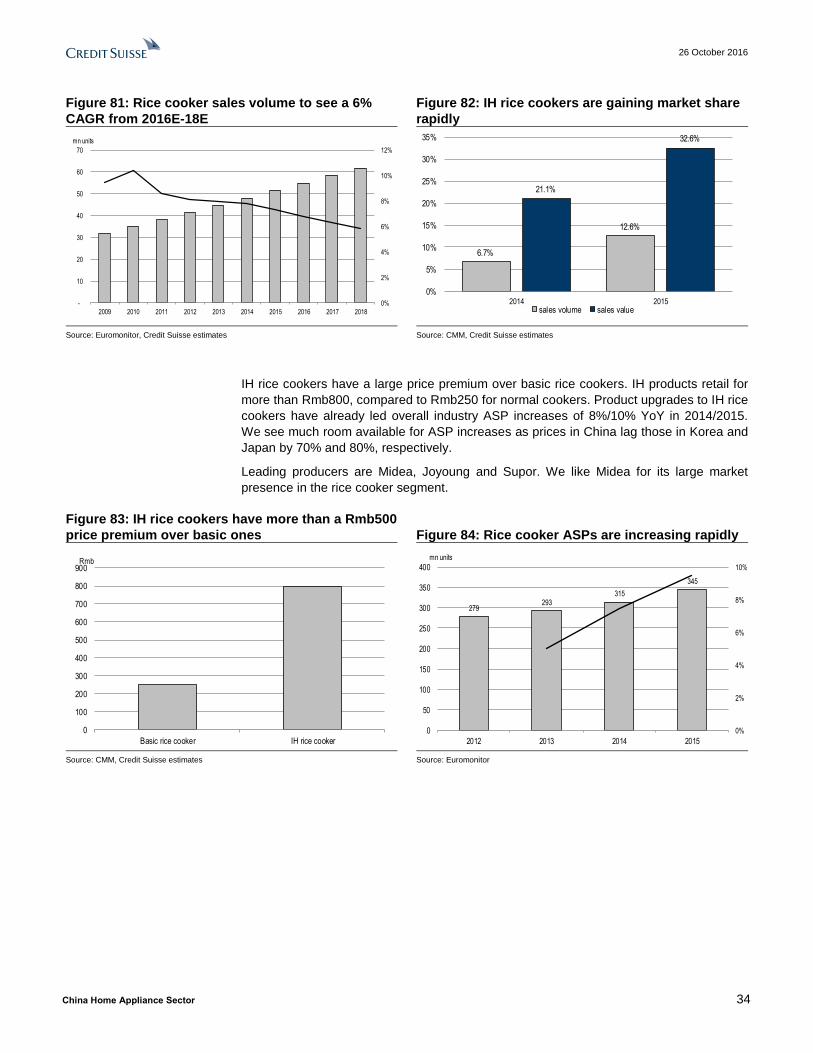

Rice cooker—upgrade to IH

Rice cooker is the largest category in the small appliance sector with a Rmb15 bn market

size and 32% of market sales. Consumers are upgrading to IH rice cookers, which have

witnessed 6.7% and 14.7% growth in volume and value, respectively, in 2015. We expect

market size will continue to see a 13-15% value CAGR from 2016E-18E. Value growth is

expected to be significantly faster than volume growth, as the price of an IH rice cooker is

more than double a normal rice cooker.

IH uses induction to heat rice and thus improve rice texture. The IH rice cooker market in

China only started in 2013 but has already taken a 13% market share.

European style Inclined style Deep covered style Flat style

42% 45% 46% 48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 6M2016

European style Inclined style Chinese style Flat style

15% 19%25%

34%40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 6M2016

>17 m3/min 15-16.9 m3/min 13-14.9 m3/min <13 m3/min

26 October 2016

China Home Appliance Sector 34

Figure 81: Rice cooker sales volume to see a 6%

CAGR from 2016E-18E

Figure 82: IH rice cookers are gaining market share

rapidly

Source: Euromonitor, Credit Suisse estimates Source: CMM, Credit Suisse estimates

IH rice cookers have a large price premium over basic rice cookers. IH products retail for

more than Rmb800, compared to Rmb250 for normal cookers. Product upgrades to IH rice

cookers have already led overall industry ASP increases of 8%/10% YoY in 2014/2015.

We see much room available for ASP increases as prices in China lag those in Korea and

Japan by 70% and 80%, respectively.

Leading producers are Midea, Joyoung and Supor. We like Midea for its large market

presence in the rice cooker segment.

Figure 83: IH rice cookers have more than a Rmb500

price premium over basic ones Figure 84: Rice cooker ASPs are increasing rapidly

Source: CMM, Credit Suisse estimates Source: Euromonitor

0%

2%

4%

6%

8%

10%

12%

-

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

mn units

6.7%

12.6%

21.1%

32.6%

0%

5%

10%

15%

20%

25%

30%

35%

2014 2015sales volume sales value

0

100

200

300

400

500

600

700

800

900

Basic rice cooker IH rice cooker

Rmb

279293

315

345

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

300

350

400

2012 2013 2014 2015

mn units

26 October 2016

China Home Appliance Sector 35

Figure 85: ASPs still have large room to grow

Figure 86: Midea has the largest rice cooker market

share

Source: Euromonitor Source: CMM

Market consolidation to continue

We have seen market consolidation in kitchenware in the past two years. The top-three

brands (in terms of volume) in both imbedded built-in kitchenware and small appliances

saw 3-6% market share gains from 2014-15.

We see faster consolidation in the imbedded built-in kitchenware segment due to relatively

low concentration. The market is scattered with more than 300 players. The top-three

brands only have a 40-45% market share, lagging the white good market's 55-65%.

In this consumption upgrade era, we expect leading brands with strong R&D capability and

premier product quality to stand out and continue to expand market share. Many

uncompetitive brands will be filtered out, in our r view.

Figure 87: We have seen market consolidation in

the past two years

Figure 88: We see further consolidation from the

built-in kitchenware segment

Source: CMM Source: CMM

34

57

119

170

0

20

40

60

80

100

120

140

160

180

China Hong Kong Korea Japan

USD/unit

Midea

41%

Joyoung

27%

Supor

14%

Others

18%

40%36%

48%

76%

65%

43%39%

46%

82%

71%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Range hood Gas stove Sterilizer Rice cooker Electric kettle

2014 2015

64%

53%50%

45% 44%40%

0%

10%

20%

30%

40%

50%

60%

70%

AC Washing machine Fridge Sterilizer Range hood Gas stove

26 October 2016

China Home Appliance Sector 36

Top picks: Midea, Robam and Gree Consumers are trading up in the home appliance sector, which has accelerated industry

consolidation. We believe that the segment leaders, which have reputable brand names,

solid channel execution and strong R&D capability, will stand out from peers. With this

sector report, we assume coverage on four white goods companies—Midea

(OUTPERFORM), Gree (OUTPERFORM), QD Haier (OUTPERFORM), Haier Electronic

(NEUTRAL) and initiate on two kitchenware companies—Robam (OUTPERFORM) and

Joyoung (Neutral).

Our top Buys are Midea, Robam and Gree. We like: (1) Gree for its attractive valuation

of 8.6x P/E (5x ex. cash P/E), 8% dividend yield and accelerating CAGR growth of 11.3%

for 2016-18 vs. a 7.4% CAGR for 2014-16; (2) Midea for its strongest earnings outlook

with a 14.8% CAGR (0.8x PEG) and well-diversified product categories; and (3) Robam for

its fastest growing outlook—a 28% EPS CAGR in 2016-18 backed by its market share

gains in the fast-growing kitchenware segment.

We rate Joyoung and Haier Electronic NEUTRAL, as we expect their earnings outlooks to

be largely in line with the industry and their valuations and dividend yields are not

attractive which cap their share price upside.

Figure 89: Revenue breakdown of our coverage companies

Company Ticker Revenue breakdown Export %

AC

Washer

Refrigerator

Water heater

Kitchenware and

small appliance

Midea 000333.SZ 43.8% 9.5% 8.6% 0.3% 26.1% 43.8%

Gree 000651.SZ 83.8% 0.0% 1.0% 0.0% 1.5% 24.0%

QD Haier 600690.SS 19.5% 16.5% 29.3% 5.0% 2.3% 29.0%

Haier Electronics 1169.HK 0.0% 18.0% 0.0% 7.0% 0.0% 4.0%

Robam 002508.SZ 0.0% 0.0% 0.0% 0.0% 98.0% 2.0%

Joyoung 002242.SZ 0.0% 0.0% 0.0% 0.0% 97.0% 2.0%

Source: Company data, Credit Suisse estimates

Figure 90: Valuation comp of our coverage companies

Company Name CS Ticker Rating Last Price TP Upside Mkt Cap Trd vol CAGR PE PE PEG PB ROE DY