chesapeake midstream partners - williams...

TRANSCRIPT

WELLS FARGO SYMPOSIUM CHESAPEAKE MIDSTREAM PARTNERS

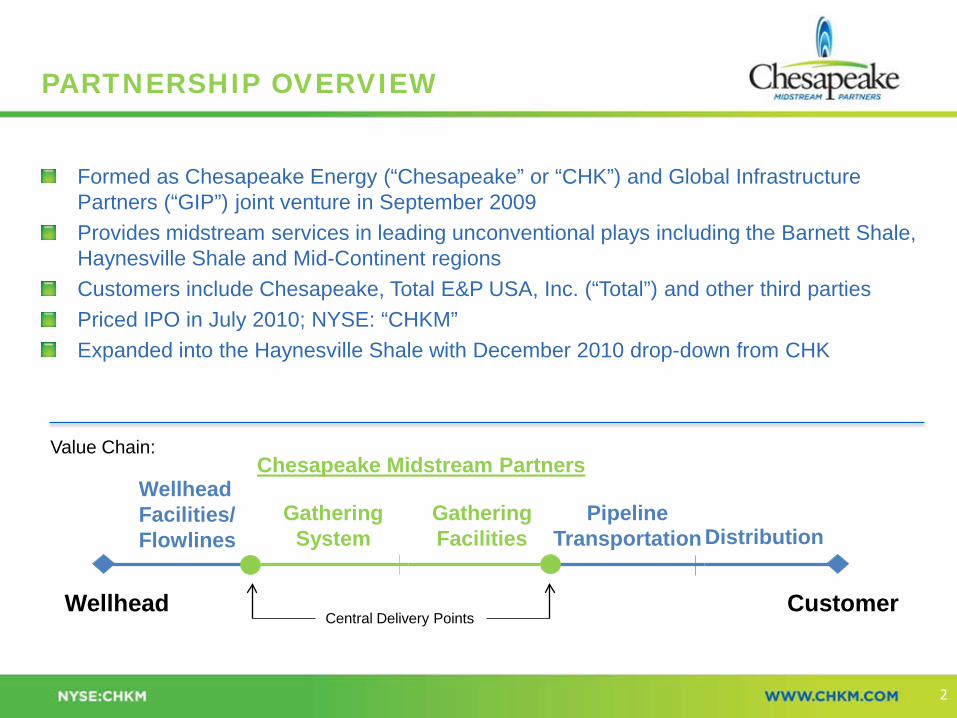

PARTNERSHIP OVERVIEW

2

Formed as Chesapeake Energy (“Chesapeake” or “CHK”) and Global Infrastructure Partners (“GIP”) joint venture in September 2009 Provides midstream services in leading unconventional plays including the Barnett Shale, Haynesville Shale and Mid-Continent regions Customers include Chesapeake, Total E&P USA, Inc. (“Total”) and other third parties Priced IPO in July 2010; NYSE: “CHKM” Expanded into the Haynesville Shale with December 2010 drop-down from CHK

Wellhead Customer

Wellhead Facilities/ Flowlines

Gathering System

Gathering Facilities

Pipeline Transportation

Chesapeake Midstream Partners Value Chain:

Central Delivery Points

Distribution

6.6% 6.2% 5.7%

Long Haul Pipeline MLPs

G&P MLPs

CHKM

Annual Distribution Growth Current Yield

Moderate Risk Business Model

Best in Class Business Model

Low Risk Business Model

DISTRIBUTION GROWTH PERFORMANCE AND TOTAL RETURN

3

Distribution Growth (growth vs. prior quarter) Yield & Total Return

CHKM combines a low risk business model with a unique growth platform

*Data current through 11/18/11 (1) Long haul pipeline includes: EPB, BWP, SEP and TCLP. G&P includes: RGNC, MWE, NGLS, WES, CPNO, DPM, APL, XTEX, CMLP, MMLP and EXLP.

(1) (1)

(1)

(1)

2.4% 2.5%

1.2%

2.5%

3.9% 3.3%

3.7% 3.6% 3.4%

1Q 2011 2Q 2011 3Q 2011

Long Haul Pipeline MLPs

G&P MLPs

CHKM

CHKM distribution growth among highest in sector

1) Data for the three-month period ended 09/30/2011

STRATEGIC MIDSTREAM ASSET BASE

High-quality, scalable asset base

High growth unconventional plays

4

Key operating data(1) Enterprise value: ~$4.1 billion

Dedicated acreage: ~3.0 million acres

Miles of pipe: ~3,511

Volume (mmcf / d):

Barnett: ~1,075 (48%)

Haynesville: ~578 (26%)

Mid-Continent: ~573 (26%)

Total: ~2,226

Wells gathered: ~4,799

Direct employees: ~299

Chesapeake Midstream Partners (CHKM) Assets

BUSINESS RISK CONSIDERATIONS AND MITIGANTS

5

Mitigants Considerations

MVC and long-term acreage dedications Rate redetermination Conservative maintenance capital

Volume & Capital

100% fixed-fee revenues Commitment to maintain contract structure / business model as business grows Concentrated in low cost basins Total and other 3rd parties today – ~17% revenue Improving CHK financial profile (25/25 Plan) Core basins to CHK for cash flow generation

Arms-length, 10-20 year contracts at market rates Critical infrastructure providing access to market Dedicated acreage

Commodity & Basin

Counterparty Concentration

Re-contracting

Barnett Shale proved to be an excellent basin to pioneer best practices for use throughout Midstream

Route development Environmental permitting Construction techniques

Barnett solutions in action – At the end of 3Q 2011, the Barnett represented

50% of total CHKM volume 60% of CHKM revenue 65% of invested capital

Overcoming the most difficult challenges translates into competitive advantage

Difficult Challenges Establish Best Practices

COMPETITIVE ADVANTAGE FROM BARNETT EXECUTION

6

CHKM Urban Operations Conservative design Rigorous construction inspection Risk assessment Integrity Management philosophy Public Awareness

Application of Latest Technology Forward Looking Infrared (FLIR) cameras Helicopter flyovers Smart Pig

Innovative & Conservative Operations BEST IN CLASS OPERATIONS

7

0

100

200

300

400

500

600

700

Jan-11 Sep-11

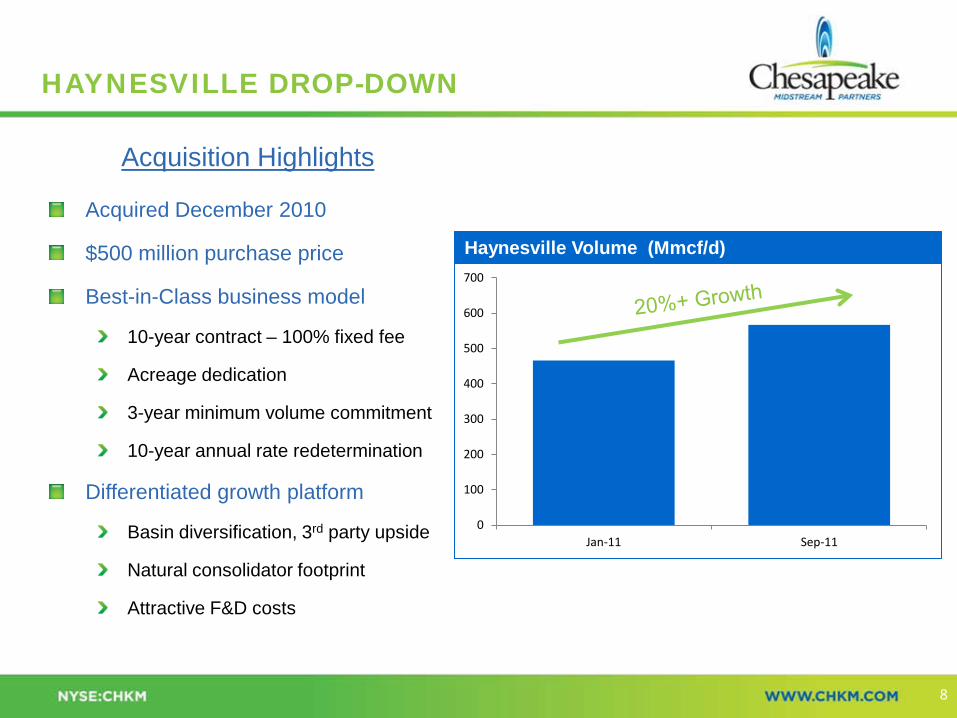

Acquired December 2010

$500 million purchase price

Best-in-Class business model

10-year contract – 100% fixed fee

Acreage dedication

3-year minimum volume commitment

10-year annual rate redetermination

Differentiated growth platform

Basin diversification, 3rd party upside

Natural consolidator footprint

Attractive F&D costs

HAYNESVILLE DROP-DOWN

8

Acquisition Highlights

Haynesville Volume (Mmcf/d)

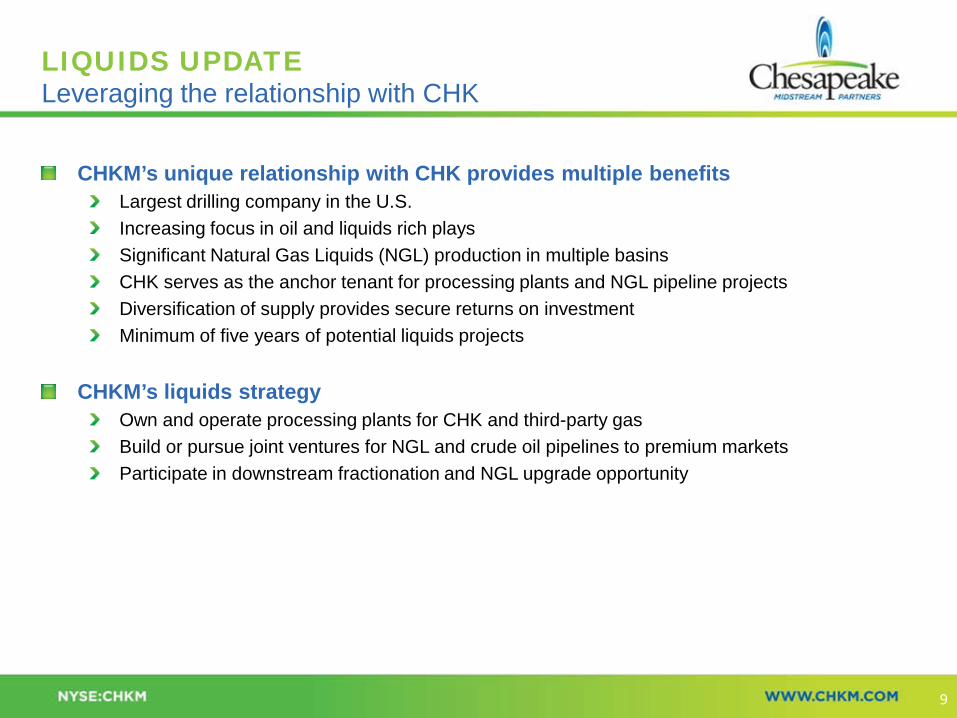

CHKM’s unique relationship with CHK provides multiple benefits

Largest drilling company in the U.S. Increasing focus in oil and liquids rich plays Significant Natural Gas Liquids (NGL) production in multiple basins CHK serves as the anchor tenant for processing plants and NGL pipeline projects Diversification of supply provides secure returns on investment Minimum of five years of potential liquids projects

CHKM’s liquids strategy Own and operate processing plants for CHK and third-party gas Build or pursue joint ventures for NGL and crude oil pipelines to premium markets Participate in downstream fractionation and NGL upgrade opportunity

LIQUIDS UPDATE Leveraging the relationship with CHK

9

CHKM LIQUIDS CHKM has position in 5 of the top plays

Wolfcamp

Eagle Ford Shale Bone Spring

TX PH Granite Wash

Tonkawa

Mississippi Lime

Cleveland

Colony Granite Wash

CHKM Chesapeake

10

SIGNIFICANT ORGANIC GROWTH PLATFORM

11

Revenue Annual fee escalation MVC, redetermination growth Contractual top line growth >4%

Operating Expenses

Significant portion fixed/capped Operating leverage/productivity

Capital Expenditures

Large acreage dedications and incremental well opportunities Fee redetermination supports return on capital Third-party opportunities – scale positions in leading basins

Organic Growth Platform Organic EBITDA Growth

Organic Growth Capex

Top Line Drivers Expense Productivity Organic Growth Capex

$303

$146

$366

0 50

100 150 200 250 300 350 400

2009 2010 2011E

($ in millions)

$340

2011E Growing Organic EBITDA

$1.5B invested to date: In addition, CHK investing ~$2.5B over the next two years

Potential access to: Over 20,000 wells on current footprint ~10.5 million gross acres of high quality unconventional assets ~7.1 Tcfe of proved reserves ~1,660 miles of pipe

MidCon Compression an additional drop-down opportunity

975,000 hp 2,850 units

SUBSTANTIAL GROWTH POTENTIAL FROM DROP-DOWNS

12

Note: Reflects current views of CHK management. Drop-down transactions are negotiated at arm’s length and are subject to CHKM board and conflicts committee approval. They may not occur as and when described, or at all.

Basin

Miles of

Pipe Throughput

(Mmcf/d)

Gross Acreage

(thousands)

Haynesville – Mansfield GGS 290 900 350

Marcellus North 370 520 1,800

Marcellus South 655 250 1,600

Eagle Ford 180 45 900

Granite Wash 115 75 350

Mississippi Lime 0 0 800

Niobrara 15 2 1,600

Cleveland/ Tonkawa 30 5 1,450

Utica Shale 5 0 1,700

Total 1,660 1,797 10,550

DELIVERING ON EXPECTATIONS & FINANCIAL STRATEGY

13

Stable cash flow generation High quality assets Best in class business model

Conservative financial structure Strong liquidity and balance sheet Conservative maintenance capital Ample distribution coverage

Delivering distribution growth 11% increase YoY in 3Q ‘11 Poised for continued strong growth

Key Financial Metrics ($ in millions) 1Q ‘11 2Q ‘11 3Q ‘11

EBITDA $72 $79 $88

Adj. DCF* $57 $58 $68

Distribution Coverage 1.16x 1.13x 1.28x

Distribution/Unit .3500 .3625 .3750

- QoQ Growth 3.7% 3.6% 3.4%

- YoY Growth N/A N/A 11.1%

Liquidity $501 $752 $733

Debt/Ebitda 1.10x 1.10x 1.18x

Financial performance highlights strength of CHKM model

*Distributable cash flow includes quarterly MVC adjustment

Organic growth capital

Significant opportunities

Mid-teens return

CHK drop-down portfolio

Leading basins

#1 acreage positions

Third-party acquisitions

Opportunistic

WELL POSITIONED TO DELIVER GROWTH

Funding Capacity

Well positioned to deliver best-in-class total return

Unique asset base growth potential

Best-in-class distribution growth

Investment-grade risk profile

Unmatched low risk, high-return investment

Growth Opportunities Industry-

Leading Opportunity

Debt/2011E EBITDA

(1) Long haul pipeline includes: EPB, BWP, SEP and TCLP. G&P includes: RGNC, MWE, NGLS, WES, CPNO, DPM, APL, XTEX, CMLP, MMLP and EXLP.

14

CHKM – $700 MM of liquidity

3.5x 3.5x

1.2x

Long Haul Pipeline MLPs (1)

G&P MLPs (1)

CHKM

Chesapeake Midstream Partners remains committed to: Protecting our country’s natural resources Encouraging our employees, contractors, suppliers and vendors to work in the safest and most environmentally-friendly manner possible Continually evaluating and improving our operating practices to minimize our environmental footprint Being a good neighbor in the areas in areas where we live and work

Commitment to Safety and Environmental Excellence SAFE AND RESPONSIBLE OPERATIONS

15