chemtura manufacturing uk ltd feasibility study on ......this study has examined the feasibility of...

TRANSCRIPT

Chemtura Manufacturing UK Ltd

Feasibility Study on substituting HBCD with polymeric flame retardant

Final report

July 2014

AMEC Environment & Infrastructure UK Limited

Copyright and Non-Disclosure Notice

The contents and layout of this report are subject to copyright owned by AMEC (©AMEC Environment & Infrastructure UK Limited 2014) save to the extent that copyright has been legally assigned by us to another party or is used by AMEC under licence. To the extent that we own the copyright in this report, it may not be copied or used without our prior written agreement for any

purpose other than the purpose indicated in this report.

The methodology (if any) contained in this report is provided to you in confidence and must not be disclosed or copied to third parties without the prior written agreement of AMEC. Disclosure of that information may constitute an actionable breach of confidence or may otherwise prejudice our commercial interests. Any third party who obtains access to this report by any means will, in any event, be subject to the Third Party Disclaimer set out

below.

Third Party Disclaimer

Any disclosure of this report to a third party is subject to this disclaimer. The report was prepared by AMEC at the instruction of, and for use by, our client named on the front of the report. It does not in any way constitute advice to any third party who is able to access it by any means. AMEC excludes to the fullest extent lawfully permitted all liability whatsoever for any loss or damage howsoever arising from reliance on the contents of this report. We do not however exclude our liability (if any) for personal injury or death resulting from our negligence, for fraud or any other matter in relation to which we cannot legally exclude

liability.

Document Revisions

No. Details Date

1 First draft report 13509i1 for client comment

29 November 2013

2 Final Report 14045i1 31 January 2014

3 Final Report 14045i2 19 February 2014

4 Final Report 140513 15 May 2014

5 Revised draft report for client comment taking into account authorisation application

25 June 2014

6. Updated report taking into account client comments

30 June 2014

7 Final Report 20140703 3 July 2014

Final Report

i

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Executive Summary

Scope

Hexabromocyclododecane (HBCD) (CAS No 3194-55-6) has been placed on the REACH

Authorisation list (Annex XIV)1, as a Substance of Very High Concern (SVHC) and the latest application date for authorisations under REACH was 21 February 2014. HBCD will be

included on the list of substances for global elimination under the UN Stockholm Convention on Persistent Organic Pollutants2 (POPs) on 26 November 2014.

This study has examined the feasibility of substituting HBCD with an alternative polymeric

substance, marketed by Chemtura under the trade name Emerald Innovation 3000. Both substances are used as flame retardants in expandable polystyrene (EPS) and extruded

polystyrene (XPS) insulation foam.

The report also contains an assessment of the information contained within the socio-economic assessment (SEA) and the analysis of alternatives (AofA) parts of the HBCD application for

authorisation published on 14 May 2014. For ease of reference the consortia of companies who comprise those applying for authorisation are referred to as “the applicants”.

Alternative Identification and Properties

Benzene, ethenyl polymer with 1,3 butadiene (brominated) (CAS 1195978-93-8) is the chemical name for Emerald Innovation 3000 (hereafter referred to as the polymeric flame retardant).

Building insulation currently accounts for over 99% of its use in Europe. The remaining

volumes are used in high impact polystyrene, which was not considered in this report. Based on information presented on 14 October 2013 at the UN POPRC meeting by Chemtura, the global

market size for HBCD in 2011 is assessed at some 31,000t per year. Of this, the EU market represents some 12,400t per year, a value that has been cross-checked using several different

sources. This compares to global figures estimated by the applicants of some 33,600t per year; with European demand of 14,483t per year. The difference reflects assumptions made by the

applicants on the extent of European demand – all other data used by the applicants are consistent with that presented by Chemtura on 14 October 2013. The value in the authorisation application – both for European and global demand – is seemingly inconsistent with the

published information available.

If HBCD was replaced with this alternative flame retardant, the overall structure of the supply

chain in Europe is not expected to change. At present there are three global companies who manufacture and/or import HBCD for the European market; the same three companies are

licensed to manufacture the polymeric alternative.

1 http://echa.europa.eu/addressing-chemicals-of-concern/authorisation/recommendation-for-inclusion-in-

the-authorisation-list/authorisation-list

2 http://chm.pops.int/TheConvention/ThePOPs/tabid/673/Default.aspx

Final Report

ii

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Technical Feasibility

HBCD is effective as a flame retardant at concentrations of c.0.7% in White EPS, c.1.1% in Grey EPS and c.1.75% in XPS3. The polymeric flame retardant has a lower bromine content

than HBCD (~ 64% vs ~ 74%) meaning that around 15% more is needed per unit of EPS and XPS. (Note that the analysis in this report considers the economic feasibility and availability

implications of an increase of 20%, based on levels being used by downstream users consulted). At these higher concentrations, technical performance characteristics are comparable.

Presentations made by industry at a side event to the UN POPRC meeting held on 14 October

2013 demonstrated that industry had found no fundamental issues with technical feasibility in the use of the polymeric flame retardant in XPS and EPS processes. The conclusion on the

product’s technical feasibility, from the majority of industry participants, was positive.

The technical feasibility of the polymeric flame retardant is not disputed by the applicants, based on the results of trials with samples of the polymeric flame retardant. The applicants state

that further testing and confirmation of technical feasibility is required by pellet and article producers, alongside marketing and certification. However, we note that, despite this statement,

the polymeric flame retardant is commercially available and is being sold; much of this work has already been undertaken by several companies.

The polymeric flame retardant is used in a similar way to HBCD. There is no need for major

capital infrastructure investment, training or additional health and safety measures amongst the users of the substance (though of course the manufacturers of the substance have had to invest

in new plant to produce it). The reformulation of the polymer recipe is the key technical change. The manufacturers of the polymeric flame retardant and major downstream users have

together demonstrated that this reformulation can be undertaken within a relatively short period of time (up to one year). Moreover, the applicants’ analysis of alternatives states that the

‘optimum’ and ‘most likely’ timings for product confirmation from commercial availability may be rather than less than this, between 6 months and 10 months, respectively4.

The applicants provide details of estimated timescales to substitute HBCD with the polymeric

flame retardant. Commentary on these assumptions is provided within the main body of the report. The overall conclusions appear inconsistent with the evidence seen in the preparation of

this study and it is unclear how the total time required for substitution (between 4 years and up to 11 years) was calculated. Whilst it is recognised that the process of optimisation is ongoing,

some companies will have fully substituted during 2014 and are selling product based on the polymeric flame retardant, and we understand that some of the applicants have also replaced

HBCD in some of their grades.

Economic Feasibility

The economic feasibility of the polymeric alternative is not disputed by the applicants. Emerald Innovation 3000 currently costs more than HBCD on a weight by weight basis and greater

quantities will be required in order to meet fire safety standards. Taking these factors into account the applicants “assume [the polymeric flame retardant] is economically feasible as EPS

producers have the intention to switch from HBCD to the Polymeric flame retardant”5.

3 Based on discussions with Chemtura.

4 HBCD AofA Figure 5.3 Page 101 and 102.

5 HBCD SEA Page 17

Final Report

iii

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

An assessment of economic feasibility of the polymeric flame retardant in comparison with

HBCD was undertaken within this study. The detailed step-by-step calculations are not shown, given that economic feasibility of the polymeric alternative is not disputed and that much of the

analysis is based on commercially confidential data (e.g. market prices).

Overall, the assessment indicates that Emerald Innovation 3000 is an economically feasible alternative to HBCD. The analysis suggests an increase in the final product price (whether per

tonne or per board of EPS) of around 1%. Such a change should be considered in light of the low proportion of the flame retardant is used in the polystyrene foam formulation and that price

of the major raw material in both EPS and XPS (the styrene monomer) has varied to a much greater extent than the price changes identified in switching from HBCD to the polymeric flame

retardant. The ability of companies to pass any costs on to the consumer (and hence not incur potentially significant costs themselves) is in part dependent on the extent of wider market

switching from HBCD.

Hazards and Risks of the Alternative

The US EPA has reviewed alternatives to HBCD, including the polymeric flame retardant. The main conclusion of that review was that the polymeric flame retardant is a substance that is safer

than HBCD for both human health and the environment. This conclusion took into account a PBT assessment of both products. Unlike HBCD, the polymeric flame retardant is not expected

to be classed as a PBT substance under REACH or as a Persistent Organic Pollutant (POP) under the UN Stockholm Convention.

As the polymeric flame retardant is likely to be used in a similar way to HBCD, occupational

exposure and releases to the environment are likely to be similar, although the flame retardant is not easily emitted from the body of the foam once it is formed. The risks associated with the

polymeric flame retardant are expected to be lower.

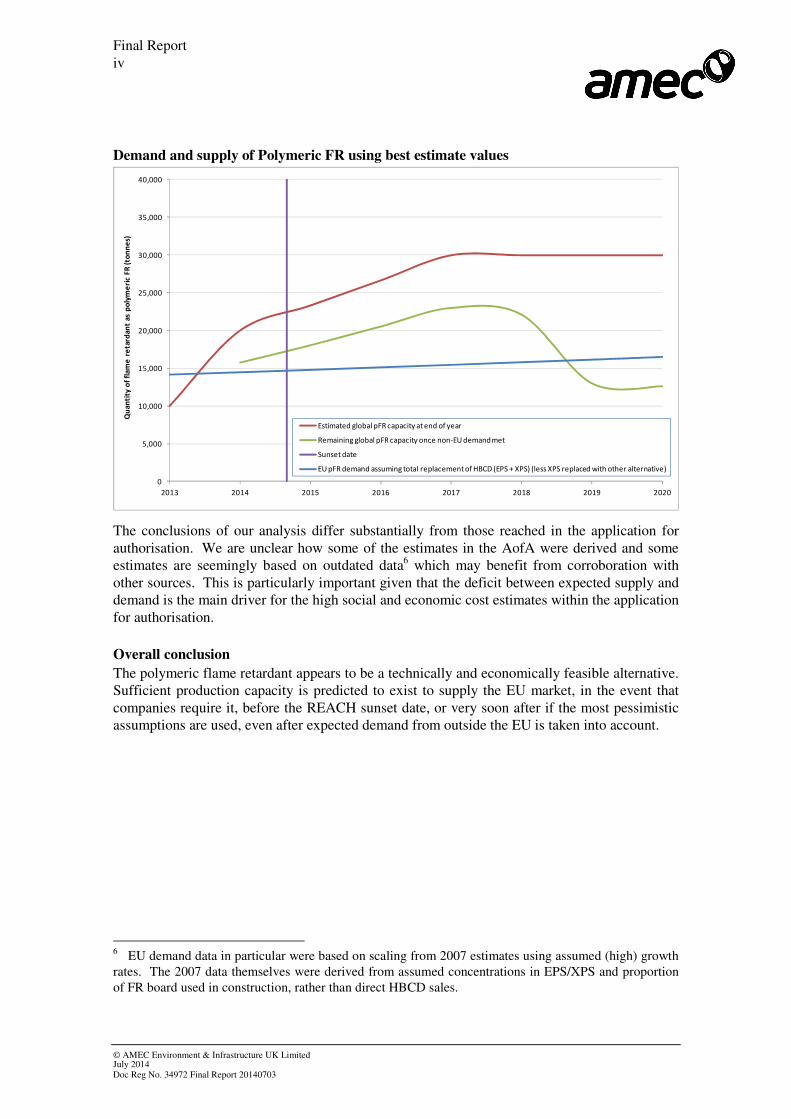

Availability

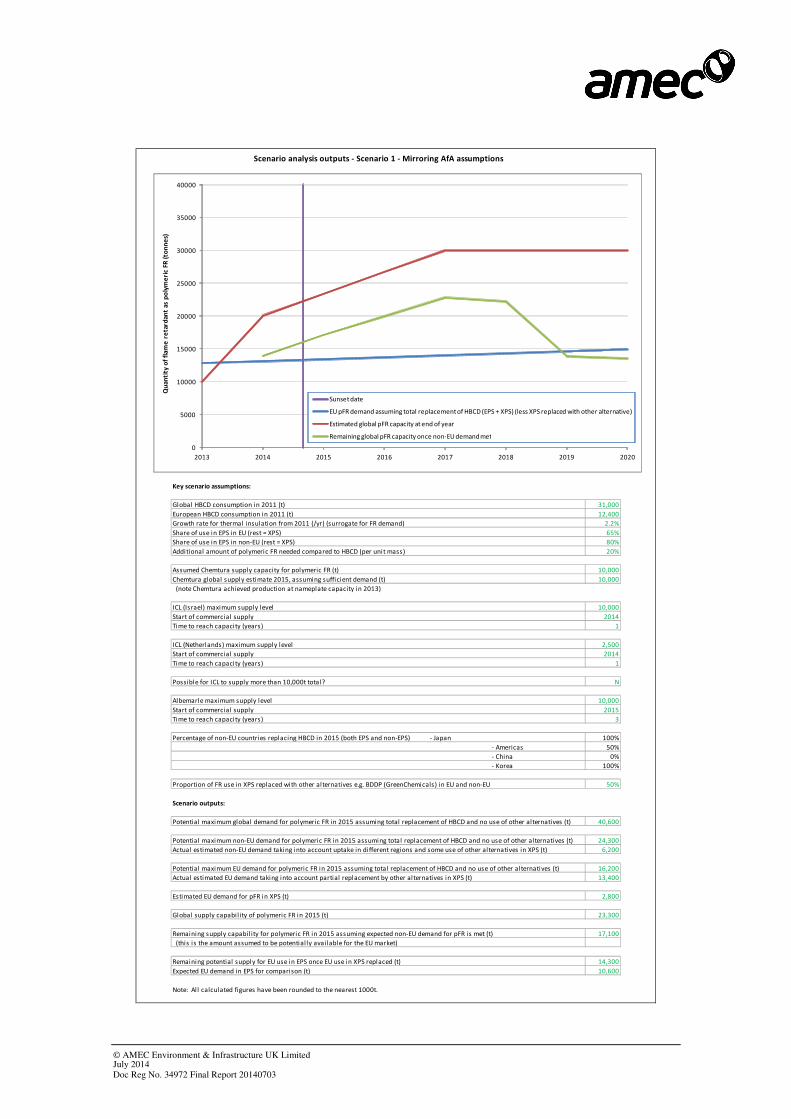

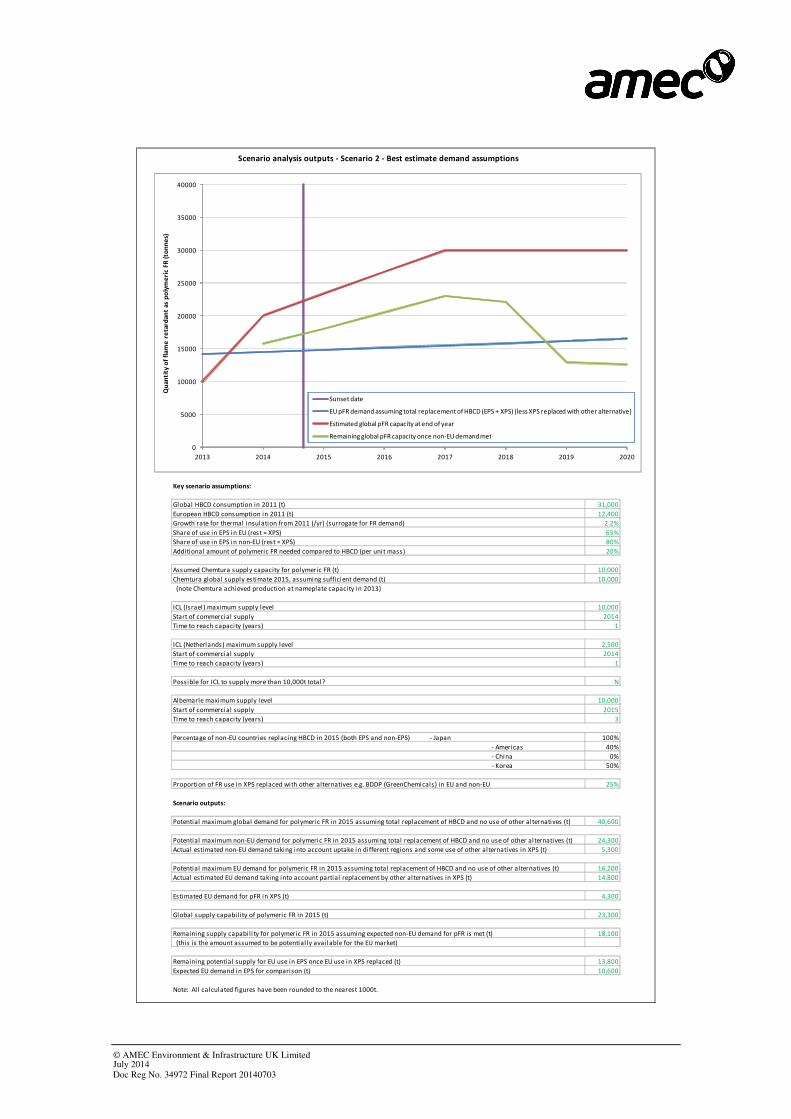

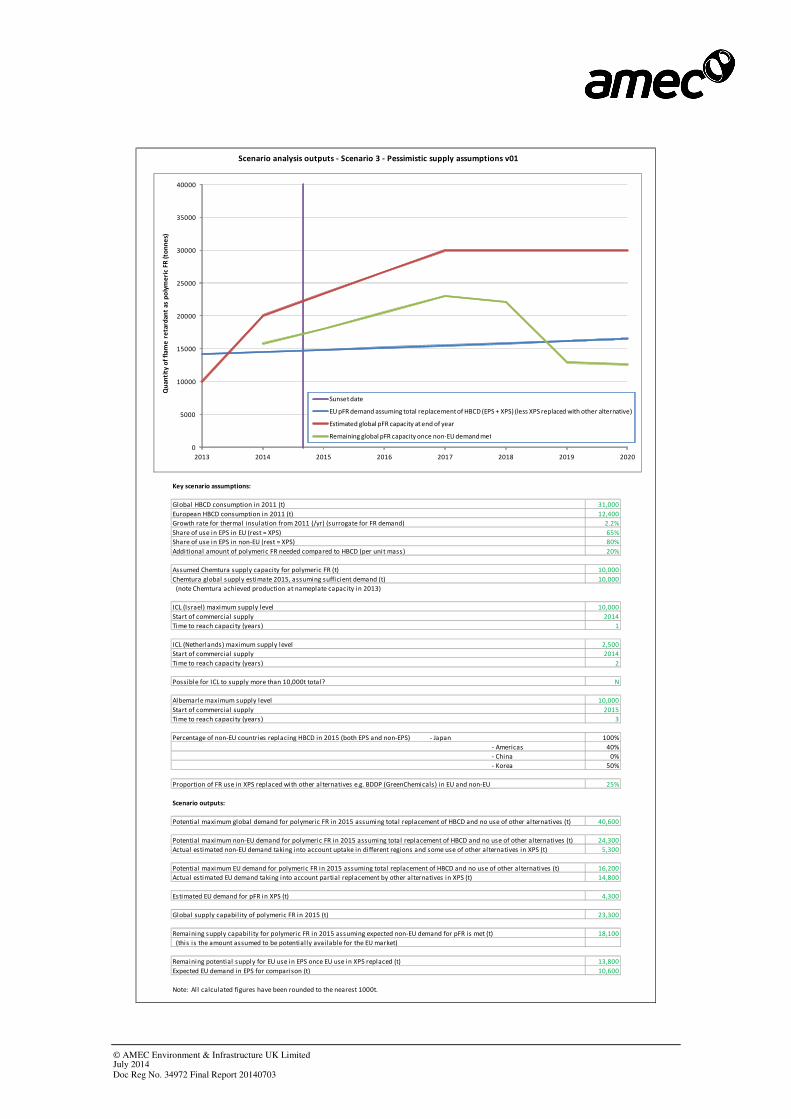

A key issue in substitution is whether the polymeric flame retardant is likely to be available, in

sufficient quantities to meet demand, by the sunset date for HBCD. To examine this, a number of demand/capacity scenarios were considered, to test the implications of changing key

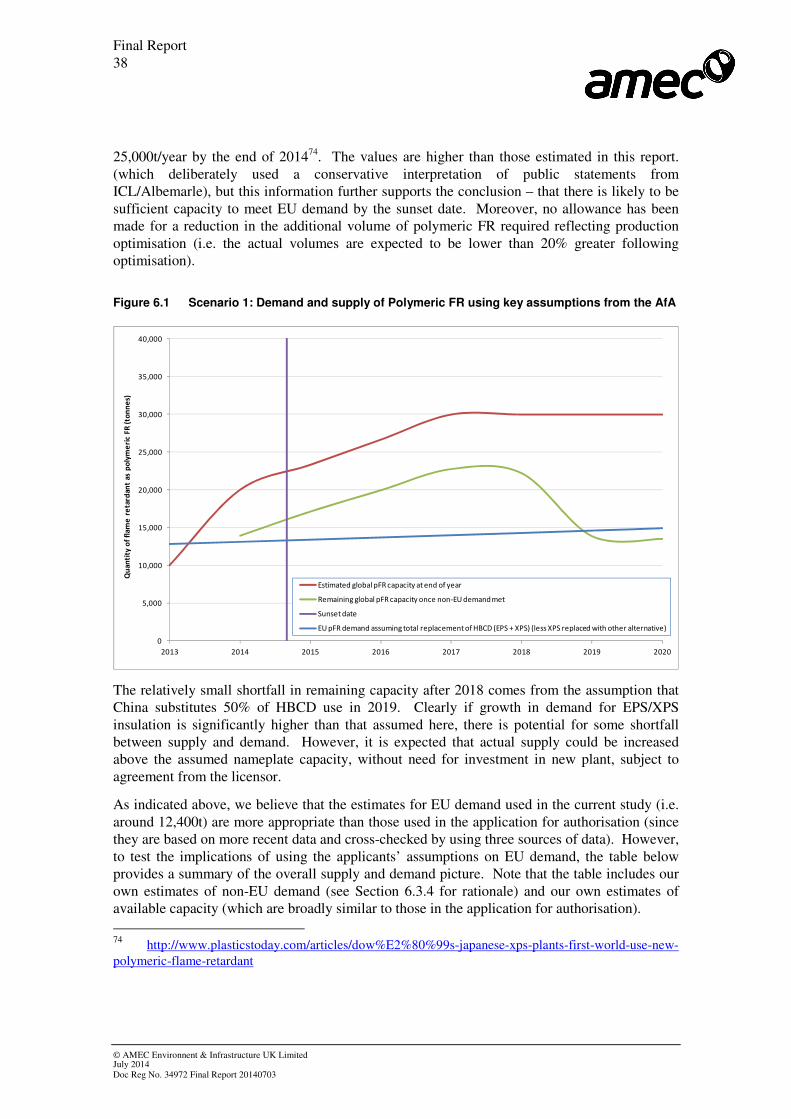

assumptions. The two main scenarios, a ‘best estimate’ and a scenario intended to mirror key assumptions from the application for authorisation are considered in detail within the report. Both suggest there is likely to be sufficient capacity from the sunset date to supply the European

EPS and XPS market with polymeric flame retardant as a replacement for HBCD in the event that authorisation is not granted.

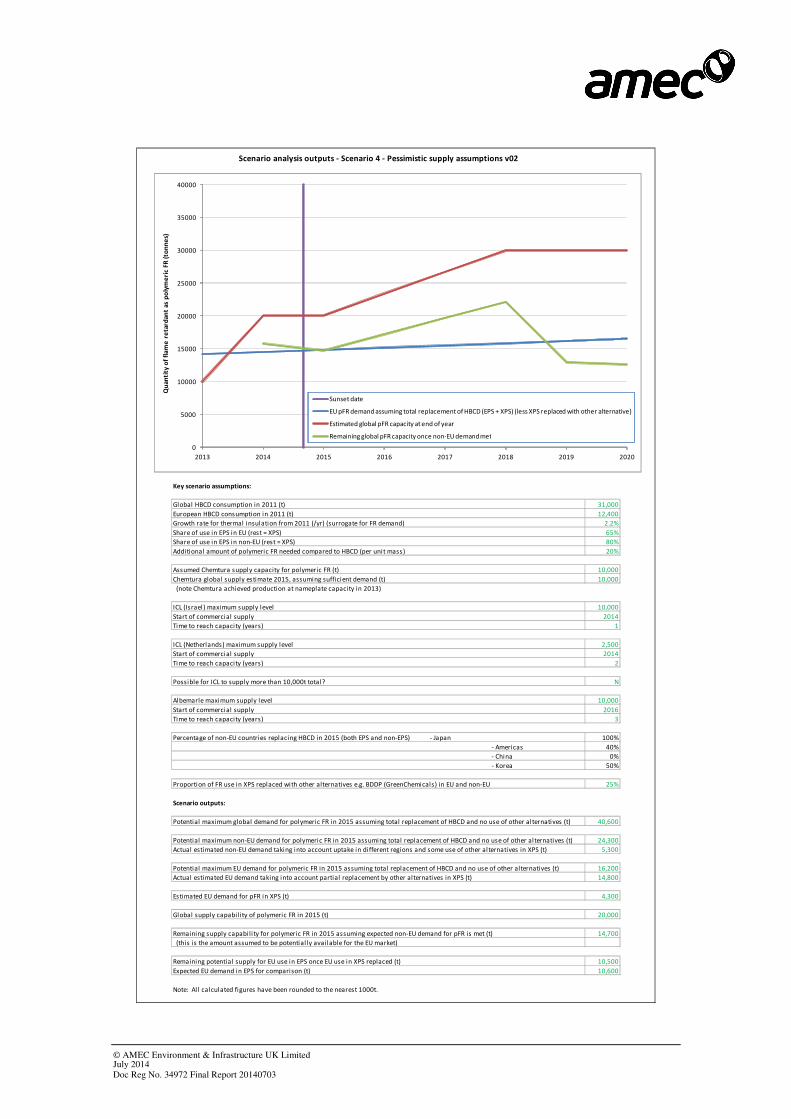

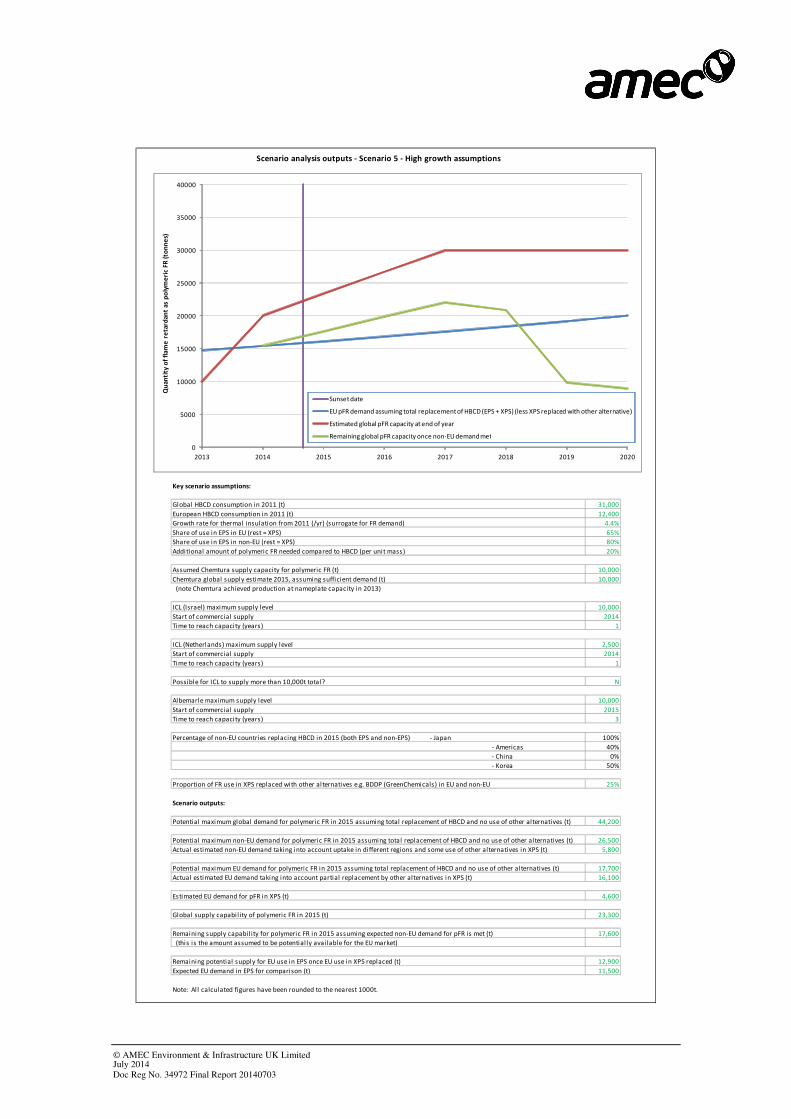

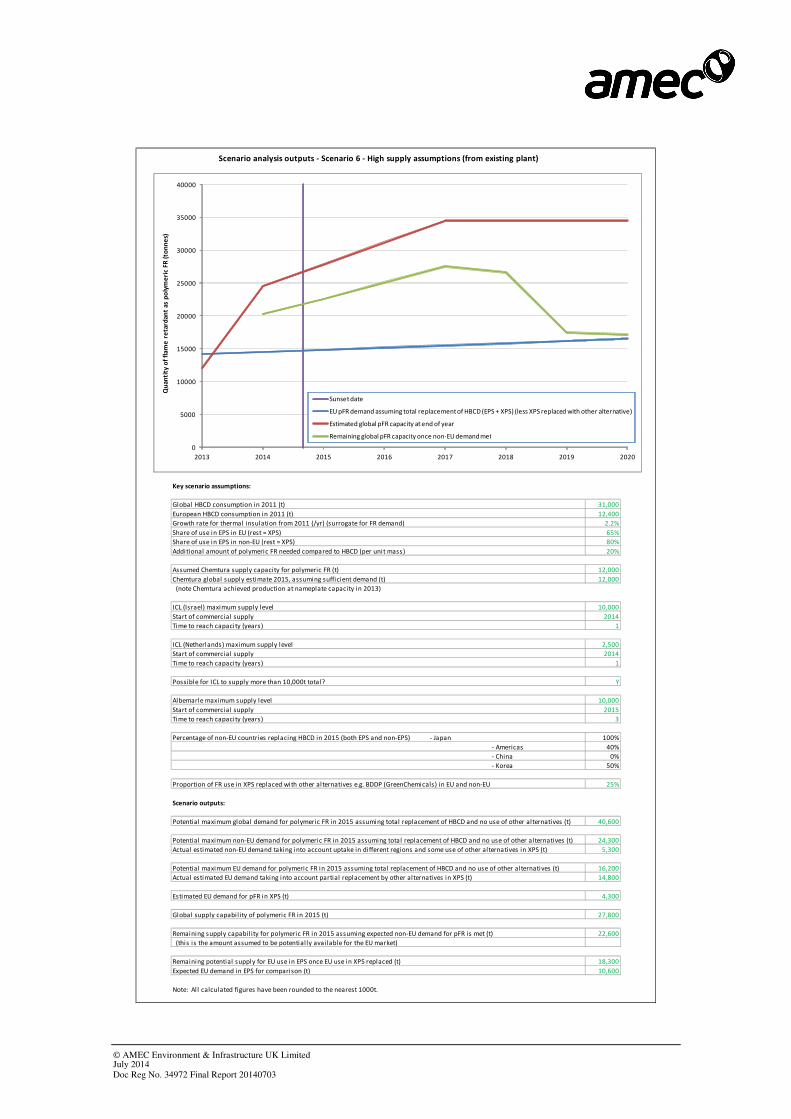

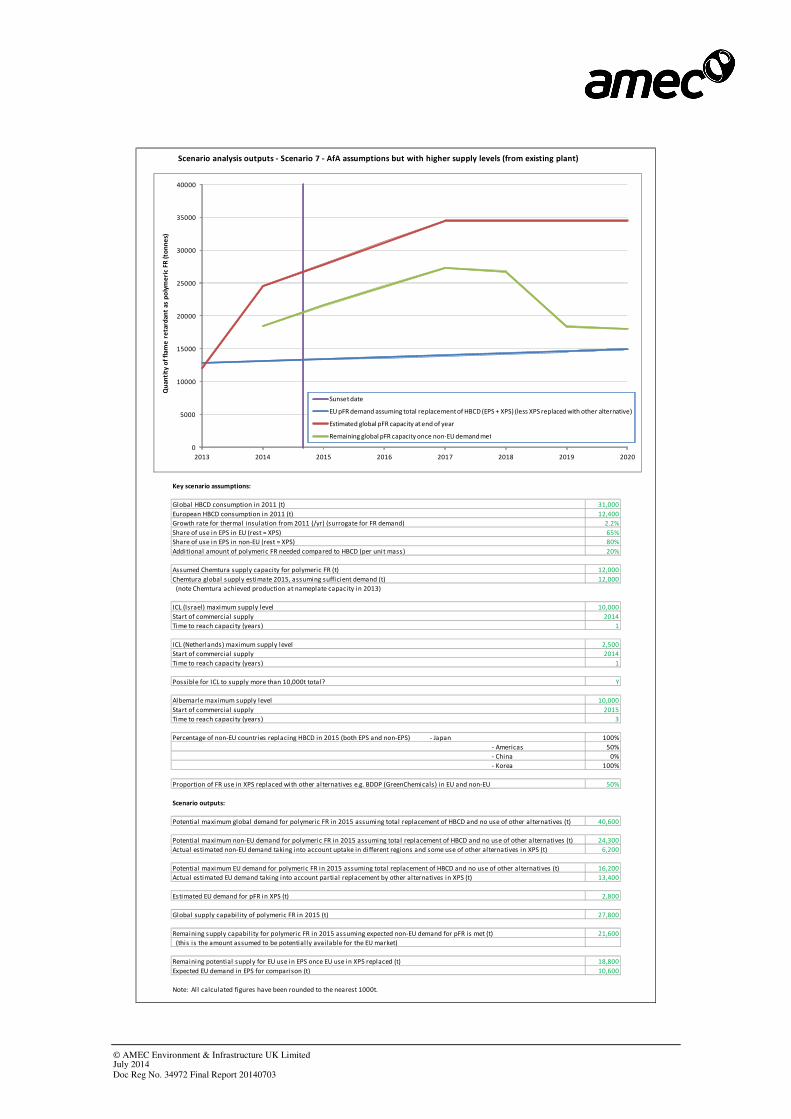

Additional scenarios are considered. Even under those using pessimistic (and probably unrealistic) assumptions regarding demand outside the EU (and factoring in growth in demand,

which was not assumed in the authorisation application), there is expected to be sufficient capacity available for the whole EU market to completely replace current HBCD volumes

within a year or so of the sunset date. The supply assumptions made in AMEC’s analysis are considered to be conservative, with estimated capacity online at the end of 2014 somewhat lower than the 25,000 tonnes estimated recently by the licensor of the polymeric flame

retardant..

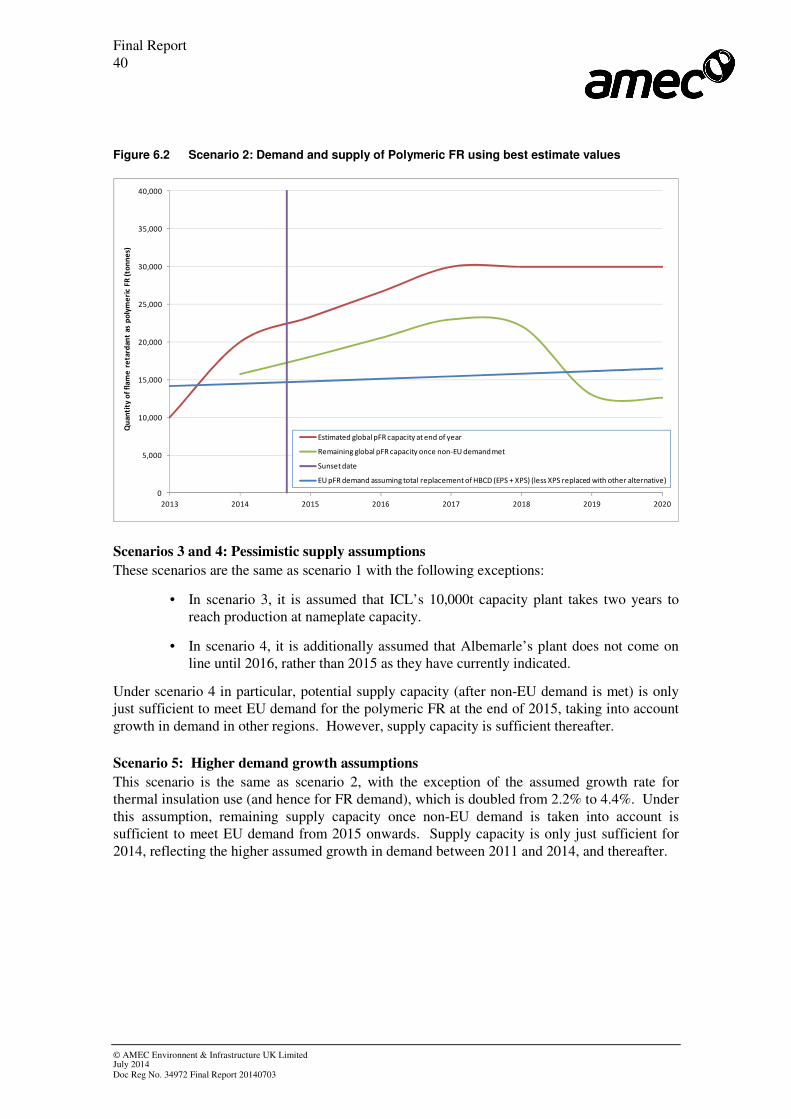

The outputs of the analysis for the best estimate scenario are shown in the figure below.

Final Report

iv

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Demand and supply of Polymeric FR using best estimate values

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2013 2014 2015 2016 2017 2018 2019 2020

Qu

an

tity

of

fla

me

re

tard

an

t as

po

lym

eri

c F

R (

ton

ne

s)

Estimated global pFR capacity at end of year

Remaining global pFR capacity once non-EU demand met

Sunset date

EU pFR demand assuming total replacement of HBCD (EPS + XPS) (less XPS replaced with other alternative)

The conclusions of our analysis differ substantially from those reached in the application for

authorisation. We are unclear how some of the estimates in the AofA were derived and some estimates are seemingly based on outdated data6 which may benefit from corroboration with

other sources. This is particularly important given that the deficit between expected supply and demand is the main driver for the high social and economic cost estimates within the application

for authorisation.

Overall conclusion

The polymeric flame retardant appears to be a technically and economically feasible alternative. Sufficient production capacity is predicted to exist to supply the EU market, in the event that

companies require it, before the REACH sunset date, or very soon after if the most pessimistic assumptions are used, even after expected demand from outside the EU is taken into account.

6 EU demand data in particular were based on scaling from 2007 estimates using assumed (high) growth

rates. The 2007 data themselves were derived from assumed concentrations in EPS/XPS and proportion

of FR board used in construction, rather than direct HBCD sales.

Final Report

v

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Contents

1. Introduction 1

1.1 Purpose of this Report 1

1.2 Status of this report 1

1.3 Methodology 2

1.4 Contents 2

2. Alternative Identification and Properties 3

2.1 Identification of the Substance 3

2.2 Manufacture and Uses 4

2.2.1 Overview of uses 4

2.2.2 Market Size 4

2.3 Classification and Labelling 7

2.4 HBCD Application for Authorisation: Commentary on the SEA and AofA 8

2.4.1 Scope of Application 8

2.4.2 Market Size 8

2.4.3 Industry Structure 9

3. Technical Feasibility 10

3.1 Introduction 10

3.2 Substance Function and Requirements for the Alternative 10

3.2.1 Requirements of the alternative 10

3.2.2 Standard production process for EPS 10

3.3 Technical Stages in Substitution 11

3.4 Implications of Substitution 12

3.5 Wider Industry Experience with Substitution 12

3.6 HBCD Application for Authorisation: Commentary on the SEA and AofA 16

4. Economic Feasibility 19

4.1 Introduction 19

Final Report

vi

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

4.2 HBCD Application for Authorisation: Commentary on the SEA and AofA 20

5. Hazards and Risks of the Alternative 22

5.1 Introduction 22

5.1.1 Overview 22

5.1.2 PBT assessments 22

5.2 Assessment of the Polymeric Flame Retardant and HBCD 24

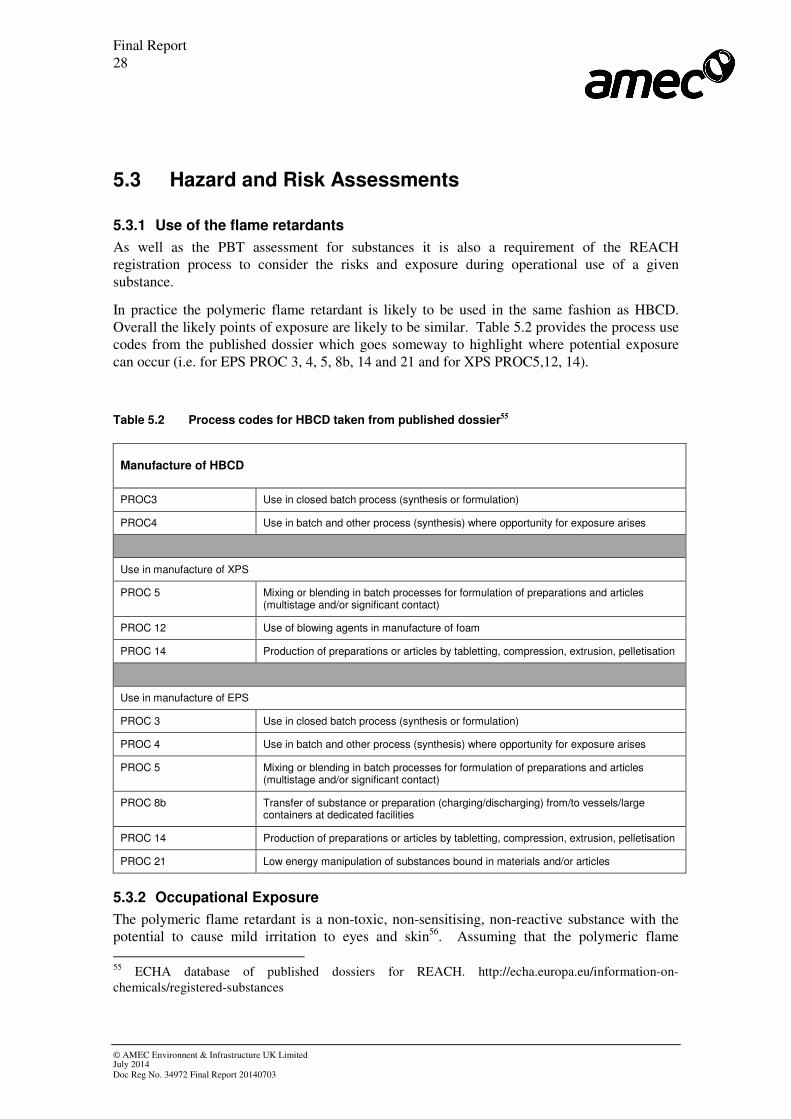

5.3 Hazard and Risk Assessments 28

5.3.1 Use of the flame retardants 28

5.3.2 Occupational Exposure 28

5.3.3 Environmental Release 29

5.4 HBCD Application for Authorisation: Commentary on the SEA and AofA 30

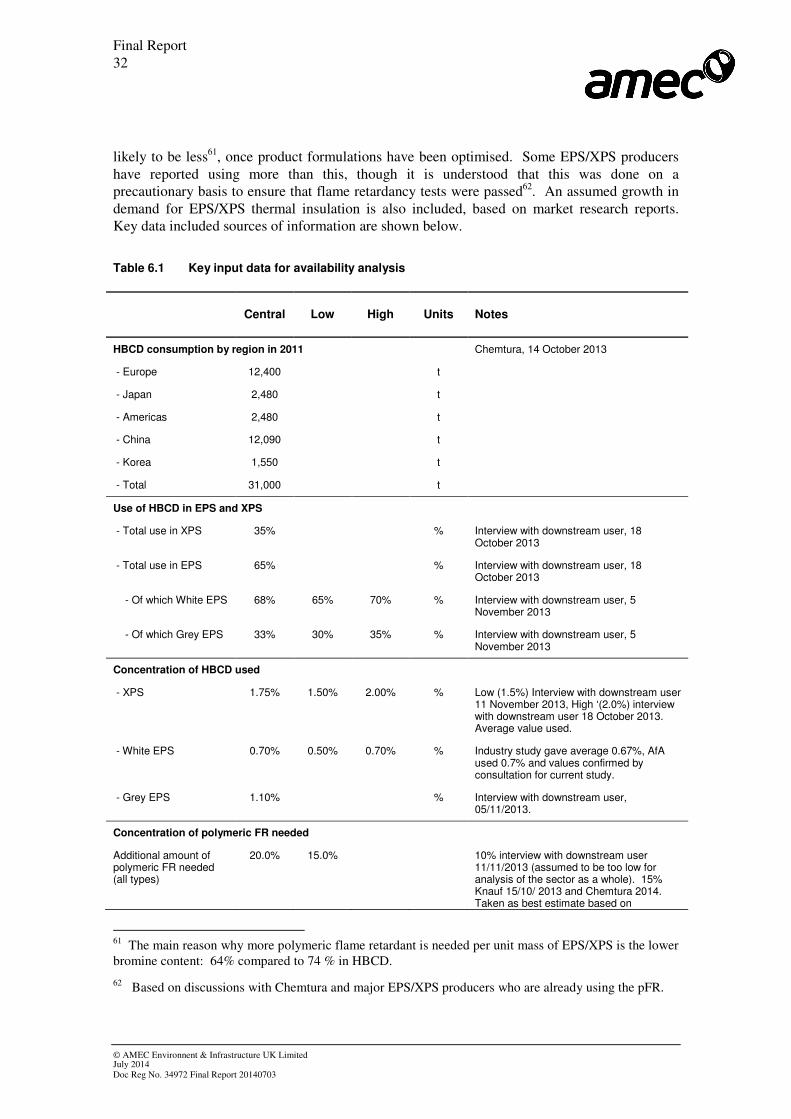

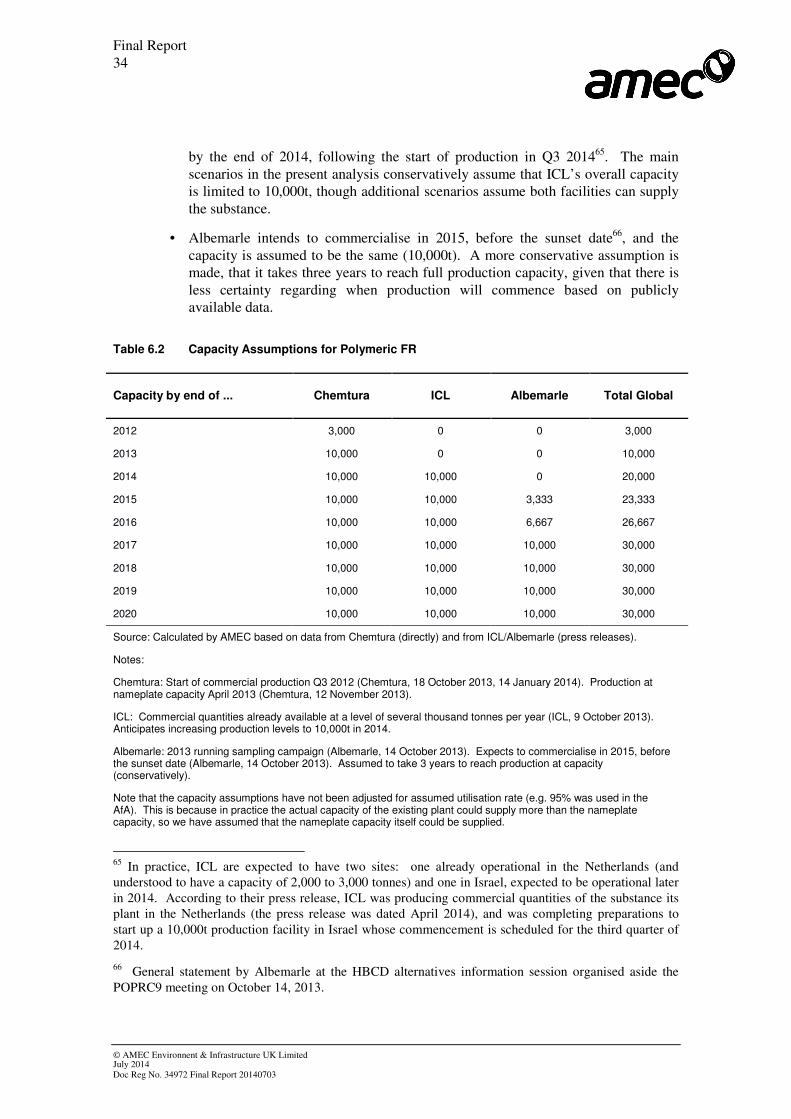

6. Availability 31

6.1 Introduction 31

6.2 Demand and Production Capacity Analysis 31

6.2.1 Overall demand and production capacity 31

6.2.2 Presentation of the scenarios 36

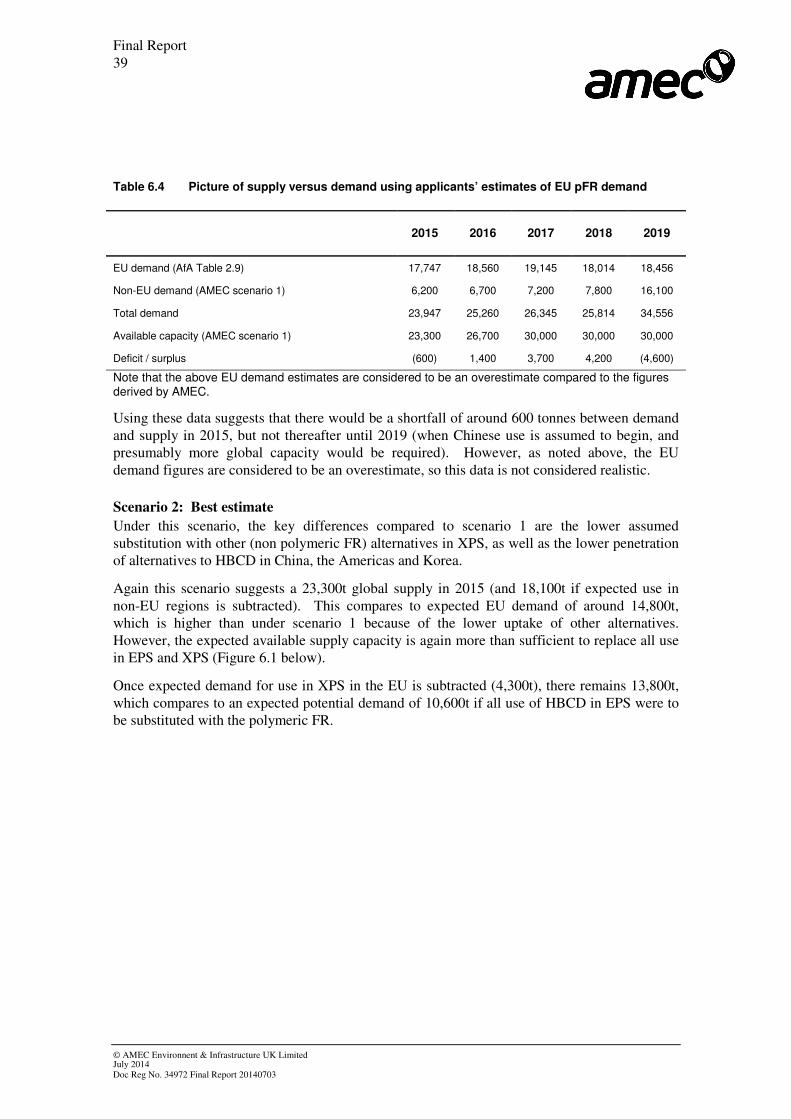

6.2.3 Scenarios 37

6.3 Key differences from the authorisation application 42

6.3.1 Overview 42

6.3.2 HBCD demand requiring replacement 42

6.3.3 Global supply of the polymeric flame retardant 43

6.3.4 Estimates of demand for polymeric FR from non-EU regions 43

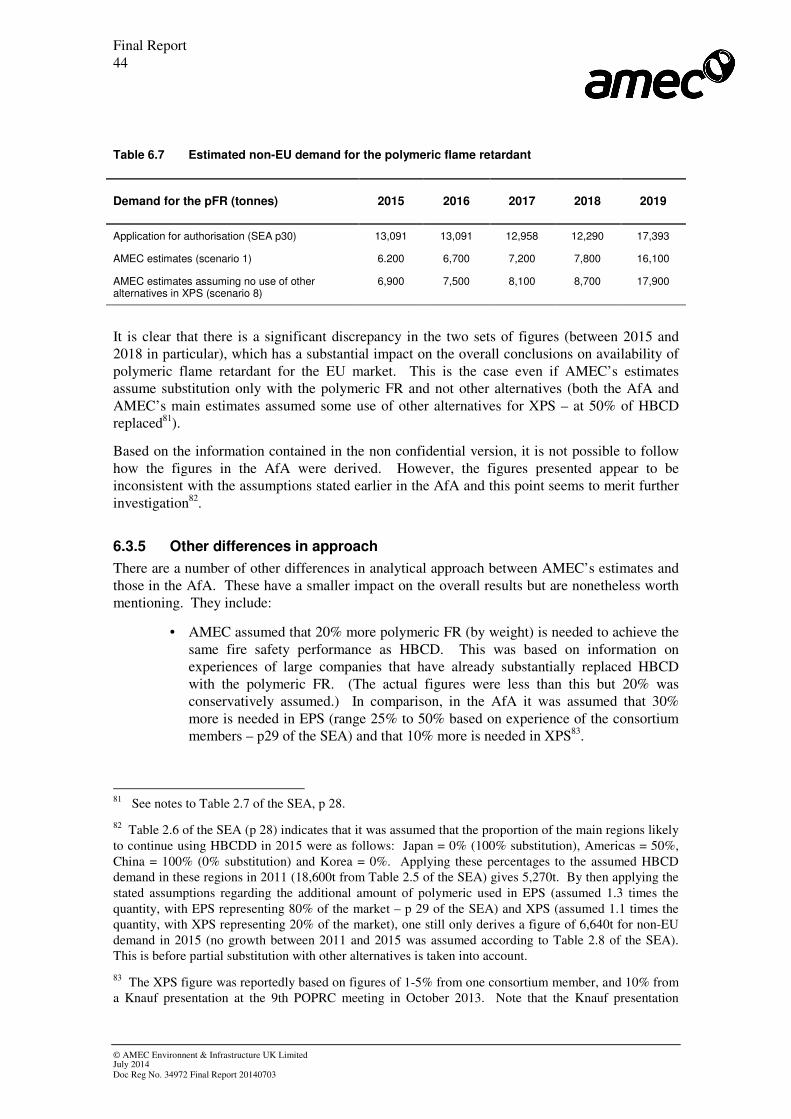

6.3.5 Other differences in approach 44

6.4 Overall conclusions on availability 45

7. Conclusion on Suitability and Availability of the Alternative 47

List of tables

Table 2.1 Physical data for Emerald Innovation 3000 Product 3 Table 2.2 Estimated Global HBCD Market (2011) 4 Table 2.3 Estimated European HBCD Market (Based on VECAP Survey data) 9 Table 3.1 Industry Experience with the polymeric flame retardant (POPRC Meeting, October 2013) 13 Table 3.2 Applicant’s assumption on timing for commercialisation of a FR Alternative 18 Table 5.1 Assessment of polymeric flame retardant and HBCD 26 Table 5.2 Process codes for HBCD taken from published dossier 28 Table 6.1 Key input data for availability analysis 32

Final Report

vii

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Table 6.2 Capacity Assumptions for Polymeric FR 34 Table 6.3 Key input parameters for scenarios 1 and 2 37 Table 6.4 Picture of supply versus demand using applicants’ estimates of EU pFR demand 39 Table 6.5 Comparison of estimated global HBCD demand in 2011 (tonnes) 42 Table 6.6 Comparison of estimates of global supply of polymeric flame retardant 43 Table 6.7 Estimated non-EU demand for the polymeric flame retardant 44

List of figures

Figure 2.1 Building Permits in the EU 28. 2007 to 2013 (Number of dwellings). Index: 2011=100 5 Figure 2.2 EU Supply chain: HBCD in EPS and XPS 7 Figure 4.1 Unit Price of Styrene relative to all other raw materials (Emerald Innovation 3000) and

HBCD (US Dollars per Kilogram) August 2008 to December 2012 – Note the data refers to EPS 20

Figure 6.1 Scenario 1: Demand and supply of Polymeric FR using key assumptions from the AfA 38 Figure 6.2 Scenario 2: Demand and supply of Polymeric FR using best estimate values 40

Appendices

Appendix A: IVH Press Release on HBCD Substitution Appendix B: Demand and Production Capacity Scenarios – Assumptions and Outputs

Final Report

viii

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Final Report 1

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

1. Introduction

1.1 Purpose of this Report

This report has been prepared by AMEC for Chemtura Manufacturing UK Ltd (Chemtura). Chemtura manufacture and supply hexabromocyclododecane (HBCD) (CAS No 25637-99-4

and 3194-55-6). The company is also one of three global licensees for a polymeric flame retardant (CAS No 1195978-93-8) which is sold under the trade name Emerald Innovation™

3000 (hereafter referred to as ‘Emerald Innovation 3000’ or ‘polymeric flame retardant’ given that other licensees will use different trade names).

The report examines the feasibility of substituting HBCD with the polymeric flame retardant.

Both substances are used as flame retardants in XPS and EPS foams. The study has been prepared taking into account relevant guidance on SEA under REACH and an assessment of the

economic feasibility of alternatives7.

HBCD has been placed on the REACH Authorisation list (Annex XIV)8, and the latest application date for authorisations under REACH was 21 February 2014. HBCD is also on the

list of prohibited substances under the Stockholm Convention on Persistent Organic Pollutants9.

The assessment follows the European Chemicals Agency (ECHA’s) suggested format for submission of information on alternatives as part of the public consultation on authorisation

applications10.

1.2 Status of this report

This report was originally prepared to examine the feasibility of substituting HBCD with the

polymeric flame retardant, with “Availability” as the key criterion. The report has subsequently been updated throughout based on an assessment of the information contained within the socio-

economic assessment (SEA) and the analysis of alternatives (AofA) parts of the application for authorisation. For ease of reference the consortia of companies who comprise those applying

7Guidance on the preparation of socio-economic analysis as part of the application for Authorisation:

http://echa.europa.eu/documents/10162/13643/sea_authorisation_en.pdf

See also: ECHA’s supplementary guidance on ‘How the Committee for Socio-Economic Analysis will

evaluate economic feasibility in applications for authorisation’:

http://echa.europa.eu/documents/10162/13580/seac_authorisations_economic_feasibility_evaluation_en.p

df

8 http://echa.europa.eu/addressing-chemicals-of-concern/authorisation/recommendation-for-inclusion-in-

the-authorisation-list/authorisation-list

9 http://chm.pops.int/TheConvention/ThePOPs/tabid/673/Default.aspx

10 http://echa.europa.eu/documents/10162/13555/instructions_third_parties_afa_en.pdf

Final Report 2

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

for authorisation are referred to as “the applicants”. This assessment is contained at the end of

each chapter.

1.3 Methodology

The study is based on a review of publicly available information on the implications of

substituting HBCD, produced in the context of REACH, the POPs Convention and work by the US EPA. This has been supplemented by interviews with Chemtura technical and commercial

staff and interviews with companies involved in the production of EPS beads (and XPS foam boards).

1.4 Contents

Following this introduction:

• Section two identifies the alternative and its properties, based on the ‘guidance for

identification of substances under REACH and CLP’.11

• The technical feasibility of the polymeric flame retardant to fulfil the same function

as HBCD as a flame retardant in EPS applications is assessed in section three.

• The economic feasibility of the polymeric flame retardant is examined in section

four.

• Section five evaluates the hazards and risks of HBCD compared to the polymeric

flame retardant.

• Section six examines the availability of the polymeric flame retardant, based on

scenarios of expected production capacity and demand in the EU and elsewhere. Detailed outputs and assumptions from the scenarios assessed are in Appendix B.

• Study conclusions are provided in section seven.

11 http://www.echa.europa.eu/documents/10162/13643/substance_id_en.pdf

Final Report 3

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

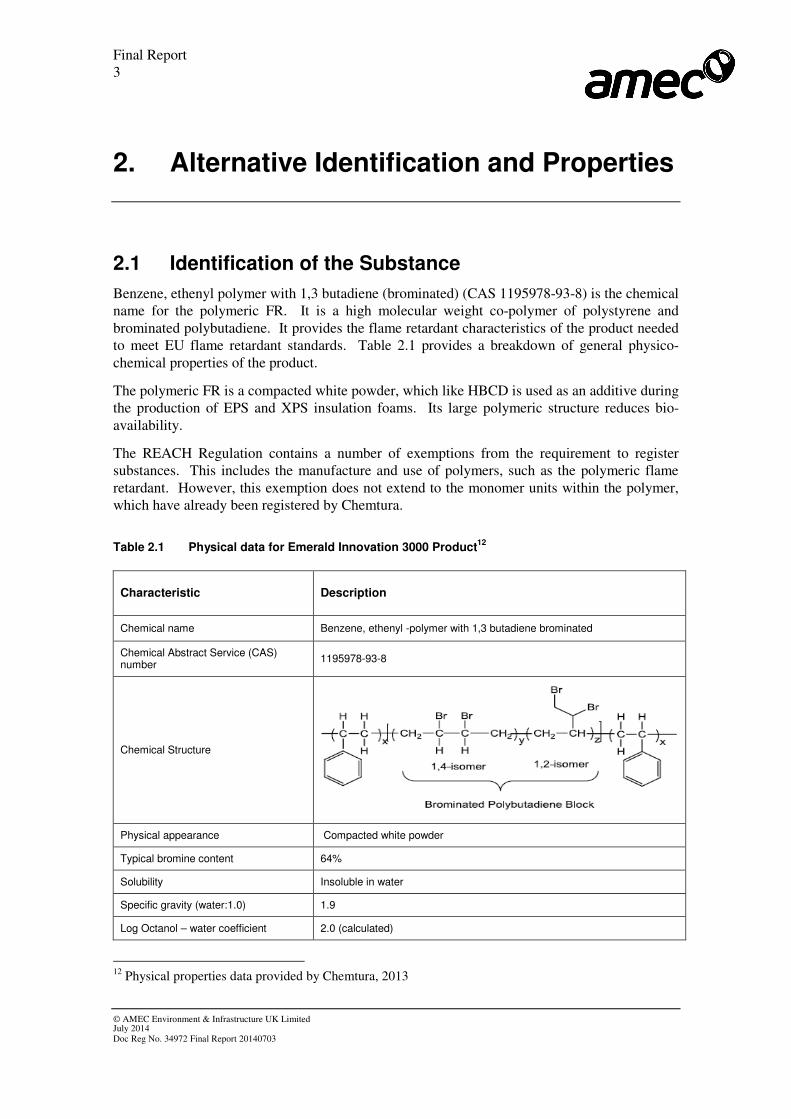

2. Alternative Identification and Properties

2.1 Identification of the Substance

Benzene, ethenyl polymer with 1,3 butadiene (brominated) (CAS 1195978-93-8) is the chemical name for the polymeric FR. It is a high molecular weight co-polymer of polystyrene and

brominated polybutadiene. It provides the flame retardant characteristics of the product needed to meet EU flame retardant standards. Table 2.1 provides a breakdown of general physico-

chemical properties of the product.

The polymeric FR is a compacted white powder, which like HBCD is used as an additive during the production of EPS and XPS insulation foams. Its large polymeric structure reduces bio-

availability.

The REACH Regulation contains a number of exemptions from the requirement to register substances. This includes the manufacture and use of polymers, such as the polymeric flame

retardant. However, this exemption does not extend to the monomer units within the polymer, which have already been registered by Chemtura.

Table 2.1 Physical data for Emerald Innovation 3000 Product12

Characteristic Description

Chemical name Benzene, ethenyl -polymer with 1,3 butadiene brominated

Chemical Abstract Service (CAS) number

1195978-93-8

Chemical Structure

Physical appearance Compacted white powder

Typical bromine content 64%

Solubility Insoluble in water

Specific gravity (water:1.0) 1.9

Log Octanol – water coefficient 2.0 (calculated)

12 Physical properties data provided by Chemtura, 2013

Final Report 4

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

2.2 Manufacture and Uses

2.2.1 Overview of uses

The use of XPS and EPS insulation foam containing HBCD flame retardant is primarily in building insulation. This use accounts for over 99% of the EU market of some 12,000 tonnes

per year. The remaining volumes, less than 1%, are used in high impact polystyrene, which is not considered further in this report13. The use of HBCD for textile back coating has largely

ceased.

The benefits of XPS and EPS insulation foam include their thermal insulation capacity, which reduces heating energy consumption/costs. The foams are lightweight and can be formulated in

a wide range of sizes/thicknesses, with excellent mechanical properties and water resistance14. The use of a flame retardant in these products protects lives and property from fire.

2.2.2 Market Size

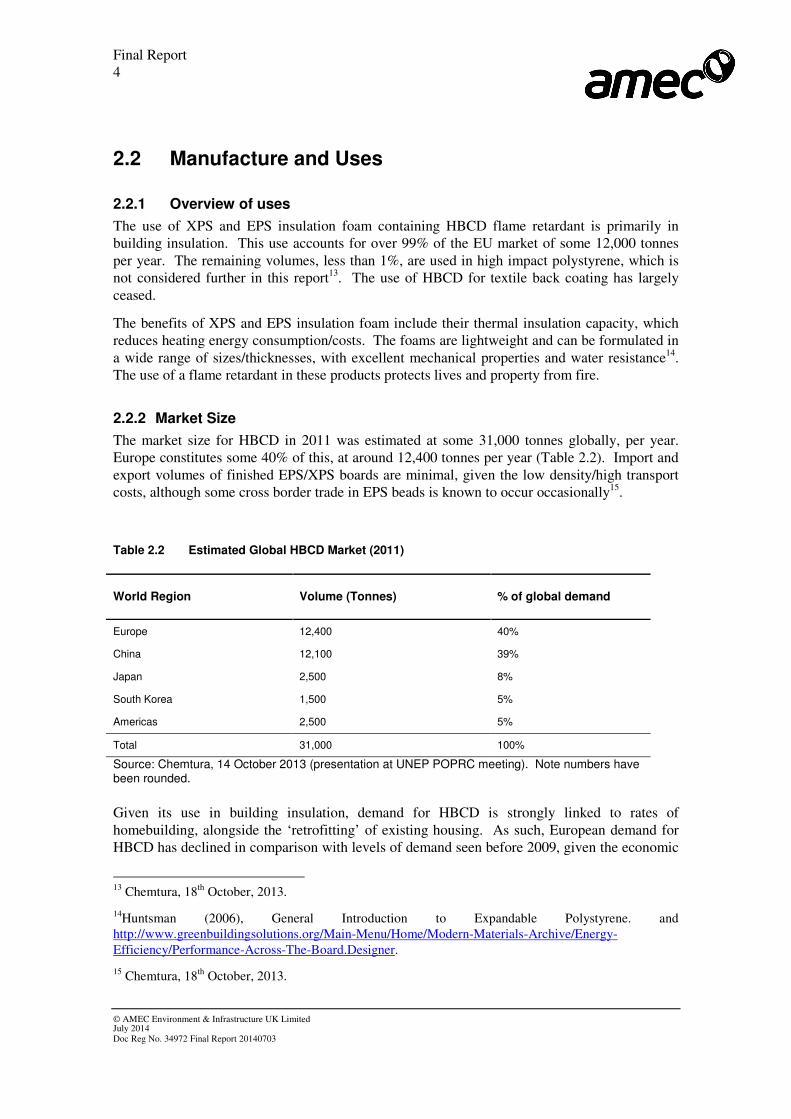

The market size for HBCD in 2011 was estimated at some 31,000 tonnes globally, per year. Europe constitutes some 40% of this, at around 12,400 tonnes per year (Table 2.2). Import and

export volumes of finished EPS/XPS boards are minimal, given the low density/high transport costs, although some cross border trade in EPS beads is known to occur occasionally15.

Table 2.2 Estimated Global HBCD Market (2011)

World Region Volume (Tonnes) % of global demand

Europe 12,400 40%

China 12,100 39%

Japan 2,500 8%

South Korea 1,500 5%

Americas 2,500 5%

Total 31,000 100%

Source: Chemtura, 14 October 2013 (presentation at UNEP POPRC meeting). Note numbers have been rounded.

Given its use in building insulation, demand for HBCD is strongly linked to rates of

homebuilding, alongside the ‘retrofitting’ of existing housing. As such, European demand for HBCD has declined in comparison with levels of demand seen before 2009, given the economic

13 Chemtura, 18th October, 2013.

14Huntsman (2006), General Introduction to Expandable Polystyrene. and http://www.greenbuildingsolutions.org/Main-Menu/Home/Modern-Materials-Archive/Energy-

Efficiency/Performance-Across-The-Board.Designer.

15 Chemtura, 18th October, 2013.

Final Report 5

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

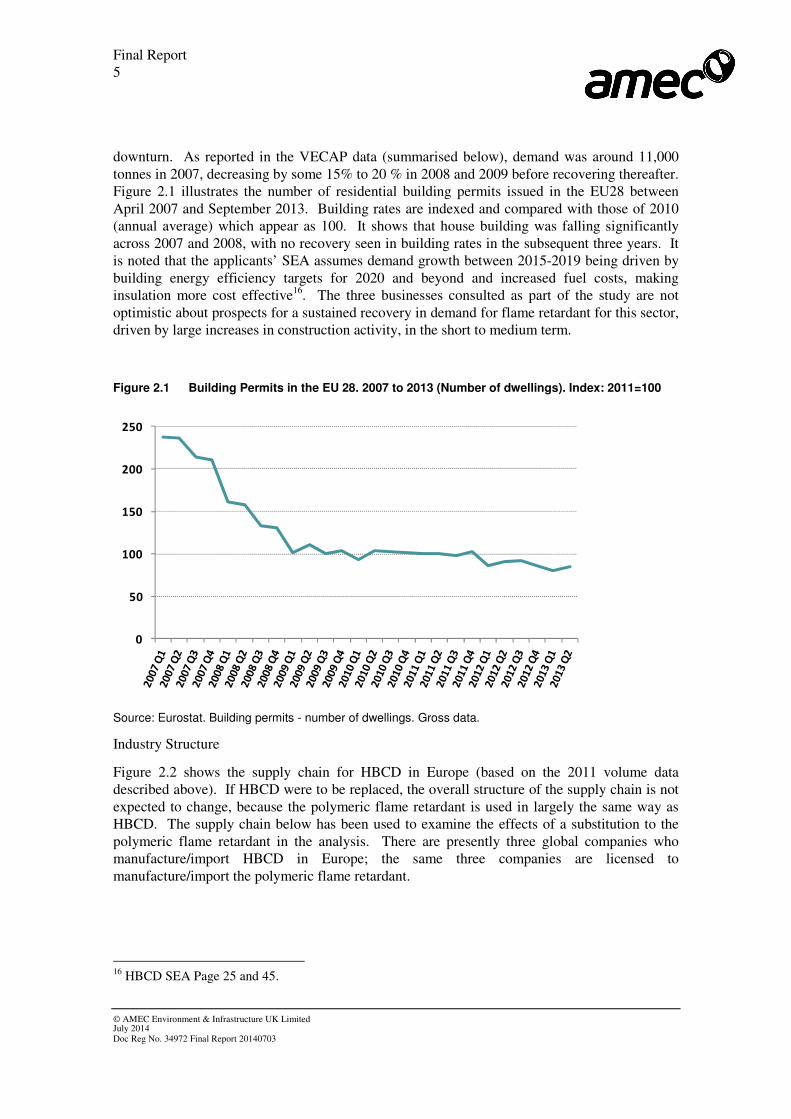

downturn. As reported in the VECAP data (summarised below), demand was around 11,000

tonnes in 2007, decreasing by some 15% to 20 % in 2008 and 2009 before recovering thereafter. Figure 2.1 illustrates the number of residential building permits issued in the EU28 between

April 2007 and September 2013. Building rates are indexed and compared with those of 2010 (annual average) which appear as 100. It shows that house building was falling significantly

across 2007 and 2008, with no recovery seen in building rates in the subsequent three years. It is noted that the applicants’ SEA assumes demand growth between 2015-2019 being driven by

building energy efficiency targets for 2020 and beyond and increased fuel costs, making insulation more cost effective16. The three businesses consulted as part of the study are not

optimistic about prospects for a sustained recovery in demand for flame retardant for this sector, driven by large increases in construction activity, in the short to medium term.

Figure 2.1 Building Permits in the EU 28. 2007 to 2013 (Number of dwellings). Index: 2011=100

0

50

100

150

200

250

Source: Eurostat. Building permits - number of dwellings. Gross data.

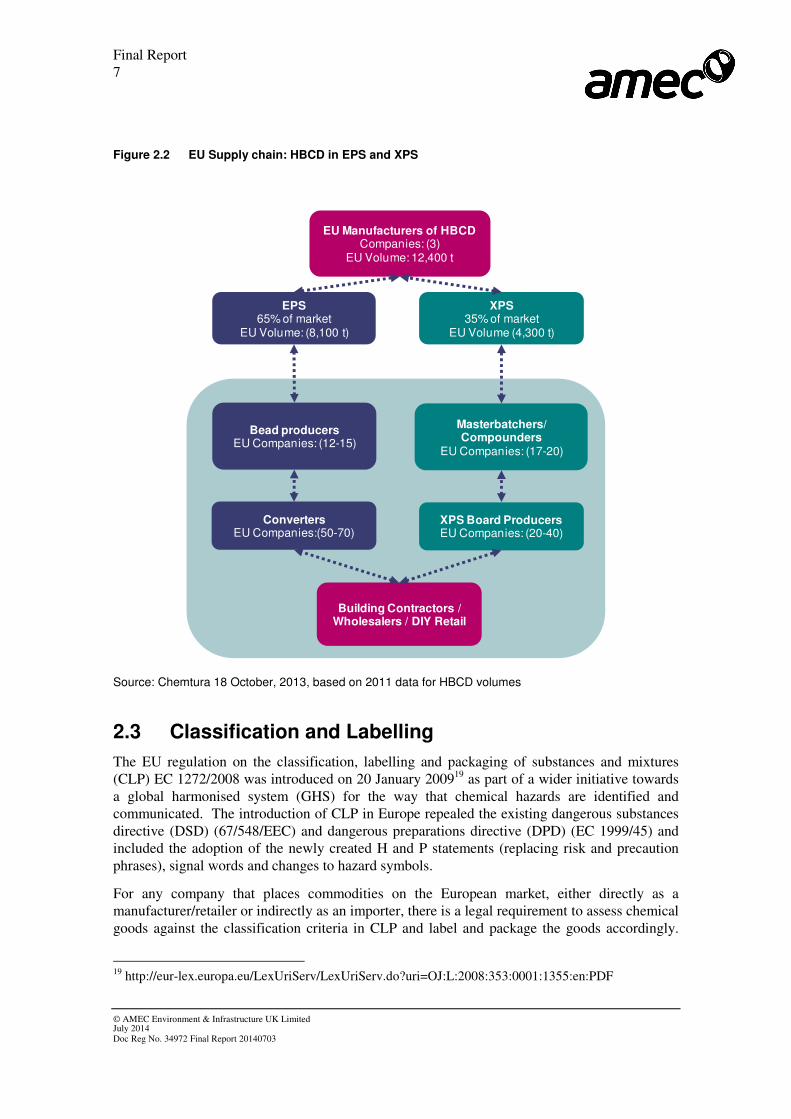

Industry Structure

Figure 2.2 shows the supply chain for HBCD in Europe (based on the 2011 volume data described above). If HBCD were to be replaced, the overall structure of the supply chain is not

expected to change, because the polymeric flame retardant is used in largely the same way as HBCD. The supply chain below has been used to examine the effects of a substitution to the

polymeric flame retardant in the analysis. There are presently three global companies who manufacture/import HBCD in Europe; the same three companies are licensed to

manufacture/import the polymeric flame retardant.

16 HBCD SEA Page 25 and 45.

Final Report 6

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

The EPS and XPS supply chains differ somewhat. Of the 12,400 tonnes of HBCD used in the

EU, some 99% (12,400t) are used in polystyrene foam (EPS or XPS)17. Of this some 65% (8,100 tonnes) are used in the manufacture of EPS. There are two types of EPS: white EPS

(some 65% to 70% of the market or around 5,400 tonnes in Europe, per year) and Grey EPS (some 30% to 35% of the market, or around 2,600 tonnes per year, in Europe).

The flame retardant is sold to EPS bead producers (around 15 companies) who sell EPS beads

to converters (some 60 companies) who then sell the finished EPS board to building contractors/wholesalers and some major retailers18.

The remaining 35% (4,300 tonnes) is used in XPS, where HBCD is sold to masterbatch/compounding firms, of which there are up to 20 in the EU. The compounds are sold to XPS board producers (of which there are between 20 and 40 companies across Europe)

and then to the same types of end users.

17 Note that a small volume - less than 1% are used in other applications, for the purpose of the analysis

this small volume has not subtracted from the total volume identified. Note that numbers have been rounded.

18 Note that we have largely considered numbers of companies within this analysis. The number of sites

is larger, as several companies operate multiple sites across Europe.

Final Report 7

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Figure 2.2 EU Supply chain: HBCD in EPS and XPS

EU Manufacturers of HBCDCompanies: (3)

EU Volume: 12,400 t

Bead producers EU Companies: (12-15)

Building Contractors / Wholesalers / DIY Retail

Converters EU Companies:(50-70)

Masterbatchers/Compounders

EU Companies: (17-20)

XPS Board ProducersEU Companies: (20-40)

EPS65% of market

EU Volume: (8,100 t)

XPS35% of market

EU Volume (4,300 t)

Source: Chemtura 18 October, 2013, based on 2011 data for HBCD volumes

2.3 Classification and Labelling

The EU regulation on the classification, labelling and packaging of substances and mixtures (CLP) EC 1272/2008 was introduced on 20 January 200919 as part of a wider initiative towards

a global harmonised system (GHS) for the way that chemical hazards are identified and communicated. The introduction of CLP in Europe repealed the existing dangerous substances

directive (DSD) (67/548/EEC) and dangerous preparations directive (DPD) (EC 1999/45) and included the adoption of the newly created H and P statements (replacing risk and precaution

phrases), signal words and changes to hazard symbols.

For any company that places commodities on the European market, either directly as a manufacturer/retailer or indirectly as an importer, there is a legal requirement to assess chemical

goods against the classification criteria in CLP and label and package the goods accordingly.

19 http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2008:353:0001:1355:en:PDF

Final Report 8

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

This includes the creation of a REACH-compliant safety data sheet (SDS) providing all relevant

information. Emerald Innovation 3000 has been assessed both against the CLP regulation and its predecessors under DPD and DSD. The substance will not require any specific hazard

symbols or phrases to be used on packaging or SDS.

2.4 HBCD Application for Authorisation: Commentary on the SEA and AofA

2.4.1 Scope of Application

The applicants are seeking continued use of EPS in building applications only. An application for authorisation for continued use of HBCD in XPS was not submitted (to our knowledge). This implies that technical and economic feasibility and availability of alternative(s) for the XPS market is accepted by the XPS market. The applicants also note that import of the final articles is not considered to be viable20.

2.4.2 Market Size

The applicants estimate demand for HBCD in both 2007 and again in 2011. This is used as a

basis for estimating demand for the polymeric flame retardant. Total demand for HBCD in Europe in 2007 is estimated by the applicants at 12,625 tonnes based on a confidential CMAI

study from 200921. Total European and global demand in 2011 is subsequently estimated, based on several assumptions and two data sources, discussed below:

• To estimate 2011 demand for HBCD in Europe, the applicants assume a 4% annual

growth rate in demand for EPS and 3% for XPS and apply this to the 12,625 figure

above. The applicants state this would equate to demand in Europe in 2011 of some 14,483 tonnes. This is based on an estimate of annual growth from the

consortium members themselves, rather than on published sales data.

• In relation to HBCD demand arising from outside of the EU, the applicants quote

data from Chemtura’s presentation at the UNEP POPPRC of 14 October 2013. The HBCD demand figures presented in the application for authorisation, in all non

EU regions (Japan, Americas, China and Korea) are the same as those presented by Chemtura.

• The applicants estimate can be compared to data published under the Voluntary

Emissions Control Programme (VECAP), which suggests EU sales of HBCD of between 10,000 and 12,500 tonnes in 2011 and in 2012, along with an earlier drop

in sales between 2007 and 2009 (Table 2.3)22. The data below appears consistent with the assumptions made in this study (set out in Table 2.2 above).

20 HBCD SEA Pages 9 and 57.

21 HBCD SEA Page 25. This figure was derived by taking the volume of EPS and XPS in 2007, and factoring in the estimated amount used in construction, the assumed amount that is flame retarded, and

the average HBCD content.

22 Chemtura, personal communication, June 2014. It should be noted that VECAP surveys include

HBCDD sales to Norway, Switzerland and Turkey. Imports from non EFRA companies to the EU are not

Final Report 9

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Table 2.3 Estimated European HBCD Market (Based on VECAP Survey data)

Volumes sold by EFRA Members (tonnes)

2007 2008 2009 2010 2011 2012

Total 10,897 [1] 8,913 [2] 9,280 [2] 10,000 -12,500 [3]

10,000 -12,500 [3]

10,000-12,500 [3]

Sources:

[1] http://www.vecap.info/uploads/VECAP_report_22%2001.pdf

[2] http://www.vecap.info/uploads/VECAP_2011_light.pdf

[3] http://www.vecap.info/uploads/VcapLayout34_WEB.pdf

Overall, the applicant’s assumptions in terms of EU demand for HBCD are much higher than the published data above, in Figure 2.1 and the assumed level of growth is not consistent with information from the three companies consulted as part of this study who have reported a fall in demand, reflecting weaker economic conditions in Europe. The 2011 European HBCD demand figure assumed by the applicants (14,483 tonnes) is some 15% higher than that used in this analysis (12,400 tonnes) and between 16% and 45% higher than that assumed by VECAP.

2.4.3 Industry Structure

The applicants identify a total of 22 sites in 2007 (with a further 4 later identified) that produce flame retardant EPS beads and a total of 587 flame retardant bead converter facilities in the EU23. A total of 56 XPS ‘production facilities’ are identified in the (enlarged) EU24. This differs from the approach taken in this study, which uses number of companies, rather than sites. It is understood that many companies have several sites/facilities.

included. In the absence of publicly available data for both of these aspects, it is understood that these

volumes are likely be broadly equal so that the figures represent a reasonable estimate of the EU market.

23 HBCD SEA Pages 33 and 35.

24 HBCD SEA page 105.

Final Report 10

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

3. Technical Feasibility

3.1 Introduction

This section details the technical feasibility of Emerald Innovation 3000 in terms of its ability to provide equivalent functionality to the existing flame retardant product HBCD. It provides a

background to EPS production and examines technical aspects of substitution. No assessment of substitution associated with XPS has been undertaken. Statements made by a number of

companies at a Stockholm Convention POP Review Committee (POPRC9) meeting held in October 2013 relating to the technical feasibility of the product are also summarised.

3.2 Substance Function and Requirements for the Alternative

3.2.1 Requirements of the alternative

To remain compliant with EU and national regulation on fire-resistant properties within

building materials, it is necessary for EPS (and XPS) insulation products to contain flame retardants. HBCD is effective at concentrations of c. 0.7 % in White EPS25, c.1.1% in Grey

EPS and c.1.75% in XPS, meeting physical and fire resistance requirements.

The two key elements for substance function are therefore that it:

i) allows EPS products to meet the required flame resistance limits; and

ii) must not alter the physical properties of the product, particularly density (which affects

costs), mechanical strength and lambda value (i.e. thermal conductivity)26.

Both HBCD and Emerald Innovation 3000 are ‘additive’ flame retardants. They are solids that are added to the polystyrene products during manufacture and blending. A brief description of

how EPS is manufactured is below.

3.2.2 Standard production process for EPS27

Production of Expanded Polystyrene (EPS) is a batch process that centres around two stages:

i) Manufacture of EPS beads. EPS beads are produced in a thermal process where styrene

monomer, additives and flame-retardant are mixed within a water solution in a pressurised

25 These are the loadings assumed in the analysis which are based on consultation with Chemtura and

other HBCD users. They are indicative, the precise formulation for flame retardant (and other additives)

is the manufacturers’ proprietary information.

26 http://www.ecotherm.co.uk/rigid_insulation/thermal_conductivity.aspx

27 Posner et al, 2010, Exploration of Management Options for HBCD – report for the UNECE

Final Report 11

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

vessel at 65-145 degrees Celsius. During this closed-cycle mixing phase, the styrene

monomer polymerises to form polystyrene incorporating the additives (including flame-retardants) and pentane into its matrix (HBCD is not chemically bonded to the polystyrene).

The polymer is then collected from solution using centrifuge and dried to form hard beads of polystyrene compound.

ii) Expansion to manufacture boards. In the second phase, EPS beads are heated with steam,

causing the pentane component to volatise and spur expansion of the bead up to 50 times its

original size. This produces a light-weight product with high thermal insulation properties. The expanded beads are then steam-heated to melt them, and allow moulding into boards or

sheets for construction of the final product. The boards can then be cut to shape as required.

3.3 Technical Stages in Substitution

The use of flame retardant chemicals occurs during the manufacture of the beads for EPS

products. A delicate mixture of compounds is blended with styrene/polystyrene to derive optimal performance in the final goods. Emerald Innovation 3000 would be used (substituted)

within this part of the process. It can be used in a similar fashion to HBCD with few requirements for new infrastructure or capital investment in equipment.

The main technical issues faced for substitution will be reformulation of the blends needed to

produce EPS. The relevant product recipes need to be modified which requires research and development work. This can involve relatively minor modifications in each case, but a fair deal

of experimentation28. The revised recipe(s) also require testing in downstream users’ equipment and this has required some technical support.

Emerald Innovation 3000 contains less bromine content (per kg) compared to HBCD (64% vs

74% in HBCD), which means that more Emerald Innovation 3000 is needed within the mixture (typically c.15% more however assessments in the present study on economic feasibility and

availability are based on a conservative figure of 20%) to reach the required fire performance. However, quantities required are still low. Products containing Emerald Innovation 3000

passed both the EN class E and German B2 flammability tests29. Reformulation of blends for EPS requires pilot trials and assessments of product, before scaling up to full operational

production.

This process can take up to 1 year to complete successfully. The applicants’ analysis of alternatives states that the ‘optimum’ and ‘most likely’ timings for product confirmation from

commercial availability was between 6 months and 10 months, respectively30. However, as Emerald Innovation 3000 has been commercially available on the market for some time (up to

three years) much of this work has already been completed, by several companies.

28 Interview with downstream user, 11 November 2013.

29 Based on discussions with Chemtura.

30 HBCD AofA Figure 5.3 Page 101 and 102.

Final Report 12

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

3.4 Implications of Substitution

Research carried out by the Industry Foam Association, European Association of Polystyrene

Producers and Research Institute for Thermal Protection (FIW) presented to the German Institute for Building Technology (DIBT)31 demonstrated that there were no performance

concerns for the polymeric flame retardant and that the heat insulating, fire performance and physical properties of the EPS products analysed were unaffected.

The most significant implication for substitution from a technical perspective is the

reformulation of blends. HBCD has been used for many years with sufficient industrial experience to fully optimise production and minimise waste. The work to integrate Emerald

Innovation 3000 into the market place has already been underway for some time with commercialisation of the product already in place (by several companies), albeit not at full

capacity. Further expansion of the market is not expected to cause any serious concerns for further optimisation of blends and production, overall, although this is an ongoing process.

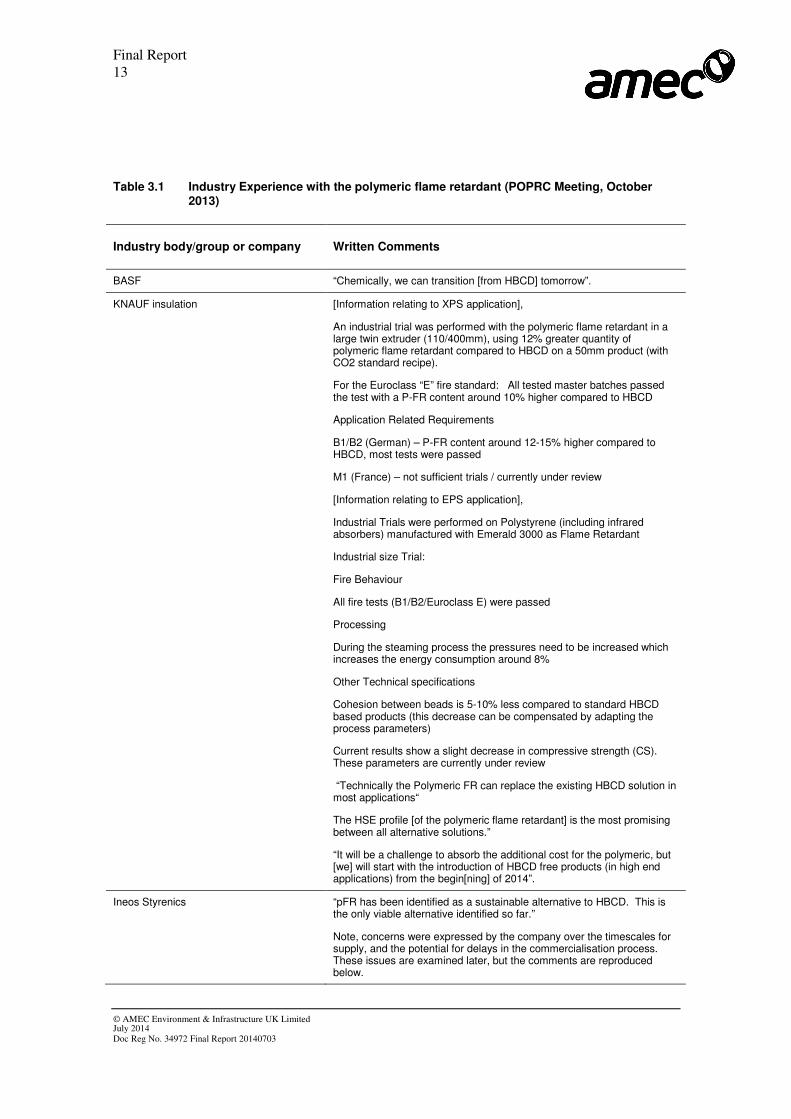

3.5 Wider Industry Experience with Substitution

During the ninth Stockholm Convention POP Review Committee (POPRC9) meeting held in October 2013, a side event was held on ‘alternatives to HBCD - state of play’32. During the side

event, presentations from across the industry were made, providing information on the alternatives available and feedback on experience with alternative substances, to date.

Presentations were made from all three licensees for the polymeric alternative: Chemtura, Albermarle and ICL, with a further presentation made by the manufacturers of a non polymeric

alternative with the trade name ‘BDDP’. User feedback was provided by a number of companies such as Ineos Styrenics, BASF, DOW, Synthos SA, Isochemicals, Kaneka

Corporation (Japan), Knauf Insulation and Flint Hills Resources USA33. There was not complete agreement between all industry members and some challenges have arisen and

concerns were aired at the meeting; however a summary of the key findings is presented in Table 3.1 below. The information is taken directly from the respective company presentations,

with minor edits provided for clarification.

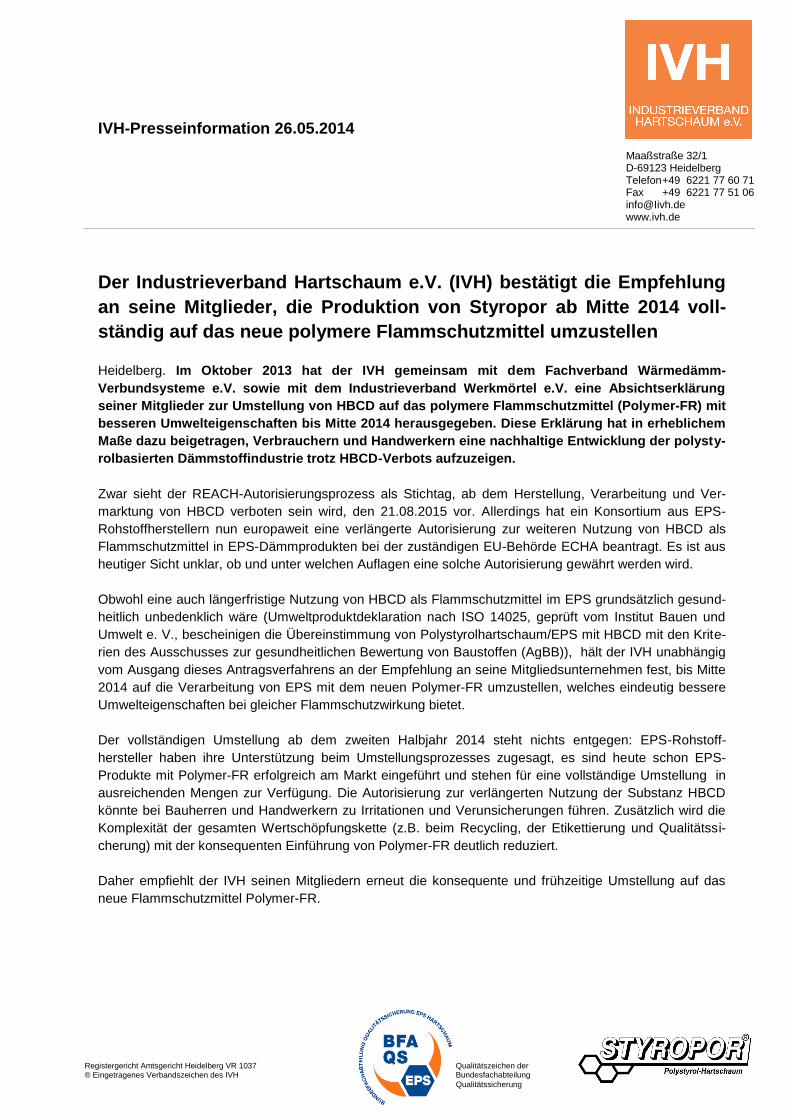

31 IVH press release, 2013, “Industry is striving for EPS flame retardant exchange by mid-2014”

(translation).

32 http://chm.pops.int/TheConvention/POPsReviewCommittee/Meetings/POPRC9/Overview/tabid/3280/mctl/ViewDeta

ils/EventModID/871/EventID/407/xmid/10326/Default.aspx

33 Source: programme for the HBCD side event, Monday 14-10-2013.

Final Report 13

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Table 3.1 Industry Experience with the polymeric flame retardant (POPRC Meeting, October 2013)

Industry body/group or company Written Comments

BASF “Chemically, we can transition [from HBCD] tomorrow”.

KNAUF insulation [Information relating to XPS application],

An industrial trial was performed with the polymeric flame retardant in a large twin extruder (110/400mm), using 12% greater quantity of polymeric flame retardant compared to HBCD on a 50mm product (with CO2 standard recipe).

For the Euroclass “E” fire standard: All tested master batches passed the test with a P-FR content around 10% higher compared to HBCD

Application Related Requirements

B1/B2 (German) – P-FR content around 12-15% higher compared to HBCD, most tests were passed

M1 (France) – not sufficient trials / currently under review

[Information relating to EPS application],

Industrial Trials were performed on Polystyrene (including infrared absorbers) manufactured with Emerald 3000 as Flame Retardant

Industrial size Trial:

Fire Behaviour

All fire tests (B1/B2/Euroclass E) were passed

Processing

During the steaming process the pressures need to be increased which increases the energy consumption around 8%

Other Technical specifications

Cohesion between beads is 5-10% less compared to standard HBCD based products (this decrease can be compensated by adapting the process parameters)

Current results show a slight decrease in compressive strength (CS). These parameters are currently under review

“Technically the Polymeric FR can replace the existing HBCD solution in most applications“

The HSE profile [of the polymeric flame retardant] is the most promising between all alternative solutions.”

“It will be a challenge to absorb the additional cost for the polymeric, but [we] will start with the introduction of HBCD free products (in high end applications) from the begin[ning] of 2014”.

Ineos Styrenics “pFR has been identified as a sustainable alternative to HBCD. This is the only viable alternative identified so far.”

Note, concerns were expressed by the company over the timescales for supply, and the potential for delays in the commercialisation process. These issues are examined later, but the comments are reproduced below.

Final Report 14

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Industry body/group or company Written Comments

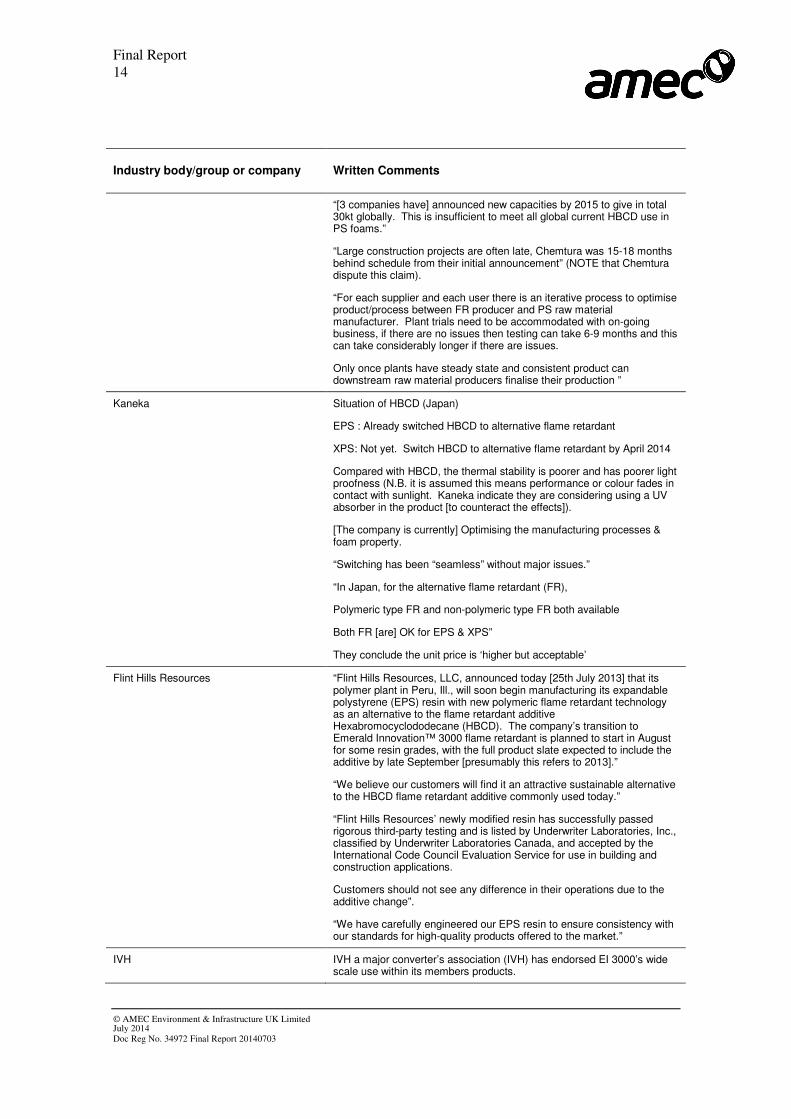

“[3 companies have] announced new capacities by 2015 to give in total 30kt globally. This is insufficient to meet all global current HBCD use in PS foams.”

“Large construction projects are often late, Chemtura was 15-18 months behind schedule from their initial announcement” (NOTE that Chemtura dispute this claim).

“For each supplier and each user there is an iterative process to optimise product/process between FR producer and PS raw material manufacturer. Plant trials need to be accommodated with on-going business, if there are no issues then testing can take 6-9 months and this can take considerably longer if there are issues.

Only once plants have steady state and consistent product can downstream raw material producers finalise their production ”

Kaneka Situation of HBCD (Japan)

EPS : Already switched HBCD to alternative flame retardant

XPS: Not yet. Switch HBCD to alternative flame retardant by April 2014

Compared with HBCD, the thermal stability is poorer and has poorer light proofness (N.B. it is assumed this means performance or colour fades in contact with sunlight. Kaneka indicate they are considering using a UV absorber in the product [to counteract the effects]).

[The company is currently] Optimising the manufacturing processes & foam property.

“Switching has been “seamless” without major issues.”

“In Japan, for the alternative flame retardant (FR),

Polymeric type FR and non-polymeric type FR both available

Both FR [are] OK for EPS & XPS”

They conclude the unit price is ‘higher but acceptable’

Flint Hills Resources “Flint Hills Resources, LLC, announced today [25th July 2013] that its polymer plant in Peru, Ill., will soon begin manufacturing its expandable polystyrene (EPS) resin with new polymeric flame retardant technology as an alternative to the flame retardant additive Hexabromocyclododecane (HBCD). The company’s transition to Emerald Innovation™ 3000 flame retardant is planned to start in August for some resin grades, with the full product slate expected to include the additive by late September [presumably this refers to 2013].”

“We believe our customers will find it an attractive sustainable alternative to the HBCD flame retardant additive commonly used today.”

“Flint Hills Resources’ newly modified resin has successfully passed rigorous third-party testing and is listed by Underwriter Laboratories, Inc., classified by Underwriter Laboratories Canada, and accepted by the International Code Council Evaluation Service for use in building and construction applications.

Customers should not see any difference in their operations due to the additive change”.

“We have carefully engineered our EPS resin to ensure consistency with our standards for high-quality products offered to the market.”

IVH IVH a major converter’s association (IVH) has endorsed EI 3000’s wide scale use within its members products.

Final Report 15

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Industry body/group or company Written Comments

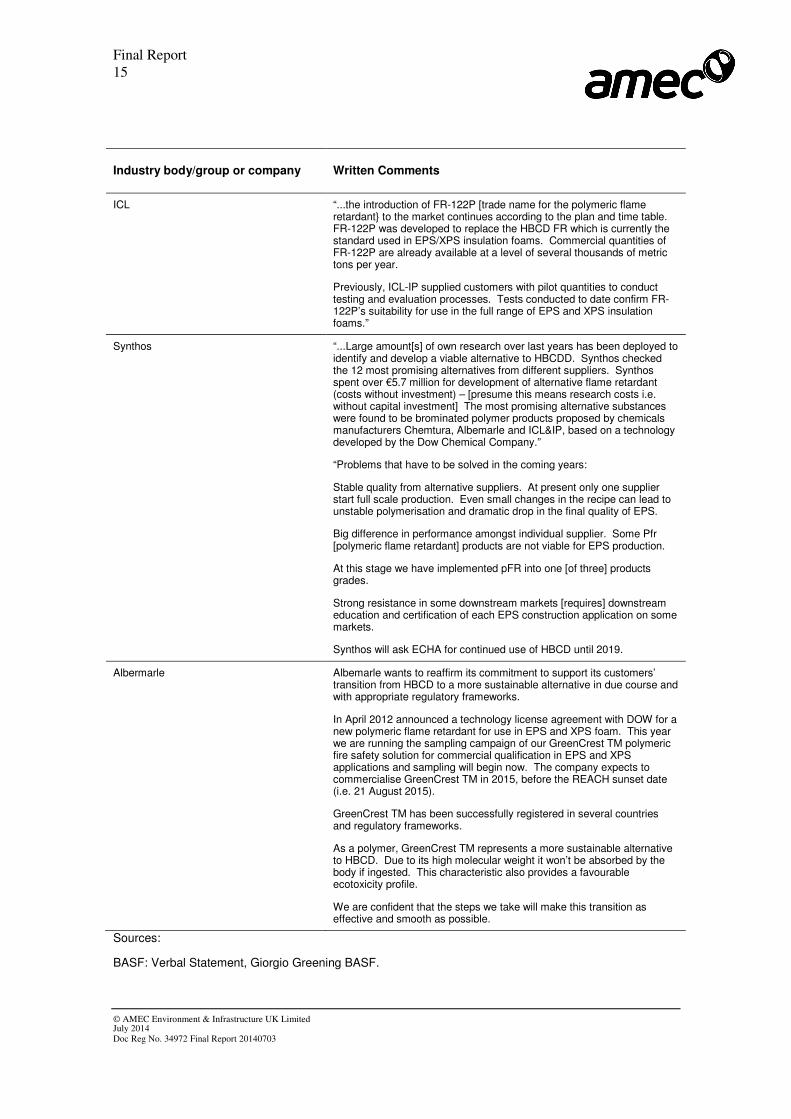

ICL “...the introduction of FR-122P [trade name for the polymeric flame retardant} to the market continues according to the plan and time table. FR-122P was developed to replace the HBCD FR which is currently the standard used in EPS/XPS insulation foams. Commercial quantities of FR-122P are already available at a level of several thousands of metric tons per year.

Previously, ICL-IP supplied customers with pilot quantities to conduct testing and evaluation processes. Tests conducted to date confirm FR-122P’s suitability for use in the full range of EPS and XPS insulation foams.”

Synthos “...Large amount[s] of own research over last years has been deployed to identify and develop a viable alternative to HBCDD. Synthos checked the 12 most promising alternatives from different suppliers. Synthos spent over €5.7 million for development of alternative flame retardant (costs without investment) – [presume this means research costs i.e. without capital investment] The most promising alternative substances were found to be brominated polymer products proposed by chemicals manufacturers Chemtura, Albemarle and ICL&IP, based on a technology developed by the Dow Chemical Company.”

“Problems that have to be solved in the coming years:

Stable quality from alternative suppliers. At present only one supplier start full scale production. Even small changes in the recipe can lead to unstable polymerisation and dramatic drop in the final quality of EPS.

Big difference in performance amongst individual supplier. Some Pfr [polymeric flame retardant] products are not viable for EPS production.

At this stage we have implemented pFR into one [of three] products grades.

Strong resistance in some downstream markets [requires] downstream education and certification of each EPS construction application on some markets.

Synthos will ask ECHA for continued use of HBCD until 2019.

Albermarle Albemarle wants to reaffirm its commitment to support its customers’ transition from HBCD to a more sustainable alternative in due course and with appropriate regulatory frameworks.

In April 2012 announced a technology license agreement with DOW for a new polymeric flame retardant for use in EPS and XPS foam. This year we are running the sampling campaign of our GreenCrest TM polymeric fire safety solution for commercial qualification in EPS and XPS applications and sampling will begin now. The company expects to commercialise GreenCrest TM in 2015, before the REACH sunset date (i.e. 21 August 2015).

GreenCrest TM has been successfully registered in several countries and regulatory frameworks.

As a polymer, GreenCrest TM represents a more sustainable alternative to HBCD. Due to its high molecular weight it won’t be absorbed by the body if ingested. This characteristic also provides a favourable ecotoxicity profile.

We are confident that the steps we take will make this transition as effective and smooth as possible.

Sources:

BASF: Verbal Statement, Giorgio Greening BASF.

Final Report 16

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

KNAUF insulation: HBCD Replacement by Brominated Butadiene-Styrene Polymer (BrBDS). Mr Kurt Muender.

Ineos Styrenics POPRC9 HBCD Side Event: A European perspective.

Kaneka: From HBCD to the alternative flame retardant.

Flint Hills: Flint Hills Resources Press Release: Flint Hills resources will manufacture expandable polystyrene with new flame retardant technology.

ICL: ‘ICL IP Commercial availability of sustainable polymeric flame retardant, October 9th 2013.

Synthos: Transitioning from HBCD to an alternative FR form PS building and construction products.

Albemarle: General statement by Albemarle at the HBCD Alternatives Information Session organised aside the POPRC9 meeting on October 14, 2013

3.6 HBCD Application for Authorisation: Commentary on the SEA and AofA

The technical feasibility of the polymeric flame retardant is not disputed by the applicants, who

are committed to the complete substitution of HBCD. The applicants state that trials have been undertaken by all EPS producers in small quantities based on samples provided by the

polymeric flame retardant suppliers and these trials have indicated technical feasibility34.

The applicants state that further testing and confirmation of technical suitability will need to be carried out by the pellet and article producers, alongside marketing and certification35.

However, as noted above, the polymeric flame retardant is already commercially available – and is being sold. As noted above, much of this work has already been completed, by several

companies. The experience of such companies suggests, whilst acknowledging the process of optimisation is ongoing, that the process of substitution has taken approximately one year. The

applicants’ analysis of alternatives states that the ‘optimum’ and ‘most likely’ timings for product confirmation from commercial availability may be rather than less than this, between 6

months and 10 months, respectively36.

In relation to fire certification, footnote 15 of the applicants’ SEA acknowledges that testing is currently being carried out on behalf of IVH to allow a ‘generic approval of the pFR as a

replacement for HBCD’37. We understand that this testing is now complete.

A press release dated 26 May 2014, from IVH (translated from German and reproduced in Appendix A) recommends that industry switch from HBCD in mid 2014 and that a complete

switch takes place by late 2014. It notes products have already been successfully brought to market using the polymeric flame retardant.

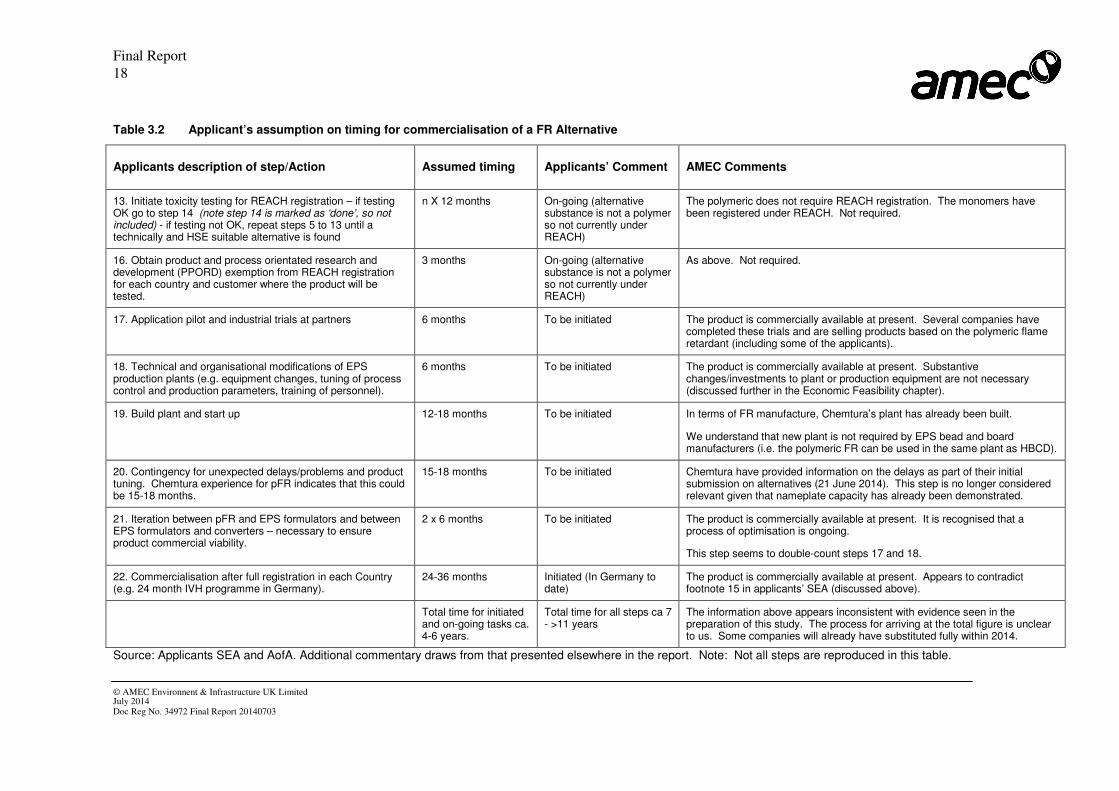

Table 1.4 of the applicants’ AofA provides further assumptions on timescales required to substitute HBCD with the polymeric. This is reproduced in Table 3.2, along with relevant

34 HBCD SEA Page 17.

35 HBCD SEA Page 18.

36 HBCD AofA Figure 5.3 Page 101 and 102.

37 HBCD SEA Page 18.

Final Report 17

© AMEC Environment & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

commentary based on our own analysis and discussion with companies who have started using

the polymeric flame retardant38.

38 HBCD AofA Page 15.

Final Report

18

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Table 3.2 Applicant’s assumption on timing for commercialisation of a FR Alternative

Applicants description of step/Action Assumed timing Applicants’ Comment AMEC Comments

13. Initiate toxicity testing for REACH registration – if testing OK go to step 14 (note step 14 is marked as ‘done’, so not included) - if testing not OK, repeat steps 5 to 13 until a technically and HSE suitable alternative is found

n X 12 months On-going (alternative substance is not a polymer so not currently under REACH)

The polymeric does not require REACH registration. The monomers have been registered under REACH. Not required.

16. Obtain product and process orientated research and development (PPORD) exemption from REACH registration for each country and customer where the product will be tested.

3 months On-going (alternative substance is not a polymer so not currently under REACH)

As above. Not required.

17. Application pilot and industrial trials at partners 6 months To be initiated The product is commercially available at present. Several companies have completed these trials and are selling products based on the polymeric flame retardant (including some of the applicants).

18. Technical and organisational modifications of EPS production plants (e.g. equipment changes, tuning of process control and production parameters, training of personnel).

6 months To be initiated The product is commercially available at present. Substantive changes/investments to plant or production equipment are not necessary (discussed further in the Economic Feasibility chapter).

19. Build plant and start up 12-18 months To be initiated In terms of FR manufacture, Chemtura’s plant has already been built.

We understand that new plant is not required by EPS bead and board manufacturers (i.e. the polymeric FR can be used in the same plant as HBCD).

20. Contingency for unexpected delays/problems and product tuning. Chemtura experience for pFR indicates that this could be 15-18 months.

15-18 months To be initiated Chemtura have provided information on the delays as part of their initial submission on alternatives (21 June 2014). This step is no longer considered relevant given that nameplate capacity has already been demonstrated.

21. Iteration between pFR and EPS formulators and between EPS formulators and converters – necessary to ensure product commercial viability.

2 x 6 months To be initiated The product is commercially available at present. It is recognised that a process of optimisation is ongoing.

This step seems to double-count steps 17 and 18.

22. Commercialisation after full registration in each Country (e.g. 24 month IVH programme in Germany).

24-36 months Initiated (In Germany to date)

The product is commercially available at present. Appears to contradict footnote 15 in applicants’ SEA (discussed above).

Total time for initiated and on-going tasks ca. 4-6 years.

Total time for all steps ca 7 - >11 years

The information above appears inconsistent with evidence seen in the preparation of this study. The process for arriving at the total figure is unclear to us. Some companies will already have substituted fully within 2014.

Source: Applicants SEA and AofA. Additional commentary draws from that presented elsewhere in the report. Note: Not all steps are reproduced in this table.

Final Report 19

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

4. Economic Feasibility

4.1 Introduction

An assessment of economic feasibility of the polymeric flame retardant in comparison with HBCD was undertaken. First, direct costs incurred to the EU EPS insulation foam market

arising through a transition from HBCD to the polymeric flame retardant were assessed. Second, costs to individual companies were examined, based on two approaches: the number of

companies in the supply chain and estimated typical production volumes. Third, the affordability of the costs identified was examined, for businesses of different sizes, based on typical margins for the sector as a whole. Fourth, the effects of these costs on final product

prices were evaluated.

The analysis was based on interviews with major EPS and XPS producers noted in the

introduction and with Chemtura, alongside publicly available data on market characteristics and prices. The detailed step-by-step calculations are not shown; given that economic feasibility of

the polymeric alternative is not disputed by the applicants and is not the subject of the central analysis within the SEA / AofA in the Authorisation Application, which relates to availability.

Overall the assessment indicates that the polymeric flame retardant is an economically feasible

alternative to HBCD. The analysis suggests an increase in the final product price (whether per tonne or per board of EPS) of around 1%. This takes account of additional volumes of the

polymeric flame retardant likely to be required and the higher units costs, in comparison with HBCD alongside fire recertification and testing costs.

Any increase in costs should be considered in light of the following factors. First, a low

proportion of the flame retardant is used in the polystyrene foam formulation. Second, in recent years the price of the major raw material in both EPS and XPS (the styrene monomer) has

varied to a much greater extent than the price changes identified in using the polymeric flame retardant. Third, the analysis has assumed a stable price for Emerald Innovation 3000. . It is

possible that its unit price will decrease, over time.

There are no effects on production speeds anticipated and substantive changes/investments to plant or production equipment are not necessary39. It is understood, from consultation carried

out as part of the study, that a price increase of the scale estimated above is not expected to result in EPS foam losing ground to functional insulation competition (mineral wool, for

example)40.

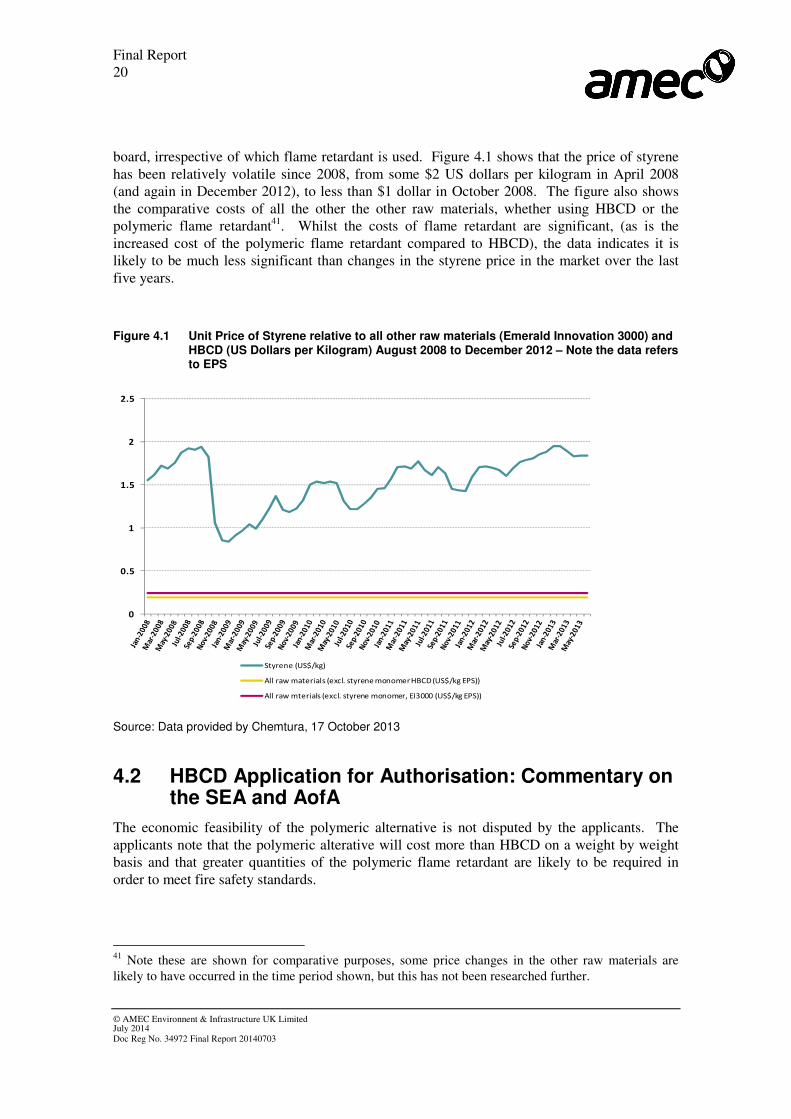

Whether using HBCD or the polymeric as the flame-retardant in EPS or XPS, there are several other raw materials which also affect the end price for EPS/XPS insulation board. For EPS

these are styrene, benzyol peroxide, t-butyl per benzoate, dicumylperoxide and pentane. Of these, the major raw material is styrene, used in approximately equal quantities in EPS and XPS

39 Interview with downstream users on, 5 November 2013, 6 November 2013; and Chemtura, 18 October

2013.

40 Source: Chemtura 4 February 2014 (based on discussions with major FR-polystyrene producers).

Final Report 20

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

board, irrespective of which flame retardant is used. Figure 4.1 shows that the price of styrene

has been relatively volatile since 2008, from some $2 US dollars per kilogram in April 2008 (and again in December 2012), to less than $1 dollar in October 2008. The figure also shows

the comparative costs of all the other the other raw materials, whether using HBCD or the polymeric flame retardant41. Whilst the costs of flame retardant are significant, (as is the

increased cost of the polymeric flame retardant compared to HBCD), the data indicates it is likely to be much less significant than changes in the styrene price in the market over the last

five years.

Figure 4.1 Unit Price of Styrene relative to all other raw materials (Emerald Innovation 3000) and HBCD (US Dollars per Kilogram) August 2008 to December 2012 – Note the data refers to EPS

0

0.5

1

1.5

2

2.5

Styrene (US$/kg)

All raw materials (excl. styrene monomer HBCD (US$/kg EPS))

All raw mterials (excl. styrene monomer, EI3000 (US$/kg EPS))

Source: Data provided by Chemtura, 17 October 2013

4.2 HBCD Application for Authorisation: Commentary on the SEA and AofA

The economic feasibility of the polymeric alternative is not disputed by the applicants. The

applicants note that the polymeric alterative will cost more than HBCD on a weight by weight basis and that greater quantities of the polymeric flame retardant are likely to be required in

order to meet fire safety standards.

41 Note these are shown for comparative purposes, some price changes in the other raw materials are

likely to have occurred in the time period shown, but this has not been researched further.

Final Report 21

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Taking these factors into account the applicants “assume [the polymeric flame retardant] is

economically feasible as EPS producers have the intention to switch from HBCD to the Polymeric flame retardant”42.

Although no price data was available, the applicants note that some EPS producers who are not

part of the HBCD consortium are thought to have secured contracts in place for initial supplies to be available43.

The applicants provide an analysis of the effects on the EU EPS sector’s economic competiveness of insufficient quantities of the polymeric flame retardant being available. This

issue is analysed in section 6. Most if not all of the costs quantified in the applicants’ SEA are predicted to occur as a result in lack of availability of the polymeric flame retardant to the applicant and not due to the relative costs between HBCD and the polymeric FR. If there is no

shortfall between available quantities and EU demand, then we assume these costs – estimated to be in the order of between €740 million and €1,175 million at present values between 2015

and 201944 – would not be incurred.

42 HBCD SEA Page 17

43 HBCD SEA Page 18.

44 HBCD SEA Page 129

Final Report 22

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

5. Hazards and Risks of the Alternative

5.1 Introduction

5.1.1 Overview

This section provides information regarding the hazards and risks of both the polymeric flame retardant and HBCD within the REACH context. The key themes within REACH are to

improve the safe use of chemical substances through the provision of health, safety and environmental data and the control of substances deemed to be of particularly high concern.

For the standard use of chemical substances it is necessary to review applications as part of a chemical safety assessment (CSA) which is then reported through the chemical safety report (CSR) as exposure scenarios in the registration dossiers, and subsequently in the extended

safety data sheet (E-SDS). This is intended to demonstrate the relationship between hazard and risk and control of those risks.

Authorisation is used to control the use of Substances of Very High Concern (SVHC). Identification of a SVHC substance and addition to the SVHC candidate list is based on

nomination by member state competent authorities (MSCAs) or ECHA based on a weight of evidence surrounding qualifying criteria of ‘Persistence, Bioaccumulation and Toxicity’ - PBT

the latter relates to Carcinogenic, Mutagenic or toxic to Reproduction – CMR properties.

HBCD has already been identified as a SVHC substance with listing on the Authorisation list (Annex XIV of REACH). During this review process it was also being assessed under the

UNEP Stockholm Convention on Persistent Organic Pollutants (POPs) for addition to the Convention annexes which can include banning substances from sale or severe restrictions on

use. Under the latter, HBCD will be included on the list of substances for global elimination on 26th November 2014, with exemption for its use in polystyrene foams for buildings.

The remaining sections of this chapter compare the polymeric flame retardant against the PBT

criteria for REACH and HBCD’s properties, as well as an overview of the likely hazards and risks during use, including a discussion of risk management measures (RMMs).

5.1.2 PBT assessments

Annex XIII of the REACH regulation sets out the specific criteria for assessment against PBT characteristics. These are detailed as follows:

Final Report 23

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Persistence

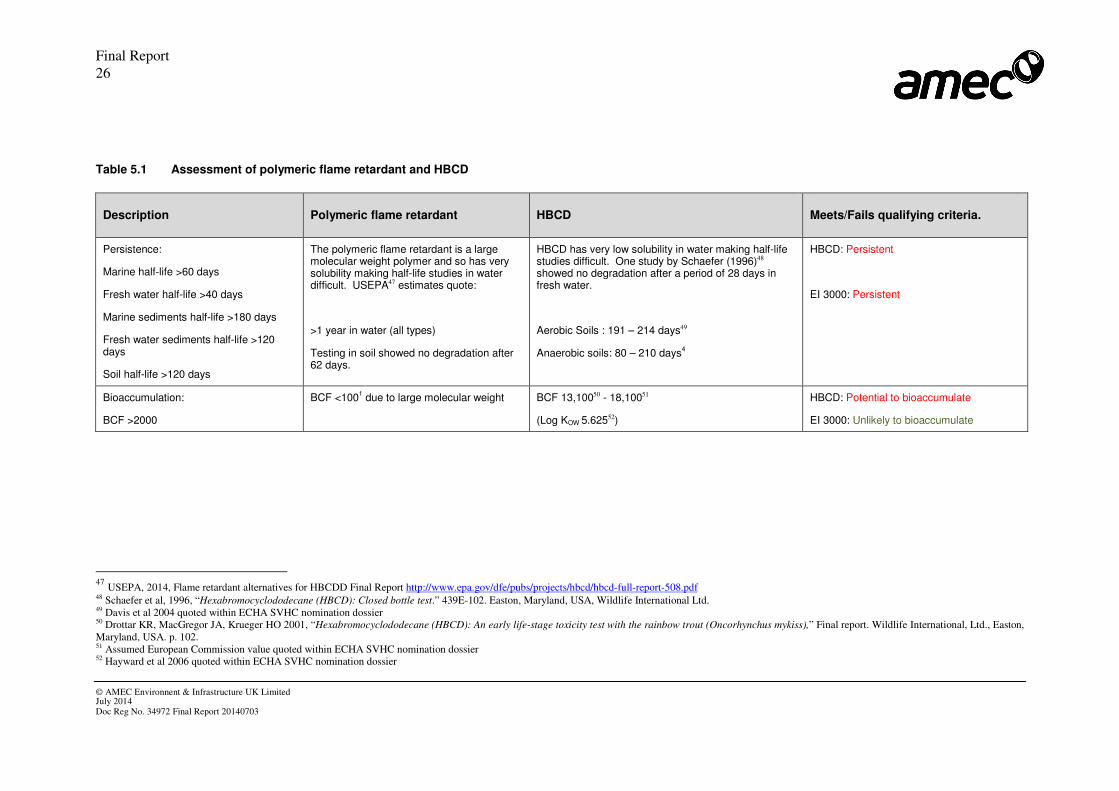

Persistence is a measure of how long a given substance survives in the natural environment in order to cause effect as that substance. Consideration is not given to breakdown products in this regard. The key measure to assess persistence is therefore what is termed ‘half-life’, which is the period of time required for 50% of the substance to have decayed or been broken down into different products. Half-life will vary depending on the natural environment (air, water, soil) and the breakdown processes available to remove a given substance from the environment in that form.

• Annex XIII of the REACH regulation considers a substance meets the ‘persistence’ characteristic if:

• Marine half-life >60 days

• Fresh water half-life >40 days

• Marine sediments half-life >180 days

• Fresh water sediments half-life >120 days

• Soil half-life >120 days

Bioaccumulation

Bioaccumulation is a measure of a given substances ability to accumulate up the food chain where toxic effects can become magnified. Typically substances capable of bioaccumulation concentrate within the fatty tissues of the body where metabolism and excretion are more difficult. Therefore the existing measures for a substance’s ability to bioaccumulate will relate to solubility within both water and oil. Under the REACH regulation the chosen measure is ‘Bio-Concentration Factor (BCF)’ which is a ratio between the quantity of substance within the body tissues of an effected species (usually fish) and the quantity of substance remaining within the water.

Annex XIII of the REACH regulation considers a substance meets the ‘bioaccumulation’ characteristic if:

• BCF >2000

Toxicity

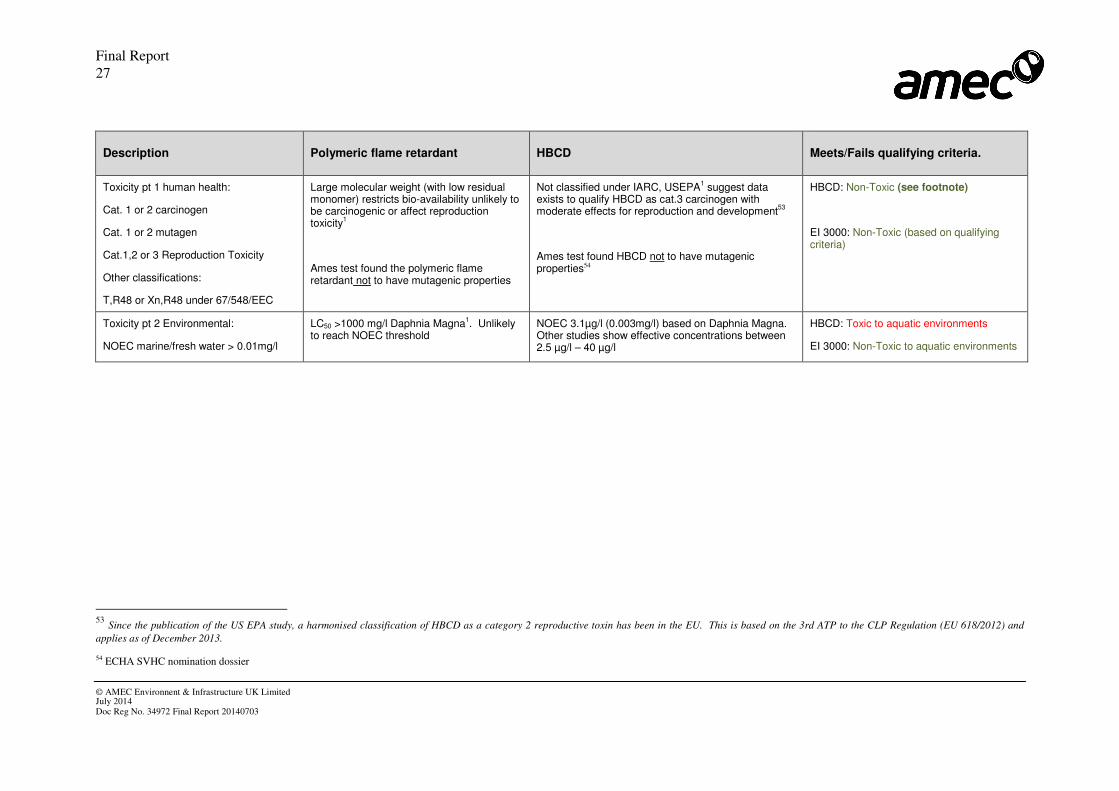

Toxicity within the REACH regulation includes both human health but also environmental affects, particularly to the aquatic environment. The key measure for toxicity affecting human health relates to the ‘Carcinogenic, mutagenic or reproduction toxicity (CMR)’ of a given substance, which is assessed by the International Agency for Research on Cancer (IARC). IARC uses differing categories to indicate the level of potential effect a substance will have with the lowest numbered categories being of the highest hazard.

Annex XIII of the REACH regulation considers a substance meets the ‘toxic’ characteristic if a substance is included in:

• IARC Cat. 1 or 2 carcinogen

• IARC Cat. 1 or 2 mutagen

• IARC Cat.1,2 or 3 Reproduction Toxicity

Other classifications:

• T,R48 or Xn,R48 under 67/548/EEC

Equally, the REACH regulation considers toxic effects for the natural environment, particularly aquatic environment, where the key measure is what is termed ‘No Effect Concentration NOEC’, this is a threshold value above which harmful effects to the aquatic eco-system may start to present.

Annex XIII of the REACH regulation considers a substance meets the ‘toxic’ characteristic if the substance causes harmful effects below the NOEC which is:

• NOEC (marine and freshwaters) 0.01mg/l

Final Report 24

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

5.2 Assessment of the Polymeric Flame Retardant and HBCD

Through the REACH SVHC process HBCD has been confirmed as having PBT characteristics and was added to the REACH Authorisation list in the spring of 2011. Alongside the REACH

process the UNEP Stockholm Convention also confirmed the identity of HBCD as meeting the ‘POP’ classifying criteria and it was provisionally added to Annex A of the convention (in

summer of 2013) requiring a full ban from sale, with specific exemptions, allowing continued use of HBCD for application as a flame retardant in expanded polystyrene (EPS) and extruded

polystyrene (XPS) insulation products in buildings. . Members of the Convention have one year from the provisional addition to ratify at which point it is fully adopted and enters into force.

The POPs Convention Review Committee recognised that replacements for HBCD may take several years to develop and implement; the exemption for EPS and XPS is set at 5 years from

full listing but may be reduced or extended depending on progress with development of alternatives.

One of the key functional characteristics of HBCD’s role as a flame retardant is a high level of

stability. This stability lends itself to the persistent ‘criteria’ under PBT assessment.

A United States EPA review of alternatives to HBCD included the polymeric flame retardant,

amongst others. It assessed all of the alternatives in terms of their health and environmental impact. This assessment included comparison to HBCD as part of the review. Its key

conclusion was that the polymeric flame retardant presented a lower risk to both health and environment than HBCD45.

Table 5.1 provides a summary of the PBT data for both HBCD and the polymeric flame

retardant. This demonstrates HBCD has a bio concentration factor (BCF) in the range between 13,100 – 18,100 (PBT threshold for BCF is 2000), with the latter value accepted by the

European Commission. This suggests that HBCD has a high potential for bioaccumulation. The assessment of evidence related to potential health effects has led to the categorisation of

HBCD as category 2 reproduction toxicity (discussed below). In terms of environmental effects, a number of studies highlight the deleterious effects of HBCD on aquatic species

particularly its role in aquatic toxicity.

As both the REACH and UNEP Stockholm Convention processes have run in tandem, industry has responded by looking to identify viable alternatives to HBCD. In this respect the core

issues have been to locate a substance which has similar or better performance capabilities, viable cost base and essentially does not breach the PBT or POP assessment criteria thereby

replacing one PBT or POP substance with another.

The polymeric flame retardant is a high molecular weight (>100,000 g/mole; Moore, 201346) co-polymer with a high degree of thermal stability and similar flame retardancy performance

levels as HBCD.

45

USEPA, 2014, Flame retardant alternatives for HBCDD, Final Report http://www.epa.gov/dfe/pubs/projects/hbcd/hbcd-full-

report-508.pdf

46 Marshall Moore (Chemtura), 2013, Presentation at the ninth UNEP POP Review Committee (POPRC)

held on 14th October 2013

Final Report 25

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

The review of the polymeric flame retardant substance against the PBT qualifying criteria is

summarised in Table 5.2 and illustrates a low level of solubility and high levels of stability within the natural environment. This high stability, low solubility (as with HBCD) meant that

half-life testing for aquatic environments was difficult, but it did meet the qualifying criteria to be assumed ‘Persistent’ under the REACH process.

The other qualifying criteria, however, differ from HBCD. While the polymeric flame retardant

has a very low solubility, the high molecular weight and size of the molecule reduces bioavailability, meaning that in assessment the potential for bioaccumulation was low, with a

BCF <100. Equally in toxicity testing and assessment for CMR properties, the high molecular weight reduces bioavailability and the potential for the substance to interact with the body in a

deleterious manner. The US-EPA review concluded that the polymeric flame retardant was unlikely to have ‘C’ or ‘R’ characteristics while Ames testing confirmed that it was unlikely to

be mutagenic. Eco-toxicity testing confirmed that toxic effects on aquatic species were also less likely.

CONFIDE NTIAL

Final Report

26

© AMEC Environnent & Infrastructure UK Limited July 2014 Doc Reg No. 34972 Final Report 20140703

Table 5.1 Assessment of polymeric flame retardant and HBCD