chartered institute for securities & investment compliance professionals summit 2010 20 october...

TRANSCRIPT

Chartered Institute for Securities & Investment

COMPLIANCE PROFESSIONALS

SUMMIT 2010

20 October 2010

Key EU Developments in Financial Services RegulationOctober 2010

Agenda

• The new European financial supervisory framework

• Capital Requirements Directive (“CRD”) reform - EU-wide remuneration principles

• MiFID review

• Market Abuse Directive (“MAD”) review

• EC short selling proposal

• The Alternative Investment Fund Managers (“AIFM”) Directive proposal

The New European Financial Supervisory Framework

• New framework agreed in September takes effect on 1 January 2011

• European Systemic Risk Board (ESRB)

• European ‘control tower and radar screens’ to detect risk to financial systems

• European System of Financial Supervisors (ESFS)

– made up of representatives from EBA, ElOPA, ESMA and national supervisors

• European Supervisory Authorities (ESAs)

CEBS → EBA

CEIOPS → EIOPA

CESR → ESMA

• The ESAs will have the power to:

• draw up specific rules for national supervisors and financial institutions, and monitor how rules are being enforced by national supervisors (can, in some circumstances, give binding instructions to national regulators and financial institutions);

• take action in emergencies, including the banning of certain products;

• mediate and settle disputes between national supervisors;

• ensure the consistent application of EU law; and

• ESMA will have direct supervisory powers over credit rating agencies registered in the EU

• Concern over basis on which decisions will be taken

The new European supervisory architecture

National Central Banks

+

ECB

EBA, EIOPA & ESMA

European Commission

Other non-voting members

+ + +

European Banking Authority

(EBA)

London

European Insurance and Occupational

Pensions Authority (EIOPA)Frankfurt

European Securities and

Markets Authority (ESMA)

Paris

National Banking Supervisors

National Insurance and Pension Supervisors

National Securities Supervisors

European Systemic Risk Board (ESRB)

European System of Financial Supervisors (ESFS)

Information on micro-prudential developments

Recommendations and/or early risk warnings

Capital Requirements Directive 3

• CRD 3 – final text adopted on 11 October 2010

• Key features:

• remuneration principles

• trading book

• new stressed VaR and Incremental Risk Charge

• align capital charges for securitised products in the trading book with existing charges in the banking book

• securitisation

• higher capital charge for re-securitisations

• more disclosure of banks’ securitisation positions

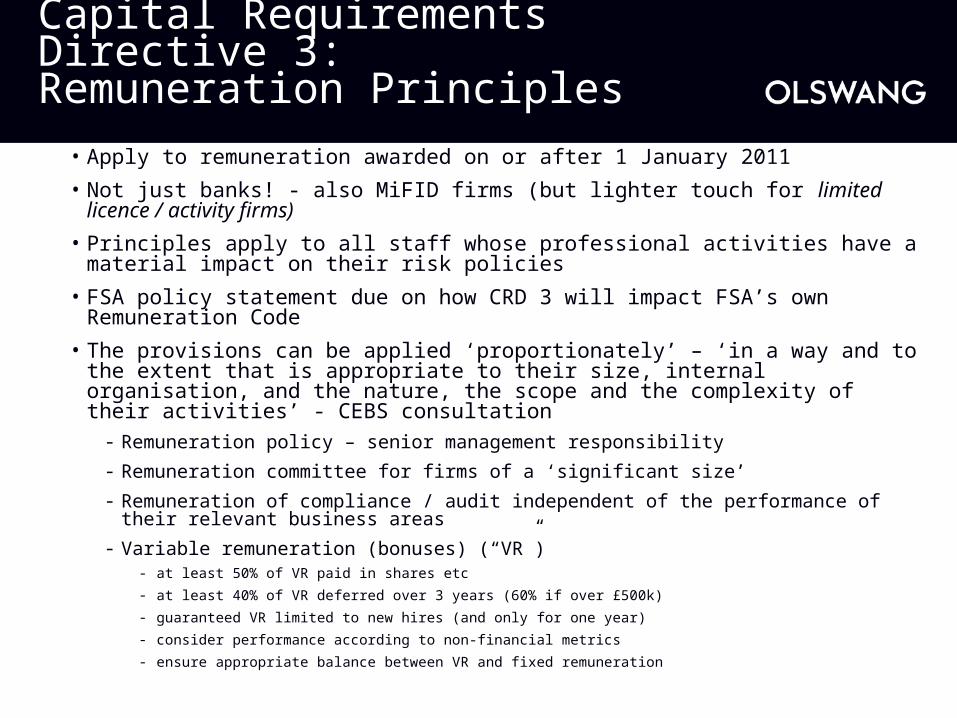

Capital Requirements Directive 3: Remuneration Principles• Apply to remuneration awarded on or after 1 January 2011

• Not just banks! - also MiFID firms (but lighter touch for limited licence / activity firms)

• Principles apply to all staff whose professional activities have a material impact on their risk policies

• FSA policy statement due on how CRD 3 will impact FSA’s own Remuneration Code

• The provisions can be applied ‘proportionately’ – ‘in a way and to the extent that is appropriate to their size, internal organisation, and the nature, the scope and the complexity of their activities’ - CEBS consultation

- Remuneration policy – senior management responsibility

- Remuneration committee for firms of a ‘significant size’

- Remuneration of compliance / audit independent of the performance of their relevant business areas

- Variable remuneration (bonuses) (“VR”)- at least 50% of VR paid in shares etc

- at least 40% of VR deferred over 3 years (60% if over £500k)

- guaranteed VR limited to new hires (and only for one year)

- consider performance according to non-financial metrics

- ensure appropriate balance between VR and fixed remuneration

The MiFID Review

• Review to look at the effectiveness of MiFID particularly in the context of market developments

• European Commission (“EC”) intends to report on possible changes to MiFID by April 2011

• EC requested technical advice from CESR on the following matters:

• Investor protection and intermediaries

- EEA regime for recording telephone conversations and electronic communications concerning orders received/transmitted

- Improved disclosure on execution quality – key metrics to be provided by ESMA

- Narrowing the scope of “non-complex instruments” for the Appropriateness Test, excl: shares in non-UCITS CIS and shares/bonds which embed a derivative

- Removing exemption from definition of investment advice for advice issued exclusively through distribution channels

The MiFID Review(continued)

• Equity markets

- Pre-trade transparency - review of pre-trade transparency waivers

- Changing the rules for systematic internalisers

- Post-trade transparency changes and a “consolidated tape”

• Transaction reporting

- Introduction of third trading capacity for “Riskless Principal” / collection of client and counterparty identifiers

• Post-trade transparency for non-equity markets

- Corporate bonds (where prospectus published) and CDS (which are eligible for CCP clearing) v asset backed commercial paper

• Derivatives and market infrastructure

- Mandatory CCP clearing for many OTC derivatives

- Interaction with AIFM directive

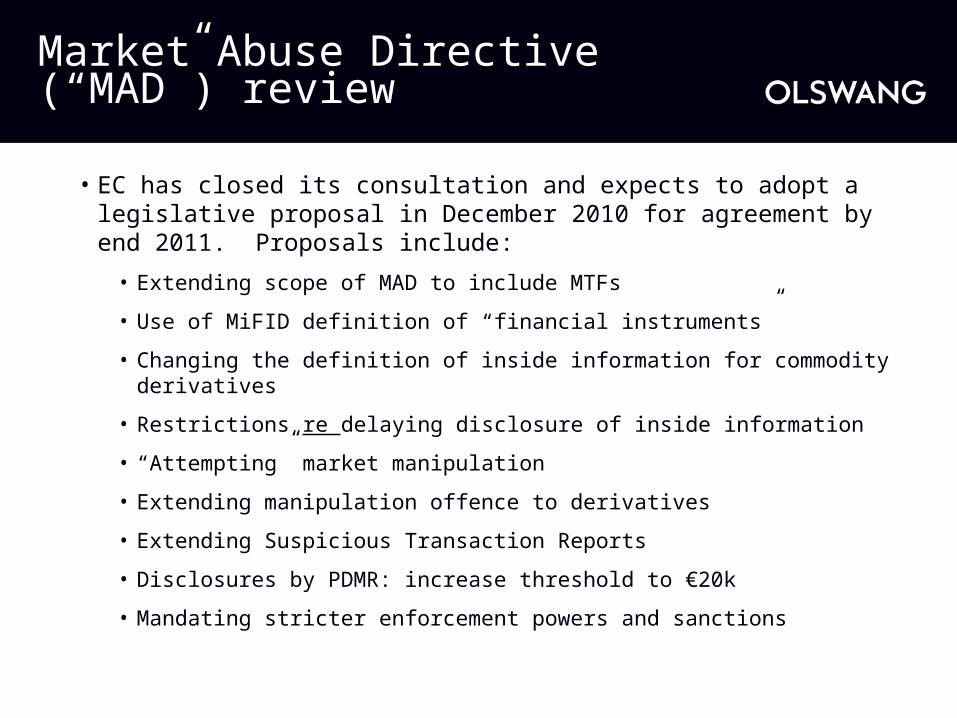

Market Abuse Directive (“MAD”) review

• EC has closed its consultation and expects to adopt a legislative proposal in December 2010 for agreement by end 2011. Proposals include:

• Extending scope of MAD to include MTFs

• Use of MiFID definition of “financial instruments”

• Changing the definition of inside information for commodity derivatives

• Restrictions re delaying disclosure of inside information

• “Attempting” market manipulation

• Extending manipulation offence to derivatives

• Extending Suspicious Transaction Reports

• Disclosures by PDMR: increase threshold to €20k

• Mandating stricter enforcement powers and sanctions

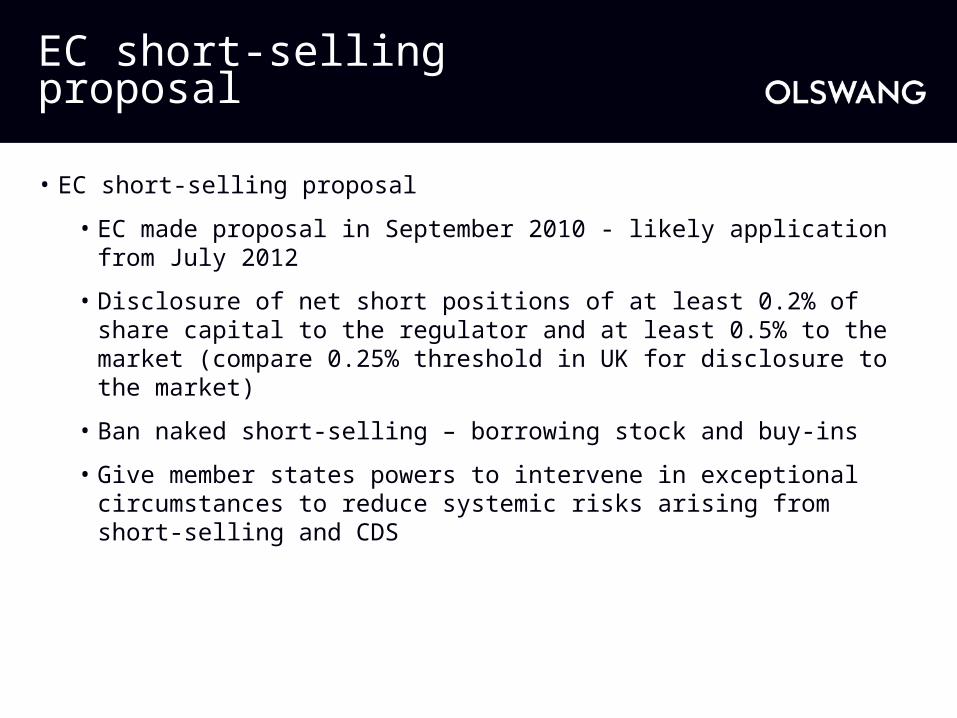

EC short-selling proposal

• EC short-selling proposal

• EC made proposal in September 2010 - likely application from July 2012

• Disclosure of net short positions of at least 0.2% of share capital to the regulator and at least 0.5% to the market (compare 0.25% threshold in UK for disclosure to the market)

• Ban naked short-selling – borrowing stock and buy-ins

• Give member states powers to intervene in exceptional circumstances to reduce systemic risks arising from short-selling and CDS

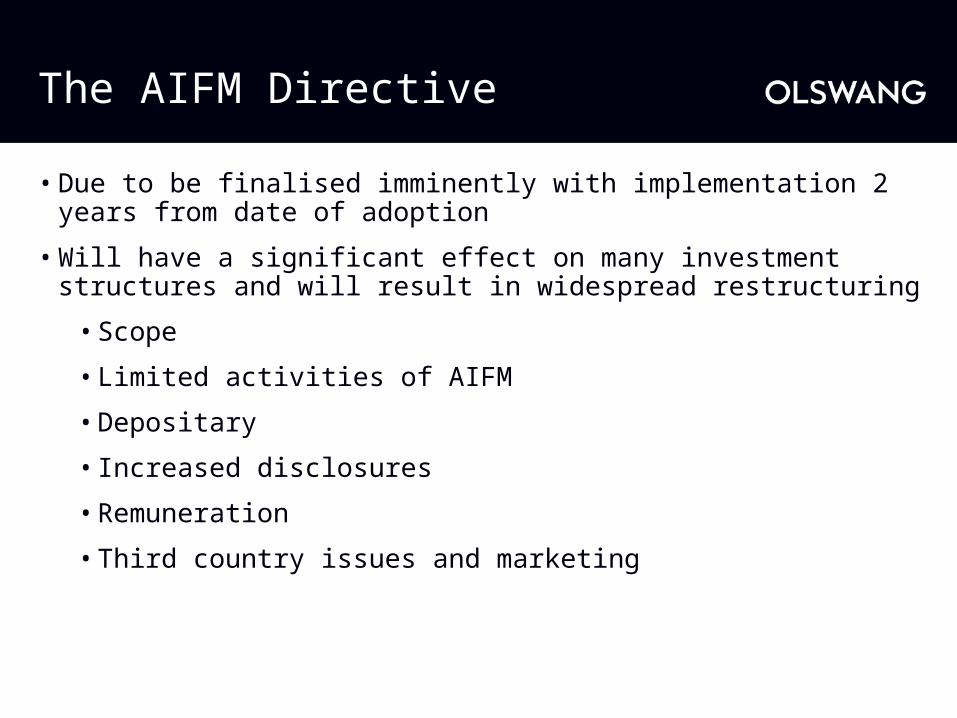

The AIFM Directive

• Due to be finalised imminently with implementation 2 years from date of adoption

• Will have a significant effect on many investment structures and will result in widespread restructuring

• Scope

• Limited activities of AIFM

• Depositary

• Increased disclosures

• Remuneration

• Third country issues and marketing

Key EU Developments in Financial Services Regulation

For more informationplease contact:

Brian McDonnell+44 207 067 [email protected]

4677034

Presentation to Members and Guests of CISIRegulatory convergence – reality or opportunity lost?Anthony Kirby, Gary Stanton

20 October 2010

Presentation to Members and Guests of CISI

Objectives of the session

Understand:► Drivers of the regulatory future agenda –

eg, G20 and Dodd Frank.

► Direct effect regulation vs. regulatory convergence?

► Key regulatory themes & impacts

19 April 2023 Presentation to Members and Guests of CISIPage 15

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISI

Background

Page 16

Presentation to Members and Guests of CISI

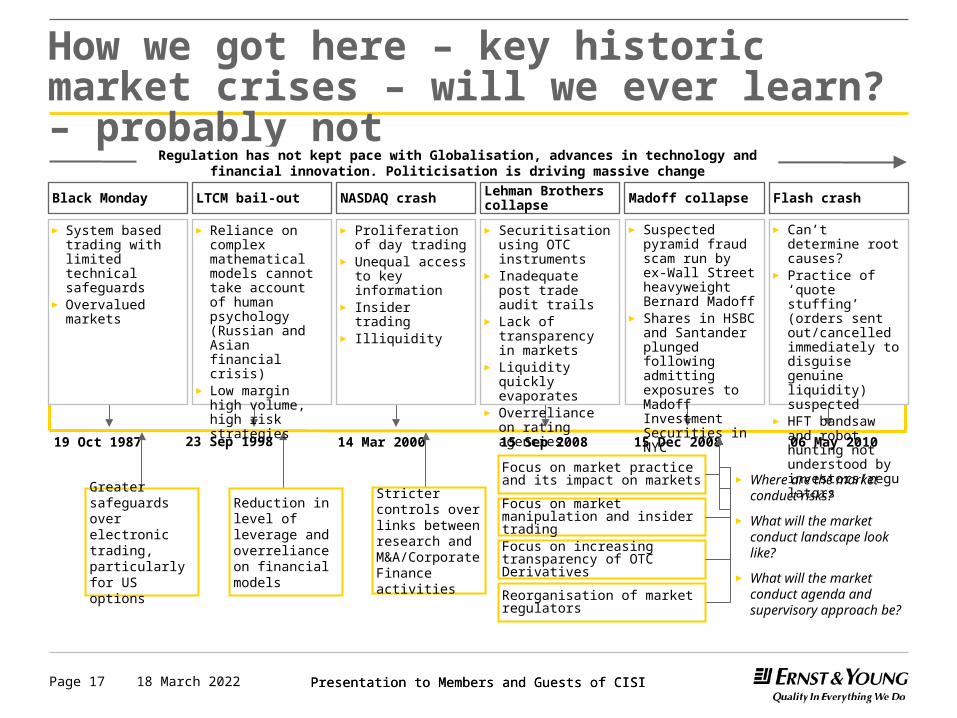

How we got here – key historic market crises – will we ever learn? – probably not

19 April 2023 Presentation to Members and Guests of CISIPage 17

► Where are the market conduct risks?

► What will the market conduct landscape look like?

► What will the market conduct agenda and supervisory approach be?

Black Monday LTCM bail-out NASDAQ crash Lehman Brothers collapse

19 Oct 1987 23 Sep 1998 14 Mar 2000 15 Sep 2008 15 Dec 2008

Greater safeguards over electronic trading, particularly for US options

Reduction in level of leverage and overreliance on financial models

Focus on market practice and its impact on markets

Focus on market manipulation and insider trading

06 May 2010

Flash crashMadoff collapse

Focus on increasing transparency of OTC Derivatives

► System based trading with limited technical safeguards

► Overvalued markets

► Reliance on complex mathematical models cannot take account of human psychology (Russian and Asian financial crisis)

► Low margin high volume, high risk strategies

► Proliferation of day trading

► Unequal access to key information

► Insider trading► Illiquidity

► Securitisation using OTC instruments

► Inadequate post trade audit trails

► Lack of transparency in markets

► Liquidity quickly evaporates

► Overreliance on rating agencies

Regulation has not kept pace with Globalisation, advances in technology and financial innovation. Politicisation is driving massive change

Stricter controls over links between research and M&A/Corporate Finance activities

Reorganisation of market regulators

► Suspected pyramid fraud scam run by ex-Wall Street heavyweight Bernard Madoff

► Shares in HSBC and Santander plunged following admitting exposures to Madoff Investment Securities in NYC

► Can’t determine root causes?

► Practice of ‘quote stuffing’ (orders sent out/cancelled immediately to disguise genuine liquidity) suspected

► HFT bandsaw and robot hunting not understood by investors/regulators

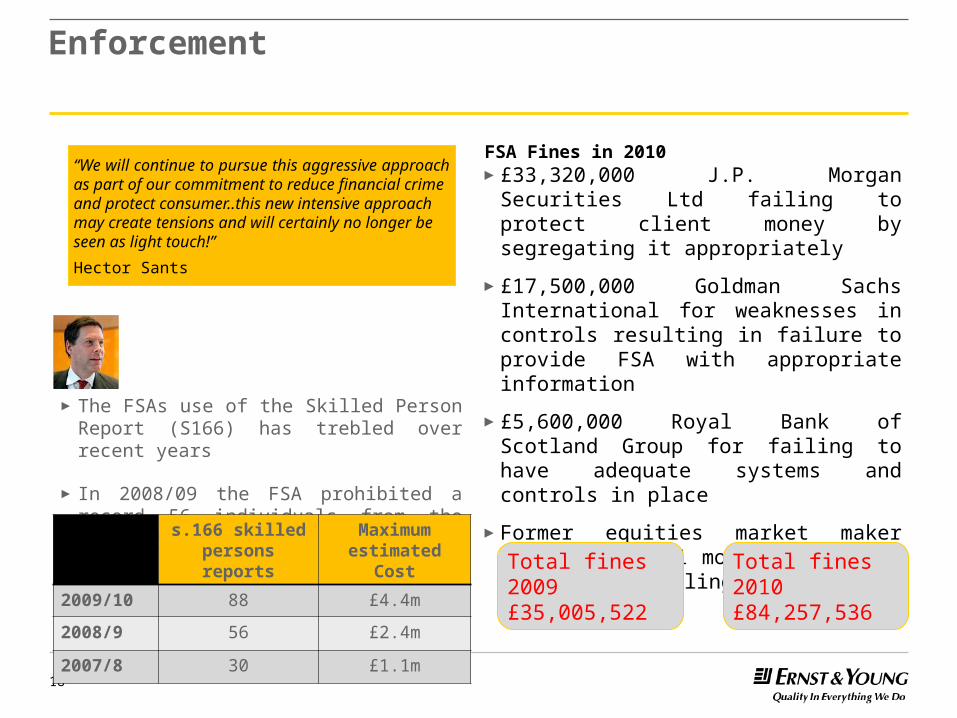

Enforcement

FSA Fines in 2010►£33,320,000 J.P. Morgan Securities Ltd

failing to protect client money by segregating it appropriately

►£17,500,000 Goldman Sachs International for weaknesses in controls resulting in failure to provide FSA with appropriate information

►£5,600,000 Royal Bank of Scotland Group for failing to have adequate systems and controls in place

►Former equities market maker sentenced to 21 months in prison for insider dealing

18

“We will continue to pursue this aggressive approach as part of our commitment to reduce financial crime and protect consumer..this new intensive approach may create tensions and will certainly no longer be seen as light touch!”

Hector Sants

► The FSAs use of the Skilled Person Report (S166) has trebled over recent years

► In 2008/09 the FSA prohibited a record 56 individuals from the industry

s.166 skilled persons reports

Maximum estimated Cost

2009/10 88 £4.4m

2008/9 56 £2.4m

2007/8 30 £1.1m

Total fines 2010 £84,257,536

Total fines 2009 £35,005,522

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 19

Market regulation reform drivers

Presentation to Members and Guests of CISI

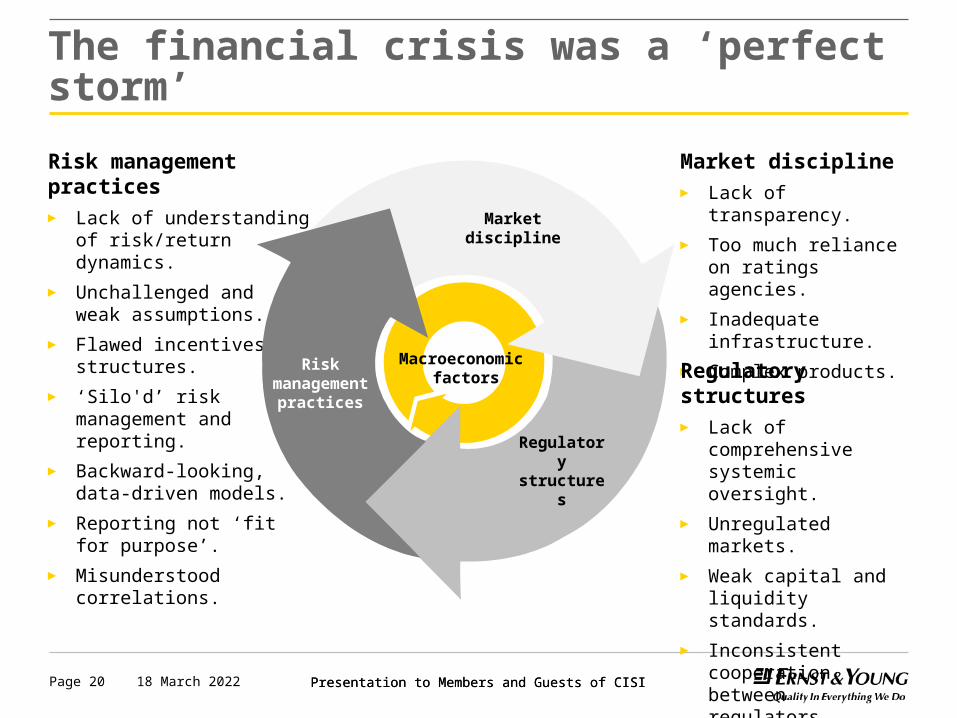

The financial crisis was a ‘perfect storm’

19 April 2023 Presentation to Members and Guests of CISIPage 20

Risk management practices► Lack of understanding of

risk/return dynamics.

► Unchallenged and weak assumptions.

► Flawed incentives structures.

► ‘Silo'd’ risk management and reporting.

► Backward-looking, data-driven models.

► Reporting not ‘fit for purpose’.

► Misunderstood correlations.

Market discipline► Lack of transparency.

► Too much reliance on ratings agencies.

► Inadequate infrastructure.

► Complex products.

Regulatory structures► Lack of comprehensive

systemic oversight.

► Unregulated markets.

► Weak capital and liquidity standards.

► Inconsistent cooperation between regulators.

Market discipline

Regulatory structures

Risk management

practices

Macroeconomic factors

Presentation to Members and Guests of CISI

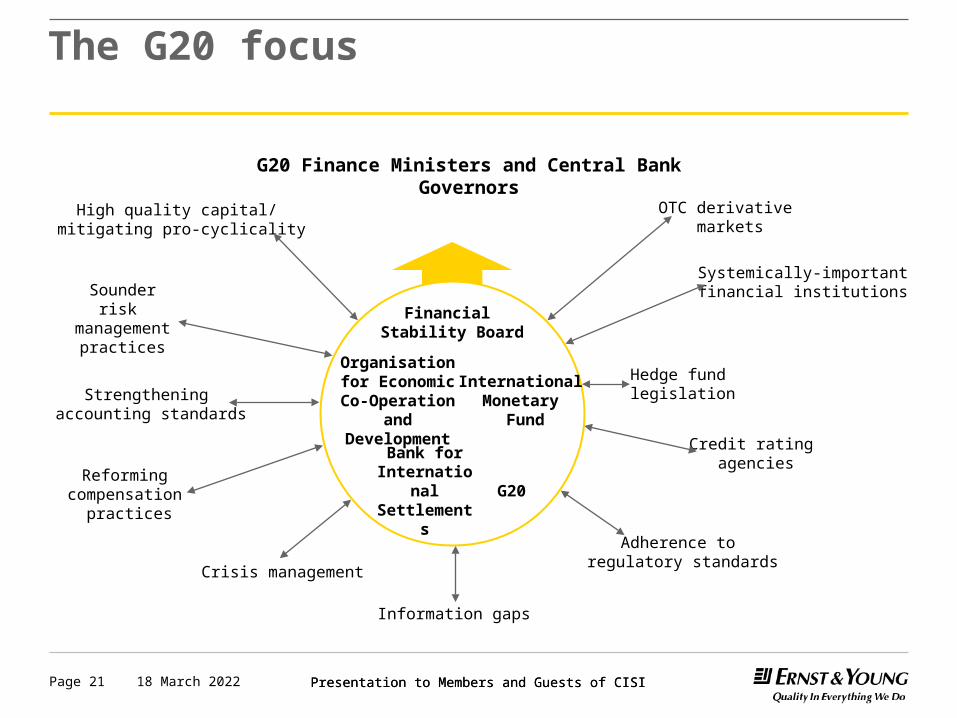

The G20 focus

19 April 2023 Presentation to Members and Guests of CISIPage 21

G20 Finance Ministers and Central Bank Governors

High quality capital/ mitigating pro-cyclicality

Sounder risk management

practices

Reforming compensation

practices

Crisis management

Strengthening accounting standards

Credit rating agencies

Hedge fund legislation

OTC derivative markets

Systemically-importantfinancial institutions

Adherence to regulatory standards

Information gaps

International Monetary

Fund

Organisation for Economic Co-Operation and Development

Bank for International Settlements

Financial Stability Board

G20

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 22

Wall Street Reform and Consumer Protection Act 2010

Reforming compensation

practices/ Clawback

Private Fund Advisor

Registration

Strengthening accounting standards

Credit rating agencies

Living Wills

OTC Derivatives markets

Systemic Regulations

Proprietary Trading and PE/ Hedge

Fund Investing

Overview of the Dodd-Frank Act

Consumer/ Investor

Protection

Capital/ Liquidity Planning

Securitisation and Loan Data

Collection

USReform

Specifications

Presentation to Members and Guests of CISI

Change of powers with the new European competent authorities

► New European bodies EBA, ESMA and EIOPA in evidence from January 2011

► The European Union's new financial regulators will wield greater power than first proposed or appeared likely just months ago, policymakers confirmed yesterday evening, in one of the rare instances when an EU integration project is strengthened rather than watered down.

► The European Union's new financial regulators will wield greater power than first proposed or appeared likely just months ago, policymakers confirmed yesterday evening.

► Negotiators from the European Parliament and the council of member countries said they have settled on a package of legislation that gives central regulatory bodies the power to overrule national authorities on points of EU law and issue binding orders to banks, insurers or securities firms.

► The lawmakers tightened a safeguard clause that had been conceived as a government veto over decisions touching on public funds. The authorities will gain some product-banning powers as well, going beyond the European Commission proposal or the recommendations it was based on, from an advisory group led by Jacques de Larosière.

► Internal-market commissioner Michel Barnier hailed the agreement as meeting his priority of ensuring ‘the credibility for the new European authorities and the European Systemic Risk Board (ESRB).’

► ‘The authorities will have real power,’ said Barnier at the news conference, after sitting in on the final round of talks.

19 April 2023 Presentation to Members and Guests of CISIPage 23

Presentation to Members and Guests of CISI

Update on regulatory developments in the UK

► In a July consultation paper, HM Treasury addressed the reform of the UK regulatory framework following the changes proposed by the new UK coalition government.

► In particular, the consultation paper discussed a revised tripartite model including three supervisory authorities: the Macro Prudential Regulation Authority (MPRA), the Prudential Regulation Authority (PRA), a supervisory authority in charge of the prudential regulation of individual firms, and the Consumer Protection and Markets Authority (CPMA), an authority responsible for consumer protection and the conduct of financial markets.

► Within the MPRA, the government proposed to include a Financial Policy Committee (FPC) under the authority of the Bank of England. The FPC would be responsible for maintaining financial stability by monitoring and addressing systemic or aggregate risks and vulnerabilities that threaten the financial sector as a whole.

► The PRA would have the responsibility of identifying risks and vulnerabilities to which the financial system is exposed and taking corrective actions to protect the broader economy.

► Finally, the CPMA will focus on consumer protection, promotion of integrity and efficiency in financial markets and regulating the conduct of participants in wholesale markets and market infrastructures such as investment exchanges.

19 April 2023 Presentation to Members and Guests of CISIPage 24

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 25

Regulatory convergence

Presentation to Members and Guests of CISI

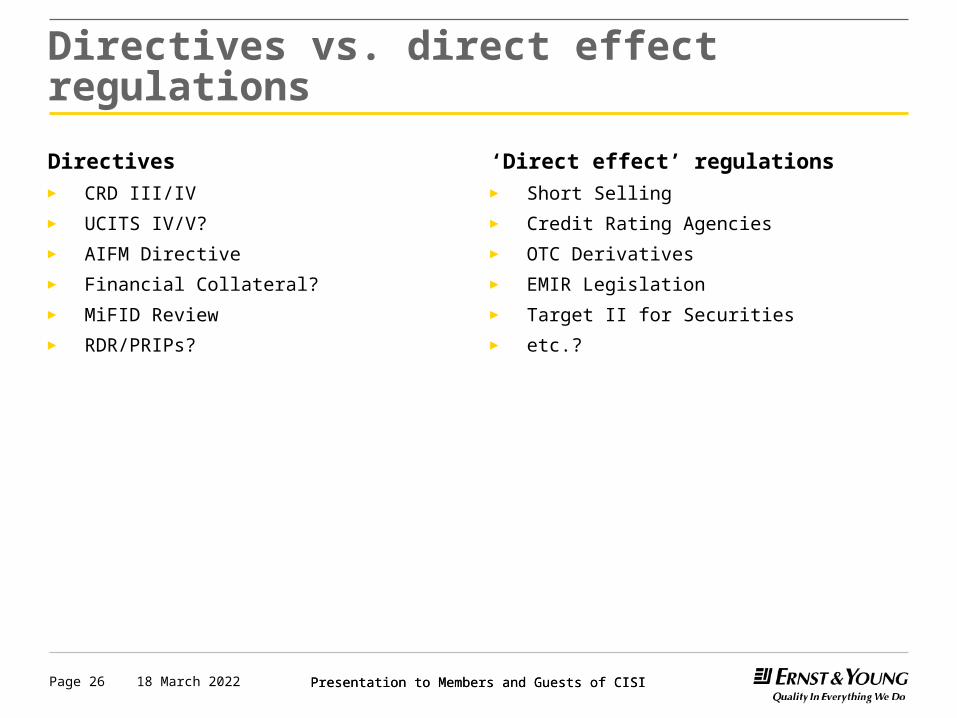

Directives vs. direct effect regulations

Directives► CRD III/IV

► UCITS IV/V?

► AIFM Directive

► Financial Collateral?

► MiFID Review

► RDR/PRIPs?

19 April 2023 Presentation to Members and Guests of CISIPage 26

‘Direct effect’ regulations► Short Selling

► Credit Rating Agencies

► OTC Derivatives

► EMIR Legislation

► Target II for Securities

► etc.?

Presentation to Members and Guests of CISI

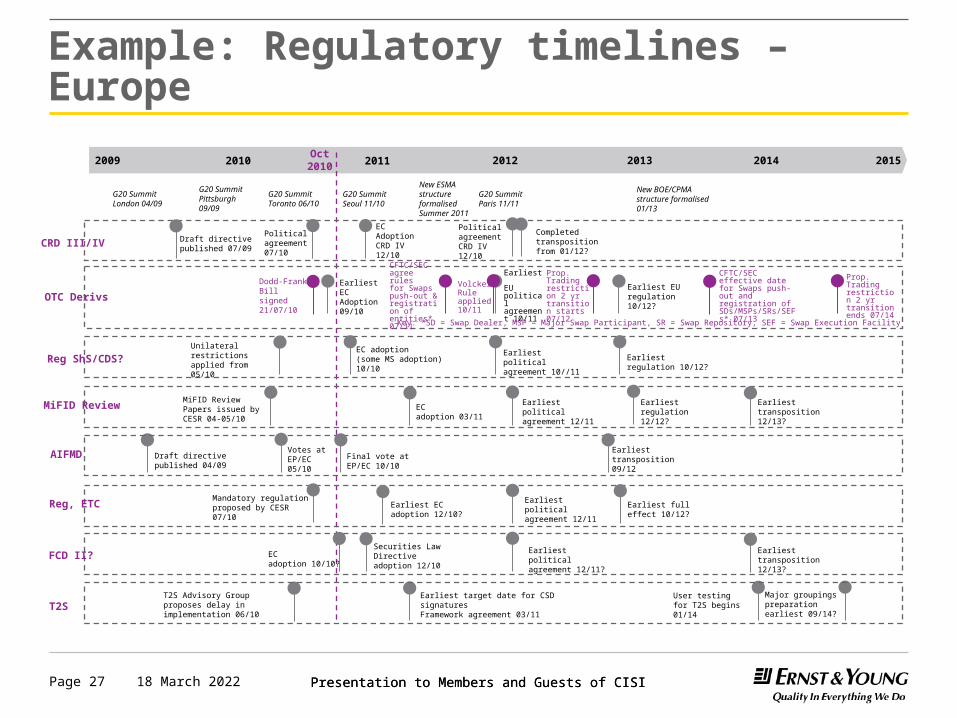

Example: Regulatory timelines – Europe

19 April 2023 Presentation to Members and Guests of CISIPage 27

2009 2012 2013 2014 2015Oct2010 20112010

CRD III/IV

OTC Derivs

EarliestEC Adoption 09/10

Earliest EU political agreement 10/11

Earliest EUregulation 10/12?

Dodd-Frank Bill signed 21/07/10

Political agreement 07/10

Completedtransposition from 01/12?

Draft directive published 07/09

New BOE/CPMA structure formalised 01/13

New ESMA structure formalised Summer 2011

Reg ShS/CDS? EC adoption(some MS adoption) 10/10

Earliest political agreement 10//11

Earliest regulation 10/12?

Unilateral restrictions applied from 05/10

ECAdoption CRD IV 12/10

Political agreement CRD IV 12/10

MiFID Review ECadoption 03/11

Earliest political agreement 12/11

Earliesttransposition 12/13?

MiFID Review Papers issued by CESR 04-05/10

Earliest regulation 12/12?

Reg, ETC Earliest ECadoption 12/10?

Earliest fulleffect 10/12?

Mandatory regulation proposed by CESR 07/10

Earliest political agreement 12/11

Draft directive published 04/09

Final vote at EP/EC 10/10

Earliest transposition 09/12

Votes at EP/EC 05/10

AIFMD

G20 Summit London 04/09

G20 Summit Toronto 06/10

G20 Summit Seoul 11/10

G20 Summit Paris 11/11

G20 Summit Pittsburgh 09/09

FCD II? ECadoption 10/10?

Earliest political agreement 12/11?

Earliesttransposition 12/13?

Securities Law Directiveadoption 12/10

T2SMajor groupings preparation earliest 09/14?

T2S Advisory Group proposes delay in implementation 06/10

Earliest target date for CSD signaturesFramework agreement 03/11

User testing for T2S begins 01/14

CFTC/SEC effective date for Swaps push-out and registration of SDs/MSPs/SRs/SEFs* 07/13

Prop. Trading restriction 2 yr transition ends 07/14

Key: *SD = Swap Dealer, MSP = Major Swap Participant, SR = Swap Repository, SEF = Swap Execution Facility

CFTC/SEC agree rules for Swaps push-out & registration of entities* 07/11

Volcker Rule applied10/11

Prop. Trading restriction 2 yr transition starts 07/12

Presentation to Members and Guests of CISI

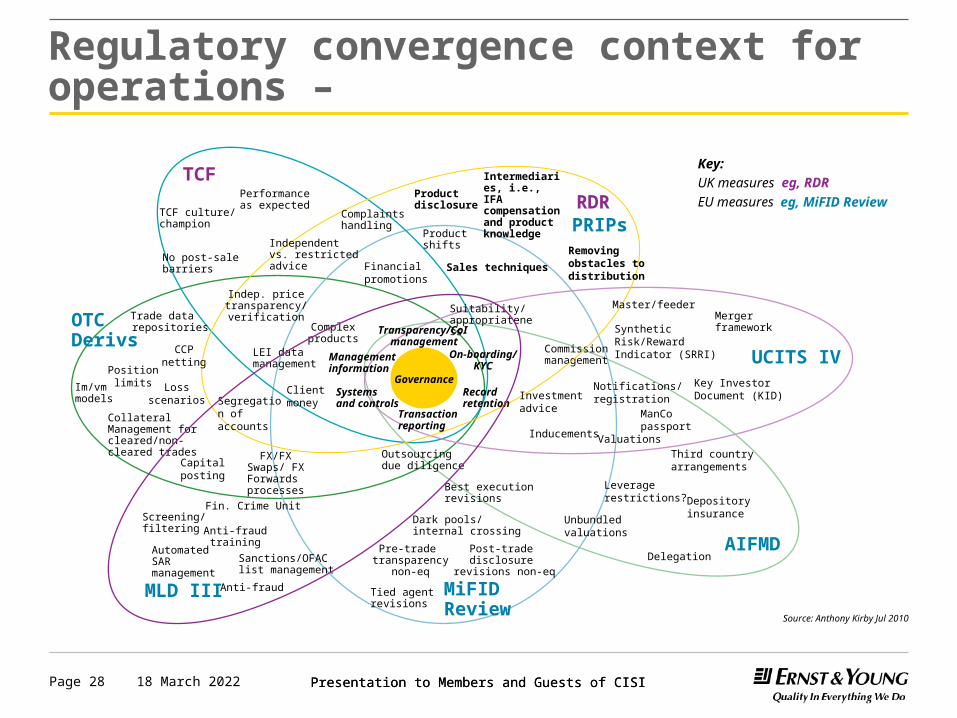

Regulatory convergence context for operations –

19 April 2023 Presentation to Members and Guests of CISIPage 28

AIFMD

OTC Derivs

CollateralManagement forcleared/non-cleared trades

MiFID Review

Commissionmanagement

TCF

FX/FX Swaps/ FX Forwards

processes

AutomatedSARmanagement

UCITS IV

Sanctions/OFAClist management

Screening/filtering

ManCo passport

Valuations

Merger framework

Key Investor Document (KID)

Financial promotions

Inducements

Clientmoney

RDR

Indep. pricetransparency/

verification

Best executionrevisions

Investment advice

LEI data management

MLD III Anti-fraud

Fin. Crime Unit

Anti-fraud training

Master/feeder

Notifications/ registration

Depository insurance

Capital posting

Unbundled valuations

Third country arrangements

Leverage restrictions?

Post-trade disclosure

revisions non-eq

Pre-trade transparency

non-eq

Dark pools/ internal crossing

Outsourcing due diligence

Complex products

Independent vs. restrictedadvice

Productshifts

TCF culture/ champion

Performance as expected

No post-sale barriers

Complaints handling

Synthetic Risk/Reward Indicator (SRRI)

Transparency/CoI management

Record retention

Systems and controls

Transactionreporting

On-boarding/ KYC

Managementinformation

Source: Anthony Kirby Jul 2010

Key:

UK measures

EU measures

eg, RDR

eg, MiFID Review

Trade data repositories

Im/vm models Segregation

of accounts

Position limits Loss

scenarios

Tied agentrevisions

Suitability/ appropriateness

CCP netting

PRIPs

Intermediaries, i.e., IFA compensation and product knowledge

Product disclosure

Removing obstacles to distribution

Sales techniques

Delegation

Governance

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 29

Key convergence themes

Presentation to Members and Guests of CISI

Governance, risk and remuneration

► Politicians and regulators have realised that all three are closely linked.

► G20, Walker, Turner, Basel, Fed, FSA and other major regulators (Germany).

► Focus on role of Senior Management in risk oversight.

► For groups right down to the legal entity view

► Link to recovery and resolution plans, challenge for most organisations, but particularly those operating in multiple overseas jurisdictions.

19 April 2023 Presentation to Members and Guests of CISIPage 30

► Need for Board engagement with risk agenda and risk appetite.

► Regulatory pressure on risk function independence.

► Legacy systems and old assumptions not able to deal with new Risk MI requirements.

► The need for an enterprise wide view of risk.

► Evolving regulations on Risk-aligned remuneration.

Presentation to Members and Guests of CISI

Management information

► Governance agenda inextricably linked to MI.

► Line of site of risks by Group Senior management down to entity level is a challenge, materiality.

► Can risk appetite be split below division.

► Requires more sophisticated MI, and in some cases technology support.

► Regulators interested in whether your systems can pump out the data needed.

19 April 2023 Presentation to Members and Guests of CISIPage 31

► More data means more work to analyse and understand.

► More Senior Management time on controlling the business and away from revenue producing aspects of the business.

► NEDS under pressure to provide challenge and will need more time and information to do this.

Presentation to Members and Guests of CISI

Recovery and resolution plans

► G20 commitment for recovery and resolution plans (RRPs).

► Mandated by G20, so far UK and US main adopters, others may follow.

► The need to articulate and mitigate systemic risks.

► Maintenance of contingency plans in BAU.

► Depositor protection scheme strengthening with impacts on operations and compliance.

19 April 2023 Presentation to Members and Guests of CISIPage 32

► Mapping business structure, intergroup funding, product and operating models with the legal entity structure.

► Potential for extra capital and liquidity buffers for systemic firms.

► Potential forced restructuring if obstacles to resolution without taxpayer bailout are too great – but limited European appetite.

► Potential increased capital and liquidity requirements as supervisory response to inadequate plans.

► Credible Living Will contingency plans are seen by some firms as possible defensive measure against forced re-structuring.

► Likely encouragement of contingent convertible debt and creditor haircuts/’bail-ins’.

► Single customer view for deposit guarantee schemes.

Presentation to Members and Guests of CISI

Consumer agenda

► Politicians and regulators need to ensure better protection for consumers including from the impacts of the economic downturn

► Fair lending practices

► Greater transparency.

19 April 2023 Presentation to Members and Guests of CISIPage 33

► UK RDR.

► Fairness and transparency of bank charges under review by regulators.

► Regulatory pressure to improve sales advice.

► New distribution requirements, commission pressure.

Presentation to Members and Guests of CISI

Basel III

19 April 2023 Presentation to Members and Guests of CISIPage 34

Basel III – focusing on changing quality and quantity of bank capital► Hybrid capital increased confidence effects► Subordinated debt – was debt► Equity capital not high enough

► But multiple buffers will add to complexity► Too much capital will drive disintermediation► Increase cost for industry

Minimum capital

Requirement for systemically

important firms?

Booms recessions

Additional requirement for markets over heating

Capital conservation buffer – stops profit being distributed

4%

5%

7%

9%

Indi

cativ

e

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 35

Markets regulatory agenda

Presentation to Members and Guests of CISI

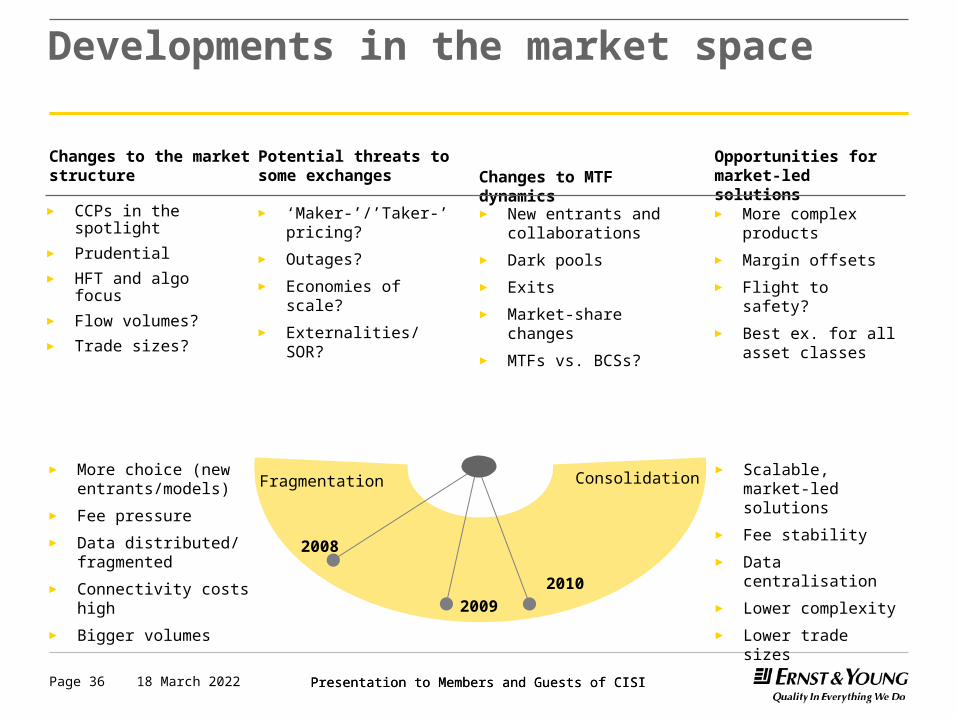

Developments in the market space

19 April 2023 Presentation to Members and Guests of CISIPage 36

► More choice (new entrants/models)

► Fee pressure

► Data distributed/ fragmented

► Connectivity costs high

► Bigger volumes

► Scalable, market-led solutions

► Fee stability

► Data centralisation

► Lower complexity

► Lower trade sizes

Changes to the market structure

Potential threats to some exchanges Changes to MTF dynamics

Opportunities for market-led solutions

Fragmentation Consolidation

2010

2008

2009

► CCPs in the spotlight

► Prudential

► HFT and algo focus

► Flow volumes?

► Trade sizes?

► New entrants and collaborations

► Dark pools

► Exits

► Market-share changes

► MTFs vs. BCSs?

► More complex products

► Margin offsets

► Flight to safety?

► Best ex. for all asset classes

► ‘Maker-’/’Taker-’ pricing?

► Outages?

► Economies of scale?

► Externalities/SOR?

Presentation to Members and Guests of CISI

MiFID Review CESR 10-802 equities

Pre-trade transparency regime for RMs/MTFs:

Data from the fact-finding shows that more than 90 percent of trading on organised markets in Europe is pre-trade transparent.

CESR seeks to move from a ‘principle based approach’ to waivers from pre-trade transparency to an approach that is more ‘rule based’.

CESR recommends the Commission undertake further analytical work based on empirical data to determine whether the existing large-in-scale (LIS) thresholds should be revised.

CESR continues to work on appropriate clarifications which may be included in binding technical standards at a later stage.

CESR recommends that MiFID be amended to clarify that actionable indications of interest (IOIs) are considered to be orders and as such subject to pre-trade transparency requirements.

Application of transparency obligations to equity-like instruments:

CESR recommends to enhance the scope of the MiFID transparency regime by applying transparency obligations to equity-like instruments admitted to trading on an RM, including depository receipts, exchange-traded funds and ‘certificates’ as defined in CESR’s advice.

These instruments are considered to be equity-like, since they are traded like shares and, from an economic point of view, equivalent to shares.

19 April 2023 Presentation to Members and Guests of CISIPage 37

Presentation to Members and Guests of CISI

MiFID Review CESR 10-802 equities (cont’d)

Post-trade transparency regime:

CESR recommends retaining the current framework for post-trade transparency but to introduce formal measures to improve the quality of post-trade data, shorten delays for regular and deferred publication and reduce the complexity of the regime.

As a supplement to the introduction of new standards on data quality and guidelines on trade publication, CESR recommends requiring investment firms to publish their trades through Approved Publication Arrangements (APAs). All APAs would be required to operate data publication arrangements to prescribed standards.

Regulatory boundaries and requirements:

As regards broker crossing systems (BCSs), CESR recommends that a new regulatory regime with tailored additional obligations be introduced for investment firms operating such systems.

This would include: notification by investments firms that they operate a BCS, publication of a list of BCSs, a requirement for a generic BCS identifier in post-trade transparency information, publication of aggregate trade information at the level of each BCS at the end of the day, and identification of BCSs in transaction reports.

CESR recommends to impose a limit on the amount of business that can be executed by BCSs before they are required to become an MTF.

19 April 2023 Presentation to Members and Guests of CISIPage 38

Presentation to Members and Guests of CISI

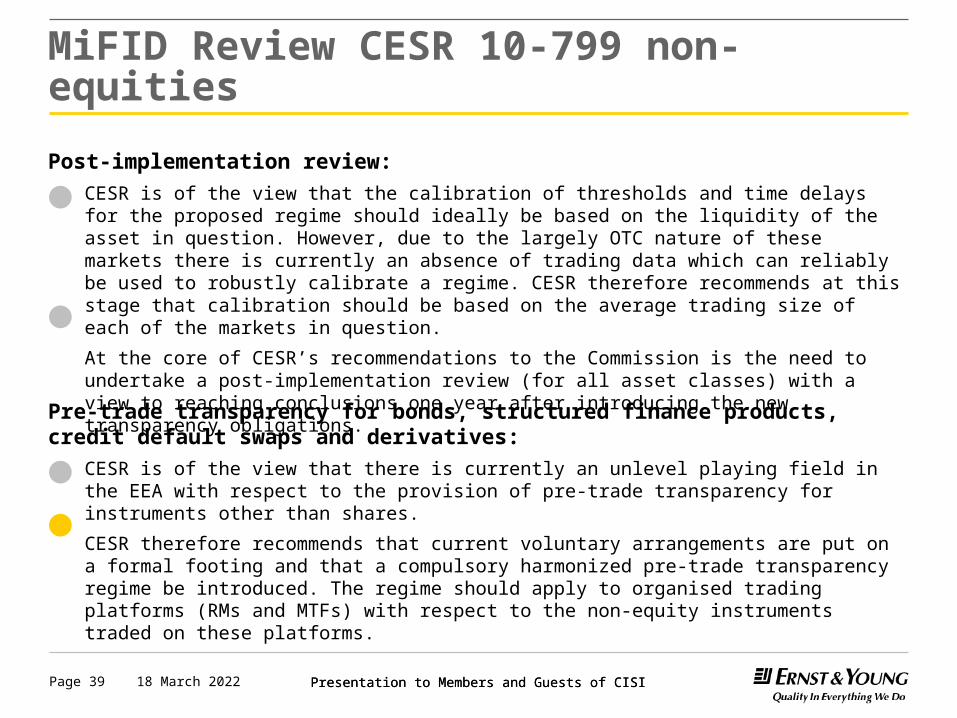

MiFID Review CESR 10-799 non-equities

Post-implementation review:

CESR is of the view that the calibration of thresholds and time delays for the proposed regime should ideally be based on the liquidity of the asset in question. However, due to the largely OTC nature of these markets there is currently an absence of trading data which can reliably be used to robustly calibrate a regime. CESR therefore recommends at this stage that calibration should be based on the average trading size of each of the markets in question.

At the core of CESR’s recommendations to the Commission is the need to undertake a post-implementation review (for all asset classes) with a view to reaching conclusions one year after introducing the new transparency obligations.

19 April 2023 Presentation to Members and Guests of CISIPage 39

Pre-trade transparency for bonds, structured finance products, credit default swaps and derivatives:

CESR is of the view that there is currently an unlevel playing field in the EEA with respect to the provision of pre-trade transparency for instruments other than shares.

CESR therefore recommends that current voluntary arrangements are put on a formal footing and that a compulsory harmonized pre-trade transparency regime be introduced. The regime should apply to organised trading platforms (RMs and MTFs) with respect to the non-equity instruments traded on these platforms.

Presentation to Members and Guests of CISI

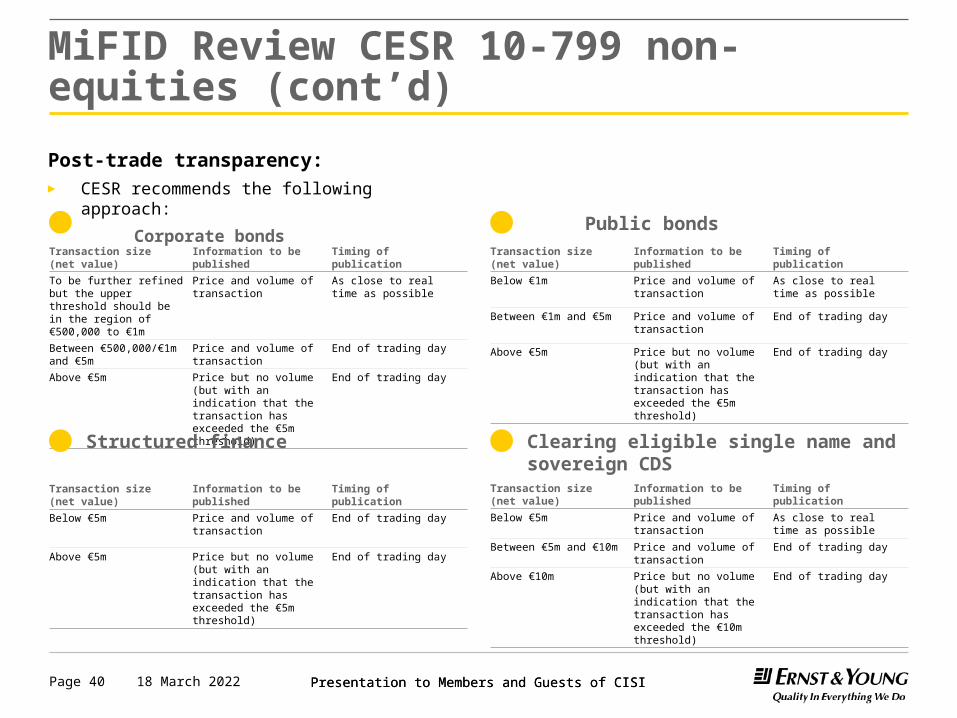

MiFID Review CESR 10-799 non-equities (cont’d)

Post-trade transparency:► CESR recommends the following approach:

Corporate bonds

19 April 2023 Presentation to Members and Guests of CISIPage 40

Transaction size (net value)

Information to be published Timing of publication

To be further refined but the upper threshold should be in the region of €500,000 to €1m

Price and volume of transaction

As close to real time as possible

Between €500,000/€1m and €5m

Price and volume of transaction

End of trading day

Above €5m Price but no volume (but with an indication that the transaction has exceeded the €5m threshold)

End of trading day

Public bondsTransaction size (net value)

Information to be published Timing of publication

Below €1m Price and volume of transaction

As close to real time as possible

Between €1m and €5m Price and volume of transaction

End of trading day

Above €5m Price but no volume (but with an indication that the transaction has exceeded the €5m threshold)

End of trading day

Structured finance

Transaction size (net value)

Information to be published Timing of publication

Below €5m Price and volume of transaction

End of trading day

Above €5m Price but no volume (but with an indication that the transaction has exceeded the €5m threshold)

End of trading day

Clearing eligible single name and sovereign CDSTransaction size (net value)

Information to be published Timing of publication

Below €5m Price and volume of transaction

As close to real time as possible

Between €5m and €10m Price and volume of transaction

End of trading day

Above €10m Price but no volume (but with an indication that the transaction has exceeded the €10m threshold)

End of trading day

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 41

Key impacts

Presentation to Members and Guests of CISI

Summary and conclusions

► Changing Global, European and UK regulatory architecture.

► Wider regulatory scope.

► More intense political challenge of regulatory bodies.

► More intrusive supervision and a more enforcement activity.

19 April 2023 Presentation to Members and Guests of CISIPage 42

► Big focus on firms of systemic importance.

► Higher capital and liquidity requirements.

► A lot more on corporate governance.

► Higher expectations and greater accountability for Senior Management.

Presentation to Members and Guests of CISI19 April 2023 Presentation to Members and Guests of CISIPage 43

Contacts

Dr Anthony W KirbyDirector

Direct Tel: +44 (0)20 7951 9729Mobile: +44 (0)77 9654 8317Email: [email protected]

Gary Stanton, Chartered FCISI Senior Manager

Direct Tel: +44 (0)20 7951 8387Mobile: +44 (0)77 8073 7737Email: [email protected]

Thank youInformation in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.

Chartered Institute for Securities & Investment

COMPLIANCE PROFESSIONALS

SUMMIT 2010

20 October 2010

RDRissues on the ground

Simon MorrisCISI20 October 2010

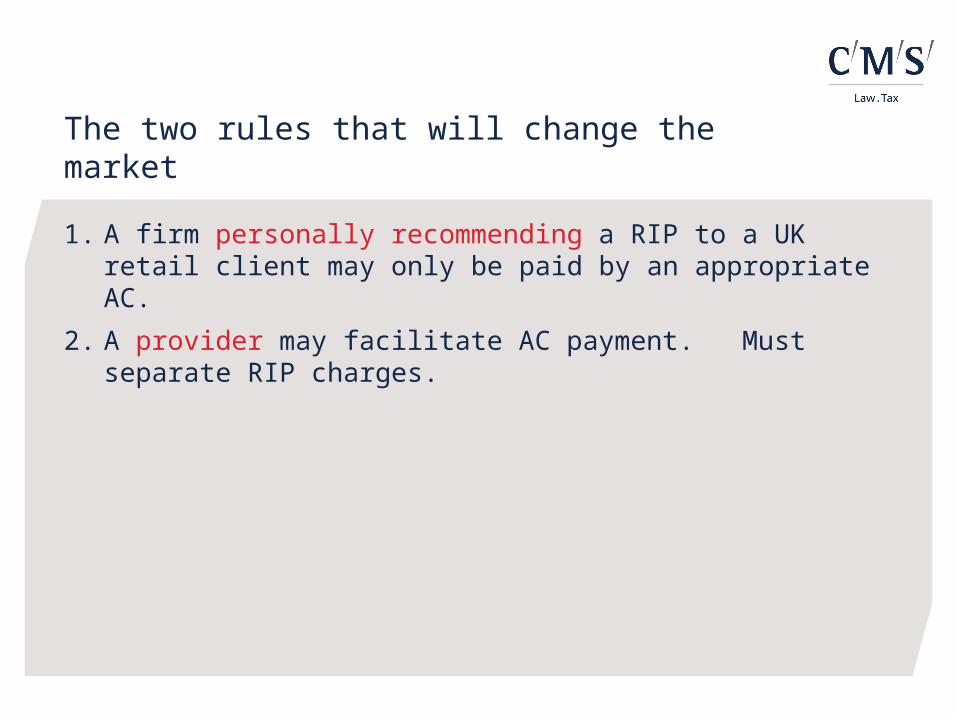

The two rules that will change the market

1. A firm personally recommending a RIP to a UK retail client may only be paid by an appropriate AC.

2. A provider may facilitate AC payment. Must separate RIP charges.

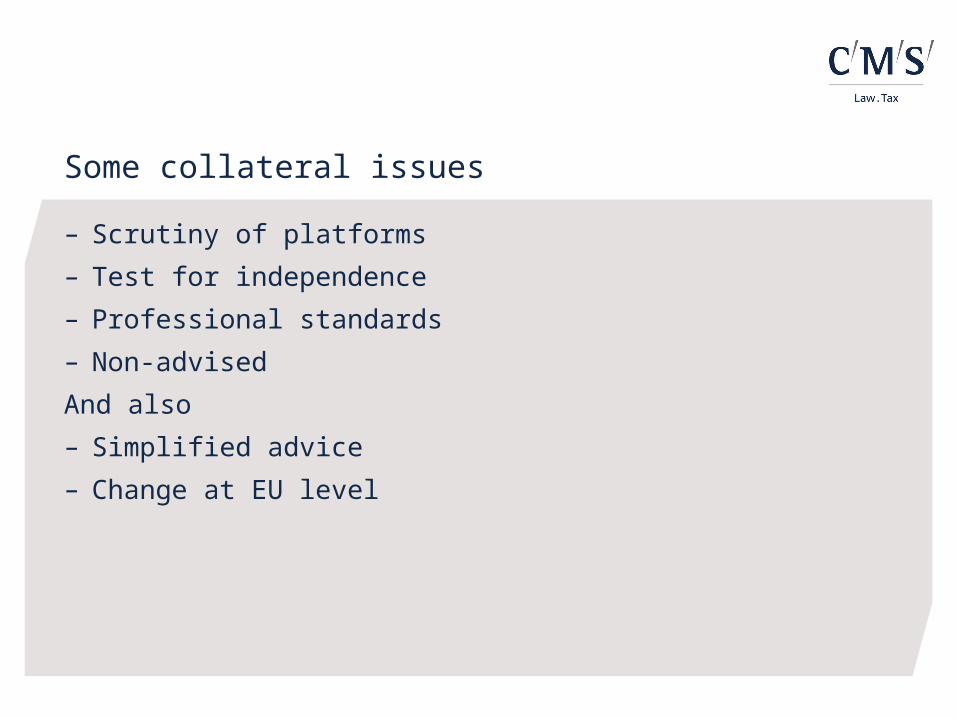

Some collateral issues

– Scrutiny of platforms

– Test for independence

– Professional standards

– Non-advised

And also

– Simplified advice

– Change at EU level

And in consequence …

– Improvement in advice

– Availability of advice

– Winners

• Wealth managers

• Bancassurers

– Losers

• Low distribution providers

• IFA-reliant providers

• Smaller IFAs & networks

THE FUTURE SHAPE OF THE RDR: PREPARING FOR JANUARY 2013

Allan Dampier

CISI Compliance Professionals SummitLondon, October 2010

RDR Preparation

AdviserService

Preparation & Implementation

ProfessionalismAdviser

Charging

December

2012

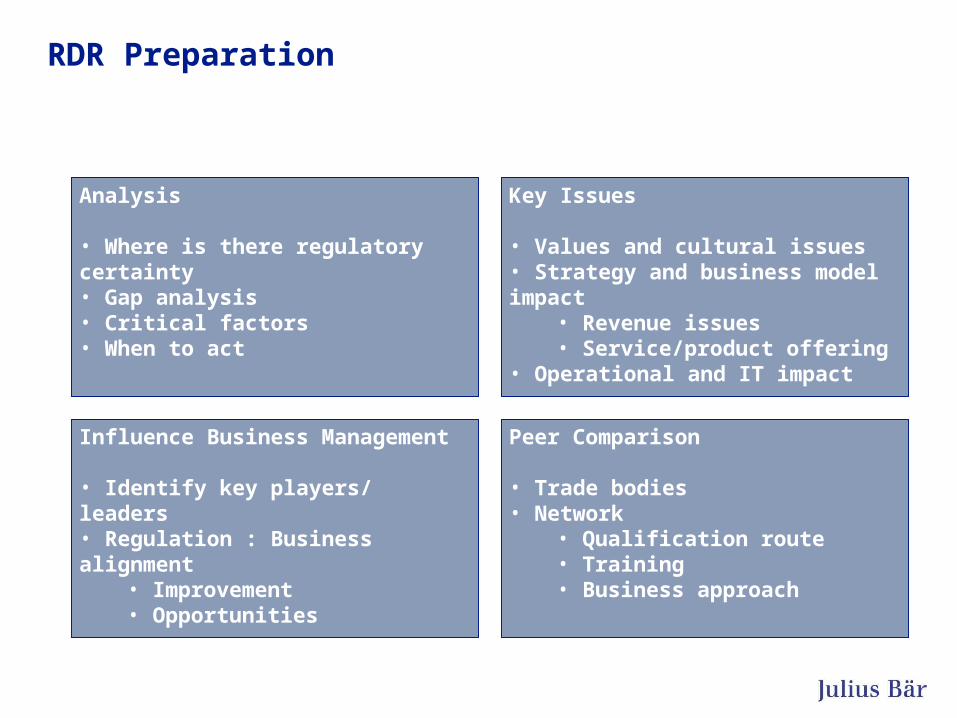

RDR Preparation

Analysis

• Where is there regulatory certainty• Gap analysis• Critical factors• When to act

Key Issues

• Values and cultural issues• Strategy and business model impact

• Revenue issues• Service/product offering

• Operational and IT impact

Influence Business Management

• Identify key players/ leaders• Regulation : Business alignment

• Improvement• Opportunities

Peer Comparison

• Trade bodies• Network

• Qualification route• Training• Business approach

Advice Services

Label or philosophy: Does independence matter?

Implications for wealth managers, especially private banks, stockbrokers and private client investment manager:

• Independent advice across all relevant markets• Would it matter to your clients or your firm - Is there a benefit or demand

• How do you position your proposition• How many relevant markets do you cover • Own funds

A contradiction? • Retail distribution review but not all investments sold to retail investors are in scope

Shift to restricted: Strong evidence wealth managers are opting for “restricted”

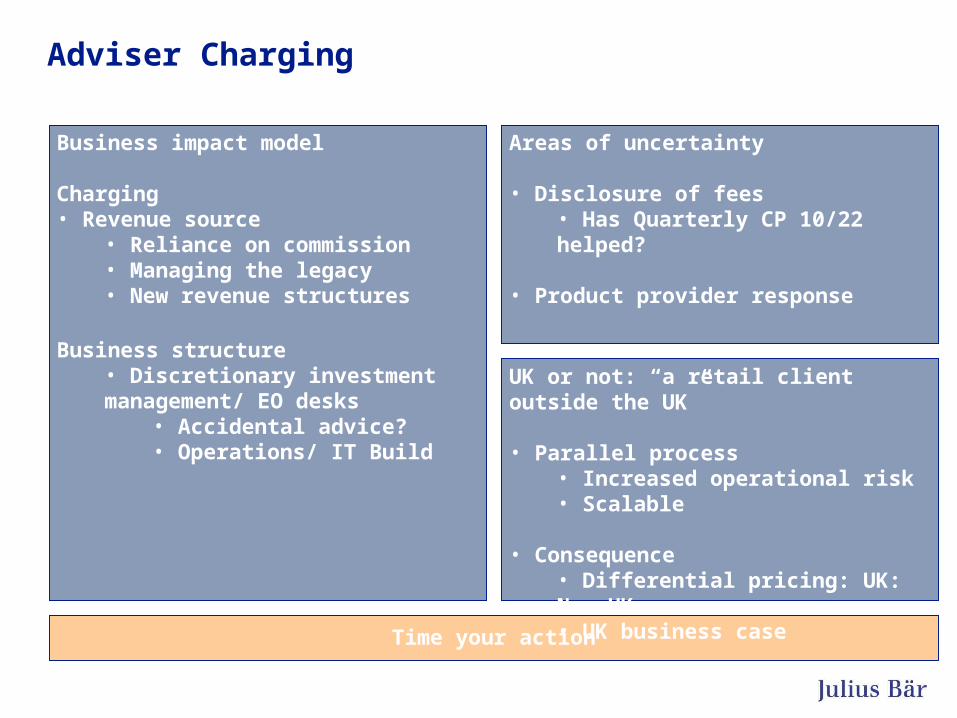

Adviser Charging

Areas of uncertainty

• Disclosure of fees• Has Quarterly CP 10/22 helped?

• Product provider response

Time your action

Business impact model

Charging• Revenue source

• Reliance on commission• Managing the legacy• New revenue structures

Business structure• Discretionary investment management/ EO desks

• Accidental advice?• Operations/ IT Build

UK or not: “a retail client outside the UK”

• Parallel process • Increased operational risk• Scalable

• Consequence• Differential pricing: UK: Non-UK• UK business case

Professionalism

Now

• Which exams• How much support• Overseas qualifications• Level 4 Gap Analysis

Looking ahead

• Wider aspects of professionalism• Redefining staff roles

• Discretionary management• Specialists• “Consultants”

• CF30’s who don’t make level 4?

Skilled Person Governance:Significant Influence Function (SIF) in practice

Gary PittsChief Compliance OfficerReligare Capital Markets

Disclaimer

The views expressed in this presentation are the views of the author and do not necessarily represent the views of Religare Capital Markets.

58

Who we are – a little context RCM wholly owned by Religare Enterprises Limited, listed in India with a market cap of

USD1.3bn REL through subsidiaries operates in:

– Investment banking– Retail broking (c.1 million accounts)– Commodity trading (largest broker on exchange)– Insurance– Collateralised finance– Mutual Funds– Asset Management– Wealth Management

RCM is investment banking arm, headquartered in London and Mumbai, with a presence in the US, Brazil, Dubai, Singapore, Hong Kong, Indonesia and Japan

59

Agenda Background and Drivers Key changes and recurring themes What is so different? Practical issues – compliance Practical issues – other stakeholders Practical issues – the global dimension (more work for MBAs?) Will this make any difference? Questions

60

Background and Drivers Banking crisis – after all, bank Boards were the only ones asleep on the job weren’t

they? CP10/03 Walker Review New Corporate Governance Code New regulatory emphasis:

– Intrusive supervision– Better understanding of governance constructs at firms– Control over the quality of senior individuals at firms

How much of this is genuinely “new” or requires new powers/rules? Open to debate.

61

Key changes and recurring themes Granularity around key roles and responsibilities

– CF 13 (Finance)– CF 14 (Risk)– CF 15 (Internal Audit)

“In consultation with your supervisor.” – more direct regulatory engagement– Extensive interviewing and engagement – more potential for moral hazard?– Impact on diversity?

Role of the Non-Executive Director:– CF2a (Chairman)– CF2b (Senior Independent Director)– CF2c (Risk Committee Chair)– CF2d (Audit Committee Chair)– CF2e (Remuneration Committee Chair)

62

What is so different? Prescriptive (despite the protestations) – but it is explicitly requiring you to do things

that a well-run firm would do as these are implicit in the existing Rules Attempt to obtain clarity around the operation of governance structures – reflects the

inherent limitations of regulation Final recognition of global matrix management structures with CF00

– Cultural and training issues– How accurate a reflection of the interplay in the governance structures?

Subtle changes, not just a “read across”

63

Practical Issues - compliance Keeping track – especially with internal changes to overseas governance impacting the

UK Documentation:

– Job specifications– Terms of Reference– Committee Minutes

Ideal and reality Realities of governance and independence

64

Practical Issues – Other Stakeholders Extension of risk More precision in roles and their supervision Role of HR Company Secretarial

65

Practical Issues – the global dimension Extension of risk overseas Draws overseas staff more actively into the governance process – practical and documentary

complexity D&O impact Understanding any buy-in Shift HQ and governance abroad?

66

Will this make any difference? Hopefully it will make it less easy for there to be the intellectually lazy “blame the Board”

approach which militates against an open and constructive analysis of root causes Moral hazard for the regulator? For well-run firms this is unlikely to be a problem – will it make a difference to the supervision of

poorly run firms? “Consult with your supervisor” – why are you not in an ongoing dialogue with them anyway? Will it militate against a diverse range of backgrounds adding value?

67

Questions?

?????

68

Chartered Institute for Securities & Investment

COMPLIANCE PROFESSIONALS

SUMMIT 2010

20 October 2010

Market Abuse: Lessons from recent cases

Nick Gibson,

Head of Compliance Solutions

Chase Cooper Limited

Agenda

• Reviewing the cases

• Identifying the themes

• What went wrong?

• Are these representative of the industry?

Structure

Over the course of this session:

• We will talk about trends, themes and FSA’s perspectives

• We will talk about focus areas for FSA Enforcement and what went wrong at firms

• I will ask for your collective and individual views

• We will do a couple of exercises– Focusing on how you as an imaginary blackguard

would circumvent FSA requirements– To equip you to detect others doing so…

FSA pronouncements

• “It is worth re-emphasising that the FSA is not – and will not become – an enforcement-led regulator”

Callum McCarthy, July 2005

• Then “Credible deterrence” emerged as a new mantra in FSA speeches from 2006, and was introduced as a policy in 2007.

• “… we’ve got to use Enforcement as one of our major tools. Our aim is to bring about real changes in behaviour to protect consumers and to guard against abuse in the markets.”

Margaret Cole, June 2008

FSA pronouncements

• “..we have clearly demonstrated that we are committed to taking on the tough challenges and risks that criminal prosecutions and other high-profile market abuse cases bring – and to using all the tools at our disposal and, where we don’t have the right tools, obtaining new ones.”

Margaret Cole, June 2010

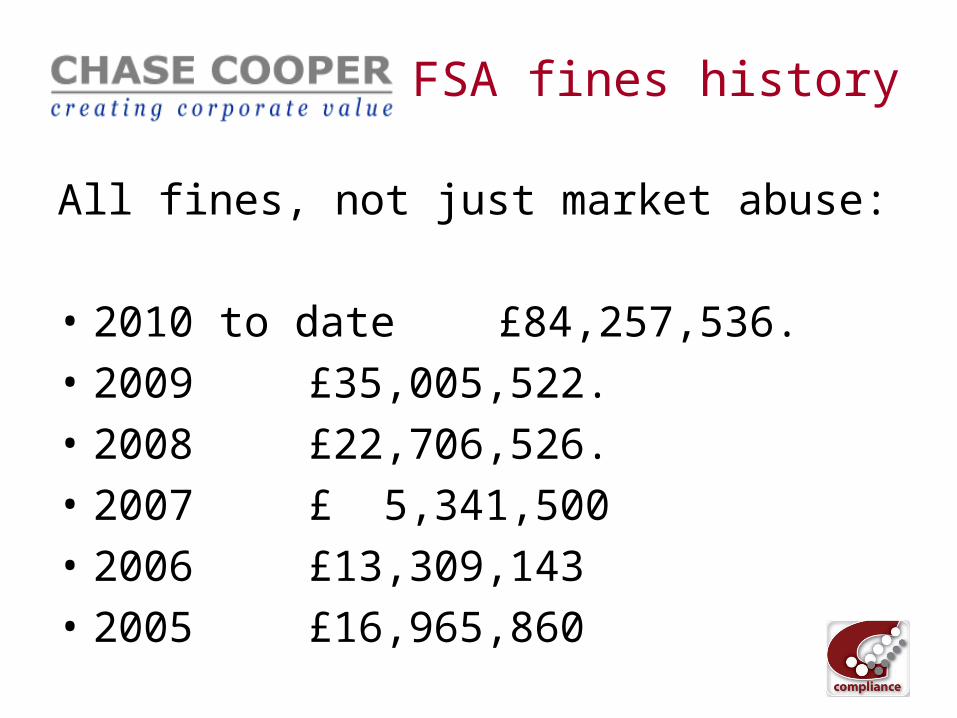

FSA fines history

All fines, not just market abuse:

• 2010 to date £84,257,536.

• 2009 £35,005,522.

• 2008 £22,706,526.

• 2007 £ 5,341,500

• 2006 £13,309,143

• 2005 £16,965,860

The convictions - 2010

10/12/2009

Matthew Uberoi 12 months

Neel Uberoi 24 months

Insider trading based on information acquired by Matthew whilst an intern at Hoare Govett and passed to his father.

The convictions - 2010

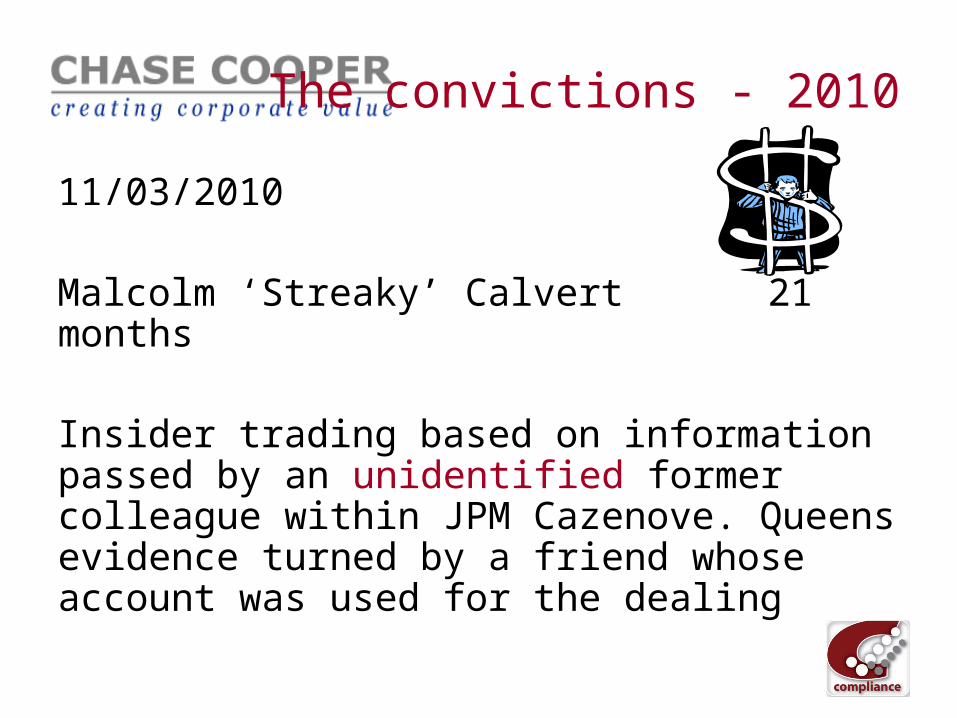

11/03/2010

Malcolm ‘Streaky’ Calvert 21 months

Insider trading based on information passed by an unidentified former colleague within JPM Cazenove. Queens evidence turned by a friend whose account was used for the dealing

The convictions - 201022/06/2010

Anjam Ahmad 10 months (suspended) 300 hours comm serv £ 50,000 fine

Insider trading in 19 different securities with an accomplice. Significant reduction in sentence due to guilty plea and extensive cooperation with FSA.

The acquittal - 2010

03/06/2010

McFall, Rimmington and King

Charged with insider trading in Neutec Pharma (King was a director). Jury found McFall and King not guilty, and case against Rimmington dismissed.

The fines - 2010

12/02/2010

Levent Akca £ 94,062Murat Ozgul £ 105,240Mehmet Sepil £ 967,005

For dealing in Heritage Oil plc shares on the basis of inside information. Sepil’s was the largest personal fine ever levied for market abuse

The fines - 2010

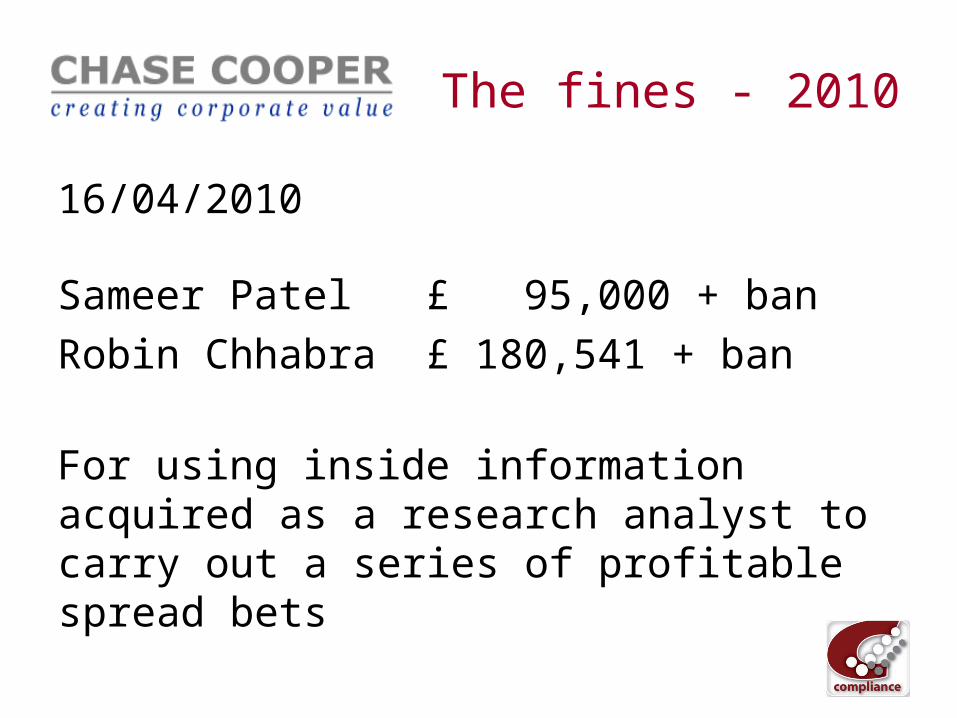

16/04/2010

Sameer Patel £ 95,000 + ban

Robin Chhabra £ 180,541 + ban

For using inside information acquired as a research analyst to carry out a series of profitable spread bets

The fines - 2010

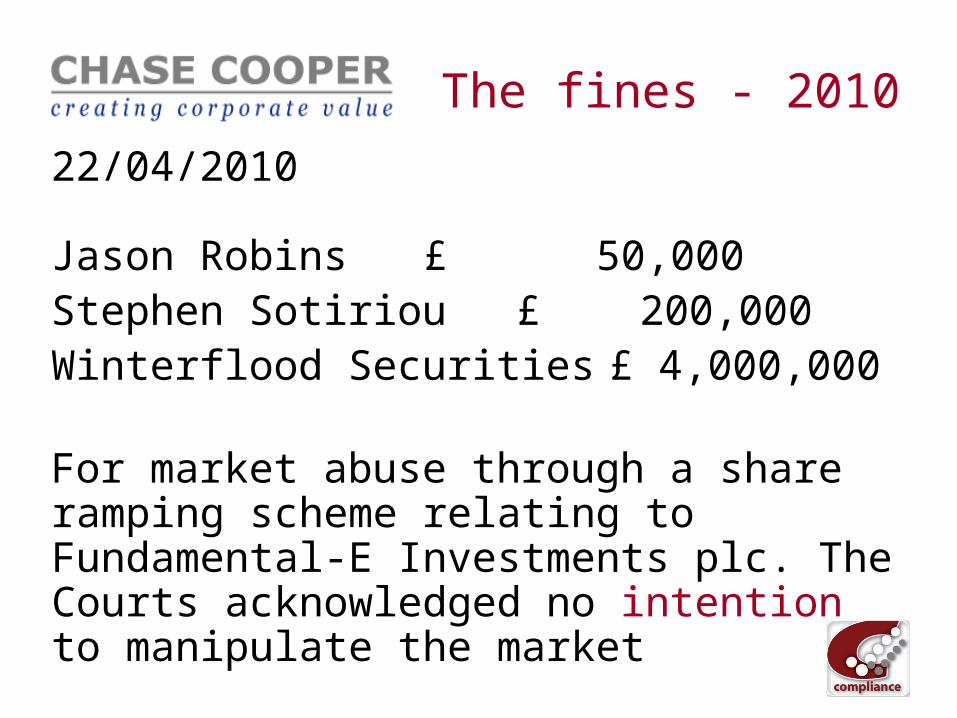

22/04/2010

Jason Robins £ 50,000Stephen Sotiriou £ 200,000Winterflood Securities £ 4,000,000

For market abuse through a share ramping scheme relating to Fundamental-E Investments plc. The Courts acknowledged no intention to manipulate the market

The fines - 2010

20/05/2010

Simon Eagle £ 2,800,000 + ban

For a complex and prolonged abusive scheme that deliberately set out to ramp up the share price of Fundamental-E Investments plc for his own benefit. The new largest personal fine for market abuse.

The fines - 2010

02/06/2010

Andrew Charles Kerr £ 100,000 + ban

Deliberately manipulating the market in LIFFE traded coffee futures and the related coffee futures options, in order to benefit a client. Ultimately, the client did not make the intended profit.

The fines - 2010

21/06/2010

Photo-Me International plc £ 500,000

For failing to disclose inside information to the market as soon as possible. The delay led to a false market in Photo-Me's shares for 44 days.

The fines - 2010

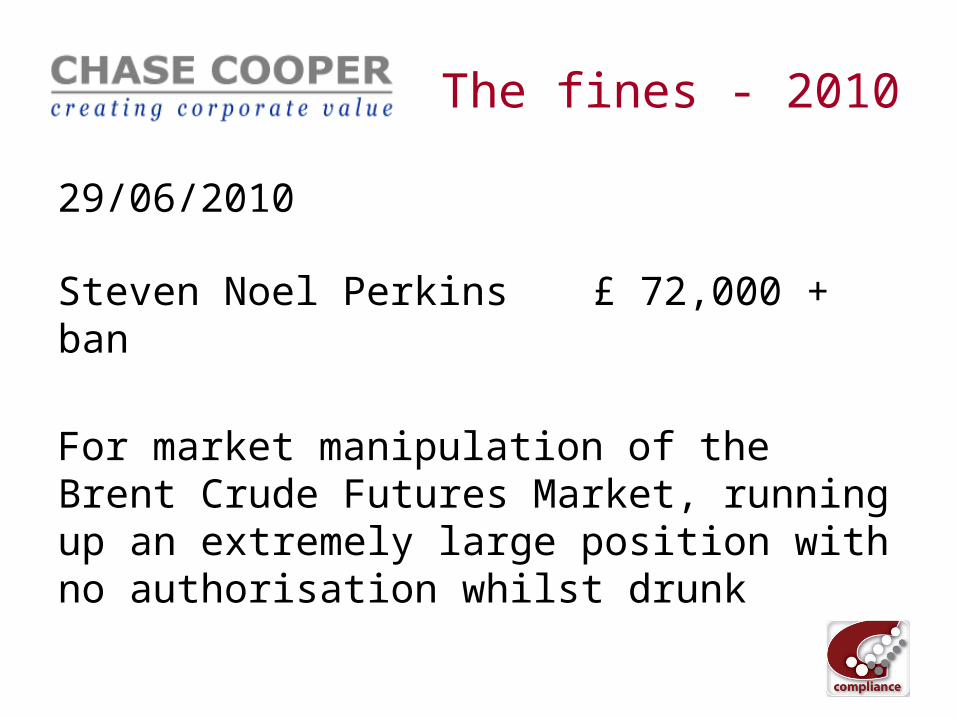

29/06/2010

Steven Noel Perkins £ 72,000 + ban

For market manipulation of the Brent Crude Futures Market, running up an extremely large position with no authorisation whilst drunk

The fines - 2010

06/07/2010

Henry Cameron £ 350,000

As CEO, making misleading announcements to the market regarding payments made by Sibir (a large energy company that was quoted on AIM) to its major shareholder Chalva Tchigirinski

The fines - 2010

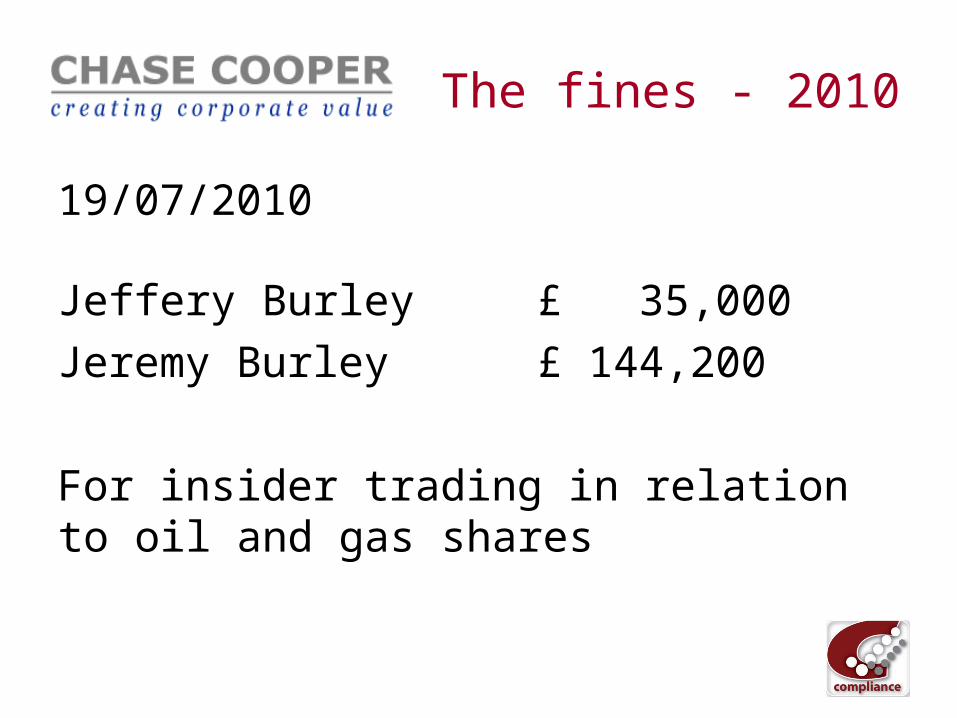

19/07/2010

Jeffery Burley £ 35,000

Jeremy Burley £ 144,200

For insider trading in relation to oil and gas shares

Impending prosecutions

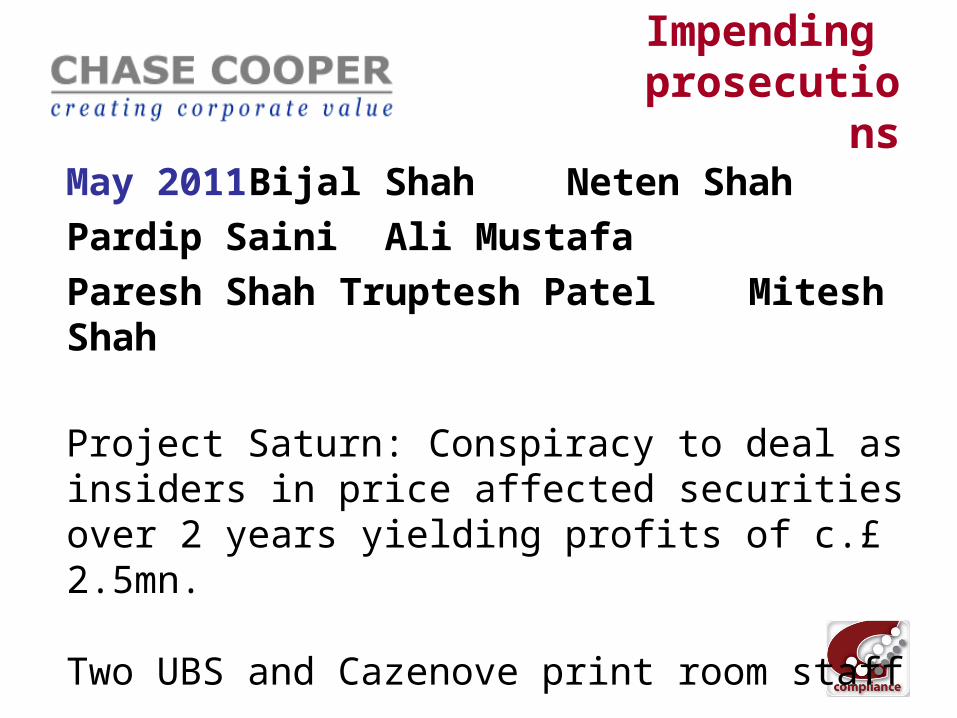

May 2011 Bijal Shah Neten Shah

Pardip Saini Ali Mustafa

Paresh Shah Truptesh Patel Mitesh Shah

Project Saturn: Conspiracy to deal as insiders in price affected securities over 2 years yielding profits of c.£ 2.5mn.

Two UBS and Cazenove print room staff

Impending prosecutions

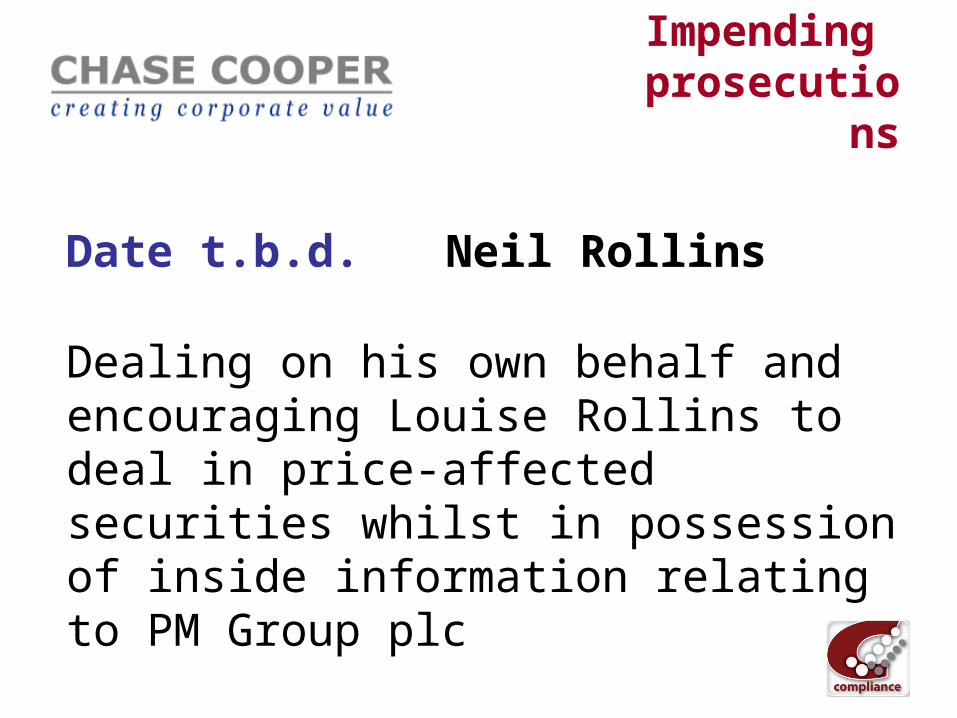

Date t.b.d. Neil Rollins

Dealing on his own behalf and encouraging Louise Rollins to deal in price-affected securities whilst in possession of inside information relating to PM Group plc

Impending prosecutions

Date t.b.d. Christian Littlewood

Angie Littlewood

Helmy Omar Sa’aid

Charged with 13 counts of insider trading between 2000 and 2009. Mr Sa’aid was arrested under a European Arrest Warrant in Mayotte (an island between Mozambique and Madagascar)

Yet to come…

The City Seven – alleged insider trading ringFSA/SOCA launched 16 simultaneous raids in March 2010, arresting six City professionals, with a further arrest made the following day.

Names cited by the media:

Deutsche Bank

Exane

Moore Capital

Aria Capital

Yet to come…

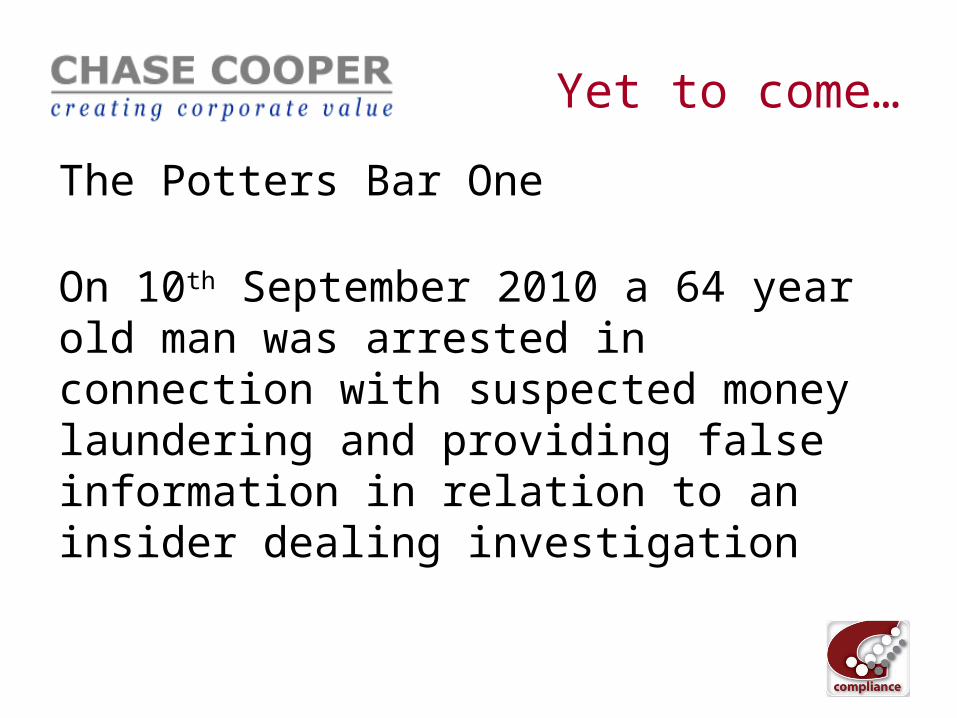

The Potters Bar One

On 10th September 2010 a 64 year old man was arrested in connection with suspected money laundering and providing false information in relation to an insider dealing investigation

Deterrence?

• Malcolm ‘Streaky’ Calvert

– Sentenced to 21 months inside

– Released after 7 months

Identifying the themes

It’s difficult….there is such variance

However:• Increasing focus on professionals rather than

amateurs• Spreading beyond equities into commodities• Almost automatic inclusion of money

laundering charges for dealing with the proceeds of market abuse

Identifying the themes

• Deployment of new tools– Plea bargaining for cooperation– Extra-territorial reach– Co-ordinated dawn raids/public profile– Serious fines for transaction reporting failures

(i.e. preventing detection)– Much higher fines across the piste for individuals

and firms

Identifying the themes

• Focus on Listed corporates’ announcements and misleading the markets

• Market abuse is effect-based, not intent-based (MAD and proved in Winterflood)

• Focus on conspirators, rather than just prime movers

• Abuse of the UK markets from overseas

What went wrong?

• People thought they’d get away with it…

• Still seen as a “victimless crime”?– Only illegal since 1980

• Opportunistic?– Possibly true for individuals, not true for rings

• History of poor detection/prosecution?

What went wrong?

• One degree of separation…– Relatives– Friends

• Who can be trusted with information?

• Ultimately, there is an inbuilt delay between the environment becoming harsher and the occupiers realising that the game has changed….

What went wrong?

• If people want to behave badly, they will..

• …..unless the disincentives outweigh the incentives

• The regulator plays a part

• Firms play a part

• What part do you play personally?

Are these representative of the industry?

• How many of you think that, yes, these cases are representative of the industry?

• Of those who thought no, what is your justification for that view?

• My view:– 99.9% wish to behave properly– 0.09% will take advantage of low risk

opportunity– 0.01% see the gravy train, take the risk

Are these representative of the industry?

• Regrettably, the rules are designed for the 0.1%, not for the 99.9%

• We all pay for it– Co-workers– Shareholders– Borrowers/depositors/investors– Society/taxpayers

• We put up with– Personal account dealing rules– Routine invasion of privacy– Idiocy?

And now for some work…

Before you criticise someone try walking a mile in their shoes

That way, if you do condemn them, you’re a mile away

and you have their shoes

Two exercises

In order to prevent or detect harm, you need to understand how it may occur

Poachers make the best gamekeepers

Burglars make the best security consultants

A reminder

• “..we have clearly demonstrated that we are committed to taking on the tough challenges and risks that criminal prosecutions and other high-profile market abuse cases bring – and to using all the tools at our disposal and, where we don’t have the right tools, obtaining new ones.”

Margaret Cole, June 2010

Mobile phone recording

• FSA CP 10/7 – Taping: removing the mobile phone exemption March 2010

• Taping rules are “..aimed mainly at combating market abuse..”

• Proposal requires firms “..to tape relevant communications on mobile phones issued by the firms for business use..”

• Also “.. to take reasonable steps to prevent employees … from using private communication equipment (which may not be recorded due to privacy laws) to make such communications”

Mobile phone recording

Your challenge is either:

• To establish what you, a front office staff member, will do if you wish to contravene this rule with maximum safety, or

• To describe three reasonable steps your firm will be taking to prevent employees from making relevant communications on personal equipment

Mobile phone recording

You have three minutes….

Time’s up…

Mobile phone recording

Your solutions,

please..

Leaks

Market Watch 37 September 2010

“We are particularly concerned about the suspected practice of core insiders strategically leaking inside information; we have stated we will increase our efforts into the causes of leaks in individual cases.”

Leaks – by the way..

• “..insiders who confirm information put to them by a journalist still potentially commit market abuse as they are in effect disclosing inside information through affirmation (even though the information was sourced first elsewhere).” MW37

• Wider implications?

• Regulation by newsletter?

Leaks – FSA approach

Series of recommendations:

• Dealing with media enquiries

• Handling leaks– 2½ pages of detailed process for investigating

leaks

• Training and communicating with staff

• Establishing a reporting culture

• Disciplinary action

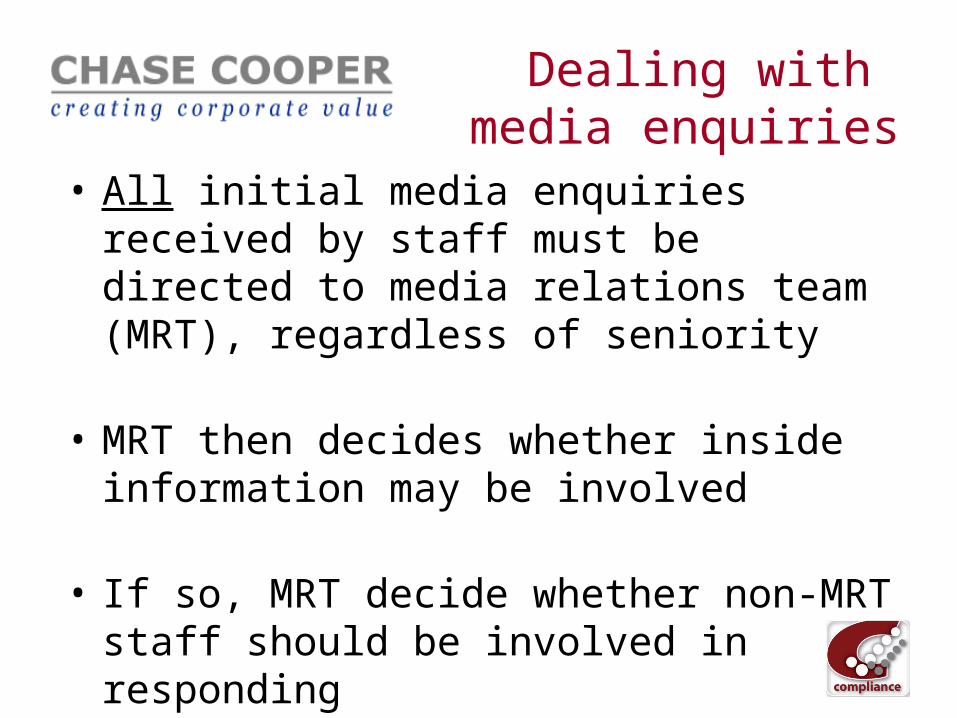

Dealing with media enquiries

• All initial media enquiries received by staff must be directed to media relations team (MRT), regardless of seniority

• MRT then decides whether inside information may be involved

• If so, MRT decide whether non-MRT staff should be involved in responding

Dealing with media enquiries

• If non-MRT staff should be involved, this is only possible where – MRT member leads on or is present at

conversation, and makes contemporaneous note, or

– Conversation with journalist and non-MRT member is taped, and/or

– Any written communication (including e-mail) is simultaneously copied to MRT

– Text messages?

Media relations code

• FSA expectation is that…

“…in most cases where an enquiry is potentially related to inside information, enquiries will be solely handled by the regulated firm’s media relations team with standard protocol responses. It is unlikely to be necessary to involve non-media relations personnel.”

Dealing with media enquiries

Your challenge is either:

• To establish what you, as a journalist, will do to follow up on a rumoured merger with the target’s corporate broker, and your conclusions

• To establish what you, as a corporate financier, will do to circumvent the rules on media contact and maintain journalistic relationships

Mobile phone recording

You have seven minutes….

Time’s up…

Mobile phone recording

Your solutions,

please..

Why, oh why…?

• Do we need new requirements?

• What ever happened to enforcing the rules that currently exist?

Conclusions

• Use your imagination and intelligence – don’t just tick boxes

• Stay aware of current FSA cases, themes and trends

• Deal properly with exceptions when they arise

• Make sure that your firm’s requirements are clear to everyone

Arbuthnot Latham & Co., Limited

Building mutually profitable relationships through a meeting of minds

Preparing for FSA Visits and what todo in between

David Moland, Group Head of Compliance Arbuthnot Latham & Co., Limited

20th October 2010

123

Who am I?

• Deputy Chairman of the CISI Compliance Forum Committee

• Compliance professional for 11 years

• Experience gained working for Lloyds TSB, FSA, Credit Suisse and Arbuthnot Banking Group

• Current Role – Group Head of Compliance covering Private Banking, Investment Banking & Retail Banking

• Direct and current experience of ARROW assessments and Theme Visits

124

Objectives

• What are the FSA’s objectives on ARROW visits?

• How does ARROW fit with ongoing supervision

• What to do in between visits

• How to be ready for a theme review

• How to measure success – and outcomes to avoid

FSA’s Objectives

125

• These will depend on the themes of the day, examples may be………………

• To set your regulatory period, to set your ICG

• To require the firm to carry out actions via the Risk Mitigation Programme

• To get a feel for how well the firm is managed and controlled

Ongoing Action

126

• Preparation starts as soon as last ARROW is complete

• Clear issues raised in the letter and RMP

• Continue to manage the relationship (KIV change of supervisor)

• Always remember that your next visit could be only days away

• Look out for Themes, Dear CEOs etc

Preparing for ARROW (1)

127

REMEMBER, you know when it is going to be!

Brief Senior Management (6 months)

1. Introduction

2. Risk Assessment Process

3. Current FSA Risk Assessment

4. Hot Topics / Expected Focus

5. Other Possible Topics

6. How to Conduct the Meetings

7. Next Steps

Preparing for ARROW (2)

128

• Meeting with Group Board & Group Audit Committee (5months)

• Face to face meeting with Directors (4 months) – get them engaged

• Key action document analysis (3 months) – cover the obvious & topical issues

Preparing for ARROW – document request

129

• Check your understanding of what they require

• Presentation is important!

• Try not to send documents that will result in the FSA asking further questions

• Get the Directors to read and review what you are going to send

• Provide copy documents to each Director / Interviewee

Note – we had 10 working days to do this!

Case Study 1

130

You are the newly appointed Head of Compliance at a firm that is on a three year

regulatory cycle, which ends in six months time. You decide that you want to start

your preparation for the next ARROW visit. You are going to do this by sending a

written briefing to all the Directors.

What are you going to include within this briefing and what if anything are you going

do prior to sending the document out?

CHATHAM HOUSE RULES

Theme Visits

131

• If you are lucky you will get a months notice, but will probably only have 10 days to satisfy

any document request

• Treat with same importance as an ARROW assessment

• You will not have time to prepare in the same way as ARROW

• Demonstrates the importance of having documents in place already and building a

relationship with the FSA

• Get the Directors / Senior Management engaged – a theme is not a gentle chat many

have ended in Enforcement for at least one of the firms selected

Case Study 2 – Theme Visits

132

You are the Head of Compliance at a small firm and you have just received a call

from the FSA advising that they are going to carry out a themed visit on AML.

You have only been at the firm for three months and you at the early stages of

reviewing the controls in place at the firm. Your first thought is (*!!*):

If only I had been here longer what would have helped me?

Having gone through these moments of reflection, what action would you now take?

CHATHAM HOUSE RULES

FSA visits in general

133

• Review documents again prior to the visit

• Carry out mock interviews (one month before)

• Brainstorm topics for discussion (one week before)

• Agree with FSA whether someone can sit in on interviews

• Debrief interviews if you don’t have someone sitting in

• Make the most of the feedback session but be aware things change, especially with

Theme Visits

Ad hoc requests and CEO letters

134

• Treat with same importance as a visit

• Get Directors to review

• Take action even if FSA do not ask for a response

• Look out for best practice papers (Data Security, Pension Transfers, Sanctions)

Case study 3 – How to measure success – and outcomes to avoid

135

• What would you consider to be a successful visit?

• From whose angle are you measuring success?

• How would you measure this?

• What would be considered to be bad outcomes?

• Can you challenge the outcome?

Conclusion

136

• Compliance have an important role to play in all interactions with the FSA

• In an ideal world, have all policies, procedures etc in a state you would be happy to

send to the FSA tomorrow

• Preparation is important

• Get Senior Management engaged

137

Any Questions?

The information given in this document is for information only and does not constitute investment, legal, accounting or tax advice, or a representation that any investment or service is suitable or appropriate to your individual circumstances.

You should seek professional advice before making any investment decision. The value of investments and the income from them can fall as well as rise. An investor may not get back the amount of money invested. Past performance is not a guide to future performance.

The facts and opinions expressed are those of the author of the document as of the date of writing and are liable to change without notice. We do not make any representation as to the accuracy or completeness of the material and do not accept liability for any loss arising from the use hereof. We are under no obligation to ensure that updates to the document are brought to the attention of any recipient of this material.

This document is produced for the person whose name is reproduced on the front cover. It may not be reproduced either in whole, or in part, without our written permission. The distribution of this document and the offer and sale of the investment in certain jurisdictions may be forbidden or restricted by law or regulation. In particular, it may not be sent to or taken into the United States or passed to any U.S. person.

Arbuthnot Latham Arbuthnot House

20 Ropemaker Street London, EC2Y 9AR

t +44(0)20 7012 2500 f +44(0)20 7012 2501

www.arbuthnotlatham.co.uk

Arbuthnot Latham & Co., Limited is authorised and regulated by the Financial Services Authority

Chartered Institute for Securities & Investment

COMPLIANCE PROFESSIONALS

SUMMIT 2010

20 October 2010

Panel Session: Everything you wanted to

know about enforcement but were too afraid to ask

Ian Mason, Baker & McKenzieNick Gibson FCSI, Chase Cooper

Tony Bronk, Chartered FCSI, BDO Investment Management

Compliance Professionals Summit 2010

Ian Mason MCSI

Partner, Baker & McKenzie, Financial Services Group

20 October 2010

3329550

“There is a view that people are not frightened of the FSA. I can assure you that this is a view I am determined to correct. People should be very frightened of the FSA.”

Hector Sants, FSA Chief Executive

3329550

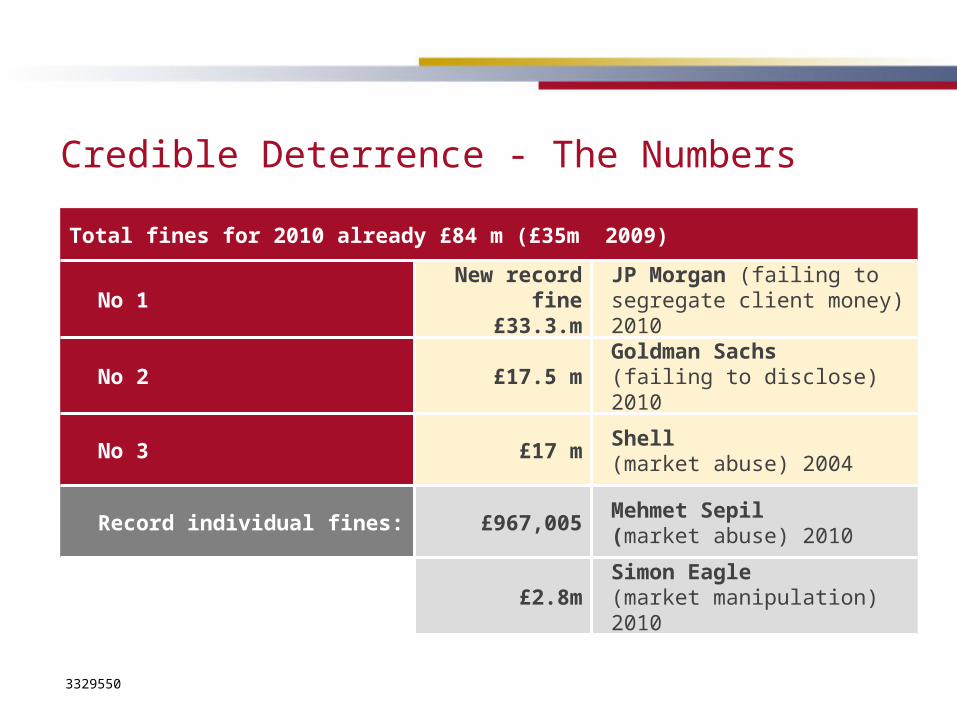

Credible Deterrence - The Numbers

Total fines for 2010 already £84 m (£35m 2009)

No 1New record

fine £33.3.mJP Morgan (failing to segregate client money) 2010

No 2 £17.5 mGoldman Sachs (failing to disclose) 2010

No 3 £17 mShell (market abuse) 2004

Record individual fines: £967,005Mehmet Sepil (market abuse) 2010

£2.8mSimon Eagle(market manipulation) 2010

3329550

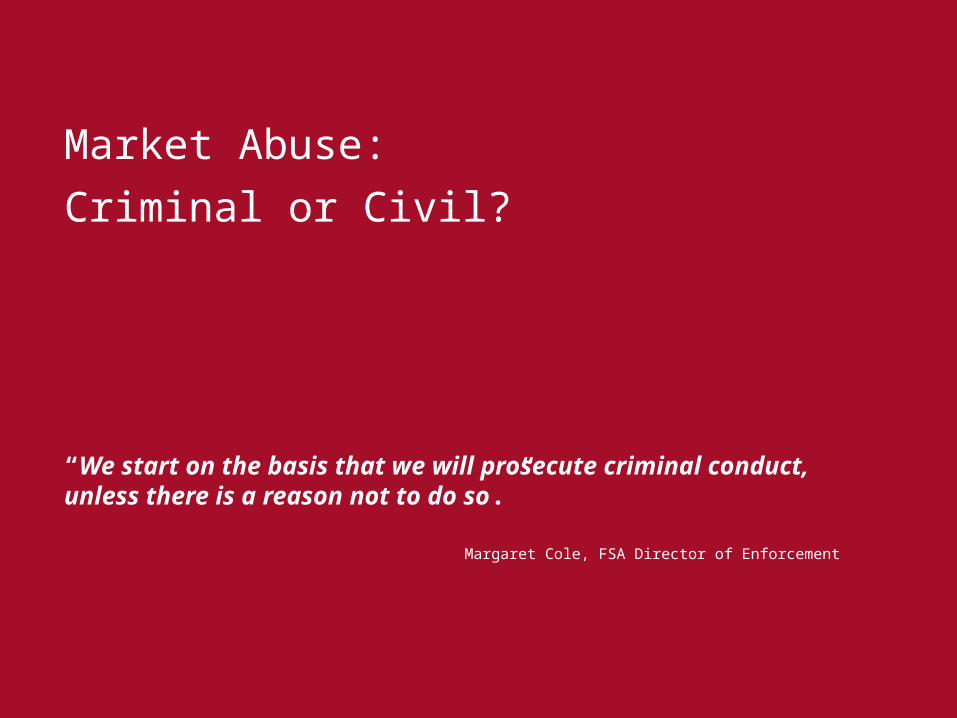

“We start on the basis that we will prosecute criminal conduct, unless there is a reason not to do so.”

Margaret Cole, FSA Director of Enforcement

Market Abuse:

Criminal or Civil?

3329550

Recent Market Abuse Cases

• Anjam Ahmad - 10 months imprisonment, 300 hours unpaid community service, £50k fine

• Matthew and Neal Uberoi - 12 and 24 months imprisonment

• Civil fines, Eagle, Sepil, Winterfloods (£4 m)

• Dawn raids

3329550

New Fining Regime: Five Stage Approach

Step 1

Disgorge any benefit

Step 2

Determine penalty that reflects nature, impact and seriousness of breach

Step 3

Adjust for any mitigating/aggravating factors

Step 2

Adjust upwards for deterrence

Step 3

Discount for early settlement

STEP 1 STEP 2 STEP 3 STEP 4 STEP 5

Minimum £100,000 fine for market abuse.

3329550

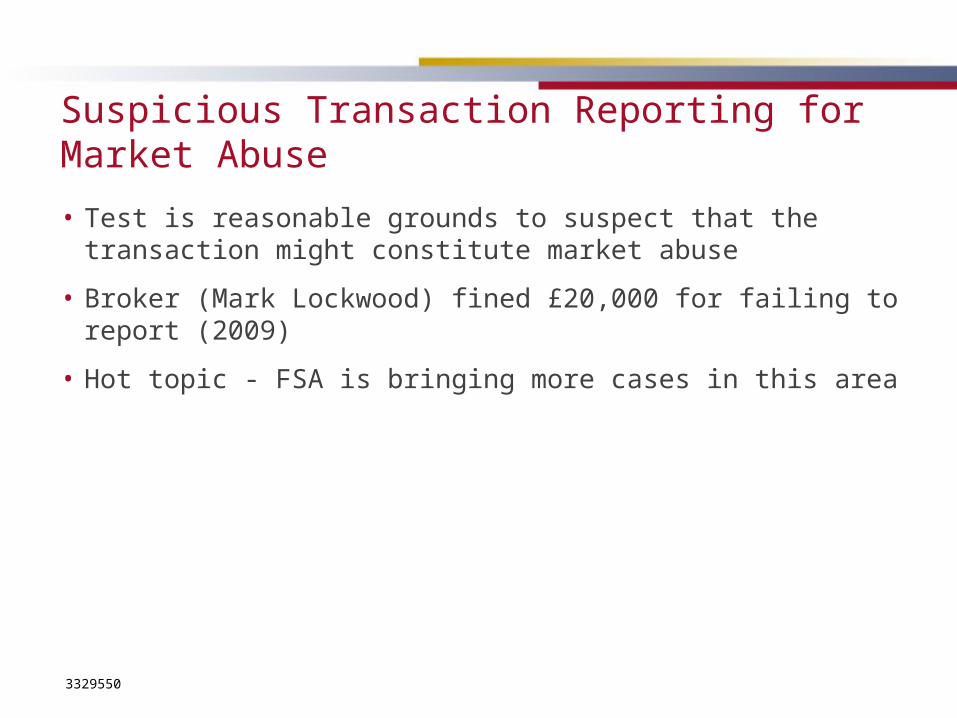

Suspicious Transaction Reporting for Market Abuse

• Test is reasonable grounds to suspect that the transaction might constitute market abuse

• Broker (Mark Lockwood) fined £20,000 for failing to report (2009)

• Hot topic - FSA is bringing more cases in this area

3329550

Recent Transaction Reporting Cases

Soc Gen £1.575 m August 2010

Credit Suisse £1.75m April 2010

Instinet £1.05m April 2010

Getco Europe £1.4m April 2010

Commerzbank £595,000 April 2010

Barclays £2.45 m 2009

3329550

Transaction Reporting Cases

• Easy cases for the FSA to bring

• Have you conducted an internal review?

• Have you followed up on any red flags?

• Technical IT issues combined with regulatory risk is a danger area!

3329550

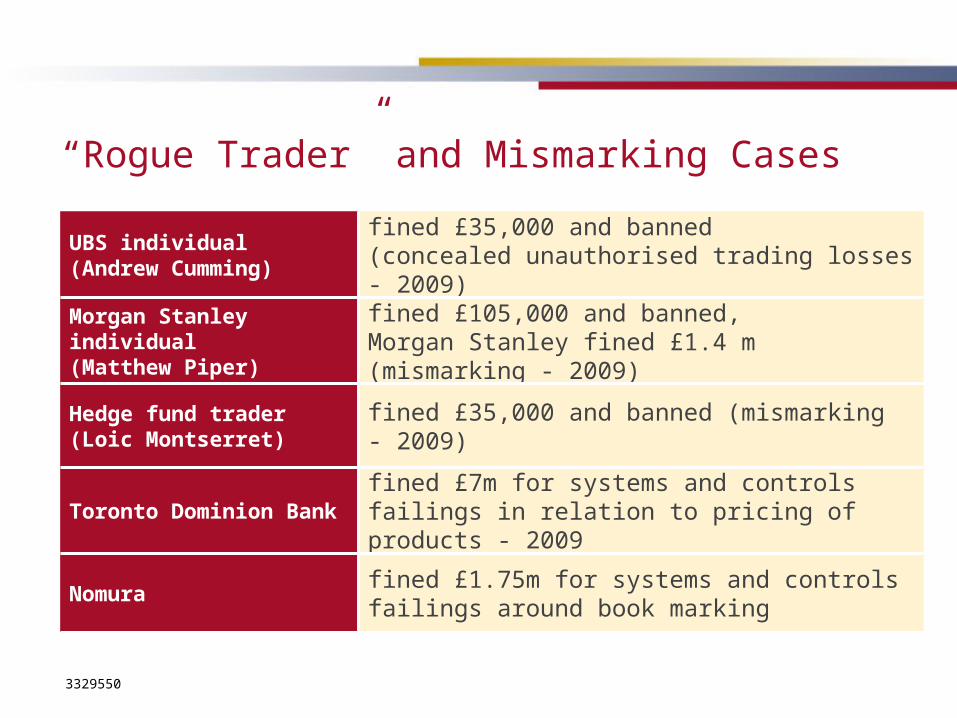

“Rogue Trader” and Mismarking Cases

UBS individual(Andrew Cumming)

fined £35,000 and banned (concealed unauthorised trading losses - 2009)

Morgan Stanley individual(Matthew Piper)

fined £105,000 and banned, Morgan Stanley fined £1.4 m (mismarking - 2009)

Hedge fund trader (Loic Montserret) fined £35,000 and banned (mismarking - 2009)

Toronto Dominion Bank fined £7m for systems and controls failings in relation to pricing of products - 2009

Nomura fined £1.75m for systems and controls failings around book marking

3329550

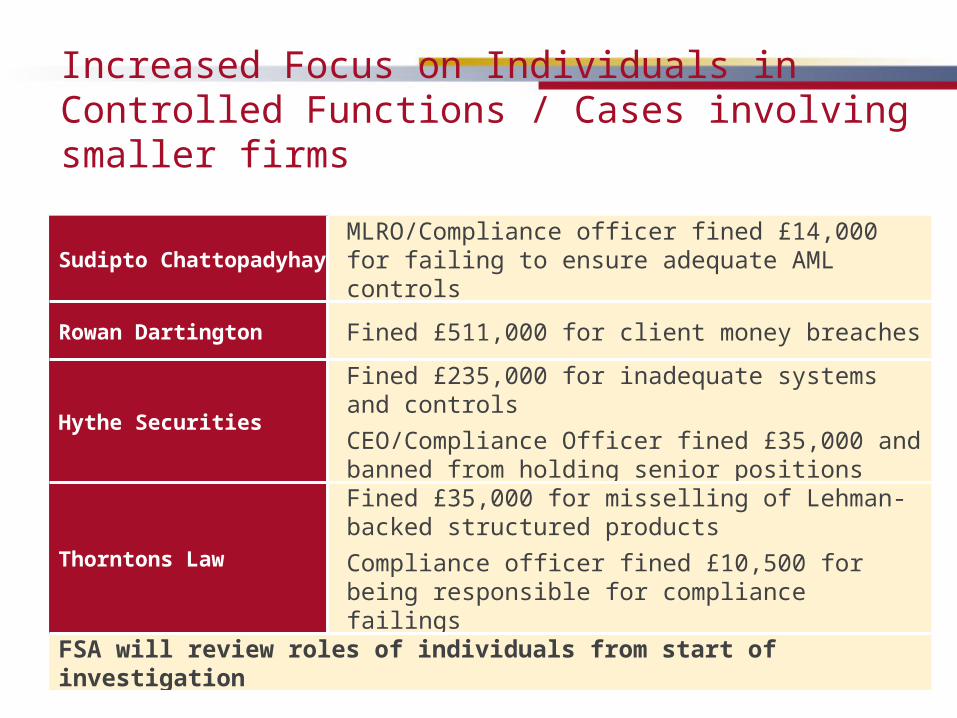

Increased Focus on Individuals in Controlled Functions / Cases involving smaller firms

Sudipto ChattopadyhayMLRO/Compliance officer fined £14,000 for failing to ensure adequate AML controls

Rowan Dartington Fined £511,000 for client money breaches

Hythe Securities

Fined £235,000 for inadequate systems and controls

CEO/Compliance Officer fined £35,000 and banned from holding senior positions

Thorntons Law

Fined £35,000 for misselling of Lehman-backed structured products

Compliance officer fined £10,500 for being responsible for compliance failings

FSA will review roles of individuals from start of investigation

3329550

How Can You Protect Your Position?

• Clear accountabilities - is your role clearly defined or is there "creep"?

• Escalation - clearly documented

• Red flags acted on with clear audit trail

• Review FSA communications, circulate, escalate

3329550

The Future

• Abolition of FSA

• Enforcement will continue

• Fines will continue to increase

• More intensive and intrusive approach from supervisors as well as enforcement

3329550

Contact Details

Ian MasonPartner

Baker & McKenzieFinancial Services GroupDD: +44( 0) 20 7919 [email protected]

Compliance Professionals Summit 2010

Baker & McKenzie LLP is a limited liability partnership registered in England and Wales with registered number OC311297. A list of members' names is open to inspection at its registered office and principal place of business, 100 New Bridge Street, London, EC4V 6JA. Baker & McKenzie LLP is a member of Baker & McKenzie International, a Swiss Verein with member law firms around the world. In accordance with the terminology commonly used in professional service organisations, reference to a "partner" means a person who is a member, partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm.

Baker & McKenzie LLP is regulated by the Solicitors Regulation Authority of England and Wales. Further information regarding the regulatory position is available at http://www.bakermckenzie.com/london/regulatoryinformation.

Ian Mason MCSI

Partner, Baker & McKenzie, Financial Services Group

20 October 2010

3329550

Panel Session: Everything you wanted to

know about enforcement but were too afraid to ask

Ian Mason, Baker & McKenzieNick Gibson FCSI, Chase Cooper

Tony Bronk, Chartered FCSI, BDO Investment Management

Chartered Institute for Securities & Investment

COMPLIANCE PROFESSIONALS

SUMMIT 2010

20 October 2010