charitable gifts of mineral...

TRANSCRIPT

Charitable Gifts of Mineral Interests

Mark Ladendorf KASPICK & COMPANY

Boston, MA

Glenn Pittsford Texas A&M Foundation College Station, TX

CHARITABLE GIFTS OF MINERAL INTERESTS Mark Ladendorf, KASPICK & COMPANY and Glenn Pittsford, Texas A&M Foundation

With energy costs increasing over the past decade, the value of mineral interests has risen

considerably. In addition, new techniques to extract natural gas from shale deposits, which are

found across the country, have brought energy investment and production to a number of new

areas. As a result, many landowners find they have considerable wealth below the surface of

their properties.

For those with charitable intent, these assets represent an opportunity to make substantial

gifts. For charities, especially those in areas that have not seen many gifts of mineral interests,

these potential gifts come with many questions and unknown risks.

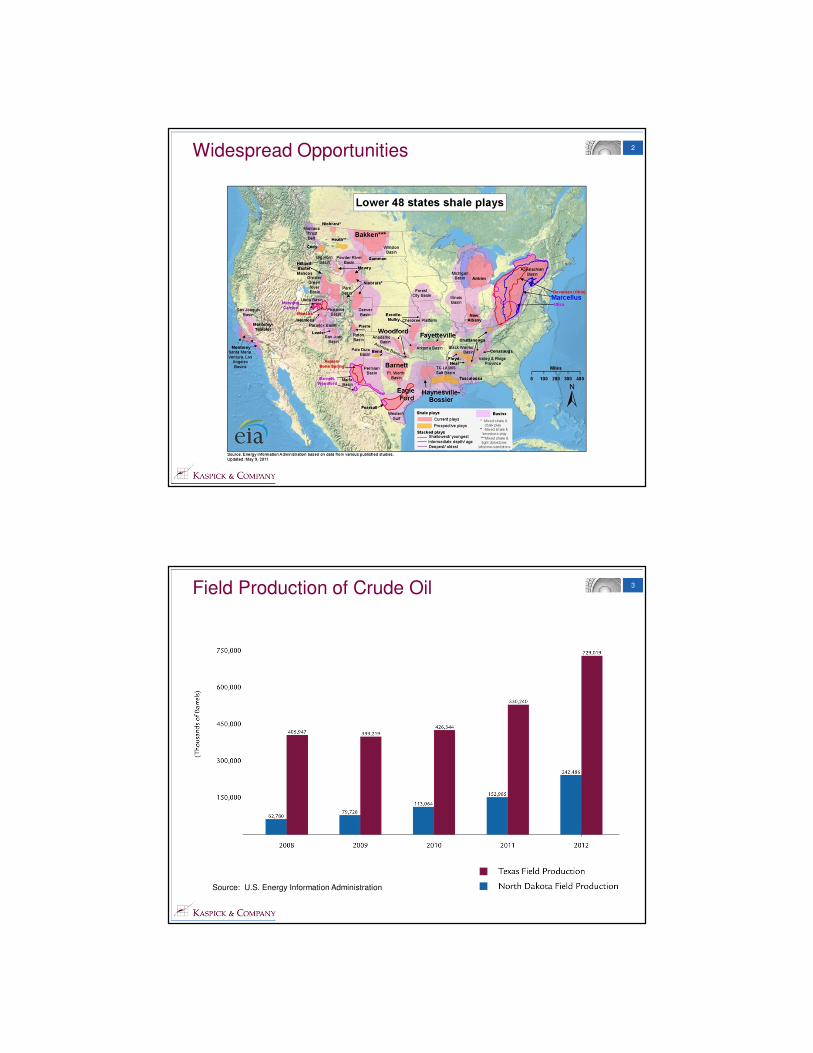

Opportunities

The expansion of mineral production in the United States, especially that of oil and gas, has

accelerated over the past decade. This is especially true in areas where a new shale deposit

extraction technique, commonly called fracking is used. This includes Barnett and Eagle Ford

Shale in Texas, Bakken Shale in North Dakota, and Marcellus Shale in the Northeast,

particularly Pennsylvania. Because of the widespread nature of shale deposits (see figure 1),

production could expand to additional areas in the future.

Figure 1

Expanded production often leads to newfound wealth for owners of mineral interests, both from

the value of the interest itself, as well as royalties obtained from the interest. Expansion of

production in two states, North Dakota (oil) and Pennsylvania (natural gas), has been particularly

impressive (see figures 2 and 3).

Figure 2

Source: Institute for Energy Research

Figure 3

While mineral interests can be complex, they can be valuable gifts for charitable organizations.

In addition, the wealth created from mineral interests can also lead to additional outright and life

income gifts. Charitable organizations that are open to these gifts and actively seek opportunities

are likely to find potential donors within their constituencies.

How Are the Mineral Interests Owned and Structured?

Figure 4 provides a basic framework of the ownership of mineral interests, and the usual

structure of interests that are being produced.

Figure 4

The ownership and transfer of mineral interests are governed by state law, and each state has its

own rules on how mineral interests are handled. In general, a landowner of property that has not

separated the surface and mineral interests is assumed to own both (or at least has the right to

extract minerals). If the interests are separated, each interest can be transferred independently

through a deed. It is important to note that ownership of mineral interests also includes the right

to access those interests. Since the only way to access the minerals is through the surface, the

surface owner can be adversely affected by mineral production.

The right to access minerals is commonly granted through the form of leases. There are two

broad types of mineral interests: working interests and royalty interests. In most cases, the

owner of the minerals gives a working interest to another party through a lease. A working

interest gives the holder of that interest the right to access the minerals through the surface of the

property, to incur the costs of exploration and production of the minerals, and to retain profits

subject to the lessor’s retained rights. The holder of the working interest has responsibility for

liability and environmental concerns. In exchange for granting the lease, the mineral interest

owner will retain a royalty interest. By leasing the right to extract minerals, the mineral interest

owner avoids the necessary investment and liability concerns, but the owner receives only a

fraction of the value of the minerals in the form of royalty payments.

Compensation for leasing the production of mineral interests under a royalty interest consists of a

bonus payment (an outright sum of cash) for the right to explore and begin production, royalty

payments when minerals are produced, and sometimes payments for non-production, called

delay rentals before production begins and shut-in royalty when existing production ceases, in

order to hold the lease. Typically, a bonus payment gives the leasing company two to three years

to begin production. If minerals are produced, royalties usually equal to between an eighth and a

quarter percent of the value of the minerals are paid.

A lease remains in force once production commences. If production does not begin in the

specified period, the owner can execute an option to extend the existing lease (if permitted by the

lease), enter into a top lease with the lessee that will take effect immediately after the expiration of

the original lease, or simply re-lease the interest to a new party.

Two additional types of royalties are common. A non-participating royalty interest (NPRI) is an

interest in oil and gas production which is created from the mineral estate. Like the standard

royalty interest it is an expense free interest, bearing no operational costs of production. The term

“non-producing” indicates that the interest owner does not share in the bonus, rentals from a lease,

nor the right, or obligation to make decisions regarding execution of leases. In other words the

NPRI has no executive rights. The NPRI owner has fewer rights than does the standard royalty

owner, who participates in at least one of the activities mentioned above.

NPRI’s are often created, transferred, or assigned when the surface estate changes ownership. Due

to the potential wealth created by a mineral interest and the associated damage to the surface estate

incurred developing the mineral estate, past and present land owners might want to share in future

oil and gas royalty production. Most people do not like giving up control or their “executive

rights”, so NPRI’s become a valuable tool in negotiations. A seller of the land might reserve the

minerals and assign an NPRI to make sure the new owner benefits from the oil and gas

development as well. On the other hand, if the buyer is acquiring the minerals, he or she might

assign a NPRI to the seller as additional compensation or goodwill.

An overriding royalty interest (ORRI) is a nonoperating interest that is carved out of the working

interest of an oil and gas lease, rather than the royalty interest. It can be created through a

conveyance, but it is more commonly created by a reservation in the assignment or transfer of an

oil and gas lease. It is a nonpossessory interest that attaches only when its share of oil and gas is

reduced to possession, giving the owner no right, absent an agreement to the contrary, to

participate in decisions with regard to the development and operation of the burdened lease. Since

an overriding royalty interest is “carved out” of the leasehold interest, it is limited in duration to the

term of the burdened lease. The working interest owner might provide the ORRI to a third party

that would in turn provide financing to develop a well and begin production.

Several different exploration and production companies are typically involved in the development

of any particular well. Each of these companies is governed by an agreement called a Joint

Operating Agreement (JOA). While in most cases, ORRI does not share in liability associated

with a well, in some cases the JOA might include the ORRI holder in the liability chain.

What Can a Charity Receive?

Whether a gift of a mineral interest is a proposed lifetime gift from a donor, or comes to the

charity through an estate, the charity should first determine the type of interest. Most charities

would not accept a working interest because of the accompanying investment necessary to

extract the minerals as well as potential liabilities associated with production. Most importantly,

the income produced from a working interest would be considered unrelated business taxable

income (UBTI) to the charity (see Rev. Rul. 69-179).

If the proposed gift is a royalty interest or NPRI, there are no liability risks, and the royalty

income, as well as bonus payments (if any), are considered passive income not subject to UBTI.

In the case of ORRI, in most cases there is no liability risk, however, the JOA should be

examined to confirm that this is the case. In order to determine the type of interest, the owner of

record, and other details, the charity should request the legal description of the interest,

ownership records, copies of leases, and a record of royalty payments.

If a donor wishes to receive a charitable deduction for the gift of a mineral interest, he must

obtain a qualified appraisal if the value exceeds $5,000. The charity would sign IRS Form 8283

at the time of the gift, and if it sells or disposes of the property within three years, would file IRS

Form 8282.

Once a gift is accepted, the charity must decide if it will retain the mineral interest or sell it.

From an economic standpoint, the charity can often receive greater value from leasing mineral

interests rather than selling them. However, due to the specialized nature of lease agreements

and their terms, charities should have internal or external expertise (preferably both) to manage

these types of assets.

Partial Interest Rules

As mentioned earlier, a landowner often will separate the surface rights from the mineral rights.

In addition, a mineral interest that is leased for production might be structured as a fractional

royalty interest. The question that arises in considering a charitable gift of this type of asset is

whether or not the gift represents a donor’s entire interest in the property. In order to claim a

charitable deduction for the gift, the donor needs to contribute his entire interest or an undivided

percentage of his entire interest. Otherwise, the “partial interest rule” will prohibit a deduction.

In many cases, a donor might own a fractional interest within a larger royalty interest. A gift

of that interest will be deductible if it is the donor’s entire interest. If a donor owns both the

surface and the mineral rights, he cannot donate just the mineral rights or just the surface rights

and claim a deduction (see Rev. Rul. 76-331). The only exception to this rule is if the value of

the mineral interest is determined to be insubstantial. Also, note that a deduction would be

denied if, immediately prior to a gift, the donor divided the property in which a partial interest

exists in order to create a separate “whole” interest (see Treas. Reg. §1.170A-7(a)(2)(i)).

Gift Options

Mineral interests share some similarity with farmland in that they are assets that are often passed

on to successive generations. Because of their value, not only currently but potentially in the

future, owners of mineral interests are reluctant to part with them. Often mineral interests come

to charity though a bequest. Whether the gift is the result of a bequest or outright, careful

evaluation of the gift is required. Information should be gathered prior to accepting a gift,

whether or not it is retained by the charity. The charity will want to estimate the value of the

interest and identify any issues related to ownership, especially issues of liability and UBTI.

Please see Guidelines for Receiving Gifts of Mineral Properties included in this article for a list

of key questions to explore and a checklist for mineral gift acceptance.

When a donor approaches a charity about using a mineral interest to fund a life income gift, the

charity should conduct the same evaluation of the interest as it would for an outright gift. If the

mineral interest is to be sold, a flip unitrust would be an attractive gift option. While mineral

interests generally can be sold without difficulty, finding a broker for the sale as well as a buyer

might take some time. If the interest is leased and providing current income, this could provide

significant income to the beneficiary in the pre-flip period. A gift annuity could also be

considered, however, a deferred gift annuity would be most appropriate to allow time for the

marketing and sale of the asset prior to the first payment. It also would be advisable to discount

the annuity rate in recognition of the costs of sale. Additionally, there is no assurance that a

mineral interest currently producing would continue to produce at the same level (or even at all)

for the period of a gift annuity payment. Therefore retaining a mineral interest for a gift annuity

comes with considerable risk.

Establishing a net income trust using mineral interests that are retained by the trust is another

possibility. Because it is structured to only distribute net income it is better suited to the

variability in income generated by the mineral interest. Because yield on mineral interests are

generally high, the interest can often generate enough income to reach the full unitrust

percentage.

One issue to consider when serving as trustee of a trust that holds mineral interests is the

fiduciary responsibility to diversify assets. If the mineral interest is the only asset, a case could

be made that the trust is not adequately diversified. Often trusts that hold mineral interest will

also hold other investable assets and therefore provide more diversification.

Valuation

A mineral interest that is not currently producing is considered to have no value for charitable

deduction purposes. This can be a surprise to the owner of the mineral interest who understands

the potential value of the interest, and who might have even been offered a substantial bonus

payment to lease production rights to one or more producers. A charity that holds mineral

interest that are not producing will often carry the interest on their books with a value of $1.00.

Once production has started, the value is generally a multiple of the yearly production value.

This multiple is usually around four, but can be higher in areas of increased attention and

production. This value is merely a “rule of thumb” and can be helpful for the charity in

understanding the value of a potential gift and whether the investment of time and effort is

warranted.

A donor that gives a gift of a mineral interest valued at more than $5,000, and who desires a tax

deduction, will need a qualified appraisal to substantiate the value of the gift. Despite the

accepted “rule of thumb” outlined above, the appraiser typically provides a more extensive

analysis of the production history of the well to determine a value for income deduction

purposes.

Should the Charity Retain the Minerals?

For some charities, there will not be a choice of whether to retain the rights or sell them. For

example, an environmental charity would likely not be interested in holding them, or a charity with

a strict policy against retaining mineral interests would likely seek to sell them as soon as possible.

Fortunately, the market for mineral interests is strong, and the charity should have little problem in

locating a buyer. They could sell the rights directly to a buyer, use a broker, or sell the rights

through auction. Prices vary greatly from area to area, with the areas seeing the most investment

and production typically demanding the highest prices.

Managing mineral interests requires thorough familiarity with local laws. Charities that retain

mineral rights or serve as trustees of life income gifts funded with mineral rights should either have

access to strong internal or external advisors, or require that the mineral interests be sold and the

proceeds invested in a diversified portfolio. Mineral interests can be complex, and considerable

due diligence is required to understand and avoid issues related to ownership.

Mineral interests that are in production and providing royalty payments can provide significant

value if held. Many charities have a policy to hold on to mineral interests when they receive

them by bequest or outright. Some even sever and retain the mineral rights associated with a gift

of property that includes the surface when the surface property is sold by the charity. If the

mineral interests are to be retained in a trust, a net income trust (with or without a make-up

provision) would be most appropriate since income from mineral interests can be highly volatile.

A charity that offers a gift annuity for a gift of a mineral interest that it intends to keep would be

assuming considerable risk due to the variability of royalty payments.

We would like to thank Tim Walton, Assistant Vice President for Real Estate Services at the

Texas A&M Foundation for information used in preparing this article and for sharing his

significant expertise with us.

Case Study #1

Joe and Jane Jones have multiple royalty interests that have supplied them with a nice income during their retirement years. For the next two years, Joe and Jane will be receiving a significant amount of money from an investment which is going to cause them to pay more income tax than they prefer to pay, so they have decided to make a charitable gift to their favorite charity. They have two goals: 1) avoid income and the additional tax it brings, and 2) make a charitable gift to their favorite charity. Joe and Jane know that if they receive the royalty income from the oil and gas company they will owe income tax on the amounts they receive. Joe and Jane know that they can donate their royalty interest to charity, but they do not want it to be on a permanent basis because they expect to need the royalty income after the two-year period is over. How can Joe and Jane avoid the oil and gas royalty income for the next two years without permanently donating the interest to charity? Joe and Jane can make a gift of their royalty interest in a specific property to charity for a specific term. The specific royalty interest is conveyed via a Term Royalty Deed. The charity receives the income for 24 months. The charity will receive a transfer order initiated by the deed transferring the interest to the charity. The charity will carefully review the transfer order to make sure that it is consistent with the lease terms. The charity monitors the royalty checks, making sure that the correct amounts have been paid. After the 24-month period is over, the payor will resume making payments to Joe and Jane. Although Joe and Jane do not receive a tax deduction for their gift, they do avoid the income it would have generated. They also are pleased to be credited with a significant charitable gift by the charity. A gift of this type requires due diligence. The charity would be wise to consult with an oil and gas attorney to understand the various legal issues associated with the gift. If instead of avoiding income for the short term, Joe and Jane wanted to make a charitable gift and receive income, they could establish a charitable remainder trust funded with the royalty interest. Depending on the type of trust, and the expertise of the trustee, the royalty interest might be maintained by the trust, or could be sold an invested to provide lifetime income to the donors.

Case Study #2

Larry Landman meets with a gift planner at a non-profit to discuss donating 36 overriding

royalty interests (ORRI) to the charity. The overriding interests are on non-producing but very

promising oil and gas lands. They are for depths of 100’ and greater than existing producing

properties. Each of the overrides are for 3% and 5% based upon the specific depth of current

production. The future proceeds, if any, would be used to create an endowment for a particular

philanthropic purpose the donor would like to support. Although these overrides are not

producing at this time and will only be booked at $1 value by the charity, significant income in

the future is a real possibility.

The gift planner consults with management of the charity and also oil and gas asset experts and

then explains to the interested donor that the charity will consider such gifts but will need to

review all leases, joint operating agreements (JOA), farmout agreements, draft assignments, etc.

to make sure the charity will not assume any current or future liabilities by accepting the

overrides.

Upon thorough review and due diligence research for each interest, it is determined that most are

acceptable as offered. However, two interests are found to carry proportionate liabilities of the

working interest owner if the working interest owner cannot meet its obligations, as indicated in

the JOA. So the charity concluded that 34 of the overrides have no contractual liabilities and are

acceptable to receive from the donor. The other 2 interests are not because of the potential

obligations and liabilities. The donor gives the 34 ORRIs to the charity, and disposes of the

other 2 ORRI in a different way.

Due diligence is of great importance. Gifts of ORRI and other oil and gas interests can be very

good gifts but it is very important to make sure the charity is fully aware of all general and

special information and factors concerning the interests as well as all obligations and liabilities

associated with the interests.

GUIDELINES FOR RECEIVING GIFTS OF MINERAL PROPERTIES

This document is intended to provide basic information regarding the issues which might be considered when properties containing oil, gas or mineral ownership are offered to a charity. It is not intended to be a treatise on the subject, but is intended to provide a summary of issues which may be of importance. It should not be considered as legal or tax advice.

Definitions

Minerals: This term requires diligent inquiry under state law because each state might define minerals differently. For example, in Texas it has been defined at different times and under different circumstances to refer (1) only to mineral substances other than oil and gas and (2) to mineral substances including oil and gas. As a general rule, the term "minerals” includes all of the property other than the surface of the property, sand, gravel limestone, caliche, and water. The mineral owner has an easement to use the surface of the property to acquire or explore for their minerals. Thus, a mineral owner is entitled to strip mine the surface of the property for coal and lignite. The mineral owner also has the exclusive right to lease the minerals, and receive any and all lease bonus and rental payments (the "executive rights"). The minerals may be divided among any number of owners in fractional interests.

Royalty: A royalty interest is the mineral owner's right to receive a percentage (recited in the oil, gas, and mineral lease) of the proceeds from the sale of oil, gas, or minerals produced from the property, free of any of the costs of production and exploration. Sometimes, a royalty is legitimately charged for its proportionate share of the cost of transportation, treatment, and gathering taxes. The royalty interest may be a part of the mineral interest, or it may be conveyed separately from the mineral interest.

Non-participating Royalty: A non-participating royalty interest, often called an NPRI, is a royalty interest that is carved out of the interest of the mineral interest owner. It entitles the holder to a share of oil and gas production proceeds, but the holder does not have the right to negotiate the terms of a lease or receive lease bonus or rentals.

Working Interest: The owner of a working interest has the exclusive right to exploit the minerals of the land. A working interest owner receives proceeds from the sale of the oil, gas, or other minerals produced from the property, but is responsible for paying his proportionate share of all costs of exploration, drilling, mining, development, operating, marketing and all other costs incident to the production and sale of the oil, gas, and other minerals produced from the lease. Working interest owners are also responsible for all liabilities. The rights and obligations of working interest owners are determined by the terms of an operating agreement.

Overriding Royalty: An overriding royalty is a percentage of the gross production of oil, gas, and other minerals under a lease that is in addition to the usual royalties paid to the mineral owner, free of any and all costs associated with the exploration and production of the well. It is an interest that is carved out of the working interest owner(s) share of the oil and gas. This type of royalty is generally owned by someone other than the owner of the property.

Joint Operating Agreement: An agreement between the working interest owners for the testing and development of a tract of land for oil and gas exploration. Typically, one of the parties is designated as the operator, which is generally the oil company that is primarily responsible for

drilling and producing the well. The operating agreement contains detailed provisions concerning the drilling of the well(s), the sharing of expenses, the method by which working interest owners are required to pay their portion of the expenses associated with the well, penalties for default, and the accounting methods to be utilized. An important function of the operating agreement is the application of restrictions and constraints on the operator, because the operator is the primary decision maker for all operations concerning the well.

Due Diligence Questions

1. Mineral Interest

• What is the amount or percentage of the ownership interest? Title examination might be required to determine the answer to this question.

• Is the mineral interest presently leased? If so, what royalty interest is provided by the lease?

• Does the mineral interest owner also own the executive rights? • Does the mineral interest owner have the right to use the surface of the land? • Are there existing wells producing the mineral interest? If so, what is the

production history?

2. Royalty Interest

• Is the royalty in oil and gas only, or is it also in other minerals? Title examination might be required to determine an answer to this question.

• What is the fraction or percentage of royalty which exists under the lease in effect on the property which creates the royalty interest?

• Does the document creating the royalty interest allow for any of the transportation or compression charges to be assessed against the royalty interest or is it a "free" royalty?

• Is the royalty owner currently receiving any payments, or does the royalty have speculative value only?

• Is the royalty "non-participating?”

3. Overriding Royalty Interest

The same questions stated above apply to an overriding royalty except that overriding royalties frequently cover several leases on various properties, so the title examination issues are often more complicated.

4. Working Interest

An offer of a working interest carries with it several difficult questions that require careful due diligence and use of outside counsel. Because of the associated liabilities and costs, gifts of working interests are typically not accepted by charities.

Checklist

Legal description of mineral interest:

How is interest owned (e.g., individually, jointly, partnership, corporation)?

Mineral Interest:

1. How much is owned (percentage or decimal)? ___________________________

2. Is the interest leased? Yes___ No___

a. Copy of lease ____

3. Is there surface use? Yes___ No___

4. Currently in production? Yes___ No___

a. Approximate yearly income ___________

5. Copy of document creating interest? Yes___ No___

6. Title history? Yes___ No___

Royalty Interest (including Overriding Royalty Interest):

1. Oil and gas only? Yes___ No___; if no, then what?___________________

2. How much is owned (percentage or decimal)?__________________________

3. Currently in production? Yes___ No___

a. Copy of division order ____

b. Approximate yearly income ____

4. Is the interest non-participating? Yes___ No___ a. Copy of JOA if overriding royalty interest ____

5. Copy of document creating interest? Yes___ No___

6. Title history? Yes___ No___

Gift planning items:

1. What type of gift is being considered (e.g., outright, trust, other)?

2. Is a tax deduction sought? Yes___ No___

3. Cost basis _____________

If your institution will retain and manage the interest:

1. Operator Name:

2. Payor(s) Name:

3. Owner (donor) Identification Number (see division order):

4. Lease Number (see division order):

5. Property Plat Map? Yes___ No___

6. Unit Designation Map? Yes___ No___

7. Mineral Owner Report? Yes___ No___

NCPP MINNEAPOLIS

October 17, 2013Glenn Pittsford, Texas A&M FoundationMark Ladendorf, KASPICK & COMPANY

CHARITABLE GIFTS OF

MINERAL INTERESTS

� Opportunities for gifts of mineral interests

� Types of interests that can be given

� Types of gifts that work well for these assets

� Evaluating, accepting, and managing gifts of mineral interests

1Topics

2Widespread Opportunities

Field Production of Crude Oil 3

Source: U.S. Energy Information Administration

Pennsylvania Natural Gas Gross Withdrawals 4

Source: U.S. Energy Information Administration

5

Non-participatingRoyalty Interest

(NPRI)

� Bonus

� Delay Rental

� Royalty Payments

� Shut-in Payments

Oil, Gas,and Mineral

Lease

MineralOwner

SurfaceOwner

JointOperatingAgreement

(JOA)

Operator(WorkingInterest)

OverridingRoyalty

Ownership of Mineral Interests

� Surface estate including minerals

� Mineral estate only

� Royalty interest

� Non-participating royalty interest (NPRI)

� Assignment of royalty payments

� Working interest?

� Overriding royalty

6What Can Be Given?

Most charities would not accept a gift of a working interest

because of liability and UBTI concerns

� To claim a deduction, a donor needs to give his entire interest or an undivided percentage of his entire interest

� If a mineral rights owner also owns the surface, he cannot give one and not the other and get a deduction

� Donor cannot divide property immediately prior to the gift to create a separate “whole” interest

� A fractional interest within a larger royalty interest that is given will be deductible if it is the donor’s entire interest

7Partial Interest Rules

� Outright gift

� Bequest

� Charitable remainder trust

– Net income trust

– Flip trust

– Standard CRT if it includes other assets or if interest will be sold

� Gift annuities and charitable remainder annuity trusts would carry significant risks

� Life estate for gifts of real estate that contain mineral interests carry special rules

8What Types of Gifts Can the Donor Fund?

� A mineral interest that is not producing has no value for charitable deduction purposes

� Once producing, the value is generally a multiple of the yearly production value

– Usually four times the annual production value

– Can be substantially higher in some areas

� Charities should assess if approximate value warrants consideration of acceptance

� If value is more than $5,000, the donor will need a qualified appraisal to substantiate the value of the gift for tax purposes

9Valuation Issues

� Who precisely is your donor?

– How is the asset titled?

– Are there co-owners of the asset?

– What rights do they have?

� What is the level of donative intent?

� Is the donor seeking a charitable deduction?

� What is the donor’s relationship to your institution?

� Are there non-philanthropic motivations?

– Tax or liquidity problem

– Desire to shed administrative burden

– Desire to get rid of a problem asset

10Acceptance Policies and ProceduresUnderstand Your Donor

� How and when was it acquired?

� Does it have clear title, free of liabilities?

� Is it held in a corporation or partnership?What type?

� Are there any restrictions on ownership?

� What type of interest is it?

– Mineral interest

– Royalty interest, including NPRI

– Overriding royalty interest

– Working interest

11Acceptance Policies and ProceduresUnderstand The Gift Asset

� What is the amount or percentage of the ownership interest? Title examination might be required to determine the answer to this question.

� Is the mineral interest presently leased? If so, what royalty interest is provided by the lease?

� Does the mineral interest owner also own theexecutive rights?

� Does the mineral interest owner have the right to use the surface of the land?

� Are there existing wells producing? If so, what is the production history?

12Due DiligenceMineral Interest

� Is the royalty in oil and gas only, or is it also in other minerals? Title examination might be required to determine an answer to this question.

� What is the fraction or percentage of royalty in the lease?

� Does the lease allow for expenses and fees, such as transportation or compression charges, to be deducted from the royalty interest?

� Is the royalty owner currently receiving any payments, or does the royalty have speculative value only?

� Is the royalty "non-participating?”

13Due DiligenceRoyalty Interest or Overriding Royalty Interest

� State laws differ, so it is critical to obtain good local advice regarding mineral interests

� Local counsel should be experienced in mineral law

– Texas has Certified Oil and Gas Attorneys

� Working interests should be avoided

� If overriding royalty interest, be sure to read and understand the JOA to be assured that liability is not shared with interest holder

� Use a checklist to assure all major items are addressed

14Protecting Charity From Risk

� Sell the asset

– Determine what is a reasonable value

– Can be sold through an oil and gas broker, or at auction

– Generally easily sold, especially in high producing areas

� Keep the asset

– Who will manage the asset on an on-going basis?

– Understand expected income

– If in a life income gift, will income produced be sufficient to support payments? If in trust, who will value the interest each year?

15Liquidate or Manage the Assets?

Many charities have a policy to keep all mineral interests,

where others (such as environmental charities) would sell

any donated interests

16

Case Studies

� What are the primary issues you identify?

� What additional questions would you most like to ask?

� What gift options might you explore?

� What fundraising strategy issues or questions do you see?

� What institutional risk issues might arise?

Discussion Questions 17

These cases are derived from actual situations, but they are presented for illustrative purposes only. Based on individual facts and circumstances, your results may differ. The cases do not represent tax or legal advice.

� Joe, a graduate of your university, and his wife Jane recently retired

� Joe sold his share of a business which resulted in a large gain

� They own multiple mineral royalty interests that provide them a reliable income

� They ask you about ideas on limiting their tax burden for the current year

18Case #1

� All the royalties are from mineral interests they own

� They have already maxed out their charitable gifts for the next two years

� They are willing to forgo income in the short term to reduce taxable income

� They are unsure about future income needs and are unwilling to give the mineral interests outright

19Case #1Additional Facts

TermRoyaltyDeed

Case #1—Outcome

� No tax deduction

� Avoided income that otherwise would have been taxed

� Made a significant gift

20

1

2

Charity

3Income for 24 months

Image: SalFalko

Case #1—Life Income Gift Option

2

1

4

5% Net

Income

Unitrust

Charity

Remainder

PaymentsIncome Tax Deduction

Gift of Royalty Interests

3

21

Image: SalFalko

� Larry is an executive with an oil company who has no relationship with your charity

� In a meeting with a gift planner he discusses the possibility of donating 36 royalty intereststo the charity

� No income is currently being producedfrom the royalty interest

22Case #2

� The mineral interests are overriding royalty interests

� Interests are held off shore and are for specific depths

� Each of the overrides are for 3% or 5% based upon specific depth of current production

� In reviewing the JOA, two interests are found to carry proportionate liabilities of the working interest owner if the working interest owner cannot meet its obligations

23Case #2Additional Facts

� 34 override royalty interests are transferred to the charity

� Charity helped find another organization that agreed to take the two interests that carried potential liability

� Charity had access to strong counsel to evaluate JOA and other documents in due diligence process

24Case #2—Outcome

25