characteristics of indian software...

TRANSCRIPT

When Strong partnership became hindrance to growth: An example from Indian Software Industry, 1990-2004

Rakesh/Mishra

AbstractThis paper investigates the impact of changes in technology on the joint venture firms in Indian Information technology (IT) Industry. It has compared the performance of two groups of firms. One group has Joint Venture (JV) firms between Indian business house and foreign technology leader and other has 100% owned Indian firms. The technology change under study is increase in microprocessor power. The study outlines the changes in the microprocessor power and its impact on the strategic environment of the Indian IT Industry. It has looked at the strategic changes that JV firms undertook to negotiate this technology change and its impact on revenue growth and profitability (PAT) of the firms. In the face of fast technology changes Joint venture firms did not grow as well as independent firms. These joint venture companies had realized the attractiveness of software service sector quite early but could not changeover their business focus fast from hardware to software. From the perspective of Indian partners of JVs the study illustrates that strong partnership will become hindrance to growth in case of fast technological changes which throws new opportunities that cannot be pursued within the objectives of partnership.

Introduction to Indian Information Technology IndustryInformation technology (IT) industry in India is comparatively a new industry. From the data in CMIE database we see 7 companies in the area of Information Technology existing in 1990. Some of these were Joint ventures. Joint ventures in Information technology industry were diversification efforts of established business houses of India e.g. Tatas, Birlas and Goenkas. After 1990 a number of new software companies were incorporated every year (table 2). The birth rate of companies picked up pace after 1994 and between 1994 and 1999, 123 new companies were incorporated. Indian software export grew from Rs. 0.3 billion in 1990 to 475 billion in 2002-03 (Nasscom, 2004).Indian software industry is much smaller compared to the global software industry. According to NASSCOM forecasts, the global IT services market is likely to grow from 394.8 billion in 2000 to US$ 700.4 billion by 2005. Total software export from India is three (3) percent of the global software export, which is miniscule.But what has attracted world’s attention is the rate of growth of the industry. Average annual growth rate of exports for ten years from 1991/92 to 2001/02 is 43%. In terms of Indian rupee the export for last five years grew at CAGR (compounded annual growth rate) of 62.3 percent. Domestic software growth rate is 46.8 percent. Also this industry has been export oriented and has grown without much support of domestic software industry, which is unique.It has generated huge employment opportunities for educated youths of India. Software industry has impacted the Indian industry in a deeper way by giving some new and innovative business philosophy like stock options for employee. It has produced an example for other industries that are desperately looking for ways to thrive in globalizing, liberalizing Indian economy.In its report ILO (1997) lauded the emergence of the Indian software industry as a shining example of how third world countries can take advantage of the liberalization of trade practices among nations and emerge as world leaders in some industries using their strength.Evolution of Indian software industry is interesting. In a short history it has shown the clear picture of organizational selection.

Nature of product/ServiceIndian IT Industry developed to meet the domestic IT needs of the country but more importantly software development capability of Indian technical manpower allowed it to supplement the Information technology Industry in US. Initially firms came to meet hardware demand like Tata Unisys, Digital, ICIM Fujitsu etc. But hardware demand started getting met largely by imports after 1996, due to the reduced import duty. There were firms which were fulfilling the software demand in India and overseas. Firms producing software packages in India is negligible. What most of the firms focused on was export of software development services. Due to the country advantage this business became so profitable that most of the firms became primarily focused on providing software services to US and other overseas market. Today is a predominantly service industry providing software development services. It is also trying to provide other service like Business process outsourcing etc to its clients. Hardware products manufacturing is limited to low-tech Personal computer and Printers and met to a large extent by grey market players.

2

Growth of processing power of microprocessorIn 1964 computers heralded into a new era. This became possible due to the Integrated circuits technology which used semiconductors to miniaturize transistors. Now thousands of tiny transistors could be put on small silicon chips. Miniaturization not only made the components take less space, but it also made it faster and economical as far as energy consumption was concerned. These third generation computers saw an increase in the memory up to 2 megabytes (MB) and processing speed of up to 5 MIPS. This increase in processing power made it possible for computers to use operating system to coordinate the working of its various components, CPU printers and other devices. Human operators were no longer needed. Monitors and keyboards were introduced to replace punch cards. These computers were designed as upgradeable. Third generation computers were accompanied by the software that people could use without extensive training. Programming languages like RPG and Pascal were developed to help programming. Computers became cheap and easy to use. These computers found a large role in businesses.Fourth generation of computers started in 1980 and is continuing since then. These computers use very large scale integrated (VLSI) technology and has 200,000 to over 3 million circuits per chip. Since 1980 microprocessors speed has increased from 5 MHz to over 200 MHz and memory capacity has increased from 2MB to 4GB. Cost of processing has been continuously falling for all types of computers Mainframe, Mini and Micro. Cost of performing 100,000 calculations have plunged from several dollars in the 1950s to less than $0.00004 in 1995 and still going down further. Today computers have become household goods. The power of computers that took one large room is now available in a small desktop. These computers have found widespread use in businesses, governments and households. Fourth generation computers lifted the limitation of processing power and storing capacity.This gave a fillip to software demand. Now people could develop software to meet their need without bothering about the processing power of the computers. This fuelled innovation in the software and created a huge demand for services for developing and maintaining the software.

Impact of the technology changeTill 1969 software used to come bundled with the hardware but in late 1960s IBM had realized the huge potential of software and beginning 1st January 1970 IBM started charging for software separately. This invited many software players who could develop software economically for the hardware supplied by the manufacturers. As a result total software industry revenue grew from US$2.5 Bn in 1979 to US$25 Bn in 1985 and continued growing astronomically.Now it was the software that was limiting the use of hardware. Software development was time consuming and labor intensive. The need for programmers who will develop and maintain the information system was increasing rapidly for US government projects and US industry. Information system was becoming a crucial input for the efficiency and effectiveness of firms. The need for programmers outstripped the supply very soon and projects started experiencing delays due to unavailability of programming professionals. With the standardization of job activities, programming languages and hardware environment the technology and skills within the software development became standardized. This made it easy for projects to source people from outside even from other countries (Greenbaum 1976, Kraft 1979). TCS tried to exploit this opportunity by starting its software export in 1974. It

3

also helped TCS meet its export obligations to import hardware. This opportunity of providing onsite programming services grew as high quality human resource became available for programming job. 1980s saw a large number of computer hardware finding its way in India and this increased the availability of trained software programmers.

Firms pursuing IT opportunities with hardware vendor partnership As early as 1960 India was identified as a manufacturing base for mainframe computers by IBM and ICL a British mainframe manufacturer. IBM wanted to develop India as a manufacturing location for its businesses in Eastern hemisphere but due to government’s policy of self-reliance, it did not happen. India lost a big opportunity to East Asian countries like Taiwan, South Korea and Singapore. And it could not develop itself as a hardware manufacturing location ever after. 1980 saw several joint ventures between Indian companies and hardware multinationals. From the data taken from CMIE database we get following companies existing in 1989 in software industry: CMC Ltd., Digital globalsoft Ltd., P S I Data systems Ltd., Tata Infotech Ltd., Tata Sons Ltd. (Tata Consultancy Services), Zensar technologies Ltd, Wipro, International data management Ltd. and Abacus Computers Ltd. Most of these companies were diversification attempts of big established business houses into growing hardware Industry. - Tata Burroughs was established in 1977 which became Tata Unisys Ltd in 1987. 100%

export oriented computer peripheral manufacturer. Unisys being a partner and major customer. Unisys 40%, Tata 40%

- Digital Equipment Corporation (India) Ltd. Incorporated in 1988. Focused on hardware business DEC (US) 40% Hinditron 35%.

- ICIM Fujitsu Ltd. started in 1983 as a JV between International computers (UK), Fujitsu (Japan), and RPG group. Fujitsu ICL was having 40% and RPG group had 40% stake. Focused on producing line printers and mini/micro computers

- PSI Data systems started as an Aditya Birla group company in 1973 to manufacture products for telecom and IT sector. In 1988 group Bull a French hardware company took 26% ownership in equity that increased to 50.35% in 1998. Group bull designs and develops servers and software. Bull was a major investor, Customer and partner. More than half of the business used to come from Bull Corporation.

Firms pursuing IT opportunity Independently- CMC Ltd. came to maintain the IBM computer installation in 1975 under deptt. Of

electronics. Before its divestment in 2001 to Tata Sons Ltd. government of India was majority stakeholder in the company up to 77%. After divestment it is a subsidiary of TCS ltd. and Tata sons holds 51% of its equity.

- Tata Sons Ltd. (Tata Consultancy Services) was pursuing software opportunities. TCS started its software service export in 1974. It was a 100% owned subsidiary of Tata Sons Ltd till 2004. It is the largest software company in India and largest service exporter.

- WIPRO Ltd. Western India vegetable products limited was renamed Wipro ltd. in 1984. Slowly Wipro shifted its focus from other businesses to providing Information technology services globally. Actually the diversification took place in 1980. Initially it was also in manufacturing of hardware for Information technology Industry. But due to market pressure it changed its focus to software services and in 1992 it went global with its global IT services division.

4

Period of confusion and Experimentation in business focus (1990-91)No new companies joined the Industry in 1990. Among the new firms starting in 1991 most of them were focused on hardware business but were niche players. They were collaborating with niche hardware players and do software business related to the hardware partner. Mahindra British telecom and Tata Elxi were Joint Ventures.

Figure 1: New Entrants in 1991 and their business focus

In 1991 Information technology Industry in India IT industry in India was populated with firms having various focuses. Some firms had their origin in hardware business that they had started with collaboration of foreign hardware manufacturers. Though they had changed their focus to exploit the new software opportunity but to a large extent previous business focus was still there. Some of the firms had their origin in the domestic market as management consultants, large company data processing centers, ex-staff of local IT Company. These IT companies were focused on domestic software market. And, there were firms focused on software exports.

Till 1990-91 this confusion remained and experimentation with business focus continued. Looking at the performance of these two clusters in 1990 we see that –

Figure 2: Performance of firms in 1990 Companies Revenue %PAT Business FocusTata Unisys 391.2

(80,310)131.4 Hardware & software (captive

supplier) Digital India 416 -3.89 Hardware ICIM Fujitsu 619.1 1.95 Hardware

Global Tele Ltd Network Engineering and IT ServicesI C D S Ltd. NBFC also in Hotel Business, diversification in Software Mahindra British Telecom Ltd.

Telecom Software and Services

Tata Elxi Ltd. Hardware manufacturer and System Integrator for SGI hardware

Lan Eseda Inds. Ltd. SoftwareRolta India Ltd. Manufactures work servers/ hardware and software.

Computer graphics, mapping and engineering software

5

Companies Revenue %PAT Business FocusTCS 882.1 10.12 Software domestic & ExportInfosys Not Avlbl Software ExportMastek Not Avlbl Software domestic

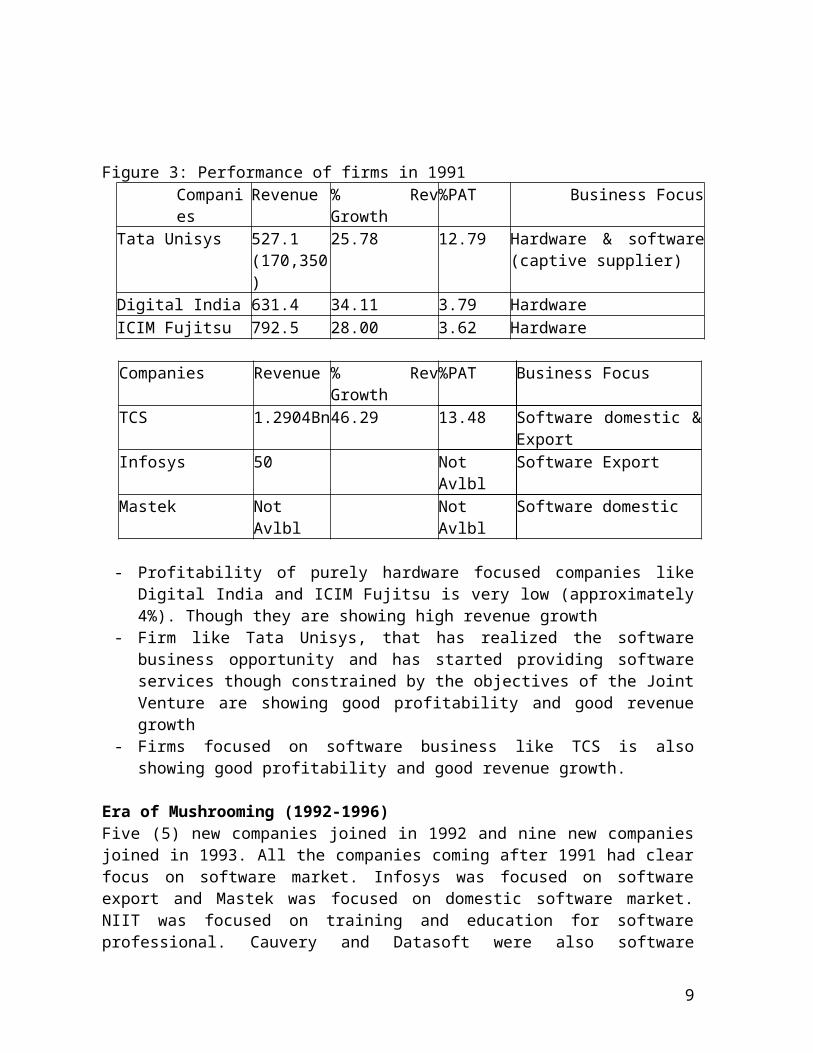

Figure 3: Performance of firms in 1991 Companies Revenue % Rev Growth %PAT Business Focus

Tata Unisys 527.1(170,350)

25.78 12.79 Hardware & software (captive supplier)

Digital India 631.4 34.11 3.79 Hardware ICIM Fujitsu 792.5 28.00 3.62 Hardware

Companies Revenue % Rev Growth %PAT Business Focus

TCS 1.2904Bn 46.29 13.48 Software domestic & ExportInfosys 50 Not Avlbl Software ExportMastek Not Avlbl Not Avlbl Software domestic

- Profitability of purely hardware focused companies like Digital India and ICIM Fujitsu

is very low (approximately 4%). Though they are showing high revenue growth- Firm like Tata Unisys, that has realized the software business opportunity and has

started providing software services though constrained by the objectives of the Joint Venture are showing good profitability and good revenue growth

- Firms focused on software business like TCS is also showing good profitability and good revenue growth.

Era of Mushrooming (1992-1996)Five (5) new companies joined in 1992 and nine new companies joined in 1993. All the companies coming after 1991 had clear focus on software market. Infosys was focused on software export and Mastek was focused on domestic software market. NIIT was focused on training and education for software professional. Cauvery and Datasoft were also software focused. Cauvery got badly affected by the collapse of poonam chambers in Bombay and since then did not recover. Given below is the table showing business focus of entrant firms to the IT industry –

Entrants in 1992All the five firms have clear focus on software. By this time software export business has emerged clear winner

Figure 4: New Entrants in 1991 and their business focus

6

Cauvery Software Engg Systems Ltd.Software. Company got hit by Natural calamity.

Infosys Technologies Ltd. SoftwareMastek Ltd. Software NIIT Ltd. Software trainingDatasoft application software(I) Ltd. Software

Entrants in 1993All the firms have clear focus on software. Henceforth all the firms coming in IT industry were focused on software business and predominantly export business.

Figure 5: New Entrants in 1991 and their business focusD S Q Software Ltd. SoftwareKirloskar Computer Services Ltd. Software

Mindteck(India) Ltd. SoftwareMphasis BFL Ltd. Software financial IndustryS Q L Star International Ltd. Software educationSilverline Technologies Ltd. SoftwareSvam software Ltd. SoftwareVakranghee softwares ltd. Restructured for software. Formerly in financial and

leasingR S Software (India) Ltd. Software

Looking at the business focus of firms joining the industry in 1992 and 1993 we see that between software opportunity and hardware opportunity software export market emerged clear winner by 1992. Unsatisfied export demand was readily available to be tapped. Competition was non-existent. Marketing was not a problem. ‘Bodyshopping’ was a business with little investment, less risk and no-lag period in receiving payments. Indian programmers were well-accepted commodity and all a firm needed to do was to hire programmers. 1980s saw a large number of computer hardware finding its way in India and this had increased the availability of trained software programmers. Small firms had low overhead costs and were more profitable than large companies till the competition increased due to large number of new firms entering the industry. Export of software services was an established money-making value chain. Entrepreneurial firms mushroomed. Between 1992-1996 eighty five (85) new companies joined the industry. Graph below shows the number of firms joining the industry yearwise –

Figure 6: New Entrants trend in Indian IT Industry

7

No. of f irms in the Industry

020406080

100120140160

Year

No.

of C

ompa

nies

No. of f irms in theIndustry

Figure 7: Number of Companies joining the industry year wise

Source: CMIE database

Structure of the IT Industry in 1996 Cluster analysis was performed using Revenue as the first variable keeping the number of clusters as 3(Three). Result of this cluster analysis is presented in the Table below.

Final Cluster CentersCluster

1 2 3Revenue(in Million INR) 11613.1 2803.8 154.2No. of firms in the cluster 1 7 104

Figure 7: Industry structure in 1996

Year of Starting Number of new companies

Total Number of companies

1988 1 11989 6 71990 0 71991 6 131992 5 181993 9 271994 38 651995 37 1021996 28 1301997 10 1401998 15 1551999 58 2132000 35 2482001 12 2602002 0 2602003 -28 2322004 -88 144

8

Industry Structure Graph

0

20

40

60

80

100

120

154 2804 11613

Revenue Centre(in Million INR)

No.

of f

irms

Series1

Source: CMIE database

Looking at the graph we see that more than 90 percent of the firms are of revenue around 1.3% of the largest revenue cluster centre. Less than 7 percent of the firms are of the revenue around 24% of the largest firm clusters. Industry is marked by few large players and a large number of small players which mushroomed to exploit the new staff augmentation opportunity in software services. Most of these small companies are highly profitable. Their profit is much higher than the bigger companies. But the profitability is reducing gradually. It was due to the software project-staffing model of business that these companies followed. This required very little investment and had no entry barrier. The software service industry (project staffing services) industry was giving extra-normal profit without asking for any investment. This attracted a large number of players at a very fast rate. This resulted in competition and reduced profitability of the firms in this segment. Profitability of this group (smallest revenue), which was over 20% in 1994, had fallen to 8% in 1996.

Looking at these two groups we see that hardware business is showing low profitability. Joint venture firms that are hardware focused have shown very low profitability and at times losses. Digital India has remained hardware focused and though they have shown good revenue growth during these years but has shown very poor profitability. In an attempt to exploit the growing software business opportunity 1994 ICIM Fujitsu merged with its subsidiary Fujitsu ICIM Software technologies and starts its software business. Fujitsu stake is raised to 50%. Software operations of the firm is small but profitable compared to the hardware business which big in revenue and experiencing negative profitability. In case of Tata Unisys Indian Partner wants to exploit growing software exports opportunity but American company is primarily focused on selling hardware. As a result Unisys has been able to export hardware to India and uses software export abilities of the company to promote hardware sales overseas. Revenue is earned from hardware and software operations both (Heeks, 1996). In 1996 revenue earned from software business, 1180 Million INR , is double of the hardware business revenue, 530 Million INR. As a result firm has seen profitability of around 10% which is less compared to the pure software focused firms but better than hardware focused firms like Digital India and ICIM Fujitsu. Tata Unisys has been

9

captive supplier of the software services and is not able to pursue the software service opportunity independent of Unisys platform.Firms pursuing IT opportunity independently have done well both in terms of profitability and revenue growth. Profitability (Profit after tax) of the firms have been around 20% and revenue growth around 40%.

10

Graphs below show the trend of profitability and revenue growth during the period of mushrooming (1992-1996).

Figure 8: Revenue growth year wise (1992-1996)

Source: CMIE database

Figure 9: % Profitability year wise (1992-1996)

Source: CMIE database

11

Revenue growth Yearwise

0

1000

2000

3000

4000

5000

6000

7000

1992 1993 1994 1995 1996

Year

Rev

enue

(in M

illio

n IN

R)

TUL

DIGI

ICIM

TCS

INFY

MASTEK

% profitability yearwise

-30

-20

-10

0

10

20

30

40

1992 1993 1994 1995 1996

Year

% P

rofit

aft

er T

ax

TUL

DIGI

ICIM

TCS

INFY

MASTEK

Government’s Policy changes and its effect on Hardware businessThe computer technology which had developed in US as fourth generation computers had affected Indian Industry scenario as well. Once the cost of microprocessor came down Domestic market size ballooned. Computer hardware demand in the domestic market picked up especially after the growth of software export service business. Demand for computers also came from domestic companies like banks financial institutions and lately from households. Computer hardware consumption grew from 2.12 Billion in 1989 to 28.25 Billion in 2003. Computer Hardware production was an emerging area. Computer hardware and peripheral production rose from 2.32 Billion in 1989 to 12.21 Billion in 1997. Though the hardware technology initially affected Indian industry mostly by relocating the manufacturing process of multinationals to India but this momentum was not sustained. Lack of infrastructure, unfavorable duty regimes and lack of incentive hindered the growth of India as a manufacturing location. Post 1997 this demand was mostly met by imports. In fact production reduced from 12.21 Billion in 1997 to 6.67 Billion in 2002 and imports rose from 0.09 billion in 1996 to 17.04 billion in 2003. Whatever growth took place was in the low technology rate of PC and printer manufacturing. Multinational majors are also not interested in manufacturing the complete set of hardware in India, they are more in assembling of the same. Graph below shows the trend in Computer Hardware & Peripheral Production, Imports, Total Supply, Exports and Consumption.

Figure 10: Trend in Computer hardware and Peripheral (1988-2003)

Source: CMIE Database

12

H/W Industry demand

0

5000

10000

15000

20000

25000

30000

35000

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Year

Prod

uctio

n/C

onsu

mpt

ion

In M

illio

n IN

R

P roduction

Imports

TotalSupply

Exports

Consumption

Period of increasing market Concentration (1997-2000)Firms were grouped based on size (using revenue) by the cluster analysis. Revenue (in Million rupees) and profitability (%) of all the firms for each year of the period were taken as input in the SPSS software. Cluster analysis was performed using Revenue as the first variable and profitability (%) as the second variable keeping the number of clusters as 3 (Three). Profitability and revenue growth trend of these clusters were studied during this period. Opposite to the era of mushrooming in this period we find that –

By 1996 no. of firms had increased to 112 compared to 7 in 1990. Most of these being small entrepreneurial type. Rivalry among existing players had become intense. After 1996 smaller companies had become unprofitable. They are somehow earning just enough to meet their expenses. Many of them are incurring losses. With no entry barrier this segment is facing increasing no. of new firms entering the market and increasing competition due to this.

Large companies had grown larger during the mushrooming era. In this era they became more profitable than small companies as well. They continued to grow in their size. After having tested Indian vendors successfully for almost a decade now the clients wanted to do bigger business with these companies in which scale mattered and bigger companies were preferred by client who could scale up in future and act like a partner than mere suppliers of software services (Bhatnagar, 1997).

Reputation also became deciding criteria for indian firms to successfully compete in the market. Size, age and reliable production processes made firms made them more competitive. Thus market became favorable to the big companies (Banerjee, 2000).

Industry Structure in 2000Final Cluster Centers

Looking at the table we see that 90 percent of the firms are of revenue around 1.5% of the largest revenue cluster centre. 8.5 percent of the firms are of the revenue around 24% of the largest firm clusters.

Looking at the two groups we see that hardware business continues to show low profitability. Joint venture firms that are hardware focused have shown very low profitability compared to their software business or independent software companies. Digital India has remained hardware focused till 1999 and though they have shown good revenue growth during 1996-1999 but has shown very poor profitability. It Sells off the hardware business to Compaq India in 1999 and becomes globally focused software company. Keeping in mind the business profile in 2001 the name is changed to Digital globalsoft Ltd. Hewlett Packard is the main customer of the software services and gives 85% of the business of the company. The profitability of the firm doubles to over 20% compared to earlier year profitability after its business gets restructured to focus on software services although on a

Cluster 1 2 3

Revenue 342.9 22463.8 5250.0No. of firms in the group

117 2 11

13

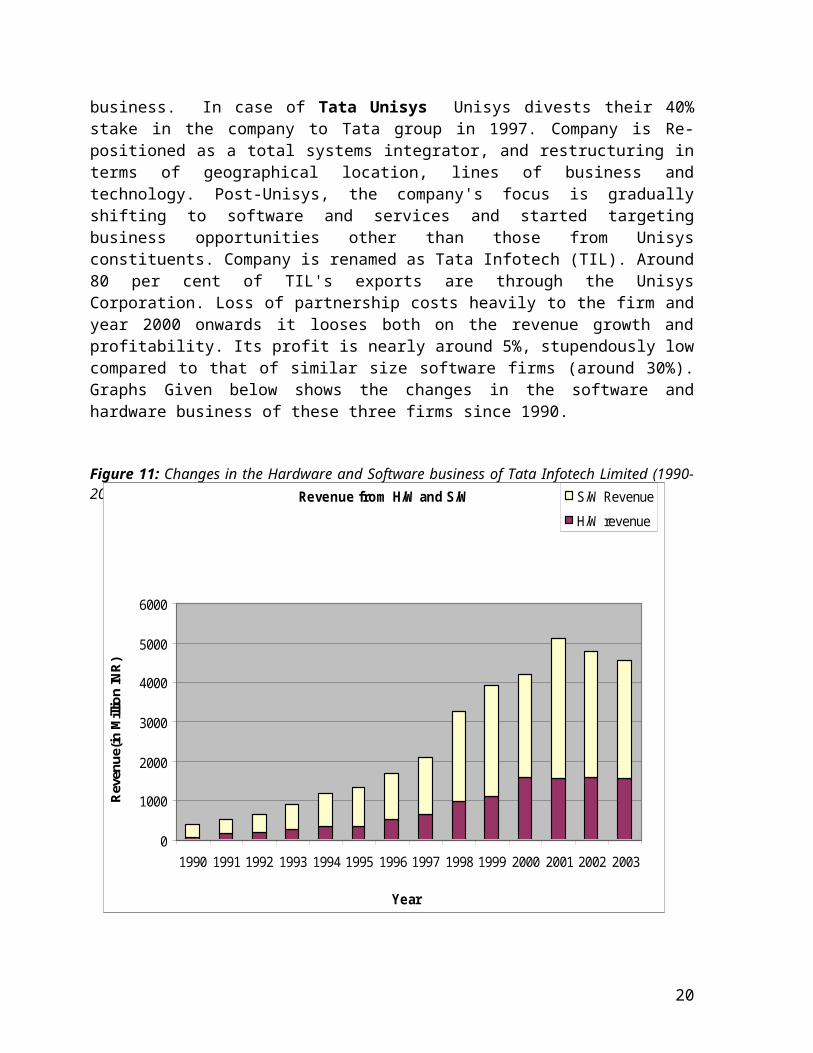

reduced base. ICIM Fujitsu sees growth of its software business and decline of its hardware business and in 1998 its software revenue surpasses its hardware revenue. Hardware continues to be very low in profitability compared to its software business. In 2000 Fujitsu ICIM sells its hardware business and on 16th August 2001 merges with its subsidiary Zensar technologies and focuses completely on software business. In case of Tata Unisys Unisys divests their 40% stake in the company to Tata group in 1997. Company is Re-positioned as a total systems integrator, and restructuring in terms of geographical location, lines of business and technology. Post-Unisys, the company's focus is gradually shifting to software and services and started targeting business opportunities other than those from Unisys constituents. Company is renamed as Tata Infotech (TIL). Around 80 per cent of TIL's exports are through the Unisys Corporation. Loss of partnership costs heavily to the firm and year 2000 onwards it looses both on the revenue growth and profitability. Its profit is nearly around 5%, stupendously low compared to that of similar size software firms (around 30%). Graphs Given below shows the changes in the software and hardware business of these three firms since 1990.

Figure 11: Changes in the Hardware and Software business of Tata Infotech Limited (1990-2003)

14

Revenue from H/W and S/W

0

1000

2000

3000

4000

5000

6000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Year

Rev

enue

(in M

illio

n IN

R)

S/W Revenue

H/W revenue

Figure 12: Changes in the Hardware and Software business of ICIM Fujitsu Limited (1990-2003)

Figure 13: Changes in the Hardware and Software business of Digital Globalsoft Limited (1990-2003)

15

ICIM FUJITSU:Rev from H/W and S/W

0

200

400

600

800

1000

1200

1400

1600

1800

Year

Rev

enue

(in M

illio

n IN

R)

S/W Revenue

H/W Revenue

Digital Globalsoft

0500

10001500200025003000350040004500

Year

Rev

enue

( in

Mill

ion

INR

)

S/W revenue

H/W Revenue

Firms pursuing IT opportunity independently have done well both in terms of profitability and revenue growth. Profitability (Profit after tax) of the firms has been increasing and has hovered around 30%.

Graphs below show the trend of profitability and revenue growth during the period of mushrooming (1997-2000).

Figure 14: Revenue growth year wise (1997-2000) By 1996

Source: CMIE database

Figure 15: % Profitability year wise (1997-2000)

16

Revenue growth yearwise

0

5000

10000

15000

20000

25000

1997 1998 1999 2000

Year

Rev

enue

( in

Mill

ion

INR

)

TUL

DIGI

ICIM

TCS

INFY

MASTEK

% Profitability yearwise

0

5

10

15

20

25

30

35

1997 1998 1999 2000

Year

% P

rofit

afte

r tax

TUL

DIGIICIM

TCS

INFYMASTEK

Era of Offshore development (2001-2003)

Year 2000 was a watershed year for Indian software industry. Slowdown in US economy reduced the IT budgets of the companies. New development project reduced and customer became cost conscious. In this new situation it became necessary to reduce the cost. On-site margin was reduced due to increased competition. Offshore delivery model could solve the price pressure problem. But offshore model was feasible only for large projects and only with reliable suppliers. Companies that were small could not compete for offshore work. Size and Number of years in business determined the reputation (Banerjee, 2000). Only companies like Infosys, Wipro and Satyam and TCS were reputed for overseas clients. Most of the onsite jobs were also linked to the offshore jobs. Smaller companies not only did not get offshore job but lost on the on-site jobs as well (Vandrewala, 2002). Bigger player switched over to new mode of ‘offshore development model’ to beat the billing rate pressure. After having tested Indian vendors successfully for almost a decade now the clients wanted to do bigger business with these companies in which scale mattered and bigger companies were preferred by the client who could scale up in future and act like a partner than mere suppliers of software services (Bhatnagar, 1997). New delivery model made bigger firms more efficient compared to smaller firms who could provide services on-site. Client relationship helped this process further. This situation was better for niche players like SISL, Rolta, Aftek Infosys etc. They continued to have market power due to their specialized offerings or due to their strong parental support in marketing. Companies like Digital globalsoft was little affected due to its captive market, its own parent company. Looking at the two groups we see that ‘reborn’ software is showing interesting trends. By 2000 firms in both the groups have refocused and are completely software business firms. Digital Globalsoft (earlier Digital India) has become globally focused software company. It has tried to diversify its business to other than parent firms and earns close to 15% of its revenue from non-parent business now. Keeping in mind the business profile in 2001 the name was changed to Digital globalsoft ltd. After mergers of parent company digital and compaq in US Hewlett Packard of USA is the major equity holder and customer. More than 85% of its revenue it earns by providing software services to its parent company (CMIE database). This partnership has proved beneficial for the firm and it has shown good growth in its revenue and profitability. The growth in revenue is best among the firms in both the groups. Profitability is also best among the firms in the sample. It is a captive software supplier of the Hewlett Packard USA. This strong partnership is allowing it the expansion of its operation and high profitability. Zensar Technologies (earlier ICIM Fujitsu) is also a joint venture. Today RPG group and Fujitsu services each hold 39% equity in the company. It has also shown good growth in revenue in profitability. In case of Tata Infotech (earlier Tata Unisys) the partnership is over. Lack of partnership is making it difficult to win contracts. Its revenue has stagnated and profitability is showing dismal performance. TIL seems to have met the worst fate earlier partnership restricted from targeting business opportunity other than from Unisys constituents and now when partnership is desired to take work offshore partnership is lost(Afuah, 2001).

17

Looking at the independent software companies we see that bigger firms are doing better than smaller companies. TCS and Infosys the larger two of the set continues to show good revenue growth and profitability compared to the smaller domestic business focused Mastek. It has technical, strategic and marketing alliances with Adobe systems, Aegis analytical, Microsoft, IBM, Oracle and Sun Microsystems etc. It acts as a value-added reseller for many of these companies’ products. It also provides comprehensive set of services and solutions on the partner’s technologies and products. Similarly Infosys In an effort to offer value to its customers has built strong relationships with leading consulting companies, strong regional companies, product companies and niche players. It has built many best-in-class alliances with product and services companies.

Graphs below show the trend of profitability and revenue growth during the period of mushrooming (2001-2004).

Figure 16: Revenue growth year wise (2001-2004)

Source: CMIE database

18

Revenue growth Yearwise

0

10000

20000

30000

40000

50000

60000

70000

2001 2002 2003 2004

Year

Rev

enue

(in M

illio

n IN

R)

TUL

DIGI

ICIM

TCS

INFY

MASTEK

Figure 17: % Profitability year wise (2001-2004)

Source: CMIE database

19

% Profitability yearw ise

0

5

10

15

20

25

30

35

40

2001 2002 2003 2004

Year

% P

rofit

afte

r Tax

TUL

DIGI

ICIM

TCS

INFY

MASTEK

Summary

With time Software export from India was becoming more attractive. Companies in Indian Information Technology industry were trying to change their focus to exploit this opportunity. Software opportunities were de-linked from the hardware manufacturers in 1970 by IBM. Firms that were joint ventures between Indian counterpart and a foreign hardware technology leader also realized the software development competence that India had. With large number of English speaking technical graduates it was easier to make money in software business in India than hardware business. Especially the Indian counterpart was more eager to change over to the software service export business like Tata Unisys. This change in the strategic environment caused by the technology change was “Radical” in the sense that they made the old skills and capabilities obsolete and demanded the firms to make substantial investment for negotiating this change. These changes made the incumbent firms inefficient and favored new entrants with software export focus. The change process got delayed in case of joint ventures as changes were not win-win for both the partners. Incumbent JV firms continued to use second best solution in the changed environment which was agreeable to both the partners. They tried to go into software business slowly. In a market place characterized by high competition these incumbent JV firms started lagging the software export focused entrant’s performance. These Incumbent JVs either went out of market or made the investment to negotiate the change very late. By this time they hade lost the market leadership to the new entrants (Christensen, 1997).Given below is the table showing top ten firms of the Indian Information technology Industry between 1990-2004. It shows the changes in market leadership in the Indian Information Technology Industry.

Rank 1991 1993 1995 1997 1999 2000 2001 2003 20041

Wipro Tata Sons

Wipro Ltd. Wipro Ltd. Tata Sons Wipro Ltd. Wipro Ltd. Tata Sons Tata Sons

2C M C

Wipro Ltd.

Tata Sons Tata Sons Wipro Ltd. Tata Sons Tata Sons Wipro Ltd. Wipro

3Tata Sons C M C

G T L Ltd. G T L Ltd. N I I T Ltd.

Infosys Technologies

Infosys Technologies

Infosys Technologies

Infosys Technologies

4Zensar Zensar Digital N I I T Ltd. G T L Ltd. N I I T Ltd.

Satyam Computer

Satyam Computer

Satyam Computer

5Digital Digital Zensar Digital

Pentamedia Graphics Ltd.

Satyam Computer G T L Ltd. C M C Ltd. C M C Ltd.

6Tata Infotech

Tata Infotech N I I T C M C Ltd.

Infosys Technologies G T L Ltd. N I I T Ltd.

Mahindra-British Telecom

Mahindra-British Telecom

7I C D S G T L C M C

Tata Infotech Tata Infotech

D S Q Software Ltd.

Pentasoft Technologies G T L Ltd.

I-Flex Solutions

8P S I Data

N I I T Ltd.

Tata Infotech

Hexaware Technologies

Satyam Computer

Hexaware Technologies

Pentamedia Graphics Ltd.

I-Flex Solutions

Digital Globalsoft

9Lan Eseda I C D S

Lan Eseda

Pentamedia Graphics Ltd.

Hexaware Technologies C M C Ltd. C M C Ltd. Tata Infotech

Tata Infotech

10

G T L Lan Eseda I C D S

Siemens Information Systems C M C Ltd. Tata Infotech Tata Infotech Digital

Polaris Software

Figure 18: Top 10 Companies (Revenue) of Indian Software IndustrySource: CMIE database

20

REFERENCES “The International Computer Software Industry,” Oxford University Press, 1995Abernathy, W. & Clark, K.B., “Mapping the winds of creative destruction”, Research Policy,

1985, 14. Abernathy, W. J., The productivity Dilemma, Roadblock to innovation in Automobile

Industry, Baltimore, John Hopkins University, 1978. Afuah, A., Dynamic Boundaries of the firm, Academy of Management Journal, 2001,44.Allen, T., Managing the flow of technology, Cambridge, MA: MIT Press, 1984.Amit, Raphael and J. H. Schomaker Paul (1993) “Strategic Assets and Organizational Rent,”

Strategic Management Journal, 14(1), 33-46. Andrews, Kenneth R. (1971) The Concept of Corporate Strategy. Homewood, Illinois: Dow-

Jones Irwines. Ansoff, H. I. (1965) Corporate Strategy: An Analytical Approach to Business Policy for

Growth and Expansion. New York: McGraw Hill.Ariyawardana, Anoma, ‘Sources of competitive advantage and firm performance: The case of

Sri Lankan value-added Tea producers’, Asia Pacific Journal of Management, 20, 2003, 73-90

Arora and Arunachalam, ‘The globalization of software: The case of the Indian Software Industry, A report submitted to the sloan foundation by Carnegie Mellon university’, 1998

Astley, W. G., “The two ecologies: Population and community perspectives on organizational evolution.”, 1985, 30.

Athanassopoulos, A. D. (2003)”Strategic Groups, Frontier Benchmarking and Performance Differences: Evidence from the UK Retail Grocery Industry,” The Journal of Management Studies, 40(4), 921-953.

Balakrishnan S and Wernerfelt B, ‘Technical change, Competition and Vertical Integartion’, SMJ 1986, Vol. 7

Banerjee, Abhijit and Duflo esther(2000), “Reputation effects and limits of contracting: A study of the Indian software Industry”, The Quarterly Journal of Economics,

Barley, S.R., “Technology as an occasion for structuring: Evidence from observations of CT scanners in radiology departments.”, 1986, 31.

Barnard, C.C., The functions of the Executive. Cambridge, MA: Harvard University Press.1938.

Barnett, W. P., & Carroll, G.R., “Competition and mutualism among early telephone companies.”, ASQ,1987, 32.

Barnett, W.P., “The Organizational ecology of a Technological System”, ASQ, 1990, 35.Barney, J. B. and Hoskisson, R. E., ‘Strategic Groups: Untested Assertions and Research

Proposals’, Managerial and Decision Economics, Vol. 11, 3, 1990 Barney, J.(1991), ‘Firm resources and sustained competitive advantage’, Journal of

Management, 17, 771-92Barrett, C. R., “Microprocessor Evolution and Technology Impact”, ieeexplore.ieee.org/iel4/

6147/16441/00760219.pdf?arnumber=760219Bedeian, Arthur G. (1990) “Choice and Determinism: A Comment,” Strategic Management

Journal, 11, 571-573.Bhatnagar, S.C. and Madan, Shirin 1997), “Indian Software Industry: moving towards

maturity”, Journal of Information Technology, 12

21

Bhatnagar, S.C. and Madan, Shirin 1997), “Indian Software Industry: moving towards maturity”, Journal of Information Technology, 12

Bingham, F.G. and Quigley, C.J., “A team approach to new product development”, Journal of Consumer Marketing, Vol. 6, No. 4, Fall 1989, pp. 5-14

Blois, K. J., The journal of Industrial Economics, Jul. 1972 Vol. 20, No 3Boehm, B.W. (1973), ‘Software and its impact: a quantitative assessment. Datamation, May

1973, 48-50.Bond, E.U., Houston, M.B.(2003),”Barriers to Matching New technologies and Market

Opportunities in Established Firms”, The Journal of Product innovation Management, Vol. 20.

Breschi, S & Lissoni, F., & Malerba, F.,“Knowledge Proximity and technological Diversification”, 1998, CESPRI, ISE Research Project.

Bresnahan, Timothy, F. and Greenstein, Shane, “Technological Competition and the Structure of the Computer Industry”, The Journal of Industrial Economics, 1999, Vol. 47, No. 1.

Brittain, J. and Freeman, J., “Organizational proliferation and density-dependent selection.” In J.R. Kimberly and R.H. Miles (eds.), The Organizational life cycles, San Francisco: Jossey-Bass, 1980.

Burgelman, R. A.,”A Process Model of Strategic Business Exit: Implications for an Evolutionary Perspective on Strategy”, Strategic Management Journal, 1996, Vol. 17 pp. 193-214.

Burns, T., & Stalker, G.M., The management of Innovation. 2nd Ed. London: Tavistock. 1966.C. Carl pegels, Chandra Sekar, ‘Determining Strategic Groups Using Multidimensional

Scaling’, Interfaces 19:3 May-June 1989, 47-57Carreira, C. & Teixeira, P., “Technological Change, Productive Efficiency and Industrial

Dynamics: An Evolutionary Model”, 2001Chakraborty, Chandana and Jayachandran C, ‘Software Sector: Trends and Constraints’,

Economic and Political weekly, August 25-31, 2001Chandler, A., Strategy and Structure. Cambridge, MA: MIT Press,1962. Chang-Wook Kim and Keun Lee(2003),”Innovation, technological regimes and

organizational selection in Industry evolution: a ‘history friendly model’ of the DRAM Industry”, Industrial and Corporate Change, 12(6), 1195-1221.

Child, J. (1972), “Organizational Structure, Environment and Performance: The Role of Strategic Choice, “ Sociology, 63(1), 2-22

Child, J., “Organization structure, environment and performance.”, Sociology, 1972, 6.Christensen, C, The Innovator’s Dilemma, HBS Press, 1997Christensen, C.M. & Rosenblum, R.S., “Explaining the attacker’s advantage: Technological

paradigms, organizational dynamics, and the value network.”, Research Policy, 1995, 24. Clark, K.B. & Fujimoto, T., The management of New product development: The case of

worldwide automobile industry. Cambridge, Mass. Harvard Business school Press, 1992.CMIE databaseCoccia, Mario,”A New approach for measuring and classifying technological change

intensity”, Paper presented at DRUID summer conference 2004.Cool, K. O. and Schendel, D. ‘Strategic Group formation and performance: The case of the

U.S. Pharmaceutical Industry’, Management Science, Vol. 33, No. 9, 1987Cyert, R.M. and March, J.G., A behavioral theory of firm, Englewood, Cliffs, N.J., Prentice

Hall, 1963.

22

Damanpour, F.(1991),”Organizational Innovation: A Meta-Analysis of effects of Determinants and Moderators”, Academy of Management Journal, Vol. 34, No. 3, 555-590.

Dess, Gregory G. and Davis, Peter S., ‘Porter’s Generic Strategies as Determinants of Strategic group membership and Organizational Performance’, SMJ, Vol. 27 No. 3, 1984, 467-488

Dickson, P.R.(1996), “Toward a general theory of competitive rationality”, Journal of Marketing, January, Vol. 56, pp. 69-83.

Dranove, David and Peteraf, Margaret and Shanley, Mark, ‘Do Strategic Groups Exist? An Economic Framework for Analysis’, SMJ, 19: 1998, 1029-1044

Dyker, David, “The Computer and Software Industries in the East European Economics. A Bridgehead to the Global Economy?”, Europe-Asia Studies, 1996, Vol.48, No. 6.

Edvardsson, bo, Haglund, L., Mattson, J.(1995), “Analysis, planning, improvisation and control in the development of new services”, vol. 6, pg. 24

Feka, V., Xouris, D., Tsiotras, G., ‘Mapping strategic groups: an international example’, The Journal of Business & Industrial Marketing. Santa Barbara: 1997. Vol. 12, Iss. 1; pg. 66

Fiegenbaum, A. and Thomas H., ‘Strategic Groups and performance: The U.S. Insurance Industry’, 1970-84, SMJ Vol. 11(1990) 197-215

Fiegenbaum, A. and Thomas, H., ‘Strategic groups as reference groups: Theory, modeling and Empirical examination of Industry and competitive Strategy’, SMJ, Vol. 16, 1995

Fiegenbaum, Avi, Sudharshan, D., Thomas H., ‘The concept of Stable Strategic Time Periods in Strategic Group Research’, Managerial and Decision Economics, Vol. 8, 1987

Flamm, Kenneth, “Technological Advance and Costs: Computers versus Communications” in Robert C. Crandall and Kenneth Flamm eds., Changing the rules: Technological change, International competition and regulation in communications. Washington DC; Brookings Institution Press, 1989, pp. 13-61.

Fombrun, C. J. and Zajac, E. J., ‘Structural and Perceptual influences on Intraindustry Stratification’, AMJ Vol. 30 No. 1, 1987

Gadrey, J., Gallouj, F., Weinstein, O.(1995), New modes of Innovation”, International Journal of Service Industry Management, Vol. 6 No.3 pp. 4-16.

Gallouj, F.(1998), “Innovating in reverse: services and the reverse product cycle”, European Journal of innovation Management, Vol. 1.

Geels, F. W.,”Technological transitions as evolutionary reconfiguration processes: A multi-level perspective and a Case Study”, Paper presented at Nelson and Winter conference 2001, Denmark.

Ghemawat, P. (1998), “Commitment The Dynamic of Strategy”, New York: The Free Press Ginsberg, A. (1988), “Measuring and Modeling Changes in Strategy: Theoretical Foundation

and Empirical Direction,” Strategic Management Journal, 9, 559-575. Greebaum, J. (1976),”Division of labour in the computer field”, Monthly Review,

July/August, 40-55.Hambrick, D.C. and Mason P.A. (1984), ”Upper echelons: The Organization as a reflection of

its top Managers,” Academy of Management Review, 9(2) 193-206. Hannan, M.T. and Freeman J, ‘Organizational Ecology’ Harvard university press, 1993Harrigan, K. R., ‘An Application of clustering for Strategic Group Analysis’, SMJ Vol. 6,

1985, 55-73

23

Haveman, H. A. (1992), “Between a Rock and a Hard Place: Organizational Change and Performance under Conditions of Fundamental Environmental Transformation,” Administrative Science Quarterly, 37, 48-75.

Heeks, R. (1996), “India’s Software Industry: State Policy, Liberalisation and Industrial development”, New Delhi: Sage Publications

Henderson, R. & Clark, K.B., “Architectural Innovation: The reconfiguration of existing product technologies and the failure of established firms”, ASQ, 1990, 35.

Henderson, R., “Underinvestment and incompetence as responses to radical innovation: evidence from the photographic alignment equipment industry”, Rand Journal of economics,1993, 24.

Hollander, Samuel. (1965), “The sources of increased efficiency: A study of Du Pont rayon plants.”, Cambridge, MA: MIT Press.

Hrebiniak, L.G. and Joyce W.F. (1985), “Organizations Adaptation: Strategic Choice and Environmental Determinism,” Administrative Science Quarterly, 30, 336-349.

http://www.digitalglobalsoft.comhttp://www.nbogroup.com/articles/leader2000_02.htmhttp://www.softwarehistory.org/index.html.Hultén, Staffan and Dattée, Brice and Hmimda, Nassef,”Do events matter? A combination of

a simulation and an event analysis of the evolution of the microprocessor industry.”, 2004, Paper presented at DRUID summer conference 2004.

Hunt S.D. and Morgan, R.(1995), “The comparative advantage theory of competition”, Journal of Marketing, April, Vol. 59, pp. 1-15.

Hunt, S.D. and Morgan, R.(1996), “The Resource-advantage theory of competition: dynamics, path-dependencies and evolutionary dimensions”, Journal of Marketing, October, Vol. 61, pp. 74-82.

Hunt, S.D.(2000) A general theory of competition, Sage Publications, Inc., Thousand Oaks, California.

ILO report (1997) http://www.ilo.org/public/english/bureau/inst/papers/1997/dp96/Jayant Sinha, ‘Interview with Jayant Sinha’, Businessline Feb 15 2004Jorgenson, Dale, W., “Information Technology and the U.S. Economy”, The American

Economic Review, 2001, Vol. 91. Karasek, R.A., Jr., “Job demands, Job decision latitude, and mental strain: Implication for job

redesign.” ASQ, 1979, 24. Kim, C.W., & Lee, K., “Innovation, technological regimes and organizational selection in

industry evolution: a ‘history friendly model’ of the DRAM industry”, Indiautrial and Corporate Change, 2003, 12.

Kim, Dong-Jae & Kogut, Bruce, “Technological Platforms and Diversification”, Organizational Scince, 1996, Vol. 7, No. 3, Special Issue Part 1 of 2: Hypercompetition (May – Jun. 1996), 283-301.

Klepper, S. (1996),”Entry, exit, growth, and innovation over the product life cycle,” American Economic Review, 86 (3), 562-583.

Klepper, Steven and Graddy, Elizabeth (1990),”The Evolution of New Industries and the Determinants of Market Structure,” Rand Journal of Economics, Spring 1990, 21(1), 27-44.

Kotler, P, ‘Marketing Management’ 11th Ed. Prentice Hall

24

Kraft, P. (1979), ‘The industrialization of computer programming: from programming to ‘software production’. In: Case studies on the labor process, A. Zimbalist(ed). Monthly review Press, New York, 1-17.

Krishnan Thiagarajan,”Frontline software companies: Challenges in going beyond the billion” Businessline. Chennai: Mar 21, 2004

Kyung Hwan Baik, Sanghack Lee. ‘Strategic groups and rent dissipation’, Economic Inquiry. Vol. 39, Iss. 4; pg. 672.

Lee, J., Lee, K., Rho, S., ‘An Evolutionary perspective on Strategic Group Embergence: A genetic Algorithm-based model’, SMJ 23, 2002

LU, Chin-Shan and Marlow, ‘Strategic groups in Taiwanese liner shipping’, Maritime Policy Management, 1999, Vol 26 No.1.

MacCormack, A., Verganti, R.(2003),”Managing the Sources of Uncertainty: Matching Processand Context in Software Development”, The Journal of Product innovation Management, Vol. 20.

Mahoney, J.T. and Pandian J.R.(1992), “Resource Based View Within the Conversation of Strategic Management,” Strategic Management Journal, 13(5), 363-380.

March, J. G. & Simon, H.F., Organizations. New York: Wiley.1958. Marlin, Dan, Huonker, J W and Minghe, Sun, ‘An Examination of the relationship between

strategic group membership and Hospital performance’, Health care management Review: 2002:27(4)

Martin, C. R., Horne, D.A.(1993),”Services innovation: Successful versus Unsuccessful Firms”, International Journal of Service Industry Management, Vol. 4, No. 1.

Mascrenhas, B., ‘Strategic Group Dynamics’, AMJ: 1989 vol. 32, No. 2.McDonald, R.E., Srinivasan, N.(2004),”Technological innovations in hospitals: what kind of

competitive advantage does adoption lead to?”, International Journal of Technology Management, Vol. 28, No. 1 pp. 103-117.

Mcgee, J. and Thomas H., ‘Strategic Groups: Theory, Research and taxonomy’, SMJ Vol. 7(1986) 141-160

McNamara, Gerry M, Luce, A. R. and Tompson, G. H., ‘Examining The effect of complexity in Strategic Group knowledge structures on firm performance’, SMJ 23: 153-170(2002)

Mehra, Ajay, ‘Strategic Groups: A Resource-based approach’, Journal of Socio-Economics, 10535357, Winter94, Vol. 23, Issue 4

- Mismanaged trade? “Strategic policy and the semiconductor industry” Washington, DC: Brookings Institution Press, 1996

Mitchell, W., “Whether and when? Probability and timing of incumbents’ entry into emerging industrial subfields.”, Administrative Science Quarterly, 1989, 34.

Moore, 1997, “An update on Moore’s law.” Speech Intel corporation, Santa Clara, CA, September 30, 1997.

Moore, W.L., “New product development practice of Industrial Marketers”, Journal of Product Innovation Management, Vol. 4 No. 1, Mar 1987, pp. 6-20.

Mowery, D.C., International collaborative ventures in US manufacturing. Cambridge, MA: Ballinger.1988.

Nair, Anil and Kotha, Suresh, ‘Does group membership matter? Evidence from the Japanese steel industry’, SMJ Vol. 22 Iss. 3, 2001

Nath Deepika and Thomas S. Gruca, ‘Convergence across alternative methods for forming Strategic Groups’, SMJ, Vol. 18:9 1997, 745-760

NCPA, “Technology and Economic growth in Information Age”, 1998

25

Nelson, R. & Winter, S., An evolutionary theory of economic change. Cambridge, MA, Harvard University Press.

Newman, H. H., ‘Strategic Groups and the Structure-Performance Relationship’, The Review of Economics and Statistics, Vol. 60, No. 3, 1978

Noble, D.F., The forces of Production: A Social History of Industrial Automation. New York: Knopf. 1984.

Nygaard, Stian,”Emerging Technology and Evolution of Industry: The case of Fuel Cell Technology”, Paper presented at DRUID Winter conference 2004.

Panayides Photis M., ‘Identification of Strategic groups using relationship Marketing criteria: A cluster Analytic Approach in Professional Services’. Service Industries Journal, Apr2002, Vol. 22 Issue 2, p149, 18p

Pavitt, keith,”Technologies, Products and Organization in the Innovating Firm: What Adam Smith tells us what Joseph Schumpeter doesn’t”, 1998.

Perrow, C.C., “A framework for the comparative analysis of organizations.” Americal Sociological Review, 1967, 32.

Peteraf, Margaret and Shanley, Mark, ‘Getting to Know You: A theory of Strategic Group Identity’, Strategic Management Journal, Vol. 18(Summer Special Issue) 1997, 165-186.

Pfeffer J. and Salancik G. R.(1978), “The External Control of Organizations: A Resource Dependence Perspective” New York: Harper and Row.

Porter, M.E. (1980) Competitive Strategy. New York: Free PressPorter, M.E. (1981),”The Contributions of Industrial Organization to Strategic Management”,

Academy of Management Review, 6(4).Quinn, J. B.(1985), “Managing innovation: controlled chaos”, Harvard Business review.Rathmell, J.R., Marketing in service sector, Winthrop, Cambridge, 1974Reger, R. K. and Huff, A. S., ‘Strategic Groups: A cognitive perspective’, SMJ Vol. 14 (1993)

103-124.Reinganum, J. F., ‘Uncertain innovation and persistence of monopoly’, American Economic

Review, 1983, 73. Riel A.C.R, Lemmink J., Ouwersloot, H.(2004), “High Technology Service Innovation

Success: A Decision-Making Perspective”, The Journal of Product Innovation Management, Vol. 21, pp. 348-359.

Robbins, H.B., Organization theory, Prentice Hall of India, 1999Schumpeter, J.A., The Theory of Economic development. Cambridge, MA: Harvard

University Press.1934.Semiconductors(2000), “On International Technology Roadmap for semiconductors (2000)”

http://public.itrs.net/

Shainesh, G.(2004), “Understanding buyer behavior in software services – Strategies for Indian firms”, International Journal of Technology Management, Vol. 28.

Simons, K.L., “Information technology and Dynamics of Firm and Industrial Structure: The British IT consulting industry as a Contemporary specimen”, Paper presented at DRUID summer conference 2002.

Skaggs, B. C. & Droege, S.B., “The Performance Effects of Service Diversification by Manufacturing Firms”, Journal of Managerial Issues, 2004,Vol. 16 Iss. 3.

Software History website – Software History website – http://www.softwarehistory.org/index.html.Special Software report, India Infoline.com

26

Stanford software Industry project - http://www.stanford.edu/group/scip/sirp.htmlStiroh, Kevin J., “Information Technology and the U.S. Productivity Revival: What Does the

industry data Say?”, Federal reserve Bank of New York Staff Report No. 115, December 2000.

Stonier, T., “The Impact of Microprocessor on employment”, Employee Relations, 1979, Vol. 1 Issue 4, p27, 2p.

Taylor, F. W., 1911, Principles of scientific management. New York: Harper & Row. Therese M. Flaherty (1980),”Industry Structure and Cost Reducing Investment”,

Econometrica, 48, 187-209. Thomas, H. and Pollock T., ‘From I-O economics’ S-C-P paradigm through Strategic groups

to competence-based competition: Reflections on the puzzle of competitive strategy’, British journal of management, vol 10, 1990, 127-140.

Thomas, H. and Venkataraman N., ‘Research on Strategic Groups: Progress and Prognosis’, Journal of Management Studies 25:6 November 1988

Thomson, J. D. (1967), Organizations in Action: Social Science Bases of Administrative Theory. New York: McGraw-Hill.

Tripsas, M., “Unraveling the process of creative destruction: Complementary assets and incumbent survival in the typesetter industry.”, Strategic management Journal, 1997, 18.

Tushman, M. L. & Anderson, P., ‘Technological discontinuities and organizational environment’, ASQ, 1986, 31.

Vandrewala, P., The Financial Express, Wednesday, January 02, 2002Verspagen, B., “Strcutural change and Technology. A long View”, Paper presented at DRUID

summer conference 2002.W. Edward Steinmueller "The International Computer Software Industry," Oxford University

Press, 1995).Wade, J., “Dynamics of organizational Communities and technological Bandwagons: An

Empirical Investigation of Community Evolution in the Microprocessor Market”, Strategic Management Journal, 1995, Vol. 16, pp. 111-133.

Wiggins, R. R and Ruefli, T. W., ‘Necessary Conditions for the predictive validity of Strategic Groups: Analysis without reliance on clustering techniques’, AMJ 1995, vol. 38, No. 6, 1635-1656

Williamson, O.E., Markets and Hierarchies. New York: Free Press.1975. www.bull.comwww.cmc.comwww.digitalglobalsoft.comwww.psidata.comwww.softwarehistory.org

www.tcs.comwww.wipro.comZaheer , A. and Venkataraman N. , ‘Relational governance as interorganizational strategy’,

SMJ June 1995, Vol. 16. Zajac, E.M. and Shortell, S.M. (1989),”Changing Generic Strategies: Likelihood, Direction

and Peformance Implications,” Strategic Management Journal, 10, 413-430.

27