chapter4 how we got the solutions

TRANSCRIPT

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 1/52

CHAPTER 4

Discounted Cash Flow Valuation

Multiple Choice Questions:

I. DEFINITIONS

ANNUITY

a 1. An annuity stream of cash flow payments is a set of:a. level cash flows occurring each time period for a fixed length of time. b. level cash flows occurring each time period forever.c. increasing cash flows occurring each time period for a fixed length of time.d. increasing cash flows occurring each time period forever.e. arbitrary cash flows occurring each time period for no more than 10 years.

Difficulty level: Easy

ANNUITIES DUE

e 2. Annuities where the payments occur at the end of each time period are called _____ , whereas _____ refer to annuity streams with payments occurring at the beginning of each time period.

a. ordinary annuities; early annuities b. late annuities; straight annuitiesc. straight annuities; late annuitiesd. annuities due; ordinary annuitiese. ordinary annuities; annuities due

Difficulty level: Easy

PERPETUITY

c 3. An annuity stream where the payments occur forever is called a(n):

a. annuity due. b. indemnity.c. perpetuity.d. amortized cash flow stream.e. amortization table.

Difficulty level: Easy

STATED INTEREST RATES

a 4. The interest rate expressed in terms of the interest payment made each period is called the _____ rate.

a. stated annual interest

b. compound annual interestc. effective annual interestd. periodic intereste. daily interest

Difficulty level: Easy

EFFECTIVE ANNUAL RATE

c 5. The interest rate expressed as if it were compounded once per year is called the _____ rate.

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 2/52

a. stated interest b. compound interestc. effective annuald. periodic intereste. daily interest

Difficulty level: Easy

ANNUAL PERCENTAGE RATE

b 6. The interest rate charged per period multiplied by the number of periods per year is called the _____ rate.

a. effective annual b. annual percentagec. periodic interestd. compound intereste. daily interest

Difficulty level: Easy

II. CONCEPTS

ORDINARY ANNUITY VERSUS ANNUITY DUE

c 7. You are comparing two annuities which offer monthly payments for ten years. Bothannuities are identical with the exception of the payment dates. Annuity A pays on the

first of each month while annuity B pays on the last day of each month. Which one of the following statements is correct concerning these two annuities?

a. Both annuities are of equal value today. b. Annuity B is an annuity due.c. Annuity A has a higher future value than annuity B.

d. Annuity B has a higher present value than annuity A.e. Both annuities have the same future value as of ten years from today.

Difficulty level: Medium

UNEVEN CASH FLOWS AND PRESENT VALUE

b 8. You are comparing two investment options. The cost to invest in either option is thesame today. Both options will provide you with $20,000 of income. Option A pays fiveannual payments starting with $8,000 the first year followed by four annual payments

of $3,000 each. Option B pays five annual payments of $4,000 each. Which one of thefollowing statements is correct given these two investment options?

a. Both options are of equal value given that they both provide $20,000 of income. b. Option A is the better choice of the two given any positive rate of return.c. Option B has a higher present value than option A given a positive rate of return.d. Option B has a lower future value at year 5 than option A given a zero rate of return.e. Option A is preferable because it is an annuity due.

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 3/52

a 9. You are considering two projects with the following cash flows:Project A Project B

Year 1 $2,500 $4,000Year 2 3,000 3,500Year 3 3,500 3,000Year 4 4,000 2,500

Which of the following statements are true concerning these two projects?I. Both projects have the same future value at the end of year 4, given a positive rate of

return.II. Both projects have the same future value given a zero rate of return.III. Both projects have the same future value at any point in time, given a positive rate of

return.IV. Project A has a higher future value than project B, given a positive rate of return.a. II only b. IV onlyc. I and III onlyd. II and IV onlye. I, II, and III only

Difficulty level: Medium

PERPETUITY VERSUS ANNUITY

d 10. A perpetuity differs from an annuity because:a. perpetuity payments vary with the rate of inflation. b. perpetuity payments vary with the market rate of interest.c. perpetuity payments are variable while annuity payments are constant.d. perpetuity payments never cease.e. annuity payments never cease.

Difficulty level: Easy

ANNUAL PERCENTAGE RATE

e 11. Which one of the following statements concerning the annual percentage rate iscorrect?

a. The annual percentage rate considers interest on interest. b. The rate of interest you actually pay on a loan is called the annual percentage rate.c. The effective annual rate is lower than the annual percentage rate when an interest rate

is compounded quarterly.d. When firms advertise the annual percentage rate they are violating U.S. truth-in-

lending laws.e. The annual percentage rate equals the effective annual rate when the rate on an

account is designated as simple interest.

Difficulty level: Easy

INTEREST RATES

b 12. Which one of the following statements concerning interest rates is correct?a. The stated rate is the same as the effective annual rate. b. An effective annual rate is the rate that applies if interest were charged annually.c. The annual percentage rate increases as the number of compounding periods per year

increases.

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 4/52

d. Banks prefer more frequent compounding on their savings accounts.e. For any positive rate of interest, the effective annual rate will always exceed the annual

percentage rate.

Difficulty level: Easy

EFFECTIVE ANNUAL RATEc 13. Which of the following statements concerning the effective annual rate are correct?

I. When making financial decisions, you should compare effective annual rates rather than annual percentage rates.

II. The more frequently interest is compounded, the higher the effective annual rate.III. A quoted rate of 6% compounded continuously has a higher effective annual rate

than if the rate were compounded daily.IV. When borrowing and choosing which loan to accept, you should select the offer with the

highest effective annual rate.a. I and II only b. I and IV onlyc. I, II, and III only

d. II, III, and IV onlye. I, II, III,and IV

Difficulty level: Medium

CONTINUOUS COMPOUNDING

d 14. The highest effective annual rate that can be derived from an annual percentage rate of 9% is computed as:

a. .09e-1.

b. e.09 × q.

c. e × (1 + .09).d. e.09 – 1.

e. (1 + .09)q.

Difficulty level: Easy

TIME VALUE

c 15. The time value of money concept can be defined asa. the relationship between the supply and demand of money. b. the relationship between money spent versus money received.c. the relationship between a dollar to be received in the future and a dollar today.d. the relationship of interest rate stated and amount paid.e. None of the above.

Difficulty level: Easy

CASH FLOWS

d 16. Discounting cash flows involvesa. discounting only those cash flows that occur at least 10 years in the future. b. estimating only the cash flows that occur in the first 4 years of a project.c. multiplying expected future cash flows by the cost of capital.d. discounting all expected future cash flows to reflect the time value of money.e. taking the cash discount offered on trade merchandise.

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 5/52

Difficulty level: Easy

INTEREST

a 17. Compound interesta. allows for the reinvestment of interest payments.

b. does not allow for the reinvestment of interest payments.c. is the same as simple interest.d. provides a value that is less than simple interest.e. Both A and D.

Difficulty level: Easy

ANNUITY

c 18. An annuitya. is a debt instrument that pays no interest. b. is a stream of payments that varies with current market interest.c. is a level stream of equal payments through time.

d. has no value.e. None of the above.

Difficulty level: Easy

COMPOUNDING

d 19. The stated rate of interest is 10%. Which form of compounding will give the highest effectiverate of interest?

a. annual compounding b. monthly compoundingc. daily compoundingd. continuous compounding

e. It is impossible to tell without knowing the term of the loan.

Difficulty level: Easy

PRESENT VALUE

b 20. The present value of future cash flows minus initial cost is calleda. the future value of the project. b. the net present value of the project.c. the equivalent sum of the investment.d. the initial investment risk equivalent value.e. None of the above.

Difficulty level: Easy

III. PROBLEMS

PRESENT VALUE – SINGLE SUM

a 21. Find the present value of $5,325 to be received in one period if the rate is 6.5%.a. $5,000.00 b. $5,023.58

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 6/52

c. $5,644.50d. $5,671.13e. None of the above.

Difficulty level: Easy

SIMPLE & COMPOUND INTEREST b 22. If you have a choice to earn simple interest on $10,000 for three years at 8% or annually

compound interest at 7.5% for three years which one will pay more and by how much?a. Simple interest by $50.00 b. Compound interest by $22.97c. Compound interest by $150.75d. Compound interest by $150.00e. None of the above.

Difficulty level: Easy

FUTURE VALUE – SINGLE SUM

d 23. Bradley Snapp has deposited $7,000 in a guaranteed investment account with a promised rate of 6% compounded annually. He plans to leave it there for 4 full years when he will make a down payment on a car after graduation. How much of a down payment will he be able to make?

a. $1,960.00 b. $2,175.57c. $8,960.00d. $8,837.34e. $9,175.57

Difficulty level: Easy

ORDINARY ANNUITY AND PRESENT VALUE

d 24. Your parents are giving you $100 a month for four years while you are in college. At a6% discount rate, what are these payments worth to you when you first startcollege?

a. $3,797.40 b. $4,167.09c. $4,198.79d. $4,258.03e. $4,279.32

Difficulty level: Easy

ORDINARY ANNUITY AND PRESENT VALUE

b 25. You just won the lottery! As your prize you will receive $1,200 a month for 100 months. If youcan earn 8% on your money, what is this prize worth to you today?

a. $87,003.69 b. $87,380.23c. $87,962.77d. $88,104.26e. $90,723.76

Difficulty level: Easy

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 7/52

ORDINARY ANNUITY AND PRESENT VALUE

b 26. Todd is able to pay $160 a month for five years for a car. If the interest rate is 4.9 percent, howmuch can Todd afford to borrow to buy a car?

a. $6,961.36 b. $8,499.13

c. $8,533.84d. $8,686.82e. $9,588.05

Difficulty level: Easy

ORDINARY ANNUITY AND PRESENT VALUE

a 27. You are the beneficiary of a life insurance policy. The insurance company informs you that youhave two options for receiving the insurance proceeds. You can receive a lump sum of $50,000today or receive payments of $641 a month for ten years. You can earn 6.5% on your money.Which option should you take and why?

a. You should accept the payments because they are worth $56,451.91 today.

b. You should accept the payments because they are worth $56,523.74 today.c. You should accept the payments because they are worth $56,737.08 today.d. You should accept the $50,000 because the payments are only worth $47,757.69 today.e. You should accept the $50,000 because the payments are only worth $47,808.17 today.

Difficulty level: Medium

ORDINARY ANNUITY AND PRESENT VALUE

c 28. Your employer contributes $25 a week to your retirement plan. Assume that you work for your employer for another twenty years and that the applicable discount rate is 5 percent. Giventhese assumptions, what is this employee benefit worth to you today?

a. $13,144.43

b. $15,920.55c. $16,430.54d. $16,446.34e. $16,519.02

Difficulty level: Medium

ORDINARY ANNUITY AND PRESENT VALUE

a 29. You have a sub-contracting job with a local manufacturing firm. Your agreement calls for annual payments of $50,000 for the next five years. At a discount rate of 12 percent, what isthis job worth to you today?

a. $180,238.81

b. $201,867.47c. $210,618.19d. $223,162.58e. $224,267.10

Difficulty level: Medium

ANNUITY DUE AND PRESENT VALUE

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 8/52

b 30. The Ajax Co. just decided to save $1,500 a month for the next five years as a safety net for recessionary periods. The money will be set aside in a separate savings account which pays3.25% interest compounded monthly. They deposit the first $1,500 today. If the company hadwanted to deposit an equivalent lump sum today, how much would they have had to deposit?

a. $82,964.59 b. $83,189.29

c. $83,428.87d. $83,687.23e. $84,998.01

Difficulty level: Medium

ANNUITY DUE AND PRESENT VALUE

b 31. You need some money today and the only friend you have that has any is your ‘miserly’ friend.He agrees to loan you the money you need, if you make payments of $20 a month for the nextsix month. In keeping with his reputation, he requires that the first payment be paid today. Healso charges you 1.5% interest per month. How much money are you borrowing?

a. $113.94

b. $115.65c. $119.34d. $119.63e. $119.96

Difficulty level: Medium

ANNUITY DUE AND PRESENT VALUE

c 32. You buy an annuity which will pay you $12,000 a year for ten years. The payments are paid onthe first day of each year. What is the value of this annuity today at a 7% discount rate?

a. $84,282.98 b. $87,138.04

c. $90,182.79d. $96,191.91e. $116,916.21

Difficulty level: Medium

ORDINARY ANNUITY VERSUS ANNUITY DUE

a 33. You are scheduled to receive annual payments of $10,000 for each of the next 25 years. Your discount rate is 8.5 percent. What is the difference in the present value if you receive these payments at the beginning of each year rather than at the end of each year?

a. $8,699 b. $9,217

c. $9,706d. $10,000e. $10,850

Difficulty level: Medium

ORDINARY ANNUITY VERSUS ANNUITY DUE

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 9/52

d 34. You are comparing two annuities with equal present values. The applicable discount rate is 7.5 percent. One annuity pays $5,000 on the first day of each year for twenty years. How muchdoes the second annuity pay each year for twenty years if it pays at the end of each year?

a. $4,651 b. $5,075c. $5,000

d. $5,375e. $5,405

Difficulty level: Medium

ORDINARY ANNUITY VERSUS ANNUITY DUE

a 35. Martha receives $100 on the first of each month. Stewart receives $100 on the last day of eachmonth. Both Martha and Stewart will receive payments for five years. At an 8% discount rate,what is the difference in the present value of these two sets of payments?

a. $32.88 b. $40.00c. $99.01

d. $108.00e. $112.50

Difficulty level: Medium

ORDINARY ANNUITY AND FUTURE VALUE

c 36. What is the future value of $1,000 a year for five years at a 6% rate of interest?a. $4,212.36 b. $5,075.69c. $5,637.09d. $6,001.38e. $6,801.91

Difficulty level: Easy

ORDINARY ANNUITY AND FUTURE VALUE

d 37. What is the future value of $2,400 a year for three years at an 8% rate of interest?a. $6,185.03 b. $6,847.26c. $7,134.16d. $7,791.36e. $8,414.67

Difficulty level: Easy

ORDINARY ANNUITY AND FUTURE VALUE

c 38. Janet plans on saving $3,000 a year and expects to earn 8.5 percent. How much will Janet haveat the end of twenty-five years if she earns what she expects?

a. $219,317.82 b. $230,702.57c. $236,003.38d. $244,868.92e. $256,063.66

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 10/52

Difficulty level: Easy

ANNUITY DUE VERSUS ORDINARY ANNUITY

b 39. Toni adds $3,000 to her savings on the first day of each year. Tim adds $3,000 to his savings onthe last day of each year. They both earn a 9% rate of return. What is the difference in their

savings account balances at the end of thirty years?a. $35,822.73 b. $36,803.03c. $38,911.21d. $39,803.04e. $40,115.31

Difficulty level: Medium

ORDINARY ANNUITY PAYMENTS

d 40. You borrow $5,600 to buy a car. The terms of the loan call for monthly payments for four yearsat a 5.9% rate of interest. What is the amount of each payment?

a. $103.22 b. $103.73c. $130.62d. $131.26e. $133.04

Difficulty level: Easy

ORDINARY ANNUITY PAYMENTS AND COST OF INTEREST

c 41. You borrow $149,000 to buy a house. The mortgage rate is 7.5% and the loan period is 30years. Payments are made monthly. If you pay for the house according to the loan agreement,how much total interest will you pay?

a. $138,086 b. $218,161c. $226,059d. $287,086e. $375,059

Difficulty level: Medium

ORDINARY ANNUITY PAYMENTS AND FUTURE VALUE

d 42. The Great Giant Corp. has a management contract with their newly hired president.The contract requires a lump sum payment of $25 million be paid to the president upon

the completion of her first ten years of service. The company wants to set aside an

equal amount of funds each year to cover this anticipated cash outflow. The companycan earn 6.5% on these funds. How much must the company set aside each year

for this purpose?a. $1,775,042.93 b. $1,798,346.17c. $1,801,033.67d. $1,852,617.25e. $1,938,018.22

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 11/52

Difficulty level: Easy

ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE

e 43. You retire at age 60 and expect to live another 27 years. On the day you retire, you have$464,900 in your retirement savings account. You are conservative and expect to earn 4.5% onyour money during your retirement. How much can you withdraw from your retirement savings

each month if you plan to die on the day you spend your last penny?a. $2,001.96 b. $2,092.05c. $2,398.17d. $2,472.00e. $2,481.27

Difficulty level: Medium

ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE

c 44. The McDonald Group purchased a piece of property for $1.2 million. They paid a down payment of 20% in cash and financed the balance. The loan terms require monthly payments

for 15 years at an annual percentage rate of 7.75% compounded monthly. What is the amountof each mortgage payment?

a. $7,440.01 b. $8,978.26c. $9,036.25d. $9,399.18e. $9,413.67

Difficulty level: Medium

ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE

d 45. You estimate that you will have $24,500 in student loans by the time you graduate. The interest

rate is 6.5 percent. If you want to have this debt paid in full within five years, how much mustyou pay each month?

a. $471.30 b. $473.65c. $476.79d. $479.37e. $480.40

Difficulty level: Medium

ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE

b 46. You are buying a previously owned car today at a price of $6,890. You are paying $500 down

in cash and financing the balance for 36 months at 7.9 percent. What is the amount of each loan payment?

a. $198.64 b. $199.94c. $202.02d. $214.78e. $215.09

Difficulty level: Medium

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 12/52

ORDINARY ANNUITY PAYMENTS AND PRESENT VALUE

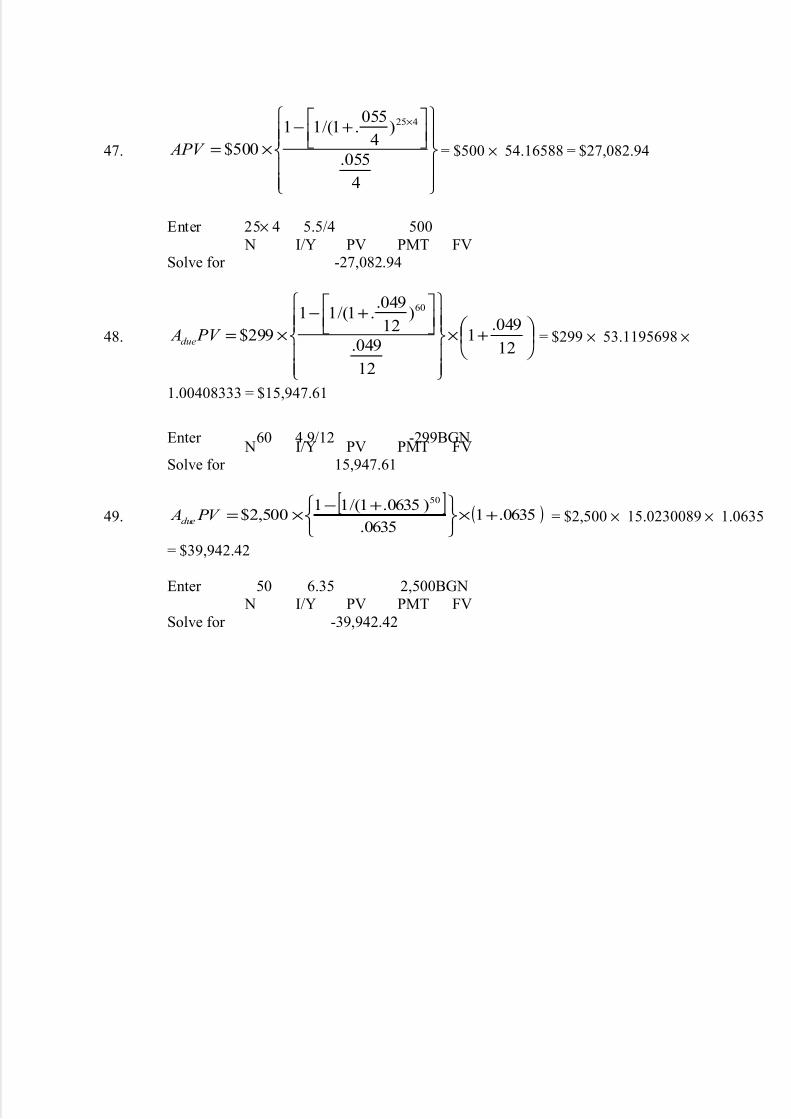

b 47. The Good Life Insurance Co. wants to sell you an annuity which will pay you $500 per quarter for 25 years. You want to earn a minimum rate of return of 5.5 percent. What is the most youare willing to pay as a lump sum today to buy this annuity?

a. $26,988.16

b. $27,082.94c. $27,455.33d. $28,450.67e. $28,806.30

Difficulty level: Medium

ANNUITY DUE PAYMENTS AND PRESENT VALUE

c 48. Your car dealer is willing to lease you a new car for $299 a month for 60 months. Payments aredue on the first day of each month starting with the day you sign the lease contract. If your costof money is 4.9 percent, what is the current value of the lease?

a. $15,882.75

b. $15,906.14c. $15,947.61d. $16,235.42e. $16,289.54

Difficulty level: Medium

ANNUITY DUE PAYMENTS AND PRESENT VALUE

d 49. Your great-aunt left you an inheritance in the form of a trust. The trust agreement states thatyou are to receive $2,500 on the first day of each year, starting immediately and continuing for fifty years. What is the value of this inheritance today if the applicable discount rate is 6.35 percent?

a. $36,811.30 b. $37,557.52c. $39,204.04d. $39,942.42e. $40,006.09

Difficulty level: Medium

SIMPLE VERSUS COMPOUND INTEREST

c 50. Beatrice invests $1,000 in an account that pays 4% simple interest. How muchmore could she have earned over a five-year period if the interest had compoundedannually?

a. $15.45 b. $15.97c. $16.65d. $17.09e. $21.67

Difficulty level: Easy

ANNUITY DUE PAYMENTS AND FUTURE VALUE

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 13/52

a 51. Your firm wants to save $250,000 to buy some new equipment three years from now. The planis to set aside an equal amount of money on the first day of each year starting today. The firmcan earn a 4.7% rate of return. How much does the firm have to save each year to achieve their goal?

a. $75,966.14 b. $76,896.16

c. $78,004.67d. $81.414.14e. $83,333.33

Difficulty level: Medium

ANNUITY DUE PAYMENTS AND FUTURE VALUE

e 52. Today is January 1. Starting today, Sam is going to contribute $140 on the first of each monthto his retirement account. His employer contributes an additional 50% of the amountcontributed by Sam. If both Sam and his employer continue to do this and Sam can earn amonthly rate of ½ of 1 percent, how much will he have in his retirement account 35 years fromnow?

a. $199,45.944. b. $200,456.74c. $249,981.21d. $299,189.16e. $300,685.11

Difficulty level: Medium

ORDINARY ANNUITY TIME PERIODS AND PRESENT VALUE

c 53. You are considering an annuity which costs $100,000 today. The annuity pays $6,000 a year.The rate of return is 4.5 percent. What is the length of the annuity time period?

a. 24.96 years

b. 29.48 yearsc. 31.49 yearsd. 33.08 yearse. 38.00 years

Difficulty level: Medium

ORDINARY ANNUITY TIME PERIODS AND PRESENT VALUE

d 54. Today, you signed loan papers agreeing to borrow $4,954.85 at 9% compounded monthly. Theloan payment is $143.84 a month. How many loan payments must you make before the loan is paid in full?

a. 29.89

b. 36.00c. 38.88d. 40.00e. 41.03

Difficulty level: Medium

ORDINARY ANNUITY TIME PERIODS AND FUTURE VALUE

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 14/52

a 55. Winston Enterprises would like to buy some additional land and build a new factory. Theanticipated total cost is $136 million. The owner of the firm is quite conservative and will onlydo this when the company has sufficient funds to pay cash for the entire expansion project.Management has decided to save $450,000 a month for this purpose. The firm earns 6%compounded monthly on the funds it saves. How long does the company have to wait beforeexpanding its operations?

a. 184.61 months b. 199.97 monthsc. 234.34 monthsd. 284.61 monthse. 299.97 months

Difficulty level: Medium

ANNUITY DUE TIME PERIODS AND PRESENT VALUE

b 56. Today, you are retiring. You have a total of $413,926 in your retirement savings and have thefunds invested such that you expect to earn an average of 3 percent, compounded monthly, onthis money throughout your retirement years. You want to withdraw $2,500 at the beginning of

every month, starting today. How long will it be until you run out of money?a. 185.00 months b. 213.29 monthsc. 227.08 monthsd. 236.84 monthse. 249.69 months

Difficulty level: Medium

ANNUITY DUE TIME PERIODS

c 57. The Bad Guys Co. is notoriously known as a slow-payer. They currently need to borrow$25,000 and only one company will even deal with them. The terms of the loan

call for daily payments of $30.76. The first payment is due today. The interest rate is 21%compounded daily. What is the time period of this loan?

a. 2.88 years b. 2.94 yearsc. 3.00 yearsd. 3.13 yearse. 3.25 years

Difficulty level: Medium

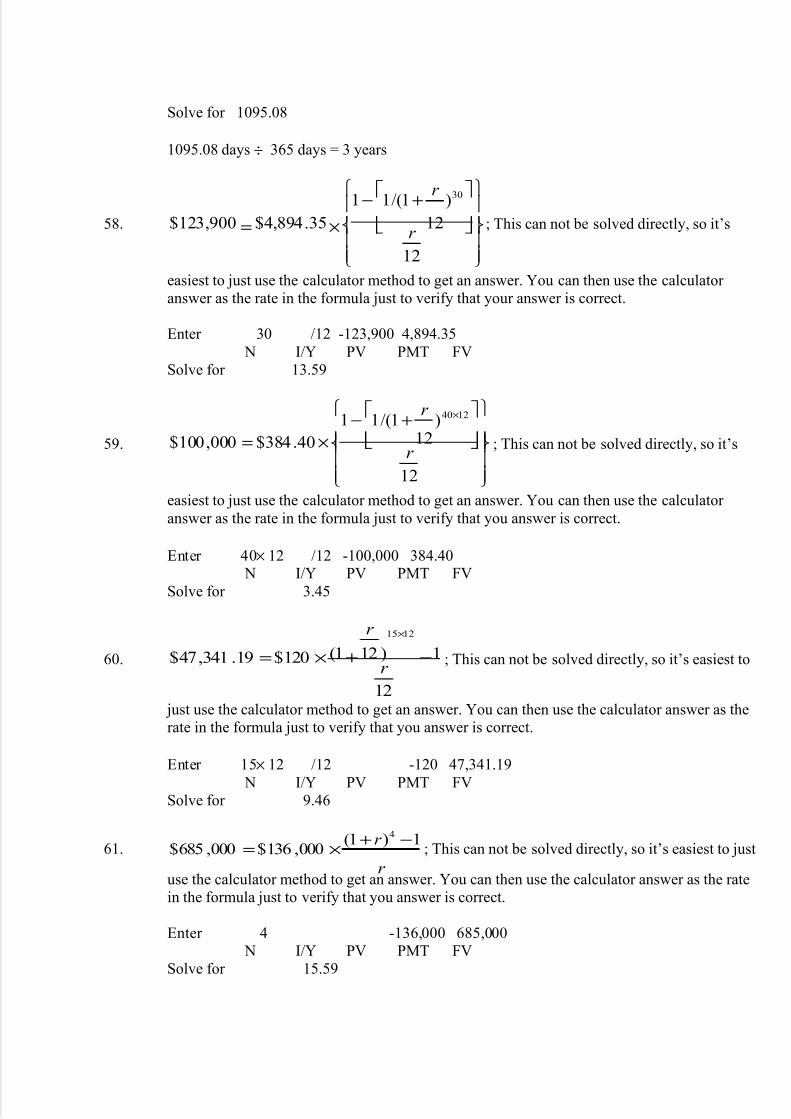

ORDINARY ANNUITY INTEREST RATE

c 58. The Robertson Firm is considering a project which costs $123,900 to undertake. The project

will yield cash flows of $4,894.35 monthly for 30 months. What is the rate of return on this project?

a. 12.53% b. 13.44%c. 13.59%d. 14.02%e. 14.59%

Difficulty level: Medium

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 15/52

ORDINARY ANNUITY INTEREST RATE

a 59. Your insurance agent is trying to sell you an annuity that costs $100,000 today. By buying this annuity, your agent promises that you will receive payments of $384.40 amonth for the next 40 years. What is the rate of return on this investment?

a. 3.45%

b. 3.47%c. 3.50%d. 3.52%e. 3.55%

Difficulty level: Medium

ORDINARY ANNUITY INTEREST RATE

e 60. You have been investing $120 a month for the last 15 years. Today, your investment account isworth $47,341.19. What is your average rate of return on your investments?

a. 9.34% b. 9.37%

c. 9.40%d. 9.42%e. 9.46%

Difficulty level: Medium

ORDINARY ANNUITY INTEREST RATE

c 61. Brinker, Inc. has been investing $136,000 a year for the past 4 years into a business venture.Today, Brinker sold that venture for $685,000. What is their rate of return on this venture?

a. 9.43% b. 11.06%c. 15.59%

d. 16.67%e. 18.71%

Difficulty level: Easy

ANNUITY DUE INTEREST RATE

b 62. Your mother helped you start saving $25 a month beginning on your 10th birthday. She alwaysmade you make your deposit on the first day of each month just to “start the month out right”.Today, you turn 21 and have $4,482.66 in your account. What is your rate of return on your savings?

a. 5.25% b. 5.29%

c. 5.33%d. 5.36%e. 5.50%

Difficulty level: Easy

ANNUITY DUE INTEREST RATE

a 63. Today, you turn 21. Your birthday wish is that you will be a millionaire by your 40th birthday.In an attempt to reach this goal, you decide to save $25 a day, every day until you turn 40. You

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 16/52

open an investment account and deposit your first $25 today. What rate of return must you earnto achieve your goal?

a. 15.07% b. 15.13%c. 15.17%d. 15.20%

e. 15.24%

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

b 64. Marko, Inc. is considering the purchase of ABC Co. Marko believes that ABC Co. can generatecash flows of $5,000, $9,000, and $15,000 over the next three years, respectively. After thattime, they feel the business will be worthless. Marko has determined that a 14% rate of return isapplicable to this potential purchase. What is Marko willing to pay today to buy ABC Co.?

a. $19,201.76 b. $21,435.74c. $23,457.96

d. $27,808.17e. $31,758.00

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

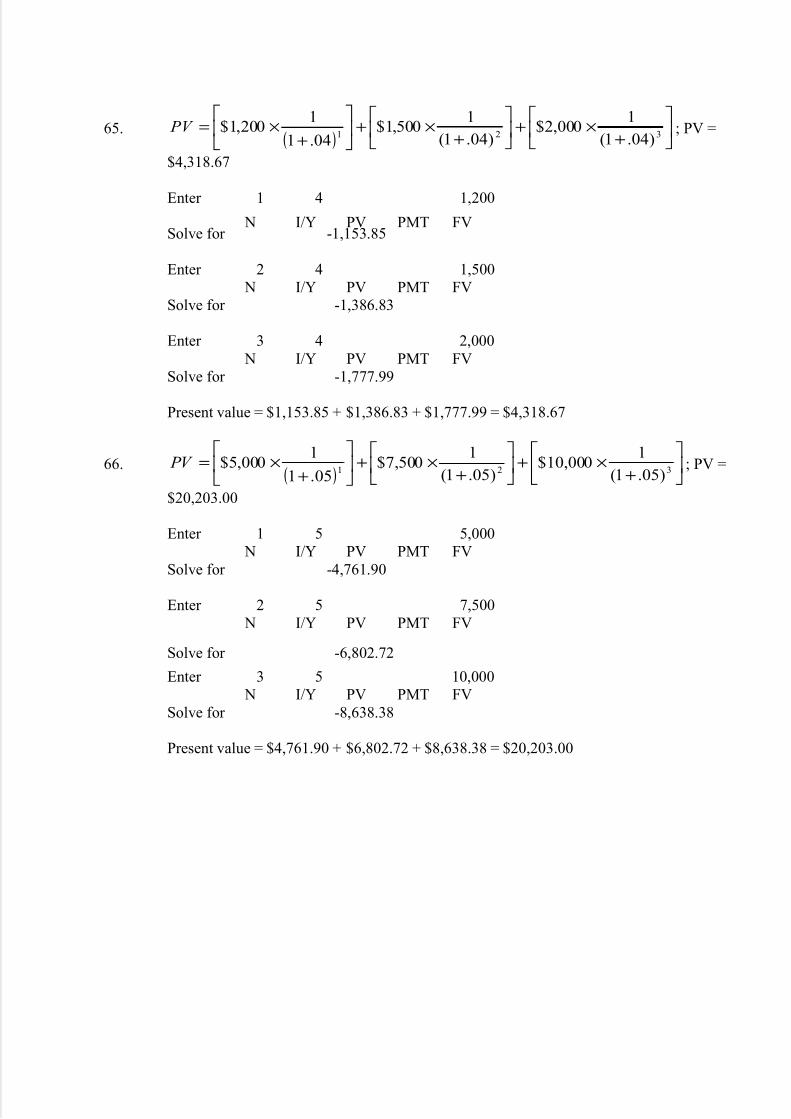

a 65. You are considering two savings options. Both options offer a 4% rate of return. The firstoption is to save $1,200, $1,500, and $2,000 a year over the next three years, respectively. Theother option is to save one lump sum amount today. If you want to have the same balance inyour savings at the end of the three years, regardless of the savings method you select, howmuch do you need to save today if you select the lump sum option?

a. $4,318.67

b. $4,491.42c. $4,551.78d. $4,607.23e. $4,857.92

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

b 66. You are considering two insurance settlement offers. The first offer includes annual paymentsof $5,000, $7,500, and $10,000 over the next three years, respectively. The other offer is the payment of one lump sum amount today. You are trying to decide which offer to accept giventhe fact that your discount rate is 5 percent. What is the minimum amount that you will accept

today if you are to select the lump sum offer?a. $19,877.67 b. $20,203.00c. $21,213.15d. $23,387.50e. $24,556.88

Difficulty level: Easy

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 17/52

UNEVEN CASH FLOWS AND PRESENT VALUE

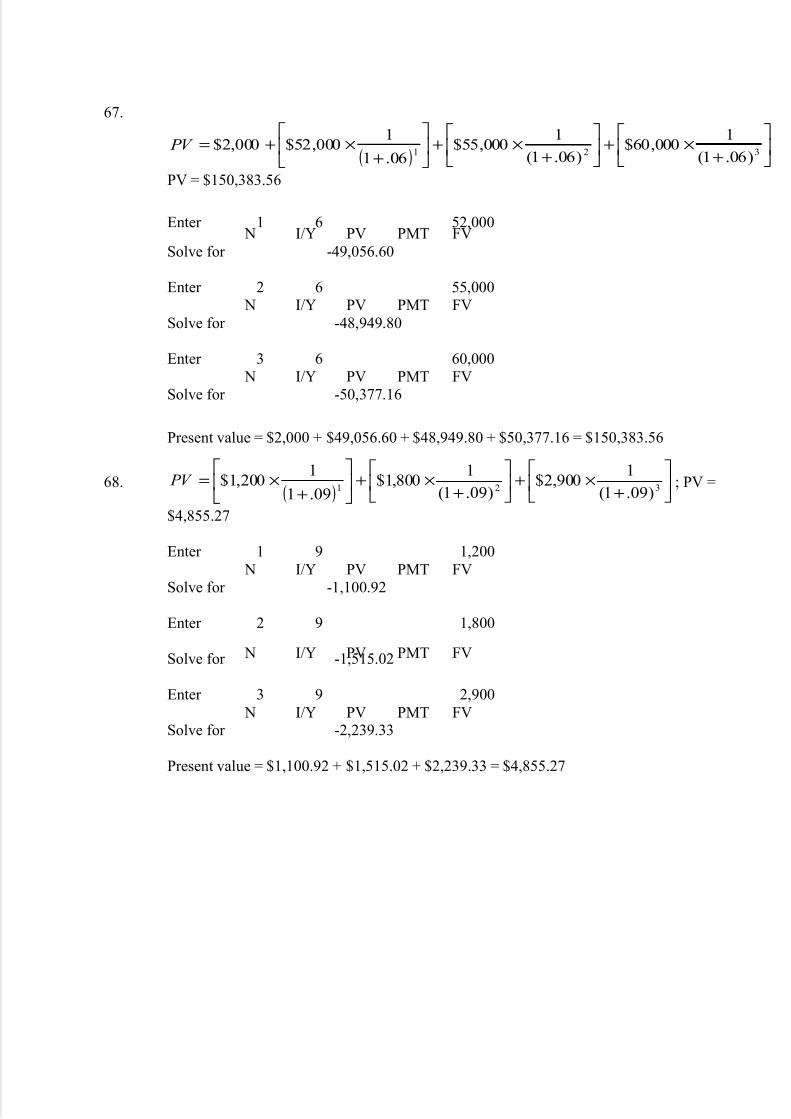

d 67. You are considering a job offer. The job offers an annual salary of $52,000, $55,000, and$60,000 a year for the next three years, respectively. The offer also includes a starting bonus of $2,000 payable immediately. What is this offer worth to you today at a discount rate of 6 percent?

a. $148,283.56

b. $148,383.56c. $150,283.56d. $150,383.56e. $152,983.56

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

b 68. You are considering a project with the following cash flows:Year 1 Year 2 Year 3$1,200 $1,800 $2,900

What is the present value of these cash flows, given a 9% discount rate?

a. $4,713.62 b. $4,855.27c. $5,103.18d. $5,292.25e. $6,853.61

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

d 69. You are considering a project with the following cash flows:Year 1 Year 2 Year 3$5,600 $9,000 $2,000

What is the present value of these cash flows, given an 11% discount rate?a. $8,695.61 b. $8,700.89c. $13,732.41d. $13,812.03e. $19,928.16

Difficulty level: Easy

UNEVEN CASH FLOWS AND PRESENT VALUE

a 70. You are considering a project with the following cash flows:Year 1 Year 2 Year 3

$4,200 $5,000 $5,400What is the present value of these cash flows, given a 3% discount rate?

a. $13,732.41 b. $13,812.03c. $14,308.08d. $14,941.76e. $14,987.69

Difficulty level: Easy

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 18/52

UNEVEN CASH FLOWS AND PRESENT VALUE

a 71. You have some property for sale and have received two offers. The first offer is for $189,000today in cash. The second offer is the payment of $100,000 today and an additional $100,000two years from today. If the applicable discount rate is 8.75 percent, which offer should youaccept and why?

a. You should accept the $189,000 today because it has the higher net present value. b. You should accept the $189,000 today because it has the lower future value.c. You should accept the second offer because you will receive $200,000 total.d. You should accept the second offer because you will receive an extra $11,000.e. You should accept the second offer because it has a present value of $194,555.42.

Difficulty level: Medium

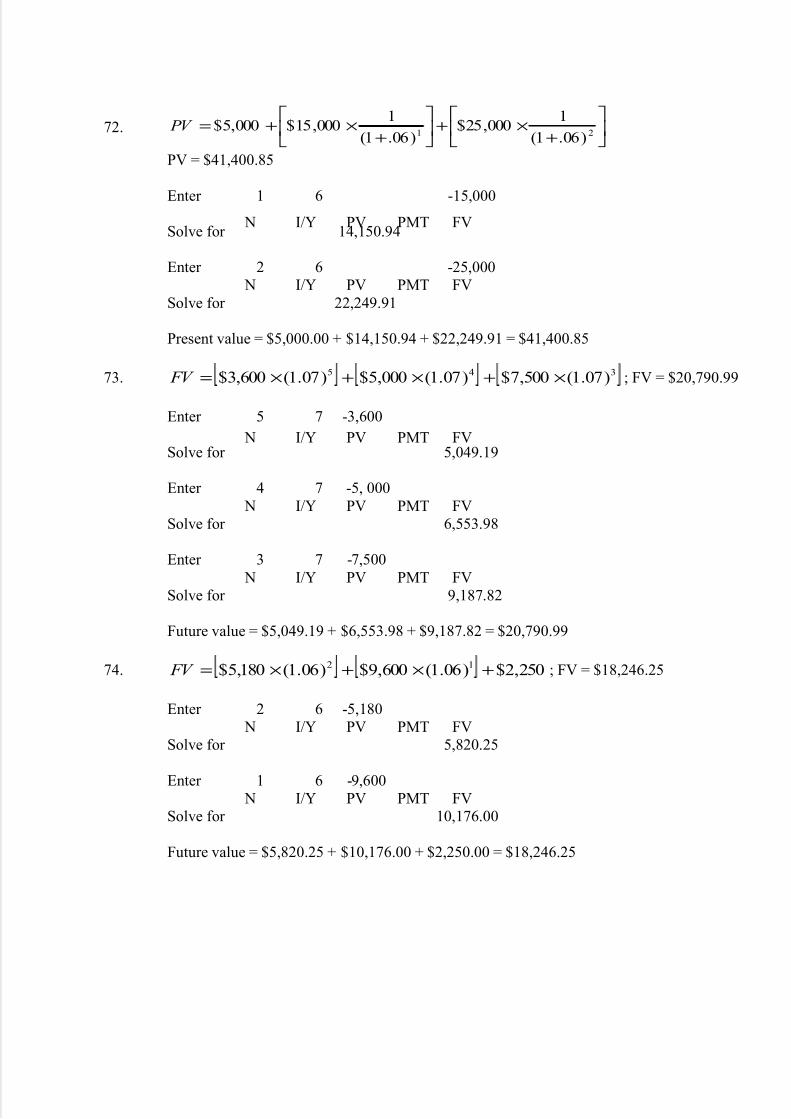

UNEVEN CASH FLOWS AND PRESENT VALUE

b 72. Your local travel agent is advertising an extravagant global vacation. The package dealrequires that you pay $5,000 today, $15,000 one year from today, and a final payment of $25,000 on the day you leave two years from today. What is the cost of this vacation in today’s

dollars if the discount rate is 6 percent?a. $39,057.41 b. $41,400.85c. $43,082.39d. $44,414.14e. $46,518.00

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

e 73. One year ago, the Jenkins Family Fun Center deposited $3,600 in an investment account for the purpose of buying new equipment four years from today. Today, they are adding another

$5,000 to this account. They plan on making a final deposit of $7,500 to the account next year.How much will be available when they are ready to buy the equipment, assuming they earn a7% rate of return?

a. $18,159.65 b. $19,430.84c. $19,683.25d. $20,194.54e. $20,790.99

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

c 74. What is the future value of the following cash flows at the end of year 3 if the interest rate is 6 percent? The cash flows occur at the end of each year.

Year 1 Year 2 Year 3$5,180 $9,600 $2,250

a. $15,916.78 b. $18,109.08c. $18,246.25d. $19,341.02e. $19,608.07

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 19/52

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

d 75. What is the future value of the following cash flows at the end of year 3 if the interest rate is 9 percent? The cash flows occur at the end of each year.

Year 1 Year 2 Year 3$9,820 $0 $4,510

a. $15,213.80 b. $15,619.70c. $15,916.78d. $16,177.14e. $17,633.08

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

c 76. What is the future value of the following cash flows at the end of year 3 if the interest rate is

7.25 percent? The cash flows occur at the end of each year.Year 1 Year 2 Year 3$6,800 $2,100 $0

a. $8,758.04 b. $8,806.39c. $10,073.99d. $10,314.00e. $10,804.36

Difficulty level: Medium

UNEVEN CASH FLOWS AND FUTURE VALUE

e 77. Suzette is going to receive $10,000 today as the result of an insurance settlement. In addition,she will receive $15,000 one year from today and $25,000 two years from today. She plans onsaving all of this money and investing it for her retirement. If Suzette can earn an average of 11% on her investments, how much will she have in her account if she retires 25 years fromtoday?

a. $536,124.93 b. $541,414.14c. $546,072.91d. $570,008.77e. $595,098.67

Difficulty level: Medium

PRESENT VALUE, PAYMENTS AND FUTURE VALUE

b 78. The Bluebird Company has a $10,000 liability they must pay three years from today.The company is opening a savings account so that the entire amount will be available when thisdebt needs to be paid. The plan is to make an initial deposit today and then deposit anadditional $2,500 a year for the next three years, starting one year from today. The account pays a 3% rate of return. How much does the Bluebird Company need to deposit today?

a. $1,867.74 b. $2,079.89

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 20/52

c. $3,108.09d. $4,276.34e. $4,642.28

Difficulty level: Medium

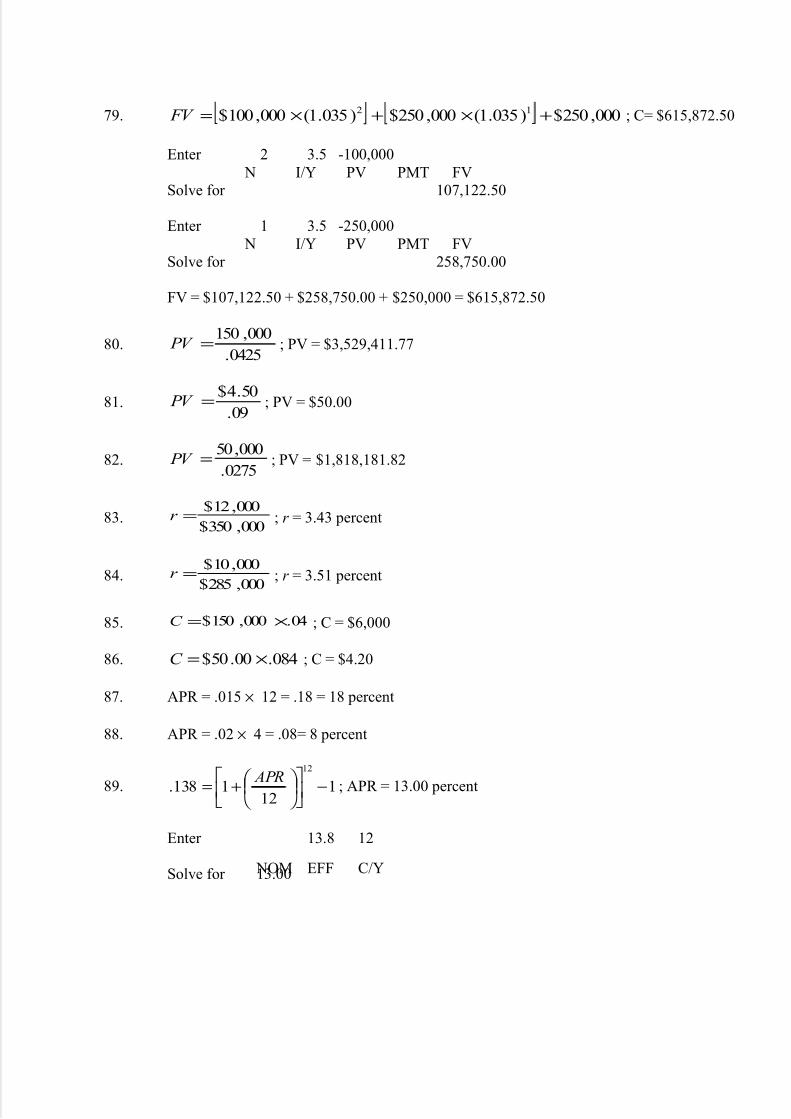

UNEVEN CASH FLOWS AND FUTURE VALUEc 79. The government has imposed a fine on the Not-So-Legal Company. The fine calls for annual

payments of $100,000, $250,000, and $250,000, respectively over the next three years. The first payment is due one year from today. The government plans to invest the funds until the final payment is collected and then donate the entire amount, including investment earnings, to anational health center. The government will earn 3.5% on the funds held. How much will thenational health center receive three years from today?

a. $613,590.00 b. $614,622.50c. $615,872.50d. $616,006.00e. $619,050.05

Difficulty level: Medium

PERPETUITY PRESENT VALUE

b 80. George Jefferson established a trust fund that provides $150,000 in scholarships each year for worthy students. The trust fund earns a 4.25% rate of return. How much money did Mr.Jefferson contribute to the fund assuming that only the interest income is distributed?

a. $3,291,613.13 b. $3,529,411.77c. $3,750,000.00d. $4,328,970.44e. $6,375,000.00

Difficulty level: Easy

PERPETUITY PRESENT VALUE

e 81. A 9% preferred stock pays an annual dividend of $4.50. What is one share of this stock worthtoday?

a. $.41 b. $4.50c. $5.00d. $45.00e. $50.00

Difficulty level: Easy

PERPETUITY PRESENT VALUE

e 82. You would like to establish a trust fund that will provide $50,000 a year forever for your heirs.The trust fund is going to be invested very conservatively so the expected rate of return is only2.75 percent. How much money must you deposit today to fund this gift for your heirs?

a. $1,333,333.33 b. $1,375,000.00c. $1,425,000.00

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 21/52

d. $1,666,666.67e. $1,818,181.82

Difficulty level: Easy

PERPETUITY DISCOUNT RATE

c 83. You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever.What rate of return are you earning on this policy?

a. 3.25% b. 3.33%c. 3.43%d. 3.50%e. 3.67%

Difficulty level: Medium

PERPETUITY DISCOUNT RATE

d 84. The Eternal Gift Insurance Company is offering you a policy that will pay you and your heirs

$10,000 a year forever. The cost of the policy is $285,000. What is the rate of return on this policy?

a. 2.85% b. 3.25%c. 3.46%d. 3.51%e. 3.60%

Difficulty level: Easy

PERPETUITY PAYMENT

e 85. Your rich uncle establishes a trust in your name and deposits $150,000 in it. The

trust pays a guaranteed 4% rate of return. How much will you receive each year if the trust is required to pay you all of the interest earnings on an annual basis?

a. $3,750 b. $4,000c. $4,500d. $5,400e. $6,000

Difficulty level: Easy

PERPETUITY PAYMENT

b 86. The preferred stock of ABC Co. offers an 8.4% rate of return. The stock is currently priced at

$50.00 per share. What is the amount of the annual dividend?a. $2.10 b. $4.20c. $5.00d. $6.40e. $8.60

Difficulty level: Easy

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 22/52

ANNUAL PERCENTAGE RATE

d 87. Your credit card company charges you 1.5% per month. What is the annual percentage rate onyour account?

a. 12.00% b. 15.00%c. 15.39%

d. 18.00%e. 19.56%

Difficulty level: Medium

ANNUAL PERCENTAGE RATE

d 88. What is the annual percentage rate on a loan with a stated rate of 2% per quarter?a. 2.00% b. 2.71%c. 4.04%d. 8.00%e. 8.24%

Difficulty level: Medium

ANNUAL PERCENTAGE RATE

c 89. You are paying an effective annual rate of 13.8% on your credit card. The interest iscompounded monthly. What is the annual percentage rate on your account?

a. 11.50% b. 12.00%c. 13.00%d. 13.80%e. 14.71%

Difficulty level: Medium

EFFECTIVE ANNUAL RATE

b 90. What is the effective annual rate if a bank charges you 7.64% compoundedquarterly?

a. 7.79% b. 7.86%c. 7.95%d. 7.98%e. 8.01%

Difficulty level: Medium

EFFECTIVE ANNUAL RATE

d 91. Your credit card company quotes you a rate of 14.9 percent. Interest is billed monthly. What isthe actual rate of interest you are paying?

a. 13.97% b. 14.90%c. 15.48%d. 15.96%e. 16.10%

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 23/52

Difficulty level: Medium

EFFECTIVE ANNUAL RATE

d 92. Mr. Miser loans money at an annual rate of 21 percent. Interest is compounded daily. What isthe actual rate Mr. Miser is charging on his loans?

a. 22.97% b. 23.08%c. 23.21%d. 23.36%e. 23.43%

Difficulty level: Medium

EFFECTIVE ANNUAL RATE

e 93. You are considering two loans. The terms of the two loans are equivalent with the exception of the interest rates. Loan A offers a rate of 7.45% compounded daily. Loan B offers a rate of 7.5% compounded semi-annually. Loan _____ is the better offer because______:

a. A; you will pay less interest. b. A; the annual percentage rate is 7.45%.c. B; the annual percentage rate is 7.64%.d. B; the interest is compounded less frequently.e. B; the effective annual rate is 7.64%.

Difficulty level: Medium

EFFECTIVE ANNUAL RATE

b 94. You have $2,500 that you want to use to open a savings account. You have found five differentaccounts that are acceptable to you. All you have to do now is determine which account youwant to use such that you can earn the highest rate of interest possible. Which account should

you use based upon the annual percentage rates quoted by each bank?Account A: 3.75%, compounded annuallyAccount B: 3.70%, compounded monthlyAccount C: 3.70%, compounded semi-annuallyAccount D: 3.65%, compounded continuouslyAccount E: 3.66%, compounded quarterly

a. Account A b. Account Bc. Account Cd. Account De. Account E

Difficulty level: Medium

CONTINUOUS COMPOUNDING

d 95. What is the effective annual rate of 14.9% compounded continuously?a. 15.96% b. 16.01%c. 16.05%d. 16.07%e. 16.17%

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 24/52

Difficulty level: Medium

CONTINUOUS COMPOUNDING

c 96. What is the effective annual rate of 9.75% compounded continuously?a. 9.99%

b. 10.11%c. 10.24%d. 10.28%e. 10.30%

Difficulty level: Medium

CONTINUOUS COMPOUNDING

d 97. The Smart Bank wants to appear competitive based on quoted loan rates and thus must offer a7.9% annual percentage rate. What is the maximum rate the bank can actually earn based on thequoted rate?

a. 7.90%

b. 8.18%c. 8.20%d. 8.22%e. 8.39%

Difficulty level: Medium

CONTINUOUS COMPOUNDING VERSUS ANNUAL COMPOUNDING

c 98. You are going to loan your friend $1,000 for one year at a 5% rate of interest. How muchadditional interest can you earn if you compound the rate continuously rather than annually?

a. $.97 b. $1.09

c. $1.27d. $1.36e. $1.49

Difficulty level: Medium

FUTURE VALUE

c 99. Today you earn a salary of $28,500. What will be your annual salary fifteen years fromnow if you earn annual raises of 3.5 percent?

a. $47,035.35 b. $47,522.89c. $47,747.44

d. $48,091.91e. $48,201.60

Difficulty level: Medium

FUTURE VALUE

e 100. You hope to buy your dream house six years from now. Today your dream house costs$189,900. You expect housing prices to rise by an average of 4.5% per year over the next six years. How much will your dream house cost by the time you are ready to

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 25/52

buy it?a. $240,284.08 b. $246,019.67c. $246,396.67d. $246,831.94e. $247,299.20

Difficulty level: Medium

PRESENT VALUE

b 101. Your grandmother invested one lump sum 17 years ago at 4.25% interest.Today, she gave you the proceeds of that investment which totaled $5,539.92. Howmuch did your grandmother originally invest?

a. $2,700.00 b. $2,730.30c. $2,750.00d. $2,768.40e. $2,774.90

Difficulty level: Medium

PRESENT VALUE

c 102. You would like to give your daughter $40,000 towards her college education thirteenyears from now. How much money must you set aside today for this purpose if you canearn 6.3% on your funds?

a. $17,750.00 b. $17,989.28c. $18,077.05d. $18,213.69e. $18,395.00

Difficulty level: Medium

INTEREST RATE FOR A SINGLE PERIOD

e 103. One year ago, you invested $3,000. Today it is worth $3,142.50. What rate of interestdid you earn?

a. 4.63% b. 4.68%c. 4.70%d. 4.73%e. 4.75%

Difficulty level: Easy

INTEREST RATE FOR MULTIPLE PERIODS

d 104. Forty years ago, your father invested $2,500. Today that investment is worth $107,921.What is the average rate of return your father earned on his investment?

a. 8.50% b. 9.33%c. 9.50%d. 9.87%

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 26/52

e. 9.99%

Difficulty level: Easy

PRESENT VALUE AND RATE CHANGES

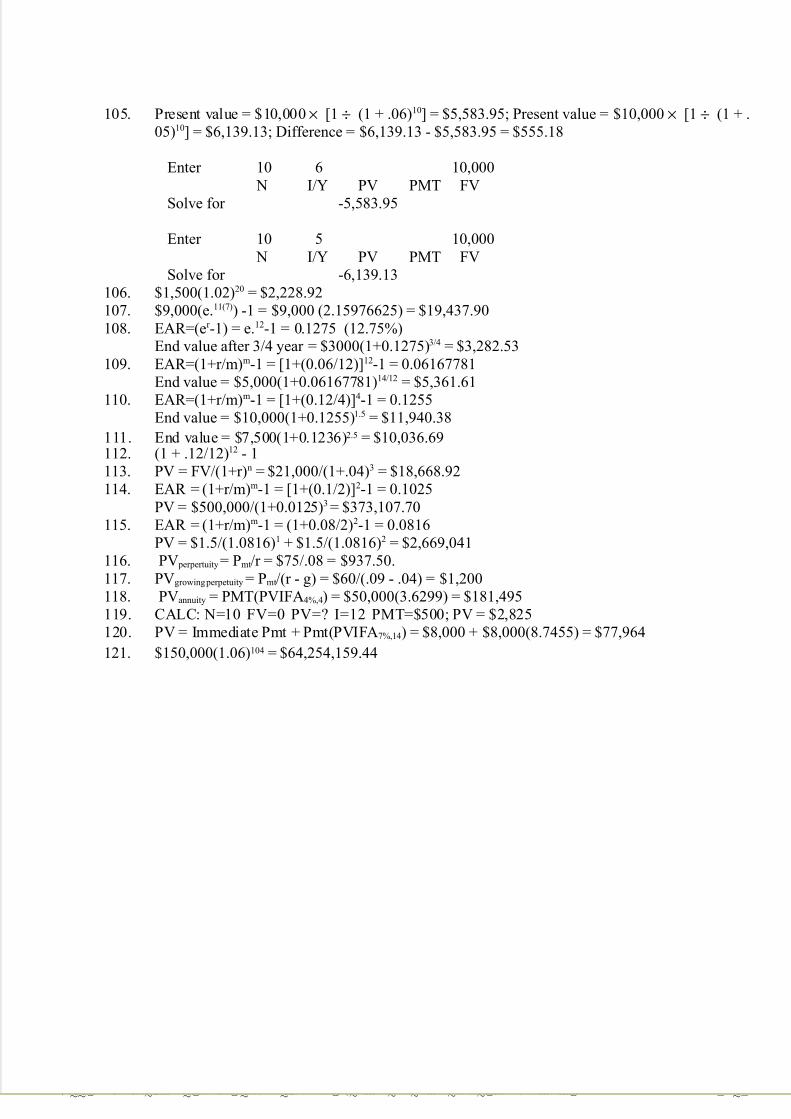

a 105. You want to have $10,000 saved ten years from now. How much less do you have to

deposit today to reach this goal if you can earn 6% rather than 5% on your savings?

a. $555.18 b. $609.81c. $615.48d. $928.73e. $1,046.22

Difficulty level: Medium

FUTURE VALUE – SINGLE SUM

c 106.You have deposited $1,500 in an account that promises to pay 8% compounded quarterly for

the next five years. How much will you have in the account at the end?a. $1,598.33 b. $2,203.99c. $2,228.92d. $6,991.44e. None of the above.

Difficulty level: Easy

FUTURE VALUE – SINGLE SUM

d 107.What is the future value of investing $9,000 for 7 years at a continuously compounded rate of 11%?

a. $15,930.00 b. $18,685.44c. $19,369.83d. $19,437.90e. None of the above.

Difficulty level: Easy

FUTURE VALUE – CONTINUOUS COMPOUNDING

b 108.What is the future value of investing $3,000 for 3/4 year at a continuously compounded rate of 12%?

a. $3,163

b. $3,263c. $3,283d. $3,287e. $3,317

Difficulty level: Challenge

EAR & FUTURE VALUE

d 109.Which of the following amounts is closest to the end value of investing $5,000 for 14 months at

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 27/52

a stated annual interest rate of 6% compounded monthly?a. $5,293 b. $5,345c. $5,352d. $5,362e. $6,183

Difficulty level: Medium

EAR & FUTURE VALUE

c 110.Which of the following amounts is closest to the end value of investing $10,000 for 18 monthsat a stated annual interest rate of 12% compounded quarterly?

a. $11,800 b. $11,852c. $11,940d. $11,961e. None of the above is within $100 of the correct answer.

Difficulty level: Medium

FUTURE VALUE

e 111.Which of the following amounts is closest to the end value of investing $7,500 for 2.5 years atan effective annual interest rate of 12.36%. Interest is compounded semiannually.

a. $ 7,531 b. $ 8,427c. $ 9,469d. $ 9,818e. $10,037

Difficulty level: Medium

EAR

d 112.If the stated rate of interest is 12% and it is compounded monthly, what is the effective annualinterest rate?

a. 12.00% b. 12.25%c. 12.46%d. 12.68%e. 12.92%

Difficulty level: Medium

PRESENT VALUE – SINGLE SUMd 113.What is the present value of a payment of $21,000 three years from now if the effective annual

interest rate is 4%?a. $17,951 b. $18,480c. $18,658d. $18,669e. $19,218

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 28/52

Difficulty level: Easy

PRESENT VALUE – FUTURE SUM

a 114.Thorton will receive an inheritance of $500,000 three years from now. Thorton's discount rateis 10% interest rate compounded semiannually. Which of the following values is closest to theamount that Thorton should accept today for the right to his inheritance?

a. $ 373,108. b. $ 375,657.c. $ 665,500.d. $ 670,048.e. None of the above is within $10 of the correct answer.

Difficulty level: Medium

PRESENT VALUE – FUTURE SUM

d 115.A mortgage instrument pays $1.5 million at the end of each of the next two years. An investor has an alternative investment with the same amount of risk that will pay interest at 8%compounded semiannually. Which of the following amounts is closest to what the investor

should pay for the mortgage instrument?a. $1,386,834 b. $1,388,889c. $2,674,897d. $2,669,041e. $3,854,512

Difficulty level: Easy

PERPETUITY

d 116.You are to receive $75 per year indefinitely. The market rate of interest for these types of payments is 8%. The price you would pay for this stream is:

a. $ 9.375 b. $ 81.00c. $ 93.75.d. $937.50.e. None of the above.

Difficulty level: Easy

GROWING PERPETUITY

c 117.Aunt Clarisse has promised to leave you an annuity that will pay $60 next year and grow at anannual rate of 4%. The payments are expected to go on indefinitely and the interest rate is 9%.What is the value of the growing perpetuity?

a. $ 667 b. $ 693c. $1,200d. $1,248e. None of the above.

Difficulty level: Medium

PRESENT VALUE - ANNUITY

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 29/52

c 118.A court settlement awarded an accident victim four payments of $50,000 to be paid at the endof each of the next four years. Using a discount rate of 4%, calculate the present value of theannuity.

a. $173,255 b. $178,495c. $181,495

d. $184,095e. $200,000

Difficulty level: Medium

PRESENT VALUE - ANNUITY

d 119.What is the present value of 10 annual payments of $500 at a discount rate of 12%?a. $1,332 b. $1,761c. $1,840d. $2,825e. $3,040

Difficulty level: Medium

PRESENT VALUE - ANNUITY

b 120.An S&L provides a loan with 15 yearly repayments of $8,000 with the first payment beginningimmediately. Which of the following amounts comes closest to the present value of the loan if the interest rate is 7%?

a. $ 72,863 b. $ 77,964c. $115,648d. $120,000e. Not enough information is given to determine the answer.

Difficulty level: Medium

FUTURE VALUE – SINGLE SUM

e 121.The great, great grandparents of one of your classmates sold their factory to the government 104years ago for $150,000. If these proceeds had been invested at 6%, how much would thislegacy be worth today? Assume annual compounding.

a. $ 936,000.00 b. $ 1,086,000.00c. $60,467,131.54d. $60,617,131.54e. $64,254,159.44

Difficulty level: Medium

IV. ESSAYS

FUTURE VALUE

122. Mr. Miser, who is 35 years old, has just inherited $11,000 and decides to use the windfall towardshis retirement. He places the money in a bank which promises a return of 6% per year until his

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 30/52

planned retirement in 30 years. If his funds earn 6% interest compounded annually, how much willhe have at retirement? Repeat the analysis for both semi-annual and continuous compounding.

$11,000(1.06)30 = $63,178.40

$11,000(1.03)60 = $64,867.63

$11,000 . e(.06)(30) = $66,546.12

PRESENT VALUE OF A PERPETUITY

123. Your aunt, in her will, left you the sum of $5,000 a year forever with payments starting immediately.However, the news is better. She has specified that the amount should grow at 5% per year tomaintain purchasing power. Given an interest rate of 12%, what is the PV of the inheritance?

$5,000 + $5,000(1.05)/(.12-.05) = $80,000

PRESENT VALUE OF AN ANNUITY

124. If you invest $100,000 today at 12% per year over the next 15 years, what is the most you can spendin equal amounts out of the fund each year over that time.

$100,000 = Annuity Payment * Ann.Factor(.12,15)6.8109 = $14,682.42 or PV=$-100,000 I/YR=12 N=15 PMT=?=$14,682.42

EFFECTIVE ANNUAL RATE VERSUS ANNUAL PERCENTAGE RATE

125. Using the example of a savings account, explain the difference between the effective annualrate and the annual percentage rate.

The effective annual rate is what you actually earn, the annual percentage rate is a quoted rate. If

interest is compounded during the year, the ending balance of a savings account cannot becalculated directly using the annual percentage rate. Also, in the case of the savings account, the

effective annual rate will always be higher than the annual percentage rate as long as the account iscompounded more than once a year and the interest rate is greater than zero.

PRESENT VALUE OF AN ANNUITY

126. There are three factors that affect the present value of an annuity. Explain what these three factorsare and discuss how an increase in each will impact the present value of the annuity.

The factors are the interest rate, payment amount, and number of payments. An increase in the

payment and number of payments will increase the present value, while an increase in the interest rate will decrease the present value.

FUTURE VALUE OF AN ANNUITY

127. There are three factors that affect the future value of an annuity. Explain what these three factors areand discuss how an increase in each will impact the future value of the annuity.

The factors are the interest rate, payment amount, and number of payments. An increase in any of

these three will increase the future value of the annuity.

PERPETUITY PAYMENTS

128. A friend who owns a perpetuity that promises to pay $1,000 at the end of each year, forever, comesto you and offers to sell you all of the payments to be received after the 25th year for a price of $1,000. At an interest rate of 10 percent, should you pay the $1,000 today to receive paymentnumbers 26 and onwards? What does this suggest to you about the value of perpetual payments?

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 31/52

The present value of the perpetuity is $10,000, and the present value of the first 25 payments is

$9,077.04, thus you should be willing to pay only $922.96 for payments 26 and onwards. This suggests that the value of a perpetuity is derived primarily from the payments received early in itslife, and the payments to be received later have little worth today.

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 32/52

SOLUTIONS TO TEST BANK PROBLEMS

Chapter 4

21. Enter 1 6.5 5325 N I/Y PV PMT FV

Solve for -5,000

22. Simple Interest = $10,000 (.08)(3) = $2,400;Compound Interest = $10,000((1.075)3 1) = $2,422.97;Difference = $2,422.97 - $2,400 = $22.97

23. $7,000 (1.06)4 = $8,837.34

24.

+−

×=

×

12

06.

)12

06.1/(11

100$

124

APV = $100 × 42.5803 = $4,258.03

Enter 4×

12 6/12 100 N I/Y PV PMT FVSolve for -4,258.03

25.

+−

×=

12

08.

)12

08.1/(11

200,1$

100

APV = $1,200 × 72.816858 = $87,380.23

Enter 100 8/12 1,200 N I/Y PV PMT FV

Solve for -87,380.23

26.

+−

×=

×

12

049.

)12

049.1/(11

160$

125

APV = $160 × 53.11957 = $8,499.13

Enter 5× 12 4.9/12 -160 N I/Y PV PMT FV

Solve for 8,499.13

27.

+−

×=

×

12

065.

)12

065.1/(11

641$

1210

APV = $641 × 88.0685 = $56,451.91

Enter 10× 12 6.5/12 641 N I/Y PV PMT FV

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 33/52

Solve for -56,451.91

28.

+−

×=

×

52

05.

)52

05.1/(11

25$

2052

APV = $25 × 657.2215 = $16,430.54

Enter 20× 52 5/52 25 N I/Y PV PMT FV

Solve for -16,430.54

29.[ ]

+−

×=12.

)12.1/(11000,50$

5

APV = $50,000 × 3.6047762 = $180,238.81

Enter 5 12 50,000 N I/Y PV PMT FV

Solve for -180,238.81

30.

+×

+−

×=

×

12

0325.1

12

0325.

)12

0325.1/(11

500,1$

125

PV Adue = $1,500 × 55.30972726 ×

1.002708333 = $83,189.29

Enter 5× 12 3.25/12 -1,500BGN N I/Y PV PMT FV

Solve for 83,189.29

31.[ ]

( )015.1015.

)015.1/(1120$

6

+×

+−

×= PV Adue = $20 × 5.697187165 × 1.015 =

$115.65

Enter 6 1.5 -20BGN N I/Y PV PMT FV

Solve for 115.65

32.[ ]

( )07.1

07.

)07.1/(11000,12$

10

+×

+−

×= PV Adue = $12,000 × 7.023582 × 1.07 =

$90,182.79

Enter 10 7 12,000BGN N I/Y PV PMT FV

Solve for -90,182.79

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 34/52

33.[ ]

+−

×=085.

)085.1/(11000,10$

25

APV = $10,000 × 10.234191 = $102,341.91

Enter 25 8.5 10,000 N I/Y PV PMT FV

Solve for -102,341.91

[ ]( )085.1

085.

)085.1/(11000,10$

25

+×

+−×= PV A

due = $10,000 × 10.234191 × 1.085 =

$111,040.97

Enter 25 8.5 10,000BGN N I/Y PV PMT FV

Solve for -111,040.97

Difference = $111,040.97 - $102,341.91 = $8,699.06 = $8,699 (rounded) Note: The difference = .085 × $102,341.91 = $8,699.06

34.[ ]

( )075.1075.

)075.1/(11000,5$

20

+×

+−

×= PV Adue = $5,000 × 10.194491

× 1.075 = $54,795.39

Enter 20 7.5 5,000BGN N I/Y PV PMT FV

Solve for -54,795.39

[ ]

+−×=

075.)075.1/(1139.795,54$20

C ; C = $5,375

Enter 20 7.5 54,795.39 N I/Y PV PMT FV

Solve for -5,375

Because each payment is received one year later, then the cash flow has to equal:

$5,000 × (1 + .075) = $5,375

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 35/52

35.

+×

+−

×=

×

12

08.1

12

08.

)12

08.1/(11

100$

125

PV Adue = $100 × 49.318409 × 1.006667 =

$4,964.72

Enter 5× 12 8/12 100BGN N I/Y PV PMT FV

Solve for -4,964.72

+−

×=

×

12

08.

)12

08.1/(11

100$

125

APV = $100 × 49.318409 = $4,931.84

Enter 5× 12 8/12 100

N I/Y PV PMT FVSolve for -4,931.84

Difference = $4,964.72 - $4,931.84= $32.88

Note: Difference 88.32$12

08.84.931,4$ =

×=

36.06.

1)06.1(000,1$

5 −+×= AFV = $1,000 × 5.63709 = $5,637.09

Enter 5 6 1,000 N I/Y PV PMT FV

Solve for -5,637.09

37.08.

1)08.1(400,2$

3 −+×= AFV = $2,400 × 3.2464 = $7,791.36

Enter 3 8 2,400 N I/Y PV PMT FV

Solve for -7,791.36

38.085.

1)085.1(000,3$

25 −+×= AFV = $3,000 × 78.667792 = $236,003.38

Enter 25 8.5 -3,000 N I/Y PV PMT FV

Solve for 236,003.38

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 36/52

39.09.

1)09.1(000,3$

30 −+×= AFV = $3,000 × 136.3075385 = $408,922.62

Enter 30 9 -3,000 N I/Y PV PMT FV

Solve for 408,922.62

( )09.109.

1)09.1(000,3$

30

+×−+×= FV Adue

= $3,000 × 136.3075385 × 1.09 =

$445,725.65

Enter 30 9 -3,000BGN N I/Y PV PMT FV

Solve for 445,725.65

Difference = $445,725.65 - $408,922.62 = $36,803.03

Note: Difference = $408,922.62 × .09 = $36,803.03

40.

+−

×=

×

12

059.

)12

059.1/(11

600,5$

124

C ; $5,600 = C × 42.66356; C = $131.26

Enter 4× 12 5.9/12 5,600 N I/Y PV PMT FV

Solve for -131.26

41.

+−

×=

×

12

075.

)12

075.1/(11

000,149$

1230

C ; $149,000 = C × 143.0176; C = $1,041.83

Enter 30× 12 7.5/12 149,000 N I/Y PV PMT FV

Solve for -1,041.83

Total interest = ($1,041.83 × 30 × 12) - $149,000 = $226,058.80 = $226,059 (rounded)

42.065.

1)065.1(000,000,25$

10 −+×=C ; $25,000,000 = C × 13.49442254; C = $1,852,617.25

Enter 10 6.5 25,000,000 N I/Y PV PMT FV

Solve for -1,852,617.25

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 37/52

43.

+−

×=

×

12

045.

)12

045.1/(11

900,464$

1227

C ; $464,900 = C × 187.3639893; C =

$2,481.27

Enter 27× 12 4.5/12 -464,900 N I/Y PV PMT FV

Solve for 2,481.27

44. Amount financed = $1,200,000 × (1 - .2) = $960,000

+−

×=

×

12

0775.

)12

0775.1/(11

000,960$

1215

C ; $960,000 = C × 106.2387933;

C = $9,036.25

Enter 15× 12 7.75/12 960,000 N I/Y PV PMT FV

Solve for -9,036.25

45.

+−

×=

×

12

065.

)12

065.1/(11

500,24$

125

C ; $24,500 = C × 51.10864813; C = $479.37

Enter 5× 12 6.5/12 24,500 N I/Y PV PMT FV

Solve for -479.37

46. Amount financed = $6,890 - $500 = $6,390

+−

×=

12

079.

)12

079.1/(11

390,6$

36

C ; $6,390 = C × 31.95885; C = $199.94

Enter 36 7.9/12 6,390 N I/Y PV PMT FV

Solve for -199.94

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 38/52

47.

+−

×=

×

4

055.

)4

055.1/(11

500$

425

APV = $500 × 54.16588 = $27,082.94

Enter 25× 4 5.5/4 500 N I/Y PV PMT FV

Solve for -27,082.94

48.

+×

+−

×=12

049.1

12

049.

)12

049..1/(11

299$

60

PV Adue = $299 × 53.1195698 ×

1.00408333 = $15,947.61

Enter 60 4.9/12 -299BGN N I/Y PV PMT FV

Solve for 15,947.61

49.[ ]

( )0635.10635.

)0635.1/(11500,2$

50

+×

+−

×= PV Adue = $2,500 × 15.0230089 × 1.0635

= $39,942.42

Enter 50 6.35 2,500BGN N I/Y PV PMT FV

Solve for -39,942.42

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 39/52

50. Ending value at 4% simple interest = $1,000 + ($1,000 × .04 × 5) = $1,200.00; Ending value at

4% compounded annually = $1,000 × (1 +.04)5 = $1,216.65;Difference = $1,216.65 - $1,200.00 = $16.65

Enter 5 4 -1,000 N I/Y PV PMT FV

Solve for 1,216.65

51. ( )047.1047.

1)047.1(000,250$

3

+×−+

×=C ; $250,000 = C × 3.143209 × 1.047 =

$75,966.14

Enter 3 4.7 250,000 N I/Y PV PMT FV

Solve for -75,966.14

52. ( )005.1005.

1)005.1()50.1140($1235

+×−+××=×

FV Adue

= $210 × 1,424.710299 ×

1.005 = $300,685.11

Enter 35× 12 .5 -(140× 1.5)BGN N I/Y PV PMT FV

Solve for 300,685.11

53.[ ]

+−×=

045.

)045.1/(11000,6$000,100$

t

; ln4 = t × ln1.045; t = 31.49

Enter 4.5 -100,000 6,000 N I/Y PV PMT FV

Solve for 31.49

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 40/52

54.

+−

×=

12

09.

)12

09.1/(11

84.143$85.954,4$

t

; ln1.3483489 = t × ln1.0075; t = 40

Enter 9/12 4,954.85 -143.84 N I/Y PV PMT FV

Solve for 40

55.

12

06.

1)12

06.1(

000,450$000,000,136$−+

×=

t

; ln 2.5111111 = t × ln1.005; t = 184.61

Note: t is stated in the number of months.

Enter 6/12 -450,000 136,000,000

N I/Y PV PMT FVSolve for 184.61

56.

+×

+−

×=1 2

0.

.

1

1 2.0 3.

)1 2.

0 3.1/ (11

5 0 0,2$9 2 6,4 1 3$

t

; t × ln.00249688 = ln.532549498; t = 213.29

Note: t is expressed in months

Enter 3/12 -413,926 2,500BGN N I/Y PV PMT FV

Solve for 213.29

57.

+×

+−

×=365

21.1

365

21.

)365

21.1/(11

76.30$000,25$

t

; t × ln.000575177 = ln.629865908;

t = 1,095.08 days = 3 years

Enter 21/365 25,000 -30.76BGN N I/Y PV PMT FV

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 41/52

Solve for 1095.08

1095.08 days ÷ 365 days = 3 years

58.

+−

×=

12

)

12

1/(11

35.894,4$900,123$

30

r

r

; This can not be solved directly, so it’s

easiest to just use the calculator method to get an answer. You can then use the calculator answer as the rate in the formula just to verify that your answer is correct.

Enter 30 /12 -123,900 4,894.35 N I/Y PV PMT FV

Solve for 13.59

59.

+−×=

×

12

)12

1/(11

40.384$000,100$

1240

r

r

; This can not be solved directly, so it’s

easiest to just use the calculator method to get an answer. You can then use the calculator answer as the rate in the formula just to verify that you answer is correct.

Enter 40× 12 /12 -100,000 384.40 N I/Y PV PMT FV

Solve for 3.45

60.

12

1)121(120$19.341,47$

1215

r

r

−+×=

×

; This can not be solved directly, so it’s easiest to

just use the calculator method to get an answer. You can then use the calculator answer as therate in the formula just to verify that you answer is correct.

Enter 15× 12 /12 -120 47,341.19 N I/Y PV PMT FV

Solve for 9.46

61.

r

r 1)1(000,136$000,685$

4 −+×= ; This can not be solved directly, so it’s easiest to just

use the calculator method to get an answer. You can then use the calculator answer as the ratein the formula just to verify that you answer is correct.

Enter 4 -136,000 685,000 N I/Y PV PMT FV

Solve for 15.59

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 42/52

62.

( )

+×

−+×=

×−

121

12

1)12

1(25$66.482,4$

121021

r

r

r

; This can not be solved directly, so

it’s easiest to just use the calculator method to get an answer. You can then use the calculator

answer as the rate in the formula just to verify that you answer is correct.

Enter (21-10)× 12 /12 -25BGN 4,482.66 N I/Y PV PMT FV

Solve for 5.29To more decimal places, the answer is 5.28632 percent.

63.

( )

+×

−+×=

×−

3651

365

1)365

1(25$000,000,1$

3652140

r

r

r

; This can not be solved directly,

so it’s easiest to just use the calculator method to get an answer. You can then use the calculator answer as the rate in the formula just to verify that you answer is correct.

Enter (40-21)× 365 /365 -25BGN 1,000,000 N I/Y PV PMT FV

Solve for 15.07To more decimal places, the answer is 15.0697117 percent.

64.( )

+

×+

+

×+

+

×=321 )14.1(

1000,15$

)14.1(

1000,9$

14.1

1000,5$ PV ; PV =

$21,435.74

Enter 1 14 5,000 N I/Y PV PMT FV

Solve for -4,385.96

Enter 2 14 9,000 N I/Y PV PMT FV

Solve for -6,925.21

Enter 3 14 15,000 N I/Y PV PMT FV

Solve for -10,124.57

Present value = $4,385.96 + $6,925.21 + $10,124.57 = $21,435.74

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 43/52

65.( )

+

×+

+

×+

+×=

321 )04.1(

1000,2$

)04.1(

1500,1$

04.1

1200,1$ PV ; PV =

$4,318.67

Enter 1 4 1,200

N I/Y PV PMT FVSolve for -1,153.85

Enter 2 4 1,500 N I/Y PV PMT FV

Solve for -1,386.83

Enter 3 4 2,000 N I/Y PV PMT FV

Solve for -1,777.99

Present value = $1,153.85 + $1,386.83 + $1,777.99 = $4,318.67

66.( )

+

×+

+

×+

+

×=321 )05.1(

1000,10$

)05.1(

1500,7$

05.1

1000,5$ PV ; PV =

$20,203.00

Enter 1 5 5,000 N I/Y PV PMT FV

Solve for -4,761.90

Enter 2 5 7,500 N I/Y PV PMT FV

Solve for -6,802.72

Enter 3 5 10,000 N I/Y PV PMT FV

Solve for -8,638.38

Present value = $4,761.90 + $6,802.72 + $8,638.38 = $20,203.00

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 44/52

67.

( )

+

×+

+

×+

+

×+=321 )06.1(

1000,60$

)06.1(

1000,55$

06.1

1000,52$000,2$ PV

PV = $150,383.56

Enter 1 6 52,000 N I/Y PV PMT FV

Solve for -49,056.60

Enter 2 6 55,000 N I/Y PV PMT FV

Solve for -48,949.80

Enter 3 6 60,000 N I/Y PV PMT FV

Solve for -50,377.16

Present value = $2,000 + $49,056.60 + $48,949.80 + $50,377.16 = $150,383.56

68.( )

+

×+

+

×+

+×=

321 )09.1(

1900,2$

)09.1(

1800,1$

09.1

1200,1$ PV ; PV =

$4,855.27

Enter 1 9 1,200 N I/Y PV PMT FV

Solve for -1,100.92

Enter 2 9 1,800

N I/Y PV PMT FVSolve for -1,515.02

Enter 3 9 2,900 N I/Y PV PMT FV

Solve for -2,239.33

Present value = $1,100.92 + $1,515.02 + $2,239.33 = $4,855.27

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 45/52

69.( )

+

×+

+

×+

+×=

321 )11.1(

1000,2$

)11.1(

1000,9$

11.1

1600,5$ PV ; PV =

$13,812.03

Enter 1 11 5,600

N I/Y PV PMT FVSolve for -5,045.05

Enter 2 11 9,000 N I/Y PV PMT FV

Solve for -7,304.60

Enter 3 11 2,000 N I/Y PV PMT FV

Solve for -1,462.38

Present value = $5,045.05 + $7,304.60 + $1,462.38 = $13,812.03

70.( )

+

×+

+

×+

+×=

321 )03.1(

1400,5$

)03.1(

1000,5$

03.1

1200,4$ PV ; PV =

$13,732.41

Enter 1 3 4,200 N I/Y PV PMT FV

Solve for -4,077.67

Enter 2 3 5,000 N I/Y PV PMT FV

Solve for -4,712.98

Enter 3 3 5,400 N I/Y PV PMT FV

Solve for -4,941.76

Present value = $4,077.67 + $4,712.98 + $4,941.76 = $13,732.41

71.

+

×+=2)0875.1(

1000,100$000,100$ PV ; PV = $184,555.42

Enter 2 8.75 100,000

N I/Y PV PMT FVSolve for -84.555.42

Present value = $100,000 + $84,555.42 = $184,555.42

You should accept the $189,000 today since it is the higher net present value.

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 46/52

72.

+

×+

+

×+=21 )06.1(

1000,25$

)06.1(

1000,15$000,5$ PV

PV = $41,400.85

Enter 1 6 -15,000

N I/Y PV PMT FVSolve for 14,150.94

Enter 2 6 -25,000 N I/Y PV PMT FV

Solve for 22,249.91

Present value = $5,000.00 + $14,150.94 + $22,249.91 = $41,400.85

73.345 )07.1(500,7$)07.1(000,5$)07.1(600,3$ ×+×+×= FV ; FV = $20,790.99

Enter 5 7 -3,600

N I/Y PV PMT FVSolve for 5,049.19

Enter 4 7 -5, 000 N I/Y PV PMT FV

Solve for 6,553.98

Enter 3 7 -7,500 N I/Y PV PMT FV

Solve for 9,187.82

Future value = $5,049.19 + $6,553.98 + $9,187.82 = $20,790.99

74. 250,2$)06.1(600,9$)06.1(180,5$ 12 +×+×= FV ; FV = $18,246.25

Enter 2 6 -5,180 N I/Y PV PMT FV

Solve for 5,820.25

Enter 1 6 -9,600 N I/Y PV PMT FV

Solve for 10,176.00

Future value = $5,820.25 + $10,176.00 + $2,250.00 = $18,246.25

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 47/52

75. 510,4$0)09.1(820,9$ 2 ++×= FV ; FV = $16,177.14

Enter 2 9 -9,820 N I/Y PV PMT FV

Solve for 11,667.14

Future value = $11,667.14 + $0 + $4,510.00 = $16,177.14

76. 0$)0725.1(100,2$)0725.1(800,6$ 12 +×+×= FV ; FV = $10,073.99

Enter 2 7.25 -6,800 N I/Y PV PMT FV

Solve for 7,821.74

Enter 1 7.25 -2,100 N I/Y PV PMT FV

Solve for 2,252.25

Future value = $7,821.74 + $2,252.25 + $0 = $10,073.99

77.232425 )11.1(000,25$)11.1(000,15$)11.1(000,10$ ×+×+×= FV

FV = $595,098.67

Enter 25 11 -10,000 N I/Y PV PMT FV

Solve for 135,854.64

Enter 24 11 -15,000 N I/Y PV PMT FV

Solve for 183,587.35

Enter 23 11 -25,000 N I/Y PV PMT FV

Solve for 275,656.68

Future value = $135,854.64 + $183,587.35 + $275,656.68 = $595,098.67

78. 500,2$)03.1(500,2$)03.1(500,2$)03.1(000,10$ 123 +×+×+×= C ; C=

$2,079.89

Enter 3 3 -2,500 10,000 N I/Y PV PMT FV

Solve for 2,079.89

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 48/52

79. 000,250$)035.1(000,250$)035.1(000,100$ 12 +×+×= FV ; C= $615,872.50

Enter 2 3.5 -100,000 N I/Y PV PMT FV

Solve for 107,122.50

Enter 1 3.5 -250,000 N I/Y PV PMT FV

Solve for 258,750.00

FV = $107,122.50 + $258,750.00 + $250,000 = $615,872.50

80.0425.

000,150= PV ; PV = $3,529,411.77

81.09.

50.4$= PV ; PV = $50.00

82.0275.

000,50= PV ; PV = $1,818,181.82

83.000,350$

000,12$=r ; r = 3.43 percent

84.000,285$

000,10$=r ; r = 3.51 percent

85. 04.000,150$ ×=C ; C = $6,000

86. 084.00.50$ ×=C ; C = $4.20

87. APR = .015 × 12 = .18 = 18 percent

88. APR = .02 × 4 = .08= 8 percent

89. 112

1138.

12

−

+= APR

; APR = 13.00 percent

Enter 13.8 12

NOM EFF C/YSolve for 13.00

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 49/52

90. 14

0764.1

4

−

+= EAR ; EAR = 7.86 percent

Enter 7.64 4 NOM EFF C/Y

Solve for 7.86

91. 112

149.1

12

−

+= EAR ; EAR = 15.96 percent

Enter 14.9 12 NOM EFF C/Y

Solve for 15.96

92. 1365

21.1

365

−

+= EAR ; APR = 23.36 percent

Enter 21 365 NOM EFF C/Y

Solve for 23.36

93. 1365

0745.1

365

−

+=

A EAR ; APR = 7.73 percent

Enter 7.45 365 NOM EFF C/Y

Solve for 7.73

12

075.1

2

−

+=

B EAR ; APR = 7.64 percent

Enter 7.5 2 NOM EFF C/Y

Solve for 7.64

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 50/52

94. EAR A = 3.75 percent

112

037.1

12

−

+=

B EAR ; EAR = 3.76 percent

Enter 3.7 12 NOM EFF C/Y

Solve for 3.76

12

037.1

2

−

+=

C EAR ; EAR = 3.73 percent

Enter 3.7 2 NOM EFF C/Y

Solve for 3.73

171828.210365.0365.

−=−= e EAR D ; EAR = 3.72 percent

Using ex on a financial calculator: EAR = 3.72 percentOn the Texas Instruments BA II Plus, the input is:.0365, 2nd, ex, -1, = .0372 = 3.72 percent

14

0366.1

4

−

+=

E EAR ; EAR = 3.71 percent

Enter 3.66 4 NOM EFF C/Y

Solve for 3.71

Account B offers the highest effective annual rate at 3.76 percent.

95. 171828.21 149.149.−=−=e EAR ; EAR = 16.07 percent

Using ex on a financial calculator: EAR = 16.07 percentOn the Texas Instruments BA II Plus, the input is:.149, 2nd, ex, -1, = .1607 = 16.07 percent

96. 171828.21 0975.0975.−=−=e EAR ; EAR = 10.24 percent

Using ex on a financial calculator: EAR = 10.24 percentOn the Texas Instruments BA II Plus, the input is:.0975, 2nd, ex, -1, = .1024 = 10.24 percent

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com

http://slidepdf.com/reader/full/chapter4-how-we-got-the-solutions 51/52

97. 171828.21 079.079.−=−=e EAR ; EAR = 8.22 percent

Using ex on a financial calculator: EAR = 8.22 percentOn the Texas Instruments BA II Plus, the input is:.079, 2nd, ex, -1, = .0822 = 8.22 percent

98. 171828.21 05.05.−=−=e EAR ; EAR = 5.127 percent

Using ex on a financial calculator: EAR = 5.127 percentOn the Texas Instruments BA II Plus, the input is:.05, 2nd, ex, -1, = .05127 = 5.127 percent

Additional interest = $1,000 × (.05127 - .05) = $1.27

99. Future value = $28,500 × (1 + .035)15 = $47,747.44

Enter 15 3.5 -28,500 N I/Y PV PMT FV

Solve for 47,747.44

100. Future value = $189,900 × (1 + .045)6 = $247,299.20

Enter 6 4.5 -189,900 N I/Y PV PMT FV

Solve for 247,299.20

101. Present value = $5,539.92 × [1 ÷ (1 + .0425)17] = $2,730.30

Enter 17 4.25 5,539.92 N I/Y PV PMT FV

Solve for -2,730.30

102. Present value = $40,000 × [1 ÷ (1 + .063)13] = $18,077.05

Enter 13 6.3 40,000 N I/Y PV PMT FV

Solve for -18,077.05

103. $3,142.50 = $3,000 × (1 + r)1; r = 4.75 percent

Enter 1 -3,000 3,142.50 N I/Y PV PMT FV

Solve for 4.75

104. $107,921 = $2,500 × (1 + r)40; r = 9.87 percent

Enter 40 -2,500 107,921 N I/Y PV PMT FV

Solve for 9.87

5/12/2018 Chapter4 How We Got the Solutions - slidepdf.com