chapter v analysis of investment...

TRANSCRIPT

155

CHAPTER – V

ANALYSIS OF INVESTMENT BEHAVIOUR

5.1 Introduction

5.2 Descriptive Analysis

5.3 Analysis of the Investment Particulars

5.4 An Analysis of the Preferences of the Investors Based on

the Weighted Mean Values

5.5 An Analysis of Different Behaviour in Investing

5.6 Differential Analysis

5.7 Association Between Gender and Various Behavioural Issues

5.8 Association Between Demographic Factors and Investment

Preferences

5.9 Association Between Savings and Demographic Factors

5.10 Association Between Average Rate of Return and

Other Variables

5.11 Association Between Demographic Factors Investment

Characteristics

5.12 Relational Analysis

156

CHAPTER – V

ANALYSIS OF INVESTMENT BEHAVIOUR

5.1 INTRODUCTION

The investment behaviour of the individual investors are analysed in

this chapter using the data collected from the respondents. Data analysis is a

vital component in any research study. The collected data are to be

processed carefully, classified systematically and tabulated scientifically.

Appropriate treatment is possible only if the data is analysed rationally. The

collected data were analysed in realization of the objectives.

The data are studied from as many dimensions as possible to draw

new insights into the investor behaviour. The data obtained on the variables

were subjected to statistical analysis. The analysis was categorized under

- Descriptive Analysis

- Differential Analysis

- Relational Analysis

157

5.2 DESCRIPTIVE ANALYSIS

It provides information about the nature of a particular group of

individuals. Mean, Median and percentages are used for the purpose of the

analysis.

In this research the investigator assessed the respondents by their

demographic characteristics, investments owned, investment features,

returns, diversifications of the portfolio, time spent for investing activity,

leveraging in investment and experience in stock market. The percentages

were found and the analysis was done as under

Following are the tables provided for analysis of demographics:

Table – 5.1 Details of Individual Investors

Table – 5.2 Marital Status and Number of Dependents

Table – 5.3 Annual Income and Annual Savings in Rupees

158

TABLE – 5.1

DETAILS OF INDIVIDUAL INVESTORS

S.NO. INVESTOR PARTICULARS NUMBER OF RESPONDENTS

PERCENTAGE

1. Gender Male 256 85.3

Female 44 14.7

2. Age Less than 30 26 8.7

30-45 105 35.0

45-60 127 42.3

Above 60 42 14.0

3. Academic Qualifications

School final 22 7.3

Graduate 124 41.3

Post graduate 81 27.0

Professional 73 24.3

4. Occupation Self employed 74 24.7

Employed in government 28 9.3

Employed in private 133 44.3

Retired 65 21.7

The above table 5.1 shows that 256 of the respondents are men and

the rest are women. Generally men bear the financial responsibility in our

culture and therefore they take most of the investment decisions at home to

fulfil the financial obligations. When it comes to age, it is found that only 26

159

investors (8.7%) belong to the age group of less than 30.Hence it can be

inferred that the younger generation do not think of savings and investments

in their early phase of employment or business. Investors in the age group of

30-45 are 105 in number constituting 35%. Similarly investors in the age

group of 45 to 60 also save and invest. An interesting finding is that 14% of

investors are above the age of 60. Among the respondents, 22 respondents

(7.3%) are investors with a High School or Matriculation diploma, whereas the

majority of the investors are graduates having the maximum number of

representation (41.3%) followed by Post graduates and Professionals

constituting 27% and 24.3 % respectively. As regards occupation, 44.3% of

the investors are employed in the private sector; 24.7% are self employed;

9.3% are employed in Government and the rest of the 21.7% are retired. Even

retired people invest in shares and mutual funds.

160

FIGURE – 5.1

DETAILS OF INDIVIDUAL INVESTORS

GENDER AGE ACADEMIC QUALIFICATION OCCUPATION

PE

RC

EN

TA

GE

161

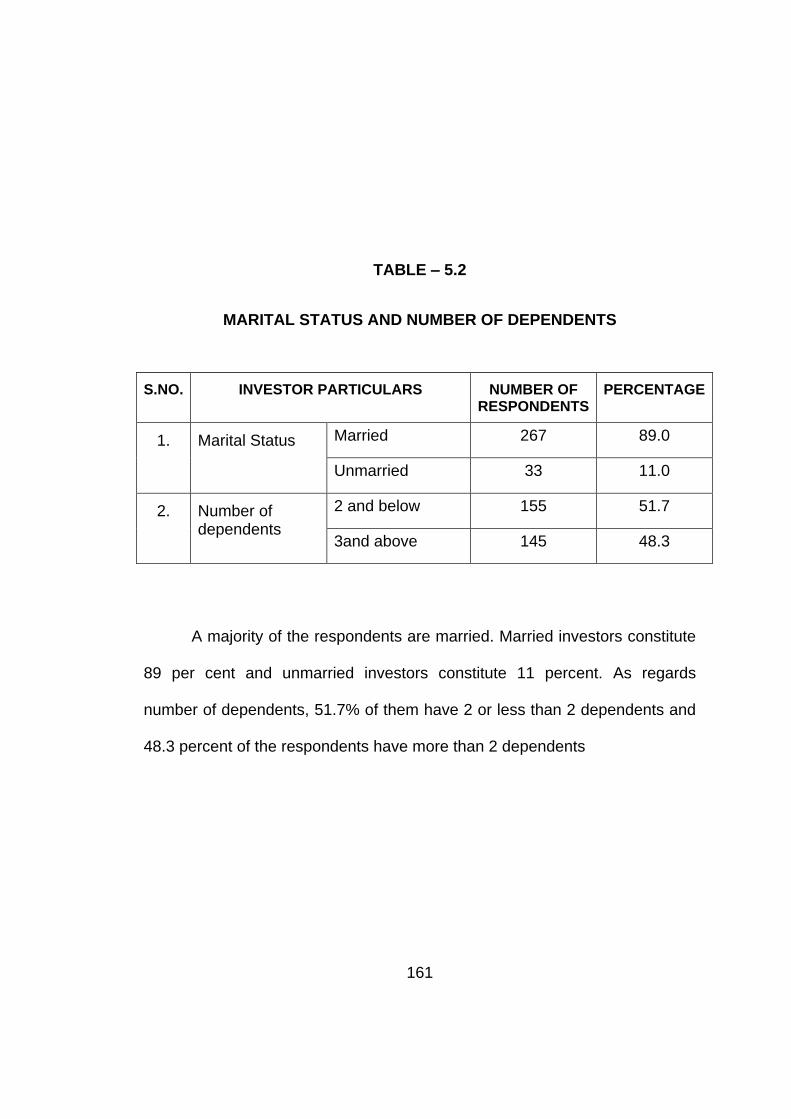

TABLE – 5.2

MARITAL STATUS AND NUMBER OF DEPENDENTS

S.NO. INVESTOR PARTICULARS NUMBER OF RESPONDENTS

PERCENTAGE

1. Marital Status Married 267 89.0

Unmarried 33 11.0

2. Number of dependents

2 and below 155 51.7

3and above 145 48.3

A majority of the respondents are married. Married investors constitute

89 per cent and unmarried investors constitute 11 percent. As regards

number of dependents, 51.7% of them have 2 or less than 2 dependents and

48.3 percent of the respondents have more than 2 dependents

162

FIGURE – 5.2

MARITAL STATUS AND NUMBER OF DEPENDENTS

MARITAL STATUS NUMBER OF DEPENDENTS

PE

RC

EN

TA

GE

163

TABLE – 5.3

ANNUAL INCOME AND ANNUAL SAVINGS IN RUPEES

S.NO. INVESTOR PARTICULARS NUMBER OF RESPONDENTS

PERCENTAGE

1. Annual Income

Below 2 lakhs 80 26.7

2-4 Lakhs 121 40.3

4-6 Lakhs 29 9.7

6 Lakhs and above 70 23.3

2. Annual Savings

Less than Rs. 25000/- 65 21.7

Rs. 25,000 – Rs. 50,000/- 61 20.3

Rs. 50,000/- - 1 lakh 56 18.7

1 lakh and above 118 39.3

As regards annual income a majority of the respondents (40.3%) have

income ranging from 2 to 4 lakhs followed by 70 (26.7%) respondents in the

income group of below 2 lakhs. 23.3 per cent of the investors earn above 6

lakhs per annum. Those who earn 4 to 6 lakhs constitute 9.7 per cent. An

interesting feature is that investors earning less than 2 lakhs too have

investments in capital market.

The investors who save 1 lakh and above per annum are 118 (39.3%)

followed by investors who save less than Rs. 25,000 per annum numbering

65 (21.7%). Those who save between Rs. 25,000 – Rs. 50,000/- per annum

are 61, constituting 20.3 per cent and 56 respondents save between Rs.

50000/- – Rs. 1,00,000/- per annum.

164

FIGURE – 5.3

ANNUAL INCOME AND ANNUAL SAVINGS IN RUPEES

ANNUAL INCOME ANNUAL SAVINGS

PE

RC

EN

TA

GE

OF

RE

SP

ON

DE

NT

S

165

5.3 ANALYSIS OF THE INVESTMENT PARTICULARS

In this part of the study the details relating to the investment are

analysed using simple percentages for assessing the respondents with

respect to their preferences for various types of assets, rate of returns earned

and other details.

The following tables are provided under this analysis.

Table – 5.4 Ownership of Assets

Table – 5.5 Details about Investments

Table – 5.6 Time Spent for Investing Activities

Table – 5.7 Leverage in Investing

Table – 5.8 Shares in Delisted Companies

Table – 5.9 Rate of Return and Experience in Stock Market

Table – 5.10 Diversification of Portfolio

166

TABLE – 5.4

OWNERSHIP OF ASSETS

S.NO. INVESTOR PARTICULARS NUMBER OF RESPONDENTS

PERCENTAGE

1. Ownership of residential house

Yes 253 84.3

No 47 15.7

2. Have Mortgage Loan Yes 78 26.0

No 222 74.0

3. Ownership of Assets -

Bank deposit

Yes 234 78.0

No 66 22.0

4. Ownership of Assets -

Postal savings

Yes 90 30.0

No 210 70.0

5. Ownership of Assets -

Insurance Policies

Yes 166 55.3

No 134 44.7

A majority of the investors have houses of their own. 84.3 per cent of

the investors have house property and 15.7 per cent do not own a house.

From the above data it is clear that ownership of residential house property is

a preferred investment for a majority of the investors. Bank deposits are a

preferred form of investment for 78 per cent of the investors. Postal Savings

are preferred by 90 investors constituting 70 per cent of the sample investors.

Insurance policies are taken by 55.3 per cent of the investors. From the above

167

it is clear that investment in house property is the most preferred asset of the

sample investors. Savings in Post office is not preferred much as shown by

the above table compared to Bank deposits. 26 percent of the investors have

mortgage loan. The above details relating to the assets owned by individual

investors in capital market prove the theory of Behavioural Portfolio of

Investors suggested by Hersh Shefrin and Meir Statman. According to them

the psychological tendencies of investors prod them to build their portfolios as

a pyramid. It explains the several goals an investor has such as safety,

income, and growth and hence he/she invests in house property, bank

deposits and insurance products along with their investments in capital

market.

168

FIGURE – 5.4

OWNERSHIP OF ASSETS

Yes No

Residential House Mortage Loan Bank Deposits Postal Savings Insurance Policies

PE

RC

EN

TA

GE

169

TABLE – 5.5

DETAILS ABOUT INVESTMENTS

S.NO. INVESTMENT NUMBER OF RESPONDENTS

PERCENTAGE

1. Form of Investments

All in Demat form 226 75.3

Mostly in demat form 50 16.7

All in Physical form 21 7.0

Mostly in Physical form 3 1.0

2. Mode of transaction

Trading through Broker 181 60.3

Using Internet 113 37.7

Others 6 2.0

From the above table 5.5 it is clear that 75.3 per cent of the

respondents have all the investments in dematerialised form and 7 percent of

the respondents have all their investments in physical form. 16.7 per cent of

the investors have most of their investments in dematerialised form and 1 per

cent of the investors have most of their investments in dematerialised form. It

is inferred from the above table that majority of the investors have shifted to

electronic form of securities and the remaining investors are also in the

process of converting to the electronic form.

The most preferred method of trading by the investors is through

brokers (60.3%) followed by internet trading (37.7%) and other methods of

trading constitute 2 percent. From the above it is clear that broker-

dependence is very high among the investors for trading even though internet

trading facility is available.

170

FIGURE – 5.5

DETAILS ABOUT INVESTMENTS

PE

RC

EN

TA

GE

171

TABLE – 5.6

TIME SPENT FOR INVESTING ACTIVITIES

S.NO. INVESTOR PARTICULARS NUMBER OF RESPONDENTS

PERCENTAGE

1. Time spend for investing activities

2-5 hours per week 57 19.0

2-5 hours per month 83 27.7

2-5 hours per year 5 1.7

Most of my spare

time

21 7.0

Every day at least

some time

134 44.7

The above table 5.6 shows that 19 per cent of the investors spend 2-5

hours per week for investment activities; 27.7 per cent spend 2-5 hours per

month and 1.7 per cent spend 2-5 hours per year and a majority of the

investors spend some time every day for investment related activities. It is a

positive aspect of the investors since the time spent for knowing the different

types of investments and other details will help increase the financial literacy

of the respondents.

172

FIGURE – 5.6

TIME SPENT FOR INVESTING ACTIVITIES

TIME SPENT IN HOURS

173

TABLE – 5.7

LEVERAGE IN INVESTING

S.NO. LEVERAGE IN INVESTING NUMBER OF RESPONDENTS

PERCENTAGE

1. Borrow and invest in

stock market

Yes 24 8.0

No 276 92.0

Using leverage in investing is a method for increasing the profit. But it

involves risks as well. From the above table it is understood that only 8 per

cent of the respondents borrow and invest in stock market. Hence majority of

the investors are conservative.

FIGURE – 5.7

LEVERAGE IN INVESTING

YES

NO

174

TABLE – 5.8

SHARES IN DELISTED COMPANIES

S.NO. DELISTED COMPANIES NUMBER OF RESPONDENTS

PERCENTAGE

1. Have Shares in

Delisted companies

Yes 58 19.3

No 242 80.7

The above table 5.8 shows that 19.3 per cent of the investors have

shares in delisted companies. Having shares in delisted companies (delisted

by stock exchanges for default) puts the shareholders in difficulty. From the

above table we understand that the problem of delisted companies still exists

in spite of the regulatory measures.

As per the survey conducted by L.C Gupta in 2004, 37.61 per cent of

the respondents were holding shares in delisted companies. Delisted

companies are a fit subject for further research since the retail investors have

to be protected in the future from the clutches of these companies. There

should be some mechanism by the regulatory authorities to warn the investors

of the impending danger attached to a company likely to be delisted.

175

FIGURE – 5.8

SHARES IN DELISTED COMPANIES

YES NO

176

TABLE – 5.9

RATE OF RETURN AND EXPERIENCE IN STOCK MARKET

S.NO. RATE OF RETURN AND EXPERIENCE IN

STOCK MARKET

NUMBER OF RESPONDENTS

PERCENTAGE

1. Average rate of return

(Past 5 years)

Below 10% 32 10.7

10-20 % 89 29.7

Above 20% 117 39.0

Net loss 62 20.7

2. Experience in

stock market

Less than 5yrs 97 32.3

5-10 yrs 66 22.0

Above 10 yrs 137 45.7

The above table 5.9 shows that 39 per cent of the investors earn an

average rate of return of above 20 per cent; 29.7 per cent earns an average

rate of return of 10-20 per cent; 10.7 per cent earn below 10 per cent and 20.7

per cent have incurred losses. As the level of risk is high in equity investing a

layman is not inclined to invest in stock market in India. The incurring of loss

by nearly 20 percent of the investors may be a reason for the low level of

retail participation in Indian Stock market.

177

FIGURE – 5.9

RATE OF RETURN AND EXPERIENCE IN STOCK MARKET

Average rate of return Experience in stock market

PE

RC

EN

TA

GE

OF

TH

E R

ES

PO

ND

EN

TS

178

TABLE – 5.10

DIVERSIFICATION OF PORTFOLIO

S.NO. DIVERSIFICATION OF PORTFOLIO NUMBER OF RESPONDENTS

PERCENTAGE

1. Number of companies in the portfolio

5 and below 72 24.0

6-15 137 45.7

16 and above 91 30.3

2. Number of sectors in the portfolio

3 and below 79 26.3

4-6 87 29.0

7 and above 134 44.7

The number of companies in the portfolio represents the diversification

of the portfolio. The above table 5.10 shows that there is a greater degree of

diversification compared to what is suggested by Investment Gurus. Warren

Buffet says that the ideal portfolio should contain no more than 10 good

stocks. But the above table shows that 30.3 per cent of the investors have

stocks in more than 16 companies and 45.7 per cent of the investors have

stocks in 6-15 companies. And 24 per cent have shares in less than 5

companies. When the portfolio involves a large number of stocks it becomes

difficult for the investor to keep track of the prospects.

The diversification in respect of the sector shows that 44.7 per cent of

the investors have shares in 7 or more sectors; 29 per cent have shares in 4-6

sectors and 26.3 per cent has shares in 3 and less than 3 sectors. This also

shows that there is a greater degree of diversification with respect to sectors

as well.

179

FIGURE – 5.10

DIVERSIFICATION OF PORTFOLIO

Number of companies in the portfolio Number of sectors in the portfolio

PE

RC

EN

TA

GE

180

5.4 AN ANALYSIS OF THE PREFERENCES OF THE INVESTORS

BASED ON THE WEIGHTED MEAN VALUES

The preferences of the investors towards investment goals, sources of

investment information, the qualities the investors expect from their Financial

Advisers, types of mutual funds and the Qualities they expect in a scheme are

analysed and ranked based on the responses given by the investors. The

responses for various parameters are given, scored in the Likert’ Rating scale

and the cumulative weights are used for ranking. It is termed as the Weighted

Mean Values.

The following tables are given under this analysis for the purpose of ranking.

Table – 5.11 Ranking of the Objectives of Savings

Table – 5-12 Ranking of the Sources of Investment Information

Table – 5-13 Ranking of the Preference for Shares

Table – 5.14 Ranking of the Basis for Buying Shares

Table – 5.15 Ranking of the Qualities of Financial Advisers

Table – 5.16 Ranking of the Preference for Mutual Funds

Table – 5.17 Ranking of the Qualities Expected of a Mutual Fund Scheme

181

i) OBJECTIVES OF SAVINGS

India is one of the countries with a growing rate in gross domestic

savings. Indians unlike their western counterparts save for many reasons.

Irrespective of the age and economic status saving is an integral part of their

financial planning. But the objectives of their savings vary from individual to

individual. An understanding of the goals of savings is helpful both for an

investor as well as for the institutions which offer various financial products for

the investors.

TABLE – 5.11

RANKING OF THE OBJECTIVES OF SAVINGS

Objectives of Savings WMV RANK

I save for my children’s education. 3.8 I

I save for my daughter’s marriage. 3.7 II

I save to provide for my retirement. 3.7 II

I save to purchase a house. 3.3 IV

I save for tax benefits. 3.3 IV

I save for contingencies. 2 VI

182

The objectives of savings are ranked in the above table using weighted

mean values of the responses given by the investors in the questionnaire.

Saving for children’s education takes the lead with the W.M.V. of 3.8. This is

in conformity with the study conducted by NCAER and Aviva Life (2010)

which says that 48 per cent of the people save for their children’s education.

This is followed by the other two objectives namely daughter’s marriage and

providing for retirement scoring the W.M.V of 3.7 each as the second rank;

Saving for tax benefits and purchasing a house are ranked as the IV objective

and saving for contingencies is the last objective Hence it is proved that

children’s education is the prime motive behind saving.

ii) SOURCES OF INVESTMENT INFORMATION

There are many sources of investment information. The sources which

are mainly used or preferred by the investors should be identified to

communicate with the investors very effectively. Individual investors are

widely scattered and a knowledge of the best media through which investors

can be contacted would offer many advantages to the financial intermediaries

and regulatory authorities. Financial Literacy programmes can be effectively

conducted by identifying the sources of information which are mostly preferred

by the investors.

183

TABLE – 5.12

RANKING OF THE SOURCES OF INVESTMENT INFORMATION

Sources WMV RANK

Professional Advisers 4.4 I

Business News Channels like CNBC,NDTV Profit 3.7 II

Family and Friends 3.5 III

Magazine or Newspapers 3.4 IV

Investment websites 3 V

Books 2.1 VI

Among the different sources of investment information Professional

Advisers are ranked first scoring a W.M.V value of 4.4. Business News

Channels like CNBC, NDTV Profit are getting the Second place. The family

and Friends of the Investors occupy the third place followed by the others.

From the above it is clear that most of the investors are dependent on the

Professional Advisers. The Consultation Paper released by the Committee on

Investor Awareness and Protection, chaired by D.Swarup, Chairman of the

Pension Fund Regulatory and Development Authority (PFRDA) begins with

the need for regulation of the market for financial products in India and to

educate the consumer. The committee has pointed out that most of the

dissemination of information relating to financial products takes place through

the distributors or intermediaries. Hence a financial adviser does two tasks

namely disseminating the information and also undertaking financial planning.

184

These financial advisers are very often unable to do both the tasks efficiently.

Hence there is an urgent need to regulate the functioning of the Professional

advisers in order to safeguard the interests of small investors.

iii) PREFERENCE FOR VARIOUS TYPES OF SHARES

The shares in the stock market are of different kinds. One way of

classifying them is growth shares and blue chip shares. Growth shares are

shares of companies which are relatively new with very good prospects for

growth. Whereas blue chip shares are shares of established companies.

Apart from this some investors have the habit of investing in companies which

are familiar to them for example a company which is situated in the nearby

locality or a company which is known to them through their family friends, etc.

TABLE – 5.13

PREFERENCE FOR SHARES

Types WMV RANK

Blue chip companies 4.43 I

Growth companies 4.14 II

Familiar Companies 3.64 III

As per the weighted mean Value Blue Chips are the most preferred

than the other types of shares. Growth shares are the second preferred type

of shares followed by shares of familiar companies. Investing in blue chip

companies shows that investors do not want to take risk with a new company.

185

iv) BASIS FOR BUYING SHARES

When an investor buys shares in the stock market he normally decides

on the basis of some important consideration. It could be based on the

fundamental analysis or technical analysis or just based on the short term

gain in the form of dividends, bonus or rights which a company is likely to give

to their shareholders. A ranking of the various bases for buying are given

below.

TABLE – 5.14

BASIS FOR BUYING SHARES

Basis WMV RANK

Fundamental analysis 4.04 I

Earnings announcements 3.96 II

Technical analysis 3.91 III

The basis of buying on the fundamentals is ranked first followed by

buying after the announcements regarding bonus, rights, and dividends in

order to get the benefits quickly. Technical analysis is not mostly favoured. It

shows that the investor values the fundamental analysis much more than

technical analysis. In the wake of recent happenings in the stock market, the

investors do not tend to depend on the technical analysis. But at the same

time the second ranking for earnings announcement reveals the fact that the

investors want to make quick money by buying shares of companies which

have announced bonus rights and dividends.

186

v) QUALITIES EXPECTED OF FINANCIAL ADVISERS

In the present study the role of the financial adviser is very important

since among the sources of financial information he is ranked first. Similarly a

large number of investors depend on the financial advisers for transacting in

the stock market. In this context the qualities expected from the financial

adviser is very important.

TABLE – 5.15

RANKING OF THE QUALITIES OF FINANCIAL ADVISERS

Qualifies of financial Adviser WMV RANK

Maximizing return 4.7 I

Fee structure 4.3 II

Trust and Confidentiality 4.2 III

Handling problems 3.6 IV

Protecting Capital 3.6 IV

Experience 3.6 IV

Brand name of the adviser 2.8 VII

Among the qualities expected of the financial advisers, maximising

returns, Reasonable fee structure and trust and confidentiality are ranked as

the first, second and third respectively. It is very interesting to note that the

brand name of the financial adviser is rated as the last rank. It is very much

evident from the fact that there are a large number of brokers operating in the

selected cities who are relatively new to the business but still have the

capacity to compete with corporates who are in the business.

187

vi) PREFERENCE FOR MUTUAL FUNDS

There are a wide variety of mutual funds. One way of classifying the

mutual funds is based on the objectives sought in income schemes, growth

schemes, and balanced schemes. There are other objectives of investing as

well like reducing the tax burden. Hence there are a wide variety of schemes

based on the investing objectives.

TABLE – 5.16

RANKING OF THE PREFERENCE FOR MUTUAL FUNDS

Mutual Funds WMV RANK

Growth Schemes 4 I

Income Schemes 3.7 II

Balanced Schemes 3.4 III

Tax Saving Schemes 3.1 IV

Index Schemes 3.1 IV

The above table 5.16 shows the preference of the investors towards

different types of mutual funds. Among the different schemes, growth

schemes are most preferred as shown by the weighted mean values. Income

Schemes are ranked second in the order of preference followed by Balanced

Schemes. Tax saving schemes and Index schemes have the least

preference.

188

vii) QUALITIES EXPECTED OF A MUTUAL FUND SCHEME

The mutual fund industry is very competitive. The liberalised market

offers a wide opportunity to an investor to choose from competing companies

offering the same type of funds whether it be growth funds, balanced funds or

income funds. In this context an understanding about the qualities preferred

by an investor in a scheme helps the mutual fund companies to design a

financial product according to the demands of the investors.

TABLE – 5.17

RANKING OF THE QUALITIES EXPECTED OF A MUTUAL FUND SCHEME

Qualities in a Scheme WMV RANK

Safety 4.3 I

Good Return 4.1 II

Capital Appreciation 4 III

Flexibility 3.9 IV

Fund Performance 3.9 IV

Liquidity 3.8 VI

Professional Management 3.8 VI

Rating given 3.8 VI

Diversification 3.7 IX

Disclosure of NAV 3.7 IX

Scheme Portfolio 3.5 XI

Fund Reputation or Brand name 3.4 XII

Tax Benefits 3.2 XIII

Sponsors reputation 3.2 XIII

Investor services 3.1 XV

Fringe benefits like credit card etc 2.2 XVI

189

The above table 5.17 shows the rankings of the various mutual fund

schemes. Among the qualities Safety is ranked as the first quality expected

followed by good returns and capital appreciations. The other rankings are

shown above. It is very interesting to note that fringe benefits like credit card

do not influence the investor for purchasing the mutual fund units. It shows the

awareness level of the investors. Similarly sponsors reputation is ranked XIII

which signifies that investors are more concerned about the returns and

whoever gives the best returns will be preferred by the investors irrespective

of whether it is sponsored by a well known company or not.

5.5 AN ANALYSIS OF DIFFERENT BEHAVIOUR IN INVESTING

The investment behaviour and preferences of the investors are

analysed using the responses given by the investors in the five point Likert’s

Rating Scale. The respondents’ views are assigned weights and the

cumulative scores are considered for the purpose of analysis. The specific

traits that are analysed and rated are given below. Questions which test the

same traits or behaviour are grouped together and cumulative scores of the

responses are used for assessing the different kinds of behaviour. Based on

the scores, respondents are divided into different levels as high, medium and

low. The different kinds of behaviour studied under this analysis are as follows

1. Herding

Herding is a psychological behaviour of following the crowd which is

observed in the stock market. When the investors buy or sell in the

190

stock market based on what others are doing and not relying on their

own information or analysis the herding tendency is said to exist. This

tendency arises due to the human psychology which wants to belong to

a group. The investors who exhibit this tendency may buy the shares

when there is a surge in the market and sell the shares when there is a

decline in the market.

2. Preference for short term gains

Investors may have short term or long term goals in the stock market.

The preferences for short term gain is assessed by the researcher

based on the responses given by the respondents. The criteria

selected for short term preferences include the frequency of trading,

selling IPO soon after allotment among other related behaviour

included in Part III of the questionnaire.

3. Risk Tolerance

Risk Tolerance refers to the extent of risk taken by the investors.

Literature review shows that there are many methods to evaluate the

risk. One such method is adopted by Dow Jones. A variety of factors

are considered for evaluating the risk tolerance of the individual

investors such as preference for long term or short term, frequent

trading, types of shares preferred, basis of buying or selling shares and

relative weights of the different types of assets in the portfolio among

other things.

191

4. Perception about Capital Market in India

Investors’ perception about the capital market is very important for

analysing the behaviour of investors. A favourable opinion about the

capital market will boost the investor confidence and it will be helpful in

the capital market growth. Hence perception about the capital market in

India is analysed using important yardsticks such as faith in the capital

market regulation, investor protection and attitudes towards different

capital market instruments.

5. Perception about Corporate Governance

Corporate governance means the way by which corporate are

managed and controlled by company managements. In the wake of

many scams such as the Satyam debacle, the faith of the investors in

Corporate Governance may be tested. The perception of the investors

about corporate Governance is evaluated by the responses they have

given on the Likert’s Rating Scale related to Corporate Governance.

6. Investor Awareness or Financial Literacy

Financial literacy is the process by which investors improve their

understanding of financial markets, products, concepts and risks. A

widely accepted definition of financial literacy is one formulated by the

U.K. National Foundation for Education Research which describes

financial literacy as “the ability to make informed judgments and take

effective decisions regarding the use and management of money. An

evaluation of the financial literacy of respondents is very basic for a

192

proper understanding of the behaviour of investors. Financial literacy is

evaluated by 12 statements related to the fundamentals in the financial

market and the responses given by the investors in three alternatives

“yes”, “not sure” and “no” are considered with relative weights

assigned to each alternative.

7. Preference for IPOs

Individual investor’s preference for IPOs as an investment option is

analysed. IPOs are very important for the development of the economy

as a whole and the capital market in particular. In the wake of

liberalisation and privatisation. IPOs are gaining a strategic role in

mobilisation of resources through disinvestments. Moreover the new

policy of the ministry of company affairs to increase the public holding

of shares in listed companies to 25 per cent within a time frame of 5

years has made IPOs a must for many body corporates. In this context,

the opinion of the individual investors towards IPOs is an important

factor for the development of the capital market.

8. Preference for Small Lots of Shares

Many individual investors can not afford to invest in huge amounts at a

time. Hence there is a habit among the small investors to buy the blue

chip companies shares in small numbers and accumulate them. This

habit has the advantage of minimising the risk at the same time

building the portfolio in a gradual way. This is analysed in this study.

193

9. Tendency for Profit booking

The preference of the investor for profit booking is analysed here.

Many investors have the habit of buying shares with an aim of selling it

after reaching the target. This is a trend found among many investors

who have a short term perspective in investing. The desire to realise

the profit makes the investors sell the winning stocks often while

holding the losing stocks.

10. Preference for Mutual Funds to Shares

A comparison between the preference for mutual fund and shares is

analysed here. A conservative investor may prefer a mutual fund to

shares.

Following tables are given for the analysis.

Table – 5.18 Herd Behaviour

Table – 5.19 Preference for Short Term Gains

Table – 5.20 Risk Tolerance

Table – 5.21 Perception about Indian Capital Market

Table – 5.22 Perception about Corporate Governance

Table – 5.23 Investor Awareness

Table – 5.24 Preference for IPOS

Table – 5.25 Preference for Small Lots

Table – 5.26 Tendency for Profit Booking

Table – 5.27 Preference for Mutual Fund to Shares

194

TABLE – 5.18

HERD BEHAVIOUR

S.No. Level Frequency Percent

1. Low 86 28.7

2. Medium 96 32.0

3. High 118 39.3

Total 300 100.0

The stock market reacts to greed and fear in addition to the usual

rational causes for change in market prices. The above table 5.18 shows that

28.7 per cent of the investors show a low level herd behaviour, 32 per cent of

the respondents a medium level and 39.3 per cent of the respondents show

high level of herding.

TABLE – 5.19

PREFERENCE FOR SHORT TERM GAINS

S.No. Level Frequency Percent

1. Low 94 31.3

2. Medium 124 41.3

3. High 82 27.3

Total 300 100.0

195

The respondents are divided over their preference for short term gains.

27.3% of the respondents show a high level for preference towards short term

investments and the rest show medium and low level of preference towards

short term gains. Buy and not hold for long is the new investor philosophy.

The average holding period of Nifty Shares by investors had fallen to 11

months in the year 2009 from 16 months in 2006 says a report by a financial

services company (livemint.com/articles 3/3/2010). This tendency is helped by

the reduction in the transaction cost from 2.5%-3% before the introduction of

online trading to 25% to 75%. Moreover the volatility in the market makes the

investors go for churning of shareholdings. Another probable reason for the

preference of short term gain is due to the broker dependent trading. In a

volatile market the brokers may encourage the investors to frequently buy and

sell so as to earn profits as also brokerage for them.

TABLE – 5.20

RISK TOLERANCE

S.No. Level Frequency Percent

1. Low 92 30.7

2. Medium 111 37.0

3. High 97 32.3

Total 300 100.0

The above table 5.20 shows that 30.7 percent of the respondents show

a low level for risk tolerance and 32.3 percent of the respondents show a high

degree of risk tolerance.

196

TABLE – 5.21

PERCEPTION ABOUT INDIAN CAPITAL MARKET

S.No. Perception Frequency Percent

1. Unfavourable 120 40.0

2. Favourable 180 60.0

Total 300 100.0

The above table 5.21 explains the perception of the investors towards

Indian capital Market with respect to the various parameters included in the

questionnaire. The opinions of the investors are divided as shown above. 40

per cent of the respondents have unfavourable perceptions about Indian

Capital Market; and 60 percent have favourable opinion about the Indian

Capital market.

TABLE – 5.22

PERCEPTION ABOUT CORPORATE GOVERNANCE

S.No. Perception Frequency Percent

1. Unfavourable 52 17.3

2. Favourable 248 82.7

Total 300 100.0

197

The above table 5.22 shows that 17.3 per cent of the investors have

unfavourable perception about corporate governance and a majority of the

investors (82.7) show favourable perception about corporate governance.

Opinion of the investors about corporate Governance is an important factor in

investment decisions in the capital market.

TABLE – 5-23

INVESTOR AWARENESS

S.No. Levels Frequency Percent

1. Low 52 17.4

2. Medium 124 41.3

3. High 124 41.3

Total 300 100.0

The above table 5.23 shows that 17.4 percent of the respondents are

classified as investors with low financial literacy levels. This is in conformity

with many earlier studies and the Government is bringing many measures to

improve the financial literacy levels. The SEBI has started many programmes

even at the school level to impart financial literacy to the students (Annual

Report SEBI, 2008-2009)

198

TABLE – 5.24

PREFERENCE FOR IPOS

S.No. Levels Frequency Percent

1. Low 87 29.0

2. Medium 85 28.3

3. High 128 42.7

Total 300 100.0

Table 5.24 shows the preference of the investors towards IPOs. Out of

300 respondents 128 respondents (42.7%) have a high level of preference for

IPOs, 29 % have low level of preference and 28.3 per cent have a medium

level of preference. Pricing of IPOs in the recent past is a matter of concern.

Many initial offers are listed below the issue price in the recent years. Hence

there is not a high level of preference for IPOs.

199

TABLE – 5.25

PREFERENCE FOR SMALL LOTS

S.No. Levels Frequency Percent

1. Low 103 34.3

2. Medium 34 11.3

3. High 163 54.4

Total 300 100.0

Table 5.25 shows that 54.4 per cent of the investors have the habit of

buying the shares in small lots since they do not want to take a big risk by

buying shares in large amounts. This is a better strategy than going in for

small value shares which have a high degree of risk.

TABLE – 5.26

TENDENCY FOR PROFIT BOOKING

S.No. Levels Frequency Percent

1. Low 17 5.7

2. Medium 87 29.0

3. High 196 65.3

Total 300 100.0

The tendency to book profit after the target is reached is shown by a

majority of the investors. This shows that a majority of the investors have a

short term goal in investing in stock market.

200

TABLE – 5.27

PREFERENCE FOR MUTUAL FUND TO SHARES

S.No. Levels Frequency Percent

1. Low 105 35.0

2. Medium 121 40.3

3. High 74 24.7

Total 300 100.0

Table 5.27 shows that 35 per cent shows low level of preference for

mutual funds to shares. And 24.7 per cent have a high level of preference for

mutual funds when compared with shares and 40.3 per cent are rather

undecided. This also shows the conservative approach of the investors.

5.6 DIFFERENTIAL ANALYSIS

In this part of the analysis the relationship between the demographic

factors and various investment behaviours are examined. Suitable

hypotheses are set and tested with the help of the appropriate statistical tools

and the variables are analysed.

201

TABLE – 5.28

ONE WAY ANALYSIS OF VARIANCE AMONG AGE GROUPS WITH

REGARD TO INVESTMENT BEHAVIOUR

S.No. Investment Behaviour

Sum of squares

Df Mean

Square Mean

Statistical Inference

1. Herd Behaviour

Between Groups

Within Groups

114.278

1408.958

3

296

38.093

4.760

G1=8.0000

G2=5.8762

G3=6.8583

G4=6.5952

F = 8.003

P<0.001

Significant

2. Preference for

short term gain

Between Groups

Within Groups

796.056

6330.861

3

296

265.352

21.388

G1=22.6538

G2=16.8286

G3=18.1496

G4=19.6190

F = 12.407

P<0.001

Significant

3. Risk tolerance

Between Groups

Within Groups

1440.324

11775.796

3

296

480.108

39.783

G1=30.6538

G2=22.7048

G3=25.0079

G4=26.2143

F = 12.068

P<0.001

Significant

4. Perception of

capital market

Between Groups

Within Groups

146.709

4556.528

3

296

48.903

15.394

G1=46.8846

G2=47.5048

G3=46.6457

G4=48.7143

F = 3.177

P<0.05

Significant

5. Perception of Corporate governance Between Groups

Within Groups

26.219

873.151

3

296

8.740

2.950

G1=12.4231

G2=13.0095

G3=12.3622

G4=12.4762

F = 2.963

P<0.05

Significant

6. Investor

Awareness

Between Groups

Within Groups

454.342

6324.005

3

296

151.447

21.365

G1=32.8077

G2=30.5619

G3=33.0000

G4=33.5952

F = 7.089

P<0.001

Significant

G1 = Less than 30 G2 = 30-45 G3 = 45-60 G4 = Above 60

202

From Table 5.28, the following results are inferred

i) The herd behaviour varies significantly between different age groups

as shown by the mean values in the above table. The mean score for

the respondents with High school qualification is much higher than

other mean scores calculated for other groups. This signifies that herd

behaviour is the highest among the respondents in the first group

namely those with High school qualification.

ii) Preference for short term gain varies significantly between different

groups of investors based on their age groups. This is evident from the

mean scores given in the table for the variable namely preference for

short term gain.

iii) The risk tolerance of investors varies significantly among the groups of

respondents belonging to different age groups. The mean scores

calculated for the variable shows there is a difference among the group

with respect to risk tolerance.

iv) The perception towards capital market varies significantly among

investors belonging to different age groups. The mean scores for

perception towards capital market given in the above table signify a

significant difference among the groups.

v) The perception of the respondents about corporate governance varies

significantly among the different groups of respondents as indicated by

the mean scores.

203

vi) The level of investor awareness of the respondents varies significantly

among respondents belonging to different age groups.

Since the results of the F Test shows significant P value, Duncan’s

Post Hoc Test is done for the variables where the results are P<0.001 and

the results are provided below.

TABLE – 5.28A

DUNCAN POST HOC TEST – HERD BEHAVIOUR

AGE N Subset for alpha = 0.05

1 2 3

30-45 105 5.8762

Above 60 42 6.5952 6.5952

45-60 127 6.8583

Less than 30 26 8.0000

Herd behaviour does not differ significantly between 30-45 and above

60 age groups. The herd behaviour differs significantly between the investors

in the age groups of less than 30 and others.

204

TABLE – 5.28B

DUNCAN POST HOC TEST – PREFERENCE FOR SHORT TERM GAIN

AGE N Subset for alpha = 0.05

1 2 3

30-45 105 16.8286

45-60 127 18.1496 18.1496

Above 60 42 19.6190

Less than 30 26 22.6538

Since table 5.28B shows the preference for short term gain varies

significantly among the respondents belonging to different age groups,

Duncan’s Post Hoc test is done. It shows the respondents in three different

groups. The preference for short term gain does not differ significantly

between the respondents in the age group of 30-45 and 45-60. Respondents

in the age group of less than 30 differ significantly from others with respect to

their preference for short term gain.

205

TABLE – 5.28C

DUNCAN POST HOC TEST – RISK TOLERANCE

AGE N Subset for alpha = 0.05

1 2 3

30-45 105 22.7048

45-60 127 25.0079 25.0079

Above 60 42 26.2143

Less than 30 26 30.6538

Table 5.28C shows that the respondents belonging to different age

groups differ significantly among themselves with respect to risk tolerance.

Post Hoc test as per table 5.28C reveals that that there are three groups

among the respondents. The above table shows that respondents in the age

group of 45-60 and above 60 do not differ significantly from one another with

respect to risk tolerance but the respondents in the age group of less than 30

differ significantly from others.

206

TABLE – 5.28D

DUNCAN POST HOC TEST – INVESTOR AWARENESS

AGE N Subset for alpha = 0.05

1 2

30-45 105 30.5619

Less than 30 26 32.8077

45-60 127 33.0000

Above 60 42 33.5952

Table 5.28D reveals that the level of investor awareness differs

significantly among different age groups. Hence Duncan’s test is done to

analyse the groupings. Table 5.28D reveals that the respondents in the age

group of 30-45 differ from the rest of the age groups with respect to the level

of investor awareness.

Summary

The analysis of the above variables with the age groups confirm the

fact that respondents in the age group of less than 30 differ from other groups

with respect to herd behaviour, preference for short term gain, risk tolerance.

Investors in the age group of less 30 show a higher level of herd behaviour,

risk tolerance and preference for short gain. The respondents in the age

group of 30-45 differ from the rest of the age groups with respect to investor

awareness.

207

TABLE – 5.29

ONE WAY ANALYSIS OF VARIANCE AMONG ACADEMIC

QUALIFICATION WITH REGARD TO INVESTMENT BEHAVIOUR

S.No. Investment Behaviour

Sum of squares

Df Mean

Square Mean

Statistical Inference

1. Herd Behaviour

Between Groups

Within Groups

42.945

1480.292

3

296

14.315

5.001

G1=6.6818

G2=7.0000

G3=6.2963

G4=6.1370

F = 2.862

P<0.05

Significant

2. Preference for

short term gain

Between Groups

Within Groups

191.561

6935.356

3

296

63.854

23.430

G1=19.5455

G2=18.9032

G3=18.0741

G4=17.0822

F = 2.725

P<0.05

Significant

3. Risk tolerance

Between Groups

Within Groups

392.036

12824.084

3

296

130.679

43.325

G2=25.9032

G1=26.2273

G3=24.3704

G4=23.2192

F = 3.016

P<0.05

Significant

4. Perception of

capital market

Between Groups

Within Groups

191.871

4511.366

3

296

63.957

15.241

G1=50.0000

G2=46.8710

G3=46.9753

G4=47.3973

F = 4.196

P<0.01

Significant

5. Perception of Corporate governance Between Groups

Within Groups

11.722

887.648

3

296

3.907

2.999

G1=12.0455

G2=12.6774

G3=12.7901

G4=12.4658

F = 1.303

P>0.05

Not Significant

6. Investor

Awareness

Between Groups

Within Groups

104.368

6673.979

3

296

34.789

22.547

G1=33.8182

G2=31.7984

G3=31.9383

G4=32.7397

F = 1.543

P>0.05

Not Significant

G1 = School final G2 = Graduate G3 = Post graduate G4 = Professional

208

Table 5.29 reveals the following results on the basis of the F Test

i) The herd behaviour varies significantly among the respondents

belonging to different academic qualifications. The mean scores of the

different groups as specified above signify a significant difference

among the group. Herd instincts based on the mean scores is highest

for G2 for graduates and lowest for Professionals.

ii) The preference for short term gain varies significantly among the

respondents belonging to different academic qualifications. The mean

score is the highest for respondents belonging to the group G1 - High

School qualifications.

iii) The table 5.29 reveals a significant difference among the respondents

with respect to the level of risk tolerance.

iv) The F Test above reveals that there is significant difference among

respondents with respect to perception of capital market as indicated

by the mean scores for the different groups.

v) The perception of the respondents with respect to corporate

governance does not vary significantly among the different academic

levels of the respondents.

vi) The level of investor awareness does not vary significantly among the

respondents belonging to different educational levels.

209

TABLE – 5.30

ONE WAY ANALYSIS OF VARIANCE AMONG OCCUPATION WITH

REGARD TO INVESTMENT BEHAVIOUR

S.No. Investment Behaviour

Sum of squares

Df Mean

Square Mean

Statistical Inference

1. Herd Behaviour

Between Groups

Within Groups

64.168

1459.069

3

296

21.389

4.929

G1=6.7162

G2=6.6786

G3=6.1203

G4=7.3077

F = 4.339

P<0.01

Significant

2. Preference for

short term gain

Between Groups

Within Groups

497.758

6629.159

3

296

165.919

22.396

G1=17.5000

G2=18.5714

G3=17.4962

G4=20.6615

F = 7.408

P<0.001

Significant

3. Risk tolerance

Between Groups

Within Groups

868.947

12347.173

3

296

289.649

41.713

G1=24.2162

G2=25.2500

G3=23.6165

G4=27.9692

F = 6.944

P<0.001

Significant

4. Perception of

capital market

Between Groups

Within Groups

6.892

4696.344

3

296

2.297

15.866

G1=47.1802

G2=47.5357

G3=47.3459

G4=47.0308

F = 0.145

P>0.05

Not Significant

5. Perception of Corporate governance Between Groups

Within Groups

48.019

851.351

3

296

16.006

2.876

G1=12.9189

G2=13.6071

G3=12.3383

G4=12.3846

F = 5.565

P<0.01

Significant

6. Investor

Awareness

Between Groups

Within Groups

345.394

6432.952

3

296

11.131

21.733

G1=32.3649

G2=28.8929

G3=32.5714

G4=32.7385

F = 5.298

P<0.01

Significant

G1 = Self Employed G2 = Employed in Government G3 = Employed in private G4 = Retired

210

One Way Analysis of Variance among Occupation with regard to Investment

Behaviour reveals the following:

i) The herd behaviour varies significantly among the respondents

belonging to different occupation. It is evident from the mean scores as

given in table 5-30 for the variable herd behaviour.

ii) The preference for short term gain of the respondents varies

significantly among the group. The mean scores given for the variable

shows there is a difference in value among the group.

iii) The level of risk tolerance of the employees varies significantly

between the groups as evident from table 5-30. The risk tolerance level

of the retired investors is much different from others.

iv) The perception towards capital market does not differ significantly

among the respondents belonging to different occupation levels. The

mean scores for the variable do not differ significantly among the

different groups.

v) The perception of the respondents towards corporate governance does

not differs significantly among the groups belonging to different

occupation.

vi) The level of investor awareness varies significantly among the

respondents belonging to different occupations. This is evident from

the mean scores.

On the basis of the results shown above, Duncan’s Post Hoc Test is

done for the variables where there is a significance level with P<0.01. The

results are presented below.

211

TABLE – 5.30A

DUNCAN POST HOC TEST – PREFERENCE FOR SHORT TERM GAIN

OCCUPATION N Subset for alpha = 0.05

1 2

Employed in private 133 17.4692

Self Employed 74 17.5000

Employed in Government 28 18.5714

Retired 65 20.6615

Table 5.30A shows that the there is significant difference in the

preference for short term gain between the retired investors and the rest of

the investors as depicted above. Similarly the table above reveals there is no

significant difference among the employed in private, self employed and

employed in government with respect to preference for short term gain.

212

TABLE – 5.30B

DUNCAN POST HOC TEST – RISK TOLERANCE

OCCUPATION N Subset for alpha = 0.05

1 2

Employed in private 133 23.6165

Self Employed 74 24.2162

Employed in Government 28 25.2500

Retired 65 27.9692

Table 5.30B reveals that there is difference between retired investors

and others with respect to their risk tolerance. Respondents who are

employed in private, employed in government and self employed do not differ

significantly with respect to risk tolerance.

The analysis of variance as done by the above table confirms that the

retired respondents differ significantly from other groups of investors with

respect to their preference for short term gain and risk tolerance.

Summary

The investment behaviour of the retired investors is very different from

the other respondents. The level of risk taking by the retired investors is very

high compared to others. This can be attributed to many factors like a higher

level of financial security, a lower level of financial commitment and also the

years of experience gained in investing.

213

TABLE – 5.31

ONE WAY ANALYSIS OF VARIANCE AMONG ANNUAL INCOME

WITH REGARD TO INVESTMENT BEHAVIOUR

S.No. Investment Behaviour

Sum of squares

Df Mean

Square Mean

Statistical Inference

1. Herd Behaviour

Between Groups

Within Groups

41.880

1481.356

3

296

13.960

5.005

G1=7.0000

G2=6.1653

G3=7.0690

G4=6.6000

F = 2.789

P<0.05

Significant

2. Preference for

short term gain

Between Groups

Within Groups

283.523

6843.393

3

296

94.508

23.120

G1=19.3875

G2=17.1818

G3=19.4138

G4=18.4571

F = 4.088

P<0.01

Significant

3. Risk tolerance

Between Groups

Within Groups

542.698

12673.422

3

296

180.899

42.816

G1=26.3875

G2=23.3471

G3=26.4828

G4=25.0571

F = 4.225

P<0.01

Significant

4. Perception of

capital market

Between Groups

Within Groups

53.858

4649.379

3

296

17.953

15.707

G1=47.3250

G2=47.4959

G3=47.8276

G4=46.5286

F = 1.143

P>0.05

Not

Significant

5. Perception of Corporate governance Between Groups

Within Groups

30.984

868.386

3

296

10.328

2.934

G1=13.0000

G2=12.5289

G3=12.9655

G4=12.1571

F = 3.520

P<0.05

Significant

6. Investor

Awareness

Between Groups

Within Groups

1006.880

5771.467

3

296

335.627

19.498

G1=29.6250

G2=33.1074

G3=30.6207

G4=34.2857

F = 17.213

P<0.001

Significant

G1 = Below 2 Lakhs G2 = 2-4 Lakhs G3 = 4-6 Lakhs G4 = 6 Lakhs and above

214

One way analysis of variance among annual income with regard to investment

behaviour reveals the following :

i) Herd behaviour of the respondents varies significantly among different

income levels. The mean scores for the various income level given for

the variable herding shows there is a difference among the

respondents belonging to different income levels.

ii) Preference for short term gain varies significantly among the

respondents belonging to different income levels. This is evident from

the mean scores given in the table.

iii) The level of risk tolerance varies significantly among the respondents

belonging to different income groups. This is shown as per the mean

scores for the various groups.

iv) The investors’ perception of capital market does not differ among the

different income groups. The mean scores as depicted above prove

that there is no significant difference.

v) The investors’ perception of Corporate Governance varies significantly

among the respondents having different income levels as shown by the

mean scores.

vi) The level of investor awareness differs significantly among the

respondents belonging to different income levels.

215

Duncan’s Post Hoc Test is done to further analyse the results as

obtained above. The findings are presented below.

TABLE – 5.31A

DUNCAN POST HOC TEST – INVESTOR AWARENESS

ANNUAL INCOME N Subset for alpha = 0.05

1 2

Below 2 Lakhs 80 29.6250

4-6 Lakhs 29 30.6207

2-4 Lakhs 121 33.1074

6 Lakhs and above 70 34.2857

Table 5.31A shows that there are two similar groups with respect to

investor awareness. Duncan’s test reveals that there is no significant

difference between the group earning below 2 lakhs and the group earning 4-

6 with respect to investor awareness. Similarly there is no significant

difference between the group who earn 2-4 lakhs and the group which earn 6

lakhs and above with regard to investor awareness.

216

5.7 ASSOCIATION BETWEEN GENDER AND VARIOUS

BEHAVIOURAL ISSUES

The relationship between demographic factors and various behavioural

issues and perceptional issues such as herding tendency, preference for short

term gain, risk tolerance and financial literacy are analysed in this study.

i) HERD BEHAVIOUR

Herd instincts are a psychological bias in investing. Instead of relying

on any analysis or basic information people tend to herd together i.e. just

follow other investors or market sentiments. This often results in irrational ups

and downs in the market not supported by any technical or fundamental

valuation. This may be due to over reaction to any market information. The

behaviour of the investors are analysed based on the responses from the

Rating scale used for the respondents. The following table V-38 is provided

for the purpose of analysis.

217

TABLE – 5.32

HERDING VS GENDER

Level Gender Total

Male Female

Low 74

(28.9)

12

(27.3)

86

(28.7)

Medium 86

(33.6)

10

(22.7)

96

(32.0)

High 96

(37.5)

22

(50)

118

(39.3)

Total 256

(100)

44

(100)

300

(100)

As per the above table 5.32, 50 per cent of female investors have a

high level of herding tendency, 22.7 per cent has medium level of herding

tendency and 27.3 per cent of the respondents have a low level. Among the

male, a high level of herding tendency is shown by 37.5 per cent of the

respondents, medium level by 33.6 per cent and low level by 28.9 per cent.

With a view to analyse the associations between the herd instincts and

gender chi square test is applied. The findings are presented below.

Chi-Square Tests

Value Df Statistical Inference

Pearson Chi-Square 2.912 2 P > 0.05

Not Significant

The results of the chi square tests revealed above prove that there is

no significant relationship between herding and the gender.

218

ii) PREFERENCE FOR SHORT TERM GAIN

The investment time frame of the investors is either short term or long

term. Short term denotes the holding period of less than one year and long

term is more than one year. Choosing between short term gain and long term

gain is a very important decision taken by every investor. Each has its own

risks and rewards associated with it. Many investment experts favour the idea

of long term gain but in a developing economy like India where the stock

markets have become very developed and exciting the tendency of the

investors to invest for a short term gain and reap the benefits is a frequently

observed phenomenon. Hence this tendency is analysed in this study. The

following table is provided for the purpose of analysis.

TABLE – 5.33

PREFERENCE FOR SHORT TERM GAIN VS GENDER

Level

Gender Total

Male Female

Low 91

(35.5)

3

(6.8)

94

(31.3)

Medium 101

(39.5)

23

(52.3)

124

(41.3)

High 64

(25.0)

18

(40.9)

82

(27.3)

Total 256

(100)

44

(100)

300

(100)

219

Among the males 25 per cent show a high level of preference for short

term gain. But among the females 40.9 per cent have shown a high level of

preference. Female investors show a higher level of preference than the male

investors. With a view to examine the association between preference for

short term gain and gender chi square test is applied. The results are given

below.

Chi-Square Test

Value Df Statistical Inference

Pearson Chi-Square 14.860 2 P < 0.01

Significant

The Pearson Chi square value signifies that there is a significant

relationship between gender and the preference for short term gain.

220

iii) RISK TOLERANCE

Risk tolerance is a very important attribute in investing which decides

the choice of investment of an individual. It also determines the rate of return

earned by the investor. There is a reward for risk taking. The attribute of risk

tolerance is analysed in this study and the factors which influence risk taking

especially demographic factors are analysed with the help of the following

table.

TABLE – 5.34

RISK TOLERANCE VS GENDER

Level Gender Total

Male Female

Low 88

(34.4)

4

(9.1)

92

(30.7)

Medium 91

(35.5)

20

(45.5)

111

(37)

High 77

(30.1)

20

(45.5)

97

(32.3)

Total 256

(100)

44

(100)

300

(100)

Table 5.34 shows that high level of risk tolerance exists more among

the female than among the male. With a view to analyse the association

between the two Chi square test is applied.

221

Chi-Square Tests

Value Df Statistical Inference

Pearson Chi-Square 11.569 2 P < 0.05

Significant

The results of the chi square test reveals that risk tolerance varies

between men and women.

iv) INVESTOR AWARENESS

Investor Awareness is the process by which investors improve their

understanding of financial markets, products, concepts and risks. Financial

literacy helps an investor to make an informed judgment about investments

keeping in mind the specific goals of investing. Financial literacy levels of the

respondents are analysed using the responses given by the respondents in

the questionnaire. It was found that a majority of them have a high level of

financial literacy. In this part of the study, the relationship between

demographic factors and financial literacy is analysed. The following table is

provided for the purpose of analysis.

222

TABLE – 5.35

INVESTOR AWARENESS VS GENDER

Level

Gender Total

Male Female

Low 37

(14.5)

15

(34.1)

52

(17.3)

Medium 106

(41.4)

18

(40.9)

124

(41.3)

High 113

(44.1)

11

(25)

124

(41.3)

Total 256

(100)

44

(100)

300

(100)

The investor awareness levels between the genders are given in table

5.35. Among the male, 44.1 per cent have high financial literacy levels.

Among the female 25 per cent have high financial literacy levels. With a view

to analyse the relationship between gender and financial literacy, chi square

test is applied.

Chi-Square Tests

Value Df Statistical Inference

Pearson Chi-Square 11.684 2 P < 0.05

Significant

The value obtained in the chi square test signifies that there is a

significant relationship between gender and the investor awareness.

223

5.8 ASSOCIATION BETWEEN DEMOGRAPHIC FACTORS AND

INVESTMENT PREFERENCES

The investors preferences for IPOs is analysed in this study.

Traditionally Indian shareholders entered the capital market through IPOs but

there is a changing trend nowadays which is evident from the poor

performance of IPOs in our country in the recent times. Similarly some

investors have the habit of buying shares in small lots (equivalent to investing

as low as possible) to minimize losses. This tendency is analysed in this

study. Another habit of the investor which is analysed in this part is the profit

booking by investors on reaching the target to realize the profit. Some

investors buy the shares with a fixed target. If the target is reached they sell

the shares and book the profits. Others do not sell the shares and continue to

hold it as a long time investment. The tendency to book profit is taken up for

analysis to study how the investors keep track of their investments. The

following tables are provided under this analysis.

224

TABLE – 5.36

ASSOCIATION BETWEEN PREFERENCE FOR IPOS AND

DEMOGRAPHIC FACTORS

S.No. Demographic factors

Level df Statistical Inference Low Medium High

1. Gender

Male

Female

82

5

75

10

99

29

2

X2=12.631

P<0.01

Significant

2. Age

Less than 30

30-45

45-60

Above 60

4

19

44

20

8

41

34

2

14

45

49

20

6

X2=26.539

P<0.01

Significant

3. Academic

Qualification

School final

Graduate

Post graduate

Professional

6

44

21

16

7

22

30

26

9

58

30

31

6

X2=12.991

P<0.05

Significant

4. Occupation

Self employed

Employed in Govt.

Employed in private

Retired

30

6

22

29

26

11

43

5

18

11

68

31

6

X2=37.981

P<0.01

Significant

5. Annual Income

Below 2 lakhs

2-4 lakhs

4-6 lakhs

6 lakhs and above

24

19

6

38

20

39

9

17

36

63

14

15

6

X2=35.193

P<0.01

Significant

225

Table 5.36 shows the association between the preference for IPOs and

the demographic factors namely gender, age, academic qualification,

occupation and annual income. The chi square test reveals the following

1. There is a significant relationship between gender and the preference

for IPOs.

2. The preference for IPOs differs significantly between the different age

groups of the respondents.

3. There is a significant relationship between academic qualification of the

respondents and the preference for IPOs.

4. The preference for IPOs differs significantly between the respondents

belonging to different categories of occupation.

5. The preference for IPOs differs significantly between the respondents

belonging to different income levels.

The tendency of the investors to invest in IPOs is influenced by the

demographic factors namely gender, age, qualification, occupation and

annual Income.

226

TABLE – 5.37

ASSOCIATION BETWEEN PREFERENCE FOR SMALL LOTS AND

DEMOGRAPHIC FACTORS

S.No. Demographic factors

Level df Statistical Inference Low Medium High

1. Gender

Male

Female

93

10

28

6

135

28

2

X2=3.086

P>0.05

Not Significant

2. Age

Less than 30

30-45

45-60

Above 60

12

19

62

10

4

19

10

1

10

67

55

31

6

X2=35.877

P<0.01

Significant

3. Academic

Qualification

School final

Graduate

Post graduate

Professional

5

50

22

26

5

9

14

6

12

65

45

41

6

X2=11.051

P>0.05

Not Significant

4. Occupation

Self employed

Employed in Govt.

Employed in private

Retired

21

2

56

24

10

6

14

4

43

20

63

37

6

X2=16.672

P<0.01

Significant

5. Annual Income

Below 2 lakhs

2-4 lakhs

4-6 lakhs

6 lakhs and above

15

33

13

42

13

12

2

7

52

76

14

21

6

X2=35.411

P<0.01

Significant

227

Table 5.37 reveals the following:

1. There is no relationship between the gender of the respondents and

the preference for small lots of shares.

2. There is a significant relationship between the age of the respondents

and the preference for small lots shares.

3. The preference for small lots of shares does not vary significantly

between respondents belonging to different academic levels

4. The preference for small lots varies between different occupations.

5. The preference for small lots varies significantly between different

income levels of the respondents.

228

TABLE – 5.38

ASSOCIATION BETWEEN PREFERENCE FOR PROFIT BOOKING AND

DEMOGRAPHIC FACTORS

S.No. Demographic

factors

Level df Statistical

Inference Low Medium High

1. Gender

Male

Female

14

3

71

16

171

25

2

X2=1.657

P>0.05

Not Significant

2. Age

Less than 30

30-45

45-60

Above 60

--

7

9

1

4

43

39

1

22

55

79

40

6

X2=30.250

P<0.01

Significant

3. Academic

Qualification

School final

Graduate

Post graduate

Professional

--

10

1

6

2

27

32

26

20

87

48

41

6

X2=19.618

P<0.01

Significant

4. Occupation

Self employed

Employed in Govt.

Employed in private

Retired

8

--

4

5

15

15

49

8

51

13

80

52

6

X2=28.377

P<0.01

Significant

5. Annual Income

Below 2 lakhs

2-4 lakhs

4-6 lakhs

6 lakhs and above

1

3

5

8

21

42

5

19

58

76

19

43

6

X2=19.826

P<0.01

Significant

229

As per the table 5.38, the following inferences are made.

1. The tendency to book profits does not differ significantly between the

genders.

2. Profit booking varies significantly between different age groups.

3. There is a significant relationship between profit booking and academic

qualification.

4. The tendency to book profits vary significantly between the

respondents belonging to different occupation.

5. There is a significant relationship between tendency to book profits and

annual income of the respondents.

230

TABLE – 5.39

ASSOCIATION BETWEEN PREFERENCE FOR GOLD AND

DEMOGRAPHIC FACTORS

S.No. Demographic factors

Level df Statistical Inference Low Medium High

1. Gender

Male

Female

63

14

138

12

55

18

2

X2=11.909

P<0.01

Significant

2. Age

Less than 30

30-45

45-60

Above 60

10

40

25

2

7

43

77

23

9

22

25

17

6

X2=31.696

P<0.01

Significant

3. Academic Qualification School final

Graduate

Post graduate

Professional

--

34

20

23

5

68

50

27

17

22

11

23

6

X2=48.295

P<0.01

Significant

4. Occupation

Self employed

Employed in Govt.

Employed in private

Retired

19

15

34

9

25

3

81

41

30

10

18

15

6

X2=45.849

P<0.01

Significant

5. Annual Income

Below 2 lakhs

2-4 lakhs

4-6 lakhs

6 lakhs and above

19

38

10

10

44

61

10

35

17

22

9

25

6

X2=14.334

P<0.05

Significant

231

Table 5.39 indicates the association between the preferences for Gold

/real assets as an investment option and various demographic factors namely

gender, age academic qualification, occupation and annual savings. The

findings are presented below.

1. The chi square value indicates the preference for gold varies

significantly between genders.

2. There is a significant relationship between preference for gold and age

of the respondents.

3. There is a significant relationship between preference for gold and

academic qualification of the respondents.

4. The preference for gold varies significantly among the respondents

belonging to different occupation.

5. There is a relationship between preference for gold and annual income.

Preference for investing in gold has a significant relationship with all

the demographic factors namely gender, age, qualification, occupation and

annual income.

232

TABLE – 5.40

ASSOCIATION BETWEEN PREFERENCE FOR MUTUAL FUND TO

SHARES AND DEMOGRAPHIC FACTORS

S.No. Demographic factors

Level df Statistical Inference Low Medium High

1. Gender

Male

Female

92

13

108

13

56

18

2

X2=7.441

P<0.05

Significant

2. Age

Less than 30

30-45

45-60

Above 60

13

36

49

7

7

37

56

21

6

32

22

14

6

X2=14.958

P<0.05

Significant

3. Academic Qualification School final

Graduate

Post graduate

Professional

1

44

30

30

10

57

38

16

11

23

13

27

6

X2=29.372

P<0.01

Significant

4. Occupation

Self employed

Employed in Govt.

Employed in private

Retired

20

13

51

21

28

6

55

32

26

9

27

12

6

X2=12.819

P<0.05

Significant

5. Annual Income