chapter ten accounting for a professional service business: the combination journal

TRANSCRIPT

CHAPTER TEN

ACCOUNTING FOR A PROFESSIONAL SERVICE

BUSINESS: THE COMBINATION JOURNAL

ACCRUAL BASIS OF ACCOUNTING

Offers the best matching of revenues and expenses

Required under Generally Accepted Accounting Principles:– Important when major businesses want to raise

large amounts of money

Smaller service organizations often use the Cash or Modified Cash Basis

CASH BASIS OF ACCOUNTING

Revenues are recorded when cash is RECEIVED

Expenses are recorded when cash is PAID

Similar to Accrual Basis if:– There are few receivables, payables, and assets

Can vary significantly if:– Business has many receivables, payables, and

assets

CASH BASIS OF ACCOUNTING

Since this method records revenues only when the cash is received:

There is noAccounts Receivable

account

CASH BASIS OF ACCOUNTINGSince this method records expenses only when cash is paid:

There is noAccounts Payable

account

CASH BASIS OF ACCOUNTINGAll cash spent is recorded as an expense, therefore:

There are noLong-term Assets

and noPrepaid Assets

ACCRUAL BASIS vs. CASH BASIS

Let’s look at some transactions and see how they are recorded

under each of the methods.

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

The Accrual Basis would saythis is revenue, since services

were provided to a client.

$600

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

But the Cash Basis does NOT recognize the revenue, since

cash was not received.

$600

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

The Accrual Basis considers the payment of wages an expense,

since services were received.

$600

(b) Paid wages $300 $300

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

The Cash Basis also considers the payment of wages an expense,

since cash was received.

$600(b) Paid wages $300 $300 $300

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

Under the Accrual Basis, revenue would have been recognized

last month (the month it was earned).

$600(b) Paid wages $300 $300 $300

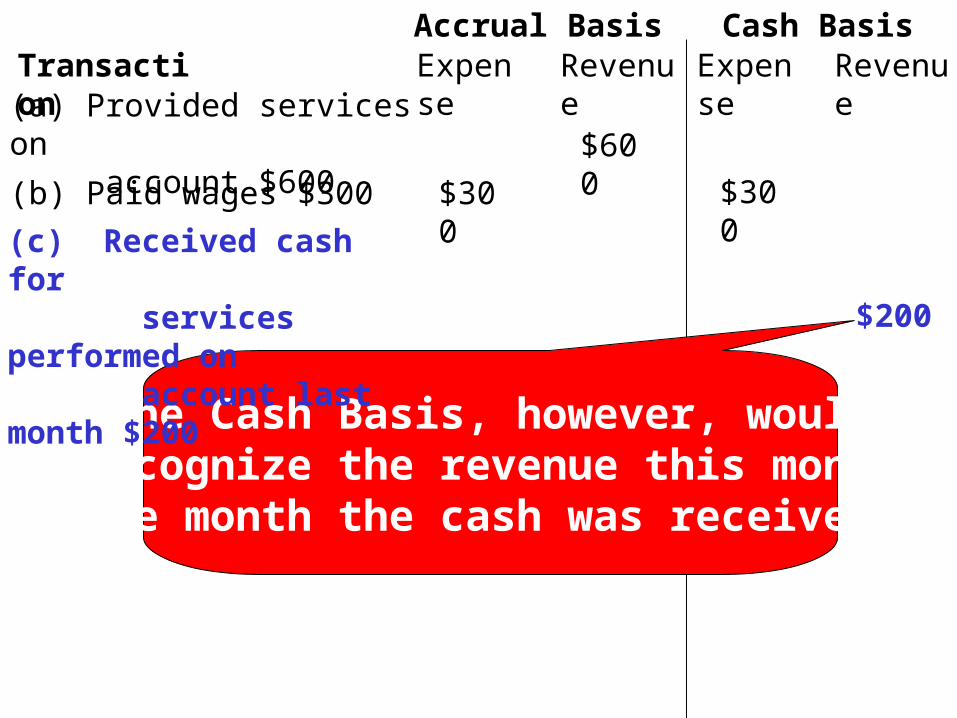

(c) Received cash for services performed on account last month $200

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

The Cash Basis, however, wouldrecognize the revenue this month

(the month the cash was received).

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

Accrual Basis says Services Received = Expense

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Cash Basis says: No Cash = No Expense

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Accrual Basis would have shown the expense last month(when advertising occurred).

(e) Paid on account for last month’s advertising $100

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Cash Basis says:Cash Paid = Expense

(e) Paid on account for last month’s advertising $100 $100

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Accrual Basis says:Supplies are an asset, not an Expense.

(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Cash Basis says:Cash spent = Expense

(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Accrual Basis says: Asset consumed = Expense

(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

(g) Supplies used during month, $40 $40

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Cash Basis says: No Cash spent, No Expense.

(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

(g) Supplies used during month, $40 $40

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250

Let’s look at the Net Income under each method.

(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

(g) Supplies used during month, $40 $40

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

(g) Supplies used during month, $40 $40

$590 $600Net Income (Loss) $10

Accrual Basis Cash BasisExpense ExpenseRevenue Revenue

(a) Provided services on account $600

Transaction

$600

(b) Paid wages $300 $300 $300

(c) Received cash for services performed on account last month $200 $200

(d) Received cleaning bill for month $250 $250(e) Paid on account for last month’s advertising $100 $100(f) Purchase of supplies $50 $50

(g) Supplies used during month, $40 $40

$590 $600

Net Income (Loss) $10$450 $200

($250)

Net Incomes (Losses) are very different!!

MODIFIED CASH BASIS

Combines aspects of the Cash and Accrual methods

Revenues and Expenses:– Cash Basis

Except for assets with a useful life > 1 accounting period – Recorded as assets (e.g., Prepaid Insurance,

Supplies, Equipment, Building, etc.)

MODIFIED CASH BASIS

PrepaidAssets

Long-TermAssets

AccountsPayable

(for asset purchases

only)

Unlike the Cash Basis, the Modified Cash Basis uses the following accounts:

COMPARISON OF METHODS

Revenue example: Performed services for cash

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

CashProfess. Fees

Cash Basis would considerthis revenue becausecash was received.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

CashProfess. Fees

CashProfess. Fees

Modified Cash Basis uses the samecriteria for determining revenues….

Cash Received = Revenue

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

CashProfess. Fees

CashProfess. Fees

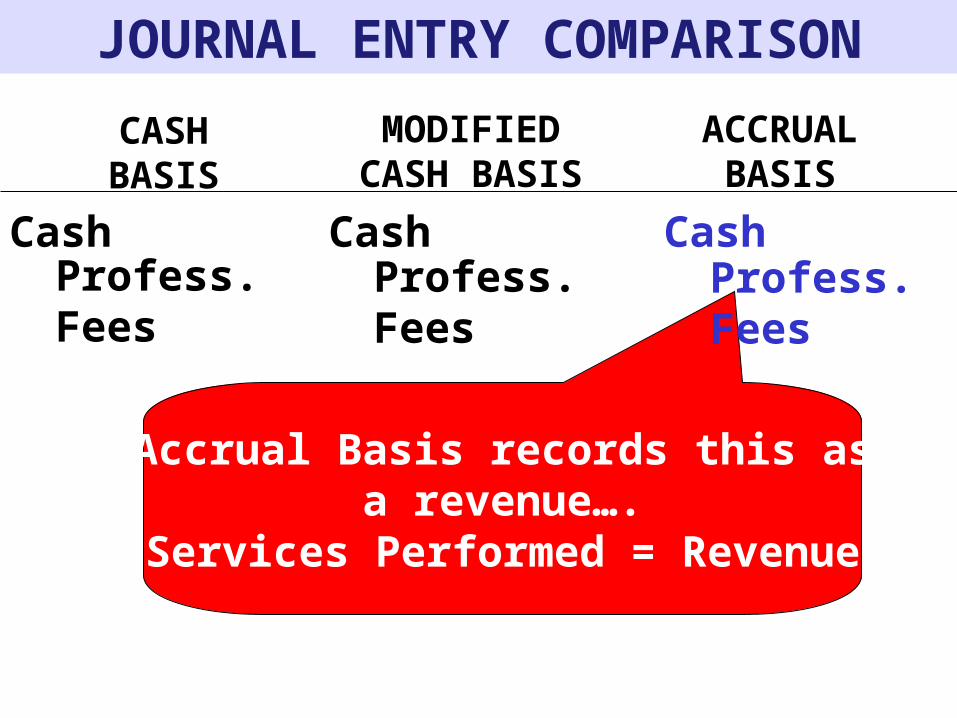

Accrual Basis records this asa revenue….

Services Performed = Revenue

CashProfess. Fees

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

CashProfess. Fees

CashProfess. Fees

CashProfess. Fees

SAME ENTRYFor all 3 methods

REVENUE EXAMPLE

Performed services on account

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Cash Basis would NOT considerthis revenue because

cash was not received.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis alsowould NOT consider this

revenue because cash was not received.

No Entry No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis DOES considerthis revenue.

Services Performed = Revenue

No Entry No Entry Accts. Rec.Profess. Fees

EXPENSE EXAMPLE

Pay cash for operating expenses (e.g., Wages, Advertising, Rent, Telephone, etc.)

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Cash Basis would considerthis an expense since

cash was spent.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Modified Cash Basis wouldalso consider this an

expense since cash was spent.

ExpenseCash

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Accrual Basis would also considerthis an expense because services were received.

ExpenseCash

ExpenseCash

EXPENSE/ASSET EXAMPLE

Pay cash for prepaid items (e.g., Insurance, Supplies, etc.)

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Cash Basis would considerthis an expense since

cash was spent.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Modified Cash Basis:Sets up an asset account for

items that will last more than one accounting period.

Prepaid AssetCash

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Accrual Basis: An asset account is debited

for items that will benefit morethan one accounting period.

Prepaid AssetCash

Prepaid AssetCash

EXPENSE/ASSET EXAMPLE

Pay cash for property, plant, and equipment

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Cash Basis would still considerthis an expense, causing a large reduction in profits

this year.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

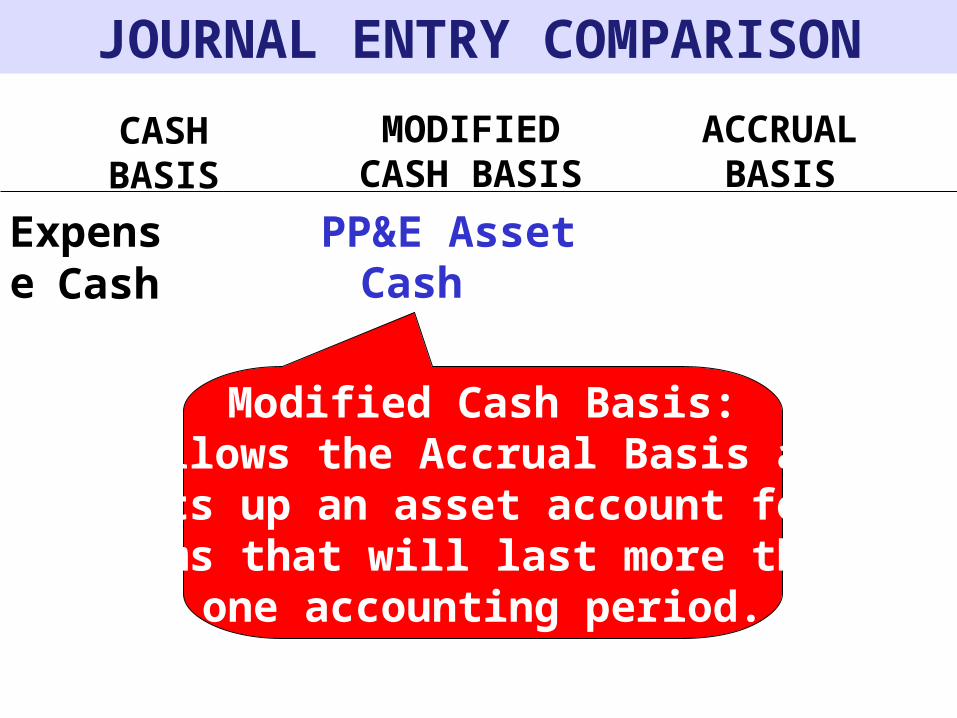

Modified Cash Basis:Follows the Accrual Basis andsets up an asset account for

items that will last more than one accounting period.

PP&E AssetCash

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Accrual Basis records Property, Plant, & Equipment

as assets so their cost can be expensed (depreciated) over

their useful lives.

PP&E AssetCash

PP&E AssetCash

EXPENSE/ASSET EXAMPLE

Received a bill for services received

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

No Entry is made sinceNo Cash was exchanged.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis also wouldNOT journalize this event.

No Cash was received or spent.

No Entry No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis records the receipt of services as an expense and

the resulting obligation as a liability.

No Entry No Entry ExpenseAccts. Payable

END-OF-PERIOD ADJUSTMENT EXAMPLE

Wages earned by employees but not paid

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

No entry is made sinceno cash was exchanged;

expense will be recognizedwhen employees are paid.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis also wouldNOT journalize this event.

No Entry No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis records the expense at the time it is incurred,

not when it is paid.The resulting liability is also recognized.

No Entry No Entry Wages ExpenseWages Payable

END-OF-PERIOD ADJUSTMENT EXAMPLE

Prepaid items used (e.g., Supplies, Insurance, etc.)

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

No entry is made sinceno cash was exchanged.Expense was recognized

when items were purchased.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis createdan asset when the items were

purchased and recognizes the expense when the items

are consumed.

No Entry ExpensePrepaid Asset

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis also createdan asset when the items were

purchased and recognizes the expense when the items

are consumed.

No Entry ExpensePrepaid Asset

ExpensePrepaid Asset

END-OF-PERIOD ADJUSTMENT EXAMPLE

Depreciation on property, plant, and equipment

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

No entry is made sinceno cash was exchanged.

Entire purchase price was recognized as an expense when

items were purchased.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis createsan asset when the items were

purchased and depreciates them over their useful lives.

No Entry Deprec. ExpAccum. Depr.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis spreads the costof long-term assets over their useful lives (Depreciation).

No Entry Deprec. ExpAccum. Depr.

Deprec. ExpAccum. Depr.

OTHER EXAMPLES

Purchase of assets on account

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

No entry is made sinceno cash was exchanged.

An expense will be recordedwhen payment is made.

No Entry

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Modified Cash Basis sets up the asset and liability

accounts.

No Entry AssetAccts. Payable

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

Accrual Basis also sets up the asset and liability

accounts.

No Entry AssetAccts. Payable

AssetAccts. Payable

OTHER EXAMPLES

Payments for assets purchased on account

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Cash Basis would considerthis an expense since

cash was spent.

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Since the Modified Cash Basishad recorded the liability

when the item was purchased,it debits the liability when

the payment is made.

Accts. PayableCash

CASH BASIS

MODIFIED CASH BASIS

ACCRUAL BASIS

JOURNAL ENTRY COMPARISON

ExpenseCash

Accrual Basis will record the payment of the liability that wascreated at the asset’s purchase.

Accts. PayableCash

Accts. PayableCash

MODIFIED CASH BASIS

No Accounts Receivable account, instead:– Appointment record, and– Client/patient ledger

Patient Ledger is used for billing. Revenue is recorded only when Cash is

received.

COMBINATION JOURNAL

Used instead of a General Journal:– Under the Modified Cash Basis– Typically used by small professional service

businesses

Speeds up the journalizing of common transactions

Special Columns for Cash Debits and Credits and other frequently used accounts

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

General columns can record entriesto all accounts.

COMBINATION JOURNAL

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

To more efficiently record cash transactions,special columns are set up to record

debits and credits to the Cash account.

COMBINATION JOURNAL

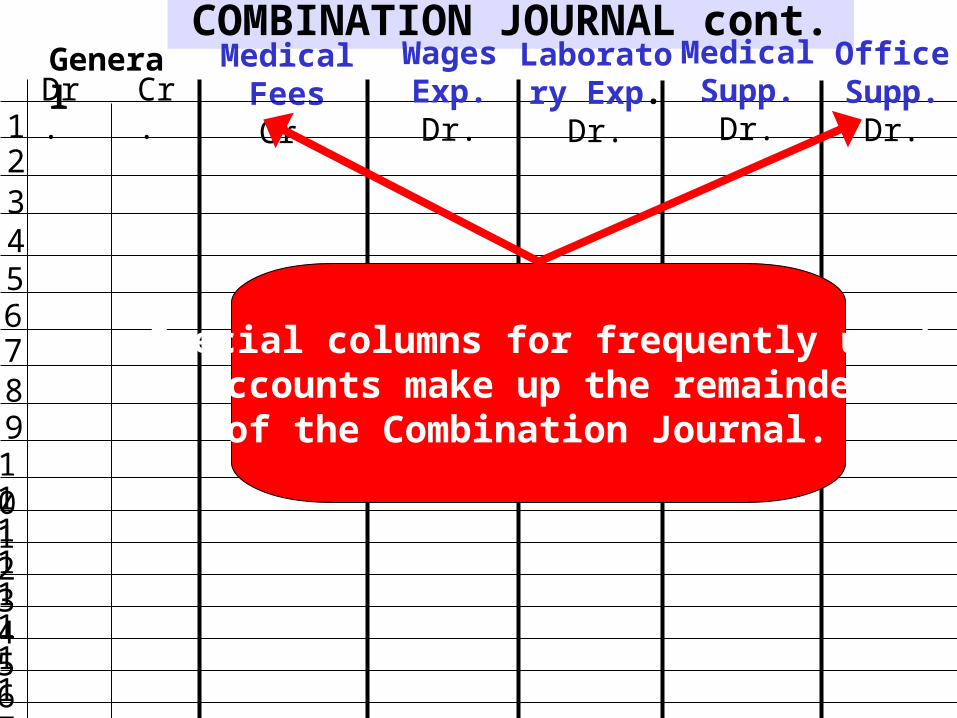

COMBINATION JOURNAL cont.GeneralDr. Cr.

Medical Fees Cr.

1234567891011121314151617

Wages Exp. Dr.

Laboratory Exp. Dr.

Medical Supp. Dr.

Office Supp. Dr.

Special columns for frequently usedaccounts make up the remainder

of the Combination Journal.

DateCash

Dr. Cr. DescriptionGeneral

Dr. Cr.1234567891011121314151617

PR

Let’s journalize some transactions.

COMBINATION JOURNAL

DateCash

Dr. Cr. DescriptionGeneral

Dr. Cr.1234567891011121314151617

PRJune 1

June 1st Ray Bonita invested$50,000 in the business.

COMBINATION JOURNAL

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PRJune 1 50,000

Cash was increased (Debit).

COMBINATION JOURNAL

DateCash

Dr. Cr. DescriptionGeneral

Dr. Cr.1234567891011121314151617

PRJune 1 50,000

Capital should be increased also. (Credit)

COMBINATION JOURNAL

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PRJune 1 50,000 50,000

This Combination Journal does nothave a special column for the

Capital account, so the “General”credit column will be used.

COMBINATION JOURNAL

DateCash

Dr. Cr. DescriptionGeneral

Dr. Cr.1234567891011121314151617

PR

When an entry is made to either of the “General” columns,

the account name must be listedin the “Description” area.

June 1 50,000 50,000R. Bonita, Capital

COMBINATION JOURNAL

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

June 2, paid for a one-year insurance policy, $6,000.

June 1 50,000 50,000R. Bonita, Capital2 6,000 Prepaid Insurance 6,000

COMBINATION JOURNAL

DateCash

Dr. Cr. DescriptionGeneral

Dr. Cr.1234567891011121314151617

PR

June 3, purchased medicalequipment for cash, $22,000.

June 1 50,000 50,000 R. Bonita, Capital2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,000

COMBINATION JOURNAL

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

June 4, paid bill forlaboratory work, $300.

June 1 50,000 50,000 R. Bonita, Capital2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 300

COMBINATION JOURNAL

GeneralDr. Cr.

Medical Fees Cr.

1234567891011121314151617

Wages Exp. Dr.

Laboratory Exp. Dr.

Medical Supp. Dr.

Office Supp. Dr.

50,0006,000

22,000300

COMBINATION JOURNAL cont.

DateCashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

June 5, purchased office furniture on credit from Bittle’s Furniture, $9,000.

June 1 50,000 50,000 R. Bonita, Capital2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005

COMBINATION JOURNAL

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

No entry is made in the “Cash” columns.

June 1 50,000 50,000R. Bonita, Capital2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

1234567891011121314151617

PR

Two entries are made in the “General” columns.

June 1 50,000 50,000 R. Bonita, Capital2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture 9,000

Accts. Pay - Bittle’s 9,000

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

123456

20212223242526

PRJune 1 50,000 50,000 R. Bonita, Capital

2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture

Accts. Pay - Bittle’s 9,000

25

273030

500 Office Furniture Accts. Pay - Bittle’s 3,500

9,000

4,000

2,5007,000

10,000 10,000R. Bonita, Drawing

Once all transactions for the month arerecorded, all columns are totaled.

The sum of the debit columns shouldequal the sum of the credit columns.

75,200 54,030 56,450 62,500

COMBINATION JOURNAL cont.GeneralDr. Cr.

Medical Fees Cr.

123456

20212223242526

Wages Exp. Dr.

Laboratory Exp. Dr.

Medical Supp. Dr.

Office Supp. Dr.

50,0006,000

22,000300

4,0003,500

10,0007,000

2,500

56,450 62,500 25,200 8,500 980 450 150

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

123456

20212223242526

PRJune 1 50,000 50,000R. Bonita, Capital

2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture

Accts. Pay - Bittle’s 9,000

25

273030

500 Office Furniture Accts. Pay - Bittle’s 3,500

9,000

4,000

2,5007,000

10,000 10,000R. Bonita, Drawing

Debit columns:Cash $ 75,200General 56,450Wages Expense 8,500Laboratory Exp. 980Medical Supplies 450Office Supplies 150Total Debits $141,730

75,200 54,030 56,450 62,500

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

123456

20212223242526

PRJune 1 50,000 50,000R. Bonita, Capital

2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture

Accts. Pay - Bittle’s 9,000

25

273030

500 Office Furniture Accts. Pay - Bittle’s 3,500

9,000

4,000

2,5007,000

10,000 10,000R. Bonita, Drawing

Credit columns:Cash $ 54,030General 62,500Medical Fees 25,200Total Credits $141,730

75,200 54,030 56,450 62,500

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

123456

20212223242526

PRJune 1 50,000 50,000R. Bonita, Capital

2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture

Accts. Pay - Bittle’s 9,000

25

273030

500 Office Furniture Accts. Pay - Bittle’s 3,500

9,000

4,000

2,5007,000

10,000 10,000R. Bonita, Drawing

Combination Journal Balances!!!Debit Columns = Credit Columns

75,200 54,030 56,450 62,500

COMBINATION JOURNAL cont.GeneralDr. Cr.

Medical Fees Cr.

123456

20212223242526

Wages Exp. Dr.

Laboratory Exp. Dr.

Medical Supp. Dr.

Office Supp. Dr.

50,0006,000

22,000300

4,0003,500

10,0007,000

2,500

56,450 62,500 25,200 8,500 980 450 150

COMBINATION JOURNALDate

CashDr. Cr. Description

GeneralDr. Cr.

123456

20212223242526

PRJune 1 50,000 50,000 R. Bonita, Capital

2 6,000 Prepaid Insurance 6,0003 22,000 Medical Equipment 22,0004 3005 Office Furniture

Accts. Pay - Bittle’s 9,000

25

273030

500 Office Furniture Accts. Pay - Bittle’s 3,500

9,000

4,000

2,5007,000

10,000 10,000R. Bonita, Drawing

Let’s look at posting.

75,200 54,030 56,450 62,500

POSTING THE GENERAL COLUMNS

Accounts debited or credited in the general columns are posted individually throughout the month.– In the same manner as posting from the

General Journal– “CJ” for Combination Journal and the page

number are entered in the PR column of the ledger account.

– Account Numbers are entered into the journal’s PR column.

POSTING THE SPECIAL COLUMNS

Post the TOTALS of the special columns to the appropriate general ledger accounts.– This saves time and reduces the potential for

errors.

“CJ” and page number are recorded in the account’s PR column.

Account number is entered in parentheses on the journal below the column total.

END-OF-PERIOD

The Modified Cash Basis work sheet is prepared in the same manner as an Accrual work sheet.

Financial Statements are also prepared in the same manner.

Adjusting and closing entries are made in the combination journal and posted to the ledger.