chapter 11morolda.pbworks.com/w/file/fetch/91232136/chap011.ppt .pdf112 % the long run in pure...

TRANSCRIPT

Chapter 11 Pure Compe**on in the Long Run

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-‐2

The Long Run in Pure Competition

• In the long-‐run • Firms can expand or contract capacity • Firms can enter or exit the industry

LO1

11-‐3

Profit Maximization in the Long Run

• Easy entry and exit • The only long-‐run adjustment we consider

• Iden*cal costs • All firms in the industry have iden*cal costs

• Constant-‐cost industry • Entry and exit of firms do not affect resource prices

LO1

11-‐4

Long Run Adjustment Process

• Adjustment process in pure compe**on • Firms seek profits and shun losses • Firms are free to enter or to exit • Produc*on will occur at firm’s minimum average total cost • Price will equal minimum average total cost

LO2

11-‐5

Long Run Equilibrium

• Entry eliminates profits • Firms enter • Supply increases • Price falls

• Exit eliminates losses • Firms leave • Supply decreases • Price rises

LO2

11-‐6

Entry Eliminates Economic Profits

(a) Single firm

(b) Industry

P P

q Q 0 0 100 90,000 80,000 100,000

ATC

MR

MC

$60

50

40 D1

S1

D2

$60

50

40

S2

LO2

11-‐7

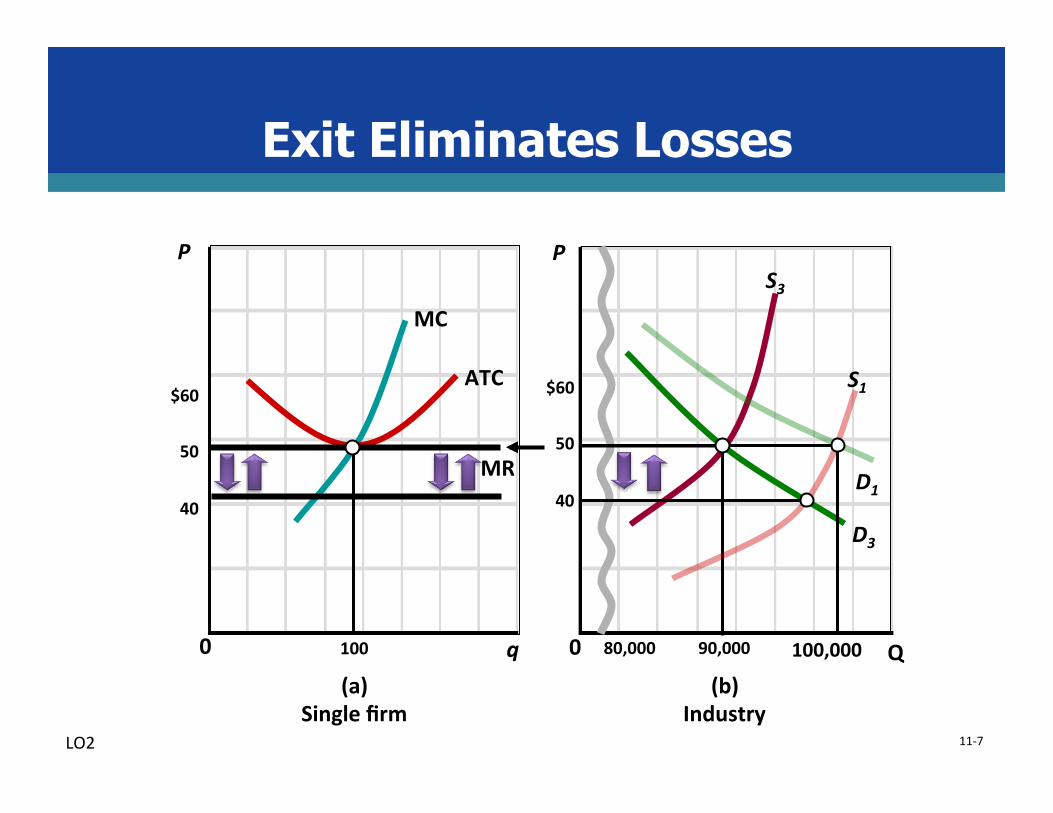

Exit Eliminates Losses

(a) Single firm

(b) Industry

P P

q Q 0 0 100 90,000 80,000 100,000

ATC

MR

MC

$60

50

40 D3

S3

D1

$60

50

40

S1

LO2

11-‐8

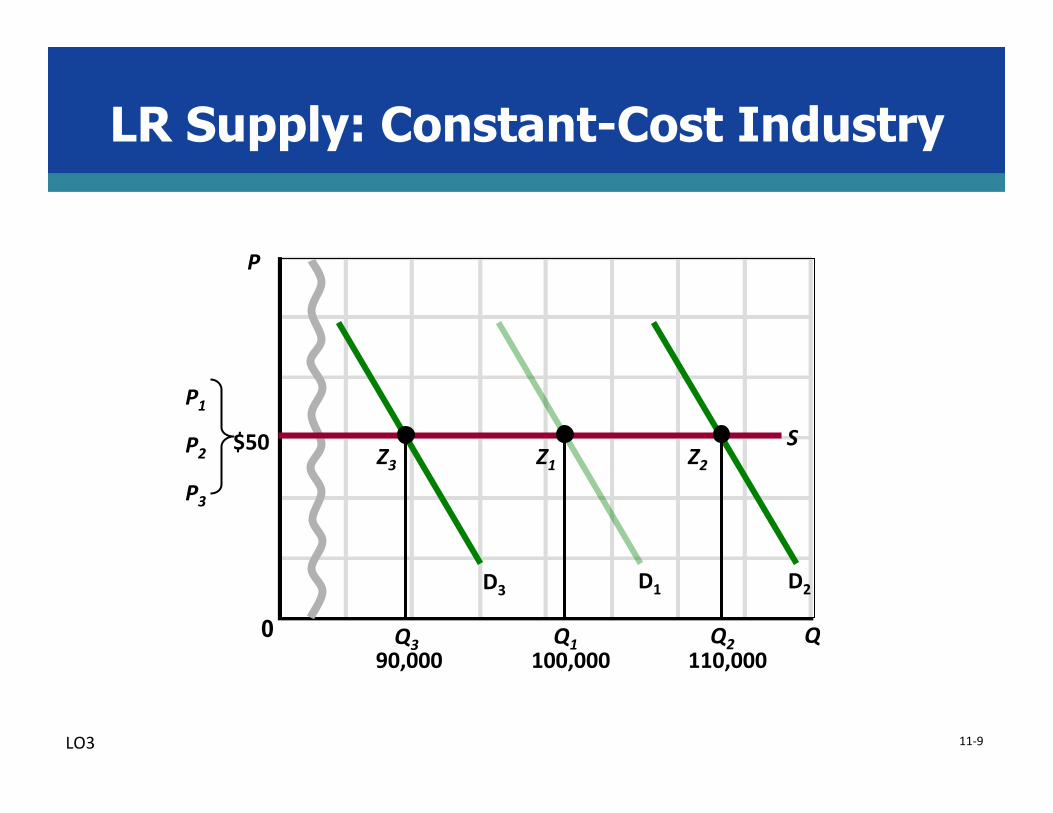

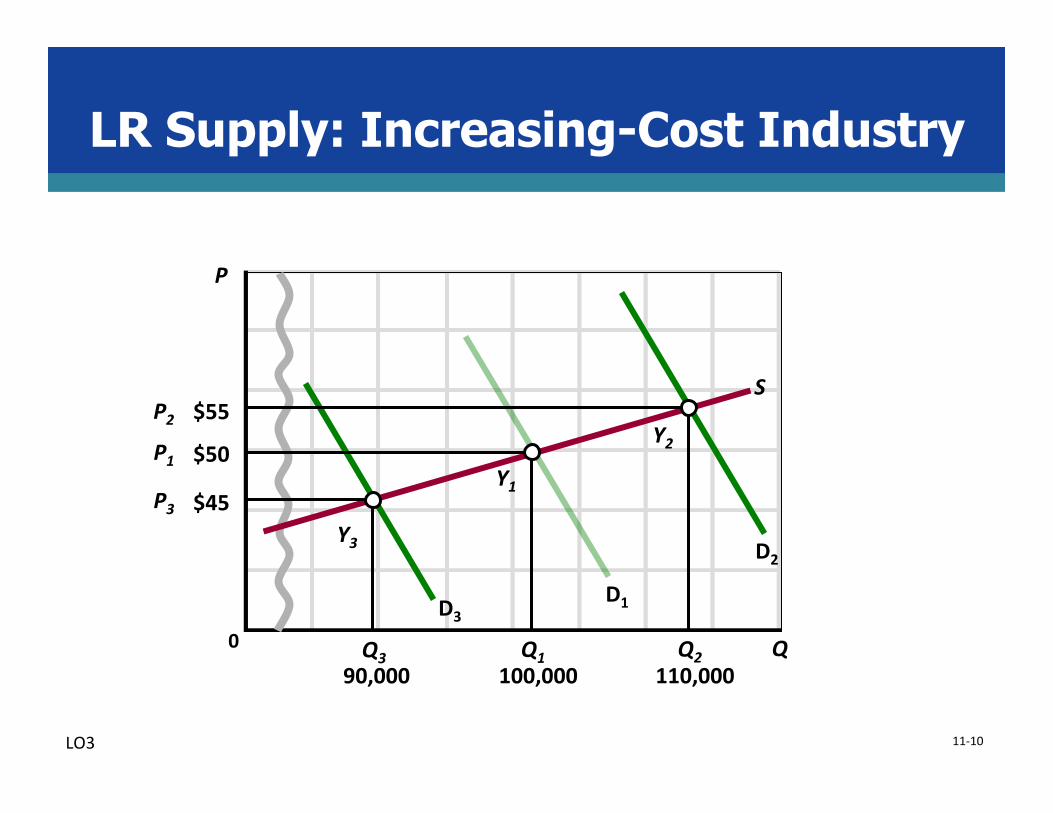

Long Run Supply Curves

• Constant-‐cost industry • Entry/exit does not affect LR ATC • Constant resource prices • Special case

• Increasing-‐cost industry • Most industries • LR ATC increases with expansion • Specialized resources

• Decreasing-‐cost industry LO3

11-‐9

LR Supply: Constant-Cost Industry

P

0 Q 90,000 100,000 110,000 Q3 Q1 Q2

$50

P1 P2 P3

S Z1 Z2 Z3

D3 D1 D2

LO3

11-‐10

LR Supply: Increasing-Cost Industry

P

0 Q 90,000 100,000 110,000 Q3 Q1 Q2

$50 P1

S

Y1

Y2

Y3

D3 D1

D2

$45

$55 P2

P3

LO3

11-‐11

LR Supply: Decreasing-Cost Industry

P

0 Q 90,000 100,000 110,000 Q3 Q1 Q2

$50 P1

S

X1

X2

X3

D3

D1

D2

$45

$55 P3

P2

LO3

11-‐12

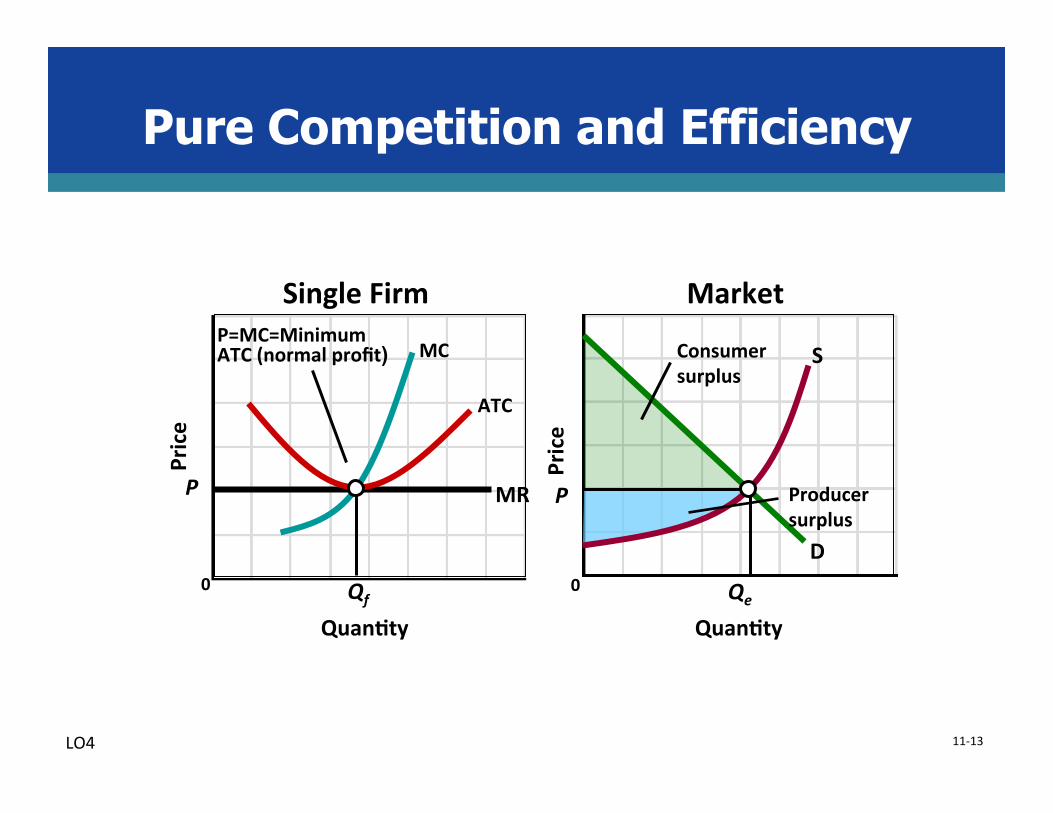

Pure Competition and Efficiency

• In the long run, efficiency is achieved • ProducKve efficiency • Producing where P = minimum ATC

• AllocaKve efficiency • Producing where P = MC

• Triple equality • P= MC= minimum ATC

• Consumer surplus and producer surplus are maximized

LO4

11-‐13

Pure Competition and Efficiency

Single Firm Market

Price

Price

QuanKty QuanKty

0 0

P MR

D

S

Qe Qf

ATC

MC P=MC=Minimum ATC (normal profit)

P

Consumer surplus

Producer surplus

LO4

11-‐14

Dynamic Adjustments

• Purely compe**ve markets will automa*cally adjust to: • Changes in consumer tastes • Resource supplies • Technology

• Recall the “Invisible Hand”

LO4

11-‐15

Technological Advance and Competition

• Entrepreneurs would like to increase profits beyond just a normal profit • Decrease costs by innova*ng • New product development

LO5

11-‐16

Creative Destruction

• Compe**on and innova*on may lead to “creaKve destrucKon”

• Crea*on of new products and methods may destroy the old products and methods

LO5

11-‐17

A Patent Failure?

• Patents give the inventor exclusive rights to market and sell their product for 20 years

• May hinder “crea*ve destruc*on” • Eliminate patents on complicated, hard to copy products

• Speed up innova*on by increasing the opportuni*es of poten*al new compe*tors