chapter iv price and volume effects of nifty...

TRANSCRIPT

76

CHAPTER IV

PRICE AND VOLUME EFFECTS OF NIFTY INDEX REVISIONS: A TEST OF PRICE PRESSURE

HYPOTHESIS

4.1 INTRODUCTION

Stock indices play a prominent role in the functioning of stock markets. They reflect

the behaviour of the overall equity market and serve as a benchmark for portfolio

performance. They are also used as an underlying asset in derivative instruments

such as index futures, index options. Further, stock indices aid in passive fund

management by index funds.

Stock indices are regularly monitored and their composition is revised, whenever

required, to ensure that they reflect the true state of the stock market. Owing to the

rapidly changing market conditions and performance of stocks, stock index revisions

have now become a common phenomenon in almost all the markets worldwide.

Stock indices may be revised on account of various reasons. For instance, a stock

currently listed in the index may no longer meet the criteria laid down for a stock’s

existence in the index; hence, the index will be revised and the stock would be

excluded from the index. Indices may be revised also when stocks undergo corporate

actions such as mergers, liquidation, among others.

Stock index revisions can have significant effect on the price and volume of the

stocks undergoing the revision. Examining such effects would help understand the

functioning of the stock markets and the behaviour of market players like index fund

77

managers. It would also aid the investors to profit by framing appropriate investment

strategies.

In the finance literature, two differing views prevail regarding the effects of stock

index revisions. One view, termed as price pressure hypothesis (PPH), argues that

the price effects associated with index revisions are temporary, whereas the other

view asserts that they are permanent, which could be due to varied reasons.

Price pressure hypothesis proposed by Scholes (1972) states that index revisions will

cause a transitory change in the price of stocks that are included to or excluded from

the index, and that the prices will gradually revert to their fundamental values after

the revision. Such price movement is attributed to the heavy trading activity of index

fund managers in response to index revisions.

When an index undergoes revision, index fund15 managers, who track the index,

would rebalance their portfolios by buying the stocks added to the index and selling

those deleted from the index; however, in order to minimize the tracking error, the

fund managers wait until the revision day to update their portfolio. Such trading

activity of index fund managers causes a shift in the demand of the concerned stocks;

the demand for the stocks added to the index increase, while that of the stocks

15 An index fund is a fund that invests in the stocks of the target index in the same proportion in which

these stocks exist in the index. It thereby tries to replicate the index returns and achieve the same

performance as the target index. The performance of such funds is evaluated on the basis of tracking

error. Tracking error refers to the difference between the fund's return and the return of the index

being tracked.

78

deleted from the index decrease. This shift in demand increases the price of the

included stocks and decreases the price of the excluded stocks. Such price increases

(decreases) attract the passive sellers (buyers) who would otherwise not trade. Thus

according to PPH, prior to index revision, price of the stocks added to the index

would increase, while that of stocks deleted from the index decrease.

Once the index revision is over and the index fund managers have updated their

portfolios, the stock prices will revert to their fundamental values, since the heavy

trading by index fund managers would dissipate. Such price reversals after index

revisions enable the passive sellers (buyers) to profit by unwinding their positions if

desired. This way, they are compensated for providing liquidity to the market at the

time of index revisions.

From the above discussion it follows that, according to price pressure hypothesis, the

price and volume effects associated with stock index revisions are temporary. The

prices of stocks added to (deleted from) the index would increase (decrease) prior to

index revision, which would eventually revert to the fundamental values post

revision. The trading volume would temporarily increase for both stock additions

and deletions.

The price and volume effects associated with stock index revisions has been

subjected to extensive empirical examination. The pioneering works on this issue are

those of Harris & Gurel (1986), Shleifer (1986) and Woolridge & Ghosh (1986).

79

Harris & Gurel (1986) investigated the price and volume effects of changes in the

composition of S&P 500 index and reported evidence supporting the price pressure

hypothesis. The study found that stock prices increased by more than three percent

after the announcement of addition and that the stock price increase fully reversed

after two weeks. Further, on the first trading day after the announcement of addition,

large increase in volume is also observed.

On the other hand, evidence refuting price pressure hypothesis was reported by

Shleifer (1986) that examined the price behaviour of stocks included to S&P 500. It

was observed that stock inclusions into S&P 500 were associated with a three

percent announcement date capital gain and that most of it persisted for at least 10 to

20 trading days.

Woolridge & Ghosh (1986) investigated the firms added to and deleted from the

S&P 500 Index and found some evidence in support of price pressure hypothesis.

The study observed temporary stock price effects around deletions. Further,

permanent stock price effect around additions was observed, along with temporary

increase in trading volume.

Since then, various studies have tested price pressure hypothesis. However, majority

of them have tested this issue for the US market and the index that has been largely

used is S&P 500. The results reported by these studies are mixed; some support PPH

whereas others refute it. Similar to Harris & Gurel (1986), the studies that found

evidence in support of PPH are Lynch & Mendenhall (1997), Erwin & Miller

(1998), Dash (2002), Elliott & Warr (2003) and Elliott et al. (2006). On the other

80

hand, similar to Shleifer (1986), studies that have found the price effects of index

revisions to be permanent are Jain (1987), Dhillon & Johnson (1991), Edmister et al.

(1994), Beneish & Whaley (1996) and Chen et al. (2004).

Apart from the above discussed studies that focus on S&P 500 index revisions,

empirical research that examines index revisions pertaining to US market other than

S&P 500 is also available. For instance, using the US stock market indices, viz.,

Dow Jones Industrial and Dow Jones Transportation Averages, Polonchek &

Krehbiel (1994) found that the price and volume effects are inconsistent with price

pressure hypothesis. Similarly, for Dow Jones Industrial Average, Beneish &

Gardner (1995) found that price pressure hypothesis is not supported. In a later

study, Consolandi et al. (2009) for Dow Jones Sustainability Stoxx Index also

documented that index revisions have permanent effects.

Madhavan (2003) examined the effects of revisions made to the US indices, viz.,

Russell 3000 and 2000 indices. The study reports that significant abnormal returns

are observed around the reconstitutions, which could be attributed to temporary price

pressure. Subsequently, Biktimirov et al. (2004) for Russell 2000 index also

supported the price pressure hypothesis. On the contrary, Chen (2006) for US

Russell indices found evidence refuting price pressure hypothesis.

Docking & Dowen (2006) examined the price and volume effects of compositional

changes made to S&P 600 index and found the effects of index revisions to be

temporary. Similar evidence supporting price pressure hypothesis is reported by

Shankar & Miller (2006) for S&P 600 index.

81

Besides US indices, prior empirical research has examined the effects of revisions

made to indices of other markets as well. However, the studies on each market are

very limited. For the Canadian stock market, using Toronto Stock Exchange 300

index, Chung & Kryzanowski (1998) have found evidence in favour of price

pressure hypothesis, whereas Masse et al. (2000) report evidence inconsistent with

price pressure hypothesis.

Chakrabarti (2002) studied the price and volume effects of addition of Indian stocks

to Morgan Stanley Capital International (MSCI) India Standard Index and found

evidence refuting price pressure hypothesis. It was observed that the price increase

associated with stock additions was permanent. Contrary to this, evidence supporting

the price pressure hypothesis was reported by Shu et al. (2004) that examined the

market reaction for Taiwanese listed firms that are added to or deleted from the

MSCI free indices. Further, Chakrabarti et al. (2005) found some evidence of price

pressure in case of additions and deletions of stocks from MSCI Standard Country

Indices for 29 countries.

For the UK market, Gregoriou & Ioannidis (2006) examined the price and volume

effects of stock inclusions and exclusions from FTSE 100 index and reported

evidence inconsistent with price pressure hypothesis. On the other hand, using the

FTSE 100 index changes, Mase (2007) and Mazouz & Saadouni (2007) found the

price effects to be temporary, thereby, lending support to the price pressure

hypothesis. Similar evidence supporting price pressure hypothesis is provided by

Vespro (2006) that examined the compositional changes in FTSE100 index along

with the French indices CAC40 and SBF120.

82

Apart from the above discussed studies, support for PPH is also found in Chan &

Howard (2002) for All Ordinaries Index of Australian stock market, Bechmann

(2004) for Danish blue-chip KFX Index and Doeswijk (2005) for Amsterdam

Exchanges index of Dutch market, while evidence refuting PPH is found in Liu

(2000) for Nikkei 500 Index of Japanese market, Hyland & Swidler (2002) for New

Zealand Stock Exchange’s NZSE40 Index and Wilkens & Wimschulte (2005) for

German Stock indices.

As far as the Indian market is concerned, very few studies have been carried out on

the effects of stock index revisions. The study by Marisetty & Vedpuriswar (2003)

tested the price dynamics around Sensex reconstitutions. The study found that there

is price reversal for additions two days after the effective day, whereas for deletions

there is no such price reversal.

In a later study, Kumar (2007) examined the effects of revisions made to Nifty index

and Junior Nifty index. It is found that, for addition (deletion) of stocks to (from)

Nifty Index, the stock prices significantly increased (decreased) on the effective day,

which reverted after about a week’s time; no abnormal volumes were observed

around the effective day. Such reactions were, however, not observed in the case of

Junior Nifty revisions. The price reactions associated with Nifty revisions provide

some support for PPH, but the lack of abnormal volume in the effective day window

makes this support less forceful.

From the review of literature, it is evident that the validity of price pressure

hypothesis has been extensively investigated by the extant studies. However, in the

83

Indian market, very few studies have focused on this issue. Of these studies, the

study by Marisetty & Vedpuriswar (2003) has examined only the price effects.

Kumar (2007) has examined both the price and volume effects of index revisions;

however, the conclusions drawn by the study regarding price pressure hypothesis are

not emphatic. In this chapter, an attempt has thus been made to test whether PPH

holds good in the Indian market by examining both the price and volume effects of

S&P CNX Nifty revisions.

4.2 METHODOLOGY

To test the validity of PPH in the Indian market, event study methodology, as

described in Wilkens & Wimschulte (2005), is employed and the impact of inclusion

(exclusion) of a stock to (from) Nifty index on the price and volume of the stock is

examined. The event study method enables to estimate and draw inferences about the

impact of a particular event on the behaviour of stocks under consideration. The

event under consideration, here, is the inclusion or exclusion of a stock from Nifty.

The basic terminology of event study is discussed below:

» Event Day: Event day is the day on which the event under consideration

occurs. In this study, the effective day of index revision i.e. the day on which

a stock is included to or excluded from Nifty is the event day and is denoted

as day ‘0’.

» Event Period: Event period is the period over which a particular event is

expected to have an impact on the stock under consideration. Event period

includes the event day and some days prior to and after the event day. The

84

event period for this study consists of the event day and 10 days prior to and

10 days after the event day i.e. -10,…,-1,0,+1,…,+10.

» Estimation Period: Estimation period is the period that is used to obtain the

values of expected return (volume). The estimation period for this study starts

from 170 days prior to and ends at 51 days prior to the announcement day

(AD) of the event i.e. AD-170 to AD-51.

4.2.1 PRICE EFFECTS OF INDEX REVISIONS

To assess the impact of index revisions on the prices of concerned stocks, abnormal

returns are computed. Abnormal return (AR) of a stock is the difference between the

stock’s observed return and its expected return. Observed return is the actual return

observed, whereas expected or normal return is the return that should have been

observed had the event had not taken place.

In this study, abnormal returns are computed using three methods viz., mean

adjusted model, market adjusted model and market model. In each of these models,

the observed return of stock i on day t (��,�) is computed as

��,� = �� � ��,���,���� (4.1)

where ��,� is the price of stock i on day t; ��,��� is the price of stock i on day t-1; i =

1,2,…..,N; N = no. of sample stocks.

85

Each of the three methods differs the way in which the expected return is computed.

The computation of abnormal return under each of the three methods is discussed

below.

(i) Mean Adjusted Model

Under this model, abnormal return of stock i on day t (���,�) is computed as

���,� = ��,� − (��) (4.2)

where ��,� is the observed return of stock i on day t; (��) is the expected return of

stock i; i = 1,2,….,N; N = no. of sample stocks; t = -10,…,0,…,+10.

The expected return of stock i [(��)] is computed as the average of the observed

returns of stock i during the estimation period,

(��) =1

120 ��,������

������

(4.3)

where ��,� is the observed return of stock i on day s; i = 1,2,….,N; N = no. of sample

stocks.

The abnormal return specified in equation (4.2) thus becomes,

���,� = ��,� −1

120 ��,������

������

(4.4)

86

(ii) Market Adjusted Model

In this model, the expected return of stock i on day t [(��,�)] is equal to the market

return on day t (��,�) i.e.

(��,�) = ��,� (4.5)

where i = 1,2,….,N; N = no. of sample stocks; t = -10,…,0,…,+10.

Therefore, the abnormal return is,

���,� = ��,� − ��,� (4.6)

(iii) Market Model

The market model assumes a linear relationship between return of a stock and the

market return, as shown in equation (4.7):

��,� = �� + ����,� (4.7)

where ��,� is the return of stock i on day t; ��,� is the market return on day t; �� is the

market model constant; �� is the slope coefficient.

For each stock i, using the stock’s return and the market return during the estimation

period, the relationship in equation (4.7) is estimated and the parameters �� and �� are obtained. Then, using these parameters, the expected return of stock i on day t

[(��,�)] is computed as,

(��,�) = �� + ����,� (4.8)

87

where �� and �� are the parameters estimated using the returns of stock i and that of

the market during the estimation period; ��,� is the market return on day t; i =

1,2,….,N; N = no. of sample stocks; t = -10,…,0,…,+10.

Abnormal return is then computed as,

���,� = ��,� − (��,�) (4.9)

After calculating the abnormal returns, the mean abnormal return (MAR) is computed

to draw an overall inference about the impact of the event on stock prices. MAR on

day t ( ���) is obtained as the average of abnormal returns of the sample stocks on

day t, i.e.

��� =1����,�

��

(4.10)

where ���,� is the abnormal return of stock i on day t; i = 1,2,…,N; N = no. of sample

stocks; t = -10,…,0,…,+10.

In order to draw inference about the impact of the event over multi-period interval,

cumulative abnormal returns (CAR) are computed. CAR over period [t1,t2] is

obtained as the sum of mean abnormal returns on each day during that period.

�����,�� = ���

��

���

(4.11)

where ��� is the mean abnormal return on day t.

88

4.2.2 VOLUME EFFECTS OF INDEX REVISIONS

To assess the impact of index revisions on the volume of stocks undergoing the

revision, abnormal volumes are computed. As a proxy for trading volume, no. of

shares traded is considered. The trading volume of stock i on day t (��,�) is log

transformed as ��(1 + ��,�). Similarly, the trading volume of market on day t (��,�)

is log transformed as ��(1 + ��,�).

Abnormal volume (AV) is computed employing three methods viz., mean adjusted

model, modified Harris/Gurel model and market model.

(i) Mean Adjusted Model

Under this model, the expected volume of stock i [(��)] is computed as the average

of the trading volume of stock i during the estimation period

(��) =1

120 ��(1 + ��,�)

�����

������

(4.12)

where ��,� is the volume of stock i on day s; i = 1,2,….,N; N = no. of sample stocks.

The abnormal volume of stock i on day t (���,�) is then computed as

���,� = ���1 + ��,�� − (��)

i.e.

89

���,� = ���1 + ��,�� −1

120 ��(1 + ��,�)

�����

������

(4.13)

where ��,� is the volume of stock i on day t; i = 1,2,….,N; N = no. of sample stocks; t

= -10,…,0,…,+10; ��,� is the volume of stock i on day s.

(ii) Modified Harris/Gurel Model

Under this model, the abnormal volume of stock i on day t (���,�) is computed as

���,� = �� � 1 + ��,�1 + ��,�

� − 1

120 ���1 + ��,�

1 + ��,�

������

������

(4.14)

where ��,� is the volume of stock i on day t; i = 1,2,….,N; N = no. of sample stocks; t

= -10,…,0,…,+10; ��,� is the market volume on day t; ��,� is the volume of stock i

on day s; ��,� is the market volume on day s.

(iii) Market Model

Abnormal volume of stock i on day t (���,�), in this model, is computed as

���,� = ���1 + ��,�� − (�� + ����(1 + ��,�)) (4.15)

where ��,� is the volume of stock i on day t; i = 1,2,….,N; N = no. of sample stocks; t

= -10,…,0,…,+10; ��,� is the market volume on day t; �� and �� are the parameters

obtained by estimating the following relation:

90

���1 + ��,�� = �� + ����(1 + ��,�) (4.16)

where ��,� is the volume of stock i on day s; i = 1,2,….,N; N = no. of sample stocks; s

= AD–170 to AD–51; ��,� is the market volume on day s.

After calculating the abnormal volumes, the mean abnormal volume on day t ( ���) is computed to draw an overall inference about the impact of the event on trading

volume. ��� is obtained as the average of the abnormal volumes of sample stocks

on day t, i.e.

��� =1����,�

��

(4.17)

where ���,� is the abnormal volume of stock i on day t; i = 1,2,….,N; N = no. of

sample stocks; t = -10,…,0,…,+10.

Testing for statistical significance

The statistical significance of ��� under each of the three models is tested using

the following test statistic

�����=

����̂( ��) (4.18)

where �̂� ��� is the standard deviation of MAR’s of estimation period computed as

91

�̂� ��� =�∑ � ��� −

1120

∑ ��������

������������

������

119

�

(4.19)

where ��� is the �� on day u; ��� is the �� on day v.

The statistical significance of �����,�� under each of the three models is tested using

the following test statistic

������,��=

�����,���̂� ������ − �� + 1 (4.20)

where �̂� ���is the standard deviation of MAR’s of estimation period as specified

in equation (4.19).

The test statistics in equations (4.18) and (4.20) follow student t-distribution with

119 degrees of freedom. The test statistic to test the statistical significance of MAV is

analogous to that of MAR.

4.2.3 HYPOTHESISED PRICE AND VOLUME EFFECTS OF INDEX REVISIONS AS PER PPH

This section discusses the hypothesized price and volume effects of index revisions

around the effective day, as per PPH. As discussed in section 4.1, when index

revisions occur, index fund managers rebalance their portfolios so as to replicate the

index. However, in order to minimize the tracking error of their portfolios, fund

managers wait until the revision day to rebalance their portfolios. PPH asserts that

such trading activity of fund managers will result in price increase on the effective

92

day for stocks added to the index and price drop for those deleted from the index.

Such price changes will result in abnormal returns on the effective day of revision.

Thus, the null hypotheses with respect to the price effects of Nifty revisions are:

H0pa: There is no abnormal return on the effective day for stocks added to Nifty

H0pd: There is no abnormal return on the effective day for stocks deleted from Nifty

Since index fund managers concentrate their trading on the effective day of index

revision, it is expected that there will be abnormal trading volume on the effective

day, both for stock additions and deletions. The null hypotheses with respect to the

volume effects of Nifty revisions are:

H0va: There is no abnormal trading volume on the effective day for stocks added to

Nifty

H0vd: There is no abnormal trading volume on the effective day for stocks deleted

from Nifty

As per PPH, once index revision is over and index fund managers have updated their

portfolios, the stock prices will revert to their fundamental values. This implies that

price effects observed on the effective day are temporary, and hence, abnormal

returns observed on the effective day should revert post index revision. To test this,

the following null hypotheses are framed.

H0ra: There are no abnormal returns in the post effective day period for stocks added

to Nifty

H0rd: There are no abnormal returns in the post effective day period for stocks

deleted from Nifty

93

4.3 EMPIRICAL RESULTS

The initial sample comprised of the revisions made to S&P CNX Nifty index during

the period September 1996 to September 2010. During this period, there were 61

stock inclusions and 61 stock exclusions. Of this initial sample, those stocks that

were excluded from Nifty on account of corporate actions such as mergers,

amalgamations, demergers etc. were removed.

From the resulting sample, revisions that did not meet the following criteria were

removed:

1. Announcement date should be available for the revision

2. The stock undergoing the revision should not have undergone any other

corporate events, such as mergers, rights issue, bonus issue, stock split,

dividend payment and buy-back of shares, in the respective event and

estimation period

3. For a stock that is included or excluded more than once, it is required that the

event period and estimation period corresponding to each of its events do

not overlap with either the event period or estimation period of its other

events

This screening yielded a sample of 32 inclusions and 32 exclusions. Of this sample,

those stocks that did not have price and volume data over their respective event and

estimation period were removed, which yielded a final sample of 24 inclusions and

31 exclusions16.

16 List of these inclusions and exclusions is provided in Appendix IV-A.

94

Data on firms included and excluded from Nifty along with the respective effective

date and announcement date of revision, the daily closing prices and number of

shares traded of sample stocks, and the daily closing prices and number of shares

traded of Nifty index are collected from Prowess database of Centre for Monitoring

Indian Economy (CMIE) and the official website of NSE17.

4.3.1 PRICE EFFECTS OF NIFTY REVISIONS

In this section, by way of calculating abnormal returns18, the price effects associated

with Nifty index revisions around the effective day of revision are examined. The

price effects around the effective day for stocks added to Nifty are reported in table

4.1. It presents the mean abnormal returns and cumulative abnormal returns under

each of the three models.

17 www.nseindia.com

18 The analysis is carried out in Eviews.

95

Table 4.1: Price effects around the effective day for stock additions to Nifty

N = 24 Mean adjusted model Market adjusted model Market model

Day MAR (%) t-stat

CAR (%) t-stat

MAR (%) t-stat

CAR (%) t-stat

MAR (%) t-stat

CAR (%) t-stat

-10 0.22 0.26 0.22 0.26 0.25 0.45 0.25 0.45 0.06 0.11 0.06 0.11

-9 0.25 0.29 0.46 0.39 -0.34 -0.60 -0.09 -0.11 -0.38 -0.70 -0.32 -0.41

-8 0.25 0.30 0.71 0.49 -0.46 -0.82 -0.55 -0.56 -0.56 -1.02 -0.88 -0.93

-7 0.70 0.83 1.41 0.84 0.24 0.42 -0.31 -0.28 -0.08 -0.14 -0.96 -0.87

-6 0.11 0.13 1.52 0.81 0.35 0.62 0.03 0.03 0.16 0.29 -0.80 -0.65

-5 -0.25 -0.30 1.26 0.62 0.00 -0.01 0.03 0.02 -0.10 -0.19 -0.90 -0.67

-4 -0.89 -1.06 0.38 0.17 -0.44 -0.79 -0.41 -0.28 -0.49 -0.90 -1.40 -0.96

-3 -0.14 -0.17 0.23 0.10 -0.01 -0.02 -0.43 -0.27 -0.02 -0.03 -1.41 -0.91

-2 -1.57 -1.88* -1.34 -0.53 0.75 1.33 0.32 0.19 1.08 1.97* -0.33 -0.20

-1 0.21 0.26 -1.12 -0.43 -0.03 -0.06 0.29 0.16 -0.10 -0.19 -0.44 -0.25

96

0 2.20 2.63*** 1.08 0.39 1.54 2.74*** 1.83 0.98 1.46 2.67*** 1.02 0.56

1 -1.08 -1.29 0.00 0.00 0.09 0.15 1.92 0.99 0.08 0.15 1.11 0.58

2 -0.14 -0.17 -0.14 -0.05 -0.36 -0.65 1.56 0.77 -0.57 -1.03 0.54 0.27

3 -0.56 -0.67 -0.70 -0.22 -0.61 -1.08 0.95 0.45 -0.68 -1.24 -0.14 -0.07

4 -0.33 -0.40 -1.03 -0.32 0.06 0.10 1.01 0.46 -0.01 -0.01 -0.15 -0.07

5 0.95 1.14 -0.08 -0.02 0.37 0.65 1.37 0.61 0.01 0.01 -0.14 -0.06

6 0.06 0.07 -0.02 -0.01 0.08 0.14 1.45 0.63 0.08 0.14 -0.06 -0.03

7 1.01 1.21 0.99 0.28 0.53 0.95 1.98 0.83 0.36 0.65 0.29 0.13

8 0.48 0.58 1.47 0.40 0.64 1.14 2.62 1.07 0.49 0.90 0.78 0.33

9 -0.92 -1.10 0.56 0.15 -0.61 -1.09 2.01 0.80 -0.70 -1.28 0.08 0.03

10 0.18 0.21 0.73 0.19 0.02 0.04 2.03 0.79 -0.04 -0.07 0.05 0.02

Note: MAR denotes Mean Abnormal Return; CAR denotes Cumulative Abnormal Return; day ‘0’ denotes the event day i.e. the effective day of stocks’ addition to Nifty index; *** and * denotes significance at 1% and 10% respectively

97

As shown in table 4.1, on day ‘0’ i.e. the effective day of stock additions to Nifty,

significant positive mean abnormal returns of 2.20%, 1.54%19 and 1.46%20 are

observed, under the mean adjusted model, market adjusted model and market model

respectively. This finding leads to the rejection of the null hypothesis H0pa, which

implies that stocks added to Nifty experience significant positive abnormal returns

on the effective day of addition.

Significant mean abnormal returns are observed also on day ‘-2’ under the mean

adjusted model and the market model. Other than this, significant mean abnormal

returns are not observed on any day in the pre-event period. Further, in the pre-event

period, no significant cumulative abnormal returns are observed. In the post-event

period, neither mean abnormal return nor cumulative abnormal return is found to be

significant on any day.

Thus, the results of table 4.1 indicate that stocks added to Nifty experience

significant positive price effect on the effective day of addition.

Table 4.2 presents the price effects around the effective day for stocks deleted from

Nifty. It reports the mean abnormal returns and cumulative abnormal returns under

each of the three models.

19 This value is exactly the same as reported by Liu (2000) for stocks added to Nikkei 500.

20 This value is almost equal to the one reported by Kumar (2007) for stocks added to Nifty.

98

Table 4.2: Price effects around the effective day for stock deletions from Nifty

N = 31 Mean adjusted model Market adjusted model Market model

Day MAR

(%) t-stat CAR

(%) t-stat MAR

(%) t-stat CAR

(%) t-stat MAR

(%) t-stat CAR

(%) t-stat

-10 0.21 0.28 0.21 0.28 0.26 0.53 0.26 0.53 0.36 0.77 0.36 0.77

-9 1.20 1.61 1.41 1.33 0.34 0.69 0.61 0.86 0.51 1.09 0.87 1.31

-8 0.78 1.05 2.19 1.69* 0.37 0.75 0.98 1.14 0.32 0.68 1.19 1.46

-7 -0.13 -0.17 2.06 1.38 -0.94 -1.87* 0.05 0.05 -0.95 -2.03** 0.24 0.25

-6 -0.56 -0.74 1.50 0.90 -0.56 -1.12 -0.51 -0.46 -0.41 -0.88 -0.17 -0.17

-5 0.67 0.90 2.17 1.19 0.78 1.56 0.26 0.22 0.86 1.84* 0.69 0.60

-4 -0.87 -1.16 1.31 0.66 -0.68 -1.37 -0.42 -0.32 -0.40 -0.86 0.29 0.23

-3 -0.03 -0.04 1.28 0.61 -0.02 -0.04 -0.44 -0.31 0.03 0.05 0.31 0.24

-2 -2.26 -3.02*** -0.98 -0.44 -0.48 -0.96 -0.92 -0.61 -0.21 -0.44 0.11 0.08

-1 0.29 0.39 -0.69 -0.29 0.30 0.60 -0.62 -0.39 0.25 0.52 0.35 0.24

99

0 -0.21 -0.28 -0.90 -0.36 -1.38 -2.76*** -2.00 -1.21 -1.34 -2.84*** -0.98 -0.63

1 -0.54 -0.73 -1.44 -0.56 0.32 0.65 -1.67 -0.97 0.51 1.09 -0.47 -0.29

2 -0.22 -0.29 -1.66 -0.61 -0.45 -0.91 -2.13 -1.18 -0.35 -0.74 -0.82 -0.48

3 -0.80 -1.08 -2.46 -0.88 -0.74 -1.49 -2.87 -1.54 -0.56 -1.19 -1.38 -0.78

4 -0.53 -0.70 -2.99 -1.03 -0.60 -1.20 -3.47 -1.79* -0.31 -0.66 -1.69 -0.93

5 0.94 1.26 -2.05 -0.68 0.28 0.56 -3.19 -1.60 0.39 0.83 -1.29 -0.69

6 -0.20 -0.26 -2.24 -0.73 -0.12 -0.24 -3.31 -1.61 -0.01 -0.01 -1.30 -0.67

7 0.42 0.56 -1.82 -0.57 -0.02 -0.05 -3.33 -1.57 0.11 0.24 -1.18 -0.59

8 0.42 0.57 -1.40 -0.43 0.22 0.43 -3.12 -1.43 0.45 0.96 -0.73 -0.36

9 0.14 0.18 -1.26 -0.38 0.27 0.53 -2.85 -1.28 0.38 0.82 -0.35 -0.17

10 -0.02 -0.02 -1.28 -0.37 -0.10 -0.21 -2.96 -1.29 -0.05 -0.10 -0.40 -0.18

Note: MAR denotes Mean Abnormal Return; CAR denotes Cumulative Abnormal Return; day ‘0’ denotes the event day i.e. the effective day of stocks’ deletion from Nifty index; ***, ** and * denotes significance at 1%, 5% and 10% respectively

100

As is evident from table 4.2, on day ‘0’ i.e. the effective day of stock deletions from

Nifty, significant negative mean abnormal returns of -1.38% and -1.34% are

observed under the market adjusted model and market model respectively. This

finding leads to the rejection of the null hypothesis H0pd, which implies that stocks

deleted from Nifty experience significant negative abnormal returns on the effective

day of deletion.

Significant mean abnormal returns are observed also on day ‘-2’ under mean

adjusted model, day ‘-7’ under market adjusted model and days ‘-7’ and ‘-5’ under

the market model. Other than these days, significant mean abnormal returns are not

observed on any day in the pre-event period. Further, in the pre-event period, except

the cumulative abnormal return on day ‘-8’ under the mean adjusted model, no

significant cumulative abnormal returns are observed. In the post-event period, other

than the cumulative abnormal return on day ‘4’ under the market adjusted model,

neither mean abnormal return nor cumulative abnormal return is found to be

significant on any day.

Thus, the results of table 4.2 indicate that stocks deleted from Nifty experience

significant negative price effect on the effective day of deletion.

4.3.2 VOLUME EFFECTS OF NIFTY REVISIONS

In this section, by way of calculating abnormal volumes21, the volume effects

associated with Nifty index revisions around the effective day of revision are

examined. Table 4.3 reports the volume effects around the effective day for stocks

21 The analysis is carried out in Eviews.

101

added to Nifty. It presents the mean abnormal volumes pertaining to stock additions

to Nifty under each of the three models.

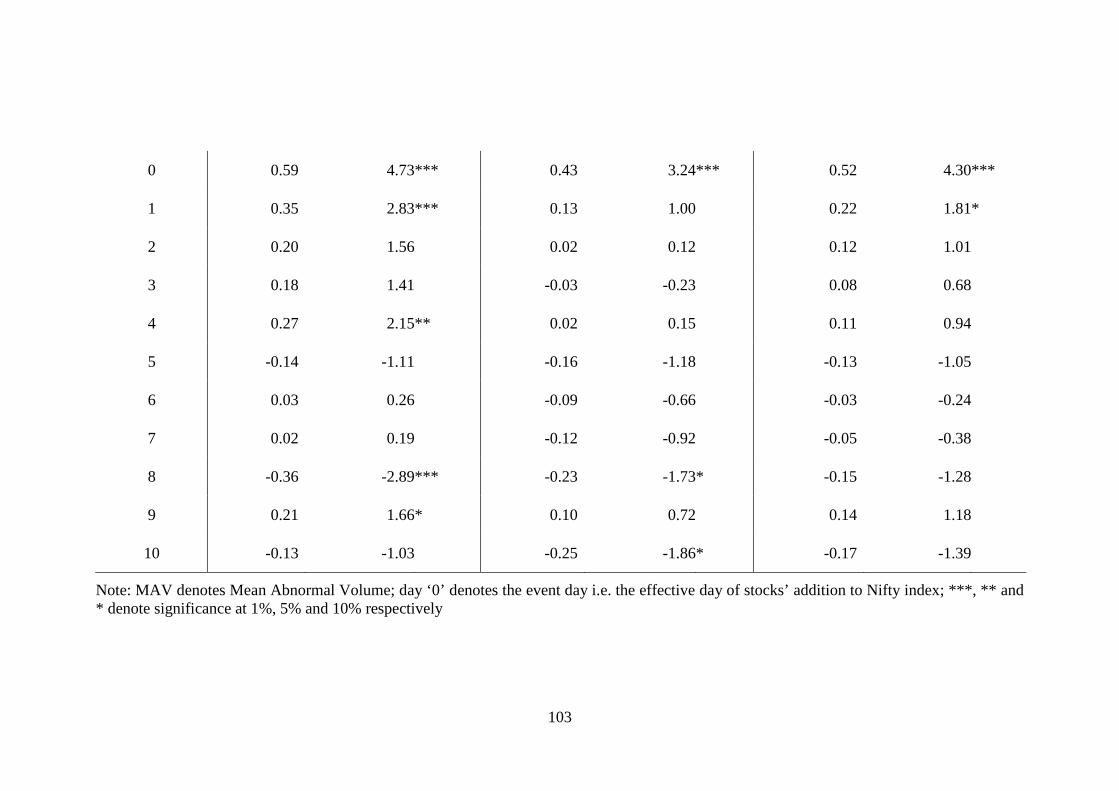

The results of table 4.3 indicate that there are significant positive mean abnormal

volumes on the effective day of addition (day ‘0’) and the day prior to addition (day

‘-1’). Significant positive mean abnormal volume of 0.59, 0.43 and 0.52 is observed,

on the effective day, under the mean adjusted model, modified Harris/Gurel model

and market model respectively. This finding leads to the rejection of the null

hypothesis H0va, which implies that stocks added to Nifty experience significant

positive abnormal trading volume on the effective day of addition.

In the pre-event period, significant positive mean abnormal volumes are observed

also on days ‘-6’ and ‘-4’ under the mean adjusted model and market model. In the

post-event period, under both these models, significant positive mean abnormal

volume is observed on day ‘1’. Further, significant mean abnormal volumes are

observed also on days ‘4’, ‘8’ and ‘9’ under the mean adjusted model and days ‘8’

and ‘10’ under the modified Harris/Gurel model.

Thus, the finding of table 4.3 that stocks added to Nifty experience significant

positive abnormal trading volume on effective day of addition and the day prior to

addition, indicates that there is increased trading volume associated with stock

additions to Nifty.

The volume effects around the effective day for stocks deleted from Nifty are

presented in table 4.4. It reports the mean abnormal volumes pertaining to stock

deletions from Nifty under each of the three models.

102

Table 4.3: Volume effects around the effective day for stock additions to Nifty

N = 24 Mean adjusted model Modified Harris/Gurel model Market model

Day MAV t-stat MAV t-stat MAV t-stat

-10 0.09 0.73 0.01 0.11 0.09 0.73

-9 0.11 0.90 -0.01 -0.08 0.03 0.25

-8 0.15 1.20 0.08 0.63 0.16 1.31

-7 0.13 1.07 -0.02 -0.17 0.07 0.54

-6 0.27 2.17** 0.15 1.12 0.22 1.82*

-5 0.15 1.21 0.06 0.42 0.19 1.55

-4 0.25 1.99** 0.15 1.10 0.21 1.74*

-3 -0.02 -0.20 -0.03 -0.23 0.05 0.43

-2 -0.21 -1.67* -0.08 -0.63 -0.05 -0.43

-1 0.63 5.04*** 0.51 3.88*** 0.60 4.95***

103

0 0.59 4.73*** 0.43 3.24*** 0.52 4.30***

1 0.35 2.83*** 0.13 1.00 0.22 1.81*

2 0.20 1.56 0.02 0.12 0.12 1.01

3 0.18 1.41 -0.03 -0.23 0.08 0.68

4 0.27 2.15** 0.02 0.15 0.11 0.94

5 -0.14 -1.11 -0.16 -1.18 -0.13 -1.05

6 0.03 0.26 -0.09 -0.66 -0.03 -0.24

7 0.02 0.19 -0.12 -0.92 -0.05 -0.38

8 -0.36 -2.89*** -0.23 -1.73* -0.15 -1.28

9 0.21 1.66* 0.10 0.72 0.14 1.18

10 -0.13 -1.03 -0.25 -1.86* -0.17 -1.39

Note: MAV denotes Mean Abnormal Volume; day ‘0’ denotes the event day i.e. the effective day of stocks’ addition to Nifty index; ***, ** and * denote significance at 1%, 5% and 10% respectively

104

Table 4.4: Volume effects around the effective day for stock deletions from Nifty

N = 31 Mean adjusted model Modified Harris/Gurel model Market model

Day MAV t-stat MAV t-stat MAV t-stat

-10 0.00 -0.01 -0.03 -0.15 -0.06 -0.34

-9 0.07 0.36 -0.05 -0.30 -0.03 -0.18

-8 0.13 0.68 0.08 0.46 0.13 0.77

-7 0.00 0.02 -0.07 -0.43 -0.09 -0.54

-6 0.07 0.38 0.02 0.14 -0.02 -0.10

-5 -0.07 -0.39 -0.12 -0.71 -0.14 -0.79

-4 0.07 0.38 0.02 0.09 0.03 0.14

-3 -0.12 -0.63 -0.03 -0.18 0.04 0.22

-2 -0.15 -0.79 0.05 0.32 -0.01 -0.06

-1 0.73 3.83*** 0.67 3.98*** 0.70 4.03***

105

0 0.45 2.37** 0.32 1.87* 0.33 1.93*

1 0.10 0.51 -0.06 -0.35 -0.06 -0.34

2 0.16 0.82 0.05 0.30 0.06 0.32

3 0.03 0.18 -0.12 -0.73 -0.09 -0.50

4 0.10 0.52 -0.06 -0.35 -0.06 -0.37

5 -0.02 -0.09 -0.07 -0.39 -0.07 -0.39

6 0.04 0.23 -0.05 -0.30 -0.04 -0.21

7 0.00 0.02 -0.13 -0.74 -0.10 -0.59

8 -0.04 -0.23 0.00 -0.01 0.10 0.56

9 -0.07 -0.38 -0.19 -1.12 -0.18 -1.02

10 -0.29 -1.51 -0.37 -2.19** -0.39 -2.25**

Note: MAV denotes Mean Abnormal Volume; day ‘0’ denotes the event day i.e. the effective day of stocks’ deletion from Nifty index; ***, ** and * denotes significance at 1%, 5% and 10% respectively

106

The results of table 4.4 indicate that there are significant positive mean abnormal

volumes on the effective day of deletion (day ‘0’) and the day prior to deletion (day

‘-1’). On the effective day of deletion, significant positive mean abnormal volume of

0.45, 0.32 and 0.33 is observed under the mean adjusted model, modified

Harris/Gurel model and market model respectively. This finding rejects the null

hypothesis H0vd, which implies that stocks deleted from Nifty experience significant

positive abnormal trading volume on the effective day of deletion. Besides these two

days, significant abnormal volumes are not observed on any of the days in the event

period, excepting day ‘10’.

Thus, the finding of table 4.4 that stocks deleted from Nifty experience significant

positive abnormal trading volume on effective day of deletion and the day prior to

deletion, indicates that there is increased trading volume associated with stock

deletions from Nifty.

In sum, the volume effects of stock additions along with the corresponding positive

price effect (tables 4.3 and 4.1), indicate that, when stocks are added to Nifty,

demand for those stocks increase leading to a rise in their prices on the effective day

of addition. Similarly, the volume effects of stock deletions together with the

corresponding negative price effect (tables 4.4 and 4.2), reveal that, when stocks are

deleted from Nifty, supply of (demand for) those stocks increase (decrease) leading

to a drop in their prices on the effective day of deletion.

107

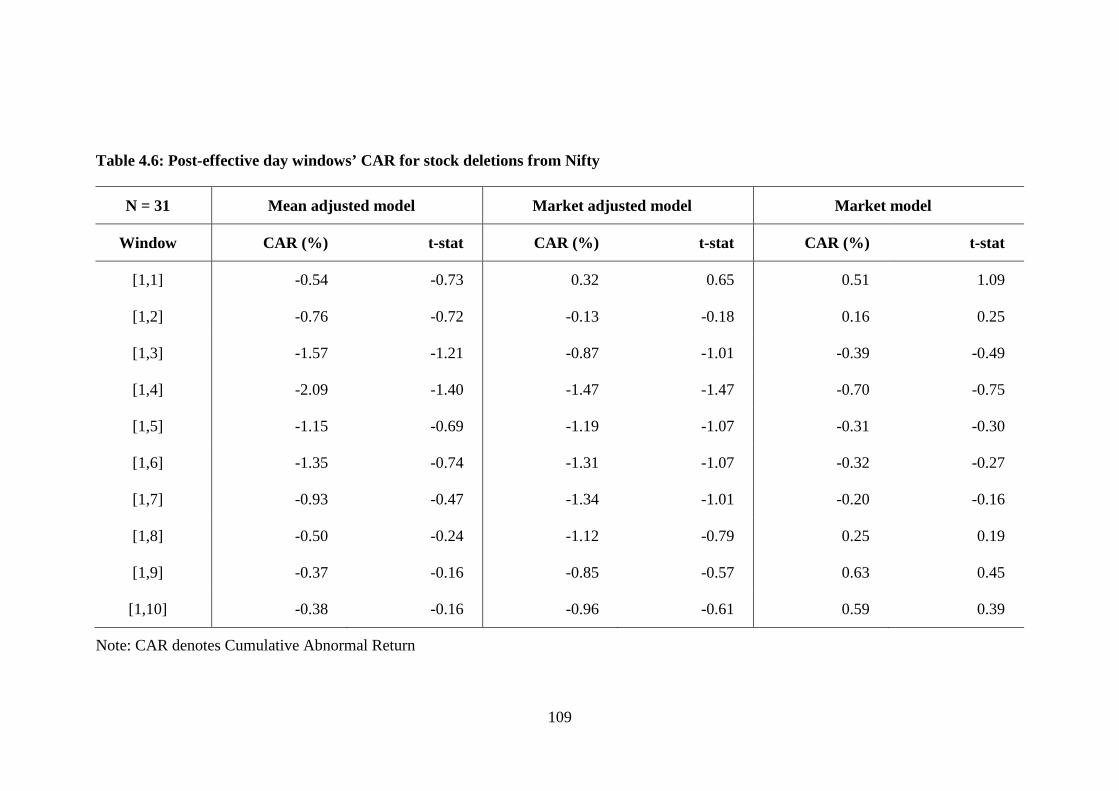

4.3.3 NIFTY REVISIONS: TEST OF PRICE PRESSURE HYPOTHESIS

The price effects that occur on the effective day of revision can be either temporary

or permanent. According to PPH, the price effects associated with index revisions

are temporary. Hence, for PPH to hold, the abnormal returns observed on the

effective day of index revision should reverse in the post effective day period. The

insignificant cumulative abnormal returns reported in tables 4.1 and 4.2 seem to

indicate that the positive (negative) price effect associated with stock additions to

(deletions from) Nifty is permanent. In order to further confirm this finding, it is

tested whether the abnormal returns observed on the effective day of Nifty revision

reveres or not in the post effective day period. For this, cumulative abnormal returns

in the various post-effective day windows, both for stock additions and deletions are

computed, the results of which are presented in tables 4.5 and 4.6.

Table 4.5 reports cumulative abnormal returns over various post-effective day

windows, for stocks added to Nifty. It is evident that, under each of the three models,

cumulative abnormal returns are not significant in any of the post-effective day

windows. This finding fails to reject the null hypothesis H0ra, which implies that, for

stocks added to Nifty, there are no abnormal returns in the post effective day period.

This indicates that the abnormal returns observed on the effective day of stock

additions to Nifty do not revert post index revision; hence, the positive price effect

associated with stock additions to Nifty is permanent.

108

Table 4.5: Post-effective day windows’ CAR for stock additions to Nifty

N = 24 Mean adjusted model Market adjusted model Market model

Window CAR (%) t-stat CAR (%) t-stat CAR (%) t-stat

[1,1] -1.08 -1.29 0.09 0.15 0.08 0.15

[1,2] -1.22 -1.03 -0.28 -0.35 -0.48 -0.62

[1,3] -1.78 -1.23 -0.89 -0.91 -1.16 -1.23

[1,4] -2.11 -1.26 -0.83 -0.74 -1.17 -1.07

[1,5] -1.15 -0.62 -0.46 -0.37 -1.16 -0.95

[1,6] -1.10 -0.54 -0.38 -0.28 -1.09 -0.81

[1,7] -0.09 -0.04 0.15 0.10 -0.73 -0.50

[1,8] 0.39 0.17 0.79 0.50 -0.24 -0.15

[1,9] -0.52 -0.21 0.18 0.11 -0.94 -0.57

[1,10] -0.35 -0.13 0.20 0.11 -0.98 -0.56

Note: CAR denotes Cumulative Abnormal Return

109

Table 4.6: Post-effective day windows’ CAR for stock deletions from Nifty

N = 31 Mean adjusted model Market adjusted model Market model

Window CAR (%) t-stat CAR (%) t-stat CAR (%) t-stat

[1,1] -0.54 -0.73 0.32 0.65 0.51 1.09

[1,2] -0.76 -0.72 -0.13 -0.18 0.16 0.25

[1,3] -1.57 -1.21 -0.87 -1.01 -0.39 -0.49

[1,4] -2.09 -1.40 -1.47 -1.47 -0.70 -0.75

[1,5] -1.15 -0.69 -1.19 -1.07 -0.31 -0.30

[1,6] -1.35 -0.74 -1.31 -1.07 -0.32 -0.27

[1,7] -0.93 -0.47 -1.34 -1.01 -0.20 -0.16

[1,8] -0.50 -0.24 -1.12 -0.79 0.25 0.19

[1,9] -0.37 -0.16 -0.85 -0.57 0.63 0.45

[1,10] -0.38 -0.16 -0.96 -0.61 0.59 0.39

Note: CAR denotes Cumulative Abnormal Return

110

Cumulative abnormal returns over various post-effective day windows for stocks

deleted from Nifty are reported in table 4.6. Under each of the three models, no

significant cumulative abnormal returns are observed in any of the post-effective day

windows. This finding fails to reject the null hypothesis H0rd, which implies that, for

stocks deleted from Nifty, there are no abnormal returns in the post effective day

period. This indicates that the abnormal returns observed on the effective day of

stock deletions from Nifty do not revert post index revision; hence, the negative

price effect associated with stock deletions from Nifty is permanent.

In sum, the empirical evidence drawn from event study reveal that stocks added to

Nifty experience positive price effect on the effective day of revision, whereas those

deleted experience negative price effect on the effective day. Also, there is increased

trading volume associated with both stock additions and deletions. The lack of price

reversal in the post effective day period indicates that the price effects associated

with stock additions to (deletions from) Nifty are permanent; hence, price pressure

hypothesis does not hold in the Indian market.

4.4 CONCLUSION

Stock index revisions are expected to have a significant effect on the price and

volume of the stocks undergoing the revision. As per price pressure hypothesis,

stock index revisions will cause a transitory change in the price and volume of stocks

that are included to or excluded from the index, and the prices will gradually revert

to their fundamental values after the revision. Such price movement is attributed to

the heavy trading activity of index fund managers in response to index revisions.

111

Extensive research has been carried out on testing the validity of price pressure

hypothesis for different markets. However, in the Indian context, very few studies

have focused on this issue; these studies have either examined only the price effects

or if both price and volume effects have been examined, conclusions drawn by the

study regarding the validity of price pressure hypothesis are not emphatic. This

chapter therefore attempted to test whether price pressure hypothesis holds good in

the Indian market by examining the price and volume effects of S&P CNX Nifty

revisions. For this purpose, stocks added to and deleted from Nifty during the period

September, 1996 to September, 2010 are considered and event study methodology is

employed.

The results of event study indicate that stocks added to Nifty experience positive

price effect on the effective day of revision, whereas those deleted experience

negative price effect on the effective day. There is also increased trading volume

associated with both stock additions and deletions. The lack of price reversal in the

post effective day period indicates that the positive (negative) price effect associated

with stock additions to (deletions from) Nifty is permanent; hence, price pressure

hypothesis does not hold in the Indian market.