chapter ii growth of spinning mills in india introduction...

TRANSCRIPT

30

CHAPTER II

GROWTH OF SPINNING MILLS IN INDIA

INTRODUCTION

The "deindustrialization" of the Indian economy and of India's textile

industries in particular, is the subject of a major historiographical debate.

While some scholars have claimed that colonial rule permanently

undermined indigenous production, others have argued that handloom

weavers were able to adjust to colonial conditions and therefore carved out

new niches for themselves. Hanretty (1991) examines handloom weavers in

one part of India, an area that is now Madhya Pradesh, between 1800 and

Indian independence in 1947. Eschewing a simplistic attachment to either of

the two main positions, Hanretty shows that while handloom weavers as a

group faced great competition in the mid-19th century from imported cloths,

some specialist producers were able to cope better than others, mainly

because of their production of specialized products and the security given by

them enhanced caste status. The real challenge came in the 20th century as

India's own mills subordinated weavers to middlemen as the former became

more dependent on mill-spun yarns.

When the British left India in 1947, the economy was only slightly

more industrialized than when they had taken formal control nearly one

hundred years earlier. Wolcott (1997) asks, were they responsible for the

lack of development? Two strains of argument suggest they were. The first,

primarily associated with Amiya Bagchi, faults the British for not giving

sufficient protection to domestic industries. The second, associated with

Morris Morris, faults them for not investing in infrastructure - specifically the

capital market and education. This article reexamines the development of

cotton textile production, the most important factory industry in colonial India.

There is no evidence that any of these factors contributed significantly to the

slow interwar growth of the industry. Thus, Wolcott concludes, there is no

basis for arguing that a national government could have speeded up

31

development. The problems were imbedded in the structure of the labor

market, beyond the control of any government.

By the end of the 19th century, domestic wool production in India was

experiencing a transformation that was largely attributable to colonial rule.

Arable land, which pastoralists needed for their sheep, was becoming less

available; hence, wool production tended to become concentrated in areas

where there were more opportunities for grazing. Railways were important in

helping to transform weaving from a small-scale household-centered activity

to larger factory production. Competition from imported wool led to greater

specialization in weaving and spinning, and encouraged the production of

finer cloth. These transformations, of which the most important seems to be

the loss of common grazing lands, have continued in postcolonial India.

Shah (2001) examines the growth of an industrial working class in

Ahmedabad, chief city of Gujarat. In textiles, the most important industry,

new recruits were chiefly lower-caste landless agricultural laborers and

handloom weavers - men, women, and children. Despite strikes against long

hours and low wages, caste identity remained strong, and stable; effective

trade unions were not achieved1.

GLOBAL TEXTILE TRADE IN INDIA

The share of India in global textile trade is more than 3 percent. It is

predominantly cotton based while world over the trend is shifting towards

Man Made Fibres and blends. In the total world exports of MMF textiles, the

share of India is 3.51 percent as compared to China with 8.35 percent,

Japan with 5.75 percent and Indonesia with 7.60 percent. Besides, the unit

price realisation of Indian exports is one of the lowest which is mainly due to

low value addition, as bulk of India’s exports is in the form of yarn, Grey

fabrics and low value garments. Though the majority of the Indian textile

machinery in weaving and processing is obsolete, the spinning sector has

been fairly modernised. Now, with the introduction of TUFS (Technology

Upgradation Fund Scheme), the weaving and processing sector has been

undergoing rapid changes, which encourages the production of more value

added items and processed fabrics.

32

The spinning industry is dominated by large units and it has been able

to undergo significant modernization since the 1990s. The main factors

behind the modernization include lowering of custom duties and other

restrictions on imports of machinery and equipment and lowering of

restrictions on imports and exports of raw cotton and yarn. The spinning

industry, which is dominated by medium and large units producing more than

90 percent of the output and total value added. During an early period of

policy reform (1983–1990), the demand increased due to spurt in exports,

which caused better utilization of existing spindles and led to reduction in idle

capacity. During later phase (1990–2005), the investment in new spindles

increased at a very rapid rate. This lead to rise in efficiency of the working

spindles and relative productivity of working spindles compared to the most

recent technology improved over time.

The units in spinning sector are relatively less as most of the units in

this segment belong to large sector. This becomes clear as units belonging

to cotton and synthetic spinning in terms of value added accounts for 22.4

percent in the total value added in textile and clothing sector. The high share

in value added compared to units is mainly because of dominance of

medium and large units in spinning sector. The share of large units in total

value addition in cotton and synthetic spinning sector accounts for 86.1

percent.

33

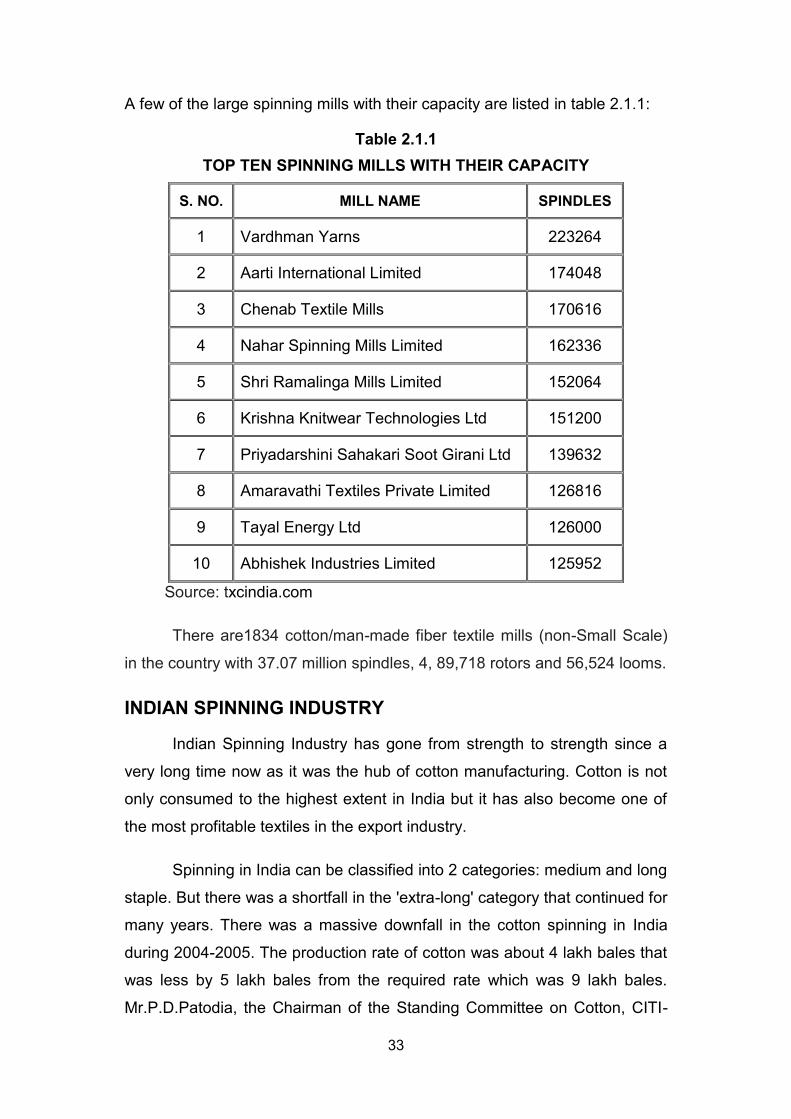

A few of the large spinning mills with their capacity are listed in table 2.1.1:

Table 2.1.1

TOP TEN SPINNING MILLS WITH THEIR CAPACITY

S. NO. MILL NAME SPINDLES

1 Vardhman Yarns 223264

2 Aarti International Limited 174048

3 Chenab Textile Mills 170616

4 Nahar Spinning Mills Limited 162336

5 Shri Ramalinga Mills Limited 152064

6 Krishna Knitwear Technologies Ltd 151200

7 Priyadarshini Sahakari Soot Girani Ltd 139632

8 Amaravathi Textiles Private Limited 126816

9 Tayal Energy Ltd 126000

10 Abhishek Industries Limited 125952

Source: txcindia.com

There are1834 cotton/man-made fiber textile mills (non-Small Scale)

in the country with 37.07 million spindles, 4, 89,718 rotors and 56,524 looms.

INDIAN SPINNING INDUSTRY

Indian Spinning Industry has gone from strength to strength since a

very long time now as it was the hub of cotton manufacturing. Cotton is not

only consumed to the highest extent in India but it has also become one of

the most profitable textiles in the export industry.

Spinning in India can be classified into 2 categories: medium and long

staple. But there was a shortfall in the 'extra-long' category that continued for

many years. There was a massive downfall in the cotton spinning in India

during 2004-2005. The production rate of cotton was about 4 lakh bales that

was less by 5 lakh bales from the required rate which was 9 lakh bales.

Mr.P.D.Patodia, the Chairman of the Standing Committee on Cotton, CITI-

34

CDRA said that the manufacturing of cotton will rise to 11-12 lakh bales in

2010.

The present downfall in the cotton production has witnessed a 50

percent increase in the price of Indian varieties of ELS, which is detrimental

for the spinning industry in India. Spinning mills require domestic

accessibility of ELS cotton in increased quantity and of better fiber qualities.

To survive this downfall in the cotton trade which is a highly profitable

textile in the Indian Spinning Industry, CITI-CDRA is conducting a

conference with various research organizations such as CICR (Nagpur),

JNKVV (Khandwa), UAS (Dharwad), and Regional Textile Mills' Association

in R&D activities. It conducted a discussion pertaining to the development of

new varieties of seeds and adopting the advanced procedure of cultivation

which will add to the profit in the cotton textile sector of the spinning industry.

The most important and efficient step towards the resurgence of cotton

manufacturing would be to develop the ELS varieties with lesser duration

crops and yield to cost-effectiveness and consistency in cultivation. This will

not only motivate the farmers but will also make them stick to the desired

sector of cotton crop.

The yarn spinning industry covers almost 25 percent of the total

industrial production of one of the world's 10 largest economies. Trends are

reviewed every year in accordance with the need and fashion. An elaborate

and detailed assessment is made on various sectors of the yarn spinning

such as production, consumption, and materials. The legislative and the

political consequences are also reviewed at the same time. In addition to it,

other areas that are being reviewed in the yarn spinning sector are exports,

imports, prices, advertising, and sales promotion patterns.

ROLE OF INDIAN SPINNING MILLS

Spinning mills across India would continue production cut till mid-June to

use up cotton yarn inventories of 500 million kg. A week after the `70,000

crore Spinning industry voluntarily cut its production by 33 percent, there has

35

been a marginal movement in the stocks that have remained unsold owing to

price volatility.

"The industry is in a hand-to-mouth situation. We have no option but to

extend our production cut till the unused stocks find takers," said chairperson

of Confederation of Indian Textile Industry (CITI) and MD of Ginni Filaments,

Shishir Jaipuria. Spinning contributes $10 billion to India's $62 billion textile

and clothing sector.

Price volatility of cotton that touched a record of 63 percent high of

`62,000 per candy in the 2010-11 crop season and then came crashing at

`44,000 per candy, destablised the prices of yarn that moved from `204 per

kg in October to `253 per kg in March and then fell `185 per kg in May. India

produced 3,500 million kg of cotton yarn and maintains a stock enough for

10-15 days2.

SHARE IN GROSS DOMESTIC PRODUCT (GDP)

Its importance is underlined by the fact that The Textile industry

accounts for around 4 percent of Gross Domestic Product, 14 percent of

industrial production, 9 percent of excise collections, 18 percent of

employment in the industrial sector, and 16 percent of the country’s total

exports earnings. The Spinning sector, which is integrated to the Textile

industry accounts to 22.4 percent of the total value of the Textile Industry3.

GDP has been quite beneficial in the economic life of the country. The

worldwide trade of textiles and clothing has boosted up the GDP of India to a

great extent as this sector has brought in a huge amount of revenue in the

country. In the past one year, there has been a massive upsurge in the

textile industry of India. The industry size has expanded from $37 billion in

2004-05 to $49 billion in 2006-07. During this era, the local market witnessed

a growth of $7 billion, that is, from $23 billion to $30 billion. The export

market increased from $14 billion to $19 billion in the same period.

36

ECONOMIC TRENDS

The Textile industry has been witnessing a massive upsurge in the

recent years. The industry size has expanded from $49 billion in 2006-07 to

$65 billion in 2009-10. During this era, the local market witnessed a growth

of $15 billion, that is, from $30 billion to $45 billion4.

SPINNING SECTOR – CURRENT SCENARIO

The textile industry turns out a wide range of products. The production

process includes four main activities: spinning, weaving and knitting, wet

processing and stitching (sewing). Production from fibers to spun yarn takes

place through the spinning process and constitutes the first stage. Spinning

involves opening, blending, carding, combing, drawing, drafting and

spinning. It uses four technologies: ring spinning, rotor spinning, air jet

spinning and friction spinning. Ring spinning is the most used in India, its

main advantage being its wide adaptability for spinning different types of

yarn. Rotor spinning technology is also widely used.

Textile spinning units in India can be categorised into three types, i.e.,

conventional, modern and semi-modern. Conventional units have

conventional machines where the production rate is low and the fluff or dust

liberation from the process is within tolerable limits. Modern units have high-

peed machines and higher production rates with increased fluff and dust

generation. Semi- modern units are those which fall between modern and

conventional. Spinning in India can also be classified into two categories

such as medium and long staple. But there was a shortfall in the ‘extra-long’

category during recent times. In the textile mill sector spinning is the most

important segment. During 2007-08, there were exist 2,992 spinning mills in

the country. Of these, 1,773 units belong to large spinning units and the

remaining to medium mills. In composite mills, spinning, weaving and dyeing

activities are integrated.

37

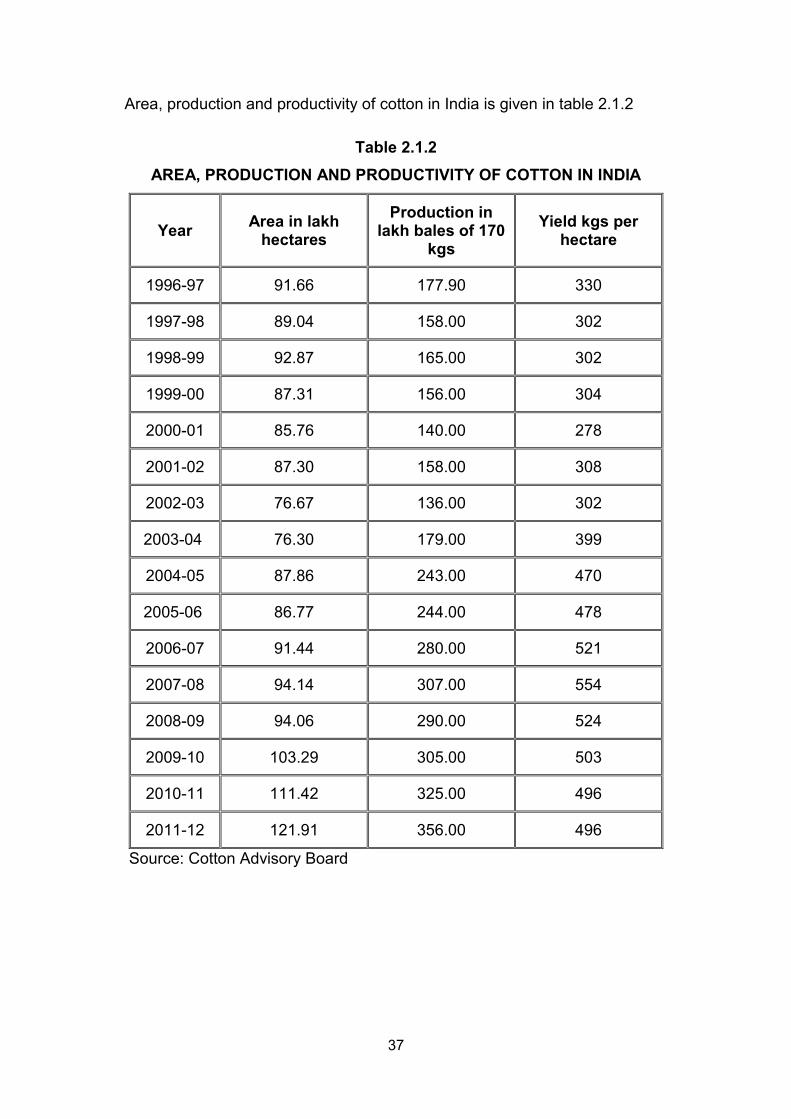

Area, production and productivity of cotton in India is given in table 2.1.2

Table 2.1.2

AREA, PRODUCTION AND PRODUCTIVITY OF COTTON IN INDIA

Year Area in lakh

hectares

Production in lakh bales of 170

kgs

Yield kgs per hectare

1996-97 91.66 177.90 330

1997-98 89.04 158.00 302

1998-99 92.87 165.00 302

1999-00 87.31 156.00 304

2000-01 85.76 140.00 278

2001-02 87.30 158.00 308

2002-03 76.67 136.00 302

2003-04 76.30 179.00 399

2004-05 87.86 243.00 470

2005-06 86.77 244.00 478

2006-07 91.44 280.00 521

2007-08 94.14 307.00 554

2008-09 94.06 290.00 524

2009-10 103.29 305.00 503

2010-11 111.42 325.00 496

2011-12 121.91 356.00 496

Source: Cotton Advisory Board

38

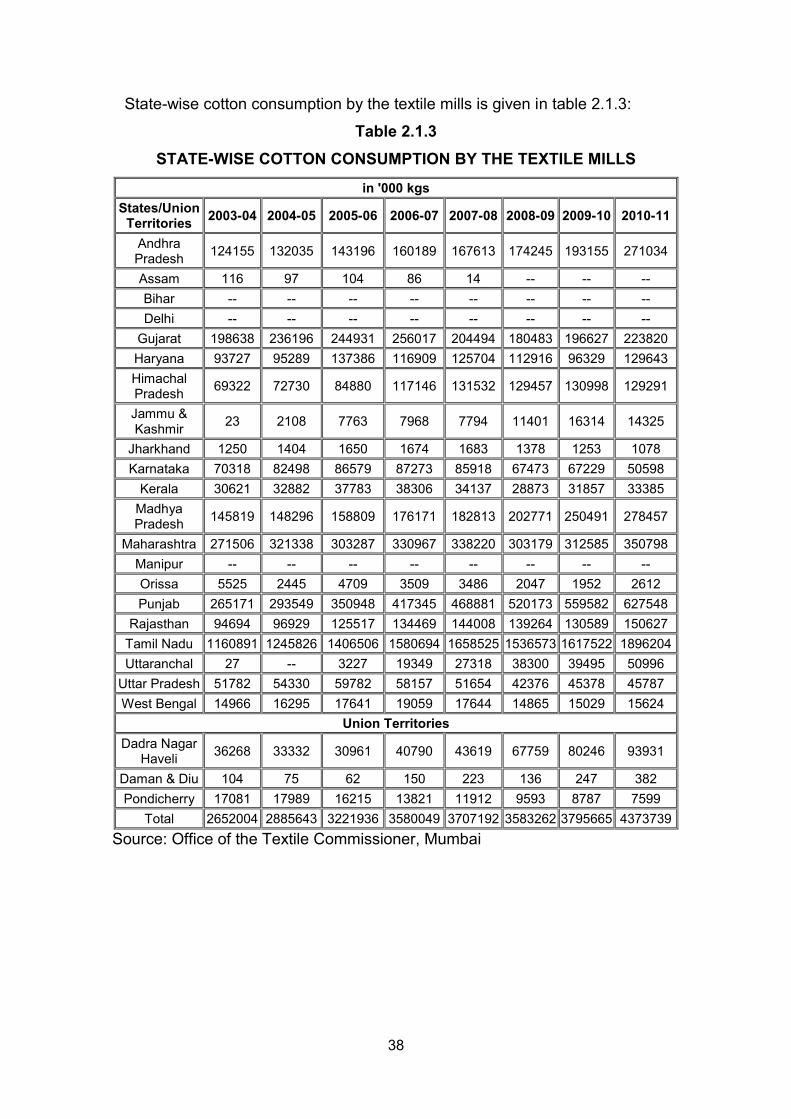

State-wise cotton consumption by the textile mills is given in table 2.1.3:

Table 2.1.3

STATE-WISE COTTON CONSUMPTION BY THE TEXTILE MILLS

in '000 kgs

States/Union Territories

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Andhra Pradesh

124155 132035 143196 160189 167613 174245 193155 271034

Assam 116 97 104 86 14 -- -- --

Bihar -- -- -- -- -- -- -- --

Delhi -- -- -- -- -- -- -- --

Gujarat 198638 236196 244931 256017 204494 180483 196627 223820

Haryana 93727 95289 137386 116909 125704 112916 96329 129643

Himachal Pradesh

69322 72730 84880 117146 131532 129457 130998 129291

Jammu & Kashmir

23 2108 7763 7968 7794 11401 16314 14325

Jharkhand 1250 1404 1650 1674 1683 1378 1253 1078

Karnataka 70318 82498 86579 87273 85918 67473 67229 50598

Kerala 30621 32882 37783 38306 34137 28873 31857 33385

Madhya Pradesh

145819 148296 158809 176171 182813 202771 250491 278457

Maharashtra 271506 321338 303287 330967 338220 303179 312585 350798

Manipur -- -- -- -- -- -- -- --

Orissa 5525 2445 4709 3509 3486 2047 1952 2612

Punjab 265171 293549 350948 417345 468881 520173 559582 627548

Rajasthan 94694 96929 125517 134469 144008 139264 130589 150627

Tamil Nadu 1160891 1245826 1406506 1580694 1658525 1536573 1617522 1896204

Uttaranchal 27 -- 3227 19349 27318 38300 39495 50996

Uttar Pradesh 51782 54330 59782 58157 51654 42376 45378 45787

West Bengal 14966 16295 17641 19059 17644 14865 15029 15624

Union Territories

Dadra Nagar Haveli

36268 33332 30961 40790 43619 67759 80246 93931

Daman & Diu 104 75 62 150 223 136 247 382

Pondicherry 17081 17989 16215 13821 11912 9593 8787 7599

Total 2652004 2885643 3221936 3580049 3707192 3583262 3795665 4373739

Source: Office of the Textile Commissioner, Mumbai

39

FOREIGN EXPORTS

The textiles industry accounts for 14 percent of industrial production

and accounts for nearly 12 percent share of the country's total exports

basket. The Government fixed the target for 2008-09 at $26.55 billion an

increase of 20 percent over the actual performance of $22.14 billion in

2007-08, for export of textiles. However, no targets were fixed for 2009-10.

At present, Indian textile industry holds 3.5 to 4 percent share in the

total textile production across the globe and 3 percent share in the export

production of clothing. USA is known to be the largest purchaser of Indian

textiles.

Nearly half of Indian export was accounted by nine countries namely

Bangladesh, Egypt, China, Portugal, Italy, Turkey, Iran, South Korea and

other countries. Export of major destinations is given in table 2.1.4:

Table 2.1.4

EXPORT TO MAJOR DESTINATIONS

S.NO. COUNTRY NAME EXPORT %

1 Bangladesh 13

2 Egypt 07

3 China 06

4 Portugal 05

5 Italy 08

6 Turkey 05

7 Iran 04

8 South Korea 04

9 Others 48

TOTAL 100

Source: ynfx.com

COTTON-EXPORTING MARKETS

Naturally certain cities in the cotton-producing countries have become

important as cotton-exporting centers. In the United States, Galveston ranks

highest in number of bales received and shipped, the amount running

40

considerably over 2,000,000 bales per year. New Orleans and Savannah

come next. New Orleans usually holds second place with a total yearly

average of nearly 2,000,000 bales, but in 1910 the amount ran down to

1,315,000 bales and Savannah came into second place with 1,365,000

bales. The other important cities receiving and shipping cotton in the

southern United States are: Norfolk, Virginia; Wilmington, North Carolina;

Mobile, Alabama; Brunswick and Charleston, South Carolina. Considerable

cotton is received overland at Baltimore, New York, Philadelphia, and even

at Boston from the cotton states. Cotton exports from India is given in table

2.1.5:

Table 2.1.5

COTTON EXPORTS FROM INDIA

Year Quantity (in lakh bales of

170 kgs) Value in ` /Crores

1996-97 16.82 1655.00

1997-98 3.50 313.62

1998-99 1.01 86.72

1999-00 0.65 52.15

2000-01 0.60 51.43

2001-02 0.50 44.40

2002-03 0.84 66.31

2003-04 12.11 1089.15

2004-05 9.14 657.34

2005-06 47.00 3951.35

2006-07 58.00 5267.08

2007-08 88.50 8365.98

2008-09 35.00 3837.13

2009-10 83.00 10270.21

2010-11 68.80 N.A.

2011-12 84.00 N.A.

Note: Value figures are estimated

NA : Not Available (A): Anticipated

Source: Cotton Advisory Board for Quantity figures

41

COTTON – IMPORTING MARKETS

Similarly, certain large cities have become prominent as the receiving

centers for the great cotton-importing countries. No city in the world receives

so much cotton as Liverpool. England's high rank as a cotton textile

producer accounts for this, although a great deal of cotton received in

Liverpool is reshipped in smaller quantities to various parts of Europe and

elsewhere. American spinners frequently buy Egyptian or East Indian cotton

in Liverpool. A few miles inland from Liverpool is another great cotton

market, Manchester, the very heart of the cotton textiles manufacturing

district of England. Cotton received here is used in the immediate vicinity.

Cotton import in India is given in table 2.1.6:

Table 2.1.6

COTTON IMPORTS IN INDIA

Year Quantity (in lakh bales of

170 kgs.)

Value

(`/Crores)

1996-97 0.30 56.42

1997-98 4.13 497.93

1998-99 7.87 772.64

1999-00 22.01 1967.92

2000-01 22.13 2029.18

2001-02 25.26 2150.01

2002-03 17.67 1789.92

2003-04 7.21 880.10

2004-05 12.17 1338.04

2005-06 5.00 695.77

2006-07 5.53 752.29

2007-08 6.38 978.54

2008-09 10.00 1377.80

2009-10 7.00 1195.64

2010-11 5.00 N.A.

2011-12 6.00 N.A.

Note: Value figures are estimated

NA : Not Available (A): Anticipated

Source: Cotton Advisory Board for Quantity figures

42

REVIVAL OF GINNING/SPINNING MILLS

Government has not received any representation regarding

closure of ginning factories, spinning mills or handloom units due to

recession in international market. However CITI has represented regarding

a slowdown in the Textiles industry due to demand contraction in cotton yarn

resulting in increased yarn stocks in the country.

Government of India, under Textile Workers Rehabilitation Fund

Scheme (TWRFS) provides interim relief to the textile workers rendered

unemployed as a consequence for permanent closure of any particular

portion or entire textile unit in the private sector. Assistance under the

Scheme is payable to eligible workers for the purpose of enabling them to

settle in another employment5. Table 2.1.7 show the details of funds

allocated and released – TWRFS.

Table 2.1.7

DETAILS OF FUNDS ALLOCATED AND RELEASED -TWRFS

Year Funds allocation Funds released

2009-10 ` 25 crore ` 24.45 crore

2010-11 ` 12.28 crore ` 12.28 crore

Source: Ministry of state for textiles

COTTON - SPINNING

Spinning machines have a metal spike called a spindle which the

thread winds around. The spindle is turned by attaching it with a pulley to a

larger wheel (or several wheels) which is rotated with one hand. One

complete turn of the large wheel makes the spindle turn many times, just like

gears on a bike. Each spinning cycle takes only a few seconds and involves

turning the wheel clockwise, anticlockwise and then clockwise again. This

cycle pulls fibers from the cylinder in the left hand, twisting the thread and

then winding the finished thread onto the spindle. After spinning, threads are

dyed and treated with chemicals to prevent shrinkage or creasing, before

weaving into fabrics.

43

The country’s cotton production has been steadily on the rise with

better farm practices. The average yield has increased to 500 kg per

hectare. From a level of importers of cotton, India has become an exporter of

cotton earning a name in the international market. Presently India is the

second largest cotton producer in the world next to US and is about to

overtake the US as the number one in the next couple of years. It is the

result of various factors. Primarily, because of rising cultivations of Bt.cotton

(Bacillus thuringnsis) and reduction of farmers input costs, while the yield as

well as quality are substantially much larger compared to traditional varieties.

In view of this development, the cotton cultivation acreage has been steadily

going up in India. The farmers have become more knowledgeable to follow

scientific methods to cultivate high yielding long staple cotton varieties.

Besides, individual mills are also simultaneously taking steps to

improve the cotton production along with Technology Mission on Cotton

(TCM), the cotton development research Associations of organizations

(CITI), South Indian Textiles Mills Association (SIMA) and Kerala State

Textile Corporation (KSTC). The resultant factor is that the quality and

quantity of raw material supply has substantially improved in the country.

Due to globalization of our economy, the consciousness of quality inputs and

pricing have become competitive to the international standards and prices.

The Indian textile industry is one of the largest in the world with a

massive raw material and textile-manufacturing base. Indian economy is

largely dependent on the textile manufacturing and trade in addition to other

major industries. About 27 percent of the exchange earning are on account

of export of textiles and clothing alone. In India, organized textile mill sector

has increased from 1787 in 2003-04 to 1789 in 2004-05.

The cotton textile industry, one of the oldest and major consumer

industries in India, has assumed national importance by virtue of size,

investment, output and employment. The industry produces a wide range of

fabrics to suit specific needs of consumers. Further, the cotton textile

industry occupies a pre eminent place in the Indian economy by contributing

a major share to the countries industrial production and providing cloth to its

44

millions. The industry also serves by providing direct employment to

60,00,000 workers in several of its related activities. India is one of the

largest textile producing countries in the world. The share of the industry in

the export basket of India is around 20 percent. However, textile industry is

the vast developing sector and when the competitions are exorbitant,

especially in its design and quality, we have to adopt modern technology

management machine so as to compete with other countries in the

international market6.

SPINNING AND TEXTILE INDUSTRY IN TAMILNADU

The Textile Mills are the backbone of Tamil Nadu’s industrial

development and are providing massive employment in the State,

predominantly spinning oriented. The State textile industry has a significant

presence in the national economy also. There are 3069 large, medium and

small spinning mills in India, of which, 1889 are located in Tamilnadu. The

spinning mills in the State comprise 18 Cooperative Spinning Mills

(5 functioning), 17 National Textile Corporation Mills (7 functioning) and 1854

Private Mills (including 23 Composite Mills). Those spinning mills provide

employment for around 2.40 lakh persons. The capacity of the spinning mills

in the State is around 18.92 million spindles. The State produces about 1612

million kg. of spun yarn per year and this is about 40 percent of the spun

yarn produced per year in the entire nation7.

At present, Tamil Nadu, despite its significant presence in the

industry, is not actively associated in the policy making processes of the

Government of India affecting the industry. It is felt that in all such matters,

the State should actively be involved in the decision making process.

According to the Annual Survey of Industries (92-93), Tamil Nadu was

the 3rd largest industrial state in the country. The gross output of its

industrial sector was `37,986 crores, accounting for 10.3 percent of the

national output. Its net value added to `7,303 crores was also 10.3 percent of

the national figure. Cotton textiles was prominent among the industry groups

that contributed to this ranking. In terms of gross output value, cotton textiles

45

increased from 18.8 percent of the national share (ranked 2) in 1982-83 to

32.2 percent (ranked 1) in 1992-93. In terms of net value added, the

corresponding figures were 18.4 percent (ranked 2) and 37.4 percent

(ranked 1). Other textile products accounted for 20.3 percent of the national

gross output value (ranked 2) in 1992-93 and 22.3 percent of that year's net

value added (ranked 2). However, in 1995-96, the textile sector as a whole in

Tamil Nadu registered a disturbing negative growth rate.

When we look at Tamil Nadu's Textile Sector in 94-95, the total yarn

production in the State was 695 million kgs, fully 33.3 percent of the

country's production. Within this, the production of cotton yarn was 611

million kgs, being 38.5 percent of the country's output and blended and

manmade fibres accounted for 84 million kgs, 16.7 percent of the national

output. This was the output of 617 textile mills (44.2 percent of the country),

comprising 595 spinning mills (52.7 percent) and 22 composite mills (8.2

percent) accounting for a total of 98.7 lakh spindles (32.5 percent). Included

in the spinning mills are 18 co-operative spinning mills accounting for 4.69

lakh spindles and 34 million kgs of yarn, a quantity sufficient to meet roughly

half the hank yarn requirement of the State.

In 1994-95, Tamil Nadu also produced 187 million metres of cloth, 11

percent of the national production, of which cotton accounted for 93 million

metres (8.4 percent) and blended varieties accounted for 94 million metre

(15.8 percent). This was the output of 7.7 lakh looms, being 5.1 percent of

the country's loomage. Of this, 4.3lakh looms were in the handloom sector

and 3.4 lakh in the powerloom and composite mill sectors.

Need for a State Textile Policy, the country's textile policy was last

specified through the Textile Policy Statement of June 1985. Prior to this, the

development of the textile industry was guided by policy announcements in

March 1981 and August 1978. The stated objective of the textile policy of

1985 was an increase in production of cloth of acceptable quality at

reasonable prices to meet the clothing requirements of growing population.

In pursuit of this objective, the employment and export potential of the

industry were also to be kept in view.

46

The national policy is a broad statement and covers every aspect of

the textile industry. However, in order to cater to the specific needs of

individual states, there is a felt need for a State Level Policy. The textile

industry continues to play a vital socio-economic role in Tamil Nadu. Hence,

the need for a dynamic, growth oriented policy is all the more important.

The objective of the State Textile Policy will be to produce textiles to

cater satisfactorily to the quantity, quality and price requirements of both

domestic and international markets, keeping in view the industry's potential

for employment8.

Until last year, spinning mills in Tamil Nadu were running round the

clock and were busy expanding their operational capacities. Textile mill in

Coimbatore districts plays a predominant part of the industry in South India.

Presently, a major part of the spinning mills which involves in manufacturing

yarn remains idle. Several units are closing down, putting the jobs of

thousands of the workers into jeopardy and many others have not received

their wages for months. 392 mills were closed during the previous year

leaving more than 2 lakh workers jobless. Saddled with recession, the

industry is tumbling down facing a steep fall in the export orders, especially

from the South East Asian markets. The economic liberalization, which was

believed to be the pivot of Coimbatore spinning mills’ success, is now being

blamed as a reason for the industrial turmoil.

The corresponding period during the previous year was a busy period

for the spinning mills in South India. The spindle capacity was doubled with

40 percent additional capacity. All these efforts have gone with the wind, with

the advent of global recession and power crisis. The fiscal year 2008-09 is

one of the most difficult periods in the history of textile mills in South India.

Cotton yarn production is already down by 20 percent during the last fiscal

year. Production which was 4003.44 million kg during 2007-08 dropped to

3239.17 million kg during the last year. Profile of textile industry in Tamil

Nadu is given in table 2.1.8:

47

Table 2.1.8

PROFILE OF TEXTILE INDUSTRY IN TAMIL NADU

ITEM ALL INDIA TAMILNADU

SPINNING SECTOR

No. of Spinning Mills 3069 1889

Workers (in lakh) 8.94 2.40

Spindles (in Million) 39.27 18.92

POWERLOOM SECTOR

Powerlooms (in lakhs) 19.03 3.66

Workers (in lakhs) 47.57 9.14

HANDLOOM SECTOR

Handlooms (in lakhs) 34.86 4.13

Weavers (in lakhs) 65.50 6.08

Handloom Cloth Production(Bn. Sq. Mt)

6.00 0.70

Value(` in Crore) 18000 1700

OTHER SECTOR

Power processing Units 2510 985

Hand Processing Units 10397 2614

Knitwear and Garment units 8000 4000

Source: Tamil Nadu - Industry Profile

The Textile Industry of Tamil Nadu has a significant presence in the

National and State economy. It is the forerunner in Industrial development

and in providing massive employment in the State. Handloom, Powerloom,

Spinning, Processing, Garment and Hosiery are the various sectors of the

Textile Industry in Tamil Nadu. It is the largest economic activity next only to

Agriculture in providing direct and indirect employment. Handloom Sector

occupies a place of pride in preserving the country's heritage and culture

and plays a vital role in the economy of the country. It has a long tradition

par excellence in its craftsmanship. The Powerloom Sector in Tamil Nadu

has also been playing an important role in meeting the clothing needs of the

people. The Powerloom Sector in Tamil Nadu is next only to Maharashtra in

terms of number of looms. The Textile Sector in Tamil Nadu is predominantly

in the private sector, spinning oriented and labour-intensive because of the

48

preponderance of the decentralized sector in most of the segments of the

industry. The Textile Industry has a very important role to play in the

industrial field with regard to employment potential, overall economic and

commercial activities. This Industry enables the Central and State

Governments to earn substantial revenue besides foreign exchange through

exports9.

CHALLENGES FOR THE COTTON SPINNING INDUSTRY

Raw cotton and cotton yarn prices have historically moved in tandem

raw cotton prices being the base and indicating corresponding movement in

prices for cotton yarn. The prices of both the commodities have been stable

over the past several years apart from inhibiting seasonal volatility on

account of cyclical conditions of the industry. However in 2010, there was a

massive crop failure in China and Pakistan mainly on account of floods. In

Pakistan alone, reports suggested close to 1/5th of the total crop as

destroyed by floods. Thus, in the second of half of 2010-11, due to supply

constraints, strong international demand propelled the international prices of

cotton and cotton yarn to new heights in a very short period of time.

Prices of raw cotton, which were `32000/candy in August 2010, rose

to `44000/candy in November 2010 and `60,000/candy in March 2011. At the

same time, Indian cotton harvest increased albeit marginally on account of

adequate rainfall and increase in area under acreage. India produced 29.5

million bales of cotton in 2010 as against 29 million bales in 2009 while

increasing the area under acreage from 94.06 lakh acres to 103.10 lakh

acres in the same period. Thus, weak global supply and stable domestic

output presented a good opportunity to the Indian cotton exporters as foreign

importers looked towards India to procure their requirements of cotton and

cotton yarn.

During October – December 2010, there emerged a deficit situation of

cotton and cotton yarn in domestic market as manufacturers chased highly

remunerative international markets. Reacting to this deficit situation, the

Government of India imposed a ban on the exports of cotton yarn between

49

January-March in 2011. Though higher realizations could be made in the

international market, exporters were unable to do so. Simultaneously,

ongoing production activities led to piling up of finished goods inventory for

majority of the cotton and cotton yarn manufacturing units in India. Industry

estimates quote the finished goods inventory of 500 to 550 million kgs as of

April 2011 in the Indian market which were produced at a higher input cost

when cotton prices were at their peak in Jan – March2011. This led to an

adverse industry situation wherein there is currently an excess supply of

finished stock manufactured at a higher input cost while customers are

waiting for prices to fall further. The average inventory as on March 31,

2011, of leading industry players, was approximately 4 months. The prices of

raw cotton have since corrected by approximately 25 percent from their peak

levels to `130/kg in May 2011.

Rising cotton imports from China and a capital on Indian cotton

exports which were the main factors driving up global cotton prices are

already experiencing a reversal and this is expected to continue with the

onset of monsoon and excess supply of finished stock in the Indian market in

2012. In the remaining months of the season, domestic cotton prices are

likely to soften, as exporters are in the process of exhausting their quota of

permissible exports and global cotton prices are also projected to decline.

Unless the quota of permissible exports is increased, cotton prices are

expected to fall further. Yarn prices have already dropped from a peak of

`280 a kg for the benchmark variety to `225 a kg in May 2011. The

Government had resumed yarn exports from April 2011, but removed export

incentives like duty drawback and Duty Entitled Pass Book scheme (DEPB)

since April 2010. This discouraged exports, as the prices in the international

markets too have also come down from its peak levels in February – March

2011 on account of tightening of export margins, reduction in Chinese

imports and an expectation of higher yield of cotton crop in 2011-12.

Moreover, resistance from domestic fabric producers would also act as a

constraining factor for hike in the prices of the yarn. Silver lining to the above

situation is the fact that the Government of India has increased the allocated

quota for the export of cotton from the present 5.5 million bales to 6.5 million

50

bales for 2012. Volatile cotton prices, fluctuating currency markets and

global economic uncertainty have raised concerns about textile exports in

the past. Currently, the scenario is that of manufacturers curtailing

production and offloading existing inventory to stabilize prices. This will lead

to decline in capacity utilization levels for the industry. Apart from integrated

spinning players who can to some extent mitigate the cost of high cost

inventory to their fabric divisions, non-integrated spinning mills are expected

to report subdued financial performance in first half of the financial year 2012

as compared to financial year 2011.

Overall, spinning companies in India are expected to feel the effect of

piling up of high cost inventory and falling prices of cotton and cotton yarn in

first half of the financial year 2012. They would have procured large

inventory (3-4 months of raw material stock) for their cotton requirements for

2012 in last quarter of financial year 2011 when cotton prices had peaked

and this would have pushed up their procurement cost. Thus, overall growth

prospects for spinning companies are expected to be constrained on

account of subdued prices and decline in capacity utilization levels. CARE

Research expects the operating margins of spinning companies to decline

by around 250 to 300 bps in 2011-1210.

51

Cotton / Man made fibre mills and closure position is given in table 2.1.9:

Table 2.1.9 COTTON / MAN MADE FIBRE MILLS AND CLOSURE POSITION

As on No. of Mills No. of mills closed

Spinning Spinning

31.03.02 1579 295

31.03.03 1599 350

31.03.04 1564 374

31.03.05 1566 379

31.03.06 1570 387

31.03.07 1608 381

31.03.08 1597 318

31.03.09 1653 340

31.03.10 1673 365

31.12.10 1766 471

31.01.2011* 1766 472

28.01.2011* 1766 472

* Figures are repeated since information from regional office under compilation.

Source: www.txcindia.com

SOME OF THE POPULAR COMPANIES ENGAGED IN THE INDIAN SPINNING INDUSTRY ARE LISTED BELOW

Bhilwara Spinners Ltd. (LNG Group) - polyester, viscose, wool-blended

fabrics and high-end products like lycra and linen. BSL Suitings and

Mayur Suitings are the two brands under Bhilwara Spinners Ltd.

Nitin Spinners Ltd. - manufactures single and multi-fold yarns in the

range from Ne 4 to Ne 40 appropriate for various applications such as

Knitted Fabrics, Woven Fabrics, Terry Towels, Denims, Furnishing

Fabrics, carpets and other Industrial Fabrics.

Sangam (India) Ltd. (Sangam Group of Companies) - Largest producer of

dyed yarn in India with a capacity of 64032 spindles in one location.

Ajay Group of Industries - Manufacturer and seller of polyester viscose,

polyester woolen and uniform fabrics.

The Spinning Industry in India is on set to hit the global market with other

fabrics as well like the cotton textiles with its enthusiasm and consistency in

52

work. It has already reached a phenomenal status in India by beating the

obstacles that caused a downfall since past few years and is now on its way

to cover a wider area in the spinning sector11.

The Indian textile industry is one the largest and oldest sectors in the

country and among the most important in the economy in terms of output,

investment and employment. The sector employs nearly 35 million people

and after agriculture, is the second-highest employer in the country. The

Indian Spinning Industry is an integral part of the Indian Textile Industry.

India claims to be the second largest manufacturer as well as provider of

cotton yarn and textiles in the world

India holds around 25 percent share in the cotton yarn industry across

the globe

India contributes to around 12 percent of the world's production of cotton

yarn and textiles

India covers 61 percent of the international textile market

In terms of spindleage, the Indian textile industry is ranked second, after

China, and accounts for 23 percent of the world’s spindle capacity12.

Spinning mills in India have been producing a large number of counts

and varieties of yarns. Many mills, besides producing more number of

counts, very often change their product-mix. No doubt, introduction of a new

count would bring-in some immediate savings but such gain should be

looked from a long-term point of view.

In view of the tough competition and narrow profit margin for the

conventional varieties of yarns such as carded, combed and hosiery, some

mills have been manufacturing special types of yarns such as compact,

fancy, chemical processed, organic and core spun yarns.

The counts and varieties of yarns manufactured by a spinning mill

depend on a number of factors such as spindleage, availability of adequate

preparatory and post-spinning machinery, profit margin, market demand and

marketing capability13.