chapter 9 - test bank cost accounting

DESCRIPTION

Chapter 9 - Test BankTRANSCRIPT

Chapter 09

Inventories: Additional Issues

True / False Questions

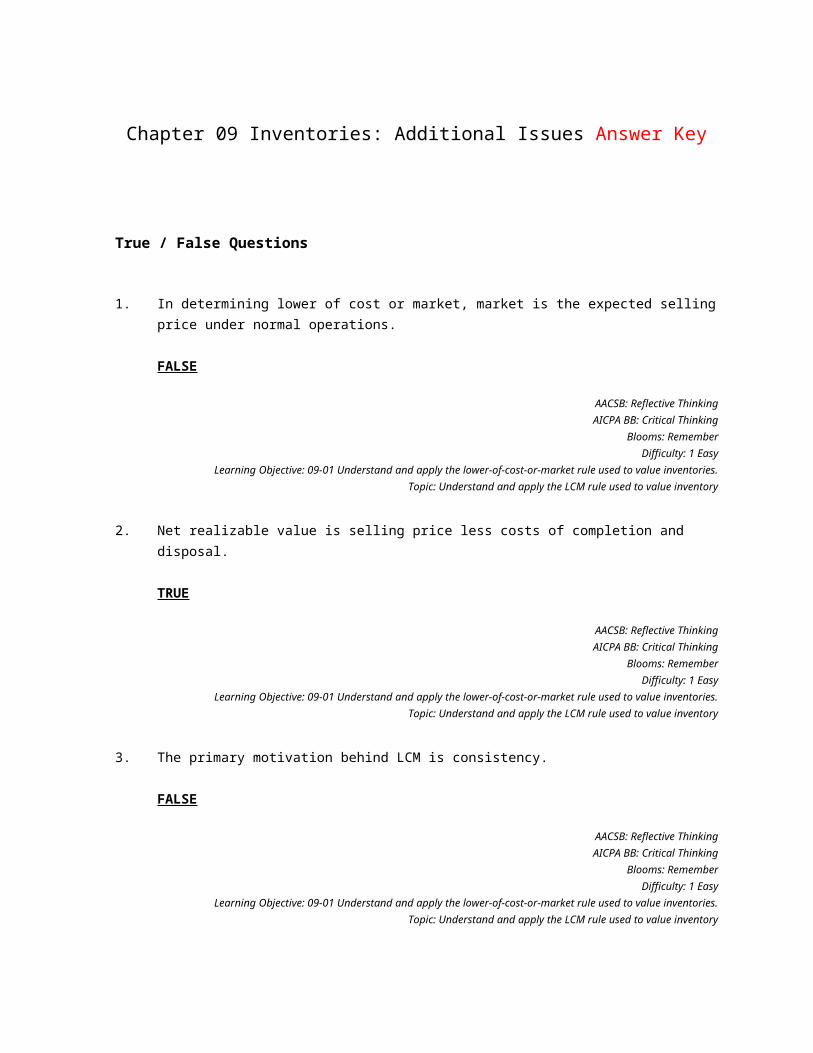

1. In determining lower of cost or market, market is the expected selling price under normal operations. True False

2. Net realizable value is selling price less costs of completion and disposal.

True False

3. The primary motivation behind LCM is consistency.

True False

4. The purpose of ceilings and floors in LCM is to prevent profit distortion.

True False

5. Losses on reduction to LCM may be charged to either cost of goods sold or to a

current loss account. True False

6. Inventory written down due to LCM may be written back up if market values increase.

True False

7. Under the LIFO retail method, the current period cost-to-retail percentage includes

both net markdowns and net markups. True False

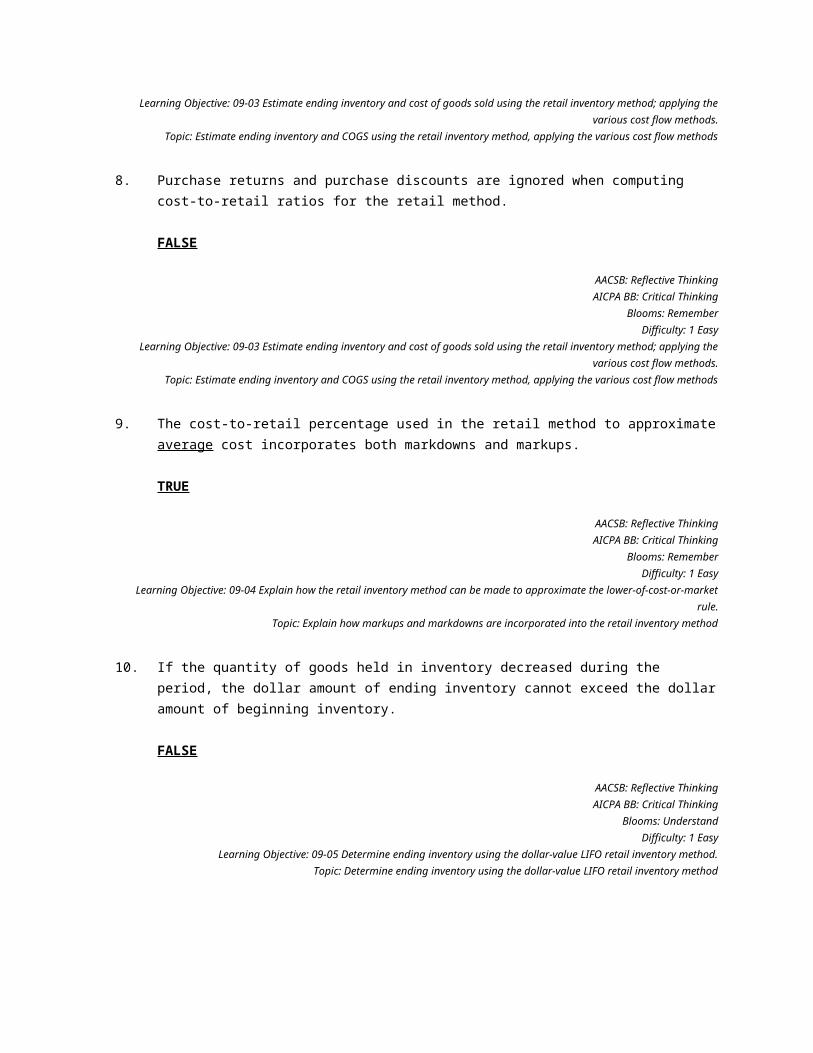

8. Purchase returns and purchase discounts are ignored when computing cost-to-retail

ratios for the retail method. True False

9. The cost-to-retail percentage used in the retail method to approximate average cost incorporates both markdowns and markups. True False

10. If the quantity of goods held in inventory decreased during the period, the dollar

amount of ending inventory cannot exceed the dollar amount of beginning inventory. True False

11. When changing from the average cost method to FIFO, the current year's income

includes the cumulative after-tax difference that would have resulted if the company had used FIFO in all prior years. True False

12. A change from LIFO to any other inventory method is accounted for retrospectively.

True False

13. For a purchase commitment contained within a single fiscal year, if the market price is

less than the contract price, the purchase is recorded at the contract price. True False

14. For a purchase commitment extending beyond the current fiscal year, if the market

price on the purchase date declines from the previous year-end price, the purchase is recorded at the market price. True False

15. International Financial Reporting Standards allow the reversal of an inventory write-

down. True False

Multiple Choice Questions

16. In applying LCM, market cannot be:

A. Less than net realizable value.

B. Greater than the normal profit.

C. Less than the normal profit margin.

D. Greater than net realizable value.

17. In applying LCM, market cannot be:

A. Less than net realizable value minus a normal profit margin.

B. Net realizable value less reasonable completion and disposal costs.

C. Greater than net realizable value reduced by an allowance for normal profit margin.

D. Less than cost.

18. Masterlink Co., in applying the lower of cost or market method, reports its inventory at

net realizable value. Which of the following statements is correct?

A. Option a

B. Option b

C. Option c

D. Option d

19. An argument against the use of LCM is its lack of:

A. Relevance.

B. Reliability.

C. Consistency.

D. Objectivity.

20. Montana Co. has determined its year-end inventory on a FIFO basis to be $600,000.

Information pertaining to that inventory is as follows:

What should be the carrying value of Montana's inventory?

A. $600,000.

B. $520,000.

C. $590,000.

D. $510,000.

Data related to the inventories of Costco Medical Supply are presented below:

21. In applying the LCM rule, the inventory of surgical equipment would be valued at:

A. $230.

B. $240.

C. $170.

D. $152.

22. In applying the LCM rule, the inventory of surgical supplies would be valued at:

A. $115.

B. $90.

C. $80.

D. $69.

23. In applying the LCM rule, the inventory of rehab equipment would be valued at:

A. $315.

B. $247.

C. $150.

D. $235.

24. In applying the LCM rule, the inventory of rehab supplies would be valued at:

A. $122.

B. $158.

C. $162.

D. $155.

Data related to the inventories of Alpine Ski Equipment and Supplies is presented below:

25. In applying the LCM rule, the inventory of skis would be valued at:

A. $162,000.

B. $128,000.

C. $120,000.

D. $126,000.

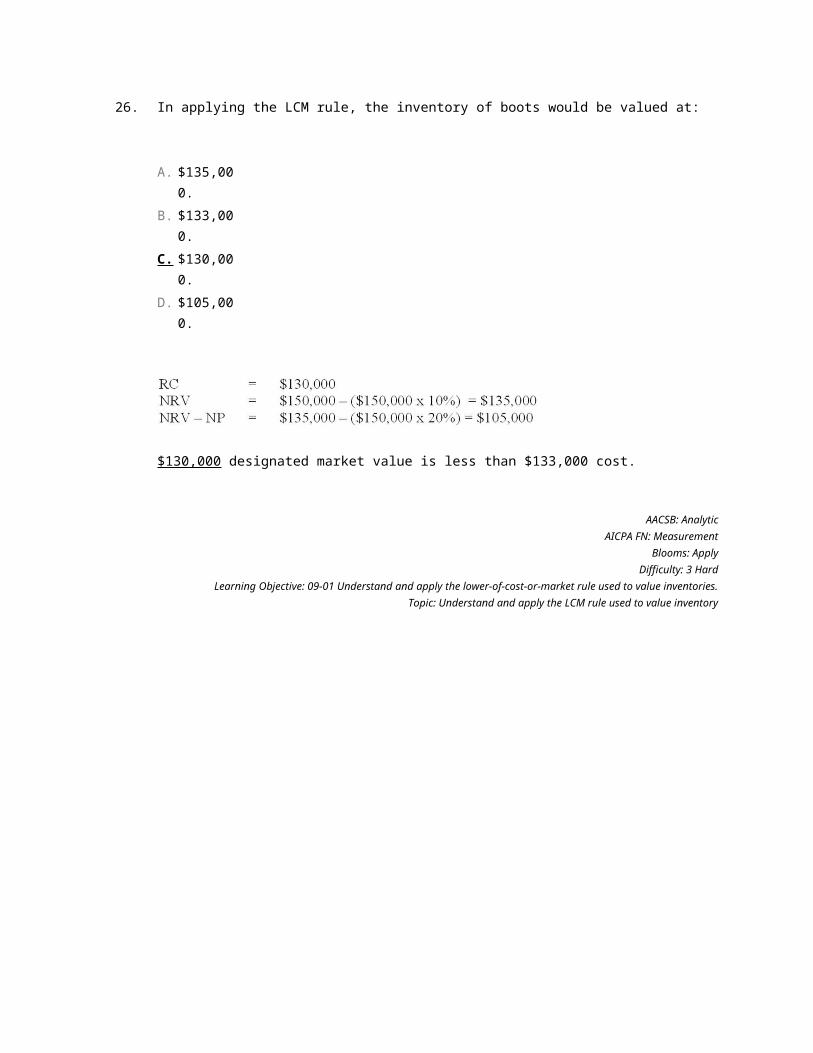

26. In applying the LCM rule, the inventory of boots would be valued at:

A. $135,000.

B. $133,000.

C. $130,000.

D. $105,000.

27. In applying the LCM rule, the inventory of apparel would be valued at:

A. $108,000.

B. $90,000.

C. $110,000.

D. $115,000.

28. In applying the LCM rule, the inventory of supplies would be valued at:

A. $45,000.

B. $54,000.

C. $41,000.

D. $42,000.

29. When using the gross profit method to estimate ending inventory, it is not necessary

to know:

A. Beginning inventory.

B. Net purchases.

C. Cost of goods sold.

D. Net sales.

30. On July 8, a fire destroyed the entire merchandise inventory on hand of Larrenaga Wholesale Corporation. The following information is available:

What is the estimated inventory on July 8 immediately prior to the fire?

A. $192,000.

B. $490,000.

C. $510,000.

D. $280,000.

31. California Inc., through no fault of its own, lost an entire plant due to an earthquake

on May 1, 2013. In preparing its insurance claim on the inventory loss, the company developed the following data: Inventory January 1, 2013, $300,000; sales and purchases from January 1, 2013, to May 1, 2013, $1,300,000 and $875,000, respectively. California consistently reports a 40% gross profit. The estimated inventory on May 1, 2013, is:

A. $302,500.

B. $360,000.

C. $395,000.

D. $455,000.

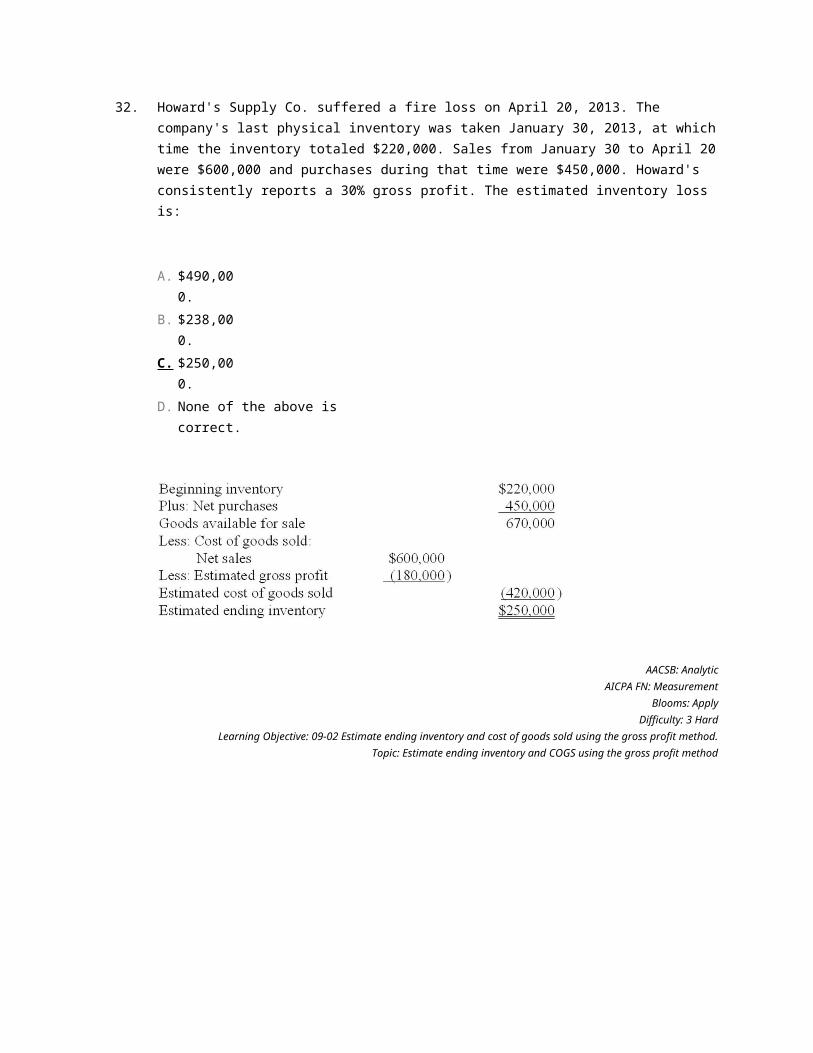

32. Howard's Supply Co. suffered a fire loss on April 20, 2013. The company's last physical inventory was taken January 30, 2013, at which time the inventory totaled $220,000. Sales from January 30 to April 20 were $600,000 and purchases during that time were $450,000. Howard's consistently reports a 30% gross profit. The estimated inventory loss is:

A. $490,000.

B. $238,000.

C. $250,000.

D. None of the above is correct.

33. Coastal Shores Inc. (CSI) was destroyed by Hurricane Fred on August 5, 2013. At

January 1, CSI reported an inventory of $170,000. Sales from January 1, 2013, to August 5, 2013, totaled $480,000 and purchases totaled $195,000 during that time. CSI consistently marks up its products 60% over cost to arrive at a selling price. The estimated inventory loss due to Hurricane Fred would be:

A. $131,175.

B. $65,000.

C. $17,143.

D. None of the above is correct.

34. Under the conventional retail method, the denominator in the cost-to-retail

percentage includes:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

35. Under the LIFO retail method, the denominator in the cost-to-retail percentage includes:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

36. Under the retail method, the denominator in the cost-to-retail percentage does not

include:

A. Purchases.

B. Purchase returns.

C. Abnormal shortages.

D. Freight-in.

37. Under the retail inventory method:

A. A company measures inventory on its balance sheet by converting retail prices to cost.

B. A company measures inventory on its balance sheet at current selling prices.

C. A company measures inventory on its balance sheet on a LIFO basis.

D. None of the above is correct.

38. Under the conventional retail method, which of the following are not included in the denominator of the current period cost-to-retail conversion percentage?

A. Purchase returns.

B. Net markups.

C. Purchases.

D. Net markdowns.

39. Under the LIFO retail method, which of the following are not included in the

denominator of the cost-to-retail conversion percentage?

A. Freight-in.

B. Purchase returns.

C. Purchases.

D. Net markdowns.

40. Under the retail method, in determining the cost-to-retail percentage for the current

year:

A. Net markups are included.

B. Net markdowns are excluded.

C. Net sales are included.

D. All of the above are correct.

41. Fad City sells novel clothes that are subject to a great deal of price volatility. A recent item that cost $20 was marked up $12, marked down for a sale by $6 and then had a markdown cancellation of $3. The latest selling price is:

A. $23.

B. $26.

C. $29.

D. $35.

Harvey's Junk Jewelry started business January 1, 2013, and uses the LIFO retail method to estimate ending inventory. Listed below is data accumulated for the year ended December 31, 2013:

42. The numerator for the current period's cost-to-retail percentage is:

A. $64,800.

B. $48,100.

C. $47,700.

D. $49,800.

43. The denominator for the current period's cost-to-retail percentage is:

A. $96,300.

B. $73,300.

C. $101,000.

D. $81,500.

44. The estimated ending inventory at retail is:

A. $27,300.

B. $25,000.

C. $26,600.

D. $26,400.

45. To the nearest thousand, the estimated ending inventory at cost is:

A. $16,000.

B. $15,000.

C. $13,000.

D. $19,000.

46. Lacy's Linen Mart uses the retail method to estimate inventories. Data for the first six months of 2013 include: beginning inventory at cost and retail were $60,000 and $120,000, net purchases at cost and retail were $312,000 and $480,000, and sales during the first six months totaled $490,000. The estimated inventory at June 30, 2013, would be:

A. $68,200.

B. $55,000.

C. $71,500.

D. $63,250.

47. Hawkeye Auto Parts uses the retail method to estimate inventories. Data for the first

six months of 2013 include: beginning inventory at cost and retail were $55,000 and $100,000, net purchases at cost and retail were $785,000 and $1,300,000, and sales during the first six months totaled $800,000. The estimated inventory at June 30, 2013, would be:

A. $330,000.

B. $360,000.

C. $362,300.

D. None of the above is correct.

Marilee's Electronics uses a periodic inventory system and the average cost retail method to estimate ending inventory and cost of goods sold. The following data is available from the company records for the month of June 2013:

48. The average cost-to-retail percentage is:

A. 52.2%.

B. 61.5%.

C. 56.8%

D. 55%.

49. To the nearest thousand, estimated ending inventory is:

A. $55,000.

B. $52,000.

C. $57,000.

D. None of the above is correct.

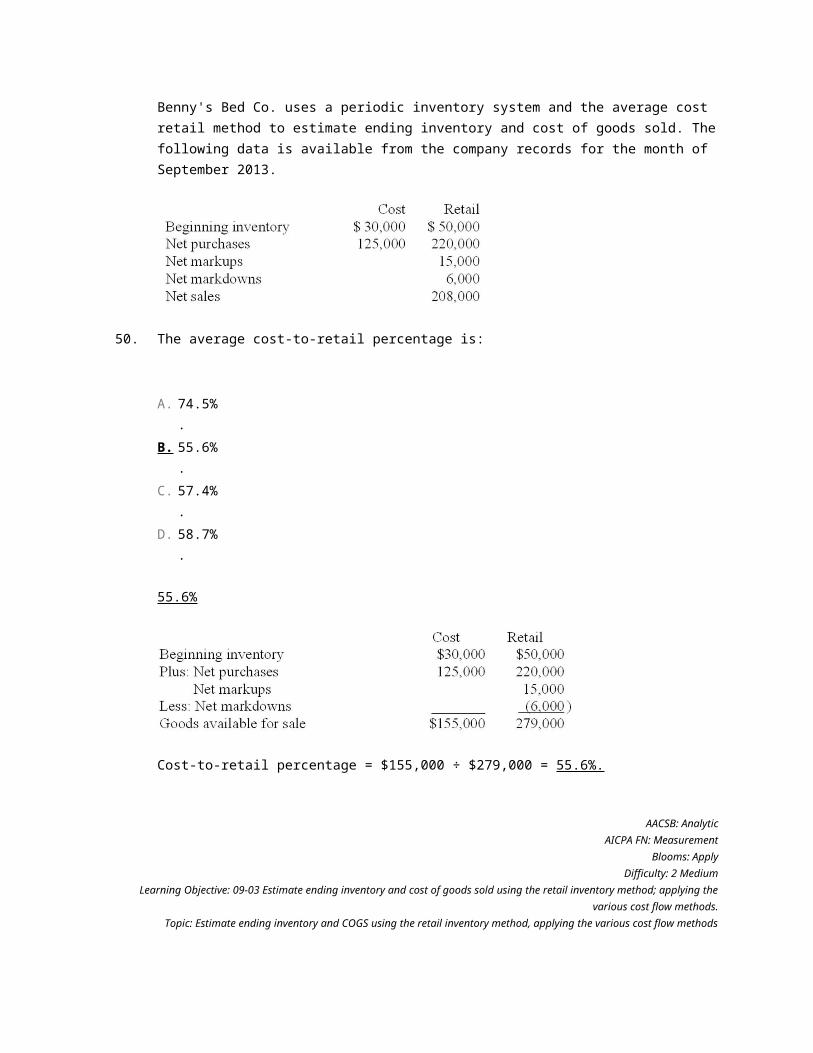

Benny's Bed Co. uses a periodic inventory system and the average cost retail method to estimate ending inventory and cost of goods sold. The following data is available from the company records for the month of September 2013.

50. The average cost-to-retail percentage is:

A. 74.5%.

B. 55.6%.

C. 57.4%.

D. 58.7%.

51. To the nearest thousand, estimated ending inventory is:

A. $41,000.

B. $37,000.

C. $51,000.

D. None of the above is correct.

Data below for the year ended December 31, 2013, relates to Houdini Inc. Houdini started business January 1, 2013, and uses the LIFO retail method to estimate ending inventory.

52. Current period cost-to-retail percentage is:

A. 70.0%.

B. 68.7%.

C. 63.6%.

D. 63.5%.

53. Estimated ending inventory at retail is:

A. $65,000.

B. $169,600.

C. $25,000.

D. $129,000.

54. Estimated ending inventory at cost is:

A. $90,720.

B. $83,500.

C. $91,600.

D. None of the above is correct.

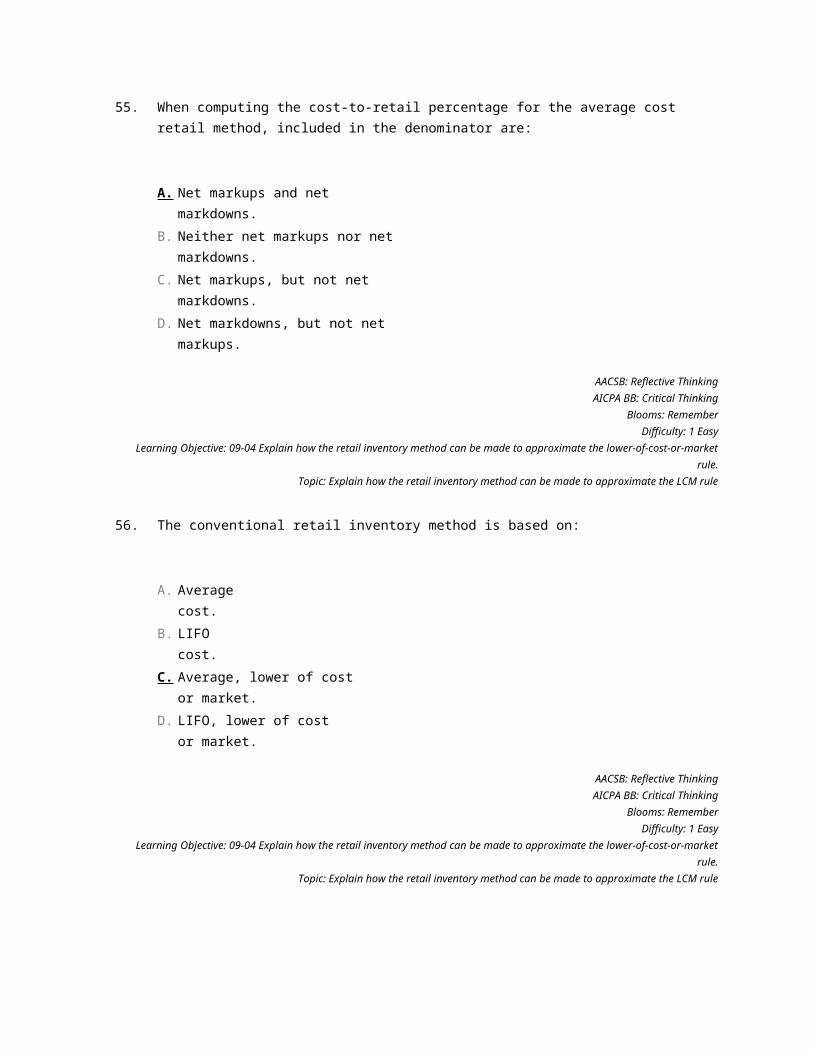

55. When computing the cost-to-retail percentage for the average cost retail method,

included in the denominator are:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

56. The conventional retail inventory method is based on:

A. Average cost.

B. LIFO cost.

C. Average, lower of cost or market.

D. LIFO, lower of cost or market.

57. Cloverdale, Inc., uses the conventional retail inventory method to account for inventory. The following information relates to current year's operations:

What amount should be reported as cost of goods sold for the year?

A. $273,600.

B. $272,861.

C. $275,000.

D. None of the above.

Willie Nelson's Boots uses the conventional retail method to estimate ending inventory. Cost data for the most recent quarter is shown below:

58. The conventional cost-to-retail percentage (rounded) is:

A. 82.6%.

B. 66.7%.

C. 71.9%.

D. 75.5%.

59. To the nearest thousand, estimated ending inventory using the conventional retail method is:

A. $37,000.

B. $32,000.

C. $34,000.

D. $30,000.

Clarabell Inc. uses the conventional retail method to estimate ending inventory. Cost data for the most recent quarter is shown below:

60. The conventional cost-to-retail percentage (rounded) is:

A. 54.9%.

B. 58.9%.

C. 53.6%.

D. 70.6%.

61. To the nearest thousand, estimated ending inventory using the conventional retail method is:

A. $163,000.

B. $124,000.

C. $127,000.

D. $136,000.

62. Using the dollar-value LIFO retail method for inventory:

A. Is the same as dollar-value LIFO, except that the inventory is measured at retail, rather than at cost.

B. Combines retail LIFO accounting with dollar-value LIFO accounting.

C. Allows companies to report inventory on the balance sheet at retail prices.

D. All of the above are correct.

63. The first step, when using dollar-value LIFO retail method for inventory, is to:

A. Determine the estimated ending inventory at current year retail prices.

B. Determine the estimated cost of goods sold for the current year.

C. Determine the cost-to-retail percentage for the current year transactions.

D. Price index adjust the LIFO inventory layers.

64. The second step, when using dollar-value LIFO retail method for inventory, is to determine the estimated:

A. Ending inventory at current year retail prices.

B. Cost of goods sold for the current year.

C. Ending inventory at cost.

D. Ending inventory at base year retail prices.

65. Under the dollar-value LIFO retail method, to determine if the increase in the value of

inventory was due to an increase in quantities:

A. Compare beginning and ending inventory amounts at current year prices.

B. Compare beginning and ending inventory amounts after adjusting both amounts to the average price level for the year.

C. Inflate beginning inventory amount to end of year prices and compare to ending inventory amount.

D. Deflate the ending inventory amount to beginning of year prices and compare to the beginning inventory amount.

66. Under the dollar-value LIFO retail method, to determine the value of a LIFO layer:

A. Divide the LIFO layer by the layer-year price index and multiply by the layer-year cost-to-retail percentage.

B. Multiply the LIFO layer by the base year price index and the current year cost-to-retail percentage.

C. Multiply the LIFO layer by the layer-year price index and by the layer-year cost-to-retail percentage.

D. Divide the LIFO layer by the layer-year cost-to-retail percentage and multiply by the layer-year price index.

67. Portman Inc. uses the conventional retail inventory method. Expressed in millions of dollars, information about Portman's 2013 inventory account is expressed in the table below:

What is the value of Portman's inventory at 12/31/13?

A. $150 million.

B. $252 million.

C. $300 million.

D. None of the above is correct.

68. Harlequin Co. has used the dollar-value LIFO retail method since it began operations

in early 2012 (its base year). Its beginning inventory for 2013 was $36,000 at cost and $72,000 at retail prices. At the end of 2013, it computed its estimated ending inventory at retail to be $120,000. Assuming its cost-to-retail percentage for 2013 transactions was 60%, what is the inventory balance that Harlequin Co. would report in its 12/31/13 balance sheet?

A. $64,800.

B. $72,000.

C. $120,000.

D. It can't be determined with the given information.

69. Retrospective treatment of prior years' financial statements is required when there is a change from:

A. Average cost to FIFO.

B. FIFO to average cost.

C. LIFO to average cost.

D. All of the above.

70. Prunedale Co. uses a periodic inventory system. Beginning inventory on January 1 was

overstated by $32,000, and its ending inventory on December 31 was understated by $62,000. These errors were not discovered until the next year. As a result, Prunedale's cost of goods sold for this year was:

A. Overstated by $94,000.

B. Overstated by $30,000.

C. Understated by $94,000.

D. Understated by $30,000.

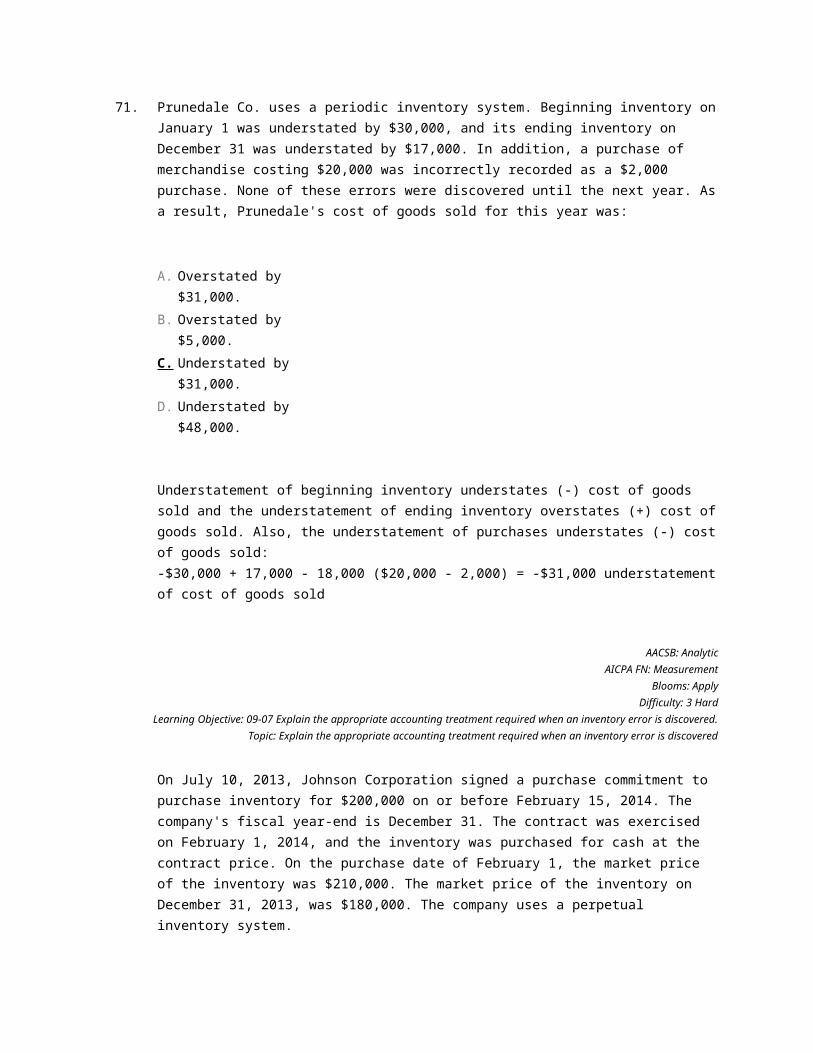

71. Prunedale Co. uses a periodic inventory system. Beginning inventory on January 1 was

understated by $30,000, and its ending inventory on December 31 was understated by $17,000. In addition, a purchase of merchandise costing $20,000 was incorrectly recorded as a $2,000 purchase. None of these errors were discovered until the next year. As a result, Prunedale's cost of goods sold for this year was:

A. Overstated by $31,000.

B. Overstated by $5,000.

C. Understated by $31,000.

D. Understated by $48,000.

On July 10, 2013, Johnson Corporation signed a purchase commitment to purchase inventory for $200,000 on or before February 15, 2014. The company's fiscal year-end is December 31. The contract was exercised on February 1, 2014, and the inventory was purchased for cash at the contract price. On the purchase date of February 1, the market price of the inventory was $210,000. The market price of the inventory on December 31, 2013, was $180,000. The company uses a perpetual inventory system.

72. How much loss on purchase commitment will Johnson recognize in 2013?

A. $10,000.

B. $20,000.

C. $30,000.

D. None.

73. At what amount will Johnson record the inventory purchased on February 1, 2014?

A. $210,000.

B. $200,000.

C. $180,000.

D. $190,000.

Sullivan Corporation has determined its year-end inventory on a FIFO basis to be $500,000. Information pertaining to that inventory is as follows:

74. What should be the carrying value of Sullivan's inventory?

A. $500,000.

B. $440,000.

C. $430,000.

D. $490,000.

75. What should be the carrying value of Sullivan's inventory if the company prepares its

financial statements according to International Financial Reporting Standards?

A. $500,000.

B. $440,000.

C. $430,000.

D. $490,000.

76. Under International Financial Reporting Standards, inventory is valued at the lower of

cost and:

A. Replacement cost.

B. Net realizable value.

C. Net realizable value reduced by a normal profit margin.

D. None of the above.

77. Haskell Corporation. has determined its year-end inventory on a FIFO basis to be $785,000. Information pertaining to that inventory is as follows:

What should be the carrying value of Sullivan's inventory if the company prepares its financial statements according to International Financial Reporting Standards?

A. $765,000.

B. $785,000.

C. $770,000.

D. $700,000.

Matching Questions

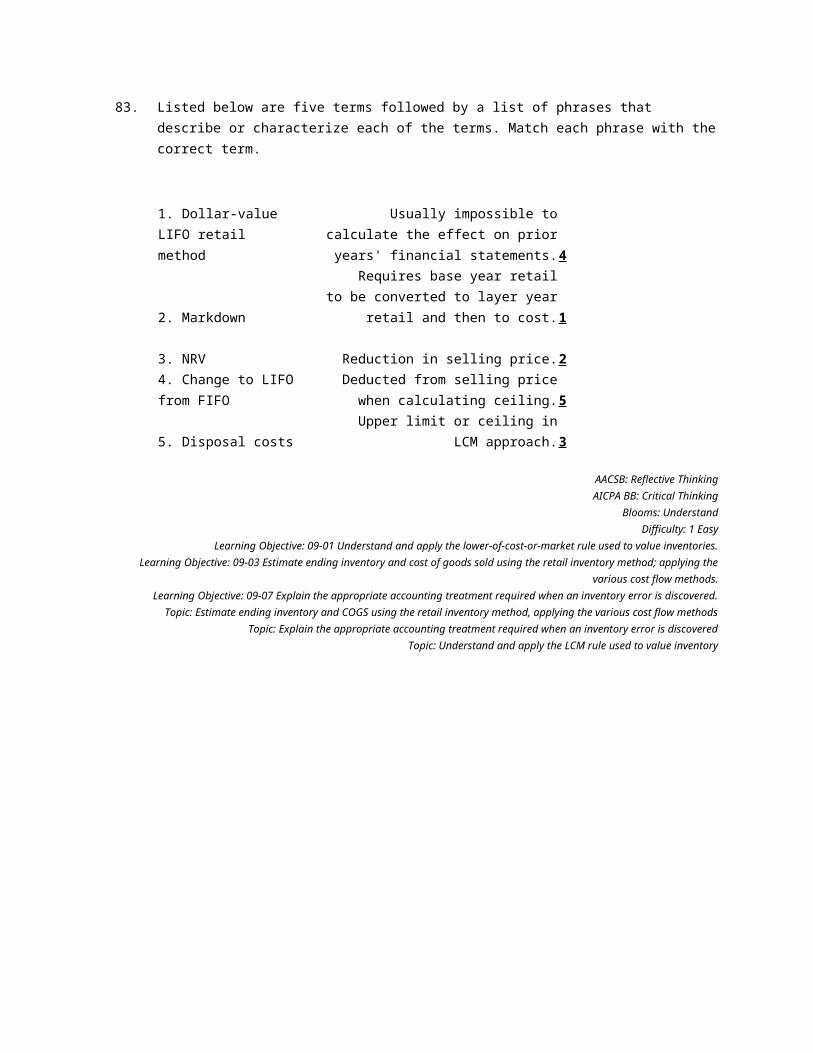

78. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

1. Retrospective treatment

Required for a change from FIFO to average cost. ____

2. Change from LIFO to FIFO

Beginning inventory is not included in the calculation of the current period's

cost-to-retail percentage. ____

3. LIFO retail Estimates value of inventory based

on historical relationships. ____4. Gross profit method

Added in arriving at ending inventory at retail. ____

5. Net markup Requires retrospective treatment. ____

79. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

1. Normal spoilage Change from LIFO to FIFO. ____

2. Cost-to-retail percentage

Always deducted after arriving at the calculation of the cost-to-retail

percentage. ____3. Requires retrospective treatment

Cost-to-retail percentage is determined for all goods available for

sale. ____4. Average cost retail method

Deducted in arriving at ending inventory at retail. ____

5. Net markdown Divide cost of goods available for

sale by goods available at retail. ____ 80. Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. Normal profit margin

Ideal for high volume, low cost inventory. ____

2. Retail inventory method Elimination of a price reduction. ____3. Markdown cancellation

Gross profit percentage times selling price. ____

4. Markup on cost Gross profit divided by cost. ____5. Gross profit ratio Gross profit divided by sales. ____

81. Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. Conventional retail method

Markdowns are not in the calculation of the cost-to-retail

percentage. ____2. Replacement cost Increase in selling price. ____3. Requires retrospective restatement

Material inventory error discovered in a subsequent year. ____

4. LCM Losses would be recognized

when values decline. ____

5. Additional markup Market if between ceiling and

floor. ____

82. Listed below are five terms followed by a list of phrases that describe or characterize each of the terms. Match each phrase with the correct term.

1. Employee discounts

Must be added to sales if sales are recorded net of discounts. ____

2. Inventory error, example NRV less "normal" profit. ____

3. Initial markup Approximates lower of average

cost or market. ____4. Conventional retail method Purchases are unrecorded. ____5. Floor in LCM approach

Original increase in selling price above cost. ____

83. Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

1. Dollar-value LIFO retail method

Usually impossible to calculate the effect on prior years' financial

statements. ____

2. Markdown

Requires base year retail to be converted to layer year retail and

then to cost. ____3. NRV Reduction in selling price. ____4. Change to LIFO from FIFO

Deducted from selling price when calculating ceiling. ____

5. Disposal costs Upper limit or ceiling in LCM

approach. ____

84. Listed below are 10 terms followed by a list of phrases that describe or characterize the terms. Match each phrase with the correct term.

1. Change to LIFO from FIFO

Requires base year retail to be converted to layer year retail and then

to cost. ____2. Change from LIFO

Divide cost of goods available for sale by goods available at retail. ____

3. Gross profit method Average cost, LCM. ____

4. Normal spoilage Accounting change requiring

retrospective treatment. ____

5. Markdown Not acceptable for the preparation

of annual financial statements. ____6. Dollar-value LIFO retail

Ceiling in the determination of market. ____

7. Net realizable value

Reduction in selling price below the original selling price. ____

8. Employee discounts

Usually impossible to calculate the effect on prior years' financial

statements. ____9. Conventional retail method

Must be added to sales if sales are recorded net of discounts. ____

10. Cost-to-retail percentage

Deducted in the retail column after the calculation of the cost-to-retail

percentage. ____

Short Answer Questions

85. Chicago Inc. applies lower-of-cost-or-market valuation to individual products and has collected the following data:

Required:

Determine the balance sheet inventory carrying value for Products A, B, and C.

Novelli's Nursery has developed the following data for lower-of-cost-or-market valuation for its products:

The normal profit margin on all trees is 20% of selling price and disposal costs are 10% of selling price.

86. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to individual trees.

87. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to classes of trees.

88. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to the total inventory.

Weldon Animal Feeds has developed the following data for lower-of-cost-or-market valuation for its products (in thousands):

The normal profit margin on all feed is 25% of selling price and disposal costs are 20% of selling price.

89. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to individual types of feeds.

90. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to classes of feeds.

91. Required:

Determine the balance sheet inventory carrying value assuming the LCM rule is applied to the total inventory.

92. Henderson Company uses the gross profit method to estimate ending inventory and

cost of goods sold when preparing monthly financial statements required by its bank. Inventory on hand at the end of July was $122,500. The following information for the month of August was available from company records:

In addition, the controller is aware of $10,000 of inventory that was stolen during August from one of the company's warehouses.

Required:

1. Calculate the estimated inventory at the end of August, assuming a gross profit ratio of 30%.2. Calculate the estimated inventory at the end of August, assuming a markup on cost of 25%.

93. On March 17, 2013, a flood destroyed the entire inventory of Beatty Co. The following information is available from its accounting records:

Required:

Compute the estimated cost of inventory lost in the flood.

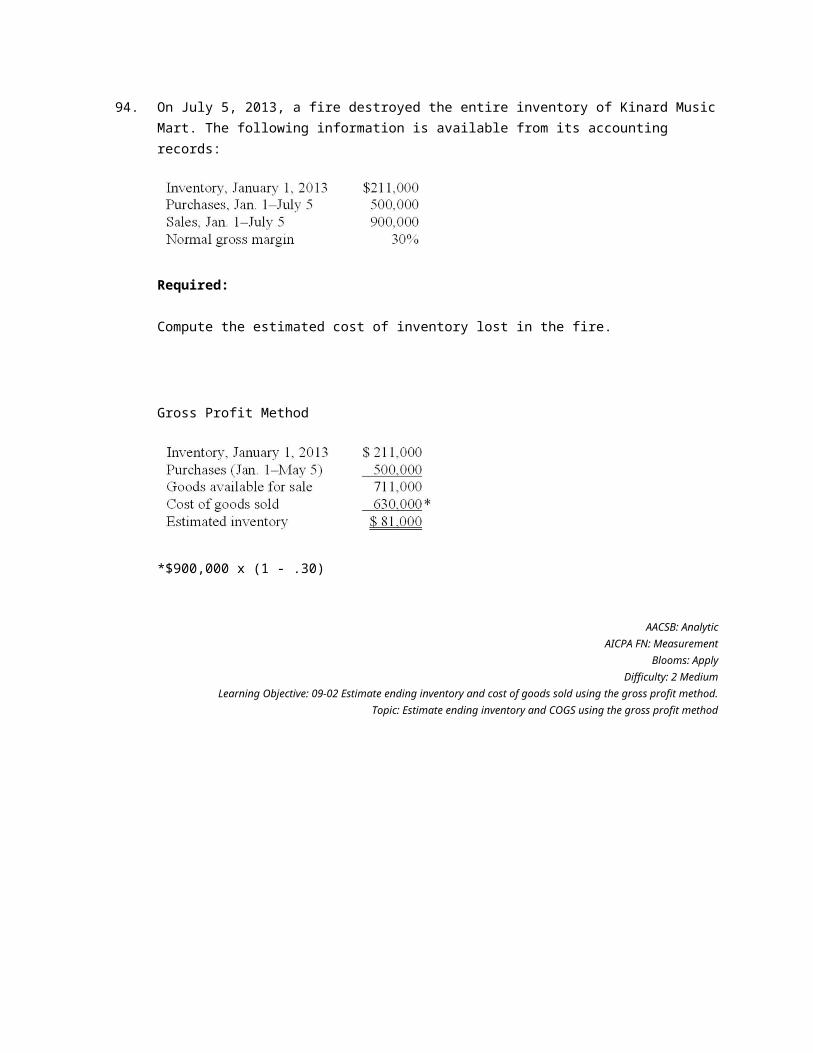

94. On July 5, 2013, a fire destroyed the entire inventory of Kinard Music Mart. The

following information is available from its accounting records:

Required:

Compute the estimated cost of inventory lost in the fire.

95. On August 31, 2013, Hurricane Chuck destroyed Bedford Craft Mart's entire inventory. The following information is available from its accounting records:

Required:

Assuming that Bedford estimates the cost of destroyed inventory at $510,000, compute gross profit margin % that Bedford uses in estimating inventory.

96. Andover Stores uses the average cost retail method to estimate its ending inventory.

Information as of June 30, 2013, is as follows:

Required:

Use the retail method to estimate the June 30, 2013, inventory.

97. DK Super Stores Inc. uses the average cost retail method to estimate its ending inventory. Information at June 30, 2013, is as follows:

Required:

Compute the cost-to-retail percentage used by DK.

98. Trask Inc. uses the average cost retail method to estimate its ending inventory. Partial information at June 30, 2013, is as follows:

Required:

Assuming Trask's cost-to-retail = 60%, compute Trask's beginning inventory at retail.

99. Manila Bread Company uses the average cost retail method to estimate its ending inventories. The following data has been summarized for the year 2013:

Required:

Estimate the ending inventory as of December 31, 2013.

100.

Penfold's Paints uses the average cost retail method to estimate its ending inventories. The following data has been summarized for the year 2013:

Required:

Compute the cost-to-retail percentage used by Penfold's Paints.

101.

Murdock Industries uses a periodic inventory system and the LIFO retail method to estimate its ending inventories. The following data has been summarized for December 31, 2013:

Required:

Estimate the LIFO cost of ending inventory. Assume stable retail prices during the period.

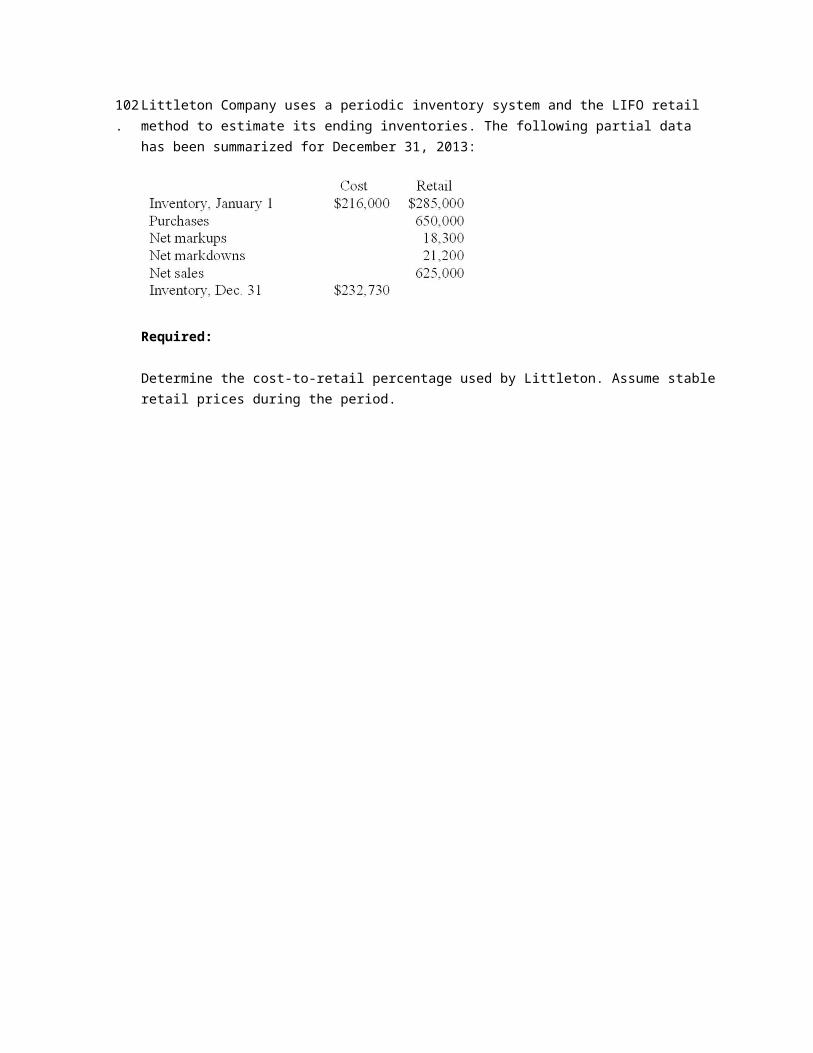

102.

Littleton Company uses a periodic inventory system and the LIFO retail method to estimate its ending inventories. The following partial data has been summarized for December 31, 2013:

Required:

Determine the cost-to-retail percentage used by Littleton. Assume stable retail prices during the period.

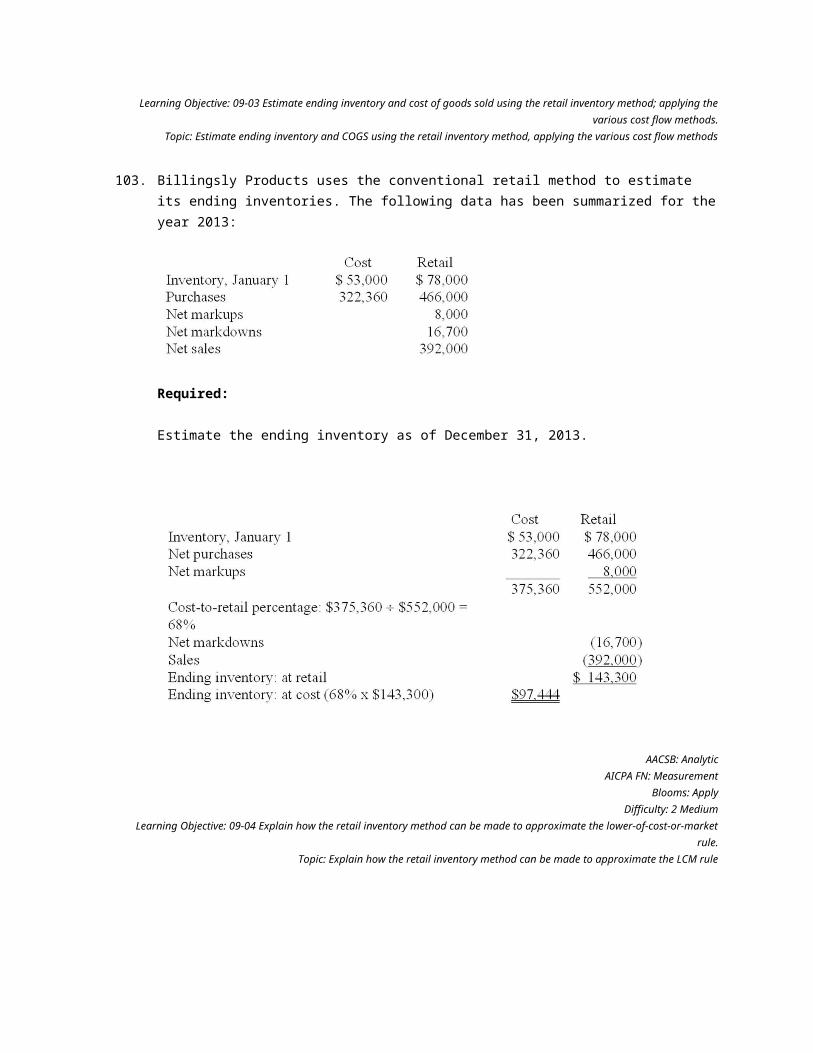

103.

Billingsly Products uses the conventional retail method to estimate its ending inventories. The following data has been summarized for the year 2013:

Required:

Estimate the ending inventory as of December 31, 2013.

104.

New York Sales Inc. uses the conventional retail method to estimate its ending inventories. The following data has been summarized for December 31, 2013:

Required:

Compute the cost-to-retail percentage used by New York Sales Inc.

105.

Harley Inc. uses the conventional retail method to estimate its ending inventories. The following data has been summarized for December 31, 2013:

Required:

Estimate the cost of ending inventory applying the conventional retail method.

106.

Zanesville Pots Co. uses the conventional retail method to estimate ending inventories. The following data has been summarized for the year ended December 31, 2013:

Required:

Estimate the cost of ending inventory applying the conventional retail method.

107.

Cornhusker Can Co. uses the conventional retail method to estimate ending inventories. The following data has been summarized for year ended December 31, 2013:

Required:

Estimate the cost of ending inventory applying the conventional retail method. Assume that sales are recorded net of employee discounts.

108.

Cindy Lou Linens uses the conventional retail method to estimate its ending inventories. The company records sales net of employee discounts. The following partial data has been summarized for the year ended December 31, 2013:

Required:

Compute the net markups for Cindy Lou Linens during 2013.

109.

Charleston Company has elected to use the dollar-value LIFO retail method to value its inventory. The following data has been accumulated from the accounting records:

Required:

Estimate the ending inventory for December 31, 2013.

110.

Green Acres Co. has elected to use the dollar-value LIFO retail method to value its inventory. The following data has been accumulated from the accounting records:

Pertinent retail price indexes:

Required:

Estimate the cost of ending inventory for December 31, 2013.

111.

Orlando Company has used the average cost method for inventory valuation since it began business in 2009, but has elected to change to the FIFO method starting in 2012. Year-end inventory valuations under each method are shown below:

Required:

How would Orlando reflect the change in accounting principle in its financial statements (ignore income taxes)?

112.

Ramsgate Company has used the FIFO method for inventory valuation since it began business in 2009, but has elected to change to the average cost method starting in 2012. Year-end inventory valuations under each method are shown below:

Required:

How, and when, would Ramsgate reflect the change in accounting principle in its financial statements (ignore income taxes)?

In the following question, inventory errors are noted for 2013. Assume that the errors are not discovered until 2012, and that the company uses a periodic inventory system. Indicate the effect of the error, if any, on the accounts noted in the columns, using the following code:U = Understated; O = Overstated; NE = No effect

113.

114.

115.

116.

117.

118.

In 2013, the internal auditors of Blooper Inc. discovered that goods costing $12 million that were shipped f.o.b. shipping point in December of 2012 were in transit on December 31. The goods were recorded as a purchase in December of 2012 but were not included in the 2012 year-end inventory.

Required:

Prepare the journal entry needed in 2013 to correct the error. Also, briefly describe any other measures Blooper would take in connection with correcting the error. (Ignore income taxes.)

119.

In the year 2013, the internal auditors of Goofy Co. discovered that goods costing $25 million that were purchased in December of 2012 were recorded for $20 million. The goods were properly measured in the December 31, 2012, ending physical inventory.

Required:

Prepare the journal entry needed in 2013 to correct the error. Also, briefly describe any other measures Goofy would take in connection with correcting the error. (Ignore income taxes.)

120.

On September 5, 2013, Howard Corporation signed a purchase commitment to purchase inventory for $130,000 on or before March 31, 2014. The company's fiscal year-end is December 31. The contract was exercised on March 4, 2014, and the inventory was purchased for cash at the contract price. On the purchase date of March 4, the market price of the inventory was $116,000. The market price of the inventory on December 31, 2013, was $120,000. The company uses a perpetual inventory system.

Required:

1. Prepare the necessary adjusting journal entry (if any is required) on December 31, 2013.2. Prepare the journal to record the purchase on March 4, 2014.

Memphis Wholesale Market applies lower-of-cost-or-market valuation to individual products and has collected the following data:

121.

Determine the balance sheet inventory carrying value for Products A, B, and C.

122.

Determine the balance sheet inventory carrying value for Products A, B, and C assuming that Memphis Wholesale Market prepares its financial statements according to International Financial Reporting Standards.

Essay Questions

123.

Briefly explain what is meant by "market" in the lower-of-cost-or-market (LCM) approach.

124.

Briefly explain how a material adjustment to inventory due to application of the lower-of-cost-or-market rule should be reported in the financial statements.

125.

The following disclosure note appeared in the 2013 annual report to shareholders of Upton Systems Inc.

Inventories are stated at the lower of cost or market. Cost is computed using standard cost, which approximates actual cost, on a first-in, first-out basis. The Company provides inventory allowances based on excess and obsolete inventories.

Another disclosure note in the annual report stated:

The Company recorded a provision for inventory, including purchase commitments, totaling $1.40 billion during fiscal 2013, which included an additional excess inventory charge as previously discussed. This additional excess inventory charge was due to a sudden and significant decrease in demand for the Company's products and was calculated in accordance with the Company's accounting policy.

A skeptic may conclude that Upton's policy and practices threaten earnings quality. Discuss how it may do so.

126.

Briefly explain the differences between U.S. GAAP and International Financial Reporting Standards in the application of the lower-of-cost-or-market rule for valuing inventory.

127.

Briefly outline the steps in the gross profit method of estimating ending inventory and indicate when the method might be used.

128.

The gross profit method and retail method are both ways of estimating ending inventory. Briefly explain how the two methods differ.

129.

Briefly explain the difference between the LIFO retail method and the dollar-value LIFO retail method.

130.

Briefly explain the financial reporting required when a company changes to or from the LIFO inventory method.

131.

Briefly explain the financial reporting required when material misstatements are found in previous years' financial statements that are included for comparative purposes in the current year's financial statements.

132.

Symington and Cribbs (S&C) is a sporting goods distributor. S&C uses the FIFO inventory method to determine the cost of its ending inventory. Ending inventory quantities are determined by a physical count. For the fiscal year-end December 31, 2013, ending inventory was originally determined to be $67 million. However, in early January of 2014, the company's controller, Amy Grant, discovered that an error was made in the inventory count. The correct amount of ending inventory should be $87 million. The auditors did not discover the error and the financial statements are scheduled to be issued on February 26, 2014. S&C is a public company.Amy's first reaction was to communicate her finding to the auditors and to revise the financial statements before they are issued. However, she knows that this was a very good year for the company with profits far exceeding analysts' expectations. If the error is not corrected this year, it will self-correct next year as long as 2014 ending inventory is correctly stated. This will help future 2014 profits. On the other hand, her fellow workers' profit sharing plans are based on annual pretax earnings and if she revises the statements, everyone's profit sharing bonus will be higher this year.

Required:

1. Is Amy correct by stating that the error will self-correct next year as long as 2014 ending inventory is correctly stated? If the error is not corrected in the current year, what will be the effect on 2013 and 2014 income before tax?2. Discuss the ethical dilemma Amy faces.

Chapter 09 Inventories: Additional Issues Answer Key

True / False Questions

1. In determining lower of cost or market, market is the expected selling price under normal operations. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

2. Net realizable value is selling price less costs of completion and disposal. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

3. The primary motivation behind LCM is consistency. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

4. The purpose of ceilings and floors in LCM is to prevent profit distortion. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

5. Losses on reduction to LCM may be charged to either cost of goods sold or to a current loss account. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

6. Inventory written down due to LCM may be written back up if market values increase. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

7. Under the LIFO retail method, the current period cost-to-retail percentage includes both net markdowns and net markups. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

8. Purchase returns and purchase discounts are ignored when computing cost-to-retail ratios for the retail method. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

9. The cost-to-retail percentage used in the retail method to approximate average cost incorporates both markdowns and markups. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-cost-or-market rule.

Topic: Explain how markups and markdowns are incorporated into the retail inventory method

10. If the quantity of goods held in inventory decreased during the period, the dollar amount of ending inventory cannot exceed the dollar amount of beginning inventory. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: UnderstandDifficulty: 1 Easy

Learning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

11. When changing from the average cost method to FIFO, the current year's income includes the cumulative after-tax difference that would have resulted if the company had used FIFO in all prior years. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-06 Explain the appropriate accounting treatment required when a change in inventory method is made.

Topic: Explain the appropriate accounting treatment required when a change in inventory method is made

12. A change from LIFO to any other inventory method is accounted for retrospectively. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-06 Explain the appropriate accounting treatment required when a change in inventory method is made.

Topic: Explain the appropriate accounting treatment required when a change in inventory method is made

13. For a purchase commitment contained within a single fiscal year, if the market price is less than the contract price, the purchase is recorded at the contract price. FALSE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-Appendix Purchase Commitments.Topic: Purchase commitments

14. For a purchase commitment extending beyond the current fiscal year, if the market price on the purchase date declines from the previous year-end price, the purchase is recorded at the market price. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-Appendix Purchase Commitments.Topic: Purchase commitments

15. International Financial Reporting Standards allow the reversal of an inventory write-down. TRUE

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-08 Discuss the primary differences between U.S. GAAP and IFRS with respect to the lower-of-cost-or-market rule for valuing inventory.

Topic: Discuss the primary differences between U.S. GAAP and IFRS with respect to the LCM rule for valuing inventory

Multiple Choice Questions

16. In applying LCM, market cannot be:

A. Less than net realizable value.

B. Greater than the normal profit.

C. Less than the normal profit margin.

D. Greater than net realizable value.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

17. In applying LCM, market cannot be:

A. Less than net realizable value minus a normal profit margin.

B. Net realizable value less reasonable completion and disposal costs.

C. Greater than net realizable value reduced by an allowance for normal profit margin.

D. Less than cost.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

18. Masterlink Co., in applying the lower of cost or market method, reports its inventory at net realizable value. Which of the following statements is correct?

A. Option a

B. Option b

C. Option c

D. Option d

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: UnderstandDifficulty: 2 Medium

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

19. An argument against the use of LCM is its lack of:

A. Relevance.

B. Reliability.

C. Consistency.

D. Objectivity.

AACSB: Reflective ThinkingAICPA FN: Decision Making

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.Topic: Understand and apply the LCM rule used to value inventory

20. Montana Co. has determined its year-end inventory on a FIFO basis to be $600,000. Information pertaining to that inventory is as follows:

What should be the carrying value of Montana's inventory?

A. $600,000.

B. $520,000.

C. $590,000.

D. $510,000.

NRV = $590,000NRV - NP = $510,000RC = $520,000Designated market is RC = $520,000 which is less than cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

Data related to the inventories of Costco Medical Supply are presented below:

21. In applying the LCM rule, the inventory of surgical equipment would be valued at:

A. $230.

B. $240.

C. $170.

D. $152.

$170 designated cost is less than $230 designated market value.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

22. In applying the LCM rule, the inventory of surgical supplies would be valued at:

A. $115.

B. $90.

C. $80.

D. $69.

$80 designated market value is less than $90 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

23. In applying the LCM rule, the inventory of rehab equipment would be valued at:

A. $315.

B. $247.

C. $150.

D. $235.

$235 designated market value is less than $250 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

24. In applying the LCM rule, the inventory of rehab supplies would be valued at:

A. $122.

B. $158.

C. $162.

D. $155.

$155 designated market value is less than $162 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

Data related to the inventories of Alpine Ski Equipment and Supplies is presented below:

25. In applying the LCM rule, the inventory of skis would be valued at:

A. $162,000.

B. $128,000.

C. $120,000.

D. $126,000.

$126,000 designated market value is less than $128,000 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

26. In applying the LCM rule, the inventory of boots would be valued at:

A. $135,000.

B. $133,000.

C. $130,000.

D. $105,000.

$130,000 designated market value is less than $133,000 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

27. In applying the LCM rule, the inventory of apparel would be valued at:

A. $108,000.

B. $90,000.

C. $110,000.

D. $115,000.

$90,000 cost is less than the designated market value of $108,000 cost.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

28. In applying the LCM rule, the inventory of supplies would be valued at:

A. $45,000.

B. $54,000.

C. $41,000.

D. $42,000.

$45,000 cost is equal to the designated market value.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-01 Understand and apply the lower-of-cost-or-market rule used to value inventories.

Topic: Understand and apply the LCM rule used to value inventory

29. When using the gross profit method to estimate ending inventory, it is not necessary to know:

A. Beginning inventory.

B. Net purchases.

C. Cost of goods sold.

D. Net sales.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: UnderstandDifficulty: 2 Medium

Learning Objective: 09-02 Estimate ending inventory and cost of goods sold using the gross profit method.Topic: Estimate ending inventory and COGS using the gross profit method

30. On July 8, a fire destroyed the entire merchandise inventory on hand of Larrenaga Wholesale Corporation. The following information is available:

What is the estimated inventory on July 8 immediately prior to the fire?

A. $192,000.

B. $490,000.

C. $510,000.

D. $280,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-02 Estimate ending inventory and cost of goods sold using the gross profit method.

Topic: Estimate ending inventory and COGS using the gross profit method

31. California Inc., through no fault of its own, lost an entire plant due to an earthquake on May 1, 2013. In preparing its insurance claim on the inventory loss, the company developed the following data: Inventory January 1, 2013, $300,000; sales and purchases from January 1, 2013, to May 1, 2013, $1,300,000 and $875,000, respectively. California consistently reports a 40% gross profit. The estimated inventory on May 1, 2013, is:

A. $302,500.

B. $360,000.

C. $395,000.

D. $455,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-02 Estimate ending inventory and cost of goods sold using the gross profit method.

Topic: Estimate ending inventory and COGS using the gross profit method

32. Howard's Supply Co. suffered a fire loss on April 20, 2013. The company's last physical inventory was taken January 30, 2013, at which time the inventory totaled $220,000. Sales from January 30 to April 20 were $600,000 and purchases during that time were $450,000. Howard's consistently reports a 30% gross profit. The estimated inventory loss is:

A. $490,000.

B. $238,000.

C. $250,000.

D. None of the above is correct.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-02 Estimate ending inventory and cost of goods sold using the gross profit method.

Topic: Estimate ending inventory and COGS using the gross profit method

33. Coastal Shores Inc. (CSI) was destroyed by Hurricane Fred on August 5, 2013. At January 1, CSI reported an inventory of $170,000. Sales from January 1, 2013, to August 5, 2013, totaled $480,000 and purchases totaled $195,000 during that time. CSI consistently marks up its products 60% over cost to arrive at a selling price. The estimated inventory loss due to Hurricane Fred would be:

A. $131,175.

B. $65,000.

C. $17,143.

D. None of the above is correct.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-02 Estimate ending inventory and cost of goods sold using the gross profit method.

Topic: Estimate ending inventory and COGS using the gross profit method

34. Under the conventional retail method, the denominator in the cost-to-retail percentage includes:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

35. Under the LIFO retail method, the denominator in the cost-to-retail percentage includes:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

36. Under the retail method, the denominator in the cost-to-retail percentage does not include:

A. Purchases.

B. Purchase returns.

C. Abnormal shortages.

D. Freight-in.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

37. Under the retail inventory method:

A. A company measures inventory on its balance sheet by converting retail prices to cost.

B. A company measures inventory on its balance sheet at current selling prices.

C. A company measures inventory on its balance sheet on a LIFO basis.

D. None of the above is correct.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

38. Under the conventional retail method, which of the following are not included in the denominator of the current period cost-to-retail conversion percentage?

A. Purchase returns.

B. Net markups.

C. Purchases.

D. Net markdowns.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-cost-or-market rule.

Topic: Explain how the retail inventory method can be made to approximate the LCM rule

39. Under the LIFO retail method, which of the following are not included in the denominator of the cost-to-retail conversion percentage?

A. Freight-in.

B. Purchase returns.

C. Purchases.

D. Net markdowns.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

40. Under the retail method, in determining the cost-to-retail percentage for the current year:

A. Net markups are included.

B. Net markdowns are excluded.

C. Net sales are included.

D. All of the above are correct.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method; applying the various cost flow methods.

Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow methods

41. Fad City sells novel clothes that are subject to a great deal of price volatility. A recent item that cost $20 was marked up $12, marked down for a sale by $6 and then had a markdown cancellation of $3. The latest selling price is:

A. $23.

B. $26.

C. $29.

D. $35.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

Harvey's Junk Jewelry started business January 1, 2013, and uses the LIFO retail method to estimate ending inventory. Listed below is data accumulated for the year ended December 31, 2013:

42. The numerator for the current period's cost-to-retail percentage is:

A. $64,800.

B. $48,100.

C. $47,700.

D. $49,800.

$49,800

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

43. The denominator for the current period's cost-to-retail percentage is:

A. $96,300.

B. $73,300.

C. $101,000.

D. $81,500.

$73,300

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

44. The estimated ending inventory at retail is:

A. $27,300.

B. $25,000.

C. $26,600.

D. $26,400.

$25,000

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

45. To the nearest thousand, the estimated ending inventory at cost is:

A. $16,000.

B. $15,000.

C. $13,000.

D. $19,000.

$16,000

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

46. Lacy's Linen Mart uses the retail method to estimate inventories. Data for the first six months of 2013 include: beginning inventory at cost and retail were $60,000 and $120,000, net purchases at cost and retail were $312,000 and $480,000, and sales during the first six months totaled $490,000. The estimated inventory at June 30, 2013, would be:

A. $68,200.

B. $55,000.

C. $71,500.

D. $63,250.

Cost-to-retail percentage = $372,000 ÷ $600,000 = 62%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

47. Hawkeye Auto Parts uses the retail method to estimate inventories. Data for the first six months of 2013 include: beginning inventory at cost and retail were $55,000 and $100,000, net purchases at cost and retail were $785,000 and $1,300,000, and sales during the first six months totaled $800,000. The estimated inventory at June 30, 2013, would be:

A. $330,000.

B. $360,000.

C. $362,300.

D. None of the above is correct.

Cost-to-retail percentage = $840,000 ÷ $1,400,000 = 60%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

Marilee's Electronics uses a periodic inventory system and the average cost retail method to estimate ending inventory and cost of goods sold. The following data is available from the company records for the month of June 2013:

48. The average cost-to-retail percentage is:

A. 52.2%.

B. 61.5%.

C. 56.8%

D. 55%.

Cost-to-retail percentage = $341,000 ÷ $620,000 = 55%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

49. To the nearest thousand, estimated ending inventory is:

A. $55,000.

B. $52,000.

C. $57,000.

D. None of the above is correct.

Cost-to-retail percentage = $341,000 ÷ $620,000 = 55%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

Benny's Bed Co. uses a periodic inventory system and the average cost retail method to estimate ending inventory and cost of goods sold. The following data is available from the company records for the month of September 2013.

50. The average cost-to-retail percentage is:

A. 74.5%.

B. 55.6%.

C. 57.4%.

D. 58.7%.

55.6%

Cost-to-retail percentage = $155,000 ÷ $279,000 = 55.6%.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

51. To the nearest thousand, estimated ending inventory is:

A. $41,000.

B. $37,000.

C. $51,000.

D. None of the above is correct.

The correct answer is $39,000 (rounded)

Cost-to-retail percentage = $155,000 ÷ $279,000 = 55.6%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

Data below for the year ended December 31, 2013, relates to Houdini Inc. Houdini started business January 1, 2013, and uses the LIFO retail method to estimate ending inventory.

52. Current period cost-to-retail percentage is:

A. 70.0%.

B. 68.7%.

C. 63.6%.

D. 63.5%.

Cost-to-retail percentage = $280,000 ÷ $400,000 = 70%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

53. Estimated ending inventory at retail is:

A. $65,000.

B. $169,600.

C. $25,000.

D. $129,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

54. Estimated ending inventory at cost is:

A. $90,720.

B. $83,500.

C. $91,600.

D. None of the above is correct.

Current period cost-to-retail percentage = $280,000 ÷ $400,000 = 70%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-03 Estimate ending inventory and cost of goods sold using the retail inventory method;

applying the various cost flow methods.Topic: Estimate ending inventory and COGS using the retail inventory method, applying the various cost flow

methods

55. When computing the cost-to-retail percentage for the average cost retail method, included in the denominator are:

A. Net markups and net markdowns.

B. Neither net markups nor net markdowns.

C. Net markups, but not net markdowns.

D. Net markdowns, but not net markups.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-cost-or-market rule.

Topic: Explain how the retail inventory method can be made to approximate the LCM rule

56. The conventional retail inventory method is based on:

A. Average cost.

B. LIFO cost.

C. Average, lower of cost or market.

D. LIFO, lower of cost or market.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-cost-or-market rule.

Topic: Explain how the retail inventory method can be made to approximate the LCM rule

57. Cloverdale, Inc., uses the conventional retail inventory method to account for inventory. The following information relates to current year's operations:

What amount should be reported as cost of goods sold for the year?

A. $273,600.

B. $272,861.

C. $275,000.

D. None of the above.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-

cost-or-market rule.Topic: Explain how the retail inventory method can be made to approximate the LCM rule

Willie Nelson's Boots uses the conventional retail method to estimate ending inventory. Cost data for the most recent quarter is shown below:

58. The conventional cost-to-retail percentage (rounded) is:

A. 82.6%.

B. 66.7%.

C. 71.9%.

D. 75.5%.

66.7%

or 2/3

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-

cost-or-market rule.Topic: Explain how the retail inventory method can be made to approximate the LCM rule

59. To the nearest thousand, estimated ending inventory using the conventional retail method is:

A. $37,000.

B. $32,000.

C. $34,000.

D. $30,000.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-

cost-or-market rule.Topic: Explain how the retail inventory method can be made to approximate the LCM rule

Clarabell Inc. uses the conventional retail method to estimate ending inventory. Cost data for the most recent quarter is shown below:

60. The conventional cost-to-retail percentage (rounded) is:

A. 54.9%.

B. 58.9%.

C. 53.6%.

D. 70.6%.

54.9%

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-

cost-or-market rule.Topic: Explain how the retail inventory method can be made to approximate the LCM rule

61. To the nearest thousand, estimated ending inventory using the conventional retail method is:

A. $163,000.

B. $124,000.

C. $127,000.

D. $136,000.

127,000

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-

cost-or-market rule.Topic: Explain how the retail inventory method can be made to approximate the LCM rule

62. Using the dollar-value LIFO retail method for inventory:

A. Is the same as dollar-value LIFO, except that the inventory is measured at retail, rather than at cost.

B. Combines retail LIFO accounting with dollar-value LIFO accounting.

C. Allows companies to report inventory on the balance sheet at retail prices.

D. All of the above are correct.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

63. The first step, when using dollar-value LIFO retail method for inventory, is to:

A. Determine the estimated ending inventory at current year retail prices.

B. Determine the estimated cost of goods sold for the current year.

C. Determine the cost-to-retail percentage for the current year transactions.

D. Price index adjust the LIFO inventory layers.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

64. The second step, when using dollar-value LIFO retail method for inventory, is to determine the estimated:

A. Ending inventory at current year retail prices.

B. Cost of goods sold for the current year.

C. Ending inventory at cost.

D. Ending inventory at base year retail prices.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 1 Easy

Learning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

65. Under the dollar-value LIFO retail method, to determine if the increase in the value of inventory was due to an increase in quantities:

A. Compare beginning and ending inventory amounts at current year prices.

B. Compare beginning and ending inventory amounts after adjusting both amounts to the average price level for the year.

C. Inflate beginning inventory amount to end of year prices and compare to ending inventory amount.

D. Deflate the ending inventory amount to beginning of year prices and compare to the beginning inventory amount.

AACSB: Reflective ThinkingAICPA BB: Critical Thinking

Blooms: RememberDifficulty: 2 Medium

Learning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

66. Under the dollar-value LIFO retail method, to determine the value of a LIFO layer:

A. Divide the LIFO layer by the layer-year price index and multiply by the layer-year cost-to-retail percentage.

B. Multiply the LIFO layer by the base year price index and the current year cost-to-retail percentage.

C. Multiply the LIFO layer by the layer-year price index and by the layer-year cost-to-retail percentage.

D. Divide the LIFO layer by the layer-year cost-to-retail percentage and multiply by the layer-year price index.

AACSB: Analytic

AICPA BB: Critical ThinkingBlooms: Apply

Difficulty: 2 MediumLearning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.

Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

67. Portman Inc. uses the conventional retail inventory method. Expressed in millions of dollars, information about Portman's 2013 inventory account is expressed in the table below:

What is the value of Portman's inventory at 12/31/13?

A. $150 million.

B. $252 million.

C. $300 million.

D. None of the above is correct.

$150 million is correct. The following table shows the correct computations:

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 Hard

Learning Objective: 09-04 Explain how the retail inventory method can be made to approximate the lower-of-cost-or-market rule.

Topic: Explain how the retail inventory method can be made to approximate the LCM rule

68. Harlequin Co. has used the dollar-value LIFO retail method since it began operations in early 2012 (its base year). Its beginning inventory for 2013 was $36,000 at cost and $72,000 at retail prices. At the end of 2013, it computed its estimated ending inventory at retail to be $120,000. Assuming its cost-to-retail percentage for 2013 transactions was 60%, what is the inventory balance that Harlequin Co. would report in its 12/31/13 balance sheet?

A. $64,800.

B. $72,000.

C. $120,000.

D. It can't be determined with the given information.

You would need to know the retail price index for 2013 transactions relative to the base year to make this computation.

AACSB: Analytic

AICPA FN: MeasurementBlooms: Apply

Difficulty: 3 HardLearning Objective: 09-05 Determine ending inventory using the dollar-value LIFO retail inventory method.

Topic: Determine ending inventory using the dollar-value LIFO retail inventory method

69. Retrospective treatment of prior years' financial statements is required when there is a change from:

A. Average cost to FIFO.

B. FIFO to average cost.

C. LIFO to average cost.

D. All of the above.

AACSB: Reflective Thinking

AICPA FN: ReportingBlooms: Remember

Difficulty: 1 Easy

Learning Objective: 09-06 Explain the appropriate accounting treatment required when a change in inventory method is made.

Topic: Explain the appropriate accounting treatment required when a change in inventory method is made