chapter 9 - emory goizueta business school intranet

TRANSCRIPT

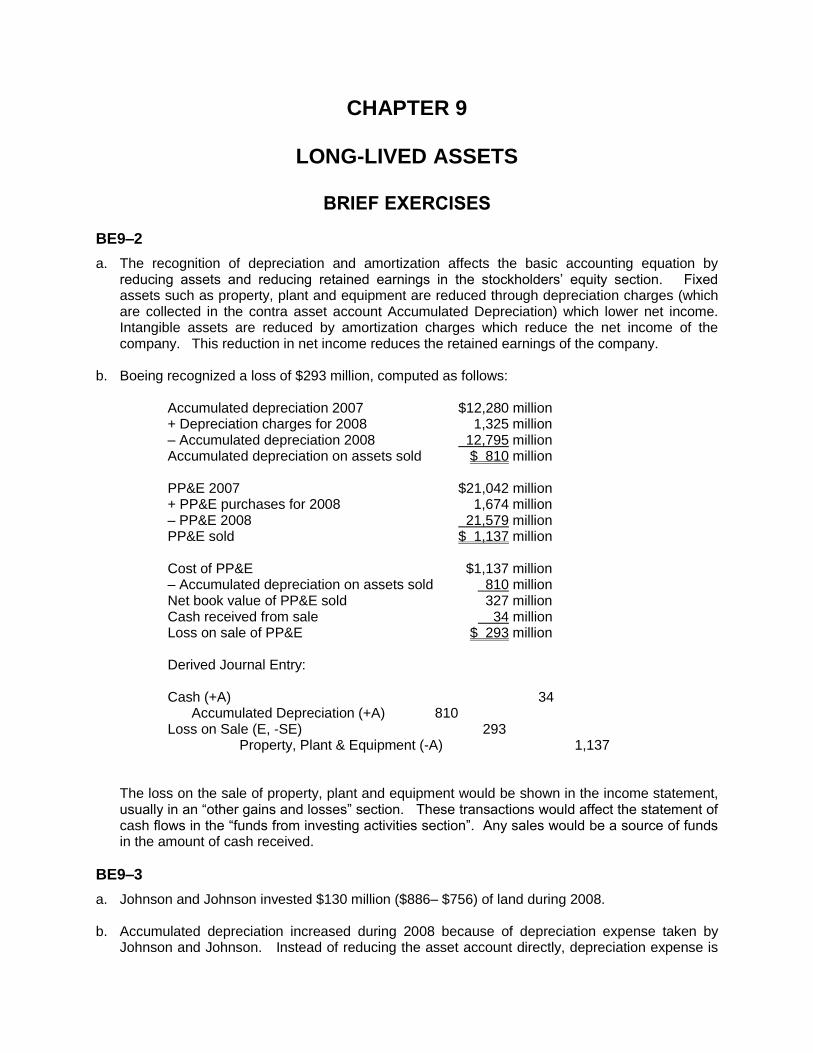

CHAPTER 9

LONG-LIVED ASSETS

BRIEF EXERCISES

BE9–2

a. The recognition of depreciation and amortization affects the basic accounting equation by reducing assets and reducing retained earnings in the stockholders’ equity section. Fixed assets such as property, plant and equipment are reduced through depreciation charges (which are collected in the contra asset account Accumulated Depreciation) which lower net income. Intangible assets are reduced by amortization charges which reduce the net income of the company. This reduction in net income reduces the retained earnings of the company.

b. Boeing recognized a loss of $293 million, computed as follows:

Accumulated depreciation 2007 $12,280 million + Depreciation charges for 2008 1,325 million – Accumulated depreciation 2008 12,795 million Accumulated depreciation on assets sold $ 810 million

PP&E 2007 $21,042 million + PP&E purchases for 2008 1,674 million – PP&E 2008 21,579 million PP&E sold $ 1,137 million Cost of PP&E $1,137 million – Accumulated depreciation on assets sold 810 million Net book value of PP&E sold 327 million Cash received from sale 34 million Loss on sale of PP&E $ 293 million Derived Journal Entry: Cash (+A) 34

Accumulated Depreciation (+A) 810 Loss on Sale (E, -SE) 293

Property, Plant & Equipment (-A) 1,137 The loss on the sale of property, plant and equipment would be shown in the income statement,

usually in an “other gains and losses” section. These transactions would affect the statement of cash flows in the “funds from investing activities section”. Any sales would be a source of funds in the amount of cash received.

BE9–3

a. Johnson and Johnson invested $130 million ($886– $756) of land during 2008. b. Accumulated depreciation increased during 2008 because of depreciation expense taken by

Johnson and Johnson. Instead of reducing the asset account directly, depreciation expense is

added to accumulated depreciation, which offsets the asset account to show its reduction in value.

c. If the company used an accelerated method of depreciation, the assets would be shown at a

lower net value in the early years. Accelerated methods take more depreciation charges in the early years of an asset’s life and less in the later years, when compared to the straight-line method.

d. Johnson and Johnson would show $14,365 million for property, plant and equipment on its

financial statement for 2008. The gross amount and the accumulated depreciation would be disclosed in the footnote.

EXERCISES

E9–1

a. Lowery, Inc., should capitalize all costs associated with getting the equipment in a serviceable condition and location. These costs would be the actual purchase price of $920,000, the transportation cost of $62,000, and the insurance cost of $10,000. Therefore, the total cost of the equipment is $992,000.

b. The depreciation base equals the dollar amount of a fixed asset's cost that the company does

not expect to recover over the asset's useful life, but instead expects to consume over the asset's useful life. Since the plant equipment's total cost is $992,000 and since Lowery, Inc., expects to sell the equipment for $50,000 at the end of its useful life, Lowery, Inc., does not expect to recover $942,000 of the asset's cost. Therefore, the depreciation base equals $942,000. The depreciation base always equals the capitalized cost of a fixed asset less its estimated salvage value.

c. The amount that will be depreciated over the life of the plant equipment is its depreciation base.

The depreciation base equals the amount of the equipment's future benefits that the company will consume. The outflow of future benefits are expenses, in this case depreciation expense. Therefore, the total amount that Lowery, Inc., will depreciate over the equipment's useful life is $942,000.

E9–3

a. All costs that are necessary and reasonable to get an asset ready for its intended use should be capitalized as part of the cost of that asset. In the case of property, plant, and equipment, "ready for its intended use" means that the asset is in a serviceable condition and location.

Land

Item Land Improvements Building

Tract of land $90,000

Demolition of warehouse 10,000

Scrap from warehouse (7,000)

Construction of building $140,000

Driveway and parking lot $32,000

Permanent landscaping 4,000

Total $ 97,000 $32,000 $140,000

b. Land: Since land is assumed to have an indefinite life, it is never depreciated. Land Improvements: Depreciation Expense—Land Improvements (E, –SE) ................... 1,600

Accumulated Depreciation—Land Improvements (–A) .............. 1,600

Depreciated land improvements.

Building: Depreciation Expense—Building (E, –SE) ...................................... 7,000

Accumulated Depreciation—Building (–A).................................. 7,000

Depreciated building.

E9–4

a. Maintenance b. Maintenance c. Maintenance d. Betterment e. Maintenance f. Maintenance g. Betterment h. Maintenance i. Betterment Note: The classification of these expenditures can be quite subjective. Some accountants might

very well classify some of these expenditures differently. For example, one might argue that the cost of the muffler in (h) is actually a betterment expenditure if the reduced noise allows workers to work more efficiently, thereby increasing the productive capacity of the machine.

E9–5

a. (1) Expensed immediately:

Income Statement 2014 2013 2012

Revenues $ 65,000 $ 65,000 $ 65,000 Amortization 0 0 40,000 Other expenses 20,000 20,000 20,000 Net income $ 45,000 $ 45,000 $ 5,000

Balance Sheet 12/31/14 12/31/13 12/31/12

Assets Current assets $ 135,000 $ 90,000 $ 45,000 Long-lived assets (including land) 50,000 50,000 50,000 Total assets $ 185,000 $ 140,000 $ 95,000 Liabilities and Stockholders' Equity Liabilities $ 35,000 $ 35,000 $ 35,000 Stockholders' equity 150,000 105,000 60,000 Total liabilities & stockholders' equity $ 185,000 $ 140,000 $ 95,000

(2) Amortized over two years: Income Statement

2014 2013 2012

Revenues $ 65,000 $ 65,000 $ 65,000 Amortization 0 20,000 20,000 Other expenses 20,000 20,000 20,000 Net income $ 45,000 $ 25,000 $ 25,000

Balance Sheet 12/31/14 12/31/13 12/31/12

Assets Current assets $ 135,000 $ 90,000 $ 45,000 Long-lived assets (including land) 50,000 50,000 70,000 Total assets $ 185,000 $ 140,000 $ 115,000

Liabilities and Stockholders' Equity Liabilities $ 35,000 $ 35,000 $ 35,000 Stockholders' equity 150,000 105,000 80,000 Total liabilities & stockholders' equity $ 185,000 $ 140,000 $ 115,000 (3) Amortized over three years:

Income Statement 2014 2013 2012

Revenues $ 65,000 $ 65,000 $ 65,000 Amortization 13,334 13,333 13,333 Other expenses 20,000 20,000 20,000 Net income $ 31,666 $ 31,667 $ 31,667

Balance Sheet 12/31/14 12/31/13 12/31/12

Assets Current assets $ 135,000 $ 90,000 $ 45,000 Long-lived assets (including land) 50,000 63,334 76,667 Total assets $ 185,000 $ 153,334 $ 121,667

Liabilities and Stockholders' Equity Liabilities $ 35,000 $ 35,000 $ 35,000 Stockholders' equity 150,000 118,334 86,667 Total liabilities & stockholders' equity $ 185,000 $ 153,334 $ 121,667

b. 2014 2013 2012 Total

Method 1: $45,000 $45,000 $ 5,000 $95,000

Method 2: 45,000 25,000 25,000 95,000

Method 3: 31,666 31,667 31,667 95,000

c. The balance sheets under all three methods report identical amounts for each balance sheet account. Since the asset was fully amortized by December 31, 2014, the method used to amortize the asset does not affect the amounts reported on the balance sheet as of December 31, 2014.

E9–7

a. An asset's book value equals the asset's initial capitalized value less the associated accumulated depreciation. With straight-line depreciation, accumulated depreciation equals depreciation expense per year times the number of years the asset has been used. Therefore, the asset's book value would be calculated as follows:

Depreciation expense per year = (Cost – Salvage Value) ÷ Useful Life = ($60,000 – $12,000) ÷ 5 years = $9,600 per year Book Value = Capitalized Cost – Accumulated Depreciation

= $60,000 – ($9,600 3 years)

= $31,200

b. Depreciation Expense = [(Cost – Accumulated Depreciation) – Salvage Value] ÷ Remaining Useful Life

= (Book value – Salvage value) ÷ Remaining useful life = ($31,200 – $12,000) ÷ 5 remaining years = $3,840

Depreciation Expense (E, –SE) ....................................................... 3,840

Accumulated Depreciation (–A) ................................................. 3,840

Depreciated asset for 2011.

E9–9

a. (1) Straight-line depreciation:

Depreciation per Year = (Cost – Salvage Value) ÷ Useful Life

= ($300,000 – $60,000) ÷ 4 years

= $60,000 per year for 2011, 2012, 2013, and 2014

(2) Double-declining-balance depreciation:

Depreciation Depreciation Accumulated Book

Date Factor Expense Cost Depreciation Value

1/1/11 $300,000 $ 0 $300,000

12/31/11 50% $150,000a 300,000 150,000 150,000

12/31/12 50% 75,000 300,000 225,000 75,000

12/31/13 50% 15,000b 300,000 240,000 60,000

12/31/14 50% 0 300,000 240,000 60,000

_____________ a Depreciation Expense = Book Value at Beginning of the Period Depreciation Factor b Book Value Depreciation Factor = $75,000 50% = $37,500. If Benick Industries

depreciated $37,500 in 2013, the asset's book value would drop below its salvage value. To prevent this from happening, depreciation expense for 2013 can be only $15,000.

b. A manager should consider the costs and benefits associated with each depreciation method.

The most likely benefit is the impact of depreciation methods on income taxes. An accelerated method decreases the present value of tax payments. However, since there is no requirement that a company use the same depreciation method for financial reporting purposes as it does for tax reporting, tax considerations are not an issue for financial reporting. A manager should also consider the bookkeeping costs associated with each method. However, with computers the bookkeeping costs should be relatively consistent across methods. Finally, since the choice of depreciation methods affects net income, managers might consider the impact of the different depreciation methods on contracts such as debt covenants and incentive compensation contracts. Comparability with other firms in the same industry may also be a factor.

E9–10

a. Computer System (+A) .................................................................... 335,000

Cash (–A) ........................................................................... 335,000

Purchased computer system.

Note: Capitalizing the $10,000 of training costs could be debated. But, without incurring these costs, the computer system would not be in a serviceable condition. Hence, the training costs meet the requirement to be capitalized as part of the fixed asset.

b. (1) Straight-line depreciation:

Depreciation per Year = (Cost – Salvage Value) ÷ Useful Life

= ($335,000 – $70,000) ÷ 5 years

= $53,000 per year for 2011, 2012, 2013, 2014, and 2015

(2) Double-declining-balance depreciation:

Depreciation Depreciation Accumulated Book

Date Factor Expense Cost Depreciation Value

1/1/11 $335,000 $ 0 $335,000

12/31/11 40% $134,000a 335,000 134,000 201,000

12/31/12 40% 80,400 335,000 214,400 120,600

12/31/13 40% 48,240 335,000 262,640 72,360

12/31/14 40% 2,360b 335,000 265,000 70,000

12/31/15 40% 0 335,000

____________ a Depreciation expense = Book value at beginning of the period Depreciation factor b Book value Depreciation factor = $72,360 40% = $28,944. If Stockton Corporation

depreciated $28,944 in 2014, the asset's book value would drop below its salvage value. To prevent this from happening, depreciation expense for 2014 can be only $2,360.

c. Depreciation Expense (E, –SE)................................................. 134,000

Accumulated Depreciation (–A) ......................................... 134,000

Depreciated fixed asset for 2011.

E9–11

1. Activity Method: Depreciation Expense per Mile = ($100,000 – $20,000) ÷ 200,000 Miles = $0.4/Mile

Depreciation Expense (E, –SE) ....................................................... 19,200

Accumulated Depreciation (–A) ................................................. 19,200

Depreciated asset for 2011.

Depreciation Expense (E, –SE) ....................................................... 14,000

Accumulated Depreciation (–A) ................................................. 14,000

Depreciated asset for 2012.

Depreciation Expense (E, –SE) ....................................................... 16,000

Accumulated Depreciation (–A) ................................................. 16,000

Depreciated asset for 2013.

Depreciation Expense (E, –SE) ....................................................... 10,000

Accumulated Depreciation (–A) ................................................. 10,000

Depreciated asset for 2014.

Depreciation Expense (E, –SE) ....................................................... 14,000

Accumulated Depreciation (–A) ................................................. 14,000

Depreciated asset for 2015.

Depreciation Expense (E, –SE) ....................................................... 4,000

Accumulated Depreciation (–A) ................................................. 4,000

Depreciated asset for 2016.

Cash (+A) ........................................................................................ 12,000

Accumulated Depreciation (+A) ....................................................... 77,200

Loss on Sale of Truck (Lo, –SE) ...................................................... 10,800

Truck (–A) .................................................................................. 100,000

Sold truck.

2. Straight-line Method: Depreciation Expense per Year = ($100,000 – $20,000) ÷ 5 Years = $16,000/year

Depreciation Expense (E, –SE) ....................................................... 16,000

Accumulated Depreciation (–A) ................................................. 16,000

Depreciated asset. Note: This entry would be made each year for five years. No entry would be made in Year 6

since the truck's estimated useful life ended at the end of Year 5, which means that the truck would have been depreciated down to its estimated salvage value.

Cash (+A) ....................................................................................... 12,000

Accumulated Depreciation (+A) ....................................................... 80,000

Loss on Sale of Truck (Lo, –SE) ...................................................... 8,000

Truck (–A) ................................................................................ 100,000

Sold truck.

E9–12

a. Depletion (E, –SE) ........................................................................... 1,200,000*

Oil Deposits (–A) ....................................................................... 1,200,000

Depleted oil deposits. __________

* $1,200,000 = ($4,000,000 ÷ 100,000 barrels) 30,000 barrels extracted

b. Depletion (E, –SE) ........................................................................... 2,000,000*

Oil Deposits (–A) ....................................................................... 2,000,000

Depleted oil deposits. __________

* $2,000,000 = ($4,000,000 ÷ 100,000 barrels) 50,000 barrels extracted

c. $800,000

E9–14

a. Cash (+A) ....................................................................................... 235,000

Accumulated Depreciation—Office Equipment (+A) ....................... 300,000

Office Equipment (–A) ............................................................... 500,000

Gain on Sale of Fixed Assets (Ga, +SE) ................................... 35,000

Sold office equipment.

b. Cash (+A) ........................................................................................ 185,000

Accumulated Depreciation—Office Equipment (+A) ....................... 300,000

Loss on Sale of Fixed Assets (Lo, –SE) .......................................... 15,000

Office Equipment (–A) ............................................................... 500,000

Sold office equipment.

E9–15

Assuming that Paris Company kept the equipment for its entire five-year estimated useful life, the

depreciation schedule on the equipment would be as follows.

Depreciation Depreciation Accumulated Book

Date Factor Expense Cost Depreciation Value

1/1/09 $25,000 $ 0 $25,000

12/31/09 40% $10,000 25,000 10,000 15,000

12/31/10 40% 6,000 25,000 16,000 9,000

12/31/11 40% 3,600 25,000 19,600 5,400

12/31/12 40% 400* 25,000 20,000 5,000

12/31/13 40% 0 25,000 20,000 5,000

__________________

* Because the equipment's book value cannot drop below its estimated salvage value, depreciation

expense for 2012 cannot exceed $400.

a. Accumulated Depreciation—Equipment (+A) .................................. 19,600

Loss on Disposal of Equipment (Lo, –SE) ....................................... 5,400

Equipment (–A) .......................................................................... 25,000

Disposed of equipment.

b. Accumulated Depreciation—Equipment (+A) .................................. 20,000

Loss on Disposal of Equipment (Lo, –SE) ....................................... 5,000

Equipment (-A)........................................................................... 25,000

Disposed of equipment.

c. Cash (+A) ....................................................................................... 8,000

Accumulated Depreciation—Equipment (+A) .................................. 19,600

Equipment (–A) .......................................................................... 25,000

Gain on Sale of Fixed Assets (Ga, +SE) ................................... 2,600

Sold equipment.

d. Fixed Asset (new) (+A) .................................................................... 30,000

Accumulated Depreciation—Equipment (+A) .................................. 20,000

Loss on Disposal of Fixed Asset (Lo, –SE) ..................................... 3,000

Cash (–A) ................................................................................... 28,000

Equipment (old) (–A) ................................................................. 25,000

Exchanged fixed assets.

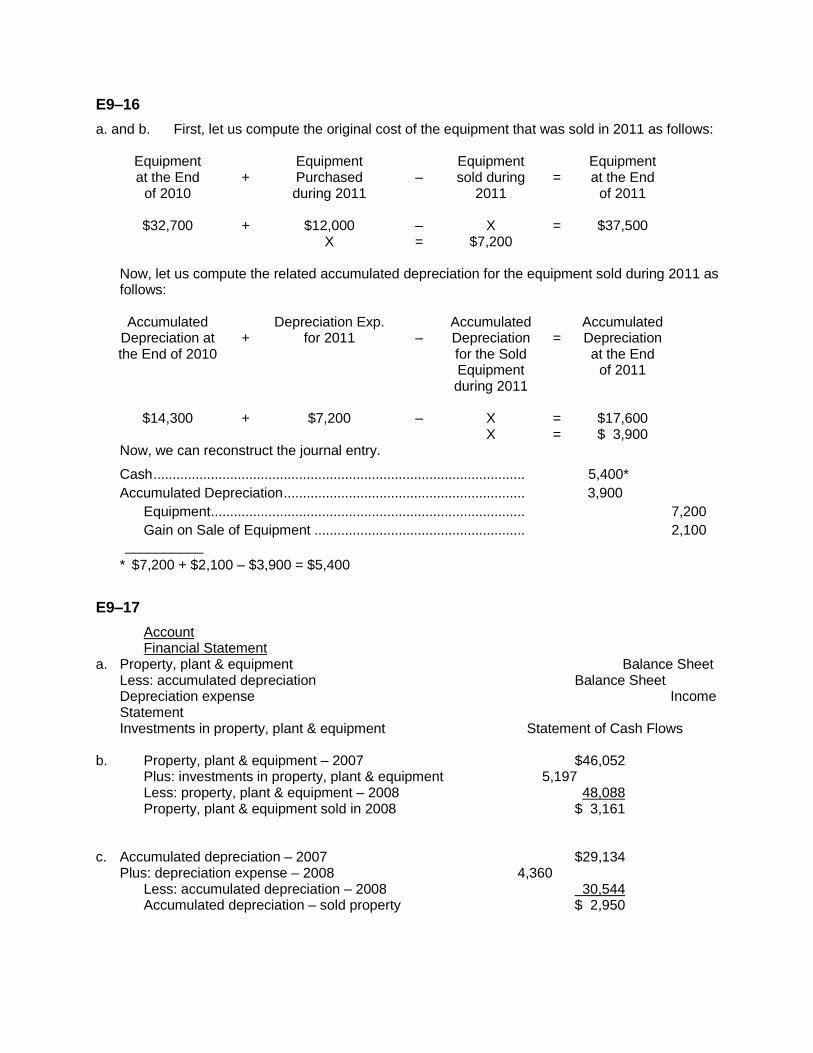

E9–16

a. and b. First, let us compute the original cost of the equipment that was sold in 2011 as follows: Equipment Equipment Equipment Equipment at the End + Purchased – sold during = at the End of 2010 during 2011 2011 of 2011 $32,700 + $12,000 – X = $37,500 X = $7,200 Now, let us compute the related accumulated depreciation for the equipment sold during 2011 as

follows: Accumulated Depreciation Exp. Accumulated Accumulated Depreciation at + for 2011 – Depreciation = Depreciation the End of 2010 for the Sold at the End Equipment of 2011 during 2011 $14,300 + $7,200 – X = $17,600 X = $ 3,900 Now, we can reconstruct the journal entry. Cash ................................................................................................. 5,400*

Accumulated Depreciation ............................................................... 3,900

Equipment .................................................................................. 7,200

Gain on Sale of Equipment ....................................................... 2,100 __________

* $7,200 + $2,100 – $3,900 = $5,400

E9–17

Account Financial Statement

a. Property, plant & equipment Balance Sheet Less: accumulated depreciation Balance Sheet Depreciation expense Income Statement Investments in property, plant & equipment Statement of Cash Flows

b. Property, plant & equipment – 2007 $46,052 Plus: investments in property, plant & equipment 5,197 Less: property, plant & equipment – 2008 48,088 Property, plant & equipment sold in 2008 $ 3,161 c. Accumulated depreciation – 2007 $29,134

Plus: depreciation expense – 2008 4,360 Less: accumulated depreciation – 2008 30,544 Accumulated depreciation – sold property $ 2,950

E9–17 Concluded d. Compute the gain on the sale:

Cost of property sold $3,161 Less: accumulated depreciation 2,950 Book value of property sold $ 211 Sales price of property $100 Less: book value of property 211 Loss on sale of property $111 This loss on sale of property would appear on the income statement.

E9–18

a. First, let us compute the related accumulated depreciation for the equipment sold during 2011 as follows:

Accumulated Depreciation Cap. Accumulated Accumulated Depreciation at + for 2011 – Depreciation = Depreciation the End of 2010 for the Sold at the End Equipment of 2011 during 2011 $9,800 + $3,800 – X = $10,500 X = $ 3,100 Now, we can reconstruct the journal entry. Cash ................................................................................................. 4,300

Loss on Sale of Equipment .............................................................. 900

Accumulated Depreciation ............................................................... 3,100

Equipment .................................................................................. 8,300

b. Equipment Equipment Equipment Equipment at the End + Purchased – sold during = at the End of 2010 during 2011 2011 of 2011 $23,400 + X – $8,300 = $26,900 X = $11,800

__________ Equipment purchased during 2011 = $11,800

E9–20

a. (1) Southern Robotics should report the costs incurred in acquiring the patent as an asset.

Therefore, the $50,000 of legal and filing fees should be capitalized as an asset in 2011. Since it is company policy not to amortize intangible assets in the year of acquisition, the company would report the entire $50,000 as an asset as of December 31, 2011.

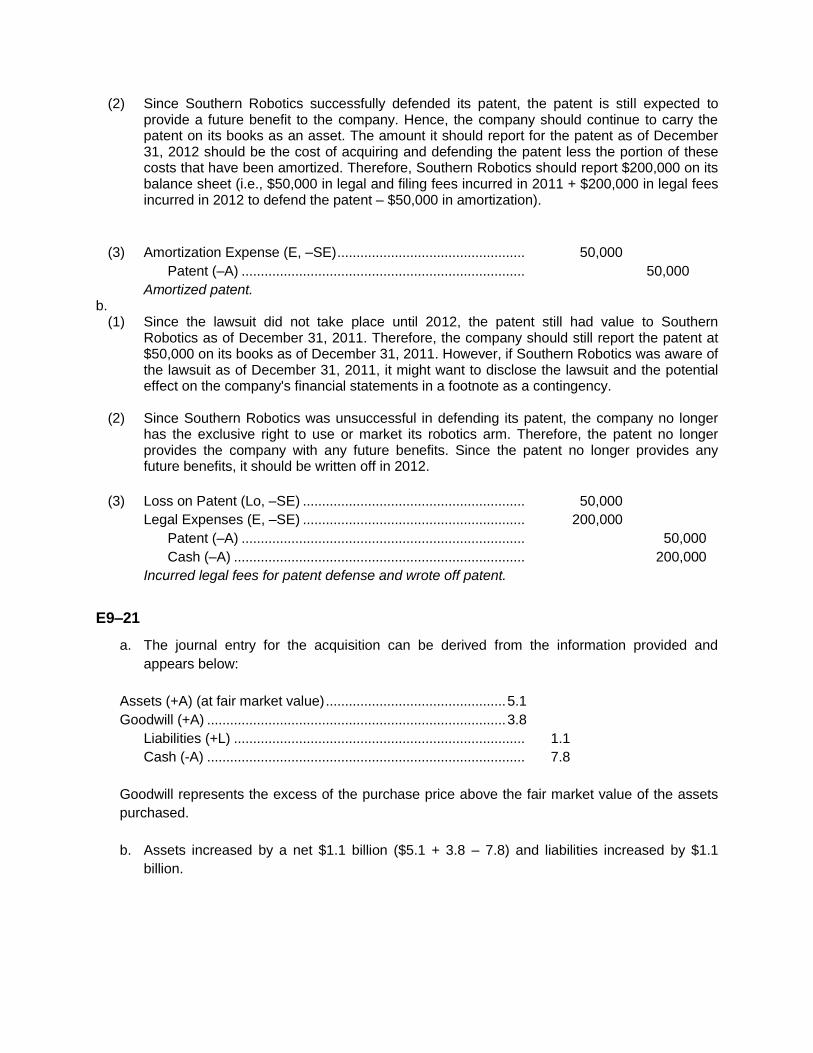

(2) Since Southern Robotics successfully defended its patent, the patent is still expected to provide a future benefit to the company. Hence, the company should continue to carry the patent on its books as an asset. The amount it should report for the patent as of December 31, 2012 should be the cost of acquiring and defending the patent less the portion of these costs that have been amortized. Therefore, Southern Robotics should report $200,000 on its balance sheet (i.e., $50,000 in legal and filing fees incurred in 2011 + $200,000 in legal fees incurred in 2012 to defend the patent – $50,000 in amortization).

(3) Amortization Expense (E, –SE) ................................................. 50,000

Patent (–A) .......................................................................... 50,000

Amortized patent. b.

(1) Since the lawsuit did not take place until 2012, the patent still had value to Southern Robotics as of December 31, 2011. Therefore, the company should still report the patent at $50,000 on its books as of December 31, 2011. However, if Southern Robotics was aware of the lawsuit as of December 31, 2011, it might want to disclose the lawsuit and the potential effect on the company's financial statements in a footnote as a contingency.

(2) Since Southern Robotics was unsuccessful in defending its patent, the company no longer

has the exclusive right to use or market its robotics arm. Therefore, the patent no longer provides the company with any future benefits. Since the patent no longer provides any future benefits, it should be written off in 2012.

(3) Loss on Patent (Lo, –SE) .......................................................... 50,000

Legal Expenses (E, –SE) .......................................................... 200,000

Patent (–A) .......................................................................... 50,000

Cash (–A) ............................................................................ 200,000

Incurred legal fees for patent defense and wrote off patent.

E9–21

a. The journal entry for the acquisition can be derived from the information provided and

appears below:

Assets (+A) (at fair market value) ............................................... 5.1

Goodwill (+A) .............................................................................. 3.8

Liabilities (+L) ............................................................................ 1.1

Cash (-A) ................................................................................... 7.8

Goodwill represents the excess of the purchase price above the fair market value of the assets

purchased.

b. Assets increased by a net $1.1 billion ($5.1 + 3.8 – 7.8) and liabilities increased by $1.1

billion.

PROBLEMS

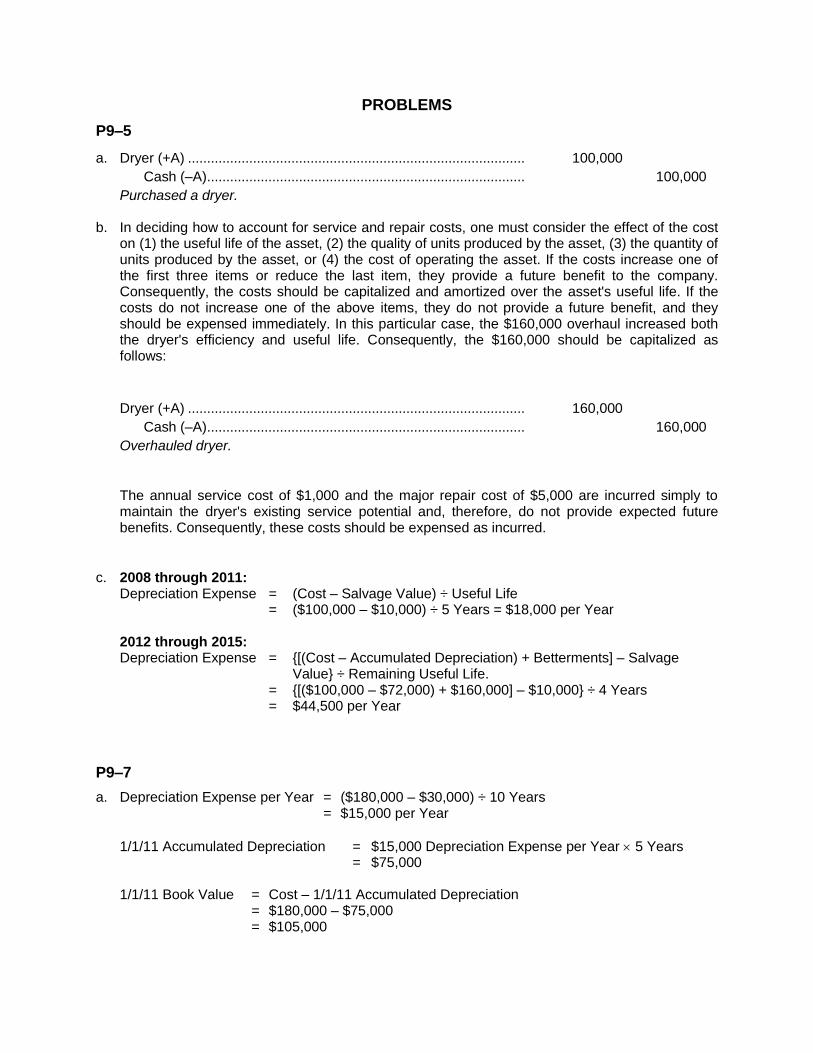

P9–5

a. Dryer (+A) ........................................................................................ 100,000

Cash (–A) ................................................................................... 100,000

Purchased a dryer.

b. In deciding how to account for service and repair costs, one must consider the effect of the cost on (1) the useful life of the asset, (2) the quality of units produced by the asset, (3) the quantity of units produced by the asset, or (4) the cost of operating the asset. If the costs increase one of the first three items or reduce the last item, they provide a future benefit to the company. Consequently, the costs should be capitalized and amortized over the asset's useful life. If the costs do not increase one of the above items, they do not provide a future benefit, and they should be expensed immediately. In this particular case, the $160,000 overhaul increased both the dryer's efficiency and useful life. Consequently, the $160,000 should be capitalized as follows:

Dryer (+A) ........................................................................................ 160,000

Cash (–A) ................................................................................... 160,000

Overhauled dryer.

The annual service cost of $1,000 and the major repair cost of $5,000 are incurred simply to maintain the dryer's existing service potential and, therefore, do not provide expected future benefits. Consequently, these costs should be expensed as incurred.

c. 2008 through 2011: Depreciation Expense = (Cost – Salvage Value) ÷ Useful Life = ($100,000 – $10,000) ÷ 5 Years = $18,000 per Year 2012 through 2015: Depreciation Expense = {[(Cost – Accumulated Depreciation) + Betterments] – Salvage

Value} ÷ Remaining Useful Life. = {[($100,000 – $72,000) + $160,000] – $10,000} ÷ 4 Years = $44,500 per Year

P9–7

a. Depreciation Expense per Year = ($180,000 – $30,000) ÷ 10 Years = $15,000 per Year

1/1/11 Accumulated Depreciation = $15,000 Depreciation Expense per Year 5 Years = $75,000 1/1/11 Book Value = Cost – 1/1/11 Accumulated Depreciation = $180,000 – $75,000 = $105,000

b. Depreciation Expense (E, –SE) ....................................................... 9,375

Accumulated Depreciation (–A) ................................................. 9,375

Depreciated fixed assets. _____________

*$9,375 = (Book Value of $105,000 – Salvage Value of $30,000) ÷ Remaining Useful Life of 8 Years

P9–9

a. Every depreciation method depreciates the same amount over the useful life of a fixed asset. Depreciation methods only vary the timing of depreciation charges. Therefore, both the straight-line method and the double-declining-balance method will give rise to the same total amount of depreciation over the four-year useful life of this equipment. The following table shows that the total depreciation under the two methods is the same.

Method Year 1 Year 2 Year 3 Year 4 Total

Straight-linea $15,000 $15,000 $15,000 $15,000 $60,000

Double-declining-balanceb 40,000 20,000 0 0 60,000

_____________ a $15,000 = ($80,000 – $20,000) ÷ 4 years

b Depreciation Depreciation Historical Accumulated Book

Date Factor Expense Cost Depreciation Value

1/1/11 $80,000 $ 0 $80,000

12/31/11 50% $40,000 80,000 40,000 40,000

12/31/12 50% 20,000 80,000 60,000 20,000

12/31/13 50% 0 80,000 60,000 20,000

12/31/14 50% 0 80,000 60,000 20,000

b. Since, as demonstrated in part (a), both depreciation methods give rise to the same total amount of depreciation over the fixed asset’s life, the total amount of net income over the asset’s life must also be the same. Therefore, the total amount of taxes will be the same regardless of which depreciation method a company selects. The following shows that the total amount of net income and taxes are the same under the two methods.

Straight-line method:

Method Year 1 Year 2 Year 3 Year 4 Total

Revenues $ 100,000 $ 100,000 $ 100,000 $ 100,000 $ 400,000

Depreciation exp. 15,000 15,000 15,000 15,000 60,000

Other expenses 60,000 60,000 60,000 60,000 240,000

Pretax income $ 25,000 $ 25,000 $ 25,000 $ 25,000 $ 100,000

Income taxes 8,750 8,750 8,750 8,750 35,000

Net income $ 16,250 $ 16,250 $ 16,250 $ 16,250 $ 65,000

Double-declining-balance:

Method Year 1 Year 2 Year 3 Year 4 Total

Revenues $ 100,000 $ 100,000 $ 100,000 $ 100,000 $ 400,000

Depreciation exp. 40,000 20,000 0 0 60,000

Other expenses 60,000 60,000 60,000 60,000 240,000

Pretax income $ 0 $ 20,000 $ 40,000 $ 40,000 $ 100,000

Income taxes 0 7,000 14,000 14,000 35,000

Net income $ 0 $ 13,000 $ 26,000 $ 26,000 $ 65,000

c. The double-declining-balance method is preferred for tax purposes because this method defers tax payments. Under this depreciation method, more depreciation is taken in the early years of an asset’s life than in later years. Increasing depreciation in an asset’s early life reduces taxable income which, in turn, reduces income taxes in the early years of the asset’s life [see part b]. The reduction in income taxes in the early years of the asset’s life is offset by higher taxes in the later years of an asset’s life. However, due to the time value of money, deferring taxes is beneficial.

d. Straight-line method:

Present Value = $8,750 from part (b) Present Value of an Ordinary Annuity Factor for i = 10% and n = 4

= $8,750 3.16987 (from Table 5) = $27,736.36

Double-declining-balance method:

Present Value = ($7,000 Present Value Factor for i = 10% and n = 2) + ($14,000

Present Value Factor for i = 10% and n = 3) + ($14,000 Present Value Factor for i = 10% and n = 4)

= ($7,000 0.82645) + ($14,000 0.75131) + ($14,000 0.68301) = $5,785.15 + $10,518.34 + $9,562.14 = $25,865.63 In present value terms, Kimberly Sisters would save $1,870.73 ($27,736.36 – $25,865.63) in

taxes on this one asset by selecting the double-declining-balance method over the straight-line method.

P9–11

a. Drilling Equipment (+A) .................................................................... 800,000

Mobile Home (+A) ............................................................................ 54,000

Cash (–A) ................................................................................... 854,000

Purchased assets for drilling fields.

b.

2011:

Depletion (E, –SE) ........................................................................... 240,000*

Drilling Equipment (or Accumulated Depletion) (–A) ................ 240,000

Depleted drilling equipment. __________

*$240,000 = ($800,000 ÷ 2,000,000 barrels) 600,000 barrels

2012:

Depletion (E, –SE) ........................................................................... 300,000*

Drilling Equipment (or Accumulated Depletion) (–A) ................ 300,000

Depleted drilling equipment. __________

*$300,000 = ($800,000 ÷ 2,000,000 barrels) 750,000 barrels

2013:

Depletion (E, –SE) ........................................................................... 260,000*

Drilling Equipment (or Accumulated Depletion) (–A) ................ 260,000

Depleted drilling equipment. __________

*$260,000 = ($800,000 ÷ 2,000,000 barrels) 650,000 barrels

c. 2011:

Depreciation Expense (E, –SE) ....................................................... 7,000*

Accumulated Depreciation (–A) ................................................. 7,000

Depreciated mobile home.

2012:

Depreciation Expense (E, –SE) ....................................................... 7,000*

Accumulated Depreciation (–A) ................................................. 7,000

Depreciated mobile home.

2013:

Depreciation Expense (E, –SE) ....................................................... 7,000*

Accumulated Depreciation (–A) ................................................. 7,000

Depreciated mobile home. __________

*$7,000 = ($54,000 – $5,000) ÷ 7 years

Different methods are used to allocate the costs of the drilling equipment and the mobile home based upon the link between the asset and the oil field. The drilling equipment is site-specific. Hence, its useful life is identical to the productive life of the oil field. Under the matching principle, the activity method provides the best matching of the costs with the associated benefits. On the other hand, the mobile home is not site-specific; it has a useful life beyond this oil field. The activity method would not be appropriate for the mobile home because the productive capabilities of future oil fields on which the mobile home may be used are not yet known. Consequently, Garmen Oil Company must select either the straight-line method or an accelerated method to depreciate the mobile home.

d. Depletion: 2011:

Depletion (E, –SE) ........................................................................... 240,000

Drilling Equipment (or Accumulated Depletion) (–A) ................ 240,000

Depleted drilling equipment.

2012:

Depletion (E, –SE) ........................................................................... 300,000

Loss on Oil Field (Lo, –SE) .............................................................. 260,000*

Drilling Equipment (or Accumulated Depletion) (–A) ................ 560,000

Depleted drilling equipment. __________

* Since the well is dry, the drilling equipment will not provide any future benefits; hence, the

remaining cost of $260,000 [($800,000 – ($240,000 + $300,000)] should be written off.

2013: No journal entries are necessary.

Depreciation: Since the mobile home is not site-specific, the entries for depreciation would be the same as in part (c).

P9–13

a. Most assets are reported on the balance sheet at historical cost or at historical cost less accumulated depreciation. The historical cost of a particular asset is constant over time. However, the fair market value of that same asset fluctuates over time. Consequently, the fair market value of assets can be less than, equal to, or greater than the historical cost of the assets at any point in time.

b. Diversified would pay more for Specialists due to goodwill (i.e., synergy). Specialists' assets considered as a package are worth more than the sum of their individual values. Goodwill arises because certain "assets" are not included on a company's balance sheet. Items that cannot be given a value (i.e., cannot be quantified) are omitted from a balance sheet. Examples include customer loyalty and the company's name recognition.

c. Assets (+A) ...................................................................................... 1,350,000

Goodwill (+A) ................................................................................... 700,000

Liabilities (+L) ............................................................................ 250,000

Cash (–A) ................................................................................... 1,800,000

Purchased Specialists, Inc.

d. Until recently under GAAP, goodwill was capitalized at the time of acquisition and then amortized over a maximum of 40 years. The school of thought holding the opposite viewpoint espouses that goodwill should be expensed at the time of acquisition. They maintain that since goodwill is a plug number on the books of the acquired company and its amortization period is totally arbitrary, it need not be put on the balance sheet. Further, goodwill should be periodically tested to see if it has been “impaired” (i.e., if the fair value of the assets acquired has dropped).

ISSUES FOR DISCUSSION

ID9–3

a. The main issue to be considered is whether the capital expenditure is a betterment or simply maintenance. To be considered a betterment, the expenditure must (1) increase the asset's useful life, (2) increase the quality of the asset's output, (3) increase the quantity of the asset's output, or (4) reduce the cost associated with operating the asset. If the expenditure meets one of these criteria, the expenditure should be capitalized. Otherwise, the expenditure should be expensed.

b. The amount may be immaterial.

c. Depreciation per year represents the remaining net cost of an asset allocated over the asset's estimated remaining useful life. In this particular case, the remaining net cost equals the sum of the asset's book value at the time of refurbishment and the cost of the refurbishment less the estimated salvage value of the plant. This amount would be depreciated over the estimated useful life of the "new" plant.

ID9–5

One of the underlying goals of an accounting system is to properly match revenues with expenses. There are many advertising and research & development costs that will help to produce revenue for the company over multiple periods. If the company expenses all of these expenses in the first year, then net income for the first year will be understated and then overstated in future years when the revenue produced is not matched with the expenses

incurred to generate it. At the same time it is very difficult to determine a rational way to allocate these costs to the revenue that it produces. When these costs are incurred it is extremely difficult to know the revenue, if any, that will be produced in future periods. The capitalization of software development costs has the opposite effect. Expenses that are incurred in the current year will not impact the income statement this year but will in future years. The predictability of the future value of software is higher than for advertising and research and development costs. Management, separate from any desires to influence the stock price, will generally want to match its expenses with the revenues that these expenses produce. Management wants to be able to evaluate the impact of both its advertising and research & development costs. Shareholders may want to see a system of charging marketing expenses that will have the best impact on stock performance. In the early years of a company this may mean capitalizing heavy marketing from the early years and defering the expense until the company has higher levels of revenue to absorb these expenses. Management may also have an incentive to report higher net income, which could cause some managers to want to change accounting policies to work to their benefit. This speaks for the benefit of consistently applying accounting policies from year to year.

ID9–6

a. The effect on profits from increased capital spending will come from increased depreciation charges. Capitalized expenditures for fixed assets will eventually hit the income statement as depreciation expense.

b. The balance sheet will reflect growth in the property, plant and equipment, as well future growth

in the contra asset accumulated depreciation account. The income statement will show increased depreciation expense. And finally, the statement of cash flow will show greater uses of cash in the investing activities section.

c. The justification of management for the increased capital expenditures will be to remain

competitive in the marketplace. If businesses do not reinvest in the long-term assets of their operations, they will not be able to remain competitive. Spending the additional money for fixed assets will affect the financial statements today, but that spending will also keep the business viable into the future. The stockholders have to allow funds to be allocated for investing activities if they want to continue to receive a return on their investment in the company.

ID9–7

a. The most likely scenario causing a restaurant’s value to be impaired is a loss in the desirability of the location. If a McDonald’s restaurant was located at a certain intersection and traffic patterns in the city changed (due to a new interstate highway, for example), the restaurant will no longer be as attractive a location. McDonald’s therefore would have to adjust downward the carrying value for that restaurant.

b. McDonald’s will record the impairment by first determining the fair value of the asset. Then, the company will record an impairment expense and reduce the asset from its current carrying value down to the (new) fair value.

c. As with other expenses that are somewhat at management’s discretion, shareholders are

vulnerable if management decides to take an impairment expense in a year where earnings are otherwise very healthy, eliminating the need to take the expense in future years when earnings are less robust. A management team could lower current earnings (and thus future earnings expectations) by taking impairment charges in current periods.

ID9–9

a. The problem with using current costs is trying to determine what the current cost is. That is, how does one determine the current cost of a specialized piece of manufacturing equipment or the current cost of an office building in a slow-moving real estate market? This difficulty in determining current costs gives managers leeway to manipulate the amounts reported in the financial statements. If managers are given the opportunity to manipulate the financial statements through subjective current costs, then financial statement users will be wary of placing any reliance on the financial statements. Thus, current costs could potentially lead to the demise of financial statements.

b. Historical costs are sunk costs in that they represent the cost of an asset at the time the asset

was acquired; historical costs do not indicate the magnitude of cash or net assets that an asset will generate in the future. Since sunk costs are irrelevant for decision-making purposes, historical costs are not relevant for decision-making purposes. Alternatively, current costs provide a measure of the value of an asset today. For example, the amount reported for Cost of Goods Sold and Depreciation Expense under current cost represents the current values of the inventory sold during the period and of the fixed assets "consumed" during the accounting period, respectively. These values essentially represent what it would cost the company to replace the inventory it sold and the fixed assets it "consumed." In addition, the amounts reported on the balance sheet for inventory and fixed assets essentially represent what it would cost the company to replace its inventory and fixed assets, which is essentially the same value as what the company would realize if it sold the inventory and fixed assets. Thus, current cost information would be very relevant for decision-making purposes because it provides information about cash inflows the company could generate and about cash outflows the company is likely to make. In short, current cost information is very relevant for decision-making purposes.

c. The argument comes down to reliability versus relevancy. Current cost information is more

relevant than historical cost information, but it is considerably more difficult to objectively determine current costs than it is to determine historical costs. If individual financial statement users were able to dictate the valuation basis to be used in preparing financial statements, each individual would be able to determine his or her personal decision on the tradeoff between reliability and relevancy. However, financial statements are intended for general use, which means that the same financial statements will be used by a variety of people. Historically, reliability has been given more importance than relevancy because (1) relevant information is not very useful if you are not sure you can rely on the information and (2) managers and auditors are legally liable to financial statement users. That is, they are uneasy about providing information that might be subjective because it could greatly increase their legal exposure.

ID9–10

a. Asset write-downs allow Kellogg to manage earnings by reducing depreciation expenses in future periods. If Kellogg has a good quarter and decides to write down an asset this lowers the book value of the asset and thereby reduces the amount of depreciation expense that will be incurred in future periods.

b. The accounting profession in general tends to prefer conservative accounting practices. By

carrying the value of assets at a lower value, the auditors reduce their risk that if something goes wrong with the company that they will be sued. So if management makes estimates that reduce the value of assets, the auditors will be less likely to object.

c. The FASB has come out against this policy of “taking a bath” by companies when they have had

a really bad quarter to begin with. Some companies will then go ahead and write down assets so that in future periods the amount of depreciation will be reduced thereby improving reported

net income. While the write down of assets may be conservative, this approach violates the matching principle. The appropriate costs are not being matched with the related revenues in future periods.

ID9–11

a. The write-off of an outdated technology system would reduce assets and equity; equity is reduced because of the write-off expense, which reduces Retained Earnings through lower profits.

b. The most likely factor in determining that a system is overvalued is the introduction of new

technology products in the market that better meet the company’s needs. The old system, still carried on the balance sheet, is no longer as valuable because of the technological updates of the new systems.

c. Management could decide to take the write-off expense in a year where earnings are

otherwise very healthy, eliminating the need to take the expense in future years when earnings are less robust. A management team could lower current earnings (and thus future earnings expectations) by taking the write-off charge in the current period.

ID9–13

a. Property, plant and equipment make up 14.8% ($1,957.7/$13,249.6) of total assets. Other long-lived assets make up 11.8% ($1,557.9/$13,249.6) of total assets.

b. According to Note 3, Machinery and Equipment is the largest category within property, plant and equipment.

c. Depreciation expense (from the Statement of Cash Flow) is 1.7% ($335.0/$19,176.1) of Net Revenue. Because depreciation is a non-cash expense, it is added back in the Statement of Cash Flow in the calculation of cash from operating activities.

d. According to Note 1, Nike depreciates its assets using the straight-line method. The

company uses 2 to 40 years for buildings and leasehold improvements, 2 to 15 years for machinery and equipment, and 3 to 10 years for computer software.

e. The company’s largest intangible asset is Trademarks.