chapter 8 capital gains: business related 1. capital gains: business avoidance – gaar capital...

TRANSCRIPT

Chapter 8

Capital Gains: Business Related

1

Capital Gains: Business

• Avoidance – GAAR

• Capital Receipt versus Income Receipt– Primary intention– Secondary intention– Badges of trade or behavioural factors

2

Reserves

• Taxpayer may not receive full proceeds in year of disposition

• Deferral of portion of gain realized available through claiming a reserve

• Reserve is lesser of:

a) × Gain = Reasonable reserve

b) (1/5 of Gain) × (4 – # of Preceding taxation years ending after disposition)

Proceeds not yet dueTotal proceeds

3

ACB and Capital Cost• Adjusted Cost Base (ACB) defined as cost plus or

minus legislated adjustments• Adjustments include:

– Cost base of land increased by interest and property taxes denied

– Denied reasonable costs of surveying or valuing property added to cost of property

– Cost of property reduce by government assistance

• Exception: ACB of depreciable property is only its capital cost (no adjustments)

4

Non-Arm’s Length Transfer of Depreciable Property

• Undepreciated capital cost (UCC) to acquirer will equal:– UCC of transferor if no election is made on the

interspousal transfer– Cost of the property to transferor immediately

prior to transfer + taxable capital gain on transfer if election is made on interspousal transfer

5

Foreign Exchange Gains and Losses

• If foreign exchange gain/loss from an income receipt, then full gain/loss included in business/property income

• If foreign exchange gain/loss from a capital receipt, then net capital gain/loss calculated in normal manner.– For individuals, net capital gain/loss is reduced by a

max. $200

6

Debts Established To Be Bad Debts

• Seller can elect to have disposed of the debt and to have reacquired it immediately at a cost of nil.Result: Capital loss to offset gain on disposition of

property represented in the debt.

7

Debts Established To Be Bad Debts

• Deemed disposition of shares of an insolvent corporation occurs to realize the capital loss if certain conditions are met [subpar. 50(1)(b)(iii)]

• Another deemed disposition for proceeds of disposition equal to ACB of shares before ssec. 50(1) deemed disposition if elected [ssec. 50(1.1)]

8

Replacement Property

• Basic deferral of some or all of the capital gain on property which is disposed of and subsequently replaced.

• Two types of disposition:– Involuntary– Voluntary

9

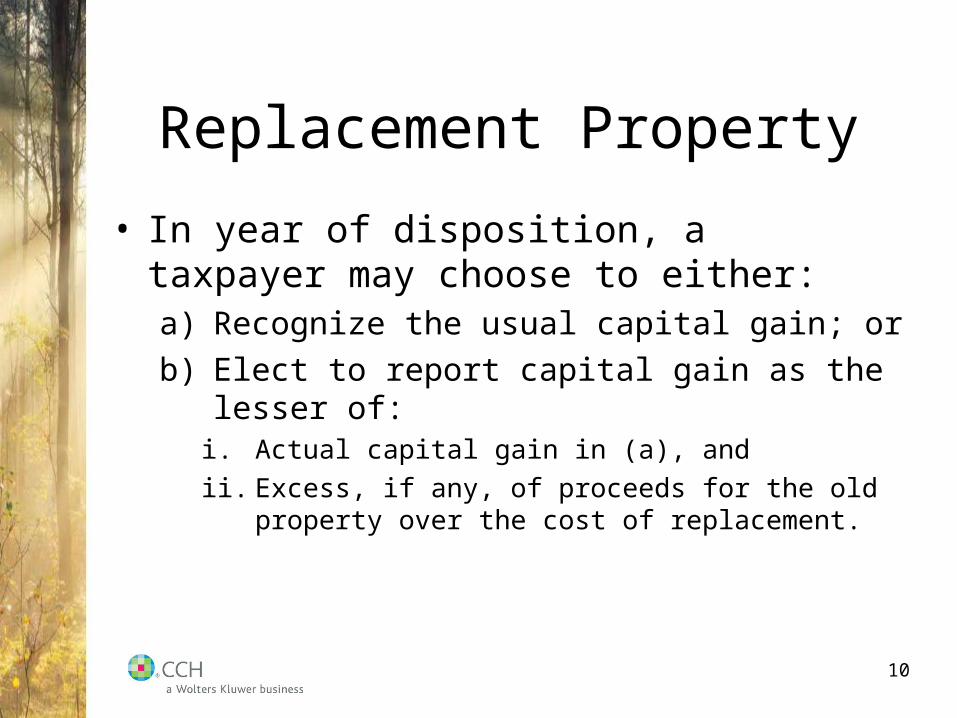

Replacement Property

• In year of disposition, a taxpayer may choose to either:a) Recognize the usual capital gain; or

b) Elect to report capital gain as the lesser of:i. Actual capital gain in (a), and

ii. Excess, if any, of proceeds for the old property over the cost of replacement.

10

Replacement Property

• To qualify for this election, the property must be replaced:a) Voluntary disposition – by later of the end of the first

taxation year after the year of disposition and 12 months after the end of the year of disposition; and

b) Involuntary disposition – by later of the end of the second taxation year after the year of disposition and 24 months after the end of the year of disposition.

11

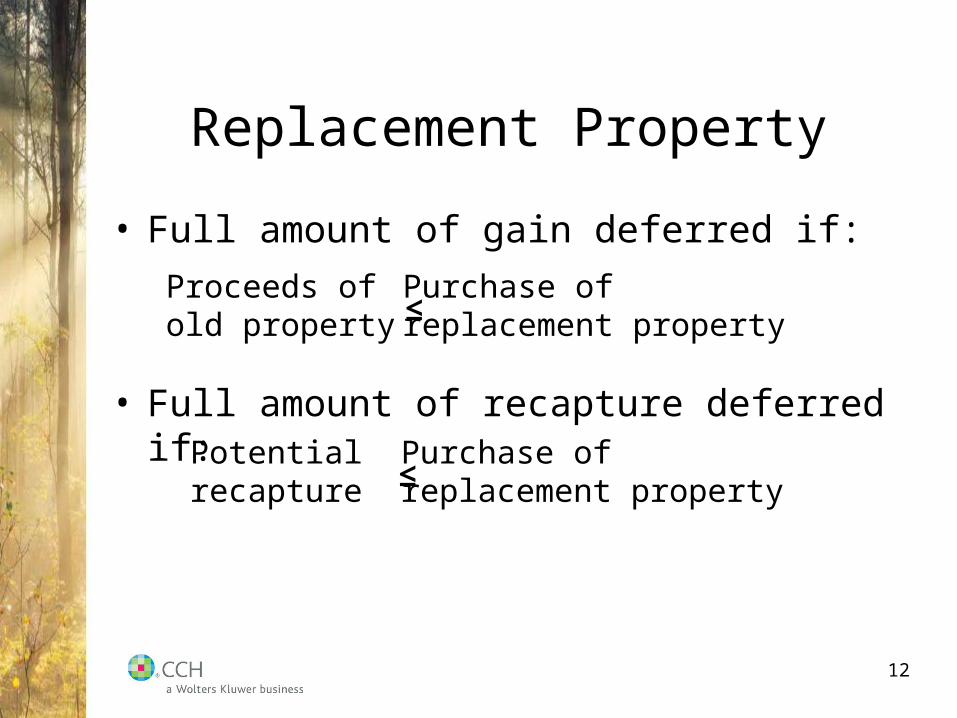

Replacement Property

• Full amount of gain deferred if:

• Full amount of recapture deferred if:

Proceeds of old property ≤

Purchase of replacement property

Potentialrecapture ≤

Purchase of replacement property

12

Disposal of Land and Building[ssec. 13(21.1)]

Is there a capital gain on the land and a terminal loss on the building?

• If so, an amount of terminal loss (but not greater than the capital gain) will reduce the proceeds on the land and increase the proceeds on the building.

• Effect: capital gain ↑ and terminal loss ↓

13

Disposition of Depreciable Property(If only one asset in class)

If P of D* > ACB:

Capital gain = P of D – ACB

Recapture = ACB – UCC

If P of D < ACB but > UCC:

Recapture = P of D – UCC

If P of D < UCC:

Terminal Loss = P of D - UCC

14*Proceeds of Disposition (P of D)

Disposition of Depreciable Property

Proceeds $100

Capital Cost $60

UCC $20

Capital Gain

Recapture

CGRecapture/

Terminal Loss

Proceeds $100 UCC $20

Cost (60) LOCP (60)

Capital Gain $40 Recapture $40

15

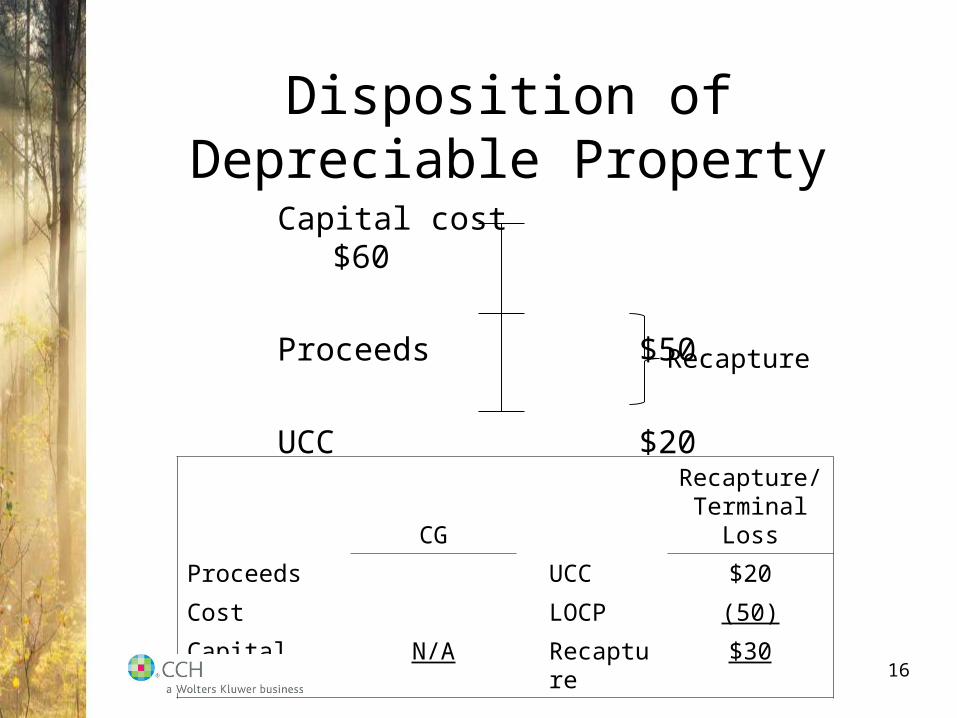

Disposition of Depreciable Property

Capital cost $60

Proceeds $50

UCC $20

Recapture

CGRecapture/

Terminal Loss

Proceeds UCC $20

Cost LOCP (50)

Capital Gain N/A Recapture $30

16

Disposition of Depreciable Property

Capital cost $60

UCC $20

Proceeds $5

Terminal loss

CG

Recapture/Terminal

Loss

Proceeds UCC $20

Cost LOCP (5)

Capital Gain N/A Terminal loss $1517

Disposition of Depreciable Property

• If there is more than one asset in the class:1. If Proceeds > ACB of asset, then there is a capital gain

and the lower of cost or proceeds is credited to the CCA class. If class then becomes negative, there is recapture. If there is a positive balance, then CCA continues to be claimed.

2. If proceeds < ACB, then the lower of cost or proceeds is credited to the CCA class. If class becomes negative, there is recapture. If class remains positive, then CCA continues to be claimed.

18

Change in Use

• On change in use of property, deemed to have sold property at FMV and reacquired same property at FMV (new ACB)

• If dual use, cost must be apportioned between uses.

• If percentage changes, proportionate deemed disposition

19

Election on Change in Use

• For personal-use property only, election to defer capital gain until taxpayer:– Decides to dispose of asset;

– Is deemed to dispose of asset; or

– Decides to rescind the election.

20

Income Reconciliation

• Major adjustment– Exclusion of book gains and losses– Inclusion of taxable capital gains and allowable

capital losses

21