chapter 7 accounting for intangibles. copyright 2003 mcgraw-hill new zealand pty ltd. ppts t/a new...

TRANSCRIPT

Chapter 7Chapter 7

Accounting for Accounting for intangiblesintangibles

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-22

ObjectivesObjectives

Understand what types of assets can Understand what types of assets can be considered as intangible assets, be considered as intangible assets, and the differences between intangible and the differences between intangible and tangible assets.and tangible assets.

Understand how to account for Understand how to account for research and development research and development expenditure and, in particular, be expenditure and, in particular, be aware of how to apply the tests for aware of how to apply the tests for deferral of research and development deferral of research and development expenditure.expenditure.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-33

Objectives (cont.)Objectives (cont.)

Be able to describe some empirical Be able to describe some empirical research that has been undertaken into research that has been undertaken into corporate research and development corporate research and development accounting practices.accounting practices.

Be able to define ‘goodwill’ and explain Be able to define ‘goodwill’ and explain how it is calculated for accounting how it is calculated for accounting purposes.purposes.

Be able to explain and apply the Be able to explain and apply the amortisation requirements applicable to amortisation requirements applicable to goodwill contained in FRS-36.goodwill contained in FRS-36.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-44

Objectives (cont.)Objectives (cont.)

Be aware of the controversies that Be aware of the controversies that arose as a result of the 1996 version of arose as a result of the 1996 version of the Australian goodwill accounting the Australian goodwill accounting standard.standard.

Be able to evaluate the deferral and Be able to evaluate the deferral and amortisation requirements of both the amortisation requirements of both the research and development and the research and development and the goodwill financial reporting standards.goodwill financial reporting standards.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-55

Objectives (cont.)Objectives (cont.)

Be aware of the brands and other Be aware of the brands and other internally generated intangible assets internally generated intangible assets debate, and how it applies in New debate, and how it applies in New Zealand.Zealand.

Be aware of some of the controversies Be aware of some of the controversies that arose as a result of the issue by that arose as a result of the issue by the Financial Reporting Standards the Financial Reporting Standards Board of Board of ED-87 ‘Accounting for Intangible ED-87 ‘Accounting for Intangible Assets’.Assets’.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-66

Intangible assetsIntangible assets

Non-monetary assets without Non-monetary assets without physical substance.physical substance.

Includes patents, goodwill, Includes patents, goodwill, mastheads, brand names, mastheads, brand names, copyrights, research and copyrights, research and development, and trademarks.development, and trademarks.

Intangible assets, as a category, Intangible assets, as a category, must be separately disclosed in the must be separately disclosed in the statement of financial position.statement of financial position.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-77

Identifiable versus Identifiable versus unidentifiable intangible unidentifiable intangible assetsassets

Identifiable intangible assetsIdentifiable intangible assets– a specific value can be placed on each a specific value can be placed on each

individual asset, and they can be individual asset, and they can be separately identified and sold.separately identified and sold.

– e.g. brand names, trademarks, research e.g. brand names, trademarks, research and development, patents, licences.and development, patents, licences.

Unidentifiable intangible assetsUnidentifiable intangible assets– intangible assets that cannot be intangible assets that cannot be

separately sold.separately sold.– e.g. goodwill.e.g. goodwill.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-88

Amortisation of Amortisation of intangiblesintangibles

Generally intangible assets have a Generally intangible assets have a limited life.limited life.

They should be amortised over their They should be amortised over their useful lives.useful lives.

SSAP-3 ‘Accounting for Depreciation’ SSAP-3 ‘Accounting for Depreciation’ remains applicable to certain remains applicable to certain intangible assets.intangible assets.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-99

Research and Research and developmentdevelopment Refer to FRS-13 ‘Accounting for Refer to FRS-13 ‘Accounting for

Research and Development Activities’.Research and Development Activities’. Research must be considered Research must be considered

separately from development.separately from development. Research defined asResearch defined as

– original and planned investigation original and planned investigation undertaken with the prospect of gaining undertaken with the prospect of gaining new scientific or technical knowledge and new scientific or technical knowledge and understanding.understanding.

Research costs must be recognised as Research costs must be recognised as an expense when incurred.an expense when incurred.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1010

Research and Research and development (cont.)development (cont.)

Development defined asDevelopment defined as– the application of research findings or other the application of research findings or other

knowledge to a plan or design for the knowledge to a plan or design for the production of new or substantially new production of new or substantially new improved materials, devices, products, improved materials, devices, products, processes, systems or services prior to the processes, systems or services prior to the commencement of commercial production or commencement of commercial production or use.use.

Development costs recognised as an Development costs recognised as an expense in the period incurred unless the expense in the period incurred unless the criteria for asset recognition are met.criteria for asset recognition are met.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1111

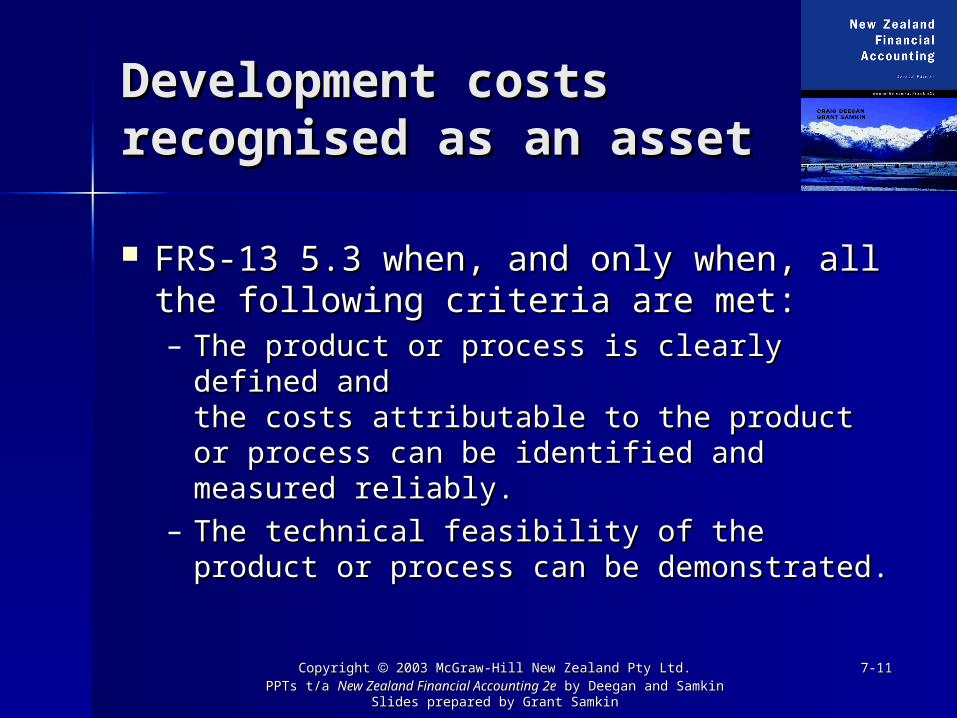

Development costs Development costs recognised as an assetrecognised as an asset

FRS-13 5.3 when, and only when, all FRS-13 5.3 when, and only when, all the following criteria are met:the following criteria are met:– The product or process is clearly defined The product or process is clearly defined

and and the costs attributable to the product or the costs attributable to the product or process can be identified and measured process can be identified and measured reliably.reliably.

– The technical feasibility of the product or The technical feasibility of the product or process can be demonstrated.process can be demonstrated.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1212

Development costs Development costs recognised as an asset recognised as an asset (cont.)(cont.)

FRS-13 5.3 when, and only when, all FRS-13 5.3 when, and only when, all the following criteria are met (cont.):the following criteria are met (cont.):– The entity intends to produce and market, The entity intends to produce and market,

or use, the product or process.or use, the product or process.– The existence of a market for the product The existence of a market for the product

or process or its usefulness to the entity, if or process or its usefulness to the entity, if it is to be used internally, can be it is to be used internally, can be demonstrated.demonstrated.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1313

Development costs Development costs recognised as an asset recognised as an asset (cont.)(cont.)

FRS-13 5.3 when, and only when, all FRS-13 5.3 when, and only when, all the following criteria are met (cont.):the following criteria are met (cont.):– Adequate resources exist, or their Adequate resources exist, or their

availability can be demonstrated, to availability can be demonstrated, to complete the project and market or use complete the project and market or use the product or process.the product or process.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1414

Costs included as part Costs included as part of research and of research and developmentdevelopment Salaries, wages and other related costs of Salaries, wages and other related costs of

personnel engaged in R&D activities.personnel engaged in R&D activities. Costs of materials and services consumed in Costs of materials and services consumed in

R&D activities.R&D activities. Depreciation of equipment and facilities used Depreciation of equipment and facilities used

in R&D.in R&D. Amortisation of other assets related to R&D.Amortisation of other assets related to R&D. Overhead costs related to specific R&D Overhead costs related to specific R&D

activities.activities. Other costs that can be attributed to R&D Other costs that can be attributed to R&D

activities, such as amortisation of patents.activities, such as amortisation of patents.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1515

Amortisation of Amortisation of development costsdevelopment costs

Any development costs must be Any development costs must be amortised and recognised as an amortised and recognised as an expense on a systematic basis.expense on a systematic basis.

Amortisation begins when the product Amortisation begins when the product or service is available for sale or use. or service is available for sale or use.

Amortisation period should not exceed Amortisation period should not exceed 5 years, unless a longer period, not 5 years, unless a longer period, not exceeding twenty years, can be exceeding twenty years, can be justified.justified.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1616

Amortisation of Amortisation of development costs development costs (cont.)(cont.) Development costs recognised as an Development costs recognised as an

asset should be reviewed annually to asset should be reviewed annually to ensure the carrying amount does not ensure the carrying amount does not exceed recoverable amount.exceed recoverable amount.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1717

Government grants for Government grants for research and research and developmentdevelopment

A grant received in relation to R&D A grant received in relation to R&D would meet the Statement of Concepts would meet the Statement of Concepts definition of revenue and should be definition of revenue and should be treated as such.treated as such.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1818

Empirical researchEmpirical research

Requirement to write-off R&D Requirement to write-off R&D expenditure caused smaller US R&D firms expenditure caused smaller US R&D firms to reduce to reduce R&D expenditure.R&D expenditure.

Requirement to write-off R&D may affect Requirement to write-off R&D may affect management decisions about R&D management decisions about R&D expenditure if management expenditure if management compensation based on profits.compensation based on profits.

May also be based on debt contract May also be based on debt contract covenants.covenants.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-1919

Disclosure requirementsDisclosure requirements

FRS-13 5.19 requires disclosure of:FRS-13 5.19 requires disclosure of:– the accounting policy adopted for R&D the accounting policy adopted for R&D

costscosts– amount of R&D costs recognised as an amount of R&D costs recognised as an

expense in the periodexpense in the period– the amortisation methods usedthe amortisation methods used

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2020

Disclosure requirements Disclosure requirements (cont.)(cont.)

FRS-13 5.19 requires disclosure of FRS-13 5.19 requires disclosure of (cont.):(cont.):– A reconciliation of the balance of unamortised A reconciliation of the balance of unamortised

development costs at the beginning and end development costs at the beginning and end of the period showingof the period showing

development costs recognised as an asset;development costs recognised as an asset; development costs recognised as an asset;development costs recognised as an asset; development costs allocated to other asset development costs allocated to other asset

accounts; andaccounts; and development costs written back together with an development costs written back together with an

explanation of the change in circumstances that led explanation of the change in circumstances that led to the write-back as an asset.to the write-back as an asset.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2121

GoodwillGoodwill

Arises when one entity acquires Arises when one entity acquires another entity, or part thereof.another entity, or part thereof.

An unidentifiable intangible asset.An unidentifiable intangible asset. Accounting governed by FRS-36.Accounting governed by FRS-36.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2222

Internally generated vs. Internally generated vs. purchased goodwillpurchased goodwill Goodwill may be internally generated or Goodwill may be internally generated or

acquired by purchasing an existing acquired by purchasing an existing business.business.

Only purchased goodwill is permitted to Only purchased goodwill is permitted to be recordedbe recorded– purchased goodwill can be measured more purchased goodwill can be measured more

reliably than internally generated goodwill, reliably than internally generated goodwill, based on the amount paid.based on the amount paid.

Purchased goodwill is measured as the Purchased goodwill is measured as the excess of the cost of acquisition excess of the cost of acquisition incurred over the fair value of the net incurred over the fair value of the net assets acquired.assets acquired.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2323

Fair valueFair value

Fair value is the amount for which an Fair value is the amount for which an asset could be exchanged between a asset could be exchanged between a knowledgeable, willing buyer and a knowledgeable, willing buyer and a knowledgeable, willing seller in an knowledgeable, willing seller in an arm’s length transaction.arm’s length transaction.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2424

Amortisation of goodwillAmortisation of goodwill

Much opposition to amortisation Much opposition to amortisation requirements.requirements.

When AAS 18 released, requirement to When AAS 18 released, requirement to amortise over a period not exceeding amortise over a period not exceeding 20 years.20 years.

Innovative methods used for Innovative methods used for amortising developed—inverted sum-amortising developed—inverted sum-of-years-digits.of-years-digits.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2525

Amortisation of goodwill Amortisation of goodwill (cont.)(cont.)

In NZ goodwill must be amortised on a In NZ goodwill must be amortised on a systematic basis over its useful life.systematic basis over its useful life.

Period must not exceed 20 years.Period must not exceed 20 years.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2626

Empirical researchEmpirical research

Amortisation method may impose costs Amortisation method may impose costs on firms with debt covenants in place.on firms with debt covenants in place.

May also affect management May also affect management compensation contracts.compensation contracts.

Little evidence that goodwill Little evidence that goodwill amortisation expense used in profit amortisation expense used in profit calculation reflects information to calculation reflects information to investors in setting share prices and investors in setting share prices and returns.returns.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2727

Accounting for Accounting for brandsbrands A brand is a symbol, design, name or A brand is a symbol, design, name or

combination of these that identifies a combination of these that identifies a seller’s product and distinguishes it seller’s product and distinguishes it from the competition.from the competition.

Internally generated brands now being Internally generated brands now being recognised by a number of NZ recognised by a number of NZ companies.companies.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2828

Background to the Background to the brand debatebrand debate

Two basic origins:Two basic origins:– the problem of accounting for goodwill and the problem of accounting for goodwill and

other assets obtained through the other assets obtained through the acquisition of another companyacquisition of another company

– desire of companies to reflect value rather desire of companies to reflect value rather than cost of certain assets on statement of than cost of certain assets on statement of financial position.financial position.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-2929

Brand/intangible asset Brand/intangible asset debatedebate

Primary issue is the trade-off between Primary issue is the trade-off between two of the qualitative characteristics of two of the qualitative characteristics of financial reporting information.financial reporting information.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-3030

ED-87 Intangibles ED-87 Intangibles requirementsrequirements

Expenditure incurred on internally Expenditure incurred on internally generated assets such as brands generated assets such as brands cannot be distinguished from the costs cannot be distinguished from the costs of developing the business as a whole.of developing the business as a whole.

Where an intangible is recognised, it Where an intangible is recognised, it must be measured initially at cost.must be measured initially at cost.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-3131

ED-87 Intangibles ED-87 Intangibles requirements (cont.)requirements (cont.)

If the intangible has been acquired as If the intangible has been acquired as part of an acquisition resulting in an part of an acquisition resulting in an entity combination, it is not necessary entity combination, it is not necessary for the fair value of the asset to be for the fair value of the asset to be determined by reference to an active determined by reference to an active market.market.

Copyright Copyright 2003 McGraw-Hill New Zealand Pty Ltd. 2003 McGraw-Hill New Zealand Pty Ltd. PPTs t/a PPTs t/a New Zealand Financial Accounting 2eNew Zealand Financial Accounting 2e by Deegan and Samkin by Deegan and Samkin

Slides prepared by Grant SamkinSlides prepared by Grant Samkin

7-7-3232

ED-87 Intangibles ED-87 Intangibles requirements (cont.)requirements (cont.)

Where an active market does not Where an active market does not exist, the fair value initially recognised exist, the fair value initially recognised must be limited to an amount that must be limited to an amount that does not create or increase any does not create or increase any negative goodwill arising at the date of negative goodwill arising at the date of acquisition.acquisition.