chapter 6 bonds.pdf9781442502000 / berk/demarzo/harford / fundamentals of corporate finance / 1st...

TRANSCRIPT

PowerPointto accompany

Chapter 6

Bonds

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.1 Bond Terminology

A bond is a security sold by governments and

corporations to raise money from investors today

in exchange for promised future payments.

Payments on the bond are made until a final

repayment date, called the maturity date of the

bond.

The time remaining until the repayment date is

known as the term of the bond.

2

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.1 Bond Terminology

Two types of payments

The principal or face value (par value) of a

bond is the notional amount we use to

calculate the interest payments, which gets

repaid at maturity.

Bonds also promise additional payments

called coupons, which are paid periodically

(for example, six-monthly) until the maturity

date of the bond.

3

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Coupon payment

The amount of each coupon payment is

determined by the coupon rate of the bond.

The coupon rate is expressed as an APR, so

the amount of each coupon payment, CPN, is:

Coupon Rate Face Value

Number of Coupon Payments per YearCPN

(Eq. 6.1)

4

6.1 Bond Terminology

FORMULA!

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example:

A $1,000 bond with a 10% coupon rate and

six-monthly payments will pay coupon

payments of:

5

6.1 Bond Terminology

CPN =$1,000 x 10%

= $50 every six months2

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6

Table 6.1 Review of Bond Terminology

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.2 Zero-Coupon Bonds

Bonds without coupons are called zero-coupon bonds and are commonly known as Bills

Zero-coupon bonds have only two cash flows—the payment for the bond at current market price and the face value at maturity.

Example:

A one-year zero-coupon bond with a $100,000 face value has an initial price of $96,618.36.

If you purchased this bond and held it to maturity, you would have the following cash flows:

7

Period: 0 1

Cash Flow: ($96,618.36) $100,000

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.2 Zero-Coupon Bonds

Although bonds pay no direct interest, investors

are compensated for the time value of money by

purchasing the bond at a discount to its face

value.

Prior to its maturity date, the price of a zero-

coupon bond is always less than its face value.

That is, zero-coupon bonds always trade at a

discount (a price lower than the face value), so

they are also called pure discount bonds.

8

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.2 Zero-Coupon Bonds

Yield to maturity of a zero-coupon bond

The IRR of an investment in a bond is called the yield to maturity (YTM).

Yield to maturity of an n-year zero-coupon bond:

(Eq. 6.2)

9

FORMULA!

The yield to maturity of a bond is the discount

rate that sets the PV of the promised bond

payments equal to the current market price of the

bond.

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.1 Yields for Different Maturities (p.161)

Problem: Suppose the following zero-coupon bonds are

trading at the prices shown below per $100 face value.

Determine the corresponding yield to maturity for each bond.

Plan: We can use Eq. 6.2 to solve for the YTM of the

bonds.

Maturity 1 year 2 years 3 years 4 years

Price $96.62 $92.45 $87.63 $83.06

10

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute:

Using Eq. 6.2, we have:

1/11

1/ 22

1/33

1/ 44

(100 / 96.62) 1 3.50%

(100 / 92.45) 1 4.00%

(100 /87.63) 1 4.50%

(100 /83.06) 1 4.75%

YTM

YTM

YTM

YTM

11

Example 6.1 Yields for Different Maturities (p.161)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.2 Zero-Coupon Bonds

Risk-free interest rates

The Law of One Price implies that all one-year risk-free investments must earn this same return, the competitive market risk-free interest rate.

A default-free zero-coupon bond that matures on date n provides a risk-free return, which equals the yield to maturity on such a bond.

Consequently, we will often refer to the yield of such a zero-coupon risk-free bond as the risk-free interest rate.

These default-free, zero-coupon yields are also called spot interest rates, because these rates are offered ‘on the spot’ at that point in time.

12

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Figure 6.1Zero-Coupon Yield Curve Consistent with the Bond Prices in Example 6.1

13

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

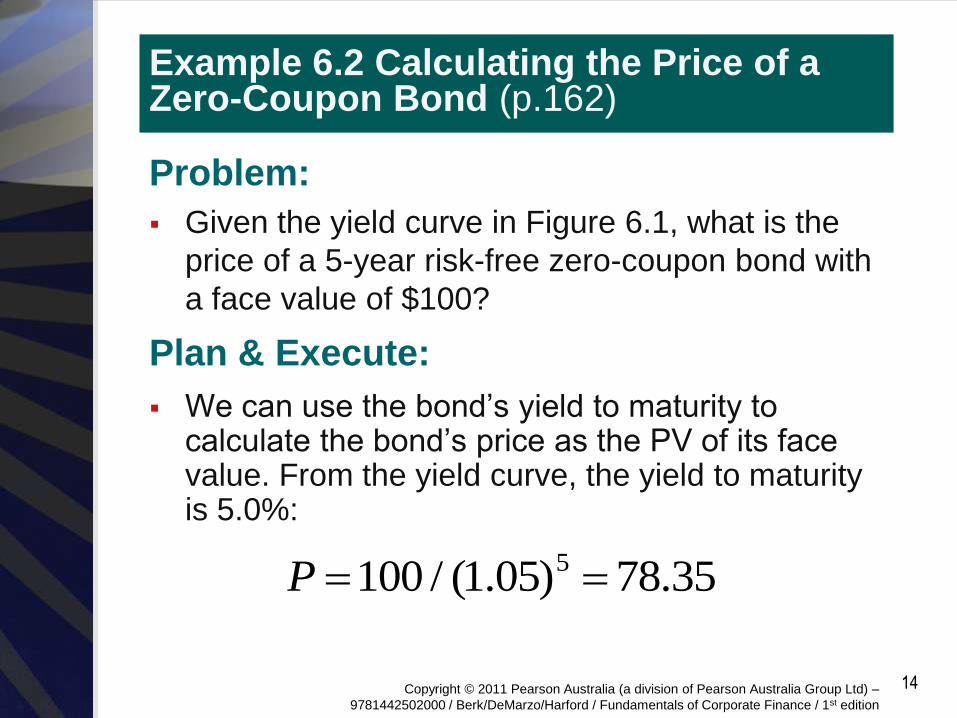

Example 6.2 Calculating the Price of a Zero-Coupon Bond (p.162)

Problem:

Given the yield curve in Figure 6.1, what is the

price of a 5-year risk-free zero-coupon bond with

a face value of $100?

Plan & Execute:

We can use the bond’s yield to maturity to calculate the bond’s price as the PV of its face value. From the yield curve, the yield to maturity is 5.0%:

14

5100 / (1.05) 78.35 P

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Evaluate:

We can calculate the price of a zero-coupon

bond simply by calculating the present value of

the face value using the bond’s yield to maturity.

Note that the price of the 5-year zero-coupon

bond is even lower than the price of the other

zero-coupon bonds in Example 6.1, because the

face value is the same, but we must wait longer

to receive it.

15

Example 6.2 Calculating the Price of a Zero-Coupon Bond (p.162)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.3 Coupon Bonds

Coupon bonds

Pay investors their face value at maturity and

make regular coupon interest payments.

The Government issues Treasury bonds into

the capital markets to meet its budgetary needs,

usually with maturities that range between three

to thirty years.

The original maturity is the term of the bond at

the time it was originally issued.

16

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Coupon bond cash flows

Return on a coupon bond comes from two sources:

the difference between purchase price and principal value

periodic coupon payments.

In the following example, we take a bond description and translate it into the bond’s cash flows.

17

6.3 Coupon Bonds

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.3 The Cash Flows of a Coupon Bond (p.163)

Problem:

Assume that it is 15 May 2013 and the Australian Office of Financial Management has just issued Treasury bonds with a May 2015 maturity, $1000 par value and a 5% coupon rate with six-monthly coupons.

The first coupon payment will be paid on 15 November 2013.

What cash flows will you receive if you hold this note until maturity?

18

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Solution:

Plan:

The phrase ‘May 2015 maturity, $1000 par value’ tells us that this is a bond with a face value of $1000 and five years to maturity.

The phrase ‘5% coupon rate with six-monthly coupons’ tells us that the bond pays a total of 5% of its face value each year in two equal six-monthly instalments.

Finally, we know that the first coupon is paid on 15 November 2013.

19

Example 6.3 The Cash Flows of a Coupon Bond (p.163)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute: The face value of this note is $1000; with six-monthly

coupons you will receive:

CPN=$1,000 x (5%/2)=$25.

Note that the last payment occurs in two years (4 six-month periods) from now and is composed of both a coupon payment of $25 and the face value payment of $1000.

20

Example 6.3 The Cash Flows of a Coupon Bond (p.163)

Timeline

May 2013 Nov 2013 May 2014 Nov 2014 May 2015

$25 $25 $25 $25 + $1,000

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Evaluate:

Since a bond is just a package of cash flows, we

need to know those cash flows in order to value

the bond.

That is why the description of the bond contains

all of the information we would need to construct

its cash flow timeline.

21

Example 6.3 The Cash Flows of a Coupon Bond (p.163)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

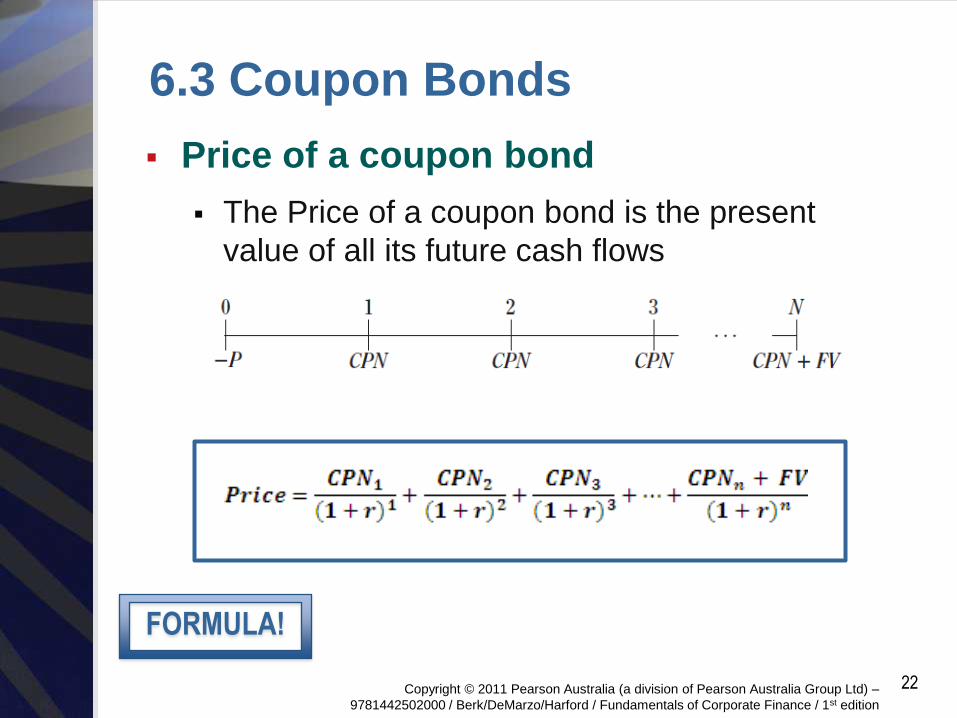

Price of a coupon bond

The Price of a coupon bond is the present

value of all its future cash flows

22

6.3 Coupon Bonds

FORMULA!

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

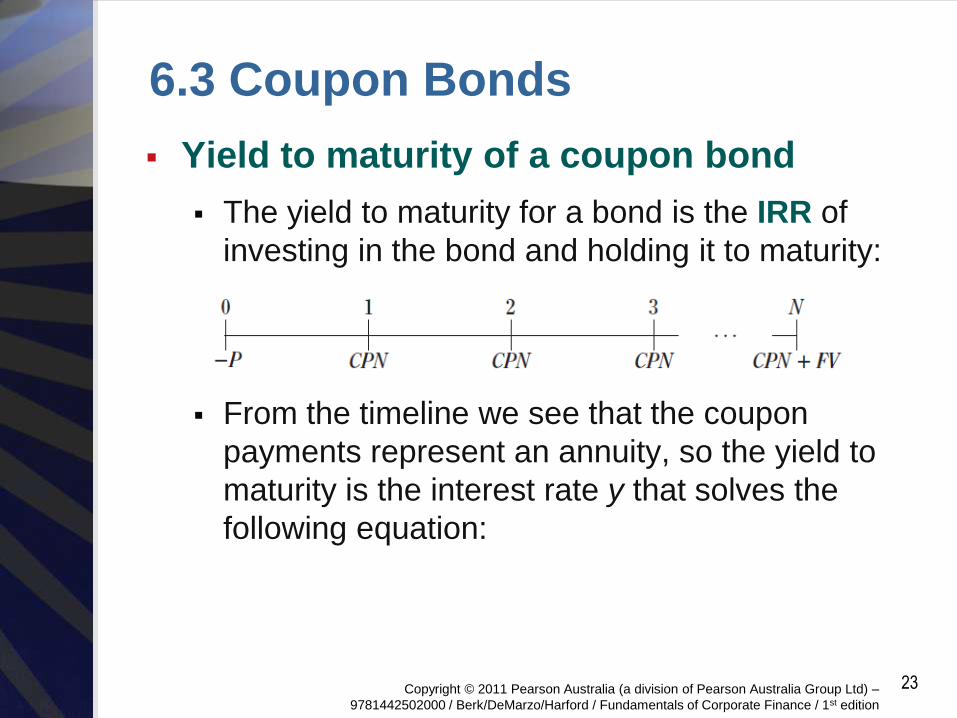

Yield to maturity of a coupon bond

The yield to maturity for a bond is the IRR of

investing in the bond and holding it to maturity:

From the timeline we see that the coupon

payments represent an annuity, so the yield to

maturity is the interest rate y that solves the

following equation:

23

6.3 Coupon Bonds

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

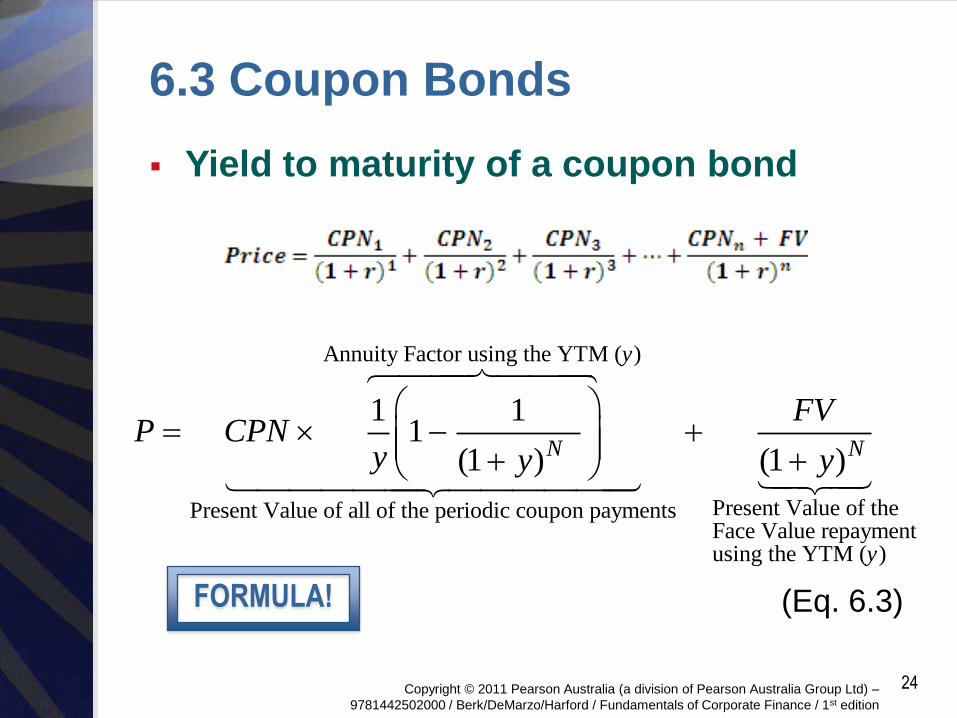

Annuity Factor using the YTM ( )

Present Value of the Present Value of all of the periodic coupon paymentsFace Value repaymentusing the YTM (

1 11

(1 ) (1 )

y

N N

y

FVP CPN

y y y

)

(Eq. 6.3)

24

Yield to maturity of a coupon bond

6.3 Coupon Bonds

FORMULA!

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.4 Calculating the Yield to Maturity of a Coupon Bond (p.165)

Problem:

Consider a five-year, $1000 bond with a 5%

coupon rate and semi-annual coupons with a

yield to maturity of 6%

What is the current price of the bond?

25

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Solution:

Plan:

From a cash flow timeline, we can see that the bond consists of an annuity of 10 payments of $25, paid every 6 months, and one lump-sum payment of $1000 in 5 years (ten six-month periods).

We can use Eq. 6.3 to solve for the price. However, we must use six-month intervals

consistently throughout the equation.

26

Example 6.4 Calculating the Yield to Maturity of a Coupon Bond (p.165)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute:

Because the bond has ten remaining coupon

payments, we calculate its price by using Eq. 6.3

for this bond:

Note that a 6% APR is equivalent to a semi-annual rate of 3%.

27

Example 6.4 Calculating the Yield to Maturity of a Coupon Bond (p.165)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.5 Calculating a Bond Price from its Yield to Maturity (p.165)

Problem:

Consider again the five-year $1000 bond with a

5% coupon rate and semi-annual coupons in

Example 6.4.

Suppose interest rates drop and the bond’s yield

to maturity decreases to 4.50% (expressed as an

APR with semi-annual compounding).

What price is the bond trading for now?

28

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Solution:

Plan:

Given the yield, we can calculate the price using Eq.6.3.

Note that a 4.50% APR is equivalent to a semi-annual rate of 2.25%.

Also, recall that the cash flows of this bond are an annuity of 10 payments of $25, paid every six months, and one lump-sum cash flow of $1000(the face value) paid in five years (10 six-month periods).

29

Example 6.5 Calculating a Bond Price from its Yield to Maturity (p.165)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute:

Using Eq. 6.3 and the 6-month yield of 2.25%,

the bond price must be:

10 10

1 1 100025 1 $1022.17

0.0225 1.0225 1.0225

P

30

Example 6.5 Calculating a Bond Price from its Yield to Maturity (p.165)

Evaluate:

The Bond’s price has risen to $1,022.17, lowering the return from investing in it from 3%to 2.25% per six-month period.

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.4 Why Bond Prices Change

Zero-coupon bonds always trade for a discount—that is, prior to maturity, their price is less than their face value.

But coupon bonds may trade at a discount, or at a premium (a price greater than their face value).

Most issuers of coupon bonds choose a coupon rate so that the bonds will initially trade at, or very close to, par (that is, at the bond’s face value).

After the issue date, the market price of a bond generally changes over time.

31

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.4 Why Bond Prices Change

Interest rate changes and bond prices

If a bond sells at par, the only return investors

will earn is from the coupons that the bond pays.

The bond’s coupon rate will exactly equal its

yield to maturity.

As interest rates in the economy fluctuate, the

yields that investors demand to invest in bonds

will also change.

As interest rates and bond yields rise, bond

prices will fall, and vice versa, so that bond

prices and interest rates always move in the

opposite direction.

32

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Figure 6.2 A Bond’s Price versus its Yield to Maturity

33

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Table 6.2 Bond Prices Immediately After a Coupon Payment

34

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.6 Determining the Discount or Premium of a Coupon Bond (p.169)

Problem:

Consider three 30-year bonds with annual

coupon payments.

One bond has a 10% coupon rate, one has a 5%

coupon rate, and one has a 3% coupon rate.

If the yield to maturity of each bond is 5%, what

is the price of each bond per $100 face value?

Which bond trades at a premium, which trades at

a discount, and which trades at par?

35

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Solution:

Plan:

Each bond has 30 years to maturity and pays its coupons annually. Therefore, each bond has an annuity of coupon payments, paid annually for 30 years, and then the face value paid as a lump sum in 30 years.

They are all priced so that their yield to maturity is 5%.

Therefore, we can use Eq. 6.3 to calculate the price of each bond as the PV of its cash flows, discounted at 5%.

36

Example 6.6 Determining the Discount or Premium of a Coupon Bond (p.169)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute:

For the 10% coupon bond, the annuity cash

flows are $10 per year (10% of each $100 face

value).

Similarly, the annuity cash flows for the 5% and

3% bonds are $5 and $3 per year.

Using Eq. 6.3, the bond prices are:

30 30

30 30

30 30

1 1 100(10% coupon) 10 1 $176.86 (trades at a premium)

0.05 1.05 1.05

1 1 100(5% coupon) 5 1 $100.00 (trades at par)

0.05 1.05 1.05

1 1 100(3% coupon) 3 1 $69.26 (tra

0.05 1.05 1.05

P

P

P

des at a discount)

37

Example 6.6 Determining the Discount or Premium of a Coupon Bond (p.169)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Evaluate:

The prices reveal that when the coupon rate of

the bond is higher than its yield to maturity, it

trades at a premium.

When its coupon rate equals its yield to maturity,

it trades at par.

When its coupon rate is lower than its yield to

maturity, it trades at a discount.

38

Example 6.6 Determining the Discount or Premium of a Coupon Bond (p.169)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.7 The Effect of Time on the Price of a Bond (pp.170-1)

Problem:

Suppose you purchase a 30-year, zero-coupon bond with a yield to maturity of 5%. For a face value of $100, the bond will initially trade for:

If the bond’s yield to maturity remains at 5%, what will its price be five years later?

If you purchased the bond at $23.14 and sold it five years later, what would the IRR of your investment be?

30

100(30 years to maturity) $23.14

1.05P

39

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Plan:

If the bond was originally a 30-year bond and five years have passed, then it has 25 years left to maturity.

If the yield to maturity does not change, then you can calculate the price of the bond with 25 years left exactly as we did for 30 years, but using 25 years of discounting instead of 30.

Once you have the price in five years, you can calculate the IRR of your investment.

The FV is the price in 5 years, the PV is the initial price ($23.14), and the number of years is 5.

40

Example 6.7 The Effect of Time on the Price of a Bond (pp.170-1)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Execute:

25

100(25 years to maturity) $29.53

1.05P

If you purchased the bond for $23.14 and then

sold it after five years for $29.53, the IRR of your

investment would be:

1/529.53

1 5.0%23.14

Your return is the same as the yield to maturity

of the bond.

41

Example 6.7 The Effect of Time on the Price of a Bond (pp.170-1)

29.53 = 23.14 x (1+IRR)5

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Evaluate:

Note that the bond price is higher, and hence the

discount from its face value is smaller, when there

is less time to maturity.

The discount shrinks because the yield has not

changed, but there is less time until the face

value will be received.

If a bond’s yield to maturity does not change, then

the IRR of an investment in the bond equals its

yield to maturity even if you sell the bond early.

42

Example 6.7 The Effect of Time on the Price of a Bond (pp.170-1)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Figure 6.3 The Effect of Time on Bond Prices

43

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

6.4 Why Bond Prices Change

Interest rate risk and bond prices

While the effect of time on bond prices is

predictable, unpredictable changes in interest

rates will also affect bond prices—and some

bonds will react more strongly than others.

Investors view long-term loans to be riskier than

short-term loans; the same is true of short-

versus long-term bonds:

44

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Example 6.8 The Interest Rate Sensitivity of Bonds (p.172)

Problem:

Consider a 10-year coupon bond and a 30-year

coupon bond, both with 10% annual coupons.

By what percentage will the price of each bond

change if its yield to maturity increases from 5%

to 6%?

45

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Solution:

Plan:

We need to calculate the price of each bond for each yield to maturity and then calculate the percentage change in the prices.

For both bonds, the cash flows are $10 per year for $100 in face value and then the $100 face value repaid at maturity.

The only difference is the maturity: 10 years and 30 years. With those cash flows, we can use Eq. 6.3 to calculate the prices.

46

Example 6.8 The Interest Rate Sensitivity of Bonds (p.172)

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

47

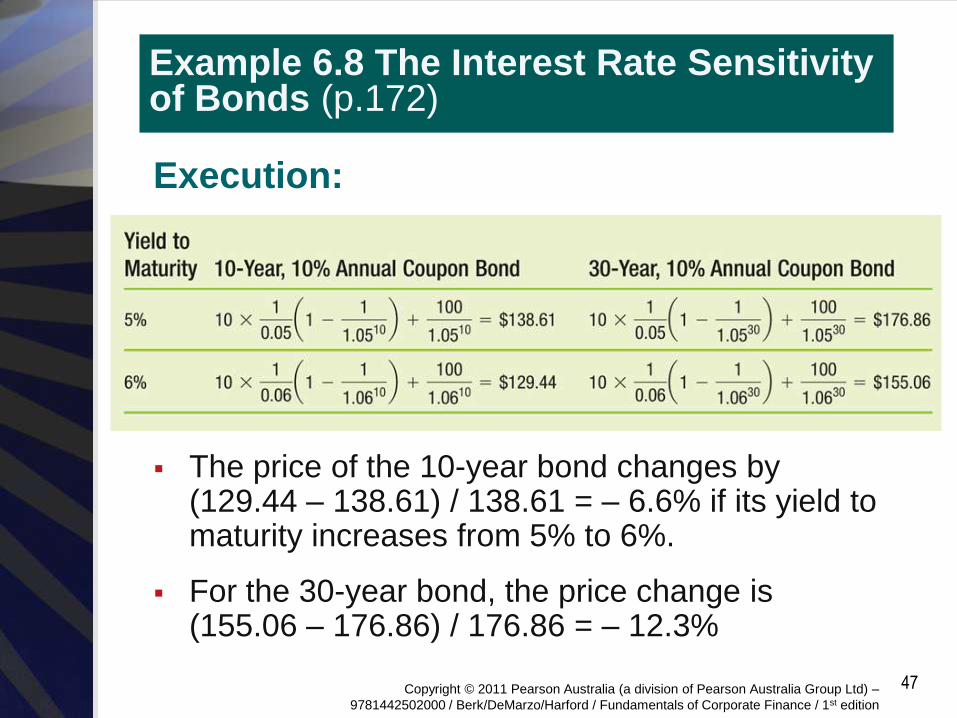

Example 6.8 The Interest Rate Sensitivity of Bonds (p.172)

Execution:

The price of the 10-year bond changes by (129.44 – 138.61) / 138.61 = – 6.6% if its yield to maturity increases from 5% to 6%.

For the 30-year bond, the price change is (155.06 – 176.86) / 176.86 = – 12.3%

Copyright © 2011 Pearson Australia (a division of Pearson Australia Group Ltd) –

9781442502000 / Berk/DeMarzo/Harford / Fundamentals of Corporate Finance / 1st edition

Evaluate:

The 30-year bond is twice as sensitive to a

change in the yield than is the 10-year bond.

48

Example 6.8 The Interest Rate Sensitivity of Bonds (p.172)