chapter 6 a comprehensive model on the investment...

TRANSCRIPT

219

CHAPTER 6

A Comprehensive Model on the Investment

Behaviour of Mutual Fund Investors

6.1 Introduction

Mutual fund (MF) industry in emerging markets has become

highly competitive which necessitates that MF marketers must fully

understand the buying behaviour of investors to be able to effectively

market their MF schemes. Hence, there is a felt need amongst MF

marketers of a comprehensive investment behaviour model to

understand the investors‟ buying decision process for MF schemes.

The current state of knowledge about the investor behaviour is

found not to be quite satisfactory and in fact it is inadequate when

applied to understand the buying decision process of MF investors. The

fundamental normative model of investment behaviour considers only

risk and return as crucial variables impacting the investors‟ buying

behaviour. Further, the model assumes investors as rational. However,

this has not been the case and humans are shown to be irrational at most

times (Shefrin, 2000). Literature in behavioral finance suggests that

220

investor behavior is “predictably irrational” (Ariley, 2008). Further,

there is adequate evidence in the literature suggesting non economic

motives influencing the behaviour of investors (Nagy and Obenberger,

1994). Hence, normative model of investment behavior has only limited

applicability for the MF marketers (Capon, Fitzsimons and Prince, 1996)

and regulators. Hence a model that captures the essence of traditional

finance, behavioral finance and consumer behavior is likely to provide

more insight into the buying decision process of MF investors. This has

more relevance in the current context as today shopping for financial

instrument has become increasingly like shopping for any other

consumer items (Wilcox, 2003).

In this chapter, therefore, a new comprehensive model of investment

behaviour is proposed to explain the impact of investors‟ subjective

knowledge (SK), perceived purchase risk (PPR), and purchase decision

involvement (PDI) on their MF investment behaviour. The proposed

model is tested empirically using the data collected through a survey

wherein a pretested structured questionnaire was administered to the 268

MF investors. In the following section, we explain the theoretical basis

for the model and provide the support for the hypothesized linkages

embedded within.

221

The rest of this chapter is organized in the following way. In

Section 6.2, the relevant literature is critically reviewed and

summarized. Section 6.3 proposes the new investment behaviour model.

The hypotheses of the study are also discussed in this section. Section

6.4 discusses the methodology and the constructs used in the study.

Section 6.5 shows the study results. Section 6.6 presents the conclusion

based on the findings of the study and further highlights the contribution

of this study. The implications of the study for MF managers and

regulators are discussed in Section 6.7. Finally, section 6.8 records the

limitations of this research and possible scope of future research in this

area.

6.2 Literature review

Over the past two decades, MFs have been the focal point of an

increasing number of research studies being conducted in the field of

finance. The basic issues of research dealt in by majority of these studies

have been: performance evaluation of MF (Carhart, Carpenter and

Lynch, 2002; Grinblatt and Titmann, 1993; Malkiel, 1995a; Sharpe,

1966), assessment of market timing ability of fund managers (Chang and

Lewellen, 1984; Grant, 1977; Jiang, 2003), closed end fund puzzle

222

(Hardouvelis La Porta and Wizman, 1993; Malkiel, 1977, 1995b;

Pontiff, 1995). There has, however, been a dearth of studies undertaken

specifically to understand the investment behaviour of MF investors

(Wilcox, 2003). The research pertaining to investors‟ behaviour in

traditional finance has made only little advances beyond the

perspectives, provided by the Markowitz (1952) framework, where

investors (assumed to be the rational utility maximizers) consider

expected returns and risks of the investing avenues as the only crucial

variables while making their investment decisions (Sharpe, 1994; Tobin,

1965).

In recent years numerous behavioural finance studies have

shown that in reality investors are “predictably irrational” and various

kind of behavioural biases (non-economic motives) influence their

investment decision (Arieley, 2008; Barber and Odean, 2001; Nagy and

Obenberger, 1994; Odean, 1999; Shefrin, 2000). Specifically, the

behavioural finance studies suggests that MF investors (a) chase past

performance (Barber et al., 2005); (b) are reluctant to sell their losses

(Barber et al., 2005); (c) react differently to various form of fund

expenses (Barber et al., 2005); and (d) attribute successful outcomes to

their own skill and blame unsuccessful outcome on bad luck (Shefrin,

2000). As yet, behavioural finance research provides little insight into:

223

(a) the causes of these behavioural biases; (b) the impact of behavioural

biases on investor‟s decision making process (Bailey et al., 2010)76

.

Finding a clear insight in to the above issues is of utmost significance

for the marketers of MFs as the shopping for financial instruments has

become increasingly like shopping for any other consumer items

(Wilcox, 2003) wherein, prospective investors now have options to

choose from a variety of financial instruments77

being offered to them.

The studies in consumer behaviour literature have proposed

various consumer behaviour models, which provide some insights into

the factors that influence consumer behaviour (Engel et al., 1995;

Howard and Sheth, 1969; Nicosia, 1966)78

. Nicosia (1966) was the first

to propose a consumer behaviour model.The model focused on the

conscious, deliberative decision making behaviour of consumer. Further,

the model views the act of purchase as only one of the stages in an

ongoing consumer decision making process. The model suggests

consumers as moving from general product knowledge to specific brand

76

Recently, studies have shown that risk perception (Nosic and Weber, 2010) and

investors knowledge (Curtis, 2004) is likely to be linked with the behavioural biases

among investors. 77

Corporate debt and equity securities, fixed deposits of companies and commercial

banks, MF schemes, Unit-linked insurance products, Chit funds from the Non-bank

finance companies etc. 78

There are various consumer behaviour models. However, only three of these models

have received adequate acclamation & recognition viz., the models proposed by the

Nicosia (1966), Howard and Sheth (1969) and Engel et al. (1995).

224

knowledge and from a passive position to an active state which are

motivated towards specific brand knowledge. The model, however,

suffers from the following limitations. First, in spite of the fact that

model discusses about consumer knowledge and motivation, it lacks

specificity with respect to the linkages among the two constructs.

Second, model does not clearly identify elements/factors (Rau and

Samiee, 1981). Third, it does not define any of the factors or elements

in variable terms; hence variables have not been operational (Rau and

Samiee, 1981). Fourth, the level of parsimony is low due to complex

linkage in the model which appears to be all encompassing, thus

resulting in many conceptual overlaps among the elements of the model

(Rau and Samiee 1981). Finally, model cannot be validated (Foxall,

1980).

Howard and Sheth (1969) proposed another model of consumer

behaviour. Their model attempted to depict rational brand choice

behaviour by buyer under conditions of incomplete information and

limited abilities. The model identifies many of the variables influencing

consumers and details how they interact with each other. This model

assumes that buyers do pass through a cognitive, affective and

behavioural stage when there is a high degree of involvement with the

product category, which is perceived to have a high degree of

225

differentiation of product within it (Kotler, 1991). However, the model

has been subject to the following criticisms: First, the sharp distinction

between exogenous and other variables has not been made (Loudon and

Bitta, 2002; Rau and Samiee, 1981). Second, in absence of definitions of

the variables, no attempt has been made to operationalize the variables

(Rau and Samiee, 1981). Third, model cannot be validated because of

there being too many variables in the model (Foxall, 1980; Loudon and

Bitta, 2002).

One of the best examples of contemporary consumer behaviour

models is probably the Engel- Blackwell- Minard model (Engel,

Blackwell and Minard, 1995), which was originally developed in 1968

by Engel–Kollat–Blackwell (Engel, Kollat and Blackwell, 1968) and has

since been subjected to numerous revisions. It stands as one of the most

popular representations of consumer behaviour. Similar to Howard and

Sheth model, the authors recognize two significantly different modes of

operation by consumers. One is described as extended problem solving

(EPS) which is characterized by high level of involvement and/or high

level of perceived risk. In this behaviour, a consumer has high

motivation to search for brand information and one gets involved in

rigorous product evaluation process. The other mode of operation is

described as limited problem solving (LPS) behaviour in which the

226

consumer is operating in low level of involvement and/or low levels of

perceived purchase risk and has low motivation to search for brand

information and to get involved in non-rigorous evaluation of

alternatives. The authors argue that the same basic model can be used to

characterize both EPS and LPS behaviour. What changes is the degree to

which a consumer experiences various stages in the model.

As per this model, the buying decision process consists of five

stages: a) problem recognition, b) information search, c) evaluation of

alternatives, d) purchase decision and e) post purchase behaviour. This

Engel-Kollat-Blackwell model focuses on the level of consumer

involvement while emphasizing on the buying decision process of

consumers. The model, however, suffers from the following limitations.

First, the model is too complex to be verified empirically (Rau and

Samiee, 1981). Second, there is vagueness regarding the role of some

variables. For example, the influence of environmental variable is noted

but their role in affecting behaviour is not well specified (Loudon and

Bitta, 2002). Third, even though the model provides a comprehensive

framework to understand the process of buying decision, it lacks clarity

in terms of causal relationship among variables which have more value

to the marketers, for developing marketing strategy.

227

Overall, the above three most recognized models of consumer

behaviour, (i.e. Nicosia, Howard and Sheth and Engel et al. models)

suffer from the following limitations. First, the above models implicitly

or explicitly acknowledge the impact of consumers‟ knowledge,

perceived purchase risk and involvement on their buying behaviour, but

how these variables interact to impact the buying behaviour is not

clearly stated. Second, the methods of measurement of these variables

have not been clearly identified. Third, even though the above

conceptual models are supported by large volume of empirical work,

most of them have been advanced in the context of studying the

purchase of tangible goods rather than intangible financial goods.

Hence, there is a felt need amongst MF marketers and

researchers for a comprehensive model to understand the investor‟s

buying decision process for MFs.

6.3 Proposed comprehensive model on the investment

behaviour of MF investors

A new comprehensive model on the investment behaviour of MF

investors is proposed as shown in figure 6.1. As per the proposed model,

228

investors purchase decision involvement (a construct used to capture the

investors level of motivation with purchase) mediates the impact of

investors subjective knowledge ( a construct used to capture the

investors‟ confidence in her making an investment decision) and

perceived purchase risk ( a construct used to capture the overall

perceived risk associated with MF purchase as perceived by investor) on

the investment behaviour of MF investors particularly information

search and information processing behaviour.

The model suggests that (a) MF investors subjective knowledge

(SK) negatively impact MF investors perceived purchase risk (PPR)

associated with MF; (b) MF investors SK positively impact purchase

decision involvement (PDI); (c) MF investors PPR negatively impact

PDI; (d) MF investors PDI positively impact their depth of information

search and information processing behaviour; (e) MF investors depth of

information search positively impacts their depth of information

processing. In the following sections (from 6.3.1 through 6.3.5) we

provide theoretical basis for the model and provide support for the

hypothesized linkages embedded within.

229

Figure 6.1

Proposed comprehensive model of investment behaviour

6.3.1 Impact of subjective knowledge on perceived purchase risk of

MF investors

Knowledge has been found to influence all the phases in the

decision process (Bettman and Park, 1980) including the consumers

evaluation of risk inherent in the purchase (Murray and Schlatcer, 1990).

Researchers have distinguished objective knowledge (i.e. what is

actually stored in memory) from subjective knowledge (i.e. what

individual perceive they know). It has been suggested that consumers

Perceived

purchase risk

Subjective

Knowledge

Purchase

decision

involvement

Information

search

behaviour

Information

processing

behaviour

(-)H3

(+)H2

(-)H1

(+)H4

(+)H5b

(+)H5a

230

SK is more related to her self confidence regarding decision making

(Brucks, 1985) hence is likely to influence the consumers‟ evaluation of

risk with the purchase. In consumer behaviour literature, Bauer (1960)

introduced the concept of perceived risk. It is defined as individual‟s

subjective feeling of uncertainty that the consequence of potential

purchase will be favorable (Cox, 1967; Cunningham, 1967). In the

context of tangible goods, there is a consensus among researchers that

subjective knowledge negatively influences the perceived purchase risk

(Havlena and DeSarbo, 1990); however there is a lack of studies that

have investigated the above relationship in the context of intangible

financial goods. Based on the above discussion it is hypothesized that;

H1: MF investors‟ subjective knowledge has a negative impact on their

perceived purchase risk.

6.3.2 Impact of subjective knowledge on purchase decision

involvement of MF investors

Literature in consumer behaviour suggests that consumer

knowledge and involvement are important constructs in understanding

consumer behaviour (Huffman and Houston, 1993; Howard, 1994).

Purchase decision involvement can be defined as the extent of interest

231

and concern that a consumer brings to bear upon a purchase decision

task (Mittal, 1989). A few studies have empirically investigated the

relationship between the SK and PDI (Chang and Huang, 2002; Lin and

Chen, 2006; Park and Moon, 2003). Study suggests that; (a) consumers‟

product knowledge is positively associated with involvement (Park and

Moon, 2003), and (b) product involvement mediates the impact of

product knowledge on purchase decision (Lin and Chen, 2006). Based

on the above discussion we posit the following hypothesis;

H2: MF investors‟ subjective knowledge has a positive impact on their

level of PDI.

6.3.3 Impact of perceived purchase risk on purchase decision

involvement of MF investor

There seems to be consensus among researchers that PPR impact

PDI (Chaffee and Mcleod, 1973; Laurent and Kapferer, 1985;

Rothschild, 1979). However the researchers disagree with the direction

of the impact of PPR on PDI. A few researchers argue that high PPR

puts consumers in a distressed and anxious state, which in turn motivates

them to engage in extensive problem solving activity to resolve it (Engel

232

et al., 1995); hence PPR is likely to positively impact PDI. Several

empirical studies have been conducted to assess the veracity of the

above theory and found mixed results. While several studies have

supported the above theory, an equal number of studies have reported

contradictory findings (Gemunden, 1985). Specifically, it has been

suggested that during purchase of complex products which requires high

technical knowhow and expertise consumers are likely to be motivated

to rely on few personal formal sources (Cho and Lee, 2006; Coleman,

Warren and Houston, 1995; Gemunden 1985) rather than actively

engaging in purchase and seeking information from multiple sources.

Hence it is likely that the impact of PPR on PDI is context specific.

Particularly in the context of the purchase of complex products,

consumers PPR will negatively impact consumers‟ motivation to engage

with purchase decision, hence their PDI.

Investment decisions particularly investment in MF is a complex

task. This is due to the fact that investors may have to go through a

complex decision making process due to the available information about

the MF product which, though abundant, is not quite organized and

comprehensible. The above discussion conjectures that PPR will

negatively impact the level of PDI. Therefore we posit the following

hypothesis;

233

H3: MF investors‟ PPR has a negative impact on their level of PDI.

6.3.4 Impact of purchase decision involvement on the depth of

information search by MFs investor

Three widely recognized contemporary consumer behaviour

model i.e. Nicosia (1966) model, Howard and Sheth model (1969) and

Engel- Blackwell- Minard model (Engel et al., 1995) considers

consumer search for information as an important prepurchase activity.

PDI is likely to have positive impact on the depth of information search.

High PDI consumers are likely use more than one source of information

(Alexander et al, 1997; Richins and Bloch, 1986) and will have a

tendency to use these sources to a high extent in order to seek advanced

information and process all relevant information‟s in detail (Beatty and

Smith, 1987; Gensch, Javalgi, and Rajshekhar, 1987). Based on the

above discussion we posit the following hypothesis;

H4: MF investors‟ PDI has a positive impact on their depthof

information search.

234

6.3.5 Impact of depth of information search and purchase decision

involvement on the depth of information processing by MF investors

Information processing is an important prepurchase activity

which includes identification of key attribute(s) for comparing the

various brands of products to be purchased and comparison of the

available brands on the basis of identified attributes.

The depth of information processing of MF investors is likely to

be positively impacted by depth of information search and level of PDI.

This is due to the fact that high depth of information search positively

impacts the attributes information available with the consumer at the

time of evaluation of products/brands. Hence with high depth of

information search consumer will bring more number of dimensions at

the time of information processing (Brucks, 1985; Johnson and Russo,

1984) which will positively impact the depth of information processing.

Further, depth of information processing is also positively

impacted by level of PDI. High PDI consumers have clearly articulated

attributes to compare brands (Lee and Marlowe, 2003). They engage in

extensive evaluation of attributes and products (Hansen, 2005). Further

they are likely to engage in high degree of cognitive activity and will

235

make strong efforts in evaluating and comparing products before

reaching a reasoned decision (Dawar and Parker, 1994). Based on the

above discussion it is hypothesized that

H5a: MF investors‟ depth of information search has a positive impact on

their depth of information processing.

H5b: MF investors‟ PDI has a positive impact on their depth of

information processing.

6.4 Methodology

6.4.1 Sample

The data was collected through a survey wherein a pretested structured

questionnaire was administered to the 350 respondents. The survey

respondents were conveniently selected from those who invested in one

or more MF scheme(s) within one month period prior to the survey date

and were based in the Jammu region of J&K (India). The condition that

respondent must have invested in one or more MF scheme(s) within one

month period prior to the survey date was applied so as to more clearly

measure the respondent‟s PPR, SK and PDI close to their purchase of

236

MF schemes. Further, the framing effect (i.e. investment choices

available with individual investor) during their investment decision was

controlled in the study by the nature of sample itself. The study was

confined to individual investors and institutional investors were

excluded from the study, hence each respondent had equal access to all

investment choice available for investors in India.

Since it was hard to reach the population, we used convenience sampling

method and identified respondents for the study by reaching to the place

where they are reasonably expected to gather. The local offices of the

five Asset Management Companies located in Jammu region, Jammu &

Kashmir (India) was identified for this purpose. A self administered

survey questionnaire was used to collect data. During the survey the

questionnaire was handed out to respondents who were asked to return

the filled questionnaire.

6.4.2 Survey Design and analysis

This study was conducted in four stages. In the first stage

(Sections 6.2 and 6.3); relevant literature was reviewed to propose a

comprehensive investment behaviour model. In this stage series of

hypotheses were also proposed. In the second stage, structured

237

questionnaire was developed and pretested for validity and reliability.

The constructs used in the pretested questionnaire are described in

Section 6.4.3. In the third stage, the data was collected through a survey

wherein a pretested structured questionnaire was administered to the 350

respondents. The total 276 respondents (78.25%) returned the filled

questionnaire. Among the 276 responses received, 8 responses were

found to be incomplete and were not included in the study. The total

usable responses were 268 (76.57 % of the sample size) which forms the

basis for the study. The final (fourth) stage involved following four

steps. In step 1, the dimensionality and reliability of the constructs was

tested. The exploratory factor analysis (EFA) was used to assess the

dimensionality of the constructs (Hair et al., 2005). Cronbach‟s alpha

was used to test the reliability of the constructs used in this study (Hair

et al., 2005). In step 2, discriminant validity is assessed for every

possible pair of constructs by constraining the estimated correlation

parameter between them to 1.0 and then performing a chi-square

difference test on the values obtained for the constrained and

unconstrained model (Anderson and Gerbing, 1988). A significantly

lower chi-square value in an unconstrained model indicates that

discriminant validity is achieved. In step 3, convergent validity is

assessed from the measurement model by determining whether each

indicator‟s estimated pattern coefficient on its posited underlying

238

construct factor is significant. In step 4, structural equation modeling

(SEM) with maximum likelihood estimate (AMOS 16) was used to test

the proposed hypotheses and the overall fit of the proposed model and

was compared with alternative models using goodness of fit measures.

6.4.3 Constructs used in the pretested questionnaire

This section describes the operationalization of various

constructs used in the study.

6.4.3.1 Subjective Knowledge (SK)

Subjective knowledge is defined as MF investor‟s subjective

assessment of perceived familiarity with the MFs (Brucks, 1985). Three

items on the five point Likert scale was used to operationalize SK. The

scores of the individual items were added to find the overall score. The

items used to measure SK are shown in table 6.1.

6.4.3.2 Perceived purchase risk (PPR)

PPR is defined as individual‟s subjective feeling of uncertainty

that the consequence of potential purchase will be favorable (Cox 1967;

239

Cunningham 1967). This study measured PPR based on measures use to

measure PPR in accounting services (Garner and Garner, 1985) and

banking services (Heaney and Goldsmith, 1999). The PPR was

measured by 4 items five point Likert scale; where 1 = not at all and 5 =

very much. The score of the individual items were added to find the

overall score. The items used to measure PPR are shown in table 6.1.

6.4.3.3 Level of purchase decision involvement (PDI)

To measure PDI, Laurent and Kapferer abridged Consumer

Involvement Profile (CIP) (Laurent & Kapferer, 1985) was used. The

PDI was measured by 3 items five point Likert scale. The scores of the

individual items were added to find the overall score. The items used to

measure PDI are shown in appendix table 6.1.

6.4.3.4 Depth of information search

It connotes the effort that an investor makes in searching and

seeking pre-purchase information. It was measured by 12 items five

point Likert scale; where 1= did not use and 5= used a lot. Each item

represented some particular source of information which investors can

possibly use as a source of information before/ at the time of purchase of

the scheme(s). The scores of the individual items were added to find the

240

overall score. The items used to measure the depth of information search

are shown in table 6.1.

6.4.3.5 Depth of information processing

It connotes the level of effort done by the respondents to evaluate

and compare the MF schemes before reaching to decision. It was

measured by 12 items five point Likert scale; where 1= did not use and

5= used a lot. Each items represented some particular attribute of the MF

schemes which investors can possibly use to compare the various MFs

before/ at the time of purchase of the MF schems(s). The scores of the

individual items were added to find the overall score. The items used to

measure depth of information processing are shown in appendix table

6.1.

6.5 Results

The demographic profiles of the sample MF investors are same

as shown in table 3.1. This section is organized as follows. First, the

scale refinement, dimensionality and reliability of each of the latent

constructs used in this study are discussed. Second, the results of test of

discriminant validity of the constructs are discussed. Next, the results of

241

the test of convergent validity are discussed. Fourth, the results of the

test of proposed hypotheses of the study are discussed. Finally, the result

of the overall fit of the proposed model is discussed and the proposed

model is compared with alternative models.

6.5.1 Dimensionality and reliability of latent research constructs

The test results of dimensionality and reliability of the constructs

are shown in Table 6.2. The dimensionality is assessed using exploratory

factor analysis (EFA), a method based on the pattern of correlations

between the questionnaire item scores. If all items share moderate to

strong correlations, this produces a single 'factor' and suggests that the

scale measures a single dimension. Several groups of such items

produce several factors, suggesting that several dimensions are being

measured through a single construct. Principal component analysis with

varimax rotation was conducted to identify the number of dimensions

(factors).

To determine the appropriateness of factor analysis, the Kaiser-

Meyer-Olkin (KMO) and the Bartlett‟s test of Sphericity are examined.

The KMO measure of sampling adequacy for all the constructs is above

minimum acceptable value of 0.60, which means data is adequate for

EFA (Tabachnick and Fidel, 1989). The Bartlett‟s test of Sphericity is

242

also found to be significant (p < .001). A significant Bartlett‟s test of

Sphericity indicates that each factor identified by EFA has only one

dimension and each attributes load only on one factor.

First the EFA of subjective knowledge construct was examined.

Principal components analysis of subjective knowledge construct reveals

the unidimensional nature of the construct as all the items are loaded

into one single factor. Second, the EFA of PPR was examined. Principal

components analysis of PPR construct also reveals the unidimensional

nature of the construct as all the items are loaded into one single factor.

Third, the principal component analysis of PDI construct also revealed

its unidimensional nature.

Fourth, “depth of information search” construct was examined

for the factorability of the twelve items “depth of information search”

scale by using correlation method. A result reveals that two items did

not correlate at least 0.3 with at least one other item; hence these items

were not included in the study. The items which did not correlate with

any other items were “To what extent you have used MF sales agent to

gather information before the purchase of recent MF scheme” and “To

what extent you have used banks to gather information before the

purchase of recent MF scheme”. Principal component analysis was used

243

to identify the underlying factors of the “depth of information search”

scale. The two factor solution which explained 49.27 % of the variance

was preferred because of its previous theoretical support. Two items

with high loading on the third factor were eliminated. The items were

“To what extent you have used mail to gather information before the

purchase of recent MF scheme” and “To what extent you have used

financial portals to gather information before the purchase of recent MF

scheme”. A principal component analysis of remaining 8 items, using

varimax rotations was conducted, with two factors explaining 55.23 %

of variance. A careful analysis of items under construct „depth of

information search‟ indicates that the items under factor 1 and 2,

respectively, measure the depth of formal information search and the

depth of informal information search by MF investors.

Finally, “depth of information processing” construct was

examined for the factorability of the twelve items “depth of information

processing” scale by using correlation method. Result reveals that all the

items correlate at least 0.3 with at least one other item. A principal

component factor analysis of 12 items, using varimax rotations was

conducted, with two factors explaining 58.51 % of variance. A careful

analysis of items under construct „depth of information processing‟

indicates that the items under factor 1 and 2, respectively, measure the

244

depth of non performance attributes processing and the depth of

performance attributes processing by MF investors.

For all the above constructs, the reported eigen value is greater

than 1 and the factor loadings exceed the acceptable threshold level of

0.4 (Hair et al., 2005).

After identifying the dimensionality, the reliability of the

constructs was measured using the Cronbach‟s Alpha (α). Table 6.1

shows that the reliability of all the constructs as measured by the

Cronbach‟s α is above the recommended minimum acceptable value of

0.7 (Hair et al., 2005). Based on the above results, it is concluded that all

the measures are adequate to measure the constructs of the study.

245

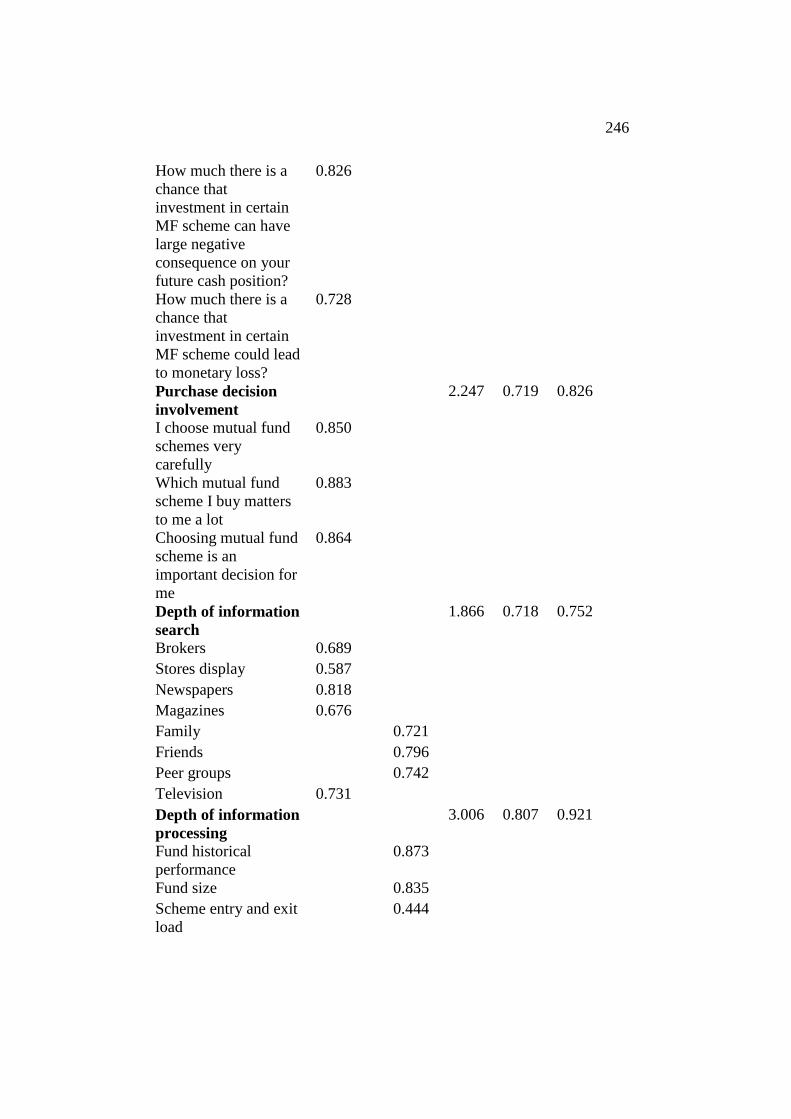

Table 6.1

Dimensionality and reliability of latent research constructs (N=268)

Construct Items Loadings Eigen

Value

KMO Cronbach’s

Alpha

Factor 1 Factor

2

Subjective

knowledge

2.261 0.715 0.836

Compared to average

men and women, I am

very familiar with

wide variety of MF

schemes.

0.892

Compared to my

friends, I am very

familiar with wide

variety of MF

schemes.

0.846

Compared to people

who invest a lot in MF

schemes, I am very

familiar with wide

variety of MF

schemes.

0.866

Perceived purchase

risk

2.385 0.680 0.770

How much there is a

chance that the

agent(s) will mislead

while purchasing MF

scheme?

0.786

How much there is a

chance that there may

be hidden charges

while/after purchasing

MF scheme?

0.745

246

How much there is a

chance that

investment in certain

MF scheme can have

large negative

consequence on your

future cash position?

0.826

How much there is a

chance that

investment in certain

MF scheme could lead

to monetary loss?

0.728

Purchase decision

involvement

2.247 0.719 0.826

I choose mutual fund

schemes very

carefully

0.850

Which mutual fund

scheme I buy matters

to me a lot

0.883

Choosing mutual fund

scheme is an

important decision for

me

0.864

Depth of information

search

1.866 0.718 0.752

Brokers 0.689

Stores display 0.587

Newspapers 0.818

Magazines 0.676

Family 0.721

Friends 0.796

Peer groups 0.742

Television 0.731

Depth of information

processing

3.006 0.807 0.921

Fund historical

performance

0.873

Fund size 0.835

Scheme entry and exit

load

0.444

247

Scheme investment

portfolio

0.631

Favorable rating of

MF scheme

0.554

Clarity of accounting

statement

0.711

Reputation of fund

manager

0.768

Fund manager

background

0.838

Investment style 0.742

Scheme tax benefit 0.623

Pending legislation 0.812

Fund advertisement

expense

0.699

Figure 6.2 represents the proposed investment behaviour model with

measurement items. The model specifies the pattern by which each measure

load on particular factor. Based on the findings of exploratory factor

analysis, depth of information search is measured by the two subscales depth

of formal search (search 1) and depth of informal search (search 2).

Similarly, depth of information processing was measured by two subscales

depth of non- performance attributes processing (processing 1) and depth of

performance attributes processing (processing 2).

248

Figure 6.2

Proposed comprehensive model of investment behaviour with

measurement items

Perceived

purchase risk

Subjective

Knowledge

H1

Purchase

Decision

Involvement

H2

X1 X2 X6

X5

X4

X8

X9

X10

H5a

Extent of

information

processing

X11 X12

X3 X7

H3

Extent of

informati

on search

H4

H5b

X13

X14

249

Note:

X1 Compared to average men and women, I am very familiar with wide variety of MF

schemes; X2 Compared to my friends, I am very familiar with wide variety of MF

schemes; X3 Compared to people who invest a lot in MF schemes, I am very familiar

with wide variety of MF schemes; X4 How much there is a chance that the agent(s)

will mislead while purchasing mutual fund scheme?; X5 How much there is a chance

that there may be hidden charges while/after purchasing mutual fund scheme?; X6

How much there is a chance that investment in certain mutual fund scheme can have

large negative consequence on your future cash position?; X7 How much there is a

chance that investment in certain mutual fund scheme could lead to monetary loss? ;

X8 I choose mutual fund schemes very carefully; X9 Which mutual fund scheme I buy

matters to me a lot; X10 Choosing mutual fund scheme is an important decision for

me; X11 Search 1; X12 Search 2; X13 Processing 1; X14 Processing 2.

6.5.2 Results of the test of discriminant validity of the constructs

In order to test the discriminant validity of each constructs, two

models were tested for each possible pair of estimated constructs. The first,

model was the constrained model where the correlation parameter was

constrained between each pair of construct to 1.00. The, second model was

the unconstrained model (free model) where the correlation parameter

between the two construct was not manipulated (Joreskog, 1971). The χ²

value was generated for both constrained and unconstrained models with the

respective degree of freedom. Afterward, a χ² difference test was performed

250

on the two models. A significantly lower χ² value for unconstrained model

demonstrates that discriminant validity has been achieved (Anderson and

Gerbing, 1988; Bogazzi and Phillips, 1982). Table 6.2 indicates that all the

constructs possesses discriminant validity.

Table 6.2

Results of discriminant validity test

Combination Correlation χ²

(Corr.

Fixed)

d.f χ²

(Corr.

Free)

d.f Change

in χ²

Change

in d.f

Sig.

Level

1 and 2 -0.302 261.2 14 84.4 13 176.8 1 0.001

1 and 3 0.588 61.5 9 19.7 8 41.8 1 0.001

1 and 4 0.257 127.6 20 64.7 19 62.9 1 0.001

1 and 5 -0.05 146.4 9 47.5 8 98.9 1 0.001

1 and 6 0.455 236.9 35 197.8 34 39.1 1 0.001

1 and 7 0.546 57.9 20 26.9 19 31 1 0.001

2 and 3 -0.284 265 14 78.9 13 186.1 1 0.001

2 and 4 -0.274 284.5 27 123 26 161.5 1 0.001

2 and 5 0.005 212.6 14 104.4 13 108.2 1 0.001

2 and 6 -0.385 436.2 44 243.8 43 192.4 1 0.001

2 and 7 -0.444 339.4 27 137.8 26 201.6 1 0.001

3 and 4 0.449 131.5 20 78.9 19 52.6 1 0.001

3 and 5 0.166 108.2 9 20.8 8 87.4 1 0.001

3 and 6 0.411 239.7 35 185.5 34 54.2 1 0.001

3 and 7 0.581 93.2 20 55.9 19 37.3 1 0.001

4 and 5 0.431 149.9 20 104.2 19 45.7 1 0.001

4 and 6 0.604 292.3 54 276.2 53 16.1 1 0.001

4 and 7 0.554 137.2 35 111.8 34 25.4 1 0.001

5 and 6 0.38 267.2 35 212.3 34 54.9 1 0.001

5 and 7 0.408 110.6 20 70 19 40.6 1 0.001

6 and 7 0.741 293.7 54 280.7 53 13 1 0.001

251

Note: Corr. = Correlation; 1 = Subjective Knowledge; 2 = Perceived purchase risk; 3 =

Purchase Decision Involvement; 4 = information search 1; 5 = information search 2; 6

= Information processing 1; 7 = Information processing 2

6.5.3 Results of the test of convergent validity of the constructs

In estimating convergent validity for structure equation modeling

studies, examining the standardized confirmatory factor analysis (CFA)

parameters estimated pattern coefficient is one method often used (Marsh

and Grayson, 1985). Convergent validity can be assessed from the

measurement model by determining whether each indicator‟s estimated

pattern coefficient on its posited underlying construct factor is significant

(Anderson and Gerbing, 1988). Statistically significant large factor loadings

indicate convergent validity. As shown in table 6.3 all of the estimated

pattern coefficients on their posited underlying construct factors were

significant at 0.05 significance level (i.e., each had a critical ratio (cr) >

±1.96). In fact, the smallest critical ratio was 3.84. Therefore, convergent

validity was achieved for all the variables in the study.

252

Table 6.3

Parameter estimates of the proposed five factor model (N=268)

Subj

ectiv

e

Kno

wled

ge

Perc

eive

d

pur

chas

e

risk

Purch

ase

Decisi

on

Involv

ement

Sear

ch1

Sear

ch2

Proc

essin

g 1

Proces

sing 2

X1* Estima

te

1.00

SE

c.r

X2 Estima

te

.77*

*

SE 0.06

c.r 11.7

6

X3 Estima

te

.93*

*

SE 0.07

c.r 12.2

2

X4 Estima

te

.86*

*

SE 0.09

c.r 8.81

X5 Estima

te

.75*

*

SE 0.09

c.r 8.10

X6* Estima

te

1

SE

c.r

X7 Estima

te

.88*

*

253

SE 0.09

c.r 9.52

X8 Estima

te

1.06**

SE 0.09

c.r 11.63

X9* Estima

te

1.00

SE

c.r

X10 Estima

te

.91**

SE 0.07

c.r 11.9

X11 Estima

te

.60**

SE 0.08

c.r 7.38

X12 Estima

te

.50**

SE 0.06

c.r 7.27

X13

*

Estima

te

1.00

SE

c.r

X14 Estima

te

.87**

SE 0.09

c.r 9.52

X15 Estima

te

.82**

SE 0.09

c.r 9.16

X16 Estima

te

.99*

*

SE 0.16

c.r 6.15

X17

*

Estima

te

1.00

254

SE

c.r

X18 Estima

te

.87*

*

SE 0.14

c.r 5.95

X19 Estima

te

1.03*

*

SE 0.07

c.r 13.13

X20 Estima

te

.86**

SE 0.07

c.r 12.17

X21 Estima

te

.75**

SE 0.08

c.r 9.41

X22

*

Estima

te

1.00

SE

c.r

X23 Estima

te

1.03*

*

SE 0.07

c.r 13.84

X24 Estima

te

.82**

SE 0.07

c.r 11.79

X25 Estima

te

.61**

SE 0.06

c.r 9.49

X26

*

Estima

te

1.00

SE

c.r

X27 Estima

te

1.10**

255

SE 0.10

c.r 10.26

X28 Estima

te

.90**

SE 0.10

c.r 8.64

X29 Estima

te

.84**

SE 0.09

c.r 8.84

X30 Estima

te

.38**

SE 0.10

c.r 3.84

Note:

Estimate= Unstandardized parameter estimate; SE = Standard error; cr = Critical ratio

* Variable (indicators) was constrained to 1.0 with the corresponding latent construct

X1 Compared to average men and women, I am very familiar with wide variety of MF

schemes; X2 Compared to my friends, I am very familiar with wide variety of MF

schemes; X3 Compared to people who invest a lot in MF schemes, I am very familiar

with wide variety of MF schemes; X4 How much there is a chance that the agent(s)

will mislead while purchasing mutual fund scheme?; X5 How much there is a chance

that there may be hidden charges while/after purchasing mutual fund scheme?; X6

How much there is a chance that investment in certain mutual fund scheme can have

large negative consequence on your future cash position?; X7 How much there is a

chance that investment in certain mutual fund scheme could lead to monetary loss? ;

X8 I choose mutual fund schemes very carefully; X9 Which mutual fund scheme I buy

matters to me a lot; X10 Choosing mutual fund scheme is an important decision for

me; X11To what extent you have used brokers as a source of information before the

256

purchase of this MF scheme? X12 To what extent you have used stores display as a

source of information before the purchase of this MF scheme?; X13 To what extent

you have used newspapers as a source of information before the purchase of this MF

scheme?; X14 To what extent you have used magazines as a source of information

before the purchase of this MF scheme?; X15 To what extent you have used television

as a source of information before the purchase of this MF scheme?; X16 To what

extent you have used family as a source of information before the purchase of this MF

scheme?; X17 To what extent you have used friends as a source of information before

the purchase of this MF scheme?; X18 To what extent you have used your peer group

as a source of information before the purchase of this MF scheme?; X19 To what

extent you have used scheme investment portfolio for comparing MF schemes

before/at the time of purchase of this scheme?; X20 To what extent you have used

clarity of accounting statement for comparing MF schemes before/at the time of

purchase of this scheme?; X21To what extent you have used reputation of fund

manager for comparing MF schemes before/at the time of purchase of this scheme?;

X22 To what extent you have used fund manager background for comparing MF

schemes before/at the time of purchase of this scheme?; X23 To what extent you have

used fund investment style for comparing MF schemes before/at the time of purchase

of this scheme?; X24To what extent you have used scheme pending legislation for

comparing MF schemes before/at the time of purchase of this scheme?; X25 To what

extent you have used fund advertisement expense for comparing MF schemes before/at

the time of purchase of this scheme?; X26 To what extent you have used fund

historical performance for comparing MF schemes before/at the time of purchase of

this scheme”; X27 To what extent you have used fund size for comparing MF schemes

before/at the time of purchase of this scheme?; X28 To what extent you have used

scheme entry and exit load for comparing MF schemes before/at the time of purchase

257

of this scheme?; X29 To what extent you have used favourable rating of fund scheme

for comparing MF schemes before/at the time of purchase of this scheme?; X30 To

what extent you have used scheme tax benefit for comparing MF schemes before/at the

time of purchase of this scheme?

6.5.4 Test of proposed hypotheses

Table 6.4 presents the mean, standard deviation and correlation among

the study variables. Figures in the diagonal represent the composite

reliability of the scales based on confirmatory factor analysis.

258

Table 6.4

Means, standard deviations, and intercorrelations among study variables

Variables M SD 1 2 3 4 5 6 7

1 Subjective

knowledge

8.73 2.75 0.83

2 Perceived

purchase risk

13.43 3.32 -

0.24**

0.77

3 Purchase

decision

involvement

9.91 2.76 0.50** -

0.24**

0.83

4 Search 1 10.14 4.36 0.23** -

0.21**

0.36** 0.76

5 Search 2 7.06 2.93 0.00 -0.03 0.11 0.32** 0.65

6 Processing 1 16.15 7.31 0.38** -

0.30**

0.36** 0.49** 0.21** 0.88

7 Processing 2 14.69 4.99 0.43** -

0.31**

0.49** 0.47** 0.26** .53** 0.74

Notes:

Figure in the diagonal represents composite reliability of scales

** p< .01 * p<.05

259

The test results of the proposed hypotheses using structural equation

model with maximum likelihood estimate (AMOS 16) are shown in Figure

6.3. Results support the entire proposed hypothesis. SK negatively impact

PPR (path estimate -.274, p<.01). SK positively impact PDI (path estimate

.593, p<.01). PPR negatively impact PDI (path estimate -.143, p<.05). PDI

positively impacts depth of information search (path estimate .483, p<.01).

Depth of information search positively impacts depth of information

processing (path estimate .605, p<.01). PDI positively impacts depth of

information processing (path estimate .408, p< .01).

260

Figure 6.3

AMOS results for proposed comprehensive model of investment

behaviour

* p<.05 ** p<.01

6.5.5 Model fit and test of alternative models

The fit statistics for the hypothesized model is displayed in Table

6.5. As shown in the table, hypothesized model appeared to fit the data

adequately based on the convention used to judge the fit statistics. The chi-

square statistics was nonsignificant and the ratio of chi-square to degree of

freedom was below 3 (Kline, 1998; but see MacCallum, 1998 for cautionary

note), GFI, AGFI, CFI, TLI and IFI statistics were greater than or close to

Perceived purchase

risk

Subjective

knowledge

Purchase

decision

involvement

Information search

behaviour

Information

processing

behaviour

.593**

.408**

.483**

.605**

-.143*

-.274**

261

0.90 (Hair et al., 2005). However RMSEA and SRMR value of 0.08 and 0.07

respectively suggests that the model only adequately fits the data. Based on

the overall analysis of the goodness of fit statistics, and the conventions used

we suggests that model adequately fits the data. The squared multiple

correlations for each structural equation were as follows: perceived purchase

risk, R² =.075; purchase decision involvement, R² =.418; depth of

information search, R² =.233; depth of information processing, R² =.771.

In evaluating a hypothesized model, it is important to compare its fit

to competing models (MacCallum et al., 1993). We estimated the following

alternative models; (a) knowledge mediates the influence of perceived

purchase risk and purchase decision involvement on investment behaviour

(referred to as Alternative 1), were by perceived purchase risk and purchase

decision involvement only directly affected the subjective knowledge which

subsequently influenced investment behaviour; (b) perceived purchase risk

mediates the influence of subjective knowledge and purchase decision

involvement on investment behaviour (referred to as Alternative 2), were by

subjective knowledge and purchase decision involvement only directly

affected the perceived purchase risk which subsequently influenced

investment behaviour.

262

The difference in chi-square between the hypothesized model and

each alternative model was significant. (Alternative 1: Δχ² = 23.54, p<.01;

Alternative 2: Δχ² = 129.68, p<.01), indicating that the alternative models

provided a significantly poorer fit the data than did the hypothesized model.

Moreover the difference between the AIC of the hypothesized model and the

alternative model was also substantial (Alternative 1: ΔAIC = 21.48, p<.01;

Alternative 2: ΔAIC= 127.62, p<.01). The other fit statistics for the

alternative models were also poorer than the hypothesized model.

263

Table 6.5

Fit statistics for hypothesized model

Model χ² Df χ²/df GFI AGFI CFI IFI SRM

R

RMSE

A

AIC

Hypothesized model 188.56 70 2.69 0.911 0.866 0.919 0.920 0.07 0.08 258.56

Alternative model 1 212.04 71 2.98 0.904 0.859 0.904 0.905 0.110 0.08 280.04

Alternative model 2 318.18 71 4.48 0.856 0.787 0.832 0.834 0.171 0.114 386.18

Note. χ² = Chi-square; df = degree of freedom; GFI= goodness-of-fit index; AGFI= adjusted goodness-of-fit index; CFI= comparative fit index; IFI=

Incremental fit index; SRMR= standardized root mean square residual; RMSEA= root-mean-square error of approximation; AIC= Akaike

Information Criterion

264

6.6 Discussion

The hypothesized comprehensive model on the investment behaviour

of MF investor was tested using maximum likelihood estimate (AMOS 16).

Overall, the findings of the study support the hypothesized model.

Specifically, the study finds that (a) SK negatively influence the PPR of MF

investors; (b) SK positively impact PDI of MF investors; (c) PPR negatively

impact PDI of MF investors; (d) PDI positively impact the depth of

information search by MF investors; (e) depth of information search

positively impact the depth of information processing by MF investors; (e)

PDI positively impact the depth of information processing by MF investors.

Following conclusion is drawn based on the findings of the study: First,

investors‟ having high confidence in their knowledge (high SK) related to

MF investment decisions will perceive MF as less risky and is motivated to

actively engage in MF investment decision (high level of PDI). This may be

due to one of the following reasons: (i) MF investors‟ level of objective

knowledge is also high due to exposure to domain knowledge (Alba and

Hutchinson, 2000) or prior experience (Schmidt and Spreng, 1996) of

purchase of MFs, which makes them feel that they have control on the

purchase risk associated with MF; (ii) MF investors‟ are over confident of

265

their information search and processing ability and their ability to control the

risk associated with MF purchase (Tapia and Yermo, 2007). Second,

investors having low confidence in their knowledge (low SK) related to MF

investment decision will perceive MF as more risky and is motivated to

remain passive during MF investment decision (low PDI). The manifestation

of this behaviour will be in form of low depth of information search and

information processing by these categories of investors.This behaviour will

be in the form of low depth of information search and information processing

by these categories of investors. Hence they will use few specific

information sources on which they rely upon (Cho and Lee, 2006; Coleman

et al., 1995; Gemunden, 1985). Further, rather than engaging in extensive

processing of attribute information related to MFs, they will rely on few

attributes which they will use as cues (decision heuristics) as an indicator of

the quality of MFs (Dawar and Parker, 1994; Tapia and Yermo, 2007).

The study makes the following contributions. First, it is one of the

few studies which have proposed an investment behaviour model to

understand the buying behaviour of MF investors and empirically validated it

on the sample of MF investors. Second, few studies have examined the

impact of knowledge, perceived purchase risk and involvement

simultaneously on the buying decision process (Chang and Huang, 2002).

Even though Chang and Huang (2002) studied the joint effect of product

266

involvement and prior knowledge on decision making path, they did not

study how prior knowledge and involvement interact to influence purchase

behaviour? Hence this study is likely to improve consumer behaviour theory

by deepening our understanding of how investors make buying decisions for

the intangible financial goods. Third, the MF regulators across the globe

want to encourage the participation of individual investors with MF product.

However, there is a dearth of empirical research on actual individual

investors and their behaviour to support the policy decisions (Wilcox, 2003).

Most of the well known empirical studies in the field of mutual fund

investment behaviour are based on secondary data which does not capture

the important behavioral stimulus like level of purchase decision

involvement, subjective knowledge, perceived purchase risk etc., which can

be captured by the primary study conducted on the actual investors. Hence,

this study will provide an insight to the regulators and policy makers

regarding the investment behaviour of individual investor.

6.7 Implications

As MF companies spend heavily on marketing of MFs, an

understanding about the investment behaviour of investors is very crucial for

them. Particularly, an understanding of the forces that activate and direct the

behaviour of MF investor is of high importance to MF marketers. This study

267

suggests that investors PDI mediate the influence of investors‟ subjective

knowledge and perceived purchase risk on their investment behaviour.

Further, the study suggests that investors‟ subjective knowledge (which

represents investor‟s confidence on her ability to make MF investment

decision) negatively influence the extent of risk investor attach to the MF

purchase. (i.e. perceived purchase risk) and positively influence the

motivation to engage in purchase decision (i.e. purchase decision

involvement). Hence MF marketers should carve different marketing strategy

for passive investors of MF schemes (investors with low SK, high PPR and

low PDI) and active investors of MF schemes (investors with high SK, low

PPR and high PDI).

Passive investors have following characteristics; (i) engage less in

information search and rely on few specific source for investment advice; (ii)

consider distribution channel as reliable source of information; (iii) engage in

less extensive processing of MF attribute information; (iv) likely to use

mental shortcuts (i.e. rule of thumb) to evaluate and select MF schemes for

example historical performance of funds (Benartzi and Thaler, 2001;

Huberman and Jiang, 2006); and (v) likely to show a preference towards

default funds/index funds. Hence, the above characteristic of these investors

may be effectively used to design and promote the MF schemes. Specifically,

MF companies should promote index fund among these categories of

268

investors. MF companies can also design innovative „default funds‟, like

teachers specific fund directed towards academicians, doctor specific fund

directed towards doctors etc. to tap these categories of investors. Further, MF

companies should effectively use their distribution channel to promote their

funds among these categories of investors. Finally, advertisement can be

more effectively targeted towards these investors rather than active investors

where the role of advertisement is somewhat limited.

Active investors have following characteristics; (i) engage

extensively for information search and rely on multiple sources of

information; and (ii) engage in extensive information processing and use

multiple attribute information to compare MF schemes. As these categories

of MF investor use large number of attributes information, they are likely to

restrict their attention to fewer number of brands during the choice of a MF

(i.e. will use brand by brand comparison) (Powell and Ansic, 1997). Hence

those MF schemes/companies which are part of the consideration set will

have more probability for being selected in comparison to those which are

not. Hence, while targeting these categories of MF investors MFCs faces a

challenge to be among the top four or five names so that they become the

part of the consideration set of these categories of MF investors. Active

investors, if engaged in the promotion of MF schemes, will effectively help

MFCs in promoting their funds.

269

The findings of the study have also implications for the MF industry

regulators. First, in order to improve the quality of decision of active MF

investors (investors with high SK), regulators and policy makers requires

having a check on the information overload. There is large empirical

evidence suggesting the notion that large number of investment options can

cause information overload (Tapia and Yermo, 2007). Hence, MF companies

should be discouraged to introduce “new fund offer” which is similar to the

existing schemes of the MF Company. Second, investors with low SK

perceive high risk in MF purchase and will remain passive during investment

decision making process (low PDI). It has been found in the earlier chapter

in this thesis that those investors who feel less confident to engage actively

in information search and processing are the one who rely more on the

distribution channels for investment advice (chapter 3, pg. 105). However,

there is adequate empirical evidence to doubt the quality of financial advice

provided by these professional due to conflict in the objective of investors

and advisor (Mahoney, 2004), lack of knowledge of advisor (Minimum

common standard for financial advisors and financial education: A

consultation paper79

), and disparity in the definition of “low risk” between

investor and advisor (Conquest Research Limited, 2004). Hence policy

makers and regulators of MF industry have to work on manifold objectives.

79

Minimum Common Standard for Financial Advisors and Financial Education : A

Consultation Paper retrieved from

http://pfrda.org.in/writereaddata/linkimages/Consultation%20Paper9207652836.pdf

270

First, strengthen the existing policy of certification and training of

distribution channels/ financial advisors to ensure that these professionals are

adequately equipped and motivated to guide investors in selecting

appropriate MF schemes. Second, encourage investors to actively engage in

investment decision by advancing their knowledge on various facets of

financial planning. Third, reduce ambiguity surrounding MF products

through effective mass communication media so that investors are rightly

able to appreciate the risk associated with MF products. Fourth, bring

measures to enhance the transparency in the working of MF industry and put

a check on mis-selling. Fifth, put mechanism in place so that financial

education program can be introduced at the school level as investment

decision substantially influence the financial well being of individuals.

6.8 Limitations and future direction of research

The findings of the study are constrained by the following

limitations. First, the study focuses on the prepurchase information search

behaviour and information processing behaviour of MF investors and the

post purchase behaviour is not discussed. Second, depth of information

processing behaviour has been discussed with reference to the extent to

271

which each type of attributes information are used by MF investors before/at

the time of purchase of MF schemes. However, more insights can be

achieved with an understanding of the sequence in which attributes

information are used, the number of stages in which the decision is taken and

the number of MF schemes considered at various stages of information

processing. Third, post purchase perceived risk of MF investors have been

measured in this study. It may be possible that there is a difference in

prepurchase perceived risk and post purchase perceived risk due to the effect

of actual purchase on perceived risk of the respondents. A natural expansion

of this study is to empirically validate this model on the sample of investors

whose prepurchase risk as well as post purchase risk is captured. This will

also capture investors post purchase regret which is not included in this

study. Fourth, the literature suggests that apart from subjective knowledge,

perceived purchase risk is also likely to be influenced by demographic

variables like age, income, wealth, gender, marital status, personality and

educational attainment (Finke and Huston, 2003; Rajarajan, 2000, 2003).

However, the study did not controlled for the effect of other variables on

perceived purchase risk due to limitation related to the sample size and

nature of respondents. This was also reflected in the squared multiple

correlations of the structural equation for perceived purchase risk (i.e. R²

=.075). The above limitation provides the future scope of research in this

field. Fifth, the sample selected for the study is through convenience

272

sampling due to non avaibility of data on MF investors. Due consideration

was given to check the validity and internal consistency of the data however

care has to be taken while generalizing upon the results. Further, use of

random sampling method to select respondents would have further improved

the statistical validity of the findings. Sixth, the study is conducted using the

respondents from the Jammu region, J&K (India). To further validate the

results similar study needs to be conducted on the residents of other region,

states and countries. Seventh, the study is confined to individual investors of

MF schemes and institutional investors are excluded from the study.

Therefore, including other categories of investors‟ might lead to different

behavioural outcome.

6.9 Conclusion

The MF industry has experienced phenomenal growth over the past

decade. In spite of that there has been limited research into the way MF

schemes are purchased by investors. This study proposes a comprehensive

model of investment behaviour of MF investors to explain their information

search and processing behaviour. The role of marketers and regulators has

also been outlined in the process.