chapter 5 structured questions list a list...

TRANSCRIPT

CHAPTER 5 – STRUCTURED QUESTIONS

1.

Match the transactions in List A with the Books of Original Entry in List B

LIST A LIST B

1. Sales on credit a) Petty cash

2. Purchases on credit b) Sales

3. Goods sold to customers were

overcharged

c)Returns outwards

4. Goods bought were returned to the

supplier for exchange

d) Purchases

5. Cash received and Cheques paid out e) Returns Inwards

6. Small sums of cash paid out f) Cash

2.

June 10th 20—Russell Babb from 7 Downtown Road, Santa Cruz, Barbados prepared a

document for Shirley of 10 Alltheway Road, Belize. Shirley sent Purchase Order #205 to

Russell requesting the following items:

PURCHASE ORDER

QUANTITY DESCRIPTION PRICE PER UNIT TOTAL

100 Cases of Quaker oats $180 $18 000

16 Cases of evaporated

milk

$200 $ 3 200

10 Bales of flour $500 $ 5 000

TOTAL COST $26 200

(a) What is the name of the document prepared by Russell Babb?

(b)In which book of original entry will Russell Babb enter the above transaction?

(c)Who is the creditor in the transaction, is it Russell or Shirley?

(d) Assume that Shirley decides to settle her account, which book of original entry will

Russell record the entry?

3.

Explain the difference between trade discount and cash discount?

4.

Gaynelle owns a bookstore. On August 13th she received the credit note shown below

from Gay Distributors Limited

Gay Distributors Limited

Tinstown

Trinidad

CREDIT NOTE

C/N – 101

TO: Gaynelle Bookstores Limited

Coffee Street

Trinidad

DATE DETAILS QUANTITY/PRICE $

August 13 Boxes of Modern

Studies textbooks

damaged in transit

and returned

10 boxes @ $1 000

per box

?????

(a) Calculate the missing amount at (???) on the credit note and enter it in the box

(b)Apart from damaged books being returned to Gaynelle, give another reason that a

credit note may be issued?

(c)In the books of Gaynelle Bookstores Limited, in which book of original entry will the

transaction be posted?

5.

Explain briefly the rule (procedures) for journalizing entries in the general journal?

CHAPTER 5 – ANSWERS

1.

LIST A LIST B

1. B

2. D

3. E

4. C

5. F

6. A

2.

(a) Invoice

(b)Sales

(c)Russell Babb

(d)Cash book

3.

Trade discount

- offered to customers who normally make large purchases

-the amount is deducted from the original price and shown on the invoice as the amount

to be paid

Cash discount

-are only offered to credit customers

-used to encourage customers to pay the full amount due earlier than the final date

4.

(a) $10 000

(b) When goods are overcharged

(c)Returns inward (Sales returns)

5.

-record the debit entry first

-then record the credit entry

-values in the debit and credit entry columns must be equal

-give a description (narration) of the entire transaction

CHAPTER 6 – STRUCTURED QUESTIONS

1.

You are to open the books of Lazeena’s Clothing Store a trader. Record the daily

transactions below for the month of July to the appropriate journals, post to the ledger,

close the ledger (showing the transfers to the relevant final account) and prepare a trial

balance

July 1 Assets: Buildings $100 000; Furniture $20 000; Stock $3 000; Debtors: Lynette

$2 000; Cash

At bank $4 000; Cash in hand $500

Liabilities: Creditors: Margaret Box $800

1 Bought goods on credit from Margaret Box $1 000 and D. Lopez 1 500

7 Sold goods on credit to Lynette $1 000 and P. Singh $800

10 Paid for wages by cheque $3 000

11 Goods returned to Lynette $200 and P. Singh $100

18 Lazeena received cheques less 2% discount from the following persons: Lynette

and P. Singh

20 The following creditors were settled by cheques less 7% discount: Margaret Box

and D. Lopez

2. Indicate the books of original entry which EACH of the following transactions would

be recorded and mark (/) the appropriate column

GENERAL

JOURNAL

CASH

BOOK

SALES PURCHASES SALES

RETURNS

PURCHASES

RETURNS

PETTY

CASH

Started

business

with

debtors

Received

cash

Bought

goods

from a

supplier

Sold

goods to a

customer

Bought

postage

stamps for

$20

Goods

returned

to a

supplier

Customers

returned

goods for

exchange

3.

Give the name of the ledger used to record the following:

(a) Goods sold on credit

(b) Revenues and expenses

(c) Goods bought on credit

4.

Categorize the following transactions under the appropriate classification of business

transactions

REVENUE

EXPENDITURE

CAPITAL

EXPENDITURE

REVENUE

RECEIPT

CAPITAL

RECEIPT

Salaries paid to

workers

Paid a plumber

to fix a burst

water line

Purchased a

machine

Received

payment for

commissions

Goods sold for

cash

Received a 20

year bank loan

The owner

invested

additional

capital into the

business

CHAPTER 6 – ANSWERS

1.

GENERAL JOURNAL

DATE DETAILS DR CR

July 1 Buildings 100 000

Furniture 20 000

Stock 3 000

Debtor: Lynette 2 000

Cash at bank 4 000

Creditors:

Margaret Box

800

Capital: Lazeena 128 700

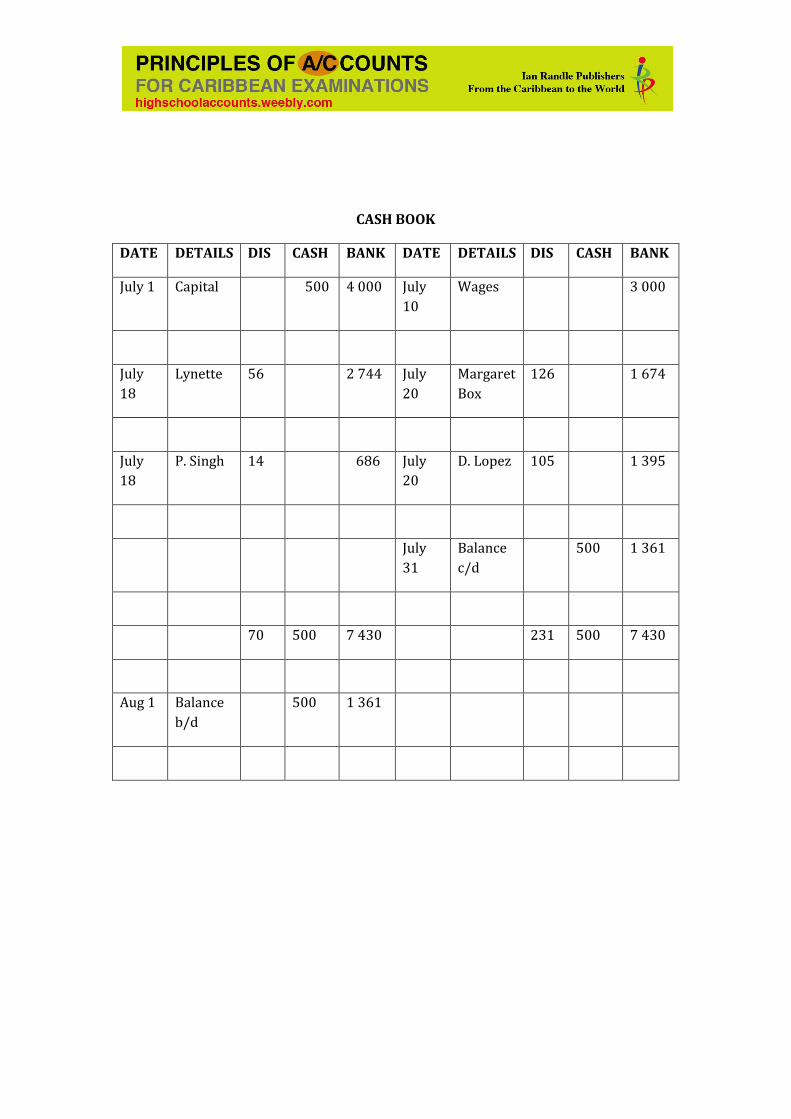

CASH BOOK

DATE DETAILS DIS CASH BANK DATE DETAILS DIS CASH BANK

July 1 Capital 500 4 000 July

10

Wages 3 000

July

18

Lynette 56 2 744 July

20

Margaret

Box

126 1 674

July

18

P. Singh 14 686 July

20

D. Lopez 105 1 395

July

31

Balance

c/d

500 1 361

70 500 7 430 231 500 7 430

Aug 1 Balance

b/d

500 1 361

SALES JOURNAL

DATE DETAILS AMOUNT

July 7 Lynette 1 000

P. Singh 800

TOTAL SALES 1 800

PURCHASES JOURNAL

DATE DETAILS AMOUNT

July 1 Margaret Box 1 000

D. Lopez 1 500

TOTAL PURCHASES 2 500

RETURNS INWARD JOURNAL

DATE DETAILS AMOUNT

July 11 Lynette 200

P. Singh 100

TOTAL RETURNS INWARDS 300

GENERAL LEDGER

Buildings a/c

July 1 Capital $100

000

July 31 Balance c/d $100

000

Aug 1 Balance b/d 100

000

Furniture a/c

July 1 Capital $20

000

July 31 Balance c/d $20

000

Aug 1 Balance c/d 20

000

Returns Inwards a/c

July 31 Total returns

$300

July 31 Balance c/d to Trading a/c

$300

Stock a/c

July 1 Capital $3

000

July 31 Balance c/d to Trading a/c

$3 000

Purchases a/c

July 11 Total purchases

$2 500

July 31 Balance c/d to Trading a/c

$2 500

Capital a/c

July 31 Balance c/d

$128 700

July 1 Balance b/d $128

700

Aug 1 Balance b/d

128 700

Sales a/c

July 31 Balance c/d to Trading a/c

$1 800

July 31 Total sales $1

800

Wages Expenses a/c

July 10 Bank

$3 000

July 31 Balance c/d to Profit and Loss

a/c $3 000

Discount Allowed a/c

July 31 Total Discounts

$ 70

July 31 Balance c/d to Profit and Loss a/c

$70

Discount Received a/c

July 31 Balance c/d d to Profit and Loss

a/c $231

July 31 Total Discounts

$231

DEBTORS LEDGER

Lynette a/c

July 1 Capital $2

000

July 11 Returns In $

200

7 Sales 1

000

18 Bank

2 744

Discount allowed

56

3

000

3

000

P. Singh a/c

July 7 Sales

$800

July 1 Returns In

$100

18 Bank

686

Discount allowed

14

800

800

CREDITORS LEDGER

Margaret Box a/c

July 20 Bank $1

674

July 1 Capital

$800

Discount received

126

1 Purchases 1

000

1

800

1

800

D. Lopez a/c

July 20 Bank $1

395

July 1 Purchases $1

500

Discount received

105

1

500

1 500

Lazeena’s Clothing Store

Trial Balance

As at July 31st

Dr. Cr.

Cash $ 500

Bank 1 361

Returns inwards 300

Purchases 2 500

Sales 1 800

Discount allowed 70

Building 100 000

Furniture 20 000

Stock 3 000

Capital 128 700

Wages 3 000

Discount received 231

130 731 130 731

2.

GENERAL

JOURNAL

CASH

BOOK

SALES PURCHASES SALES

RETURNS

PURCHASES

RETURNS

PETTY

CASH

Started

business

with

debtors

/

Received

cash

/

Bought

goods

from a

supplier

/

Sold goods

to a

customer

/

Bought

postage

stamps for

$20

/

Goods

returned

to a

supplier

/

Customers

returned

goods for

exchange

/

3.

(a) Sales (Debtor)

(b) General

(c)Purchases (Creditor)

4.

REVENUE

EXPENDITURE

CAPITAL

EXPENDITURE

REVENUE

RECEIPT

CAPITAL

RECEIPT

Salaries paid to

workers

/

Paid a plumber

to fix a burst

water line

/

Purchased a

machine

/

Received

payment for

commissions

/

Goods sold for

cash

/

Received a 20

year bank loan

/

The owner

invested

additional capital

into the business

/