chapter 36 - lipsey. financial assets wealthbonds interest earning assets claims on real capital...

TRANSCRIPT

THE ROLE OF MONEY IN MACROECONOMICS

Chapter 36 - Lipsey

FINANCIAL ASSETS

Wealth

Bonds

Interest earning assets

Claims on real capital

Money

Medium of exchange

THE RATE OF INTEREST AND PRESENT VALUE

• Present Value – of a bond or any asset refers to the value now of the future payments to which the asset represents a claim

Present Value = Future Value/(1+interest rate)n

• Present value of an asset is negatively related to the interest rate

PRESENT VALUE AND MARKET PRICE • Present value is important because it establishes the

market price for an asset• In a free market, the equilibrium price of any asset

will be the present value of the income stream that it produces.

THE RATE OF INTEREST AND MARKET PRICE

• A rise in the market price of an asset is equivalent to a decrease in the rate of interest earned.

• The sooner is the maturity date of a bond, the less responsive bond value is to interest rate changes.

THE SUPPLY OF MONEY

• Money supply is a stock and not flow

• Monetary authorities (Central Bank) control

the total money stock directly.

• In other words money supply is exogenously

fixed by policy-makers.

DEMAND FOR MONEY

• The opportunity cost of holding money is the extra interest that could have been earned if that money were used to purchase bonds.

• Motives of holding money– Transactions Motive– Precautionary Motive– Speculative Motive

REAL AND NOMINAL MONEY BALANCES

Nominal money demand

The demand for money in monetary units.

Real money demand

Number of units of purchasing power that the public wishes

to hold in the form of money balances expressed in constant

prices.

Real Money Demand = (Nominal money demand/Price level)

The Quantity Theory of Money

1. Demand for money = Value of transactions (k) *Nominal Income (PY)MD = kPY

2. Supply of money set by the Central BankMS = M

3. Equilibrium: Money demand = Money SupplyMD = MS

4. Substituting equations 1 and 2 into 3 yields M = kPY

5. Velocity of Money (V): assumed as a constant V = 1/k

Therefore quantity theory of money is presented by:MV = PY

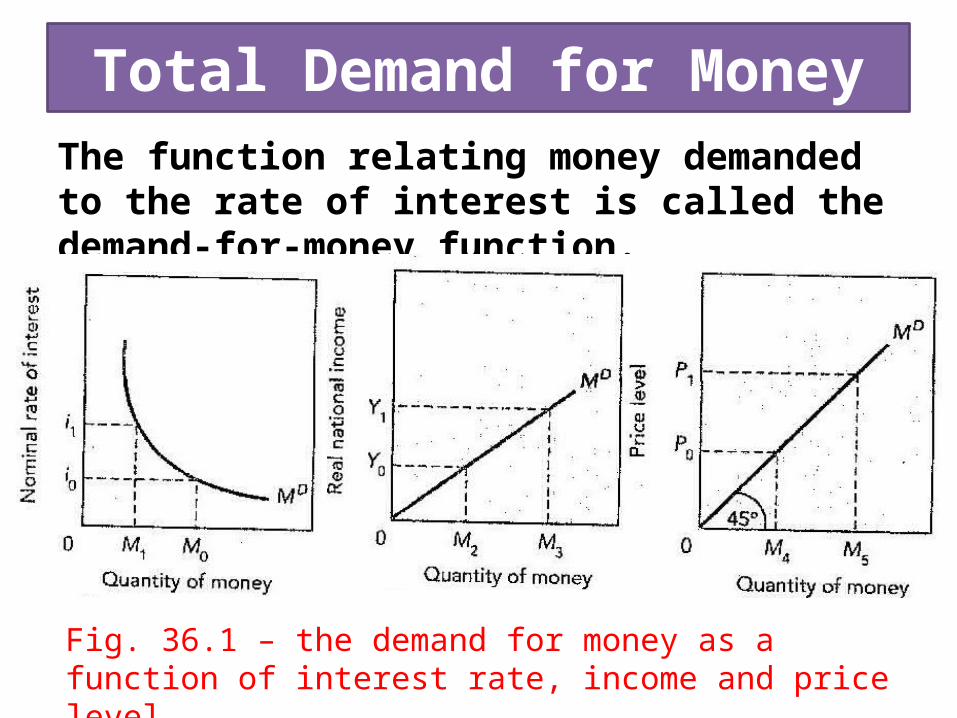

Total Demand for MoneyThe function relating money demanded to the rate of interest is called the demand-for-money function.

Fig. 36.1 – the demand for money as a function of interest rate, income and price level.

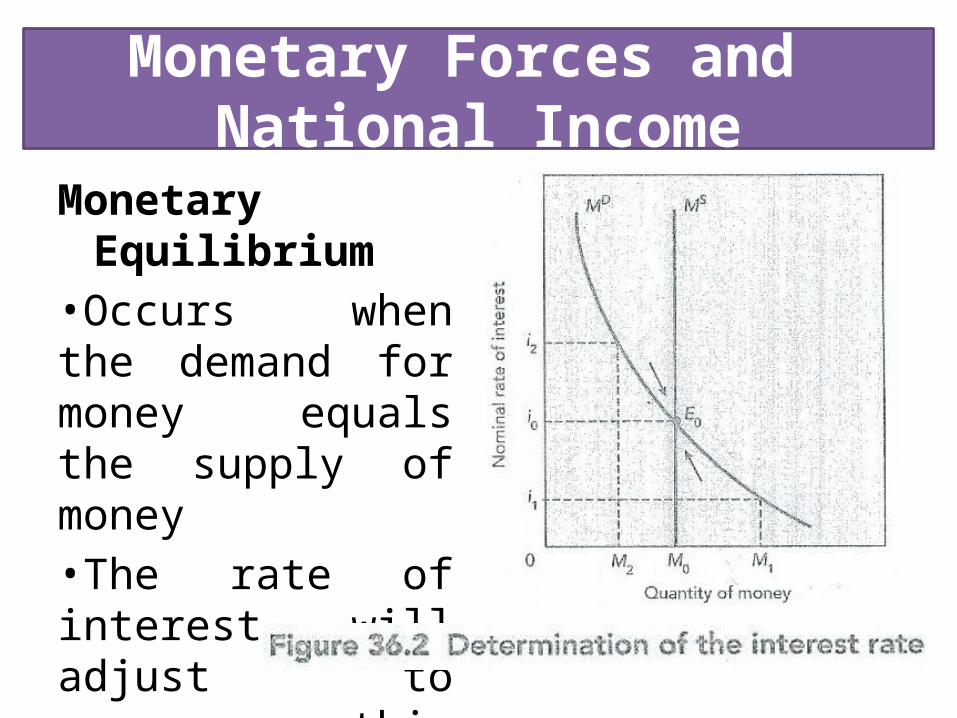

Monetary Forces and National Income

Monetary Equilibrium•Occurs when the demand for money equals the supply of money•The rate of interest will adjust to ensure this equilibrium

THE TRANSMISSION MECHANISM

Monetary disturbances cause interest rate to change.

Changes in interest rate affect investment expenditure.

Investment expenditure in turn affect aggregate demand.

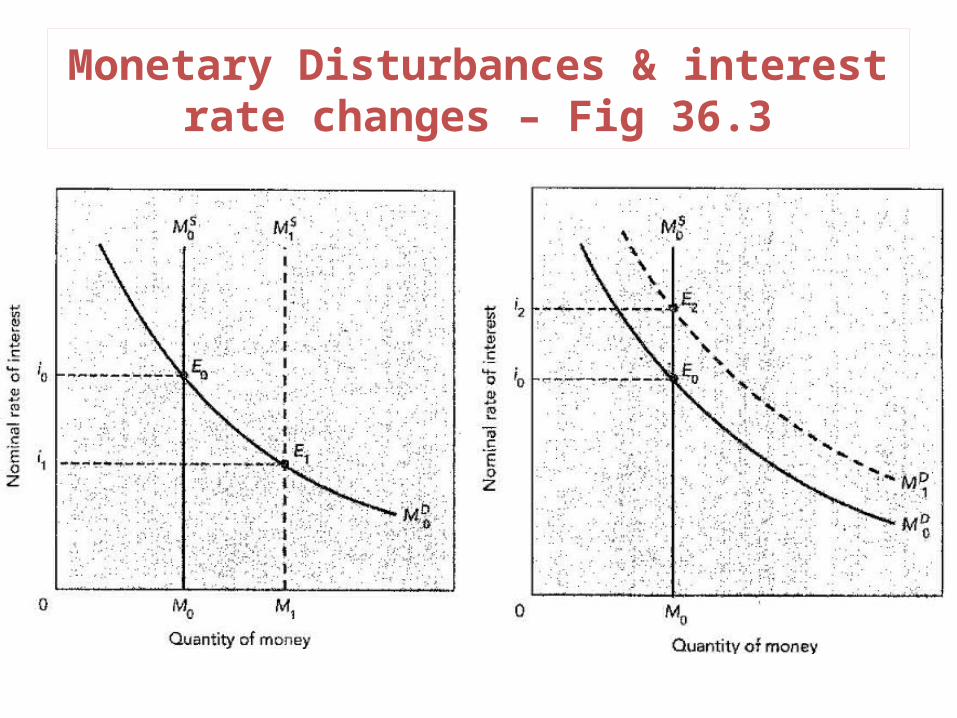

Monetary Disturbances & interest rate changes – Fig 36.3

The effects of changes in money supply on investment expenditure – Fig 36.4

The effects of changes in money supply on aggregate demand –Fig 36.5

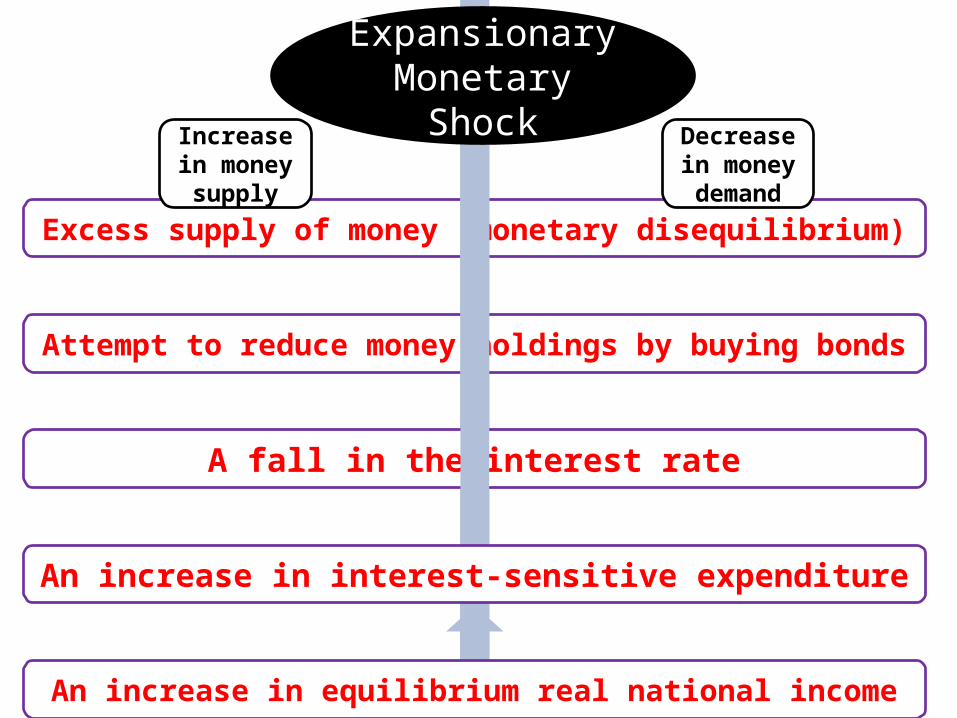

Excess supply of money (monetary disequilibrium)

Attempt to reduce money holdings by buying bonds

A fall in the interest rate

An increase in interest-sensitive expenditure

An increase in equilibrium real national income

Expansionary Monetary Shock

Increase in money supply

Decrease in money

demand

Excess Demand for money (monetary disequilibrium)

Attempt to increase money holdings by selling bonds

A rise in the interest rate

An reduction in interest-sensitive expenditure

An reduction in equilibrium real national income

Contractionary Monetary Shock

Decrease in money supply

Increase in money

demand

AN ALTERNATIVE DERIVATION OF THE AGGREGATE DEMAND

CURVE:

IS/LM

THE IS CURVEFIG. 36.7

• The IS curve shows the equilibrium level of national income associated with each given rate of interest

• Equilibrium in the goods market

THE LM CURVE

FIG. 36.8 The LM curve shows the combinations of national income and the interest rate that are consistent with the equality of money demand and supply and given price level.

IS-LM AND AGGREGATE DEMAND

FIG. 36.9 – the AD curve plots the IS-LM equilibrium level of national income for each given price level, holding all exogenous expenditures and the nominal money supply constant.

AGGREGATE DEMAND, THE PRICE LEVEL, AND

NATIONAL INCOME

THE EFFECT OF A MONEY SUPPLY CHANGE IN THE SHORT RUN

• An increase in money supply in the short run – shifts LM to the right – shifts AD to the right – upward pressure on prices – real money supply falls & wealth effects – IS and LM shift left slightly to point A.

THE EFFECT OF A MONEY SUPPLY CHANGE IN THE LONG RUN

• An increase in money supply in the long run – LM shifts to the right – AD shifts to the right – prices rise – inflationary gap drive wages higher – shift leftward in SRAS curve increasing prices more – leftward shift in IS & LM. Output returns to potential level.

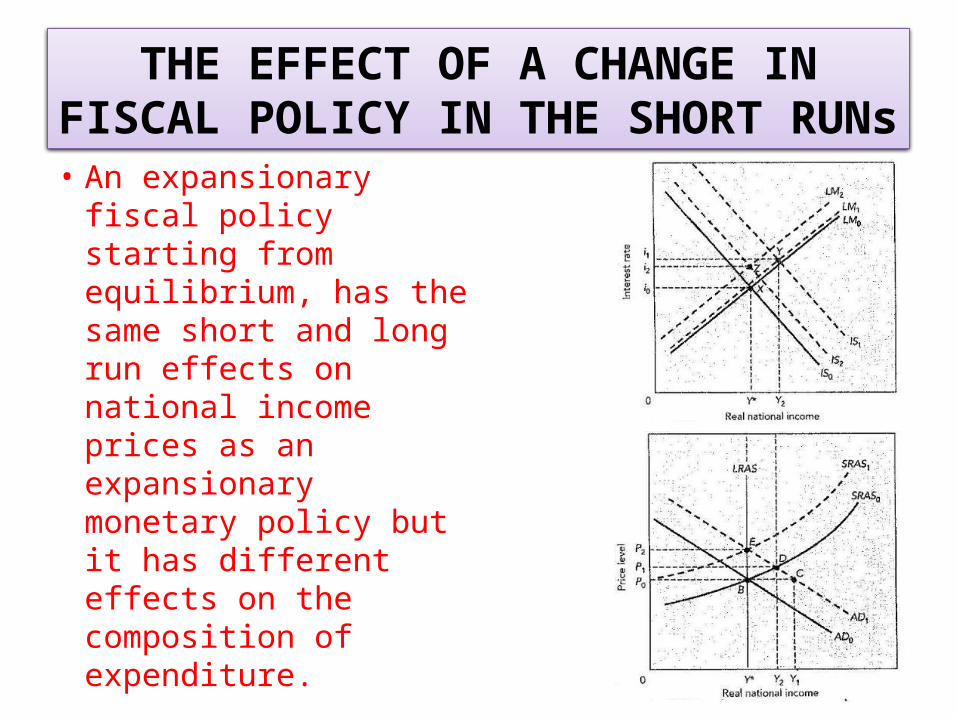

THE EFFECT OF A CHANGE IN FISCAL POLICY IN THE SHORT RUNs

• An expansionary fiscal policy starting from equilibrium, has the same short and long run effects on national income prices as an expansionary monetary policy but it has different effects on the composition of expenditure.

THE EFFECT OF A CHANGE IN FISCAL POLICY IN THE LONG RUN

• The adjustment from the long to short run case is the same for fiscal policy changes as for monetary policy since it involves a leftward shift in the SRAS curve which results from increases in input prices specially wages.

• There may long run implications of the fact that the government is now running a budget deficit when it was not before.