chapter 31 the cost of credit. interest calculations - determining factors interest rates – the...

TRANSCRIPT

Chapter 31

The Cost of Credit

Interest Calculations - Determining Factors

Interest Rates – The percentage that is applied to your debt expressed as a fraction or decimal.

Principal – The amount of debt to which the interest rate is applied.

Time Factor – The length of time for which interest will be charged. Let’s look at the way interest is computed on loans.

Interest Calculations

Simple Interest – An expression of interest based on a one-year period of time.

This is the Interest often used on Single-Payment Loans.

Formula = I (Interest) = P (Principal) X R (Rate) X T (Time)

Simple Interest - Examples

If $1000 is borrowed at 9 percent for one year…

I = Principal x Rate x Time

I = 1000 x .09 x 1 = $90

Rules for Computing Simple Interest

In order to figure out the interest on this problem, there are three things to remember…1. The interest rate must be expressed in the

form of a fraction or decimal.

2. Interest is charged for each dollar or part of a dollar borrowed.

3. The interest rate is based upon one year of time.

Rule 1 – Simple Interest

The interest rate must be expressed in the form of a fraction or decimal.

An interest rate of 12 percent would be expressed as either a

– fraction = 12/100 or a – decimal = .12

Rule 2 – Simple Interest

Interest is charged for each dollar or part of a dollar borrowed.

So, if the interest rate is 12 percent, that means that you must pay 12 cents for each dollar you borrow for a year.

Thus if you borrow $1 at 12 percent, you will pay $ .12 for the year. If you borrowed $2 at 12 percent, you will pay $ .24 for the year.

Rule 3 – Simple Interest

The interest rate is based upon one year of time.

So, if you borrow $100 at 12 percent for one year, you must repay the $100 plus the $12 of interest for the year. If you borrow the same amount, at the same rate, for two years, you must repay the $100 plus the $24 of interest for the two years.

Maturity Dates

Maturity Date – – The date on which a loan must be repaid.

Determining Maturity Dates – – When the time of the loan is stated in months, the

date of maturity is the same day of the month as the date on which the loan was made.

Started on Jan. 15….maturity date for one month would be Feb. 15

Two months would mean March 15

More on Maturity Dates

Determining Maturity Dates for a loan given in days. The would mean that the exact number of days would have to be counted.

So if the loan were made on January 10, there would be 21 days left in the month to be counted. Then add the days in the following months until the total equals the required number of days.

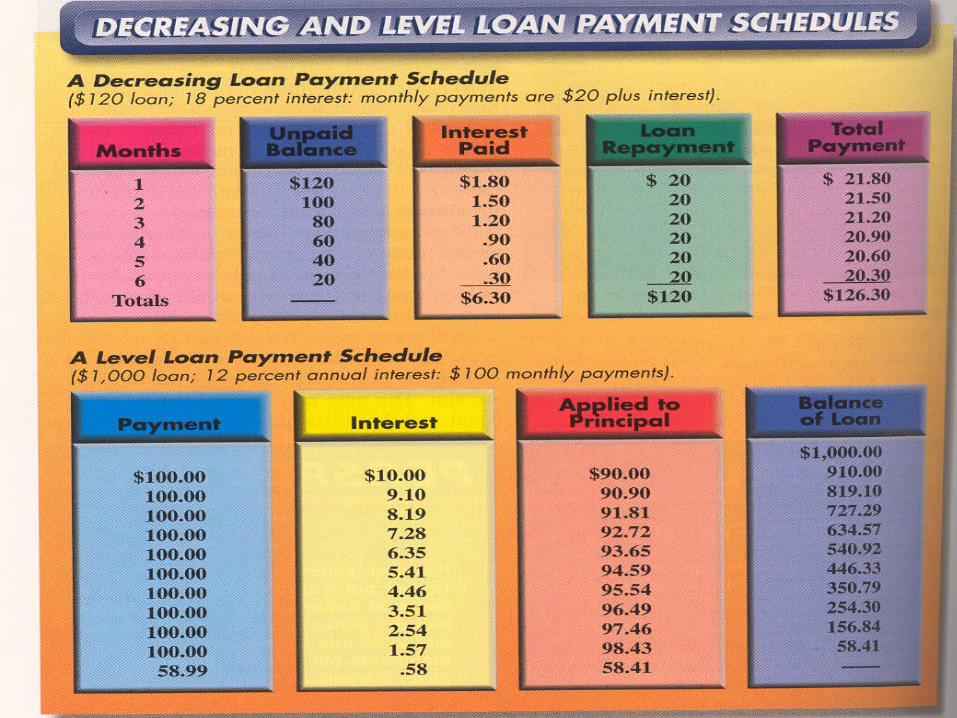

Installed Interest

A loan that is repaid in partial payments is called an Installment Loan.

Installment Loans are offered from many banks, savings and loan associations, credit unions, and consumer finance companies.

On an installment loan, the borrower is usually given a schedule of payments, or a payment book, that shows how much is to be paid each month.

Installment Loan – Payment Options

Based on the figuring of Interest, some loans are better to be paid off in different schedules.

The most common way would be to make equal payments each month until the borrower has paid the lender back the entire loan.

While on some loans, the interest is calculated on the amount that is unpaid at the end of each month.

Payment Schedules

Finance Charges

Annual Percentage Rate (APR) – is a disclosure required by law, and it states the percentage cost of credit on a yearly basis.

In addition to interest, the APR includes other charges that may be made.

Service Fees are made to cover the cost of any expense that the creditor might incur due to your borrowing of their money.

Credit Insurance

Most of the time with loans, credit insurance is paid for in these service fees.

Credit Insurance – – Special insurance that repays the balance of the amount owed

if the borrower dies or becomes disabled prior to the full settlement of the loan.

Credit Insurance, Interest, and any other fees that lender might charge you for your loan, makes up the finance charges of your loan.

– These Finance Charges need to be completely expressed in the written contract.

Credit Alternatives

Borrowing money is costly. Always make sure that you are borrowing from

the right place and getting the best possible deal for your loan.

Things to look for…– APR– Amount of Monthly Payments– Finance Charges

Final Thoughts…

“Effectively used, credit can help you have more and enjoy more. Misused, credit can result in excessive debt, loss of reputation, and even bankruptcy.”