chapter 3

DESCRIPTION

Time Value of MoneyTRANSCRIPT

Contemporary Engineering Economics, 4th

edition ©2007

Time Value of Money

Lecture No.4Chapter 3Contemporary Engineering EconomicsCopyright © 2006

Contemporary Engineering Economics, 4th

edition © 2007

Time Value of MoneyMoney has a time value because it can earn more money over time (earning power).Money has a time value because its purchasing power changes over time (inflation).Time value of money is measured in terms of interest rate.Interest is the cost of money—a cost to the borrower and an earning to the lender

This a two-edged sword whereby earning grows, but purchasing power decreases (due to inflation), as time goes by.

Contemporary Engineering Economics, 4th

edition © 2007

The Interest Rate

Contemporary Engineering Economics, 4th

edition © 2007

Practice Problem

Problem StatementIf you deposit $100 now (n = 0) and $200 two years from now (n = 2) in a savings account that pays 10% interest, how much would you have at the end of year 10?

Contemporary Engineering Economics, 4th

edition © 2007

Solution

0 1 2 3 4 5 6 7 8 9 10

$100$200

F

10

8

$100(1 0.10) $100(2.59) $259$200(1 0.10) $200(2.14) $429

$259 $429 $688F

+ = =

+ = == + =

Contemporary Engineering Economics, 4th

edition © 2007

Practice problem

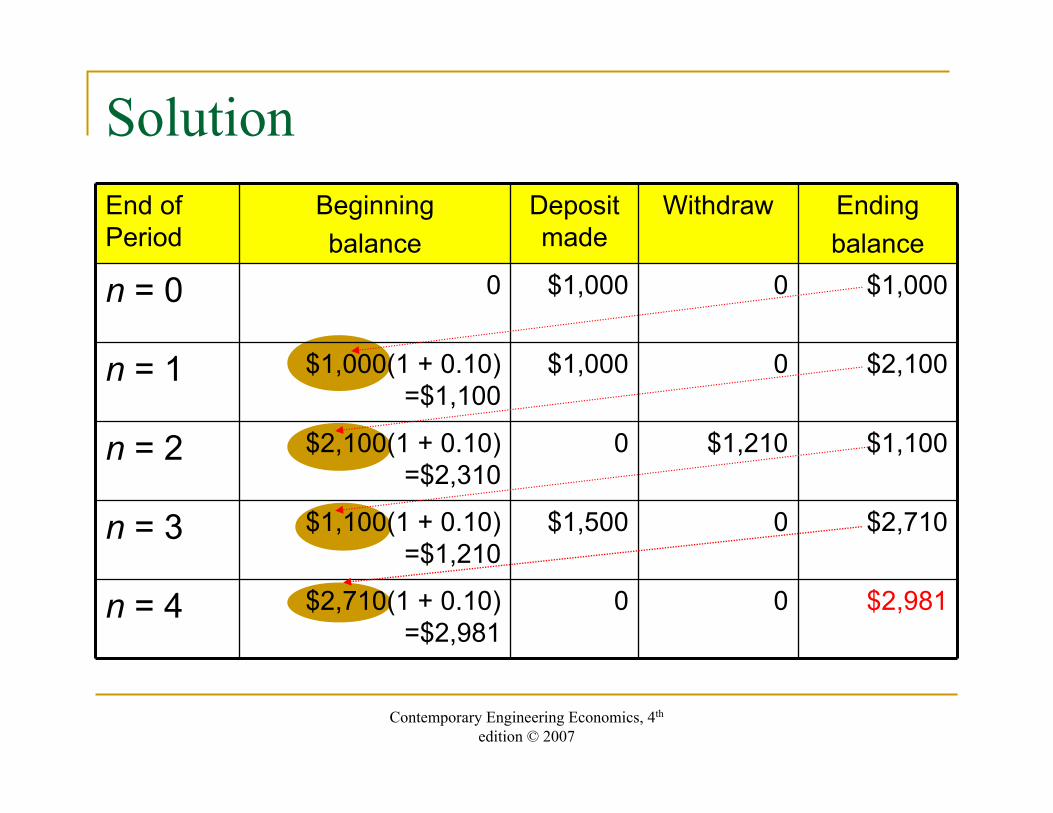

Problem StatementConsider the following sequence of deposits and withdrawals over a period of 4 years. If you earn a 10% interest, what would be the balance at the end of 4 years?

$1,000 $1,500

$1,210

0 1

2 3

4?

$1,000

Contemporary Engineering Economics, 4th

edition © 2007

$1,000$1,500

$1,210

0 1

2

3

4

?

$1,000

$1,100

$2,100 $2,310

-$1,210

$1,100

$1,210

+ $1,500

$2,710

$2,981

$1,000

Contemporary Engineering Economics, 4th

edition © 2007

SolutionEnd of Period

Beginningbalance

Deposit made

Withdraw Endingbalance

n = 0 0 $1,000 0 $1,000

n = 1 $1,000(1 + 0.10) =$1,100

$1,000 0 $2,100

n = 2 $2,100(1 + 0.10) =$2,310

0 $1,210 $1,100

n = 3 $1,100(1 + 0.10) =$1,210

$1,500 0 $2,710

n = 4 $2,710(1 + 0.10) =$2,981

0 0 $2,981

Contemporary Engineering Economics, 4th

edition ©2007

Economic Equivalence

Lecture No.5Chapter 3Contemporary Engineering EconomicsCopyright © 2006

Contemporary Engineering Economics, 4th

edition © 2007

Economic Equivalence

Economic equivalence exists between cash flows that have the same economic effectand could therefore be traded for one another.Even though the amounts and timing of the cash flows may differ, the appropriate interest rate makes them equal.

Contemporary Engineering Economics, 4th

edition © 2007

If you deposit P dollars today for N periods at i, you will have Fdollars at the end of period N.

N

F

P

0

NiPF )1( +=

Equivalence from Personal Financing Point of View

P F≡

Contemporary Engineering Economics, 4th

edition © 2007

F dollars at the end of period N is equal to a single sum P dollars now, if your earning power is measured in terms of interest rate i.

N

F

P

0

(1 ) NP F i −= +

Alternate Way of Defining Equivalence

N0

Contemporary Engineering Economics, 4th

edition © 2007

Practice Problem

0 1 2 33 4 5

$2,042

5

F

0

At an 8% interest, what is the equivalent worth of $2,042 now in 5 years?

If you deposit $2,042 today in a savingsaccount that pays an 8% interest annually.how much would you have at the end of5 years?

=

Contemporary Engineering Economics, 4th

edition © 2007

Solution

5$2,042(1 0.08)$3,000

F= +=

Contemporary Engineering Economics, 4th

edition ©2007

Interest Formulas for Single Cash Flows

Lecture No.6Chapter 3Contemporary Engineering EconomicsCopyright © 2006

Contemporary Engineering Economics, 4th

edition © 2007

Types of Common Cash Flows in Engineering Economics

Contemporary Engineering Economics, 4th

edition © 2007

Equivalence Relationship Between P and F

Contemporary Engineering Economics, 4th

edition © 2007

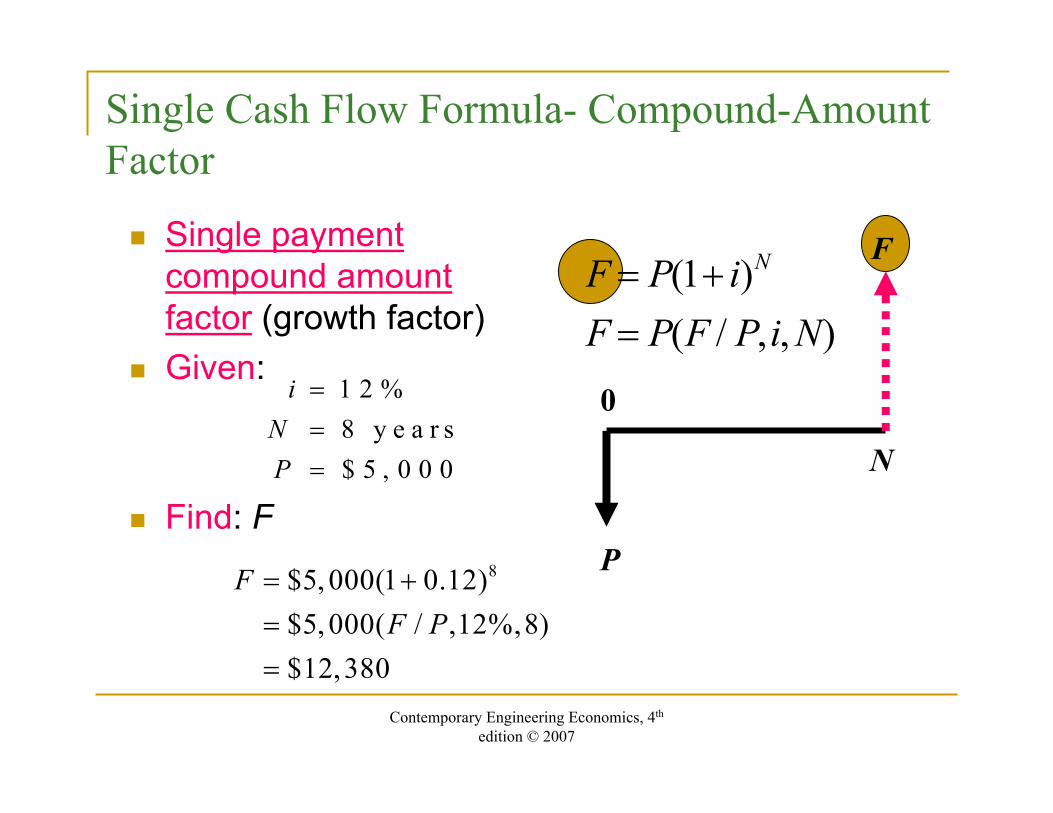

Single Cash Flow Formula- Compound-Amount Factor

Single payment compound amount factor (growth factor)Given:

Find: FP

F

N

0

F P iF P F P i N

N= +=

( )( / , , )1

1 2 %8 y e a r s$ 5 , 0 0 0

iNP

===

8$5, 000(1 0.12)$5, 000( / ,12%,8)$12,380

FF P

= +==

Contemporary Engineering Economics, 4th

edition © 2007

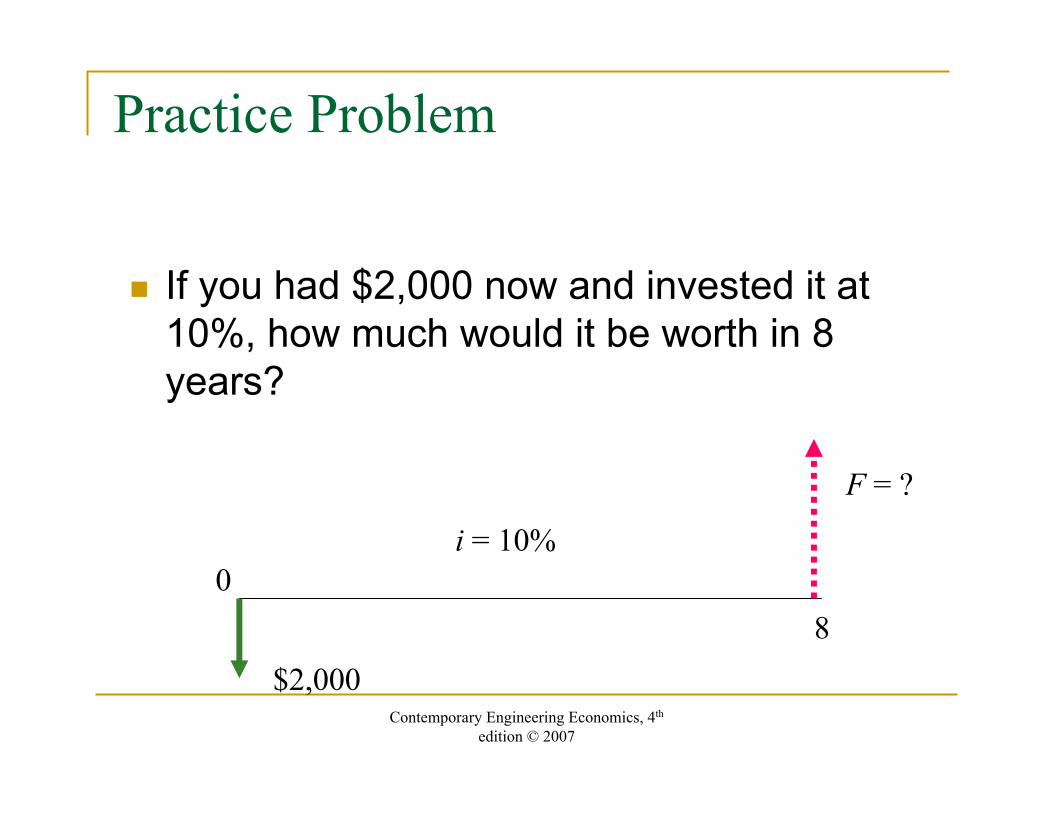

Practice Problem

If you had $2,000 now and invested it at 10%, how much would it be worth in 8 years?

$2,000

F = ?

80

i = 10%

Contemporary Engineering Economics, 4th

edition © 2007

Solution

8

G i v e n :$ 2 , 0 0 01 0 %8 y e a r s

F i n d :

$ 2 , 0 0 0 (1 0 . 1 0 )$ 2 , 0 0 0 ( / , 1 0 % , 8 )$ 4 , 2 8 7 . 1 8

E X C E L c o m m a n d := F V ( 1 0 % , 8 , 0 , 2 0 0 0 , 0 )= $ 4 , 2 8 7 . 2 0

Pi

N

F

FF P

===

= +==

Contemporary Engineering Economics, 4th

edition © 2007

Single Cash Flow Formula – Present-Worth Factor

Single payment present worth factor (discount factor)Given:

Find:P

F

N

0

P F iP F P F i N

N= +=

−( )( / , , )1

iNF

==

=

1 2 %5

0 0 0 y e a r s

$ 1 ,

PP F

= +

=

=

−$1, ( . )$1, ( / , )$567.40

000 1 0 12000 12%,5

5

Contemporary Engineering Economics, 4th

edition © 2007

Practice Problem

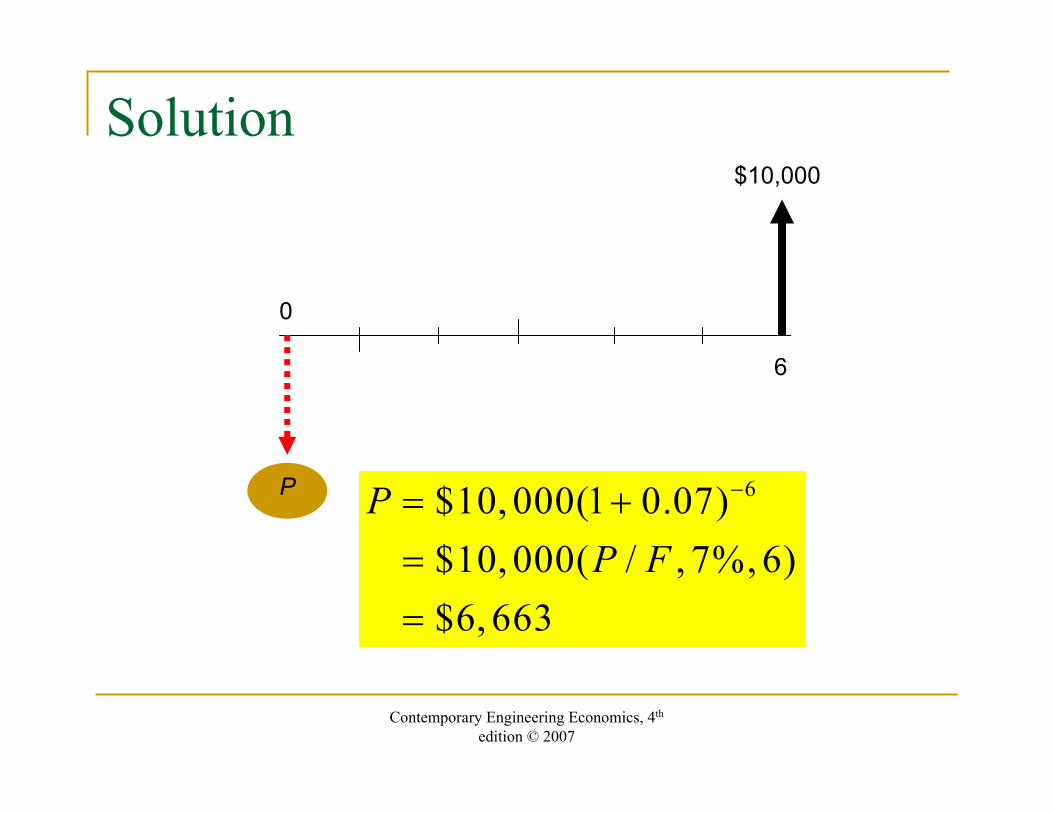

You want to set aside a lump sum amount today in a savings account that earns 7% annual interest to meet a future expense in the amount of $10,000 to be incurred in 6 years. How much do you need to deposit today?

Contemporary Engineering Economics, 4th

edition © 2007

Solution

0

6

$10,000

P 6$10, 000(1 0.07)$10, 000( / , 7%, 6)$6, 663

PP F

−= +==

Contemporary Engineering Economics, 4th

edition © 2007

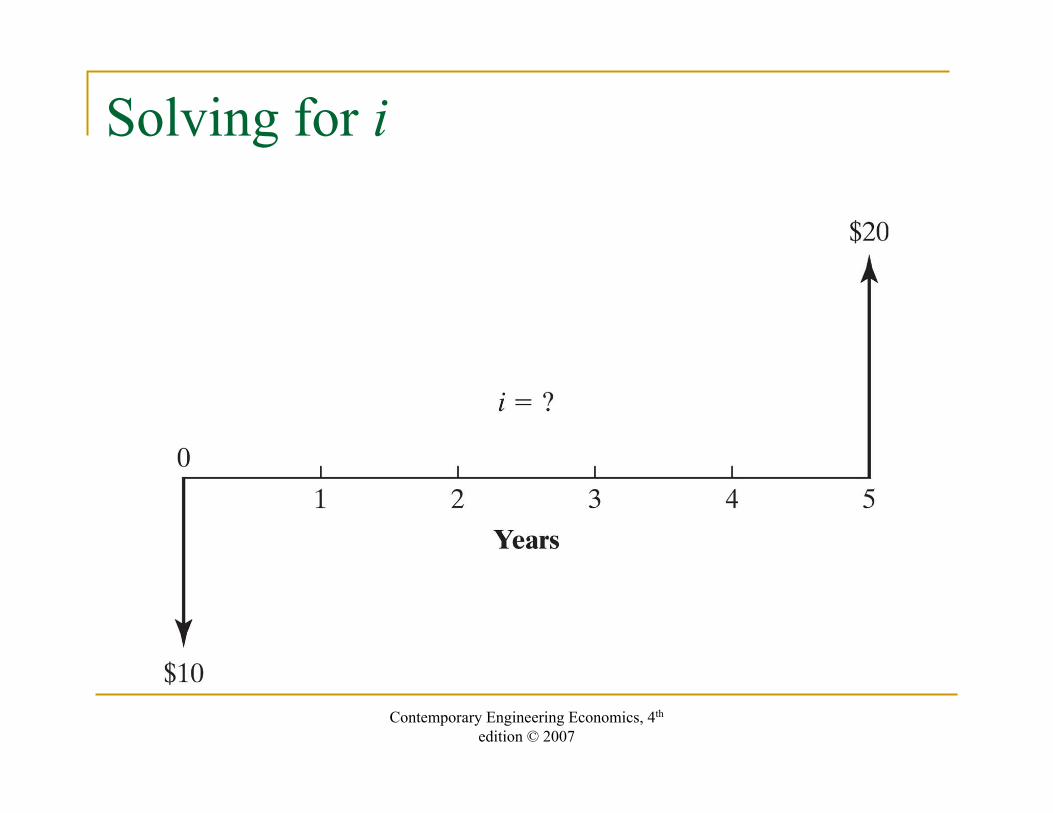

Solving for i

Contemporary Engineering Economics, 4th

edition © 2007

Solution

5

5

$20 $10(1 )2 (1 )

14.87%

ii

i

= +

= +=

EXCEL Solution using RATE Function

=RATE(5,0,-10,20)=14.87%

Contemporary Engineering Economics, 4th

edition © 2007

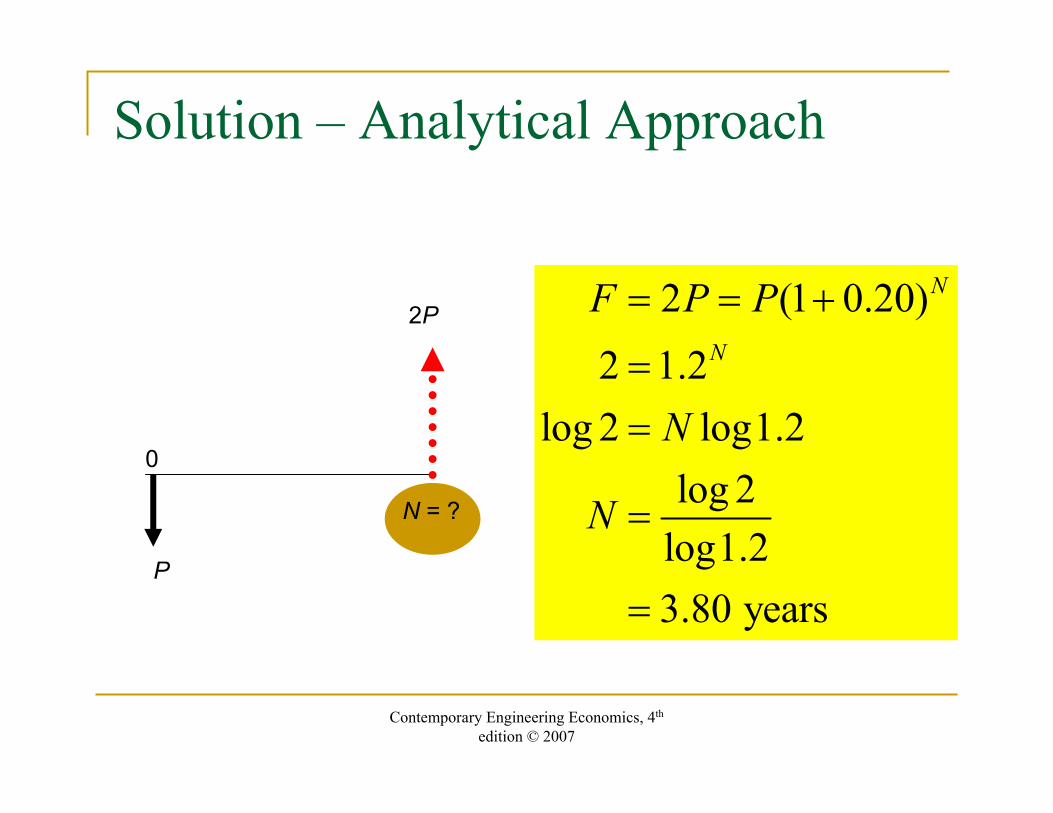

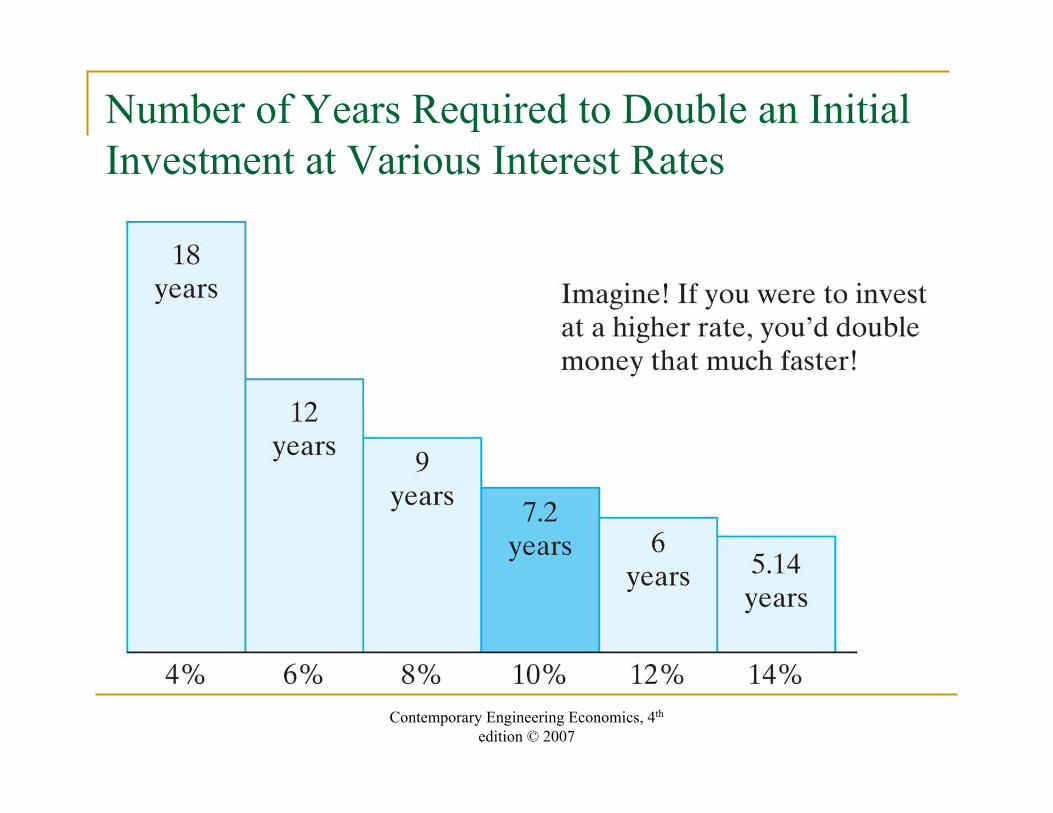

Rule of 72 – Number of Years Required to Double Your Investment

Contemporary Engineering Economics, 4th

edition © 2007

Solution – Analytical Approach

2 (1 0.20)2 1.2

log 2 log1.2log 2

log1.23.80 years

N

N

F P P

N

N

= = +

==

=

=P

2P

0

N = ?

Contemporary Engineering Economics, 4th

edition © 2007

Solution - Rule of 72

Approximating how long it will take for a sum of money to double

72interest rate (%)72203.6 years

N ≅

=

=

Contemporary Engineering Economics, 4th

edition © 2007

Number of Years Required to Double an Initial Investment at Various Interest Rates

Contemporary Engineering Economics, 4th

edition © 2007

Uneven Payment Series

How much do you need to deposit today (P) to withdraw $25,000 at n=1, $3,000 at n = 2, and $5,000 at n =4, if your account earns 10% annual interest?

0

1 2 3 4

$25,000

$3,000 $5,000

P

Contemporary Engineering Economics, 4th

edition © 2007

0

1 2 3 4

$25,000

$3,000 $5,000

P

0

1 2 3 4

$25,000

P1

0

1 2 3 4

$3,000

P2

0

1 2 3 4

$5,000

P4

+ +

1 $25,000( / ,10%,1)$22,727

P P F==

2 $3,000( / ,10%,2)$2,479

P P F==

4 $5,000( / ,10%,4)$3,415

P P F==

1 2 4 $28,622P P P P= + + =

Uneven Payment Series

Contemporary Engineering Economics, 4th

edition ©2007

Interest Formulas – Equal Payment Series

Lecture No.7Chapter 3Contemporary Engineering EconomicsCopyright © 2006

Contemporary Engineering Economics, 4th

edition © 2007

Equal Payment Series

0 1 2 N

0 1 2 N

A A A

F

P

0 N

Contemporary Engineering Economics, 4th

edition © 2007

Equal Payment Series – Compound Amount Factor

0 1 2 N0 1 2 N

A A A

F

0 1 2N

A A A

F

=

Contemporary Engineering Economics, 4th

edition © 2007

Process of Finding the Equivalent Future Worth, F

0 1 2 N 0 1 2 N

A A A

F

A(1+i)N-1

A(1+i)N-2

1 2 (1 ) 1(1 ) (1 )N

N N iF A i A i A Ai

− − ⎡ ⎤+ −= + + + + + = ⎢ ⎥

⎣ ⎦

A

Contemporary Engineering Economics, 4th

edition © 2007

Another Way to Look at the Compound Amount Factor

Contemporary Engineering Economics, 4th

edition © 2007

Equal Payment Series Compound Amount Factor (Future Value of an Annuity)

F A ii

A F A i N

N

=+ −

=

( )

( / , , )

1 1

Example:Given: A = $5,000, N = 5 years, and i = 6%Find: FSolution: F = $5,000(F/A,6%,5) = $28,185.46

0 1 2 3N

F

A

Contemporary Engineering Economics, 4th

edition © 2007

Validation

F =?

0 1 2 3 4 5

$5,000 $5,000 $5,000 $5,000 $5,000

i = 6%

4

3

2

1

0

$5,000(1 0.06) $6,312.38$5,000(1 0.06) $5,955.08$5,000(1 0.06) $5,618.00$5,000(1 0.06) $5,300.00$5,000(1 0.06) $5,000.00 $28.185.46

+ =

+ =

+ =

+ =

+ =

Contemporary Engineering Economics, 4th

edition © 2007

Finding an Annuity Value

Example:Given: F = $5,000, N = 5 years, and i = 7%Find: ASolution: A = $5,000(A/F,7%,5) = $869.50

0 1 2 3N

F

A = ?

A F ii

F A F i N

N=+ −

=( )( / , , )1 1

Contemporary Engineering Economics, 4th

edition © 2007

Handling Time Shifts in a Uniform Series

F = ?

0 1 2 3 4 5

$5,000 $5,000 $5,000 $5,000 $5,000

i = 6%

First deposit occurs at n = 0

Contemporary Engineering Economics, 4th

edition © 2007

5 $5,000( / ,6%,5)(1.06)$29,876.59

F F A=

=

Annuity Due

Excel Solution

=FV(6%,5,5000,0,1)Beginning period

Contemporary Engineering Economics, 4th

edition © 2007

Sinking Fund Factor

Example: College Savings PlanGiven: F = $100,000, N = 8 years, and i = 7%Find: ASolution:

A = $100,000(A/F,7%,8) = $9,746.78

0 1 2 3N

F

A

A F ii

F A F i N

N=+ −LNM

OQP

=

( )( / , , )

1 1

Contemporary Engineering Economics, 4th

edition © 2007

Excel Solution

Given:F = $100,000i = 7%N = 8 years

01 2 3 4 5 6 7 8

$100,000

i = 8%

A = ?

Current age: 10 years old

• Find:

=PMT(i,N,pv,fv,type)=PMT(7%,8,0,100000,0)=$9,746.78

Contemporary Engineering Economics, 4th

edition © 2007

Example 3.15 Combination of a Uniform Series and a Single Present and Future Amount

Contemporary Engineering Economics, 4th

edition © 2007

Solution: A Two-Step Approach

Step 1: Find the required savings at n = 5.

Step 2: Find the required annual contribution (A) over 5 years.

$4,298.70( / ,7%,5)$747.55

A A F==

Required Savings

$500( / ,7%,5) $701.30$5,000 $701.30 $4,298.70

CF F PF

= == − =

Contemporary Engineering Economics, 4th

edition © 2007

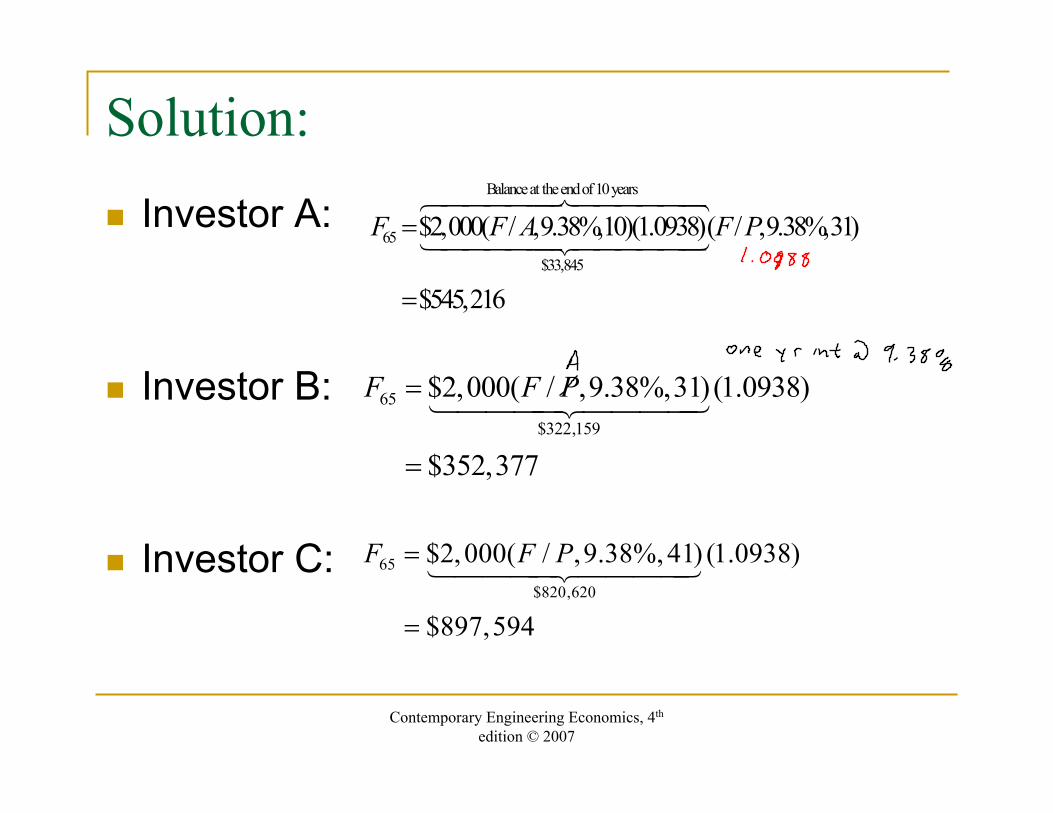

Comparison of Three Different Investment Plans – Example 3.16

Contemporary Engineering Economics, 4th

edition © 2007

Solution:Investor A:

Investor B:

Investor C:

Balance at the end of 10 years

65

$33,845

$2,000( / ,9.38%,10)(1.0938)( / ,9.38%,31)

$545,216

F F A F P=

=

65

$322,159

$2,000( / ,9.38%,31)(1.0938)

$352,377

F F P=

=

65

$820,620

$2,000( / ,9.38%, 41) (1.0938)

$897,594

F F P=

=

Contemporary Engineering Economics, 4th

edition © 2007

How Long Would It Take to Save $1 Million?

Contemporary Engineering Economics, 4th

edition © 2007

Loan Cash Flows

Contemporary Engineering Economics, 4th

edition © 2007

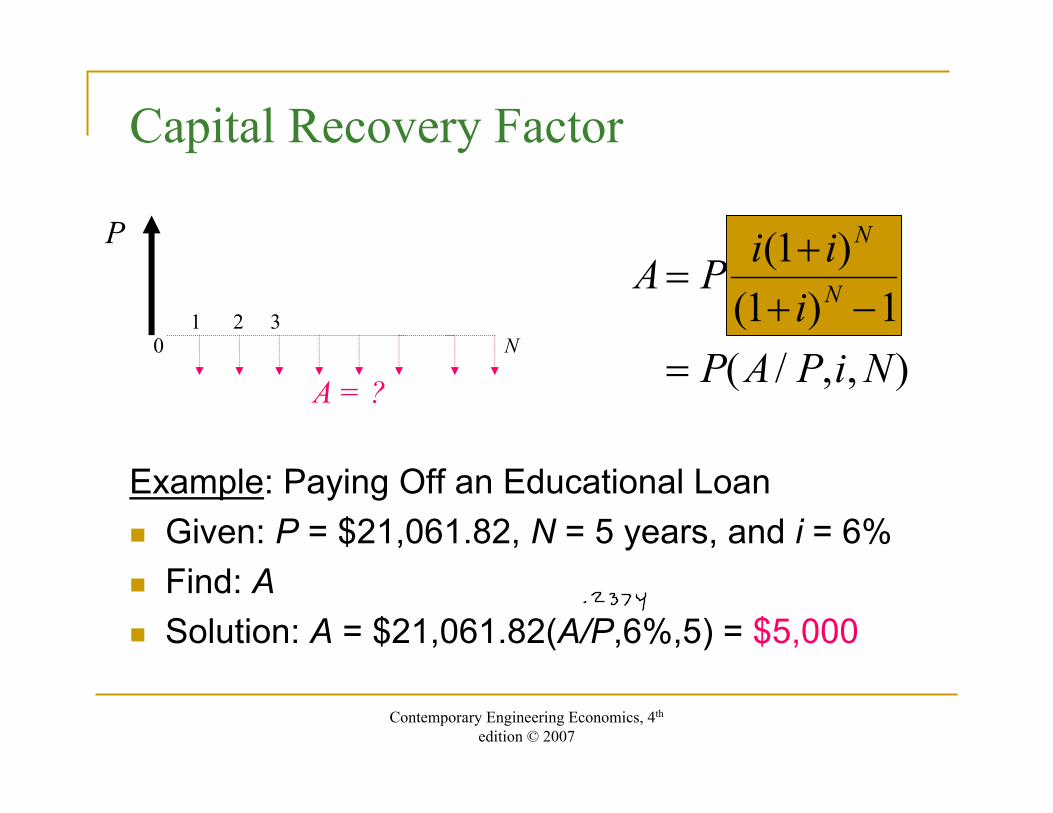

Capital Recovery Factor

Example: Paying Off an Educational LoanGiven: P = $21,061.82, N = 5 years, and i = 6%Find: ASolution: A = $21,061.82(A/P,6%,5) = $5,000

1 2 3N

P

A = ?0

A P i ii

P A P i N

N

N=+

+ −=

( )( )( / , , )

11 1

Contemporary Engineering Economics, 4th

edition © 2007

Example 3.17 Loan Repayment

Contemporary Engineering Economics, 4th

edition © 2007

Solution:

Using Interest Factor:

Using Excel:

$250,000( / ,8%,6)$250,000(0.2163)$54,075

A A P===

PMT( , , )PMT(8%,6, 250000)$54,075

i N P== −=

Contemporary Engineering Economics, 4th

edition © 2007

Example 3.18 – Deferred Loan Repayment

Contemporary Engineering Economics, 4th

edition © 2007

A Two-Step Procedure

' $250,000( / ,8%,1)$270,000

' $270,000( / ,8%,6)$58, 401

P F P

A A P

====

Contemporary Engineering Economics, 4th

edition © 2007

P = ?

1 2 3N

A0

P A ii i

A P Ai N

N

N=+ −+

=

( )( )

( / , , )

1 11

Present Worth factor – Find P, Given A, i, and N

Contemporary Engineering Economics, 4th

edition © 2007

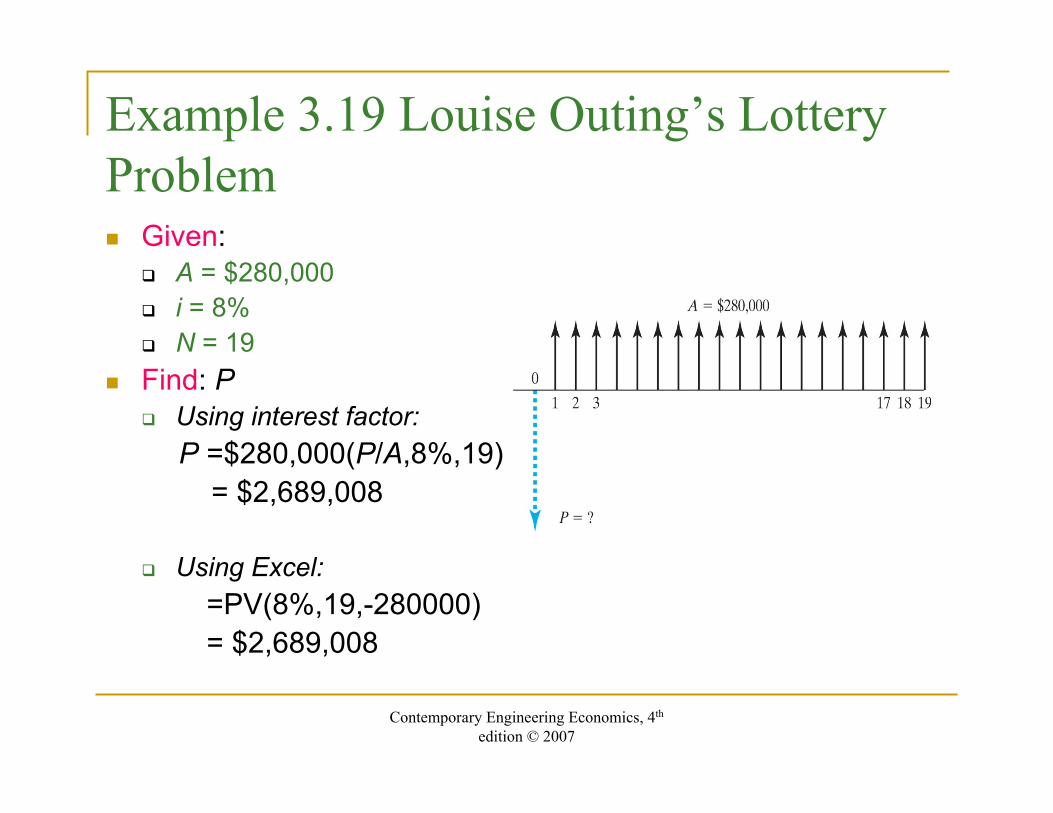

Example 3.19 Louise Outing’s Lottery Problem

Given:A = $280,000i = 8%N = 19

Find: PUsing interest factor:P =$280,000(P/A,8%,19)

= $2,689,008

Using Excel:=PV(8%,19,-280000)= $2,689,008

Interest Formulas(Gradient Series)

Lecture No.8Chapter 3

Contemporary Engineering EconomicsCopyright © 2006

Linear Gradient Series

P G i i iNi i

G P G i N

N

N=+ − −

+LNM

OQP

=

( )( )

( / , , )

1 112

P

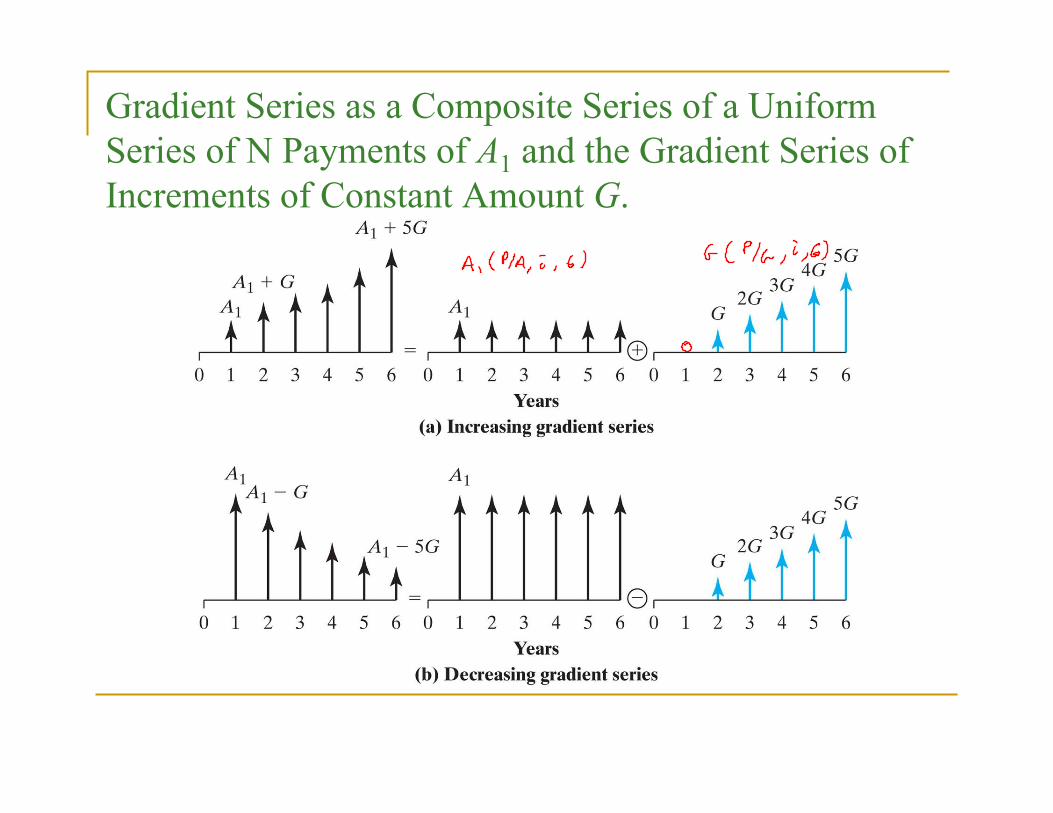

Gradient Series as a Composite Series of a Uniform Series of N Payments of A1 and the Gradient Series of Increments of Constant Amount G.

$1,000$1,250 $1,500

$1,750$2,000

1 2 3 4 50

P =?

How much do you have to depositnow in a savings account that earns a 12% annual interest, if you want to withdraw the annual series as shown in the figure?

Example – Present value calculation for a gradient series

Method 1: Using the (P/F, i, N) Factor

$1,000$1,250 $1,500

$1,750$2,000

1 2 3 4 50

P =?

$1,000(P/F, 12%, 1) = $892.86$1,250(P/F, 12%, 2) = $996.49$1,500(P/F, 12%, 3) = $1,067.67$1,750(P/F, 12%, 4) = $1,112.16$2,000(P/F, 12%, 5) = $1,134.85

$5,204.03

Method 2: Using the Gradient Factor

P P G2 12%,559920

=

=

$250( / , )$1, .P= +

=

$3, . $1, .$5,204

60408 59920

P P A1 000 12%,560480

=

=

$1, ( / , )$3, .

Gradient-to-Equal-Payment Series Conversion Factor, (A/G, i, N)

Example 3.21 – Find the Equivalent Uniform Deposit Plan

Solution:

1Given: $1,000, $300, 10%,and, 6Find:

$1,000 $300( / ,10%,6)$1,000 $300(2.22236)$1,667.08

A G i NA

A A G

= = = =

= += +=

Example 3.22 Declining Linear Gradient Series

Solution:

1 2Equivalent Present Worth at = 0

1( / ,10%,5) $200( / ,10%,5) ( / ,10%,5)$1,200(6.105) $200(6.862)(1.611)$5,115

n

F F F

A F A P G F P

= −

= −= −=

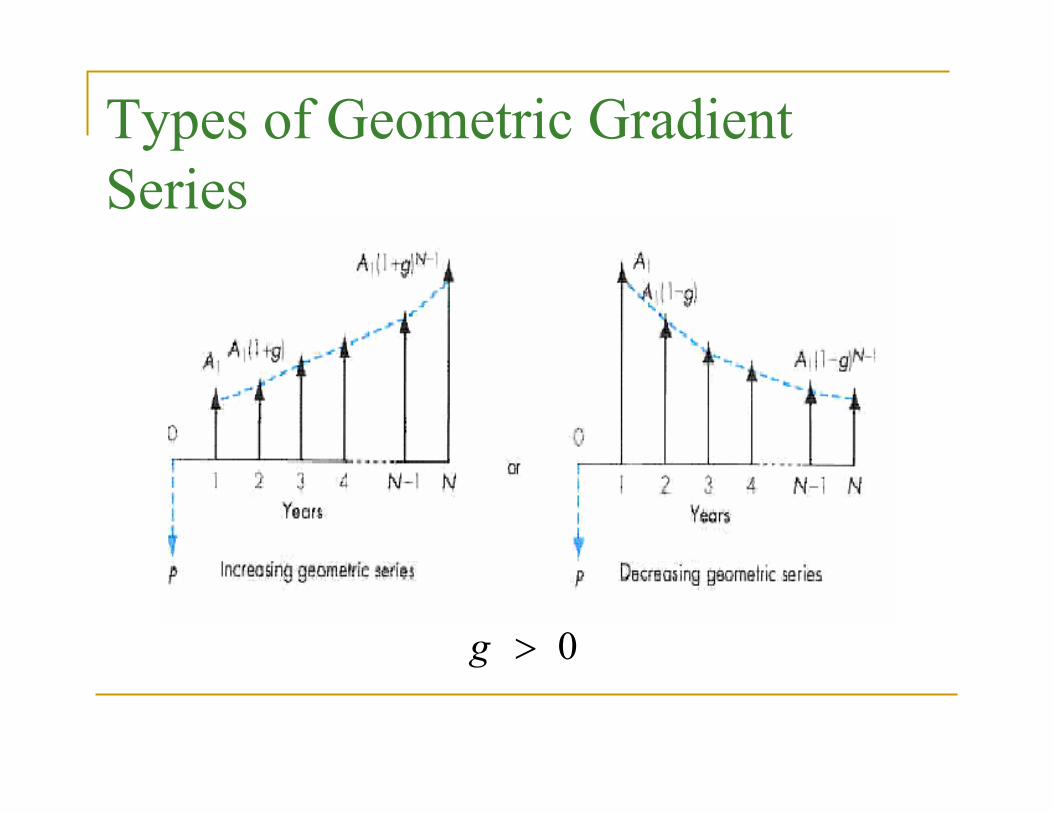

Types of Geometric Gradient Series

0g >

Present Worth Factor

P A g ii g

i g

NA i i g

N N

=− + +

−LNM

OQP ≠

+ =

RS|T|

−

1

1

1 1 1

1

( ) ( )

/( ),

, if

if

Example 3.23 Annual Power Cost if Repair is Not Performed

Solution – Adopt the new compressed-air system

5 51 (1 0.07) (1 0.12)$54,4400.12 0.07

$222,283$54,440(1 0.23)( / ,12%,5)$41,918.80(3.6048)$151,109

Old

New

P

P P A

−⎡ ⎤− + += ⎢ ⎥−⎣ ⎦== −

==

Example 3.24 Jimmy Carpenter’s Retirement Plan – Save $1 Million

What Should be the Size of his first Deposit (A1)?

20 20

20 1

1

1

1 (1 0.06) (1 0.08)0.08 0.06

(72.6911)$1, 000, 000$1, 000, 000

72.6911$13, 757

F A

A

A

−⎡ ⎤− + += ⎢ ⎥−⎣ ⎦==

=

=

Unconventional Equivalence Calculations

Lecture No. 9Chapter 3

Contemporary Engineering EconomicsCopyright © 2006

Equivalent Present Worth Calculation – Brute Force Approach using Only P/F Factors

$50$100 $100 $100

$150 $150 $150 $150$200

G r o u p 1 $ 5 0 ( / , 1 5 % , 1 )

$ 4 3 .4 8

P P F=

=

G r o u p 2 $ 1 0 0 ( / , 1 5 % , 3 ) ( / , 1 5 % , 1)

$ 1 9 8 .5 4

P P A P F=

=

G r o u p 3 $ 1 5 0 ( / , 1 5 % , 4 ) ( / , 1 5 % , 4 )

$ 2 4 4 .8 5

P P A P F=

=

G r o u p 4 $ 2 0 0 ( / , 1 5 % , 9 )

$ 5 6 .8 5

P P F=

=$ 4 3 .4 8 $ 1 9 8 .5 4 $ 2 4 4 .8 5 $ 5 6 .8 5$ 5 4 3 .7 2

P = + + +=

01 2 3 4 5 6 7 8 9

Equivalent Present Worth Calculation –Grouping Approach

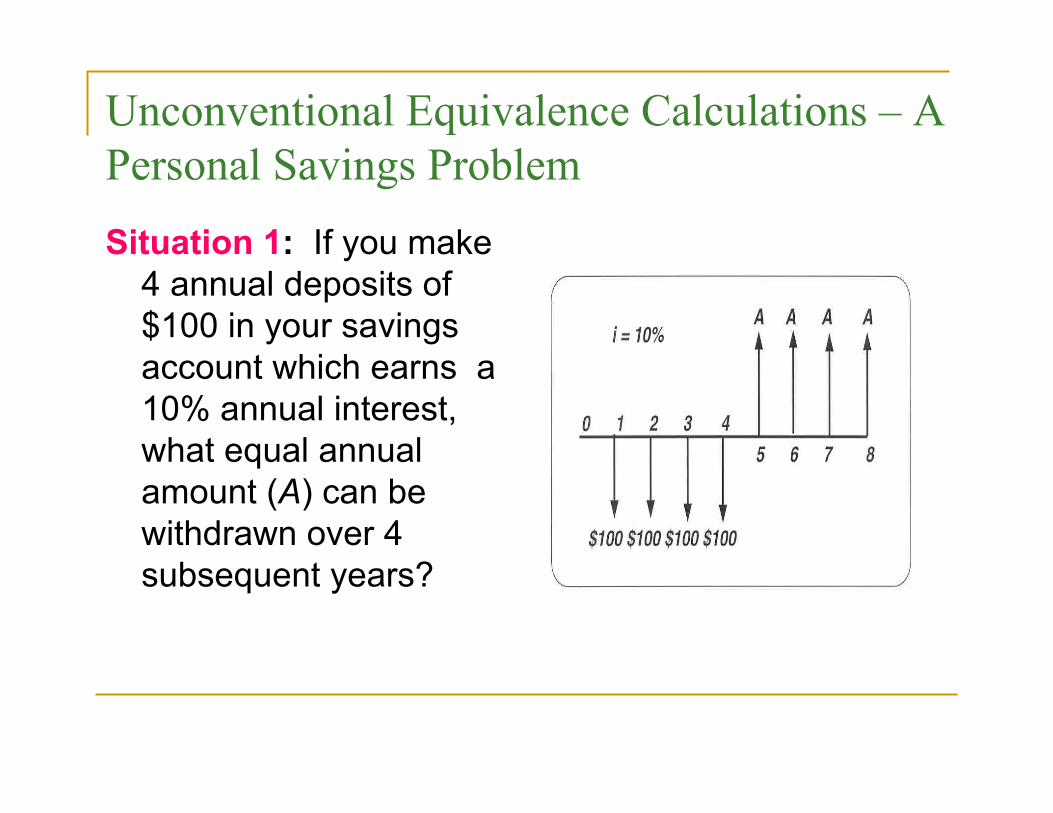

Unconventional Equivalence Calculations – A Personal Savings Problem

Situation 1: If you make 4 annual deposits of $100 in your savings account which earns a 10% annual interest, what equal annual amount (A) can be withdrawn over 4 subsequent years?

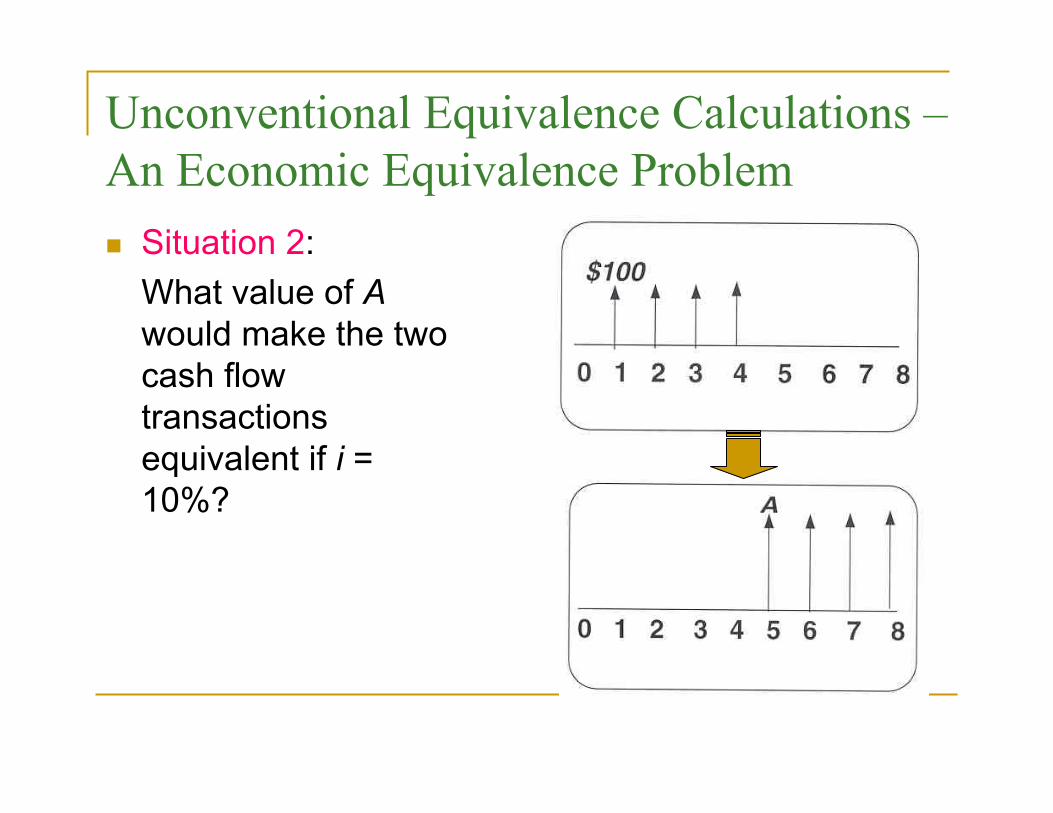

Unconventional Equivalence Calculations –An Economic Equivalence Problem

Situation 2:What value of Awould make the two cash flow transactions equivalent if i = 10%?

Method 1: Establish the Economic Equivalence at n = 0

Method 2: Establish the Economic Equivalence at n = 4

Multiple Interest Rates

$300$500

$400

5% 6% 6% 4% 4%

Find the balance at the end of year 5.

0

12

34 5

F = ?

Solution1 :

$300( / , 5% ,1) $3152 :

$315( / , 6% ,1) $500 $833.903 :

$833.90( / , 6% ,1) $883.934 :

$883.93( / , 4% ,1) $400 $1, 319.295 :

$1, 319.29( / , 4% ,1) $1, 372.06

nF P

nF P

nF P

nF P

nF P

==

=+ =

==

=+ =

==

Cash Flows with Missing Payments

P = ?

$100

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Missing paymenti = 10%

Solution

P = ?

$100

01 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Pretend that we have the 10th

Payment in the amount of $100i = 10%

$100Add $100 tooffset the change

Approach

P = ?

$100

01 2 3 4 5 6 7 8 9 10 11 12 13 14 15

i = 10%

$100

Equivalent Cash Inflow = Equivalent Cash Outflow

$100( / ,10%,10) $100( / ,10%,15)$38.55 $760.61

$722.05

P P F P AP

P

+ =+ =

=

Equivalence Relationship

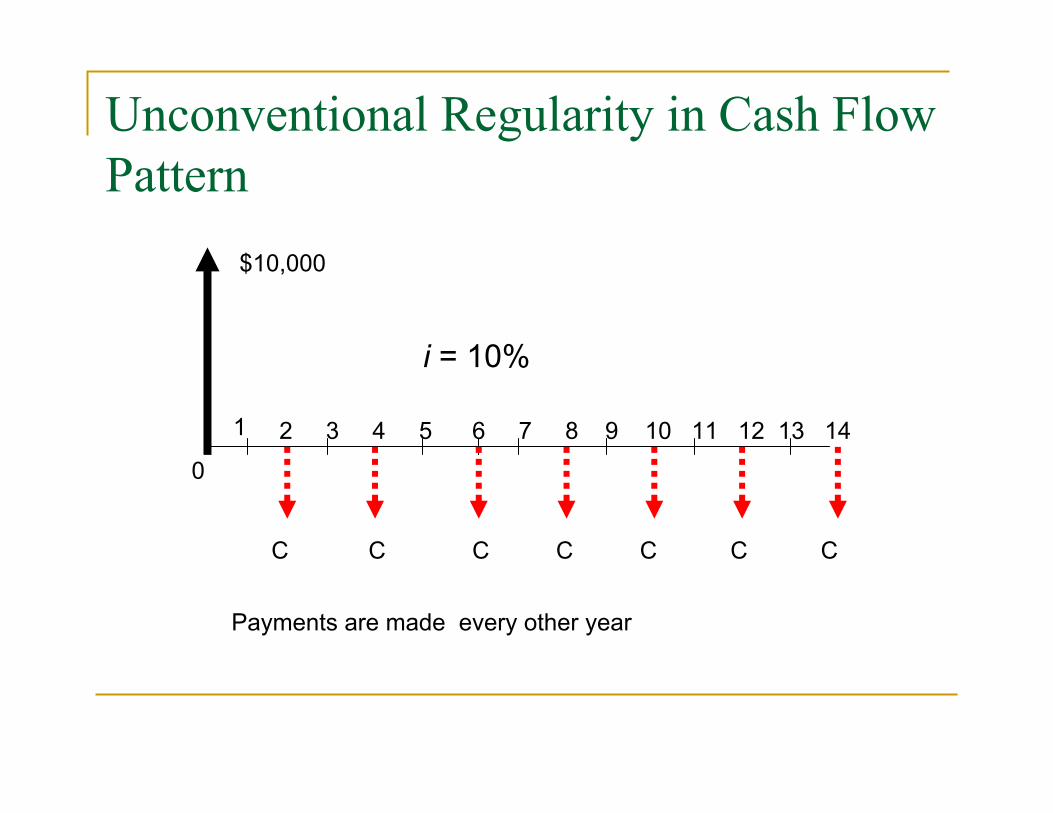

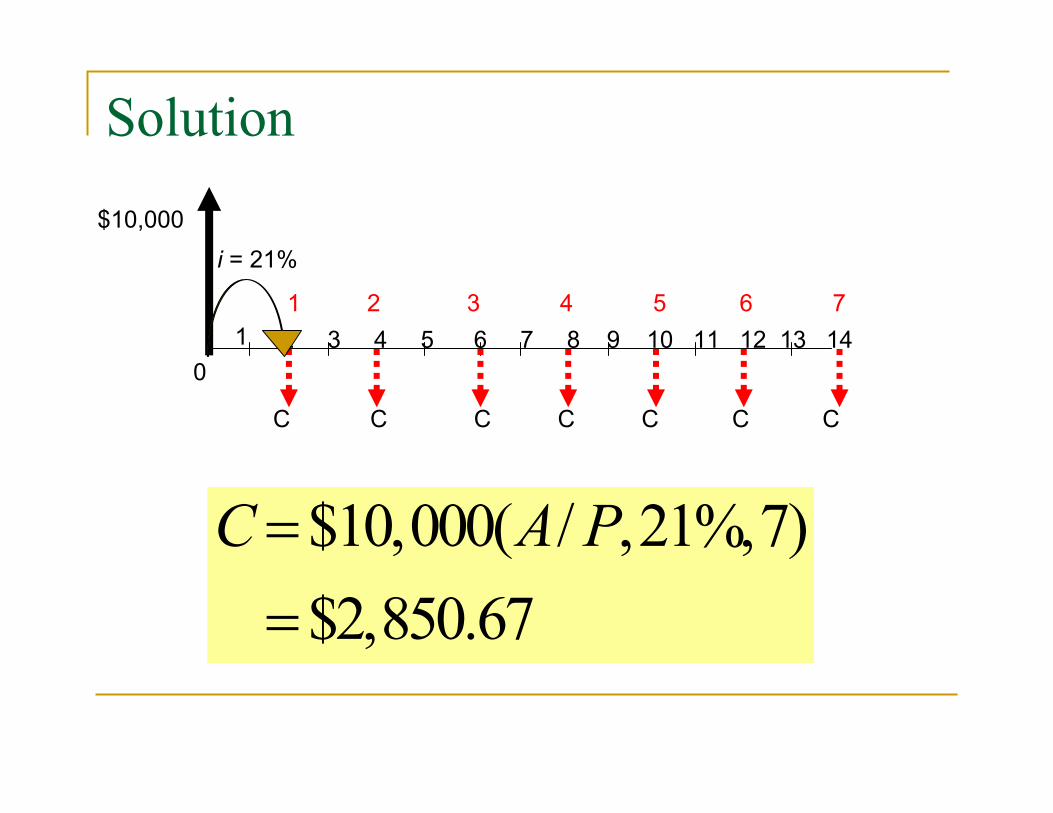

Unconventional Regularity in Cash Flow Pattern

$10,000

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14

C C C C C C C

i = 10%

Payments are made every other year

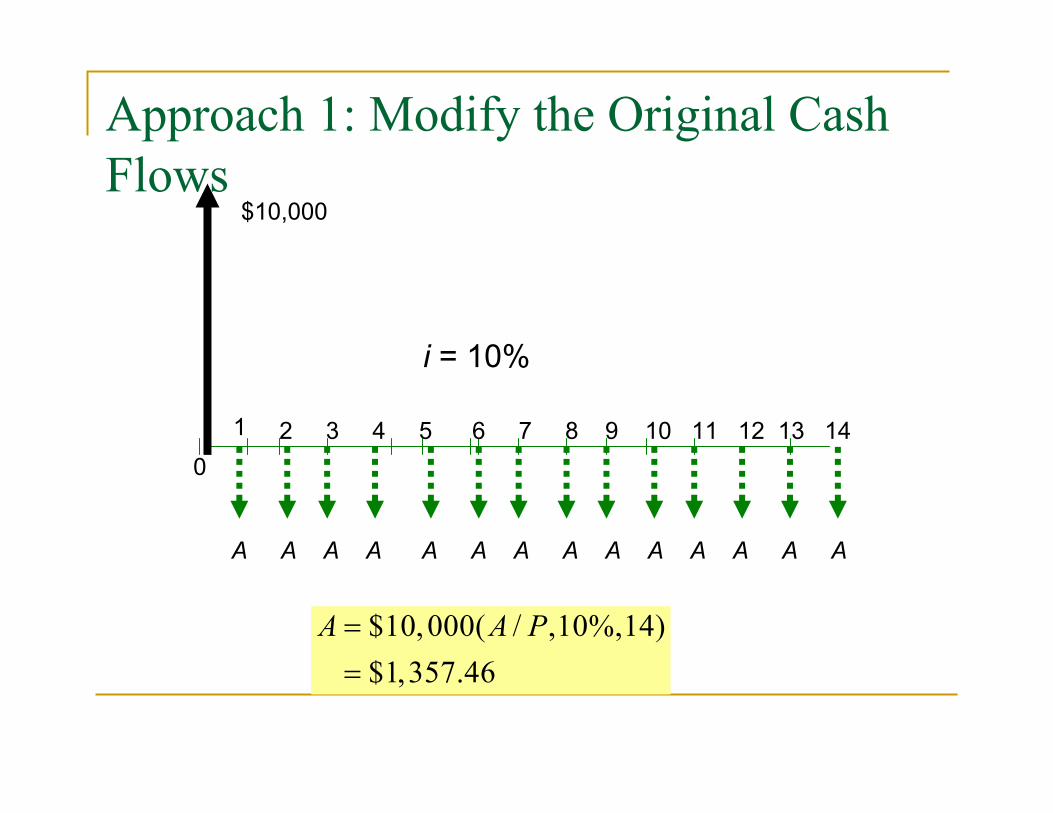

Approach 1: Modify the Original Cash Flows

$10,000

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14

i = 10%

A A A A A A A A A A A A A A

$10,000( / ,10%,14)$1,357.46

A A P==

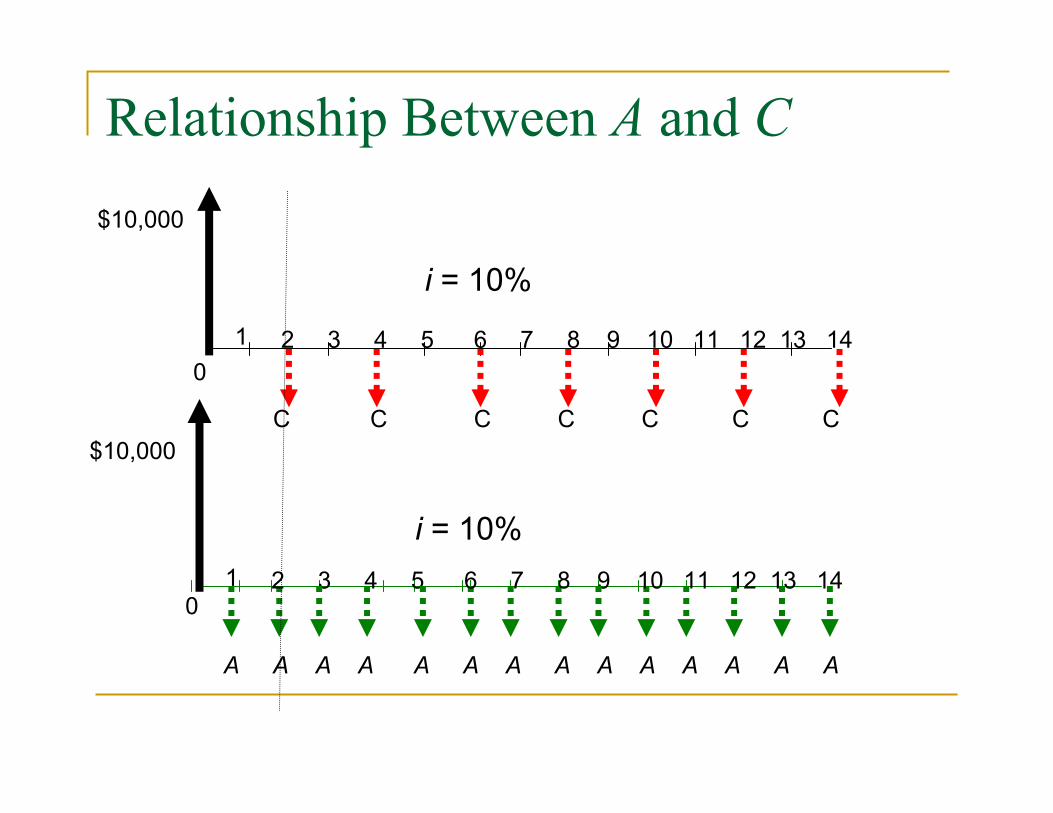

Relationship Between A and C

$10,000

01 2 3 4 5 6 7 8 9 10 11 12 13 14

i = 10%

A A A A A A A A A A A A A A

$10,000

01 2 3 4 5 6 7 8 9 10 11 12 13 14

C C C C C C C

i = 10%

C≡

A =$1,357.46

A A

i = 10%

$10,000( / ,10%,14)$1,357.46

( / ,10%,1)1.12.12.1($1,357.46)$2,850.67

A A P

C A F P AA AA

==≡= += +===

Solution

Approach 2: Modify the Interest Rate

Idea: Since cash flows occur every other year, let's find out the equivalent compound interest rate that covers the two-year period. How: If interest is compounded 10% annually, the equivalent interest rate for two-year period is 21%.

(1+0.10)(1+0.10) = 1.21

Solution

$10,000

01 2 3 4 5 6 7 8 9 10 11 12 13 14

C C C C C C C

i = 21%

$10,000( / ,21%,7)$2,850.67

C A P==

1 2 3 4 5 6 7

Example 3.25 – At What Value of C would Make the Two Cash Flows Equivalent?

1

2

$100( / ,12%,2) $300( / ,12%,3) $932.55( / ,12%,2) ( / ,12%,2)( / ,12%,1) 3.6290

3.6290 $932.55$256.97

V F A P AV C F A C P A P F CCC

= + == + ===

Example 3.26 Establishing a College Fund

Solution: Establish the Economic Equivalence at n = 18

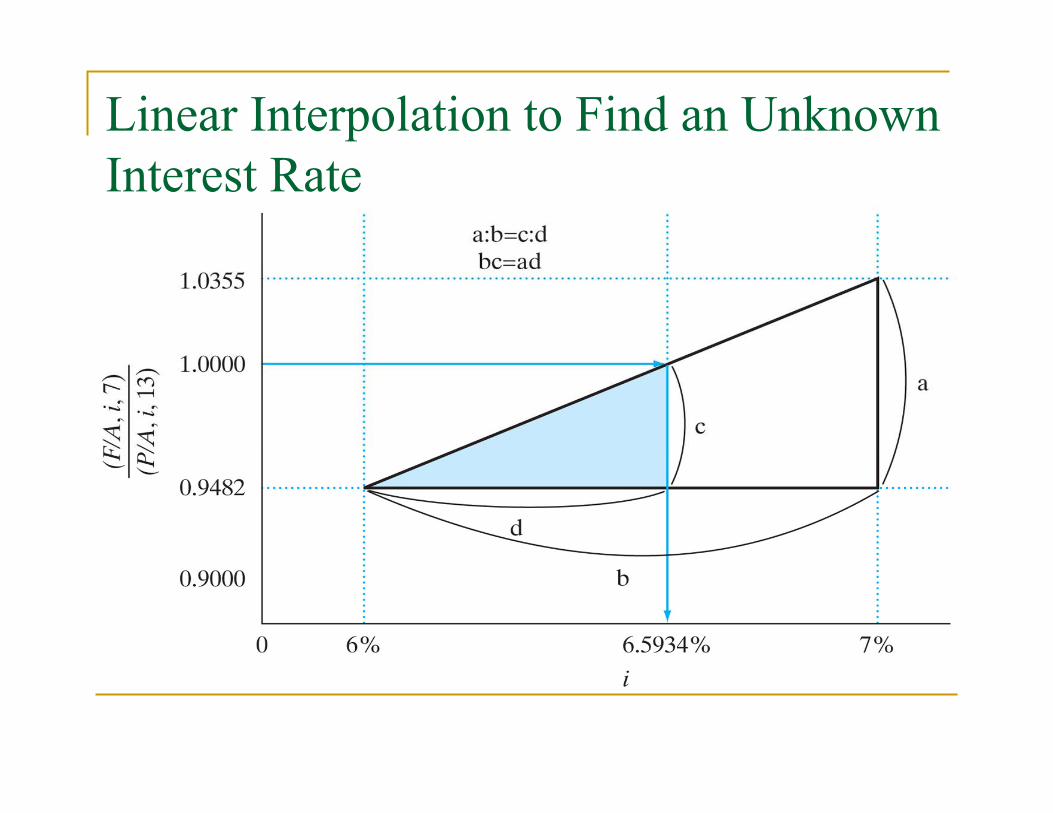

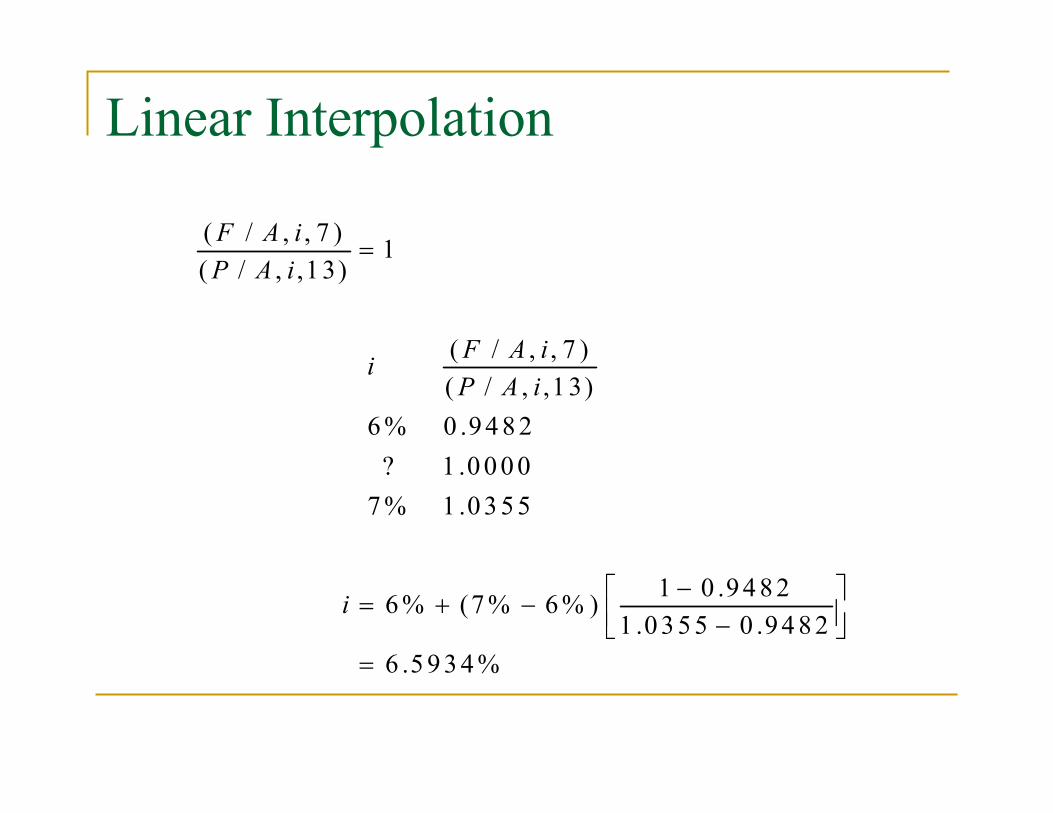

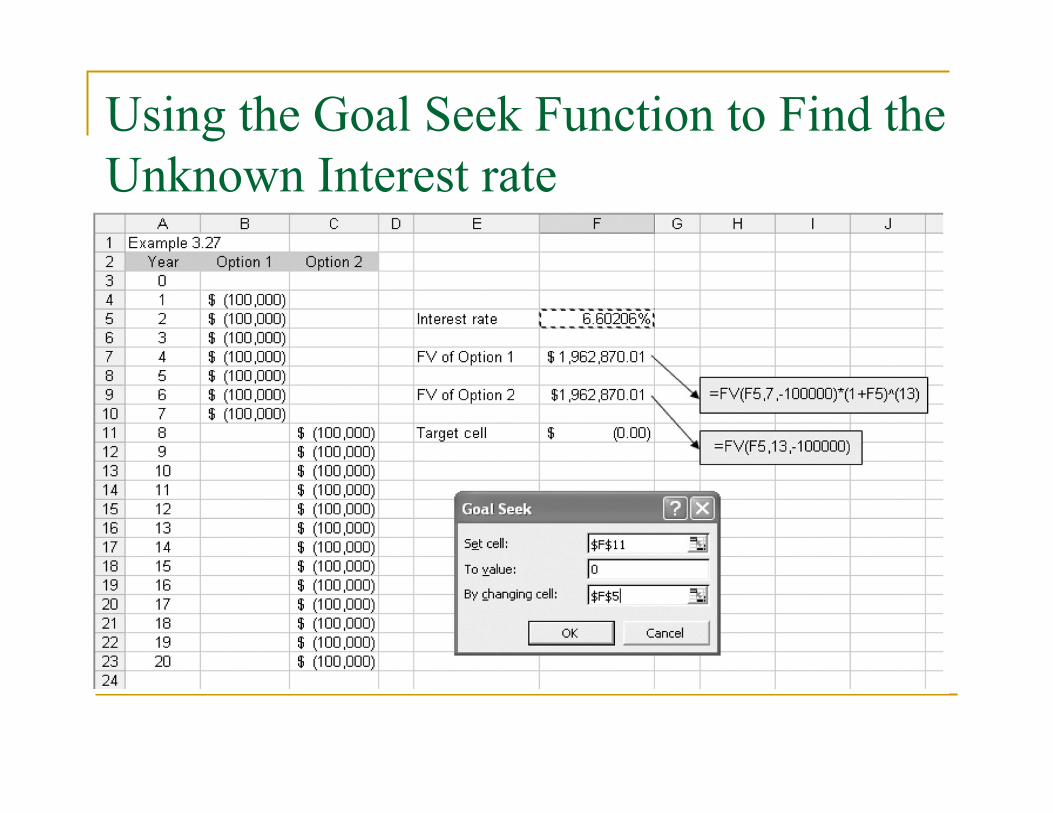

Example 3.27 Calculating an Unknown Interest Rate with Multiple Factors

Establish an economic Equivalence at n =7

Linear Interpolation to Find an Unknown Interest Rate

Linear Interpolation

( / , , 7 ) 1( / , ,1 3)

( / , , 7 ) ( / , ,1 3)

6 % 0 .9 4 8 2? 1 .0 0 0 0

7 % 1 .0 3 5 5

1 0 .9 4 8 26 % (7 % 6 % )1 .0 3 5 5 0 .9 4 8 2

6 .5 9 3 4 %

F A iP A i

F A iiP A i

i

=

−⎡ ⎤= + − ⎢ ⎥−⎣ ⎦=

Using the Goal Seek Function to Find the Unknown Interest rate