chapter 16 n

TRANSCRIPT

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 1/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Capital ExpenditureDecisions

Chapter 16

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 2/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

LearningObjective

1

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 3/52

Discounted-Cash-Flow Analysis

1-3

Cost reduction

Plant expansion

Equipment selection

Lease or buy

Equipment replacement

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 4/52

Net-Present-Value Method

1-4

o Prepare a table showing cash flows for each year,

o Calculate the present value of each cash flow using adiscount rate,

o Compute net present value,

o If the net present value (NPV) is positive, accept theinvestment proposal. Otherwise, reject it.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 5/52

Net-Present-Value Method

1-5

Mattson Co. has been offered a five year contract toprovide component parts for a large manufacturer.

Cost and revenue information

Cost of special equipment $160,000Working capital required 100,000

Relining equipment in 3 years 30,000

Salvage value of equipment in 5 years 5,000

Annual cash revenue and costs: Sales revenue from parts 750,000

Cost of parts sold 400,000

Salaries, shipping, etc. 270,000

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 6/52

Net-Present-Value Method

1-6

• At the end of five years the working capitalwill be released and may be used elsewhereby Mattson.

• Mattson uses a discount rate of 10%.

Should the contract be accepted?

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 7/52

Net-Present-Value Method

1-7

Annual net cash inflows from operations

Sales revenue 750,000$

Cost of parts sold 400,000Gross margin 350,000

Less out-of-pocket costs 270,000

Annual net cash inflows 80,000$

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 8/52

Net-Present-Value Method

1-8

Years CashFlows 10%Factor PresentValue

Investment in equipment Now $(160,000) 1.000 (160,000)$Working capital needed Now (100,000) 1.000 (100,000)

Annual net cash inflows 1-5 80,000 3.791 303,280

Relining of equipment 3 (30,000) 0.751 (22,530) Salvage value of equip. 5 5,000 0.621 3,105

Working capital released 5 100,000 0.621 62,100 Net present value 85,955$

Mattson should accept the contract because thepresent value of the cash inflows exceeds the present

value of the cash outflows by $85,955. The projecthas a positive net present value.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 9/52

Internal-Rate-of-Return Method

1-9

• The internal rate of return is the trueeconomic return earned by the asset over itslife.

• The internal rate of return is computed byfinding the discount rate that will cause thenet present value of a project to be zero.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 10/52

Internal-Rate-of-Return Method

1-10

• Black Co. can purchase a new machine at acost of $104,320 that will save $20,000 peryear in cash operating costs.

• The machine has a 10-year life.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 11/52

Internal-Rate-of-Return Method

1-11

Future cash flows are the same every year inthis example, so we can calculate the

internal rate of return as follows:

Investment requiredNet annual cash flows

= Present value factor

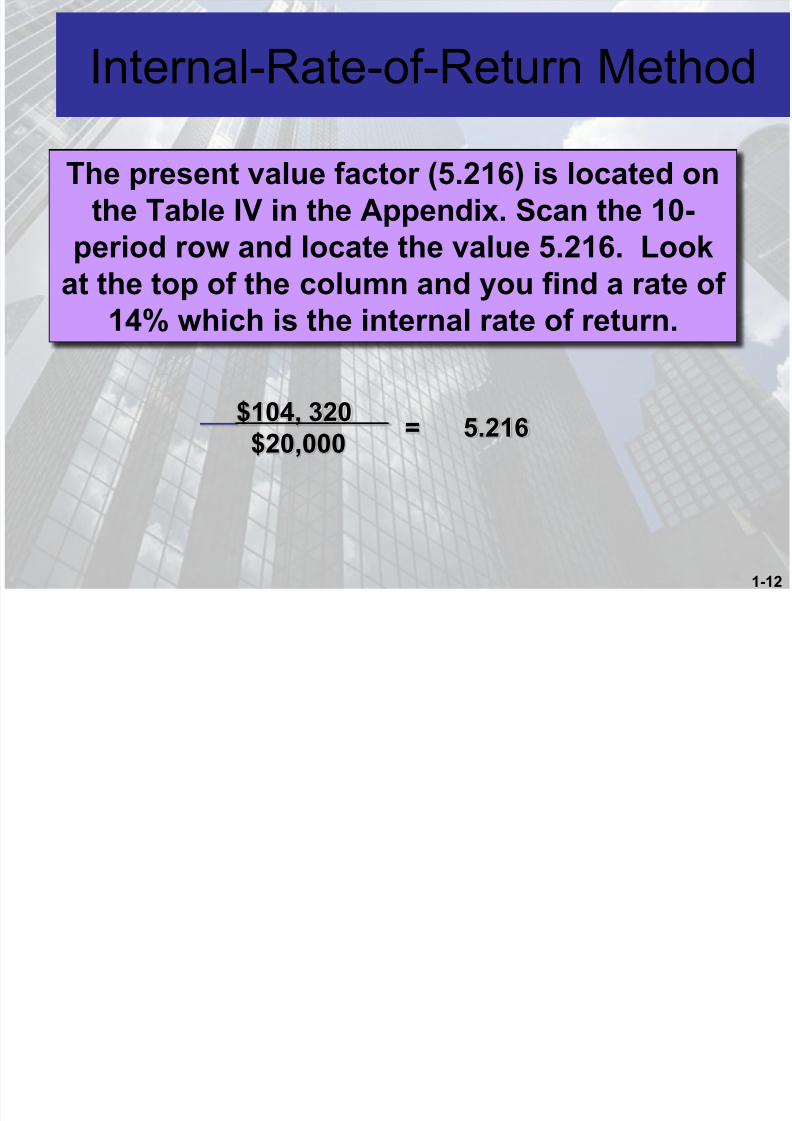

$104, 320$20,000

= 5.216

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 12/52

Internal-Rate-of-Return Method

1-12

$104, 320$20,000

= 5.216

The present value factor (5.216) is located onthe Table IV in the Appendix. Scan the 10-

period row and locate the value 5.216. Look

at the top of the column and you find a rate of14% which is the internal rate of return.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 13/52

Internal-Rate-of-Return Method

1-13

Here’s the proof . . .

Year Amount

14%

Factor

Present

ValueInvestment required Now (104,320)$ 1.000 (104,320)Annual cost savings 1-10 20,000 5.216 104,320 Net present value -$

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 14/52Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

LearningObjective

2

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 15/52

Comparing the NPV and IRRMethods

1-15

Internal Rate of Return

The cost of capital iscompared to theinternal rate of returnon a project.

To be acceptable, aproject’s rate of

return must begreater than the cost

of capital.

Net Present ValueThe cost of capital

is used as the

actual discount rate.

Any project with a

negative netpresent value isrejected.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 16/52

Comparing the NPV and IRRMethods

1-16

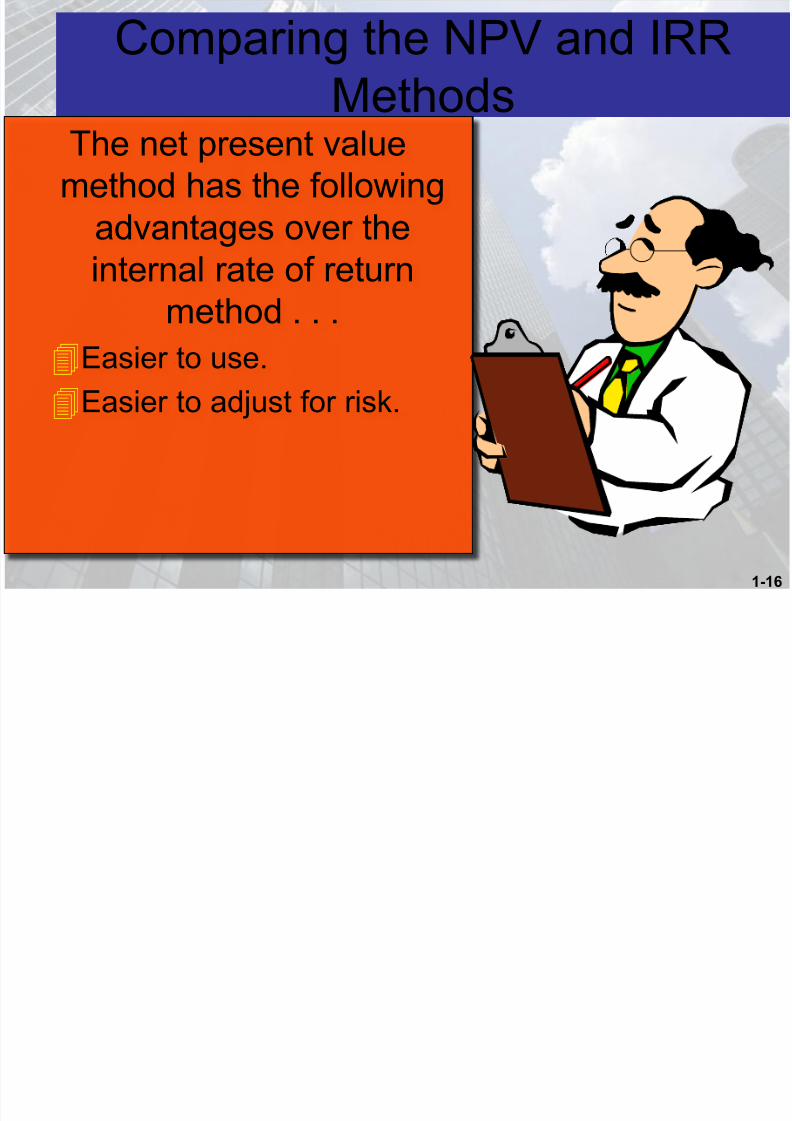

The net present valuemethod has the following

advantages over the

internal rate of returnmethod . . .

Easier to use.

Easier to adjust for risk.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 17/52

Assumptions UnderlyingDiscounted-Cash-Flow Analysis

1-17

All cash flows aretreated as though

they occur at year end.

Cash flows aretreated as if

they are knownwith certainty.

Cash inflows areimmediately

reinvested atthe required

rate of return.

Assumes aperfectcapital

market.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 18/52

Choosing the Hurdle Rate

1-18

• The discount rate generallyis associated with thecompany’s cost of capital.

• The cost of capital involvesa blending of the costs of all sources of investment

funds, both debt and equity.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 19/52Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective3

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 20/52

Comparing Two InvestmentProjects

1-20

To compare competing investment projectswe can use the following net present value

approaches:

– Total-Cost Approach. – Incremental-Cost Approach.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 21/52

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 22/52

Total-Cost Approach

1-22

MAINFRAME ($) Today Year 1 Year 2 Year 3 Year 4 Year 5 Acquisition cost computer (400,000) Acquisition cost software ( 40,000)System update ( 40,000)Salvage value 50,000Operating costs (335,000) (335,000) (335,000) (335,000) (335,000) (335,000)Time sharing revenue 20,000 20,000 20,000 20,000 20,000 20,000Total cash flow 440,000 (315,000) (315,000) (355,000) (315,000) (265,000)

X Discount factor X 1.000 X .893 X .797 X .712 X .636 X .567Present value (440,000) (281,295) (251,055) (252,760) (200,340) (150,255)

SUM = ($1,575,705)

PERSONAL COMPUTER ($) Today Year 1 Year 2 Year 3 Year 4 Year 5 Acquisition cost computer (300,000) Acquisition cost software ( 75,000)

System update ( 60,000)Salvage value 50,000Operating costs (235,000) (235,000) (235,000) (235,000) (235,000) (235,000)Time sharing revenue -0- -0- -0- -0- -0- -0- _Total cash flow 375,000 (235,000) (235,000) (295,000) (235,000) (205,000)X Discount factor X 1.000 X .893 X .797 X .712 X .636 X .567Present value (375,000) (209,855) (187,295) (210,040) (149,460) (116,235)

SUM = ($1,247,885)

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 23/52

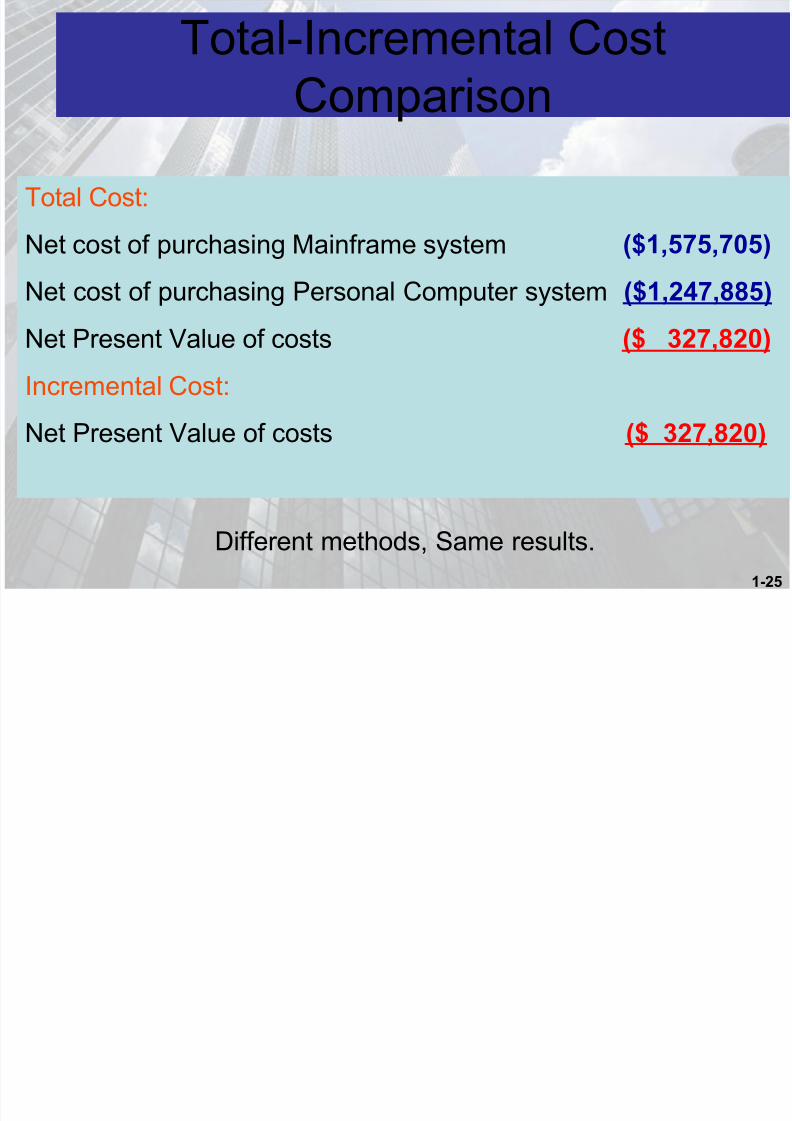

Total-Cost Approach

1-23

Net cost of purchasing Mainframe system ($1,575,705)

Net cost of purchasing Personal Computer system ($1,247,885)

Net Present Value of costs ($ 327,820)

Mountainview should purchase the personalcomputer system for a cost savings of

$327,820.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 24/52

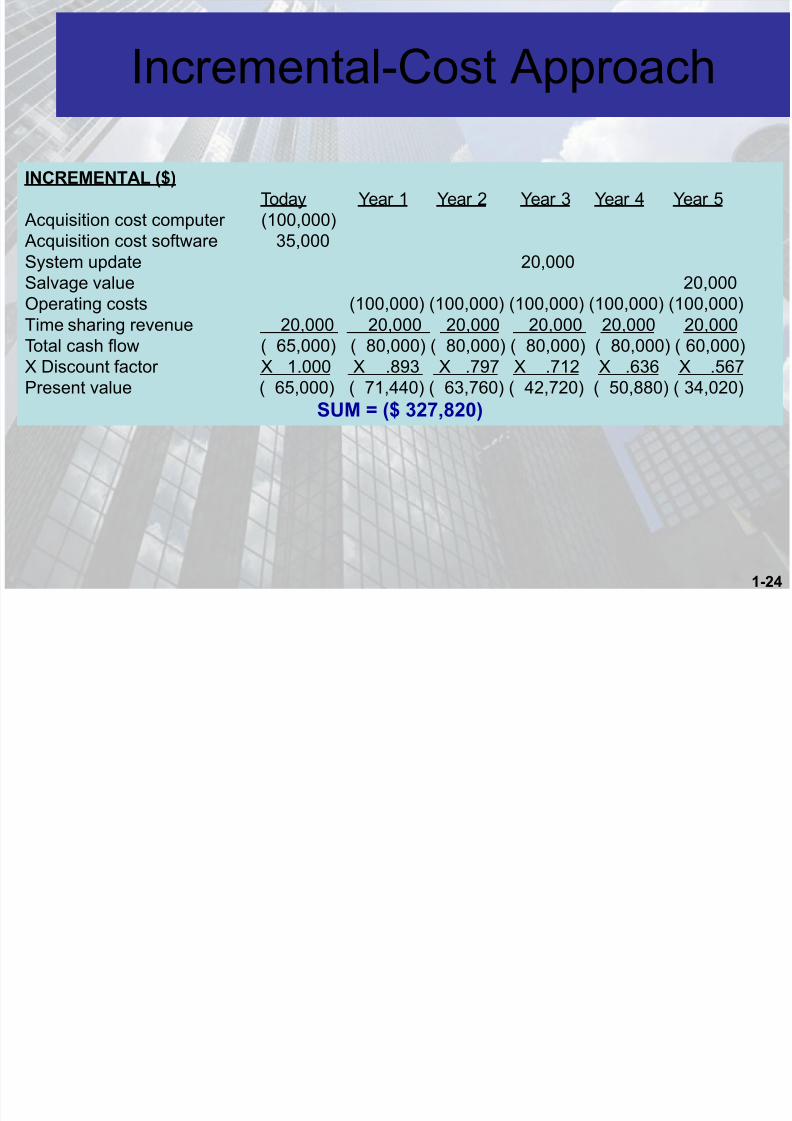

Incremental-Cost Approach

1-24

INCREMENTAL ($)Today Year 1 Year 2 Year 3 Year 4 Year 5

Acquisition cost computer (100,000) Acquisition cost software 35,000System update 20,000

Salvage value 20,000Operating costs (100,000) (100,000) (100,000) (100,000) (100,000)Time sharing revenue 20,000 20,000 20,000 20,000 20,000 20,000Total cash flow ( 65,000) ( 80,000) ( 80,000) ( 80,000) ( 80,000) ( 60,000)X Discount factor X 1.000 X .893 X .797 X .712 X .636 X .567Present value ( 65,000) ( 71,440) ( 63,760) ( 42,720) ( 50,880) ( 34,020)

SUM = ($ 327,820)

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 25/52

Total-Incremental CostComparison

1-25

Total Cost:

Net cost of purchasing Mainframe system ($1,575,705)

Net cost of purchasing Personal Computer system ($1,247,885)

Net Present Value of costs ($ 327,820)

Incremental Cost:

Net Present Value of costs ($ 327,820)

Different methods, Same results.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 26/52

Managerial Accountant’s Role

1-26

Managerial accountants are often asked topredict cash flows related to operating cost

savings, additional working capital

requirements, and incremental costs andrevenues.

When cash flow projections are very uncertain,

the accountant may . . .1. increase the hurdle rate,

2. use sensitivity analysis.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 27/52

Postaudit of Investment Projects

1-27

A postaudit is a follow-up after the project hasbeen approved to see whether or notexpected results are actually realized.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 28/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective4

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 29/52

Income Taxes and CapitalBudgeting

1-29

Cash flows from an investment proposal affectthe company’s profit and its income tax

liability.

Income = Revenue - Expenses + Gains - Losses

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 30/52

After-Tax Cash Flows

1-30

The tax rate is 40%, so income taxes are

$525,000 40% = $ 210,000

High Country Department Stores

Income StatementFor the Year Ended Jun 30, 2007

Revenue $ 1,000,000

Expenses (475,000)Income before taxes 525,000

Income taxes (210,000)

Net Income 315,000

Not all expenses require cash outflows. The most common example is depreciation.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 31/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective5

M difi d A l t d C t

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 32/52

Modified Accelerated CostRecovery System (MACRS)

1-32

Tax depreciation is usually computed usingMACRS. Here are the depreciation rate for 3,

5, and 7-year class life assets.

Year 3-year 5-year 7-year

1 33.33% 20.00% 14.29%

2 44.45% 32.00% 24.49%

3 14.81% 19.20% 17.49%

4 7.41% 11.52% 12.49%5 11.52% 8.93%

6 5.76% 8.92%

7 8.93%

8 4.46%

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 33/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective6

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 34/52

Investment in Working Capital

1-34

Some investment proposals require additionaloutlays for working capital such as

increases in cash, accounts receivable, and

inventory.

Current assets 100,000$

Less: current liabilities (65,000)

Working capital 35,000$

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 35/52

Extended Illustration

1-35

For a complete present value analysis for aninvestment decision facing High Country

Department Stores, Inc., see the textbook.

High Country

Department

Stores

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 36/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective7

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 37/52

Ranking Investment Projects

1-37

We can invest in either of these projects.Use a 10% discount rate to determinethe net present value of the cash flows.

Project A Project B

Immediate cash outlay 100,000$ 100,000$Cash inflows:

Year 1 50,000$ 30,000$

Year 2 40,000 40,000

Year 3 30,000 50,000 Total inflows 120,000$ 120,000$

The total cash flows are the same, but the pattern of

the flows is different.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 38/52

Ranking Investment Projects

1-38

Let’s calculate the present value of the cashflows associated with Project A.

This project has a positive net present value which meansthe project’s return is greater than the discount rate.

Project A PV Factor PV

Immediate cash outlay (100,000)$ 1.000 (100,000)$Cash inflows:

Year 1 50,000$ 0.909 45,450

Year 2 40,000 0.826 33,040

Year 3 30,000 0.751 22,530

Net present value 1,020$

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 39/52

Ranking Investment Projects

1-39

Here is the net present value of the cash flowsassociated with Project B.

Project B PV Factor PV

Immediate cash outlay (100,000)$ 1.000 (100,000)$

Cash inflows:

Year 1 30,000$ 0.909 27,270

Year 2 40,000 0.826 33,040

Year 3 50,000 0.751 37,550

Net present value (2,140)$

Project B has a negative net present value which meansthe project’s return is less than the discount rate.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 40/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective8

Alt ti M th d f M ki

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 41/52

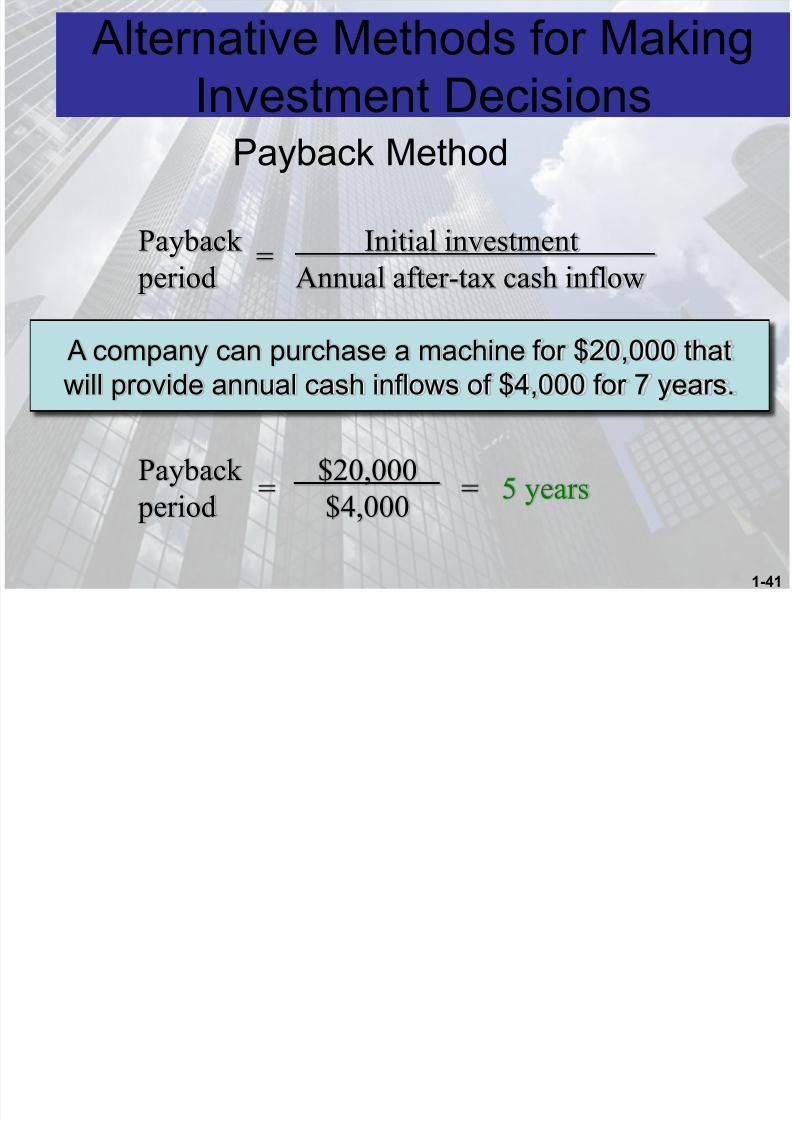

Alternative Methods for MakingInvestment Decisions

1-41

Payback Method

Payback

period

Initial investment

Annual after-tax cash inflow

=

Payback

period=

$20,000

$4,000= 5 years

A company can purchase a machine for $20,000 thatwill provide annual cash inflows of $4,000 for 7 years.

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 42/52

Payback: Pro and Con

1-42

1. Fails to considerthe time value ofmoney.

2. Does not considera project’s cash

flows beyond the

payback period.

1. Provides a tool forroughly screeninginvestments.

2. For some firms, it

may be essentialthat an investmentrecoup its initialcash outflows asquickly aspossible.

Accounting Rate of Return

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 43/52

Accounting-Rate-of-ReturnMethod

1-43

Discounted-cash-flow method focuses oncash flows and the time value of money.

Accounting-rate-of-return method focuses onthe incremental accounting income that

results from a project.

Accounting Rate of Return

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 44/52

Accounting-Rate-of-ReturnMethod

1-44

The following formula is used to calculate theaccounting rate of return:

Accountingrate ofreturn

=

Average Averageincremental incremental expenses,revenues including depreciation &

income taxes

-

Initial investment

Accounting Rate of Return

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 45/52

Accounting-Rate-of-ReturnMethod

1-45

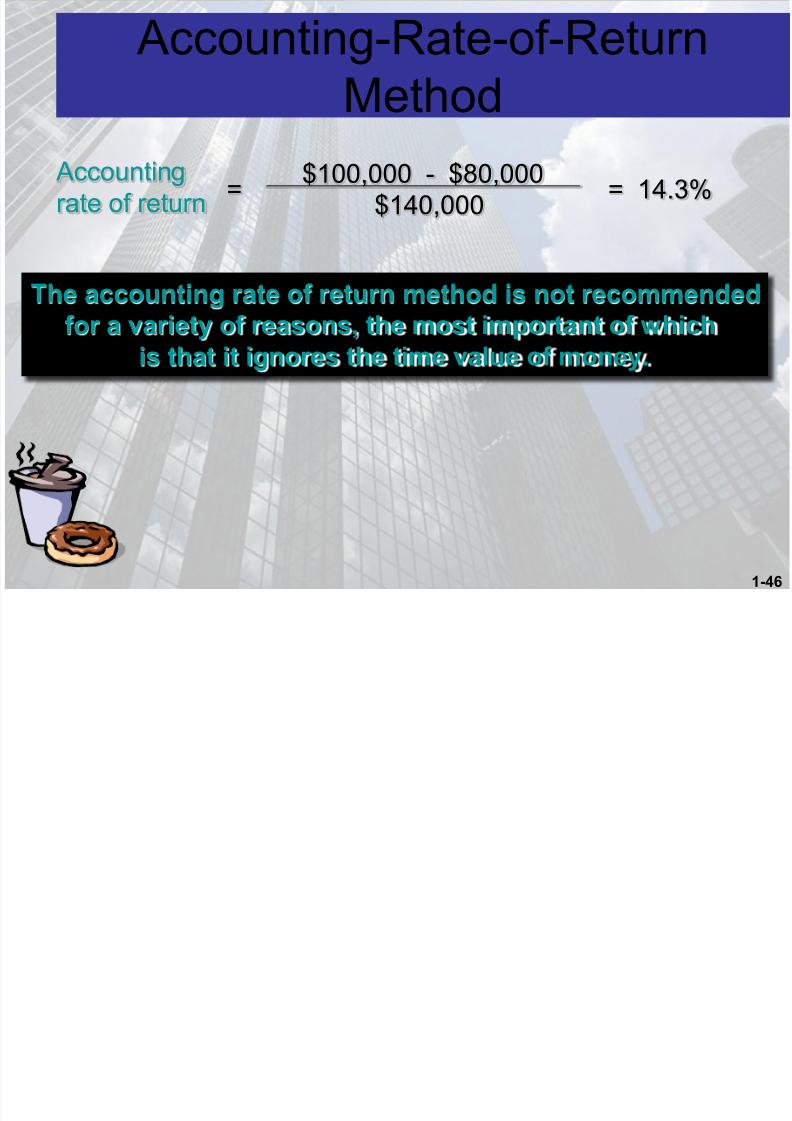

Meyers Company wants to install an espresso barin its restaurant.

The espresso bar:

– Cost $140,000 and has a 10-year life. – Will generate incremental revenues of $100,000 and

incremental expenses of $80,000 includingdepreciation.

What is the accounting rate of return on theinvestment project?

Accounting Rate of Return

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 46/52

Accounting-Rate-of-ReturnMethod

1-46

The accounting rate of return method is not recommendedfor a variety of reasons, the most important of which

is that it ignores the time value of money.

Accountingrate of return

$100,000 - $80,000$140,000

= 14.3%=

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 47/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective9

E ti ti C h Fl

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 48/52

Estimating Cash Flows:The Role of Activity-Based Costing

1-48

ABC systems generally improve the ability ofan analyst to estimate the cash flowsassociated with a proposed project.

J tifi ti f I t t i Ad d

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 49/52

Justification of Investments in AdvancedManufacturing Systems

1-49

Hurdle

rates aretoo high

Timehorizons

are tooshort

Bias

towardsincrementalprojects

Greatercash flow

uncertainty

Benefitsdifficult toquantify

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 50/52

Copyright

© 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Learning

Objective10

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 51/52

Inflation Effects

1-51

Nominal DollarsReal dollars

8/10/2019 Chapter 16 n

http://slidepdf.com/reader/full/chapter-16-n 52/52

End of Chapter 16