chapter 15 the cost of home ownership copyright © 2011 by the mcgraw-hill companies, inc. all...

TRANSCRIPT

Chapter 15

The Cost of Home The Cost of Home OwnershipOwnership

Copyright © 2011 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

15-2

1. List the types of mortgages available

2. Utilize an amortization chart to compute monthly mortgage payments

3. Calculate the total cost of interest over the life of a mortgage

The Cost of Home Ownership#15#15Learning Unit ObjectivesTypes of Mortgages and the Monthly Mortgage Payment

LU15.1LU15.1

15-3

1. Calculate and identify the interest and principal portion of each monthly payment

2. Prepare an amortization schedule

The Cost of Home Ownership#15#15Learning Unit ObjectivesAmortization Schedule -- Breaking Down the Monthly PaymentLU15.2LU15.2

15-4

Table 15.1 - Amortization Chart (PARTIAL)

(Mortgage principal and interest per $1,000)

Termsin years 5.50% 6.00% 6.50% 7.00% 7.50% 8.00% 8.50% 9.00%

10 10.86 11.11 11.36 11.62 11.88 12.14 12.40 12.6712 9.51 9.76 10.02 10.29 10.56 10.83 11.11 11.3915 8.18 8.44 8.72 8.99 9.28 9.56 9.85 10.1517 7.56 7.84 8.12 8.40 8.69 8.99 9.29 9.5920 6.88 7.17 7.46 7.76 8.06 8.37 8.68 9.0022 6.51 6.82 7.13 7.44 7.75 8.07 8.39 8.7225 6.15 6.45 6.76 7.07 7.39 7.72 8.06 8.4030 5.68 6.00 6.33 6.66 7.00 7.34 7.69 8.0535 5.38 5.71 6.05 6.39 6.75 7.11 7.47 7.84

15-5

Computing the Monthly Payment for Principal and Interest

Gary bought a home for $200,000. He made a 20% down payment. The 9% mortgage is for 30 years (30 x 12 = 360 payments). What are Gary’s monthly payment andtotal cost of interest?

15-6

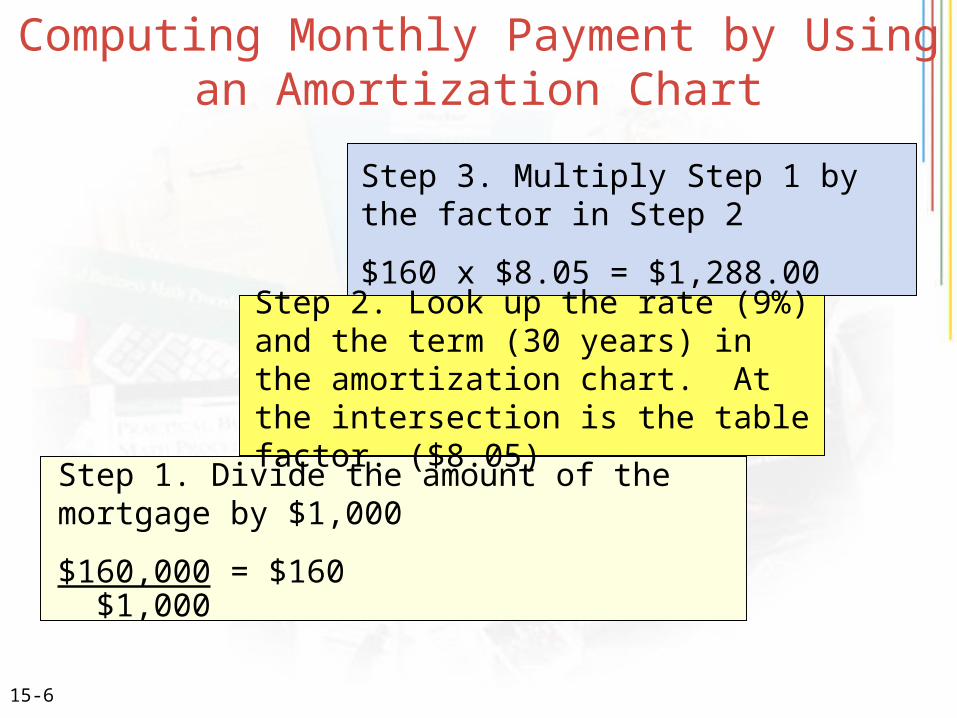

Step 2. Look up the rate (9%) and the term (30 years) in the amortization chart. At the intersection is the table factor. ($8.05)

Step 3. Multiply Step 1 by the factor in Step 2

$160 x $8.05 = $1,288.00

Step 1. Divide the amount of the mortgage by $1,000

$160,000 = $160 $1,000

Computing Monthly Payment by Using an Amortization Chart

15-7

Computing the Monthly Payment for Principal and Interest

$160,000 = 160 x $8.05 (table rate) = $1,288.00 $1,000

Total payments Mortgage Total interest

$463,680 - $160,000 = $303,680 ($1,288.00 x 360)

Monthly Payment

15-8

Table 15.2 - Effect of Interest Rates on Monthly Payments

9% 11% Difference

Monthly payment $1,288.00 $1,524.80 $236.80

(160 x $8.05) (160 x $9.53)

Total cost of interest $303,680 $388,828 $85,248

($1,288.00 x 360) - $160,000 ($236.80 x 360)

($1,524.80 x 360) - $160,000

15-9

The Effect of Loan Types on Monthly Payments

Suppose Gary chose a 15-year mortgage vs. a 30-year mortgage. What would be the effect?

15 Year 30 Year Difference

Monthly Payment $1,624.00 $1,288.00 $336.00

Total Interest $100,912 $303,680 ($202,768) ($1,624.00 x 180) -$140,000

($1,288.00 x 360) - $160,000

15-10

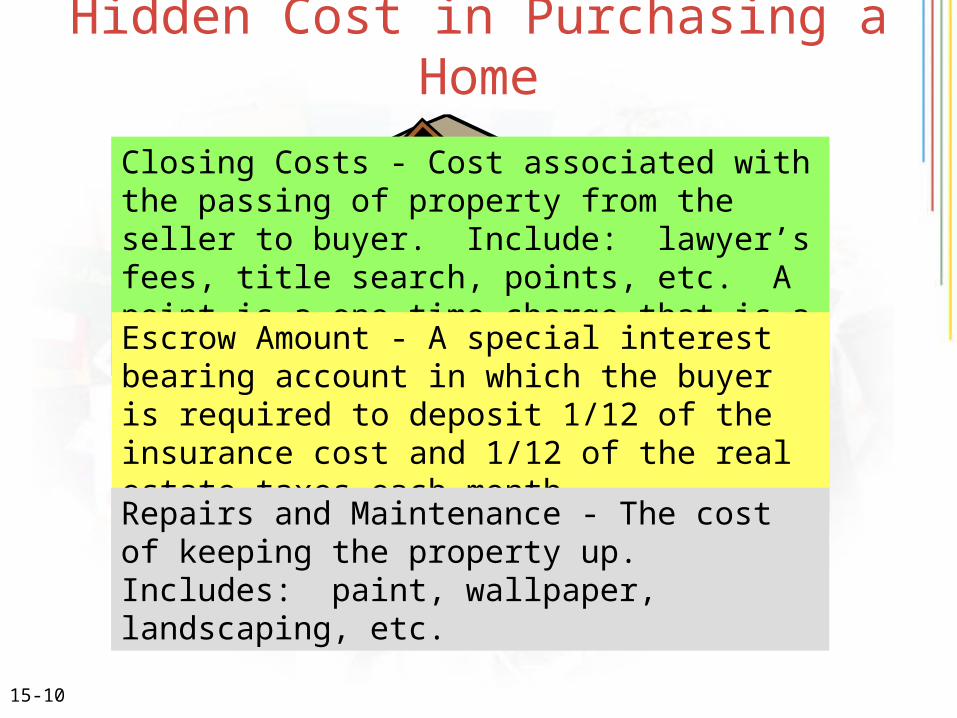

Hidden Cost in Purchasing a Home

Closing Costs - Cost associated with the passing of property from the seller to buyer. Include: lawyer’s fees, title search, points, etc. A point is a one-time charge that is a percent of the mortgage.

Escrow Amount - A special interest bearing account in which the buyer is required to deposit 1/12 of the insurance cost and 1/12 of the real estate taxes each month

Repairs and Maintenance - The cost of keeping the property up. Includes: paint, wallpaper, landscaping, etc.

15-11

Step 2. Calculate the amount used to reduce the principal: Principal reduction = Monthly payment - Interest (Step 1.) $1,288.00-$120.00 = $88.00

Step 3. Calculate the new principal: Current principal - Reduction of principal (Step 2) = New Principal $160,000 - $88.00 = $159,912.00

Step 1. Calculate the interest for a month (use current principal): Interest = Principal x Rate x Time

$160,000 x .09 x 1/12 = $1,200.00

Calculating Interest, Principal, and New Balance of Monthly Payment

15-12

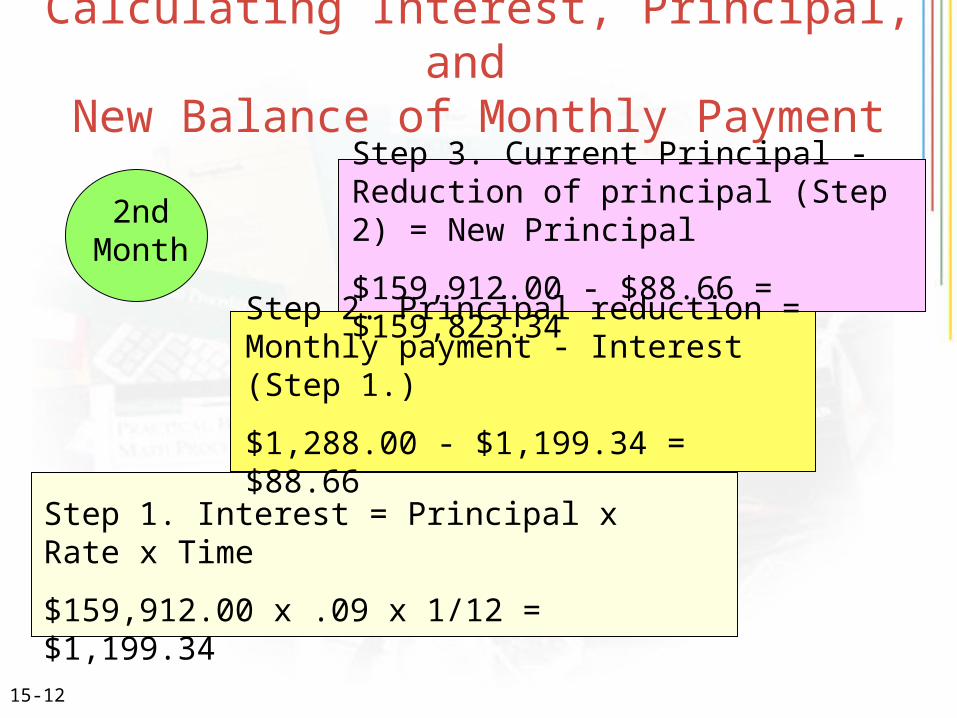

Step 2. Principal reduction = Monthly payment - Interest (Step 1.)

$1,288.00 - $1,199.34 = $88.66

Step 3. Current Principal - Reduction of principal (Step 2) = New Principal

$159,912.00 - $88.66 = $159,823.34

Step 1. Interest = Principal x Rate x Time

$159,912.00 x .09 x 1/12 = $1,199.34

Calculating Interest, Principal, and New Balance of Monthly Payment

2nd Month

15-13

Table 15.3 - Partial Amortization Schedule

Payment Principal Principal Balance of

number (current) Interest reduction principal

1 $160,000 $1.200.00 $88.00 $159,912.00

($160,000 x .09 x 1/12) ($1,288.60 – 1,200) ($160,000 - $88.00)

2 $159,912.00 $1,199.34 $88.66 $159,823.34

($159,912 x .09 x 1/12) ($1,288 – 1,199.34) ($159,912 - $88.66)

3 $159,823.34 $1,198.68 $89.32 $159,734.02

4 $159,734.02 $1,198.01 $89.99 $159,644.03

5 $159,644.03 $1,197.33 $90.67 $159,553.36

15-14

Problem 15-9:

$215,000 x 0.2 = $43,000

$215,000 - $43,000 = $172,000

$172,000/$1,000 = 172 x $5.37 = $923.64

15-15

Problem 15-10:

$50,000,000 $50,000,000

X .20 (down payment) - 10,000,000

$ 10,000,000 (down) $40,000,000 mortgage

payment

$40,000,000

$1,000 = $40,000 x $6.66 = $266,400 monthly payment

15-16

Problem 15-11:

$140,000 - $28,000 = $112,000/$1,000 = 112 x $5.68 = $636.16 x 360 = $229,017.60 - $112,000 = $117,017.60 total interest

15-17

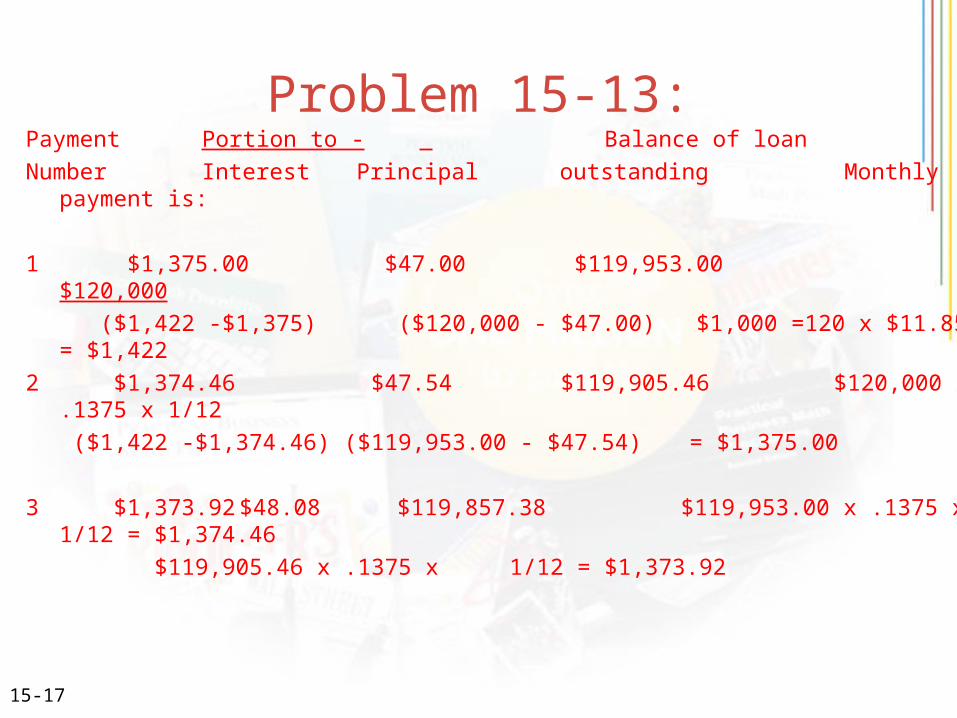

Problem 15-13:Payment Portion to - Balance of loan

Number Interest Principal outstanding Monthly payment is:

1 $1,375.00 $47.00 $119,953.00 $120,000

($1,422 -$1,375) ($120,000 - $47.00) $1,000 =120 x $11.85 = $1,422

2 $1,374.46 $47.54 $119,905.46 $120,000 x .1375 x 1/12

($1,422 -$1,374.46) ($119,953.00 - $47.54) = $1,375.00

3 $1,373.92 $48.08 $119,857.38 $119,953.00 x .1375 x 1/12 = $1,374.46

$119,905.46 x .1375 x 1/12 = $1,373.92

15-18

Problem 15-14:

a. 40 x $10.17 = $406.80 x 300 = $122,040 - $40,000 = $82,040

b. 40 x $10.91 = $436.40 x 300 = $130,920 - $40,000 = $90,920

c. 40 x $11.66 = $466.40 x 300 = $139,920 - $40,000 = $99,920

d. 40 x $12.81 = $512.40 x 300 = $153,720 - $40,000 = $113,720

e. $113,720 - $82,040 = $31,680 difference

f. 40 x $12.65 = $506 x 360 = $182,160 - $40,000 = $142,160

40 x $9.91= $396.40 x 360 = $142,704 - $40,000 = - 102,704

difference $ 39,456