chapter 12

TRANSCRIPT

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Introduction to Binomial Trees

Chapter 12

1

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

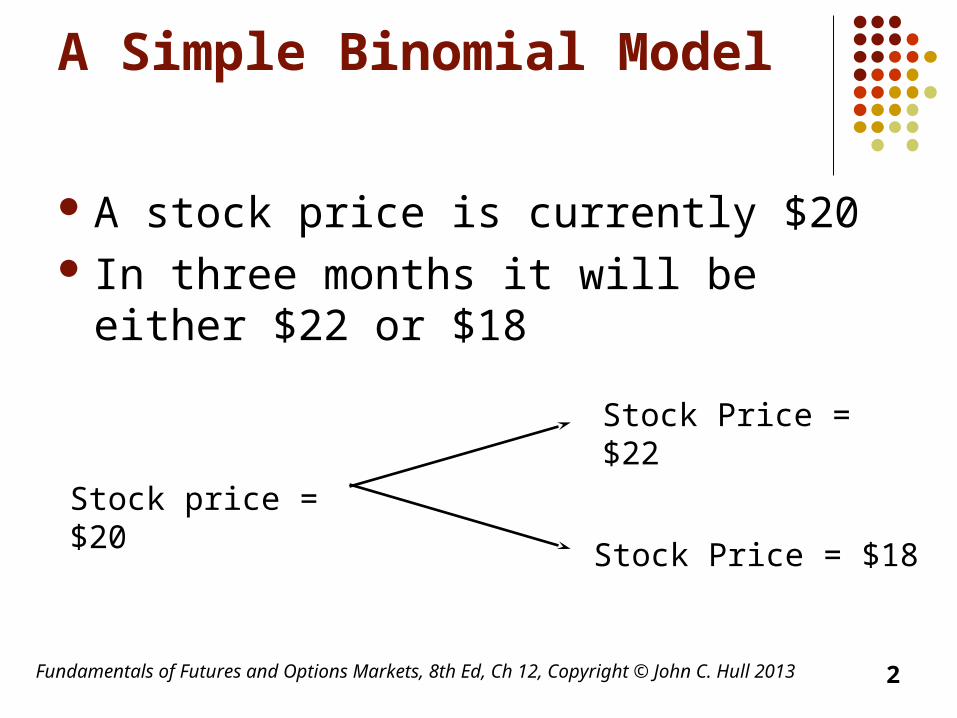

A Simple Binomial Model

A stock price is currently $20 In three months it will be either $22 or $18

Stock Price = $22

Stock Price = $18

Stock price = $20

2

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

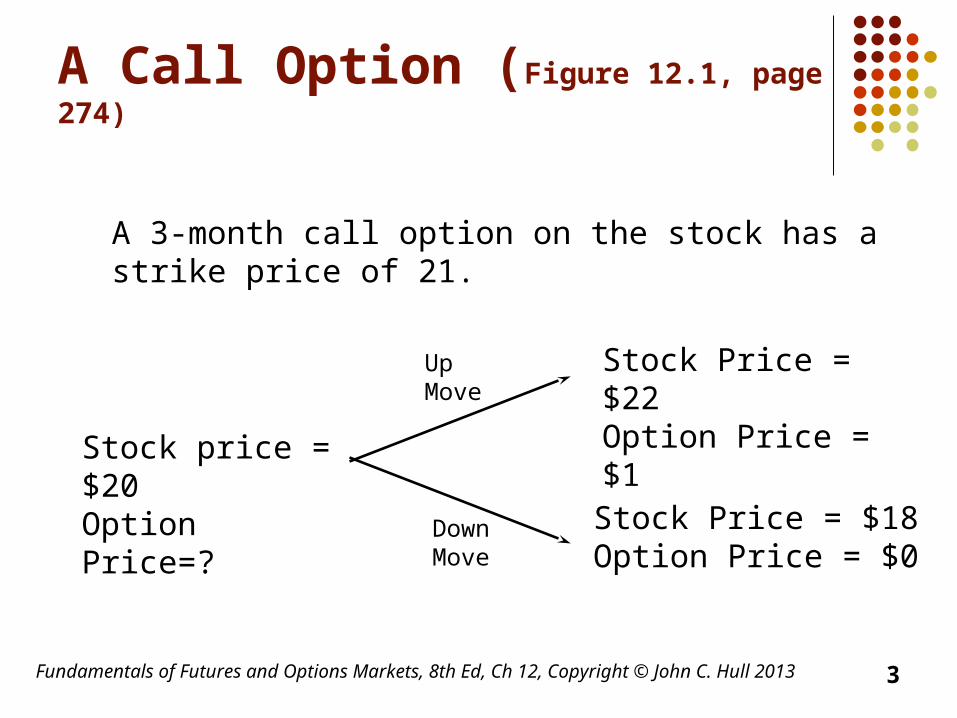

Stock Price = $22Option Price = $1

Stock Price = $18Option Price = $0

Stock price = $20Option Price=?

A Call Option (Figure 12.1, page 274)

A 3-month call option on the stock has a strike price of 21.

3

Up Move

Down Move

Setting Up a Riskless Portfolio For a portfolio that is long shares and a short 1 call

option values are

Portfolio is riskless when 22– 1 = 18 or = 0.25

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 4

22– 1

18

Up Move

Down Move

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Valuing the Portfolio(Risk-Free Rate is 12%)

The riskless portfolio is:

long 0.25 sharesshort 1 call option

The value of the portfolio in 3 months is 22 0.25 – 1 = 4.50

The value of the portfolio today is 4.5e – 0.120.25 = 4.3670

5

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Valuing the Option

The portfolio that is

long 0.25 sharesshort 1 option

is worth 4.367 The value of the shares is

5.000 (= 0.25 20 ) The value of the option is therefore

0.633 (= 5.000 – 4.367 )

6

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Generalization (Figure 12.2, page 275)

A derivative lasts for time T and is dependent on a stock

Su ƒu

Sd ƒd

Sƒ

7

Up Move

Down Move

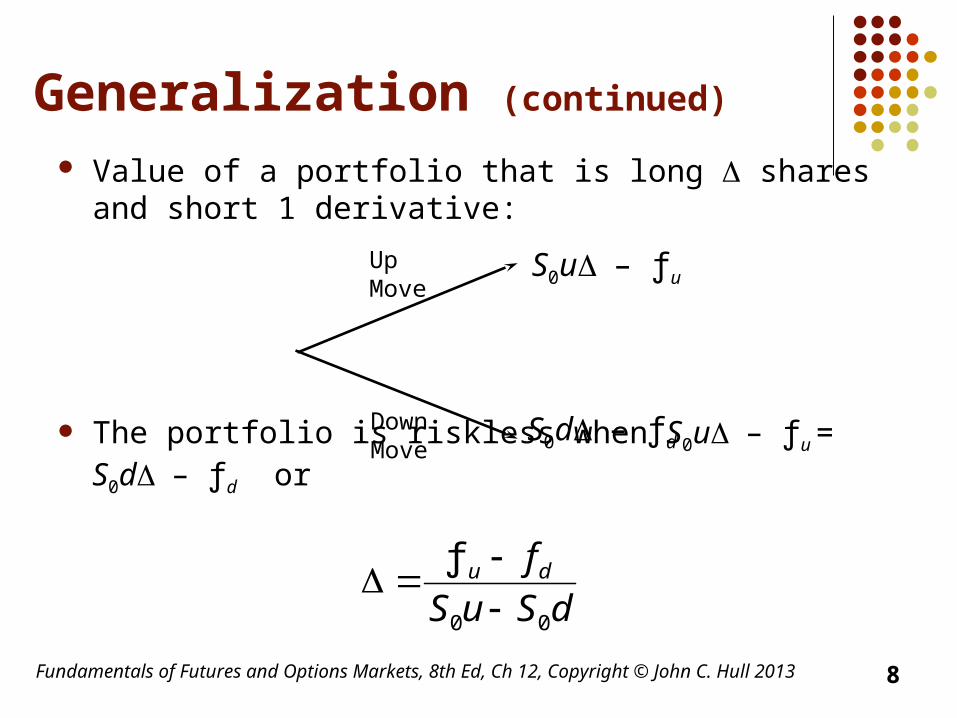

Generalization (continued)

Value of a portfolio that is long shares and short 1 derivative:

The portfolio is riskless when S0u– ƒu = S0d– ƒd or

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 8

dSuS

fdu

00

ƒ

S0u– ƒu

S0d– ƒd

Up Move

Down Move

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Generalization(continued)

Value of the portfolio at time T is Su – ƒu

Value of the portfolio today is (Su – ƒu )e–rT

Another expression for the portfolio value today is S – f

Hence ƒ = S – (Su – ƒu )e–rT

9

Generalization(continued)

Substituting for we obtain

ƒ = [ pƒu + (1 – p)ƒd ]e–rT

where

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 10

pe d

u d

rT

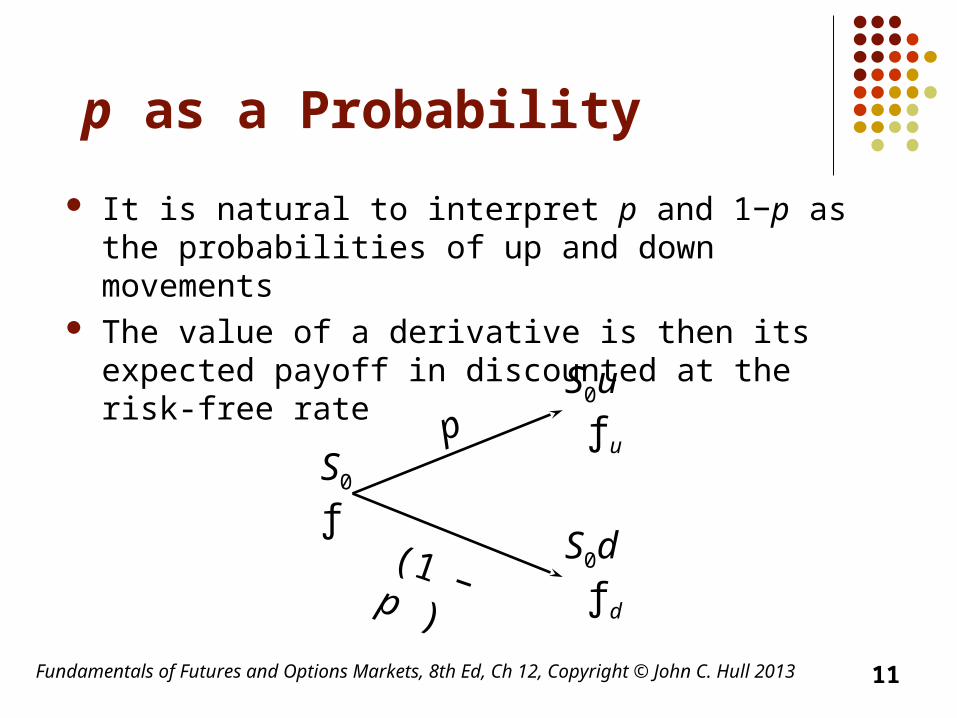

p as a Probability

It is natural to interpret p and 1−p as the probabilities of up and down movements

The value of a derivative is then its expected payoff in discounted at the risk-free rate

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 11

S0u ƒu

S0d ƒd

S0

ƒ

p

(1– p )

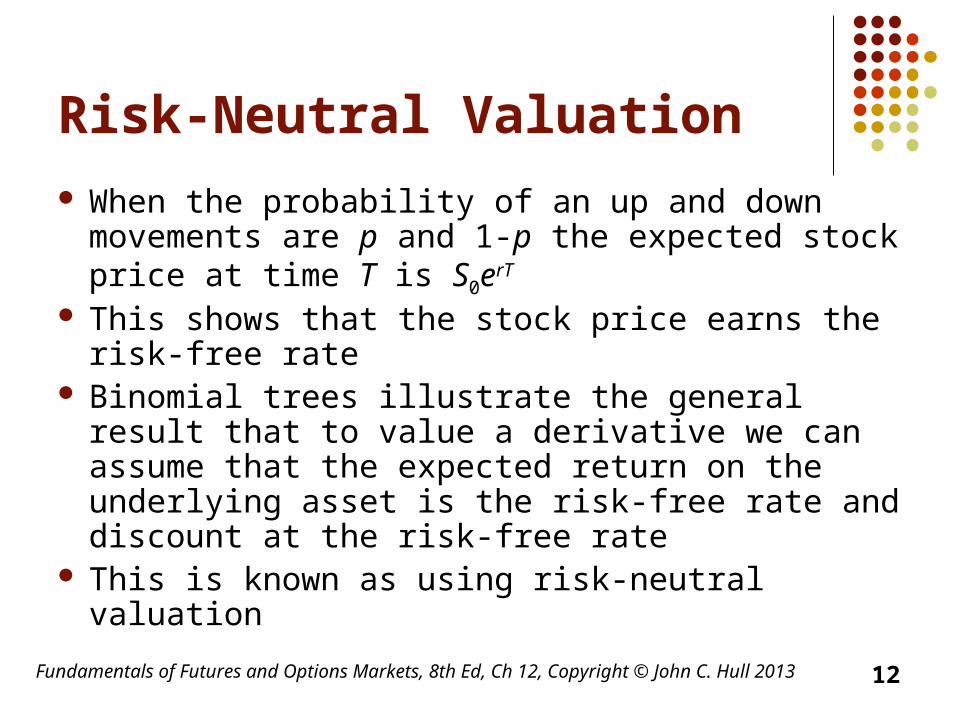

Risk-Neutral Valuation

When the probability of an up and down movements are p and 1-p the expected stock price at time T is S0erT

This shows that the stock price earns the risk-free rate

Binomial trees illustrate the general result that to value a derivative we can assume that the expected return on the underlying asset is the risk-free rate and discount at the risk-free rate

This is known as using risk-neutral valuation

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 12

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Irrelevance of Stock’s Expected Return

When we are valuing an option in terms of the underlying stock the expected return on the stock is irrelevant

13

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

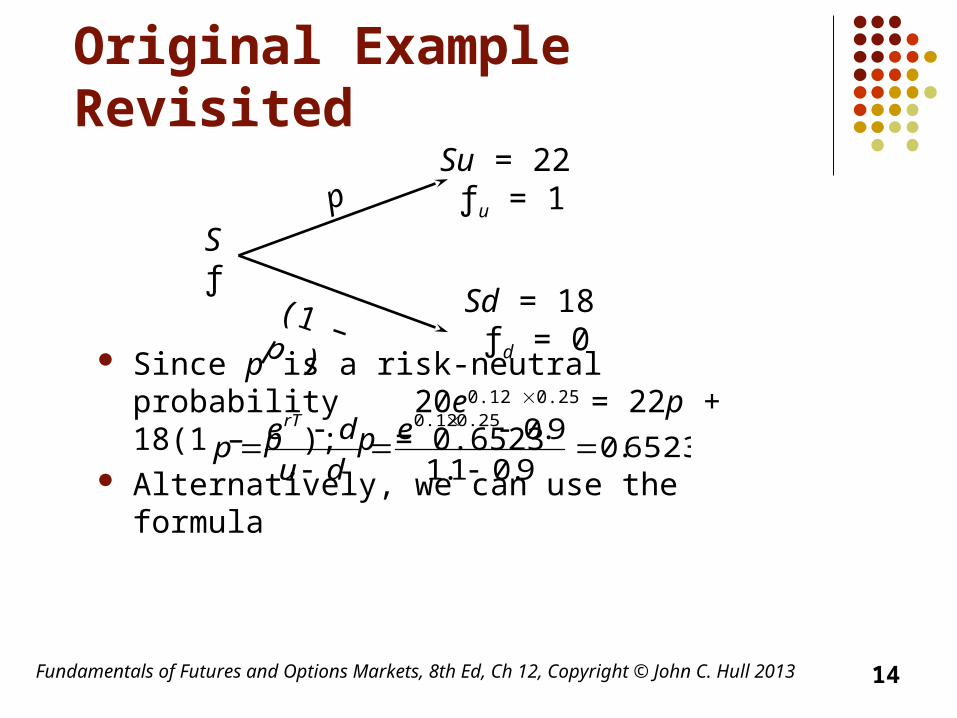

Original Example Revisited

Since p is a risk-neutral probability20e0.12 0.25 = 22p + 18(1 – p ); p = 0.6523

Alternatively, we can use the formula

6523.09.01.1

9.00.250.12

e

du

dep

rT

Su = 22 ƒu = 1

Sd = 18 ƒd = 0

Sƒ

p

(1– p )

14

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

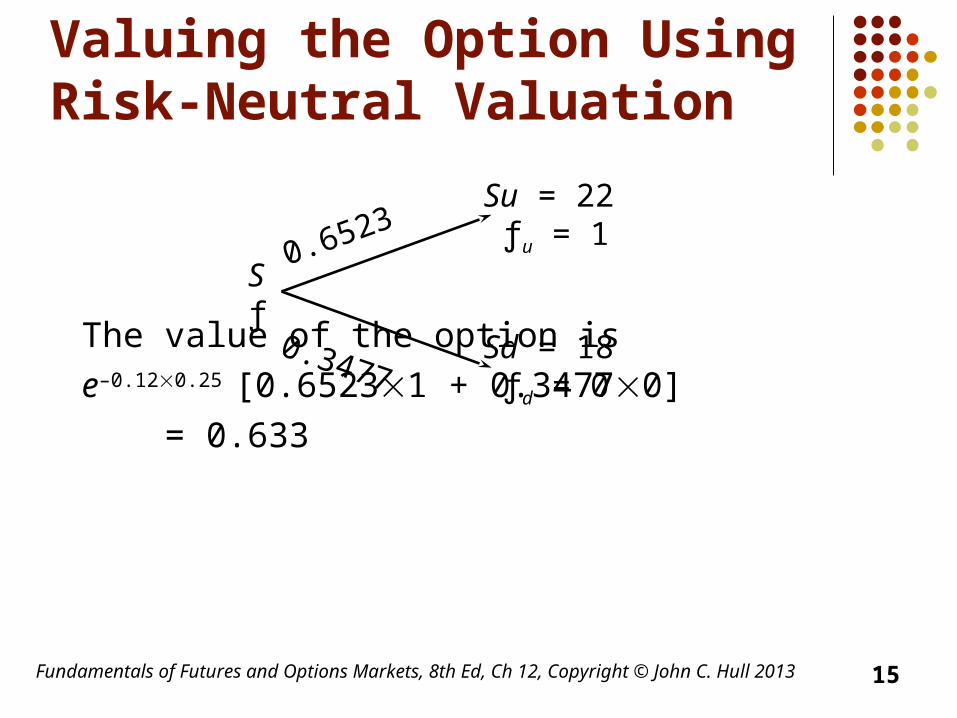

Valuing the Option Using Risk-Neutral Valuation

The value of the option is

e–0.120.25 [0.65231 + 0.34770]

= 0.633

Su = 22 ƒu = 1

Sd = 18 ƒd = 0

Sƒ

0.6523

0.3477

15

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

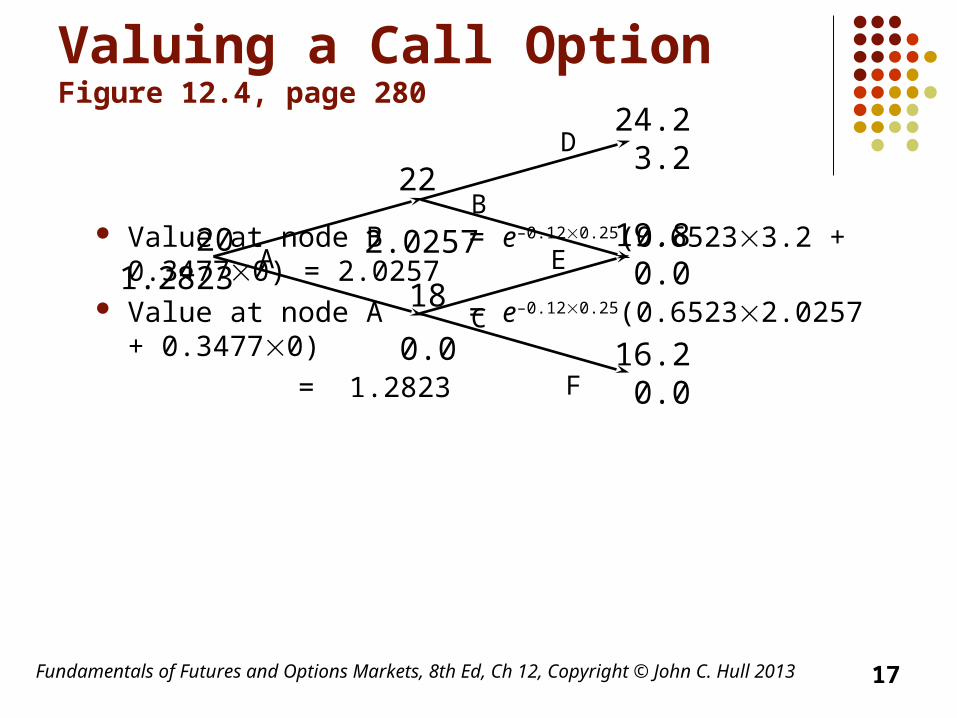

A Two-Step ExampleFigure 12.3, page 280

Each time step is 3 months K=21, r =12%

20

22

18

24.2

19.8

16.2

16

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Valuing a Call OptionFigure 12.4, page 280

Value at node B = e–0.120.25(0.65233.2 + 0.34770) = 2.0257

Value at node A = e–0.120.25(0.65232.0257 + 0.34770)

= 1.2823

201.2823

22

18

24.23.2

19.80.0

16.20.0

2.0257

0.0

A

B

C

D

E

F

17

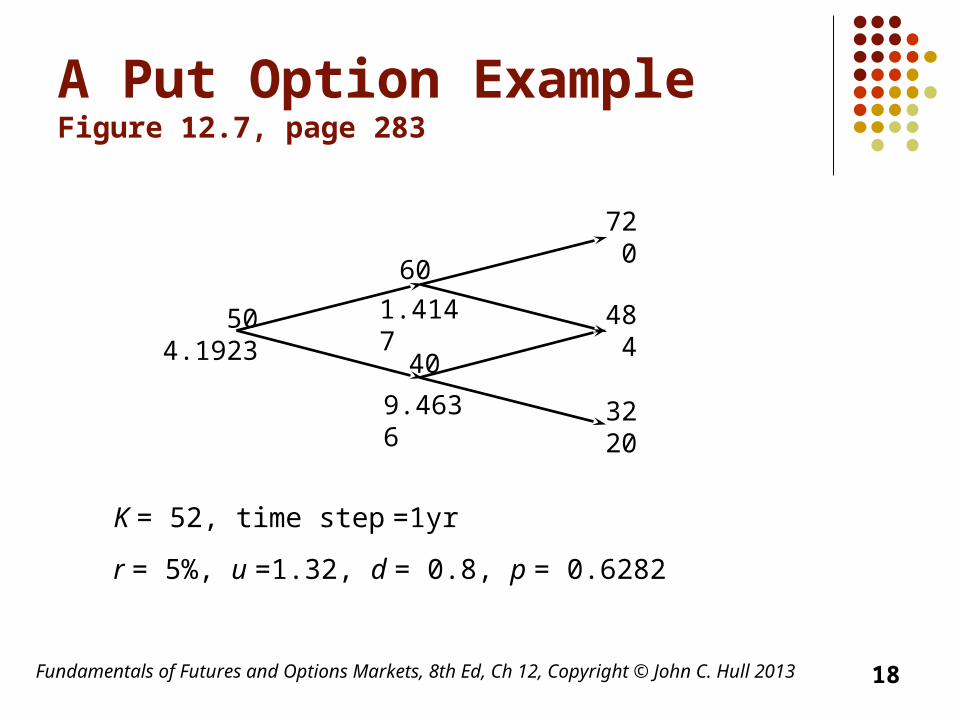

A Put Option ExampleFigure 12.7, page 283

K = 52, time step =1yr

r = 5%, u =1.32, d = 0.8, p = 0.6282

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 18

504.1923

60

40

720

484

3220

1.4147

9.4636

What Happens When the Put Option is American (Figure 12.8, page 284)

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 19

505.0894

60

40

720

484

3220

1.4147

12.0CThe American feature

increases the value at node C from 9.4636 to 12.0000.

This increases the value of the option from 4.1923 to 5.0894.

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Delta

Delta () is the ratio of the change in the price of a stock option to the change in the price of the underlying stock

The value of varies from node to node

20

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013

Choosing u and d

One way of matching the volatility is to set

where is the volatility andt is the length of the time step. This is the approach used by Cox, Ross, and Rubinstein (1979)

t

t

eud

eu

1

21

Assets Other than Non-Dividend Paying Stocks

For options on stock indices, currencies and futures the basic procedure for constructing the tree is the same except for the calculation of p

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 22

The Probability of an Up Move

contract futures a for 1

rate free-risk foreign the is herecurrency w a for

index the on yielddividend the is eindex wher stock a for

stock paying dnondividen a for

a

rea

qea

ea

du

dap

ftrr

tqr

tr

f )(

)(

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 23

Increasing the Time Steps

In practice at least 30 time steps are necessary to give good option values

DerivaGem allows up to 500 time steps to be used

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 24

The Black-Scholes-Merton Model

The BSM model can be derived by looking at what happens to the price of a European call option as the time step tends to zero

See Appendix to Chapter 12

Fundamentals of Futures and Options Markets, 8th Ed, Ch 12, Copyright © John C. Hull 2013 25