chapter 10 domestic institutions and markets

DESCRIPTION

It's Chartered Institute of Management Accountants Course: C-04 Fundamentals of Business Economics ,Class LSBF Manchester ,Q's By Teacher Micheal Mubaiwa.TRANSCRIPT

www.studyinteract ive.org 113

Chapter 10

Financial systems 2 domestic institutions

and markets

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

114 www.studyinteractive.org

CHAPTER CONTENTS

LEARNING OUTCOMES ------------------------------------------------- 115

COMMERCIAL BANKS AND CREDIT CREATION ---------------------- 116

FINANCIAL INSTRUMENTS -------------------------------------------- 119

ROLE OF CENTRAL BANKS --------------------------------------------- 122

FINANCIAL MARKETS -------------------------------------------------- 123

THE GLOBAL BANKING CRISIS ---------------------------------------- 124

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

115 www.studyinteractive.org

LEARNING OUTCOMES

(a) Explain the role of commercial banks in the process of credit creation and in

determining the structure of interest rates.

(b) Explain the role and in prudential

regulation.

(c) Explain the origins of the 2008 banking crisis and credit crunch.

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

116 www.studyinteractive.org

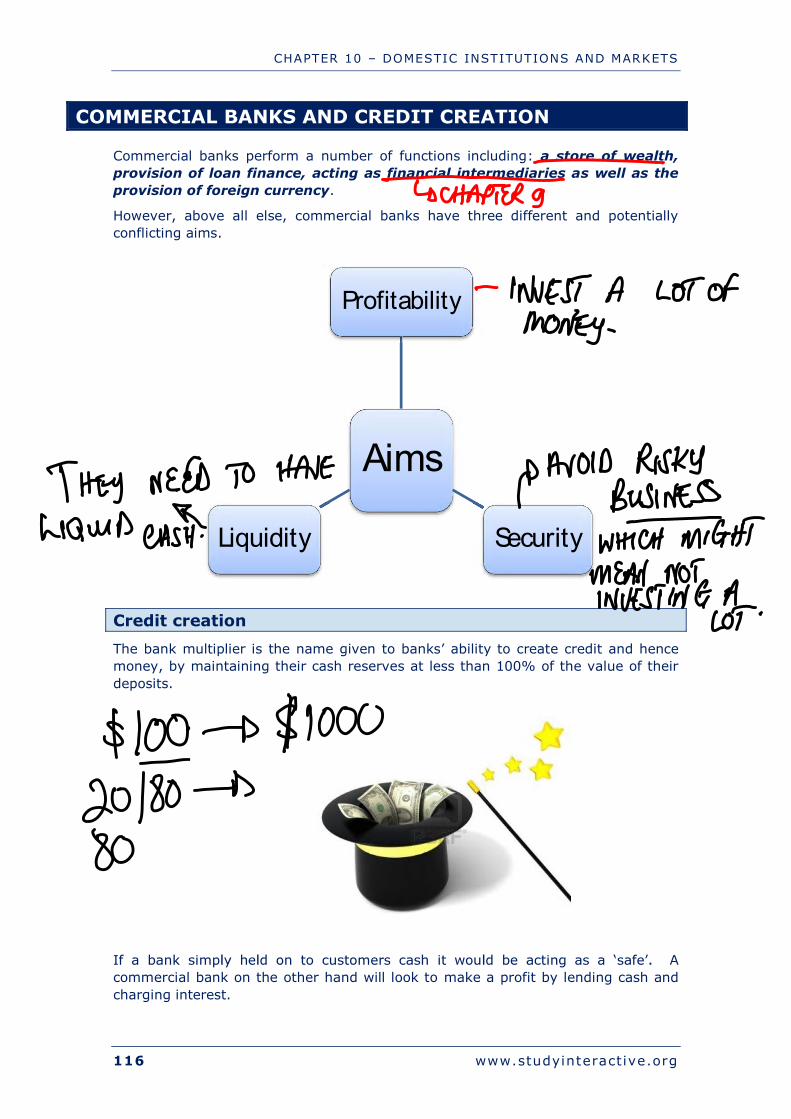

COMMERCIAL BANKS AND CREDIT CREATION

Commercial banks perform a number of functions including: a store of wealth,

provision of loan finance, acting as financial intermediaries as well as the

provision of foreign currency.

However, above all else, commercial banks have three different and potentially

conflicting aims.

Credit creation

The bank multiplier is the name given to banks ability to create credit and hence

money, by maintaining their cash reserves at less than 100% of the value of their

deposits.

A

commercial bank on the other hand will look to make a profit by lending cash and

charging interest.

Aims

Profitability

Security Liquidity

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

117 www.studyinteractive.org

The cash ratio describes the percentage of cash that a bank holds in reserve in

order to honor on demand withdrawals.

Exercise 1

In the following illustration we shall assume that there is only one bank in the

banking system and that all money lent by the bank is re-deposited by secondary

customers. The bank wishes to maintain a 25% cash ratio.

Complete the following table:

Deposit Cumulative

Deposits

Cash Reserve

Ratio (25%)

Cumulative

Loans

Incremental

Loan

$1,000 $1,000 $250 $750 $750

$750

Formula to calculate the quantitative side of credit creation:

Deposits =

Note: exam questions may well ask for either the total money supply following an

initial injection, or alternatively for just the increase. If asked to calculate the

increase then remember to deduct the initial deposit.

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

118 www.studyinteractive.org

Exercise 2

If all the commercial banks in a national economy operated on a cash reserve ratio

of 20%, how much cash would have to be deposited with the banks for the money

supply to increase by $300 million?

A $60 million

B $75 million

C $225 million

D $240 million

Exercise 3

A banking system in a small country consists of just four banks. Each bank has

decided to maintain a minimum cash ratio of 10%. Each bank now receives

additional cash deposits of $1 million. There will now be a further increase in total

bank deposits up to a maximum of:

A $400,000

B $4 million

C $36 million

D $40 million

Capital adequacy rules

In order to reduce their risk exposure banking institutions are required to maintain

a minimum amount of financial capital, ensuring the financial soundness and

consumer confidence in such institutions.

The Basel III Agreement was developed following the recent world financial

crisis, adding more stringent requirements regarding capital adequacy ratios and

minimum capital requirements.

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

119 www.studyinteractive.org

FINANCIAL INSTRUMENTS

Financial instruments are tradable assets. The yield on a financial instrument refers

to the return on an investment, calculated by dividing the nominal return by the

market price.

Nominal and real rates of interest

The real value of income from investments is eroded by inflation. The rate of

return after inflation has been deducted is called the real rate of interest.

The real rate of interest may be calculated as follows:

= 1 + real rate

Treasury bills

Treasury bills (T-Bills) are short term debt obligations. Their key characteristics

include:

Maturity < 1 year

Issued at a discount from their par value

The par value is re-paid at maturity.

Yield calculations

Discount yield

Investment yield

Key

F = face value

P = purchase price

M = maturity of bill in days

� ����

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

120 www.studyinteractive.org

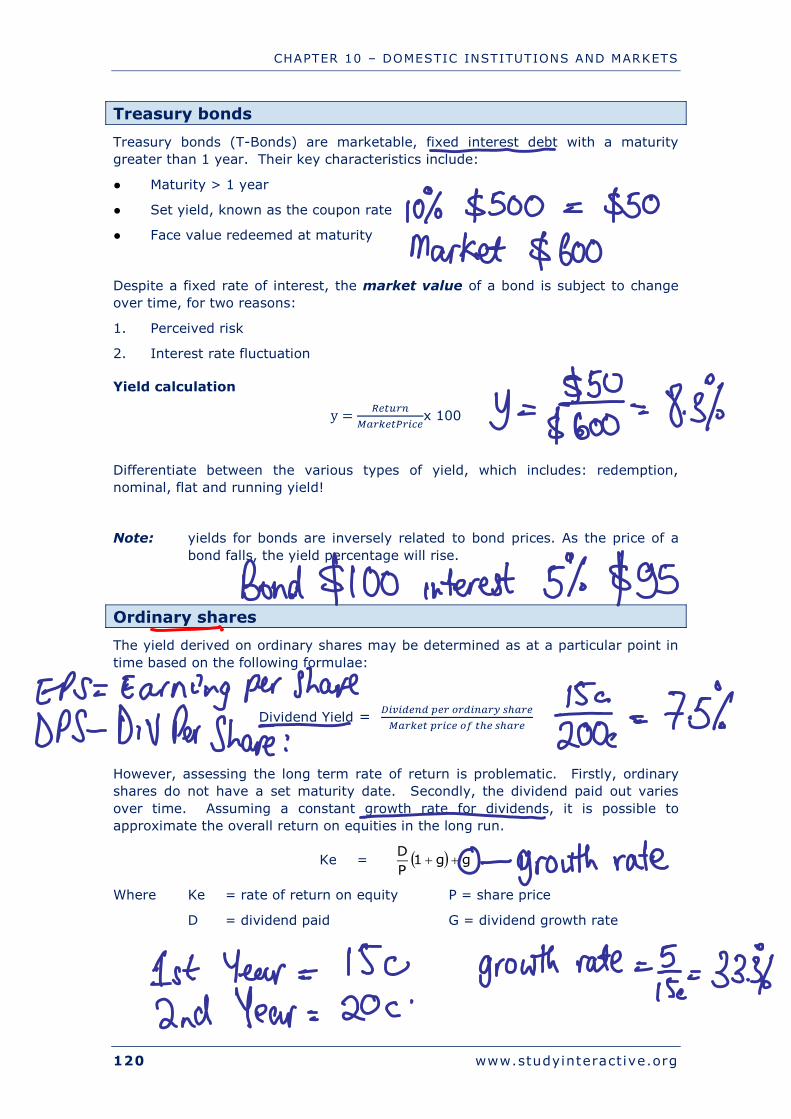

Treasury bonds

Treasury bonds (T-Bonds) are marketable, fixed interest debt with a maturity

greater than 1 year. Their key characteristics include:

Maturity > 1 year

Set yield, known as the coupon rate

Face value redeemed at maturity

Despite a fixed rate of interest, the market value of a bond is subject to change

over time, for two reasons:

1. Perceived risk

2. Interest rate fluctuation

Yield calculation

x 100

Differentiate between the various types of yield, which includes: redemption,

nominal, flat and running yield!

Note: yields for bonds are inversely related to bond prices. As the price of a

bond falls, the yield percentage will rise.

Ordinary shares

The yield derived on ordinary shares may be determined as at a particular point in

time based on the following formulae:

Dividend Yield =

However, assessing the long term rate of return is problematic. Firstly, ordinary

shares do not have a set maturity date. Secondly, the dividend paid out varies

over time. Assuming a constant growth rate for dividends, it is possible to

approximate the overall return on equities in the long run.

Ke =

Where Ke = rate of return on equity P = share price

D = dividend paid G = dividend growth rate

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

121 www.studyinteractive.org

Risk and return on financial instruments

The relative ordering of the above instruments relates to the degree of certainty surrounding the investors return.

Low risk High risk

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

122 www.studyinteractive.org

ROLE OF CENTRAL BANKS

A central bank is a bank which acts on behalf of the government. The central bank

for the UK is the Bank of England. The Bank of England is a nationalised

corporation.

Monetary stability

Lender of last resort

Holds forex

Adviser to govt

Banker to govt' &

commercial banks

Issuing new notes

Financial stability

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

123 www.studyinteractive.org

FINANCIAL MARKETS

Financial markets comprise:

1. Money markets which trade short term instruments.

2. Capital markets which trade in long term instruments such as bonds and

shares.

Money markets

Money markets are essentially short term debt markets, with loans being made for

a specified period at a specified rate of interest. The money market may be sub-

divided as follows:

Capital markets

Stock markets enable the trade in company equities. Significant markets include

the New York Stock Exchange and the London Stock Exchange.

A stock exchange is an organised capital market. Within a functioning economy,

stock exchanges:

Enable firms to raise long term capital.

Publicises the prices of quoted shares.

Enforces rules of conduct, providing investor confidence.

-

-

CHAPTER 10 DOMESTIC INSTITUTIONS AND MARKETS

124 www.studyinteractive.org

THE GLOBAL BANKING CRISIS

In many respects the global economy is still reeling from the effects of the 2007-

2010 financial crisis.

Causes of the 2007-2010 financial crisis

1. The US Property boom of 1997 2006

2. The sub-prime mortgage crisis

3. Low market interest rates

4. Poor regulation of the financial sector

5. Excessively complex financial assets

6. Greed and poor governance.

Consequences of the 2007 2010 financial crisis

1. Collapse of the property sector

2. Credit squeeze

3. Government intervention

4. More regulation of banks and financial institutions

5. Austerity budgets

6. Concern over structural deficits.