chapter 1 investments: background and issues copyright © 2010 by the mcgraw-hill companies, inc....

Post on 19-Dec-2015

218 views

TRANSCRIPT

Chapter 1

Investments: Background and

Issues

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

1.1 Real Versus Financial Assets

1-2

Real Versus Financial Assets

• Essential nature of investment• Reduce current consumption in hopes of greater

future consumption

• Real Assets• Used to produce goods and services: Property,

plant & equipment, human capital, etc.

• Financial Assets• Claims on real assets or claims on asset income

1-3

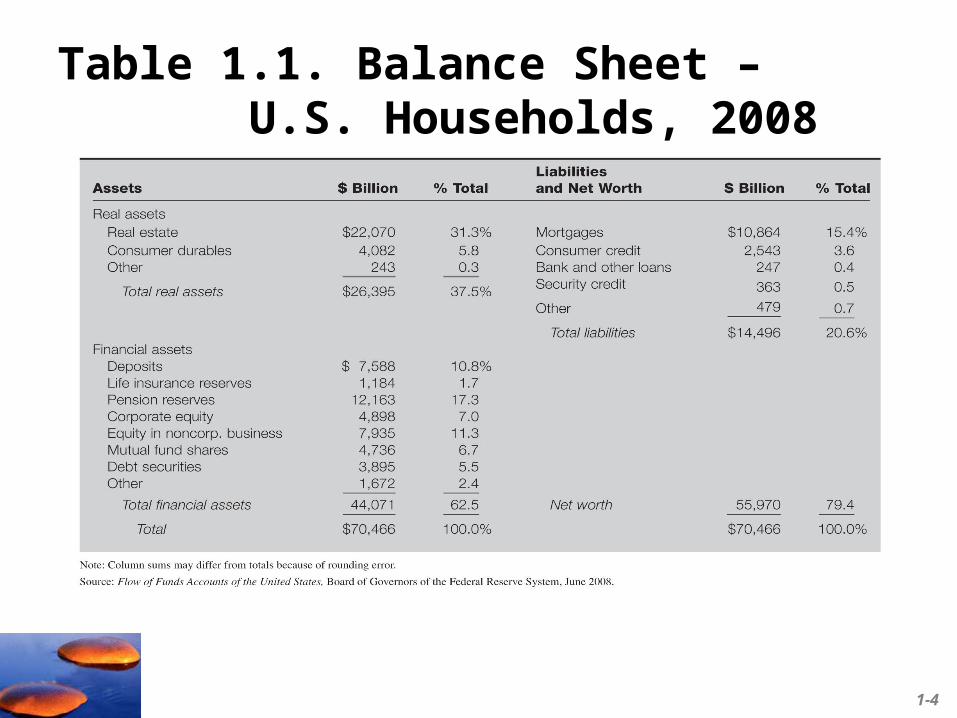

Table 1.1. Balance Sheet – U.S. Households, 2008

1-4

Real versus Financial Assets

• All financial assets (owner of the claim) are offset by a financial liability (issuer of the claim).

• When we aggregate over all balance sheets, only real assets remain.

• Hence the net wealth of an economy is the sum of its real assets.

1-5

Table 1.2 Domestic Net Worth, 2008

1-6

1.2 A Taxonomy of Financial Assets

1-7

Major Classes of Financial Assets or Securities

• Debto Money market instruments

• Bank certificates of deposit, T-bills, commercial paper, etc.

o Bondso Preferred stock

• Common stocko Ownership stake in the entity, residual cash flow

• Derivative securitieso A contract whose value is derived from some

underlying market condition.

1-8

1.3 Financial Markets and the Economy

1-9

Financial Markets

• Informational Role of Financial Marketso Do market prices equal the fair value estimate of a

security’s expected future risky cash flows?o Can we rely on markets to allocate capital to the

best uses?• What other mechanism could we use to

allocate capital? • What would be the advantages and

disadvantages of another system?

1-10

Consumption Timing

o People tend to smooth consumption over time.

o If one has more than enough cash to meet their basic needs in the current time period one might shift consumption through time by investing the surplus.

1-11

Allocation of Risk

o Investors can choose a desired risk level

• Bonds versus stock of a given company

• Bank CD versus company bond

• Tradeoff between risk and return?

1-12

Separation of Ownership and Management

• Large size of firms requires separation of ownership and managemento In 2008 GE had over $800 billion in assets and

over 650,000 stockholderso Owners (principals) ≠ Managers (agents)o Agency costs: Owners’ interests may not align

with managers’ interestso Mitigating factors:

• Performance based compensation• Boards of Directors may fire managers• Threat of takeovers

1-13

Example 1.1• In February 2008, Microsoft offered to buy Yahoo at $31

per share when Yahoo was trading at $19.18.

• Yahoo rejected the offer, holding out for $37 a share.

• Billionaire Carl Icahn led a proxy fight to seize control of Yahoo’s board and force the firm to accept Microsoft’s offer.

• He lost, and Yahoo stock fell from $29 to $21.• Did Yahoo managers act in the best interests of their

shareholders?

1-14

Corporate Governance and Corporate Ethics

• Business and market require trust to operate efficientlyo Without trust additional laws and regulations are

requiredo All laws and regulations are costly

• Governance and ethics failures have cost our economy billions if not trillions of dollars.o Eroding public support and confidence in market

based systems

1-15

Corporate Governance and Corporate Ethics

• Accounting Scandalso Enron, WorldCom, Rite-Aid, HealthSouth, Global

Crossing, Qwest, • Misleading Research Reports

o Citicorp, Merrill Lynch, others• Auditors: Watchdogs or Consultants?

o Arthur Andersen and Enron

1-16

Corporate Governance and Corporate Ethics

• Sarbanes-Oxley Acto Increases the number of independent directors on

company boardso Requires the CFO to personally verify the

financial statementso Created a new oversight board for the

accounting/audit industryo Charged the board with maintaining a culture of

high ethical standards

1-17

1.4 The Investment Process

Choosing the percentage of funds in asset classes

Choosing specific securities w/in an asset class

Stocks

Bonds

Alternative Assets

Money market securities

60%

30%

6%

4%

o Asset allocation

o The asset allocation decision is the primary determinant of a portfolio’s return

o Security selection & analysis

1-18

1.5 Markets Are Competitive

o Risk-return trade-off: o Assets with higher expected returns have higher risk.

A stock portfolio can be expected to lose money about 1 out of every 4 years.

o Bonds have a much lower average rate of return (under 6%) and have not lost more than 13% of their value in any one year.

Average Annual Return

Minimum (1931)

Maximum (1933)

Stocks About 12% -46% 55%

1-19

o How do we measure risk?

o How does diversification affect risk?

o Discussed in Part 2 of the text

Risk-Return Trade- Off

1-20

Efficient Markets

o Market efficiency: o Securities should be neither underpriced nor

overpriced on average

o Security prices should reflect all information available to investors

o Whether we believe markets are efficient affects our choice of appropriate investment management style.

1-21

Active vs. Passive Management

Active Management (inefficient markets)Finding undervalued securitiesTiming the market

Passive Management (efficient markets)No attempt to find undervalued securitiesNo attempt to timeHolding a diversified portfolio:

Security Selection

Asset Allocation

• Indexing• Constructing an

“efficient” portfolio

1-22

1.6 The Players

1-23

The Players• Business Firms – net borrowers• Households – net savers• Governments – can be both borrowers and

savers• Financial Intermediaries “Connectors of

borrowers and lenders”o Commercial Banks

• Traditional line of business: Make loans funded by deposits

o Investment companieso Insurance companieso Pension fundso Hedge funds

1-24

The Players Cont.

• Investment Bankerso Firms that specialize in primary market

transactions

o Primary market:• A market where newly issued securities are offered to

the public. • The investment banker typically ‘underwrites’ the issue.

o Secondary market• A market where pre-existing securities are traded among

investors.

1-25

Investment Bankers• Investment Bankers

o Commercial and investment banks’ functions and organizations were separated by law from 1933 to 1999.

o Post 1999 large investment banks, collectively known as “Wall Street,” operated independently from commercial banks, although many of the large commercial banks increased their investment banking activities, pressuring profit margins of investment banks.

o In September 2008 major investment banks either went bankrupt, reorganized as commercial banks or were purchased by commercial banks as a result of the collapse of the mortgage markets.

1-26

• Investment Bankerso Some investment banks chose to become

commercial banks to obtain deposit funding and government assistance

o All of the major investment banks are now under the much stricter commercial bank regulations.

• What are the implications for innovation and capital issuance resulting from these changes?

1-27

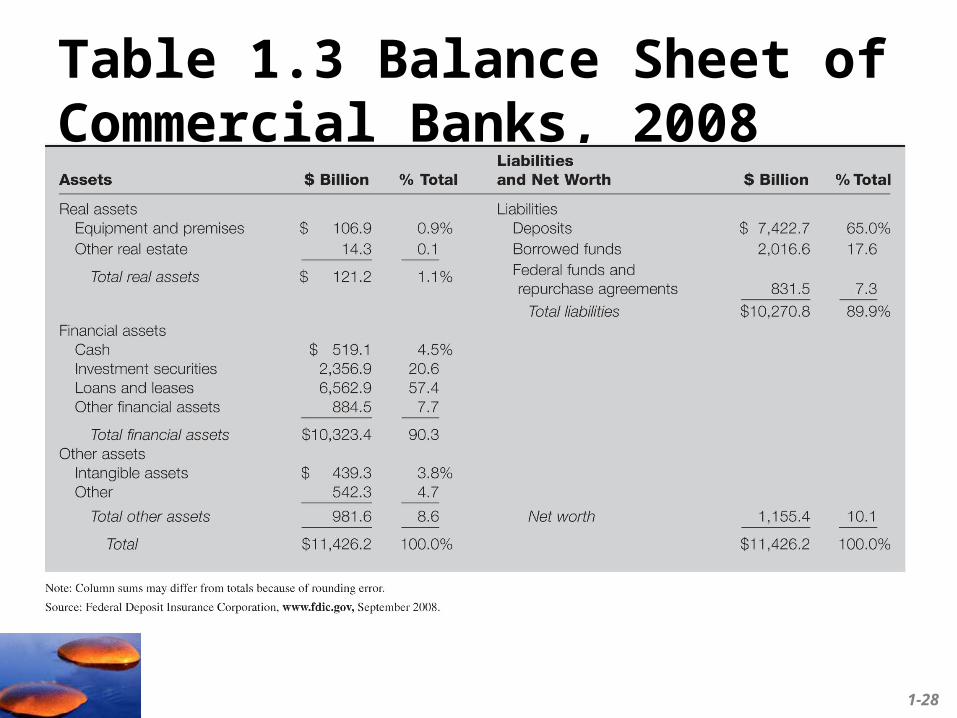

Table 1.3 Balance Sheet of Commercial Banks, 2008

1-28

Table 1.4 Balance Sheet of Nonfinancial U.S. Business, 2008

1-29

1.7 Recent Trends

• Globalization

• Securitization

• Financial Engineering

• Information and Computer Networks

1-30

Globalization • Domestic firms compete in global markets

• Performance in one country or region depends on other regions

• Opportunities for better returns & implications for risko Managing foreign exchangeo International diversification reduces risko Instruments and vehicles continue to develop

(ADRs and WEBs)o Information and analysis improves

1-31

Securitization• Loans of a given type such as mortgages are

placed into a ‘pool’ and new securities are issued that use the loan payments as collateral.

• The securities are marketable and are purchased by many institutions.

• “Shadow banking system”

• End result is more investment opportunities for purchasers, and spreading loan credit risk among more institutions

1-32

Securitization• Securitization has grown rapidly due to

• Changes in financial institutions and regulation permitting its growth, particularly lower capital requirements on securitized loans,

• Improvement in information capabilities,

• Credit enhancement provided by pool issuers has improved marketability.

1-33

Figure 1.1 Asset-backed Securities Outstanding

1-34

Financial Engineering• Repackaging cash flows of a security to enhance

marketability• Bundling and unbundling of cash flows

oBundling:

Combining more than one asset into a composite security, for example securities sold backed by a pool of mortgages.

oUnbundling

Selling separate claims to the cash flows of one security, for example a CMO

1-35

Figure 1.2 Building a Complex Security

1-36

Figure 1.3 Mortgage Security

1-37

Computer Networks

• Online low cost trading• Information made cheaply and widely available• Direct trading among investors via electronic

communication networks

• What have been the effects on Wall Street firms’ profit margins? o How has Wall Street responded?

1-38

The Future• Globalization will continue and investors will

have far more investment opportunities than in the past

• Securitization will continue to grow after the crisis

• Continued development of derivatives and exotics, more regulation for “over the counter” derivatives

• Strong fundamental foundation of understanding is critical

• Understanding corporate finance requires understanding investments

1-39

1.8 Text Outline

• Part One: Introduction to Financial Markets, Securities and Trading Methods

• Part Two: Modern Portfolio Theory• Part Three: Debt Securities• Part Four: Equity Security Analysis• Part Five: Derivative Markets• Part Six: Active Investment Management

Strategies: Performance Evaluation, Global investing, Taxes, and the Investment Process

1-40