chap. 1 the study of financial markets financial markets – a definition: –markets in which funds...

TRANSCRIPT

Chap. 1The Study of Financial Markets

• Financial Markets – A Definition:– Markets in which funds are transferred between

savers (investors) and borrowers– Funds are transferred from Surplus Units (Savers,

Investors) to Deficit Units (Borrowers)– Examples of Each:

• Surplus Units = Households and Investment Groups• Deficit Units = Financial, Non-Fin. Corps. and Individuals

– This promotes greater market efficiency (i.e. lowers transaction and search cost)

Chap. 1The Study of Financial Markets

• Debt Markets and Interest Rates– Financial Instruments (Securities)• A Claim on the Issuers Future Income and or

Assets• Financial claims are also called financial assets/

liabilities, securities, loans, and investments

– Assets• An Owned Financial Claim or Piece of Property• For every financial asset, there is an offsetting

financial liability

Chap. 1The Study of Financial Markets

• Debt Markets and Interest Rates– Bond Markets (Debt Markets)• Bond – A debt security promising to make

payments over a specified period of time

– The Rate of Interest• Interest Rate – The price or cost of borrowing

money expressed as a percentage

• Interest rates are determined in the Bond/Debt Markets

Chap. 1The Study of Financial Markets

• Interest Rates and Financial Institutions– Interest Rates directly effect the

performance of Financial Institutions– Example:• If a bank issues short term CD’s during a period

of rising interest rates what might happen to the bank’s cash flow assuming that assets are constant or declining?

– Int. Rates can differ b/w Time to Maturity

Chap. 1The Study of Financial Markets

• The Stock Market– Stock: A security representing a claim of

ownership in a corporations earnings and assets

– Primary Market• Initial Public Offering (IPO)• Seasoned Equity Offering (SEO)

– Secondary Market• NYSE, AMEX, NASDAQ

Chap. 1The Study of Financial Markets

• The Foreign Exchange Market– Allows funds from one country to be

transferred to another country– Implicit in this definition is the conversion of

one currency for another (i.e. Euros to Dollars)

• Foreign Exchange Rate– The price of one country’s currency relative to

another country’s (Can$ 1.5416 per 1 US)

Chap. 1The Study of Financial Markets

• The Foreign Exchange Market– Fluctuation in exchange rates between

currency’s lead to a variety of economic impacts

– Example:• When the US Dollar is strong (expensive) relative

to other currencies, American Consumers can buy abroad cheaper than they can domestically. However US firms may suffer as exports decline.

Chap. 1The Study of Financial Markets

• Financial Institutions– Central Banks• The government or quasi-government agency

tasked with managing monetary policy• In the US this agency is known as the Federal

Reserve System (or the Fed)

–Monetary Policy• Management of interest rates and the money

supply (M1, M2, M3, MZM)

Chap. 1The Study of Financial Markets

• Financial Institutions– Banks – An institution that accepts deposits

and makes loans– Types of Banking Institutions• Commercial Banks

• Savings and Loan Associations

• Mutual Savings Banks

• Credit Unions

Chap. 1The Study of Financial Markets

FINANCIAL ASSET HOLDINGS OF DEPOSIT-TYPE INTERMEDIARIES (1998)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CommercialBanks

ThriftInstitutions

Credit Unions

Pe

rce

nt

of

To

tal F

ina

nc

ial A

ss

ets

U.S. Governmentsecurities

Municipal bonds

Corporate and foreignbonds

Consumer loans

Business loans

Real estate loans

Other financial assets

FINANCIAL ASSET HOLDINGS OF DEPOSIT-TYPE INTERMEDIARIES (1998)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CommercialBanks

ThriftInstitutions

Credit Unions

Per

cen

t o

f T

ota

l F

inan

cial

Ass

ets

U.S. Governmentsecurities

Municipal bonds

Corporate and foreignbonds

Consumer loans

Business loans

Real estate loans

Other financial assets

Chap. 1The Study of Financial Markets

• Financial Institutions– Other Types of Financial Institutions• Investment Banks

• Mutual Funds

• Pension Funds

• Insurance Companies

• Finance Companies

• Government Agencies (HUD, Dept. Ag.)

Chap. 1The Study of Financial Markets

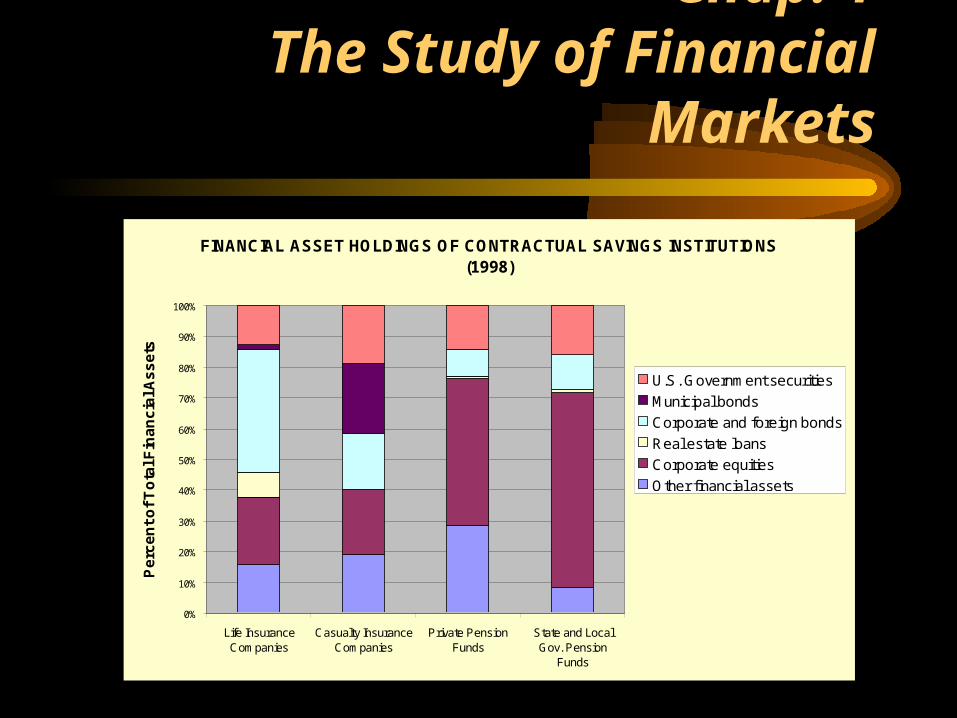

FINANCIAL ASSET HOLDINGS OF CONTRACTUAL SAVINGS INSTITUTIONS (1998)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Life InsuranceCompanies

Casualty InsuranceCompanies

Private PensionFunds

State and LocalGov. Pension

Funds

Pe

rce

nt

of

To

tal F

ina

nc

ial A

ss

ets

U.S. Government securities

Municipal bonds

Corporate and foreign bonds

Real estate loans

Corporate equities

Other financial assets

Chap. 1The Study of Financial Markets

FINANCIAL ASSET HOLDINGS OF INVESTMENT FUNDS (1998)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Money Market Mutual Funds Mutual Funds

Pe

rce

nt

of

To

tal F

ina

nc

ial A

ss

ets

U.S. Government securities

Municipal bonds

Corporate and foreign bonds

Corporate equities

Commercial Bank CDs

Commercial Paper

Other financial assets

Chap. 1The Study of Financial Markets

• Financial Intermediation– A financial "intermediary" writes a separate

contract with the Investor (bank depositor) and Borrower (auto loan)

– Financial intermediaries hold direct claims on Borrowers as financial assets and issue indirect financial claims to Investors as liabilities

Chap. 1The Study of Financial Markets

• Advantages of Financial Intermediation– Economies of scale from specialization– Transaction and search costs are lowered– Financial intermediaries may be able to

gather borrower information more effectively and discreetly

Chap. 1The Study of Financial Markets

• Services of Financial Intermediation– Denomination Divisibility - Issue varying

sized contracts of assets and liabilities– Currency Transformation - buying and

selling financial claims denominated in various currencies

– Maturity Flexibility - Offer contracts with varying maturities to suit both Borrowers and Investors

Chap. 1The Study of Financial Markets

• Services of Financial Intermediation– Credit Risk Diversification - Assume credit

risks of Borrowers and keep the risks manageable by spreading the risk over many varied types of Borrowers (loan portfolios)

– Liquidity - Provide a place to store liquidity for Investors (deposits); a place to find (borrow) liquidity for Borrowers

Chap. 1The Study of Financial Markets

0%

20%

40%

60%

80%

100%

1955 1965 1975 1985 1990 1995 1998

Pe

rce

nt

of

To

tal F

ina

nc

ial A

ss

ets

Finance Companies

Mutual Funds

Money Market Mutual Funds

State and Local Gov. PensionFunds

Private Pension Funds

Casualty InsuranceCompanies

Life Insurance Companies

Credit Unions

Thrift Institutions

Commercial Banks

Chap. 1The Study of Financial Markets

• Financial Innovation– The Advent of Electronic Banking/Investing• ATM’s• Smart Cards and Point of Sale Transactions• Telephone Banking• Web Bill Payment & Account Access• Electronic/Internet Securities Trading

– Can lead to higher profits for FI’s and lower costs for Investors and Borrowers

Chap. 1The Study of Financial Markets

Managing Risk in Financial Institutions• Types of Risk– Credit or default risk - the risk that a borrower will

not pay as agreed, thus affecting the rate of return on a loan or security

– Interest rate risk - the risk of fluctuations in a security's price or reinvestment income caused by changes in market interest rates

– Liquidity risk - the risk that a financial institution will be unable to generate sufficient cash flow to meet required cash outflows

Chap. 1The Study of Financial Markets

Managing Risk in Financial Institutions

• Types of Risk (Cont’d)– Foreign exchange risk -the risk that foreign

exchange rates will vary in the future affecting the profit of a financial institution

– Political risk - the cost or variation in returns caused by actions of governments or regulators

Chap. 1The Study of Financial Markets

• Managing Risk in Financial Institutions– Financial Instruments for Risk Management• Forwards

• Futures

• Options

• Swaps