changing professional opportunities for csr in india

TRANSCRIPT

CHANGING PROFESSIONAL OPPORTUNITIES FOR CSR IN

INDIABombay Chartered Accountants Society

6 February, 2019

ZFB & ASSOCIATES, Chartered Accountants

1

CONTENTS

• EVOLUTION OF CSR IN INDIA

• CHANGING PARADIGMS OF CSR IN INDIA

• BROAD PROFESSIONAL DIMENSIONS IN CSR

ZFB & ASSOCIATES, Chartered Accountants 2

EVOLUTION OF CSR IN INDIA

• PILLARS OF SOCIAL RESPONSIBILITY

• DIMENSIONS OF SOCIAL RESPONSIBILITY

• FACILITATORS OF CSR

• CONCEPT OF 4Ps

• PHASES OF CSR IN INDIA

ZFB & ASSOCIATES, Chartered Accountants 3

4

PILLARS OF SOCIAL RESPONSIBILITY

• The elements of social responsibility can betraced to what each person can do individuallyand collectively for the good of the society.

• Making small contributions by donating both incash and kind either directly or throughintermediaries generally in the form of trusts orNGOs, which would provide the basic foundationto sustained development of the society.

• These “donations / contributions” can take fourforms (see next slide)

ZFB & ASSOCIATES, Chartered Accountants

PILLARS OF SOCIAL RESPONSIBILITY

• Donate Time in the form of voluntary initiativesby individuals either solely or collectively toengage in formalized or unstructured initiativeson their own accord or through NGOs within theirown areas or for the wider benefit of the society.

• Donate in Kind – in the form of donations in kindby individuals on their own accord to otherindividuals based on the needs and wants orthrough NGOs who in turn could channelize thesame to the needy and deserving beneficiaries.

ZFB & ASSOCIATES, Chartered Accountants 5

PILLARS OF SOCIAL RESPONSIBILITY

• Donate Waste – in the form of collection and segregation of wasteespecially dry waste like papers, plastic, glass etc. and its recyclingby specialised agencies and the donation of the value generatedtherefrom in support of various initiatives. Similarly, items donatedby individual citizens like books, clothes etc. can be redistributed tothe needy. This form of donation also results in environmentalsustainability.

• Donate Wealth- most common form of donation whereinindividuals can either solely or collectively engage in donating theirwealth based on their ability and affordability in formalized orunstructured initiatives on their own accord or through NGOs.

• Social responsibility including Corporate Social Responsibility in whicheverform or scale ultimately revolves around these four pillars.

ZFB & ASSOCIATES, Chartered Accountants 6

DIMENSIONS OF SOCIAL RESPONIBILITY

• Personal Social Responsibility

• Professional Social Responsibility

ZFB & ASSOCIATES, Chartered Accountants 7

PERSONAL SOCIAL RESPONSIBILITY

• Primarily governed by the needs and circumstances of eachindividual or the organization with which he is associated.

• Based on family traditions.• People may wish to donate articles or organize to have food served

on particular days to certain organisations in memory of their deardeparted ones on their birth and death anniversaries.

• People who are associated with certain organisations, whethercommercial or social, may go with the flow in participating invarious types of social initiatives covering the four pillars describedearlier.

• It is primarily driven by individual motives which more often thannot are selfish in nature coupled with an element of bias and maynot always go toward deserving causes. Hence it is important thatwe exercise and element of discretion and judgement whilstundertaking and / or participating in social causes.

ZFB & ASSOCIATES, Chartered Accountants 8

PROFESSIONAL SOCIAL RESPONSIBILITY

• Primarily governed by the desire of an individual to give back to thesociety what he has learnt during the course of his professionalwork either during his active working life or subsequently, withoutexpecting any substantial rewards in return thereof.

• Accomplished through teaching, training, coaching and mentoringon an individual or collective basis by tying up with the relevantprofessional or social organisations on a full time or part time basisdepending upon ones other professional commitments.

• Can also manifest itself in ways whereby the professional whetherhe is a lawyer, doctor, chartered accountant etc. may provide freeor concessional services to the poorer and disadvantaged sectionsof the society whilst at the same time charging others at normalcommercial terms.

ZFB & ASSOCIATES, Chartered Accountants 9

PROFESSIONAL SOCIAL RESPONSIBILITY

• Increasing trend whereby senior level executives and professionalsare seeking early retirement from their existing jobs or otherprofessional commitments due to the high level of stress associatedwith such activities and taking up training and teaching withoutnecessarily reaping the desired commercial gains.

• Such activities may also be undertaken from a commercialperspective to reap handsome personal gains. Though there isnothing wrong per se in using our knowledge for commercialbenefit it is imperative that the professional seeks to balance thetwin objectives of commercial gain and social responsibility.

• Finally, the professional bodies itself may mandate that itsmembers contribute towards social causes either for its ownmembers or for other disadvantaged persons. (e.g. contribution tothe CA Benevolent Fund)

ZFB & ASSOCIATES, Chartered Accountants 10

FACILITATORS OF CSR

• Government

• Business

ZFB & ASSOCIATES, Chartered Accountants 11

GOVERNMENT

• Role of the Government is of paramount importance infacilitating the social fabric and laying down theguiding principles of social responsibility whilst framinglaws and regulations

• Part IV of the Constitution of India lays down theDirective Principles of State Policy which lay down thefundamental principles which need to be kept in mindwhilst framing laws.

• The main articles under Part IV of the Constitution ofIndia, which articulate social responsibility in variousforms are given in the next slide

ZFB & ASSOCIATES, Chartered Accountants 12

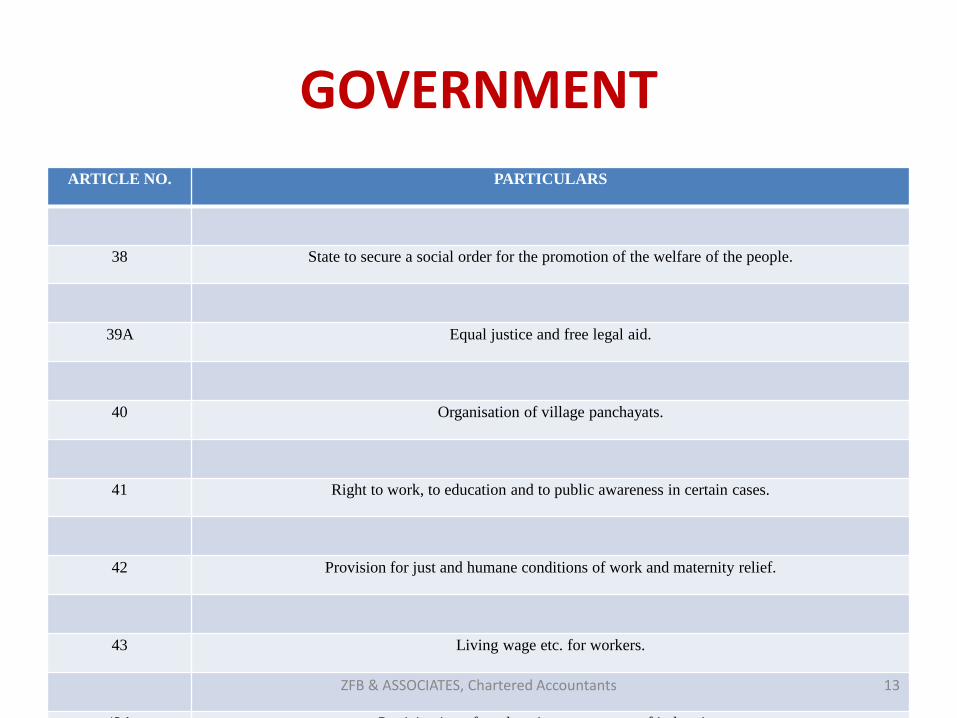

GOVERNMENT

ARTICLE NO. PARTICULARS

38 State to secure a social order for the promotion of the welfare of the people.

39A Equal justice and free legal aid.

40 Organisation of village panchayats.

41 Right to work, to education and to public awareness in certain cases.

42 Provision for just and humane conditions of work and maternity relief.

43 Living wage etc. for workers.

43A Participation of workers in management of industries.

ZFB & ASSOCIATES, Chartered Accountants 13

GOVERNMENT

ARTICLE NO. PARTICULARS

44 Uniform civil code for citizens.

45 Provision of free and compulsory education for children.

46 Promotion of education and economic interests of Scheduled Castes, Scheduled Tribes and other weaker

sections.

47 Duty of the State to raise the level of nutrition and standard of living and to improve public health.

48 Organisation of agriculture and animal husbandry.

48A Protection and improvement of environment and safeguarding of forest and wild life.

49 Promotion of monuments and places and objects of national importanceZFB & ASSOCIATES, Chartered Accountants 14

GOVERNMENT

The legislative and regulatory framework for CSRcan broadly be categorized under the followingbroad categories, under each of which there arevarious laws, regulatory prescriptions and otherpolicy initiatives:• Sustainability and Environmental Protection• Labour Welfare• Promoting Diversity and Protection of Women• Benefits to Marginalized Sections of Society• Transparency and Governance

ZFB & ASSOCIATES, Chartered Accountants 15

BUSINESS

• The most commonly understood objective of a business is to makeprofit which is also referred to as the “Bottom Line” which is turn iscalculated as revenue less expenses

• Over the years advocates of social justice as well asenvironmentalists have coined the term “Triple Bottom Line” togive the concept of bottom line or profit a much broaderconnotation.

• Apart from the traditional financial or accounting bottom line thereis also a social and environmental bottom line and all three of themtogether are also popularly referred to as 3P or more commonlyreferred to as “People, Profit and Planet” which in turn add up tobeing the three pillars for which a business exist and ultimatelylead to it playing a social and sustainable role

• A Fourth P viz. “Processes and Products” can also be added

ZFB & ASSOCIATES, Chartered Accountants 16

BUSINESS

• SEBI has mandated that the top 500 listed companiesby market capitalisation, are required to include aBusiness Responsibility Report (BRR) as part of theirAnnual Report

• BRR requires disclosure of the initiatives undertaken bythem in terms of nine principles laid down in theNational Voluntary Guidelines on Social,Environmental and Economic Responsibilities ofBusiness released by the Ministry of CorporateAffairs. (NVGs)

• These principles are modelled on the 3P approach(discussed later)

ZFB & ASSOCIATES, Chartered Accountants 17

BUSINESS

• Some of the key aspects which need to be taken care of anddisclosed in respect of these principles are as under:

1. Whether there are policies covering each of the principles?2. Whether the policies have been formulated in consultation with

the relevant stakeholders and conform to National / InternationalStandards?

3. Whether the policies have been approved by the Board ofDirectors and the periodical implementation thereof is overseenby the Board, a committee thereof or by a designated official andthere is a proper implementation structure for the same?

4. Whether there is a grievance redressal mechanism for the saidpolicies?

5. Whether an independent evaluation / audit has been undertakenin respect of the policies?

ZFB & ASSOCIATES, Chartered Accountants 18

CONCEPT OF 4 P

• People

• Planet

• Profit

• Processes and products

ZFB & ASSOCIATES, Chartered Accountants 19

PEOPLE

• The role of people in a business manifestsitself in three forms:

1. As an employer;

2. Towards business associates; and

3. To the broader community

ZFB & ASSOCIATES, Chartered Accountants 20

PEOPLE

As an employer:• Providing a means of sustained livelihoodTowards Business Associates (including the Government):• Fairness in business dealings• Good governance• Rewarding the shareholders through dividends• Paying taxes as a responsible corporate citizenTo the Broader Community:• Sponsorships• Welfare measures like health and educationThe impact of each of the above roles can not only be capturedthrough the expenditure incurred, taxes paid and dividendsdistributed but the reputation and brand image which it builds upover a period of time.

ZFB & ASSOCIATES, Chartered Accountants 21

PEOPLE

• The “people” aspect gets covered by the following principles of the NVGs:

1. Businesses should promote the wellbeing of all employees (Principle 3).

2. Businesses should respect the interests of and be responsive towards all stakeholders, especially those who are disadvantaged, vulnerable and marginalized (Principle 4).

3. Businesses should respect and promote human rights (Principle 5).4. Businesses when engaged in influencing public and regulatory

policy should do so in a responsible manner (Principle 7).5. Businesses should engage with and provide value to their

customers and consumers in an equitable manner (Principle 9).

ZFB & ASSOCIATES, Chartered Accountants 22

PLANET

• Manifests itself through environmental issues, which need ongoingattention and which need to be addressed, irrespective of thenature of its activities.

• All businesses must strive to minimize the ecological impact in all itsactivities from sourcing of materials, production processes,marketing and administration of its products and services.

• Some of these aspects like pollution control measures areenforceable by laws and regulations, other aspects like recycling ofproducts, supporting sourcing initiatives from disadvantagedsections of the society need to be adhered to on a proactive basisby the individual entities.

• It is imperative that all entities frame appropriate policies whichresult in the long term sustainability of the business from anecological and environmental perspective.

ZFB & ASSOCIATES, Chartered Accountants 23

PLANET

• The “planet” aspect gets covered by thefollowing principles of the NVGs:

1. Businesses should provide goods and servicesthat are safe and contribute to sustainabilitythrough their life cycle (Principle 2).

2. Businesses should respect, protect and makeefforts to restore the environment (Principle6)

ZFB & ASSOCIATES, Chartered Accountants 24

PROFIT

• It is not only the extent of profit earned which isimportant but the manner in which it is earnedi.e. the means are as important as the ends.

• Profits should be earned honestly, diligently andin conjunction and harmony with the two Psabove, else it would have dire consequences onits standing and reputation which if damagedonce takes a lot of time and effort to remediate.

ZFB & ASSOCIATES, Chartered Accountants 25

PROFIT

• The “profit” aspect gets covered by thefollowing principles of the NVGs:

1. Businesses should conduct and governthemselves with Ethics, Transparency andAccountability (Principle 1).

2. Businesses should support inclusive growthand equitable development (Principle 8)

ZFB & ASSOCIATES, Chartered Accountants 26

PRODUCTS AND PROCESSES

Manifests itself through the manufacturing ofproducts and undertaking processes which are:

• Environment friendly and sustainable

• Provide innovative services and solutionswhich ultimately lead to the overall societalgood

ZFB & ASSOCIATES, Chartered Accountants 27

EVOLUTION OF CSR IN INDIA

• FIRST PHASE

• SECOND PHASE

• THIRD PHASE

• FOURTH PHASE

ZFB & ASSOCIATES, Chartered Accountants 28

FIRST PHASE

• Charity and philanthropy the main drivers• Categorized into two sub-phases viz. the pre-industrialisation period till

1850 and the period of colonial rule subsequent thereto till theindependence movement in the early 20th century

• In the first sub-phase, wealthy merchants shared a part of their wealthwith the society at large by setting up temples and helping during faminesand epidemics by providing food from their godowns and other monetaryhelp

• In the second sub-phase, various industrial families like, Tata, Godrej, Birla,Bajaj, Modi and Singhania undertook various CSR initiatives like buildingtownships, setting up schools and hospitals and introducing various otherfacilities primarily for their employees and their families or for thecommunity near in the vicinity of their factories.

• Primarily driven by religious and caste motives coupled with the objectiveof employee welfare and were futuristic in nature.

• Some of the fforts were also driven by political motives.

ZFB & ASSOCIATES, Chartered Accountants 29

SECOND PHASE

• Coincided with the independence movement.• Main driving force during this phase was the concept

of trusteeship articulated by Mahatma Gandhi interms of which industry leaders had to manage theirwealth so as to benefit the common man.

• Thus many businesses established trusts for schoolsand colleges and also helped in establishing varioustraining and scientific institutions.

• Primary motives behind establishing these trusts wereabolition of untouchability, empowerment of womenand rural development which have continued toremain important till the current day.

ZFB & ASSOCIATES, Chartered Accountants 30

THIRD PHASE

• From 1960 to 1980• Characterised by the emergence of the Public Sector

Undertakings (PSUs) in the early years of independent Indiaas part of the “mixed economy” under the leadership ofJawaharlal Nehru followed by that of his daughter IndiraGandhi with the thrust being on a socialist welfare state

• Several legislations relating to labour and environmentalstandards as part of the agenda of sustainable developmentwere enacted.

• The private sector was forced to take a back seat and the PSUswere seen as the prime movers of development and to ensuresuitable and equitable distribution of resources like food,wealth etc. It was also referred to as the era of “commandand control”, primarily because of stringent industriallicencing, high taxes and malpractices.

ZFB & ASSOCIATES, Chartered Accountants 31

THIRD PHASE

• Nationalization of Life Insurance Corporation of Indiain 1956, followed by the nationalisation of around 20banks in 1969 and 1970 and the General InsuranceBusiness in 1972 with objective of providing insuranceand banking services to the poor and the need

• The private sector was also forced to abandon itstraditional engagement with CSR as a tool to mainlycomply with legislative requirements or serve tobenefit it employees or communities in thesurrounding areas of their operations and integrate itinto a sustainable business strategy

ZFB & ASSOCIATES, Chartered Accountants 32

FOURTH PHASE• Commenced in the 1980s continues till the present day.• It resulted in Indian companies both public and private abandoning their

traditional engagement with CSR and integrating it into a sustainablebusiness strategy.

• Starting from the 1990s a series of economic reform measures undertakenby the Government like doing away with licencing, partial divestment ofshareholding in PSU undertakings, permitting private sector banks andinsurance companies etc. have given a tremendous boost to economicactivity and facilitated the growth, competitiveness and globalization ofIndian companies.

• Various other path breaking initiatives like PPP model of development,financial inclusion, RTI, Make in India etc. which have been introduced inthe recent past and have made and would continue to facilitate inclusivegrowth and sustained development.

• The technological advances have also facilitated all round growth,development and prosperity to a wider spectrum of society

ZFB & ASSOCIATES, Chartered Accountants 33

FOURTH PHASE

• This phase continues to see various CSR initiatives bycorporate houses and PSUs in the form of donations andcharity events, sponsoring health, environmental andeducation initiatives, joining hands with NGOs to use theirexpertise in devising programmes which address wider socialproblems and setting up their own Trusts / Foundations toundertake CSR activities.

• Emphasis has shifted from mere cheque book philanthropyand employee engagement initiatives to wider communitybased initiatives which would result in maximization of thecorporates overall impact on the society and stakeholders.

• More and more corporates are framing CSR policies andprogrammes which are comprehensively integrated with theirbusiness operations and policies and managed and monitoredby specialized teams.

ZFB & ASSOCIATES, Chartered Accountants 34

CHANGING PARADIGMS OF CSR IN INDIA

• COMMERCIALISATION

• PROFESSIONALISM

• TRANSPARENCY

• EMPLOYEE ENGAGEMENT

• POLITICISATION

ZFB & ASSOCIATES, Chartered Accountants 35

COMMERCIALISATION

• Any new idea or concept which is mandated and thrust uponsociety drives its commercialisation, which is nothing but aformalised and systematic approach at launching the same.

• CSR which was hitherto largely seen as a voluntary concept is nowmandatory, which would require companies, through the CSRCommittee, to formalise various processes and formulate policieson various matters which are laid down in the Rules.

• The policies and procedures should cover various aspects like when,where, what and how to launch such activities within ethical andlegal boundaries and keeping in mind the overall socialresponsibilities which are expected to take care of the interest ofvarious stakeholders.

• These questions would need to be kept in mind by the CSRCommittee and the Management whilst framing the CSR policy

ZFB & ASSOCIATES, Chartered Accountants 36

COMMERCIALISATION

Certain specific aspects laid down in the CSR Rules which would need to bekept in mind whilst framing the CSR policies and procedures are as under:• The expenditure is required to be incurred only in respect of activities

which are prescribed. This would require companies which are alreadyundertaking CSR activities to reassess whether the same meet the criteriaof eligible CSR spend. Also, any activities undertaken in the normal courseof business though they may be in the nature of CSR activities need to beexcluded. CSR projects / programs / activities are required to beundertaken in India only.

• CSR projects / programs / activities benefitting only the employees of theCompany and their families will not be considered as CSR activities.

• Contribution of any amount directly or indirectly to any political party willnot be considered as CSR activity.

• The policy shall specify that any surplus arising out of the CSR projects orprograms or activities shall not form part of the business profit of theCompany.

ZFB & ASSOCIATES, Chartered Accountants 37

COMMERCIALISATION

• The CSR Rules provide that the CSR programmes /activities which are approved can beimplemented through either of the following:

1. A registered trust, or

2. A registered society, or

3. A company established by the company or itsholding or subsidiary or associate companywhether as a “not for profit” company orotherwise

ZFB & ASSOCIATES, Chartered Accountants 38

COMMERCIALISATION

• If any of the earlier referred entities is notestablished by the company or its holding orsubsidiary or associate company, it must have anestablished track record of 3 years in undertakingsimilar programs or projects.

• The company must also specify the projects orprograms to be undertaken through theseentities, the modalities of utilization of funds onsuch projects and programs and the monitoringand reporting mechanism.

ZFB & ASSOCIATES, Chartered Accountants 39

COMMERCIALISATION

• The Rules also provide that the companies may build CSR capacitiesof their own personnel as well as those of their implementingagencies through institutions with established track record of atleast three financial years.

• However, such expenditure is capped at 5% of total CSRexpenditure of the company in a particular financial year.

• Collaboration with other companies for undertaking CSR activities isalso permissible provided that the CSR Committees of respectivecompanies are in a position to report separately

• The provisions if implemented in the right spirit would lead to asignificant amount of funds getting channelized for the poorer anddisadvantaged sections resulting in sustainable and all-rounddevelopment.

ZFB & ASSOCIATES, Chartered Accountants 40

COMMERCIALISATION

• For companies which are already incurring expensestowards the benefit of their employees and families orin respect of other social causes which are notspecifically within the purview of CSR activitiesprescribed in the Rules would have to incur additionalexpenses which may lead to a reduction of thedistributable profits and consequentially lower returnsto the shareholders.

• It is imperative that companies engage in a dialoguewith the various stakeholders when formulating theCSR policy.

ZFB & ASSOCIATES, Chartered Accountants 41

PROFESSIONALISM

• Professionalism is inevitable when commercialisation creeps in andthe same is bound to happen also in the case of CSR.

• Many companies would take the help of various classes ofprofessionals in formulation of customised CSR strategies alignedwith the company’s core values as well as on various types ofactivities to be undertaken and the effective implementationthereof within the boundaries imposed by regulations so as not tofail on the legal front and be exposed to penalties.

• Opening of opportunities for professionals at the same timeincreasing the cost for companies in the form of fees.

• Would also creep in internally through setting up of specialiseddepartments by companies staffed by experienced professionalswith the desired competencies to enable companies to navigatethrough the CSR regulatory maze.

ZFB & ASSOCIATES, Chartered Accountants 42

TRANSPERANCY

• Commercialisation and professionalism maketransparency inevitable.

• The Act and the Rules contain various provisions /requirements which would bring about transparency,some of which are as follows:

1. Displaying the CSR policy duly approved by the Boardof Directors on the company’s web site.

2. Detailed disclosures in the Board Report regarding thepolicy developed and implemented by the Companyand the specific initiatives undertaken by theCompany on the CSR front.

ZFB & ASSOCIATES, Chartered Accountants 43

TRANSPERANCY

• SEBI through an amendment to the Listing Agreement, mandatedthe top 500 companies in terms of market capitalisation to includea Business Responsibility Report containing prescribed particularsdealing with various aspects of the company’s contribution towardsvarious sustainability initiatives which amongst others would alsoinclude its CSR initiatives, including the amount spent towards thesame.

• Could lead to some amount of duplication and informationoverload between the disclosures under the Act and the ListingAgreement for the large companies.

• Whilst greater transparency is always desirable, it could also havenegative connotations since competing recipients / donors ofservices could demand greater benefits for themselves therebyputting undue pressure on companies.

ZFB & ASSOCIATES, Chartered Accountants 44

EMPLOYEE BENEFITS

• Presently many companies equate CSR with providing benefitsto their employees and their families in the form of housing,education and medical benefit which are not considered asCSR activities in the revised guidelines.

• Companies would have to go much beyond their employeesto fulfill their CSR obligations.

• Any social service activities undertaken by the employees ofthe company not represented by actual spending by thecompany on the prescribed activities would not be consideredto fall within the purview of CSR.

ZFB & ASSOCIATES, Chartered Accountants 45

POLITICISATION

• Though donations to political parties and politicalcontributions are not covered as eligible CSR spend,the CSR mandate could lead to certain forms of indirectcontributions to political parties under whichcompanies could be forced to incur CSR spend throughorganisations which have some form of politicalpatronage or in areas of specific interest to the localpolitical parties.

• Contribution to the Prime Ministers’ National Relieftogether with contributions to the Swach Bharat Koshand Clean Ganga fund as permissible avenues for CSRspend would lend political overtones.

ZFB & ASSOCIATES, Chartered Accountants 46

BROAD PROFESSIONAL DIMENSIONS IN CSR

• Internal Restructuring and Reorganization,

• Job Opportunities.

• Involvement of Specialized External Agencies.

• Training and Education.

ZFB & ASSOCIATES, Chartered Accountants 47

INTERNAL RESTRUCTURING AND REORGANISATION

• Role of Board of Directors

• Role of Finance, Accounting and CommercialPersonnel

• Role of Company Secretary, Legal andCompliance Personnel (collectively referredto as Compliance Personnel)

ZFB & ASSOCIATES, Chartered Accountants 48

ROLE OF THE BOARD OF DIRECTORS

• Collective Role

• Role of Managing / Executive Directors

• Role of Independent Directors

ZFB & ASSOCIATES, Chartered Accountants 49

COLLECTIVE ROLE OF THE BOARD OF DIRECTORS

• Setting the Tone at the Top

• Operational Roles and Responsibilities

• Risk Assessment

ZFB & ASSOCIATES, Chartered Accountants 50

TONE AT THE TOP

• Without a proper tone at the top, there could arise a number ofCSR related issues that can result in disruptions, loss of brand value,law suits and other commercial challenges especially if the CSRteam works in a silo.

• By establishing a tone at the top, the Board ensures that thecompany operates consistently with its commitments to and theexpectations of the key stakeholders and ensure that the social andenvironmental impacts of its CSR activities are responsiblyaddressed.

• The Board must ensure that CSR should be related to theCompany’s core values and not be just seen as a compliance withthe regulations to spend the prescribed amounts towardsprescribed purposes.

• The compliance should be in spirit rather than in letter.

ZFB & ASSOCIATES, Chartered Accountants 51

OPERATIONAL ROLES AND RESPONSIBILITIES

• Formation and Composition of the CSRCommittee

• Formulating the CSR Policy

• Formulating the CSR Strategy

• Identifying the CSR Projects and ImplementationRoad Map thereon

• Monitoring Performance and ImpactAssessment

• Reporting Framework

ZFB & ASSOCIATES, Chartered Accountants 52

CSR COMMITTEE

• Ensuring that the members are selected carefully in thefirst instance.

• Ensuring that there is a proper mix of independent andnon-independent directors. Whilst the regulationsrequire only one independent director it would be agood practice to have a majority of independentdirectors.

• Ensuring that any director does not have a conflict ofinterest whilst discharging their CSR role e.g. being atrustee or governing Board member of any NGO/ NPOwhich is an implementation agency or provides otherexternal services in connection with the CSR activities.

ZFB & ASSOCIATES, Chartered Accountants 53

CSR COMMITTEE

• Evaluating the composition of the committeeagainst a maturity model (foundational,developed, advanced & strategic).

• In case of corporates having large CSR budgets itwould be worthwhile to rope in specialists havingthe requisite skills and expertise either asadvisors or also as full time Board members.

• Ensuring that a proper written charter is framedwhich is in sync with the overall Board Charter.

• Laying a down a protocol for accountability of theCommittee to the Board

ZFB & ASSOCIATES, Chartered Accountants 54

CSR COMMITTEE

• Composition of the Committee

• Terms of Reference

ZFB & ASSOCIATES, Chartered Accountants 55

COMPOSITION OF THE COMMITTEE

• There is no maximum limit specified on the number of directors. Further, only oneindependent director is mandatorily required to appointed. This could leave theCompany at the mercy of the promoters and other controlling shareholdersthereby possibly compromising on the objectivity and independence of the CSRactivities and keep it open to abuse, especially where the company is listed orthere is public interest involved. As a result quite a lot of companies, atleast in theinitial years of CSR implementation will be at the mercy of the promoters andcontrolling shareholders. It is hoped that suitable amendments over a period oftime are made to ensure that majority of independent directors, atleast on thesame lines as is required for the Audit Committee, wherever constituted, areinducted to bring in greater rigour and formality in the process with the ultimateaim of benefiting all concerned

• On the matter of whether KMPs should mandatorily be a part of the Committee,the answer is no, since as per Section 135(1), it is basically a Committee ofDirectors. However, there is nothing wrong if or more KMPs are members of thecommittee. Further, to ensure the independence of the Committee, KMPs shouldnot have any voting rights. The regulators may lay down appropriate guidelines indue course.

ZFB & ASSOCIATES, Chartered Accountants 56

COMPOSITION OF THE COMMITTEE

• The provisions are equally applicable to all kinds of companies, whether public or private, listed orunlisted, whether public interest is involved or not etc. Whilst there is no doubting that CSRobligations are not a function of the type or nature or structure of the company, constituting acommittee and the attendant compliance and record keeping obligations may not always be costeffective and may prove burdensome especially for private limited companies with no publicinterest involved. For such entities the Board itself may be entrusted with ensuring compliance withthe various requirements.

• In the context of the requirements of including in the Articles of Association the socialresponsibilities of corporates as envisaged by Mr. J.R.D.Tata, it would be a good practice forcorporates to include the various aspects of their CSR obligations in the Articles of Association,especially those dealing with the constitution of the Committee, its composition, minimum andmore particularly the maximum number of directors. This would impart greater clarity andtransparency about the role of the committee for the various stakeholders, especially consideringthe fact that any amendments / insertions in the Articles of Association require the shareholders’consent in the General Meeting under the Act. The Government may also consider amendingSchedule I of the Act by suggesting model clauses to be included in the Articles of Association.

ZFB & ASSOCIATES, Chartered Accountants 57

COMPOSITION OF THE COMMITTEE

• Foreign companies, including those which may not necessarily havea physical presence, meeting the thresholds are also required tocomply with the requirements. This may present various challengesin effective compliance with the requirements outlined above.

• There is currently no requirement of holding a certain minimumnumber of meetings during a calendar or financial year which isspecified in the Act. However, though not explicitly specified, itappears that Committee is required to meet atleast once a year inview of Section 135(3)(c) of the Act which requires monitoring ofthe CSR Policy from time to time. even if it does not have tomandatorily spend, so as to ensure effective monitoring andgovernance. Further guidelines could be laid down for holding aminimum of two meetings during the calendar / financial yearwhere there are spending obligations. Necessary amendments /clarifications could be considered in this regard.

ZFB & ASSOCIATES, Chartered Accountants 58

TERMS OF REFERENCE

• To formulate and recommend to the Board theCSR Policy which shall indicate the activities to beundertaken by the Company as specified inSchedule VII of the Act.

• To recommend the amount of expenditure to beincurred on the above activities. Thus it is clearthat a Company cannot incur any CSR expenditurewithout the concurrence of the Committee

• To monitor the CSR Policy periodically.

ZFB & ASSOCIATES, Chartered Accountants 59

CSR POLICY

• Ensuring that the policy is in line with the core businessobjectives of the Company.

• The policy should be in line with core competencies so as toensure that the implementation is efficient and effectiveand derives maximum benefits for the Company.

• The policy should be in line with the expectations of thevarious stakeholders.

• Whilst there are various regulatory requirements whichhave been specified, it would be a good practice to gobeyond the legal requirements.

• The policy should enhance the brand and reputation of theCompany.

ZFB & ASSOCIATES, Chartered Accountants 60

CSR STRATEGY

• Ensuring that the CSR strategy is in line withthe vision / mission statement of theCompany.

• Aligning the CSR strategy with therequirements laid down under the Act and theRules as discussed earlier.

ZFB & ASSOCIATES, Chartered Accountants 61

POLICY AND STRATEGIC FRAMEWORK

• List of the CSR projects / programmes planned to be undertaken during aparticular implementation period / year, the areas chosen, withpreference being given to the local areas around which the Companyoperates.

• The implementation schedules for the same.• The CSR activities should not include activities undertaken in pursuance

of the normal course of business even if they relate to areas specified inSchedule VII.

• Expenditure on CSR activities undertaken outside India are notpermissible even if the Company has branches located outside India.

• Expenditure incurred exclusively for the benefit of the employees and theirfamilies is also not permissible. This aspect is analysed in a subsequentchapter.

• Contribution of any amount directly or indirectly to any political partyunder Section 182 of the Act, is also not permissible.

ZFB & ASSOCIATES, Chartered Accountants 62

POLICY AND STRATEGIC FRAMEWORK

• Pooling and collaboration with other companies, both within and outsidethe group is permitted, provided the individual companies are in aposition to report separately on such projects and programmes.

• Considering that CSR demands specialised expertise, companies arepermitted to “outsource” their CSR activities to NGOs in the form oftrusts or societies having an established track record or to Non ProfitOrganisations registered under Section 8 of the Companies Act, 2013 orSection 25 of the Companies Act, 1956.

• Companies may undertake capacity building of their own personnel aswell as those of the implementing agencies discussed above, to whomthey have outsourced their CSR obligations, subject to such expenditurenot exceeding 5% of the total CSR expenditure in a financial year.

• The monitoring process for the above programmes or projects.• Any surplus arising out of the CSR activities cannot form part of the

business profits of the Company.

ZFB & ASSOCIATES, Chartered Accountants 63

INDENTIFYING PROJECTS AND LAYING IMPLEMENTATION ROADMAP

• Identifying the CSR projects in line with the CSR policy and strategy.• Ensuring that the CSR projects are in areas specified under the Act

and Rules.• Laying down the modalities whereby certain projects can be

undertaken under extraneous circumstances which are not in linewith the policy and strategy adopted earlier.

• Laying down the timelines for undertaking the various CSRprogrammes / activities.

• Laying down the criteria / guidelines for identifying the projectimplementation partners.

• Laying down the broad guidelines / methods for implementation ofthe CSR projects or activities which are long term in nature.

ZFB & ASSOCIATES, Chartered Accountants 64

INDENTIFYING PROJECTS

• Location of Projects:a) Undertake a gap assessment in and around the areas where the offices and

plants are located to determine the extent and proportion of projects therein.b) In respect of projects in other areas whether and to what extent it should cover

urban, backward and tribal areas, based on a gap assessment.• Number of Projects:a) Funds available.b) The maximum permissible allocation for each project keeping in mind the funds

available.c) The geographical spread.d) The number of agencies which may be employed.e) The expectations of the stakeholders including the Government.f) The extent / proportion of contingency funds which need to be kept aside for

meeting requirements arising out of unforeseen contingencies like naturaldisasters.

ZFB & ASSOCIATES, Chartered Accountants 65

INDENTIFYING PROJECTS

• Selection of Projects:a) The intended beneficiaries based on ground

level gap assessments.b) The viability / feasibility of the projects.c) The technical competency of the company,

collaborating parties and implementingagencies.

d) The nature, level and extent of involvement,whether one time, recurring and operational.

e) The nature of capacity building required.

ZFB & ASSOCIATES, Chartered Accountants 66

IMPLEMENTING PROJECTS

• On its own, coupled with capacity building initiatives (in house trainingor training for implementation agencies)

• Through specialised implementation agencies, both within the group andoutside to be selected based on the following criteria:

a) Evaluating the legal / registration status of the entity and verifying thesame with the necessary documents.

b) Evaluating the track record / execution capabilities including theexperience in terms of number of years, and cross verifying the samewith publicly available information and reference checks.

c) Evaluating the financial soundness based on the audited accounts forpast periods.

ZFB & ASSOCIATES, Chartered Accountants 67

IMPLEMENTING PROJECTS

d) Evaluating the technical and managerial expertise of thepersonnel involved and if required the nature and extentof capacity building initiatives required as discussedsubsequently.

e) Entering into a proper MOU / other document to clarifythe roles and responsibilities including but not limited toproject selection criteria, disbursement of funds,obtaining of duly audited / authenticated information on aregular basis about utilisation of funds and measuring andmonitoring the impact of the various activities andprojects.

• Through pooling and collaboration with other entities andimplementation agencies.

ZFB & ASSOCIATES, Chartered Accountants 68

MONITORING AND IMPACT ASSESSMENT

• Laying down the broad criteria against which theprojects need to be monitored keeping in mindtheir nature, duration and the cost – benefitanalysis which is likely to be derived.

• Developing an impact assessment frameworkkeeping in mind their nature, duration and thecost – benefit analysis which is likely to bederived.

• Identifying whether and in what circumstancesany external help would be required forconducting an impact assessment.

ZFB & ASSOCIATES, Chartered Accountants 69

MONITORING

• Compliance with the conditions of the Sanction Letter /MOU

• Certificate of utilisation of previously released funds, if any• Physical progress verified through photographs, site visits,

contractors bills etc.• Any other relevant documents / evidence.• Internal Monitoring through a Tabular Milestone Grid

(discussed in the next slide)• External Monitoring through:a) Accounting and Auditing Firmsb) Engineering and Technical Firmsc) Sustainability Service Firms

ZFB & ASSOCIATES, Chartered Accountants 70

TABULAR MILESTONE GRID

Nature of the Project (e.g prevention of blindness)• Expected Impact (e.g. improvement in the overall

life of the community)• Agreed Outcomes (e.g. Enhanced Income

generation)• Agreed Output (e.g. Increase in the monthly

income from 5 to 25%)• Baseline, Mid-line and End-line Indicators

(involves comparison of actual targets of increasein income against the estimated targets over aperiod ranging from 1 to 5 years.

ZFB & ASSOCIATES, Chartered Accountants 71

IMPACT ASSESSMENT

• Environmental

• Social

• Life cycle

ZFB & ASSOCIATES, Chartered Accountants 72

REPORTING FRAMEWORK

• Ensuring that the reporting requirements arein line with the various statutory andregulatory frameworks as applicable to thecompany.

• Ensuring the reporting is in line with thestakeholder’s perceptions and expectations.

• Ensuring that only information which isrelevant and credible is reported with utmosttransparency and avoid an over kill of data.

ZFB & ASSOCIATES, Chartered Accountants 73

RISK ASSESSMENT

• Risks from the Stakeholders perspective

• Business Risks

ZFB & ASSOCIATES, Chartered Accountants 74

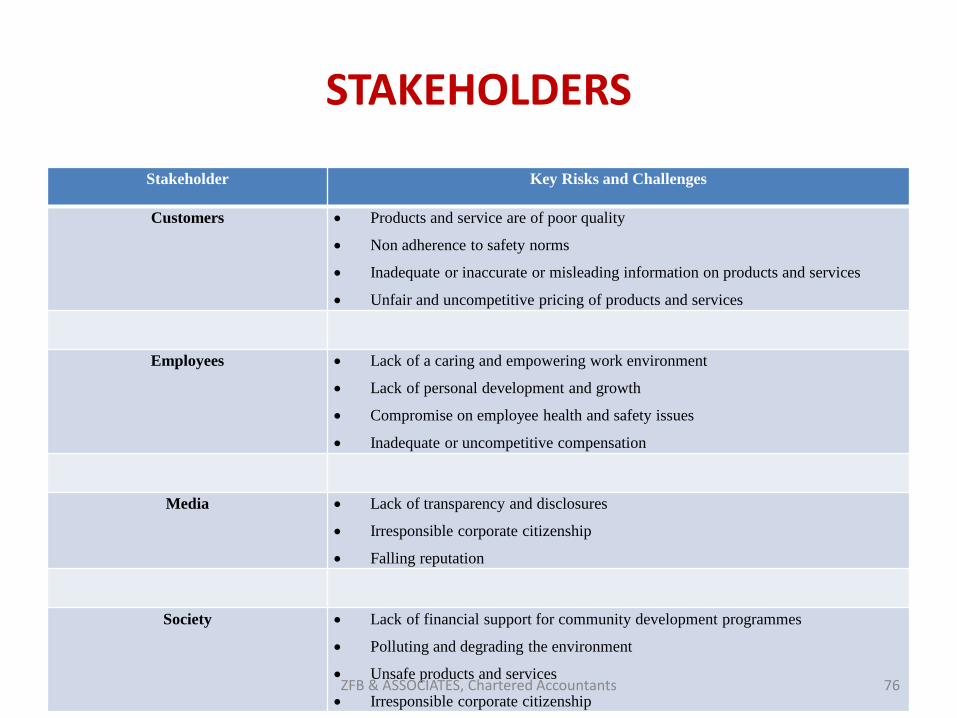

STAKEHOLDERS

Stakeholder Key Risks and Challenges

Providers of Financial Capital Lack of transparent and effective communication

Poor or inadequate investor servicing

Financial performance not being as per expectations

Inadequate Corporate Governance mechanisms

Government and Regulatory

Authorities

Non- compliance with statutory, regulatory and legal requirements

Lack of transparency in disclosures

Customers Products and service are of poor quality

Non adherence to safety norms

Inadequate or inaccurate or misleading information on products and services

Unfair and uncompetitive pricing of products and services

ZFB & ASSOCIATES, Chartered Accountants 75

STAKEHOLDERS

Stakeholder Key Risks and Challenges

Customers Products and service are of poor quality

Non adherence to safety norms

Inadequate or inaccurate or misleading information on products and services

Unfair and uncompetitive pricing of products and services

Employees Lack of a caring and empowering work environment

Lack of personal development and growth

Compromise on employee health and safety issues

Inadequate or uncompetitive compensation

Media Lack of transparency and disclosures

Irresponsible corporate citizenship

Falling reputation

Society Lack of financial support for community development programmes

Polluting and degrading the environment

Unsafe products and services

Irresponsible corporate citizenshipZFB & ASSOCIATES, Chartered Accountants 76

SPECIFIC BUSINESS RISKS

• Managers, promoters and shareholders can engage in theirpersonal interests in the garb of CSR thereby squandering theprofits which belong to the shareholders or which could be used forthe overall betterment of the external stakeholders.

• Political interference can hamper genuine CSR efforts bycorporates.

• The lack of professionalism and awareness on the part of NGOs andimplementing agencies would lead to misappropriation and misuseof funds allocated for CSR purposes.

• Inadequate capacity building measures could expose the companydue to lack of awareness in monitoring the implementation of andassessing the impact of the CSR activities

• Possibility of Class Action Suits – Section 245 of the CompaniesAct, 2013

ZFB & ASSOCIATES, Chartered Accountants 77

ROLE OF MANAGING / EXECUTIVE DIRECTORS

• In case where companies are required to mandatorily appoint a Managing orExecutive Director, it would invariably lead the Board to delegate all authority tomanage CSR within the levels of authority specified by the Board from time totime.

• Accordingly, the Managing or Executive Director would be required to reportregularly to the Board on the progress being made with regard to the CSR activitiesin addition to the other business functions.

• The nature and level of reporting would vary on a case to case basis dependingupon the size of the entity and the nature and level of CSR interventions.

• Further, in many cases it is observed that the Managing or Executive Director isalso a member of the CSR Committee. In such cases it is important for them towear two hats and ensure that there is no conflict of interest between both theroles whilst at the same time striking a right balance between the two roles.

• Finally, in cases where a company has more than one Managing / ExecutiveDirector, the Board should clearly identify the director who is responsible for theCSR activities.

ZFB & ASSOCIATES, Chartered Accountants 78

ROLE OF INDEPENDENT DIRECTORS

• Collective Role

• Individual Role

ZFB & ASSOCIATES, Chartered Accountants 79

COLLECTIVE ROLE

• Ensure independence and avoid conflicts of interest which can arise fromseveral angles as under:

a) Employed in a CSR role whether as an employee, auditor or consultant inany subsidiaries or group companies. This could become relevant in thecontext of the foundations which are established by companies.

b) Directly involved in the provision of advice or consulting services relatingto CSR activities where the amount paid during the year for that adviceor services exceed 5% of the total fees earned by that firm.

c) Directly involved with a supplier to the Company which provides CSRrelated services which exceed 5% of the revenue of that Company.

• The Board could consider laying down appropriate criteria to ascertaincircumstances whereby in their opinion there could arise a situation ofconflict of interest.

• It would also not be a bad idea for the regulators to lay down appropriateguidelines in the future.

ZFB & ASSOCIATES, Chartered Accountants 80

INDIVIDUAL ROLE

• As members of the CSR committee there wouldnormally be a challenge since in most of the cases, theindependent directors are in a minority and hence it ispossible that many of the decisions involving CSRmatters may be taken keeping the promoters /controlling shareholders interests in mind.

• Hence it would be appropriate for the regulators to laydown that in case of public companies having CSRspending limits beyond a particular threshold to have amajority of independent directors on the CSRcommittee. This will ensure objectivity and fair play inthe CSR activities which are undertaken by the Compa

ZFB & ASSOCIATES, Chartered Accountants 81

INDIVIDUAL ROLE

• Atleast one of the independent directors should haveexpertise and experience in social service activities or isconnected with social organisations. However since in theinitial years of the regulatory change, this could lead topractical challenges, the alternative could be to have as amember of the committee in an advisory capacity, a personwho has the relevant expertise and experience in socialservice activities or is connected with social organisations.

• It would be a good practice for companies to encouragetheir independent directors to attend seminars andundergo appropriate training programmes which could beconducted by specialised agencies including Chambers ofCommerce and Industry or stock exchanges specificallytargeted towards independent directors.

ZFB & ASSOCIATES, Chartered Accountants 82

ROLE OF FINANCE, ACCOUNTING AND COMMERCIAL PERSONNEL

• Operationalising the entire gamut of the CSR institutionalmechanism like nature / legal structure of the implementingagencies, finance, accounting, HR and IT systems etc. required tosupport the CSR activities.

• Assessing the funds available for CSR based on the regulatoryrequirements.

• Allocating the funds for various activities and projects.• Conducting a due diligence of the implementation partners.• Developing the project parameters.• Approving the project for funding and finalizing the arrangement

with the implementing agency.• Monitoring the progress of the project.• Impact assessment.

ZFB & ASSOCIATES, Chartered Accountants 83

ROLE OF COMPLIANCE PERSONNEL

• Applicability

• CSR Committee

• Activities / Projects

• Documentation

• Reporting

ZFB & ASSOCIATES, Chartered Accountants 84

APPLICABILITY

• Determining whether the correct parameters liketurnover, net worth and net profit are identifiedand appropriately calculated since that woulddetermine the total funds available for CSRactivities on an annual basis.

• Proper inclusions and exclusions whilstcalculating the relevant parameters are properlyidentified.

• Co-ordination with finance and accountingpersonnel to ensure that the financialinformation is updated on an ongoing basis.

ZFB & ASSOCIATES, Chartered Accountants 85

CSR COMMITTEE

• Ensuring that the committee is formed once any of the applicability triggers ofturnover, net worth or net profit are applicable even though there is no net profitand consequently spending on CSR is not required.

• The proper constitution of the committee should be ensured based on the class /type of company by ensuring that at least one independent director is appointedwhere the company is required to appoint them.

• To consider the qualifications and experience of the members of the committeeand recommend to the Board or Senior Management the need to invite advisors /outside experts to join the committee depending upon the nature and magnitudeof the CSR requirements and the resources and capabilities which are available.

• The terms of reference to be properly documented by means of a Charter or otherappropriate manner and cover at a bare minimum the specific matters laid downin the Act and other procedural aspects like passing of resolutions, maintainingminutes etc. specified generally in the Act.

• Currently, the Act is silent regarding the number of meetings of the committeewhich are required to be held. However, the Secretarial Standards issued by theICSI provide that the Committees should meet as often as is necessary.Accordingly, it is imperative for the Company Secretary / Compliance Officer toadvise the Board and the Senior Management appropriately.

ZFB & ASSOCIATES, Chartered Accountants 86

CSR COMMITTEE

• The Act is also silent in respect to the quorum for the CSRcommittee meetings. In this context it is interesting to note that theSecretarial Standard on Board Meetings issued by the ICSI providesfor the presence of all members of any committee constituted by theBoard to form the quorum unless otherwise stipulated by the Act orany other law or the Articles or by the Board. Accordingly it isimportant that the Company Secretary / Compliance Officerensures that the necessary quorum is laid down by the Board or inthe Articles.

• Finally, the Company Secretary / Compliance Officer should ensurethat all the decisions of the Board and the Committee areappropriately minuted and the necessary resolutions are passed byrequisite majority including, where necessary, by circulation

ZFB & ASSOCIATES, Chartered Accountants 87

ACTIVITIES / PROJECTS

• Advise the Board and the Committee and consequentiallyensure that the CSR activities are undertaken only inrespect of areas specified in the Act.

• Ensuring that they should be undertaken in programme /project mode which implies that they should be recurring innature and not one off events even if the same are inrespect of areas specified in the Act.

• In case of any disputes / differences of opinion eitherinternally or with external agencies the legal team shouldprovide a proper and articulated opinion considering thefacts and circumstances without any bias or subjectivity.

ZFB & ASSOCIATES, Chartered Accountants 88

DOCUMENTATION

• Preparing and reviewing the documentationinvolved at various stages starting from the CSRCommittee Charter / Terms of Reference, CSRPolicy, Agreements / MOUs with theimplementing and monitoring agencies,preparation of budgets etc.

• Ensuring that the respective departments havecomplied with the statutory provisions and alsokept the interests of the Company and allstakeholders in mind.

ZFB & ASSOCIATES, Chartered Accountants 89

REPORTING

• Ensuring that the various departmentscompile the requisite data for disclosure in theAnnual Report and the Web Site in a timelyand precise manner and in accordance withthe prescribed statutory requirements

• Presenting the same to the Committee andthe Board for approval before publishing anddisseminating the same.

ZFB & ASSOCIATES, Chartered Accountants 90

JOB OPPORTUNITIES

• CHIEF CSR / SUSTAINABILITY OFFICER

• PROGRAMME MANAGER

• CSR FUND RAISING MANAGER

• CSR COMMUNICATION MANAGER

ZFB & ASSOCIATES, Chartered Accountants 91

CHIEF CSR / SUSTAINABILITY OFFICER

• Could be in the rank of a Director / President / Vice President• The role would encompass both the CSR responsibilities arising out

of the changing regulatory landscape, as well as the sustainability ofthe entire business which is much wider than CSR

• Role can also encompass the following sustainability issues:a) Managing environmental riskb) Resource conservation and managementc) Waste reductiond) Product stewardship and life cycle footprintse) New 'green' product lines or servicesf) Community Involvement and volunteerismg) 'Green' Communications, reporting and marketing strategyh) Employee Transportation Plans and Incentives

ZFB & ASSOCIATES, Chartered Accountants 92

CHIEF CSR / SUSTAINABILITY OFFICER

• Could be made responsible for defining and developing thestrategies which underpin a company’s CSR objectives.

• Conduct research, come up with ideas, develop policies, createdetailed plans, build relationships with partner organisations, andthen implement and coordinate a range of activities and initiativeswhich are designed to have a positive impact on the environmentand local communities.

• Responsible for overseeing the recruiting, managing and trainingjunior staff members and other HR related matters

• As CSR and sustainability sink into the corporate psyche, whereinCompanies would mandatorily be required to appoint a CSO if theyhave CSR spending beyond prescribed limits or any other acceptablethresholds on the same lines as the mandatory appointment of CFOsand other key management personnel

ZFB & ASSOCIATES, Chartered Accountants 93

PROGRAMME MANAGER

• Since companies are now mandatorily required to undertake theirCSR activities under programme / project mode either on their ownor through implementing agencies, whether singly or incollaboration, there would be an increasing need for companies andimplementing agencies to recruit programme managers to workunder the CSO.

• Their main functions would be to ensure implementation ofprojects in a uniform manner at the ground level and also lay downmonitoring and evaluation systems in respect thereof and ensurequality assurance in the entire CSR life cycle, based on theobjectives and strategies which are laid down by the CSO or topmanagement.

• The Company or the implementing agency could appoint as manyprogramme managers as it deems necessary depending upon thenumber, type and nature of projects and the level / degree ofcomplexity / specialization involved in implementing them.

ZFB & ASSOCIATES, Chartered Accountants 94

CSR FUND RAISING MANAGER

• This is a position which could typically be relevant for largeNGOs who would act as implementing partners in respectof the CSR projects which would be undertaken on behalfof corporates based on the level of spending statutorilyrequired.

• Their role would be to understand the resource needs forindividual projects / programmes and approach thecorporates for funds out of their CSR budgets and ensureoptimum utilization in respect thereof.

• The resources may be tied up for a one time programmes /projects or on an on-going basis, the idea being that thereshould be an ongoing tap available for implementation.

ZFB & ASSOCIATES, Chartered Accountants 95

CSR COMMUNICATIONS MANAGER

• Relevant both for corporates and implementing agencies.• Corporates are now incredibly keen to make sure that their

practices, processes, products and procedures are ethical,sustainable and environmentally friendly

• An impressive CSR strategy can also enhance a company’sreputation and thus maximise its profitability.

• All these make out a case for large companies to hire adedicated CSR Communications Manager.

• Such personnel can ensure that the CSR initiatives arepublicised effectively and make the company moreattractive and reputable in a variety of ways.

ZFB & ASSOCIATES, Chartered Accountants 96

CSR COMMUNICATIONS MANAGER

• They can also help the recruitment process byattracting the best candidates, and they can activelyreduce outgoings by helping the organisation to cutdown on its consumption of valuable resources.

• They can make sure that their endeavours have apositive impact on society and the environment.

• By acting as an internal and external representative forthe company’s CSR policies and projects they would beresponsible for raising awareness of the company’scommitment to CSR and generating publicity around itsaltruistic endeavours.

ZFB & ASSOCIATES, Chartered Accountants 97

SPECIALISED EXTERNAL AGENCIES

• PROJECT IMPLEMENTATION AGENCIES

• PROJECT MONITORING AGENCIES

• AUDIT AND COMPLIANCE AGENCIES

ZFB & ASSOCIATES, Chartered Accountants 98

PROJECT IMPLEMENTATION AGENCIES

• NGOs / Trusts

• In house foundations promoted bycompanies (Corporate Foundations)

ZFB & ASSOCIATES, Chartered Accountants 99

NGOs / TRUSTS

Factors to be considered for selection:• Number of years in the business• Reputation and Location• Certification and Registration• Documentation• Infrastructure• Financial Capabilities• Credentials• Technical Skills

ZFB & ASSOCIATES, Chartered Accountants 100

CORPORATE FOUNDATIONS

Benefits:

• It facilitates the corporates in giving back to the society in amore structured manner and creates a peaceful environmentaround their operating areas.

• It can serve as a common vehicle to consolidate the CSRactivities of different groups companies and also differentgeographical location within the same company.

• It helps the Company to segregate the profit motive from thedevelopment motive of a business in such a way that thebusiness motive does not undercut the development motive.

• A company with a foundation will likely be seen as sociallyconscious and thus likely to be the brand of choice for thediscerning customer.

ZFB & ASSOCIATES, Chartered Accountants 101

CORPORATE FOUNDATIONS

• A company which contributes to foundations which arerecognized for tax exemptions would be able to enjoybenefits which otherwise could get denied whilstincurring CSR expenses.

• The governance structure and monitoring is generallystronger in case of foundations due to betterregulatory oversight which outweighs thedisadvantages which could arise due to family /promoter’s dominance and influence.

• Foundations because of their stronger governancestructure are able to attract better talented people.

• However, Corporate Foundation

ZFB & ASSOCIATES, Chartered Accountants 102

CORPORATE FOUNDATIONS

Common Pitfalls:• In many cases they act merely as a buffer between the company and the

community which is not seen in a positive light by the community byvirtue of the impact of their activities like displacement, environmentdegradation, economic and social inequity for which they prefer engagingwith the community through an agency which is not profit-oriented but atthe same time represents the company. This is normally the case withcompanies in the mining and extractive industries.

• Though a foundation may have robust governance structures, they usuallyare oblivious to the key issues and ground realities which the local NGOshave a better grip on and hence they may not be as process oriented asthe NGOs.

• Many a times, foundations may not be able to function in an autonomousmanner due to the strong influence of the promoters and controllingshareholders.

ZFB & ASSOCIATES, Chartered Accountants 103

CORPORATE FOUNDATIONS

• Foundations are sometimes perceived as a waste of effort, time andmoney since they may be formed just to enable a company tosatisfy its regulatory requirements and thus is nothing but asmokescreen. NGOs are much better at handling social issues and afoundation will take a lot of time to reach that stage. NGOs alsohave proven capacity and have a community connect so it doesn’talways make sense to create a parallel structure.

• Despite being established by companies, foundations constantlyseek to create a separate identity with the community orbeneficiaries. However, the demarcation is not very simple. Many atime they are perceived as the company. In turn, foundations are attimes expected by the company to be their representatives on theground. In times of a conflict between the company and thecommunity, the foundation finds itself at the receiving of bothparties.

ZFB & ASSOCIATES, Chartered Accountants 104

PROJECT MONITORING AGENCIES

• Engineering and Technical Service Firms

• Sustainability Service Firms

ZFB & ASSOCIATES, Chartered Accountants 105

ENGINEERING AND TECHNICAL SERVICE FIRMS

• Whilst the emphasis of the CSR regulations is onfinancial spending and reporting, the same would bemeaningless unless the CSR projects / activities /interventions achieve the desired impact in physicalterms to the intended beneficiaries which involvestechnical assessment depending upon the assessmentof the expected impacts, agreed outcomes and agreedoutputs

• Such firms would be able to better provide anassurance on various complex technical matters sincethey understand the complexities involved and canapply a multi-disciplinary approach.

ZFB & ASSOCIATES, Chartered Accountants 106

SUSTAINABILITY SERVICE FIRMS

• CSR and sustainability or sustainable development are synonymous since CSRinvolves conduct of the business in such a manner that it minimizes the harm tothe environment and local and general communities as well as benefitingconsumers and employees and thus ensuring sustainable development.

• CSR activities which are mandated as per regulations are an important componentof the sustainability initiatives of the Company which need to be captured in acomprehensive document referred to as the Sustainability Report or BusinessResponsibility Report, which captures the critical aspects of an organisation’seconomic, social and environmental impacts.

• The need for publishing a sustainability report arises due to various factors likeglobalisation of business, investor, customers and activitist’s pressure, as wellemployee considerations.

• A need arises for a third party assurance to evaluate the credibility, accuracy andrelevance of the disclosures in the sustainability report, which can be provided byspecialised firms who have focus and expertise in sustainability related issues andhave better experience with the various stakeholders.

ZFB & ASSOCIATES, Chartered Accountants 107

AUDIT AND COMPLIANCE AGENCIES

• As a Statutory Auditor

• As an Internal Auditor / Consultant / Advisor

ZFB & ASSOCIATES, Chartered Accountants 108

ROLE OF STATUTORY AUDITOR

• Disclosures in the financial statements in terms of therequirements of Schedule III of the Companies Act,2013.

• Compliance with the specific requirements of theGuidance Note on Accounting for Expenditure onCorporate Social Responsibility (CSR) Activities issuedby the ICAI and the Accounting Standards notifiedunder the Rules issued under the Companies Act,2013, as applicable to specified types of entities.

• Concept of Constructive Obligation (disclosures in theBoard Report and the Web site)

ZFB & ASSOCIATES, Chartered Accountants 109

ROLE OF STATUTORY AUDITOR

• Compliance with the Standards on Auditing issued by the ICAI.

a) SA-250 on Consideration of Laws and Regulations in anAudit of Financial Statements

b) SA-260 on Communication to Those Charged withGovernance

c) SA-265 on Communicating Deficiencies in Internal Controld) SA-315 on Identifying and Assessing the Risks of Material

Misstatements Through Understanding the Entity and itsEnvironment

e) SA-720 – The Auditor’s Responsibility in Relation to OtherFinancial Information in Documents Containing AuditedFinancial Statements

ZFB & ASSOCIATES, Chartered Accountants 110

GUIDANCE NOTE ON CSR EXPENSES

• Normally any amount spent on CSR would be an expenditure even if theamount represents an asset e.g. school built since the economic benefitstherefrom would not flow to the Company since it is precluded fromincluding any surplus from CSR activities as its profits.

• In some cases, a company may supply goods manufactured by it or renderservices as CSR activities. In such cases, the expenditure incurred shouldbe recognised when the control on the goods manufactured by it istransferred or the allowable services are rendered by the employees. Thegoods manufactured by the company should be valued in accordance withthe principles prescribed in Accounting Standard (AS) 2, Valuation ofInventories. The services rendered should be measured at cost. Indirecttaxes (like excise duty, service tax, VAT or other applicable taxes) on thegoods and services so contributed will also form part of the CSRexpenditure.

• Where a company receives a grant from others for carrying out CSRactivities, the CSR expenditure should be measured net of the grant.

ZFB & ASSOCIATES, Chartered Accountants 111

GUIDANCE NOTE ON CSR EXPENSES

• Since the surplus arising from CSR activities is not arising from a transaction withthe owners, it would not be considered as ‘income’ for accounting purposes. Inview of the aforesaid requirement any surplus arising out of CSR project orprogramme or activities shall be recognised in the statement of profit and loss andsince this surplus cannot be a part of business profits of the company, the sameshould immediately be recognised as liability for CSR expenditure in the balancesheet and recognised as a charge to the statement of profit and loss.

• No provision needs to be made for the difference between the amount required tobe spent and the actual expenditure incurred unless it meets the recognitioncriteria for an expense provision in terms of the Accounting Standards. (Concept ofConstructive Obligation may be relevant)

• All expenditure on CSR activities, that qualify to be recognised as expense as aboveshould be recognised as a separate line item as ‘CSR expenditure’ in the statementof profit and loss. Further, the relevant note should disclose the break-up ofvarious heads of expenses included therein and separately indicating anyexpenditure resulting in the construction / creation of an asset

• Disclosure of transactions with related parties, if any, should be made.

ZFB & ASSOCIATES, Chartered Accountants 112

ROLE AS INTERNAL AUDITOR/ CONSULTANT/ ADVISOR

• Developing a CSR Strategy / Policy.• Advising on the constitution of the CSR Committee and maintaining

the minutes of the same and communicating and implementing thedecisions made thereon

• Operationalising the institutional mechanism like nature / legalstructure of the implementing agencies, finance, accounting, HRand IT systems etc.

• Conducting a due diligence of the implementation partner and themonitoring agency.

• Developing the project parameters.• Approving the project for funding and finalizing the arrangement

with the implementing agency.• Monitoring the progress of the project.• Impact assessment.

ZFB & ASSOCIATES, Chartered Accountants 113

Questions????

ZFB & ASSOCIATES, Chartered Accountants 114