challenges and opportunities for the u.s. dairy industry · jeff bulk konhokton south new berlin...

TRANSCRIPT

1

Challenges and Opportunities Challenges and Opportunities for the U.S. Dairy Industryfor the U.S. Dairy Industry

Greg WickhamGreg WickhamCEO, Dairylea Cooperative Inc.CEO, Dairylea Cooperative Inc.

Dairylea Cooperative Inc.Dairylea Cooperative Inc.2,200 Members2,200 Members5.5 Billion Pounds Marketed Annually5.5 Billion Pounds Marketed Annually

2

U.S. Cooperative Rankings

Source: Hoard’s Dairyman; October 2007

A Cooperative Milk Marketing A Cooperative Milk Marketing Joint Venture in the NortheastJoint Venture in the Northeast

3

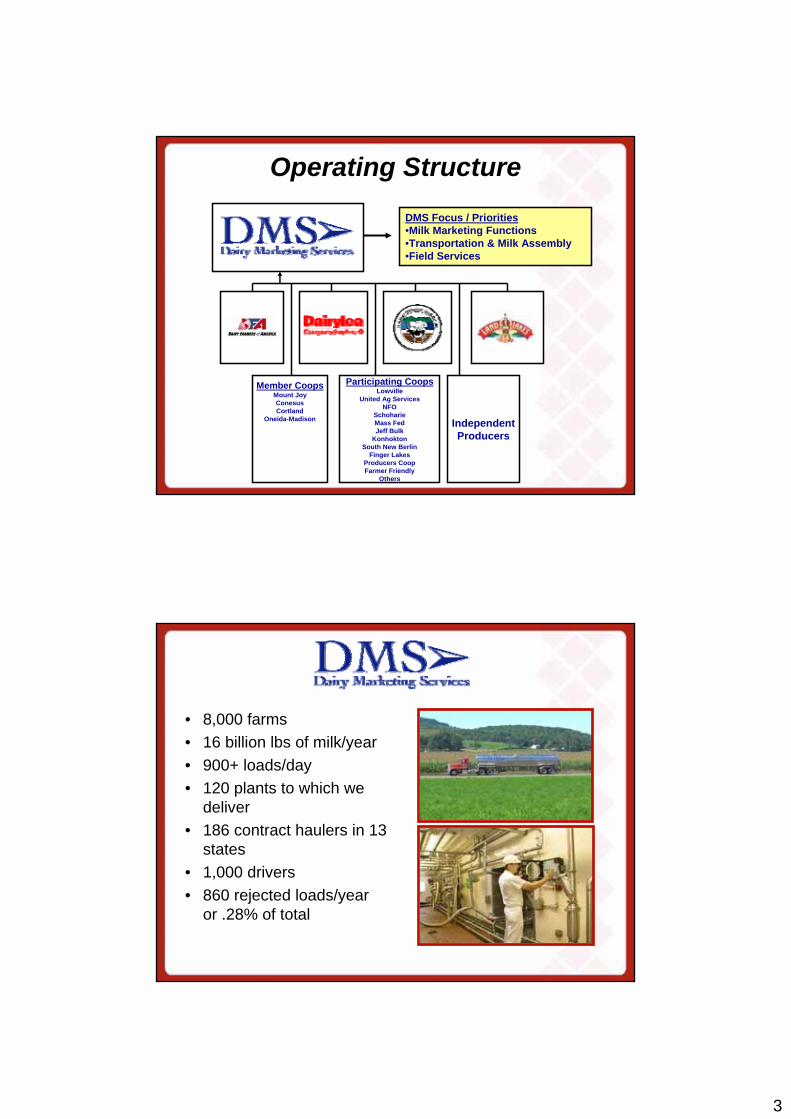

Operating Structure

Participating CoopsLowville

United Ag ServicesNFO

SchoharieMass FedJeff Bulk

KonhoktonSouth New Berlin

Finger LakesProducers CoopFarmer Friendly

Others

IndependentProducers

DMS Focus / Priorities•Milk Marketing Functions•Transportation & Milk Assembly•Field Services

Member CoopsMount JoyConesusCortland

Oneida-Madison

• 8,000 farms• 16 billion lbs of milk/year• 900+ loads/day• 120 plants to which we

deliver• 186 contract haulers in 13

states• 1,000 drivers• 860 rejected loads/year

or .28% of total

4

December 2007Northeast Market Share

DMS 56.1%

Unknown 4.8%

Independents13.6%

DMS MEC1.2%

AgriMark8.9%

Upstate Niagara5.6%

MD-VA4.2%

Other Cooperatives4.4%

Division 951.0%

7 Unique Farm Services

5

Dairylea is a Dairylea is a Member Cooperative of DFAMember Cooperative of DFA

Area Councils

American Dairy BrandsAmerican Cheese

Italian Cheese Formulated Dairy Foods

AffiliatesIngredients

DFA Business Units

Fluid

6

Dairy PlantsDFA Marketing Network

DFA Marketing NetworkDean Foods (105)DFA Branded (4)DFA Cheese (5)DFA Formulated (6)DFA Manufacturing (7)Fluid JV (64)Leprino Foods Co (9)Manufacturing JV (15)

Member Demographics

12,183 Members

500 Largest Farms Make 50% of total milk marketed

7

EconomicsEconomics

What Affects Milk Prices?• International markets• National milk

production• Economy• Dairy product

consumption• CWT• Weather• rbST use

8

$7 Corn and $120 Oil$7 Corn and $120 OilDo not work with Do not work with

$18 Milk$18 Milk

Prices Will Continue to Cycle but at a Higher Level

Central NY Annual Average Gross Milk Price 1996-2008

$11.00

$13.00

$15.00

$17.00

$19.00

$21.00

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

E

$ pe

r hu

ndre

dwei

ght

9

U.S. Milk Production GrowthYear-over-year, 2005-2008

3.9%2.7%

2.1%2.7%

0.0%1.0%2.0%3.0%4.0%5.0%

2005 2006 2007 2008E

U.S. Dairy Exports as a Percent of U.S. Milk Production, 2001-2007

5.5 5.15.7

7.58.3

9.3 9.5

0

2

4

6

8

10

01 02 03 04 05 06 07

% o

f milk

pro

duct

ion Data Source: US Dairy Export Council

10

Costs UpCosts UpSubstantiallySubstantially

U.S. Average Purchased Feed Cost, 2002-2008

$3.59 $3.68 $3.97 $3.50 $3.88$5.22

$7.23

$0

$2

$4

$6

$8

2002 2003 2004 2005 2006 2007 2008E

$ pe

r C

WT

of M

ilk

11

U.S. Dairy Industry U.S. Dairy Industry Trends & Trends &

BackgroundBackground

Size of Average U.S. Dairy Farm1992 - 2007

74 76 80 84 87 92 100105 111 118123135140 147

155

129

0

25

50

75

100

125

150

175

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Dai

ry C

ows

per F

arm

12

Farm Size Trends… % of Milk in U.S. by Farm Size

Year 200-499 500-999 1,000-1,999 2,000+ Total1980 2.10% 0.50% 0% 0% 2.60%2002 17.5% 13.9% 13.0% 15.0% 59.4%2009 11.6% 12.3% 17.3% 33.8% 75.0%

U.S. Annual Milk Production 1997-2007

150,000

155,000

160,000

165,000

170,000

175,000

180,000

185,000

190,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Mill

ion

Poun

ds

Annual Growth Rate Approximately 2% Over Time

13

Production Per Cow1997-2007

10,000

12,000

14,000

16,000

18,000

20,000

22,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Poun

ds

U.S.Northeast

The 3,000 biggest farms in the The 3,000 biggest farms in the U.S. produce more milk than U.S. produce more milk than any single country in the EU!any single country in the EU!

14

Regional Changes10-Year Milk Shed Shift

50%50%50%50%50%50%50%50%50%

-53%-53%-53%-53%-53%-53%-53%-53%-53%

-17%-17%-17%-17%-17%-17%-17%-17%-17%

-15%-15%-15%-15%-15%-15%-15%-15%-15% -41%-41%-41%-41%-41%-41%-41%-41%-41%-27%-27%-27%-27%-27%-27%-27%-27%-27%

-42%-42%-42%-42%-42%-42%-42%-42%-42%

-38%-38%-38%-38%-38%-38%-38%-38%-38%

-10%-10%-10%-10%-10%-10%-10%-10%-10%1%1%1%1%1%1%1%1%1%

62%62%62%62%62%62%62%62%62% -62%-62%-62%-62%-62%-62%-62%-62%-62%

49%49%49%49%49%49%49%49%49%

56%56%56%56%56%56%56%56%56%

-10%-10%-10%-10%-10%-10%-10%-10%-10%

-7%-7%-7%-7%-7%-7%-7%-7%-7%

131%131%131%131%131%131%131%131%131%

-15%-15%-15%-15%-15%-15%-15%-15%-15%

8%8%8%8%8%8%8%8%8%

85%85%85%85%85%85%85%85%85%-31%-31%-31%-31%-31%-31%-31%-31%-31%

-54%-54%-54%-54%-54%-54%-54%-54%-54%

-10%-10%-10%-10%-10%-10%-10%-10%-10%

31%31%31%31%31%31%31%31%31%

-10%-10%-10%-10%-10%-10%-10%-10%-10%

-48%-48%-48%-48%-48%-48%-48%-48%-48%

-28%-28%-28%-28%-28%-28%-28%-28%-28%

15%15%15%15%15%15%15%15%15%

3%3%3%3%3%3%3%3%3%

20%20%20%20%20%20%20%20%20%

92%92%92%92%92%92%92%92%92%

5%5%5%5%5%5%5%5%5%

-29%-29%-29%-29%-29%-29%-29%-29%-29%

-39%-39%-39%-39%-39%-39%-39%-39%-39%

9%9%9%9%9%9%9%9%9%

-5%-5%-5%-5%-5%-5%-5%-5%-5%

38%38%38%38%38%38%38%38%38%

1%1%1%1%1%1%1%1%1%

-24%-24%-24%-24%-24%-24%-24%-24%-24%

3%3%3%3%3%3%3%3%3%

-37%-37%-37%-37%-37%-37%-37%-37%-37%

16%16%16%16%16%16%16%16%16%

13%13%13%13%13%13%13%13%13%

-5%-5%-5%-5%-5%-5%-5%-5%-5%

5%5%5%5%5%5%5%5%5%

-24%-24%-24%-24%-24%-24%-24%-24%-24%

4%4%4%4%4%4%4%4%4%

26%26%26%26%26%26%26%26%26%

Pct Change in Annual Milk Production3-Year Average: 1995-1997 / 2005-2007

Increase greater than 25% (10)Increase from 10 to 25% (4)Increase from 0 to 10% (9)Decrease from 0 to 10% (6)Decrease from 10 to 25% (6)Decrease greater than 25% (13)

Why the Shift West?

• Land availability & price

• California Real Estate $$

• State incentives• Environmental

15

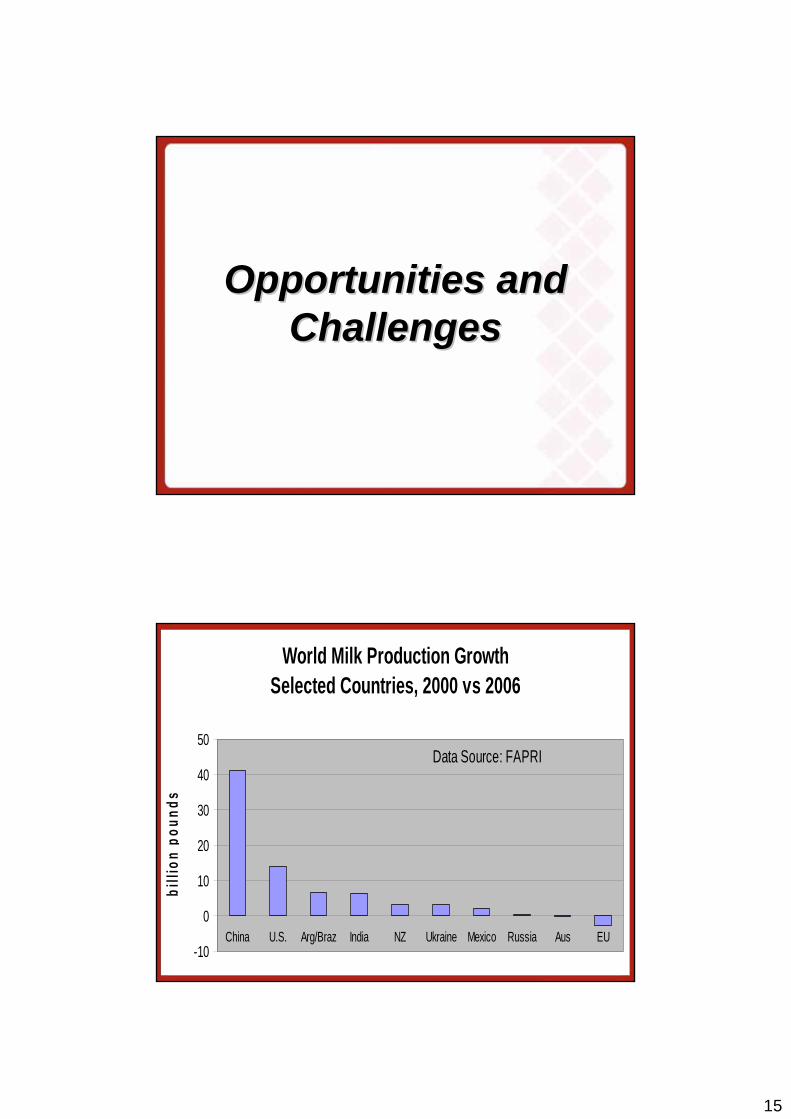

Opportunities and Opportunities and ChallengesChallenges

World Milk Production GrowthSelected Countries, 2000 vs 2006

-10

0

10

20

30

40

50

China U.S. Arg/Braz India NZ Ukraine Mexico Russia Aus EU

billi

on p

ound

s

Data Source: FAPRI

16

Reduced World Inventories

Low World Stocks = Low World Stocks = Upward Price Pressure Upward Price Pressure

& More Volatility& More Volatility

17

China's GDP Per Person, RNB, 1953-2005

02,0004,0006,0008,000

10,00012,00014,00016,000

53 56 59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04

Year

RN

B P

er P

erso

n RNB = Renminbi, official currency of China

• China GDP has almost doubled since 2000• RNB 14,000 = $ 1,866• U.S. GDP per person = $ 44,000

U.S. History of Exports

• 1950 – 1995“Anyhow Exporter”

• 1995 – 2000Farm Leadership Interest in Exports

• 2000 – PresentIndustry Very Focused on Exports

18

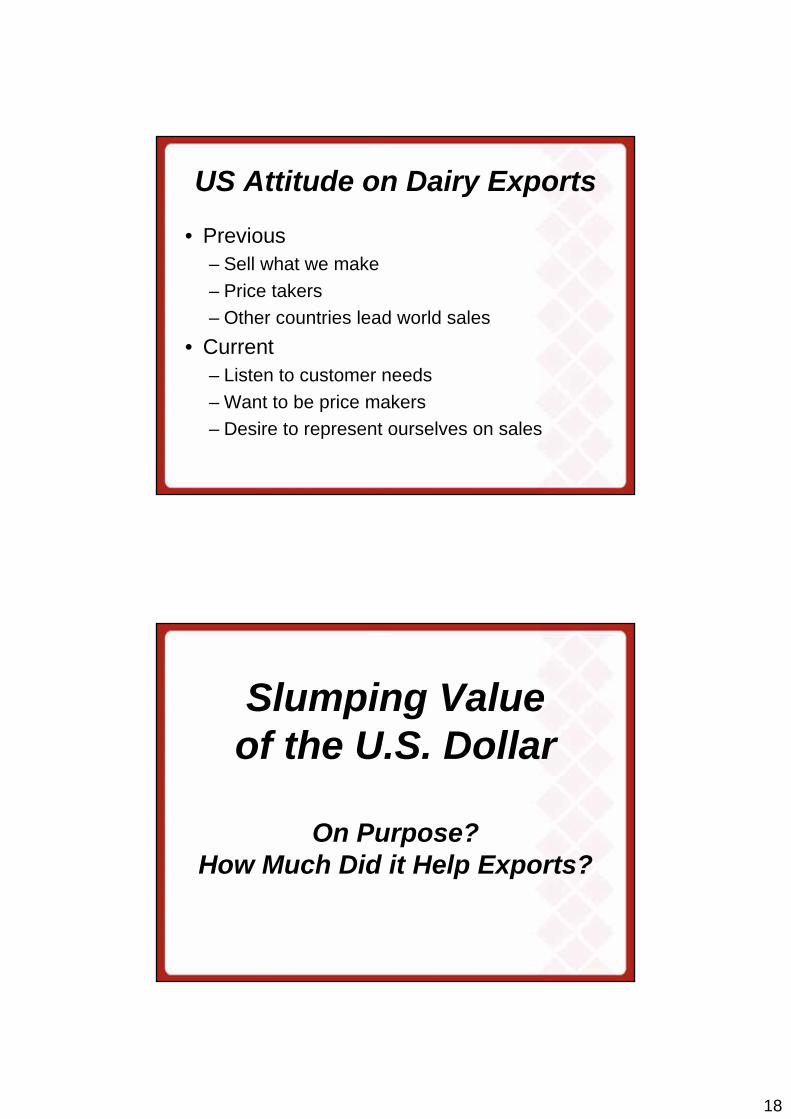

US Attitude on Dairy Exports

• Previous– Sell what we make– Price takers– Other countries lead world sales

• Current– Listen to customer needs– Want to be price makers– Desire to represent ourselves on sales

Slumping Value of the U.S. Dollar

On Purpose?How Much Did it Help Exports?

19

Ethanol Boom or Bust…

Biofuel … Is It Good U.S. Policy?

20

Is Sustainability a Passing Fad?

If Carbon Footprint If Carbon Footprint is Important …is Important …

How Do We Rank?How Do We Rank?

21

Carbon Footprint

• Low– Maximum

Technology• High

– Organic / Less Technology

Industry Consolidation

• Processors• Cooperatives• Dairy Farms• Federal Orders

22

Will rbST RIP?

23

!

!

! !

!

!!

!

!

CrowleyConcord

CalabroEast Haven

FarmlandWallington

OaktreeEast Northpor

St AlbansSt Albans

OakhurstPortland

HoodPortland

GrantsBangor

Houlton DairyHoulton

rbST-free Plants 2006

24

!

!

!!

!

!

!

!

!

!

! !

!!

!

!

!

!

!

!

!

!

!!

!

!

GarelickE Greenbush

Schneider ValleyWilliamsport

Dietrich BST freeReading

RosenbergersHatfield

GarelickFlorence

FarmlandWallington

CrowleyBinghamton

Dietrich BST freeMiddlebury Ctr.

Agro-FarmaS. Edmeston

Morningstar BST freeFraser

Hood BST freeOneida

Hood BST freeVernon

Crescent RidgeSharonHood

Agawam

OaktreeEast Northport

CalabroEast Haven

GuidaNew Britain

Garelick BST freeFranklin

CrowleyConcord

HoodBarre

MonumentWeybridge

St AlbansSt Albans

OakhurstPortland

HoodPortland

GrantsBangor

Houlton DairyHoulton

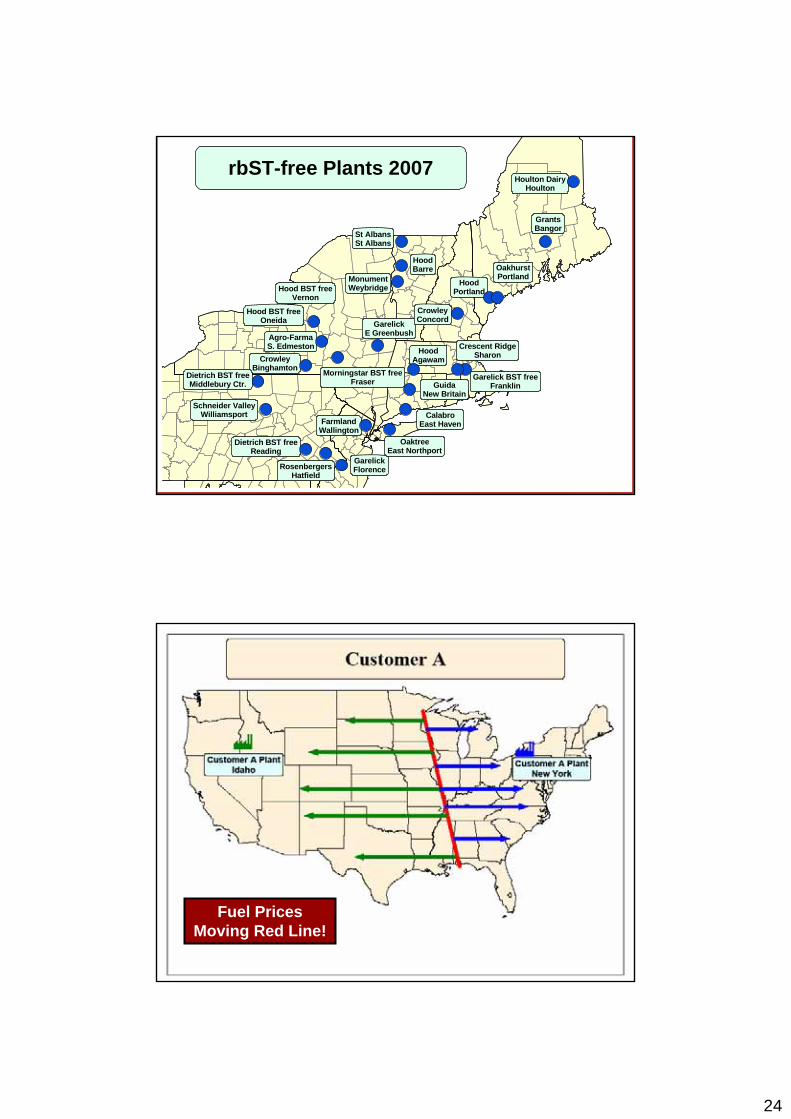

rbST-free Plants 2007

Fuel Prices Moving Red Line!

25

Immigration Reform

Can the U.S. Dairy Can the U.S. Dairy Industry Continue Industry Continue

To Grow?To Grow?

26

New Technology• Remove Water

• Genetics

• Robotics

• Fractionalization

Will U.S. Farms Will U.S. Farms Invest Outside the Invest Outside the

U.S.?U.S.?

27

Thank YouThank You