challenger aged care guide - penheiro financial … · challenger aged care guide 3 aged care guide...

TRANSCRIPT

Challenger Aged care guide

July 2013 Adviser use only

Table of contentsWelcome to the Challenger aged care guide 1

Advising your clients about aged care 2

Before entering an aged care facility 6Aged Care Assessment Teams 7

How long does an ACAT approval last? 7

Managing the entry point to aged care 8Accommodation bonds 9

Accommodation charges 11

The ongoing costs 14Basic daily fee 15

Income-tested fee 15

Extra service fee 17

Aged care golden rules 18Evaluate whether to keep the family home 19

Weigh up the benefits of negotiating a higher accommodation bond 20

Invest for cash flow 21

Case study 24

Other factors to consider 30

Learn more 33

Index 34

Challenger Aged care guide 1

Welcome to the Challenger Aged care guide

Around 59,000 aged care assessments will be carried out this year for people looking to enter an aged care facility. With average non-home equity wealth of $175,000 per person1, it’s likely that these people will need financial advice.

Entering an aged care facility, or assisting a family member to do so, can place great demands on your client’s time and patience. Think of the value you can add by helping them decide whether to sell the family home, and by investing your client’s capital to minimise aged care costs and maximise their social security entitlements.

There’s an average life expectancy of around three years for people in residential aged care. Providing aged care advice will often bring you in touch with the client’s extended family, because eventually there will be an estate to manage. If you have delivered sound advice to this point, you should be well-placed to assist with the needs of the next generation.

If you’re interested in providing advice in this important and growing area, then this guide can help. It is a reference guide of aged care rules and other information, and provides hypothetical worked examples to illustrate how these principles can be applied.

Note that the fees and charges outlined in this guide refer to aged care facilities that are subsidised by the Commonwealth Government. In order for low and high level care facilities to receive residential care subsidies from the Government, they must be accredited by the Aged Care Standards and Accreditation Agency. Facilities that are not Commonwealth funded do not have the same fee restrictions and may be subject to different fees.

1 Australian Bureau of Statistics, Department of Health and Ageing, Centrelink, Challenger Life analysis.

2 Challenger Aged care guide

Advising your clients about aged care

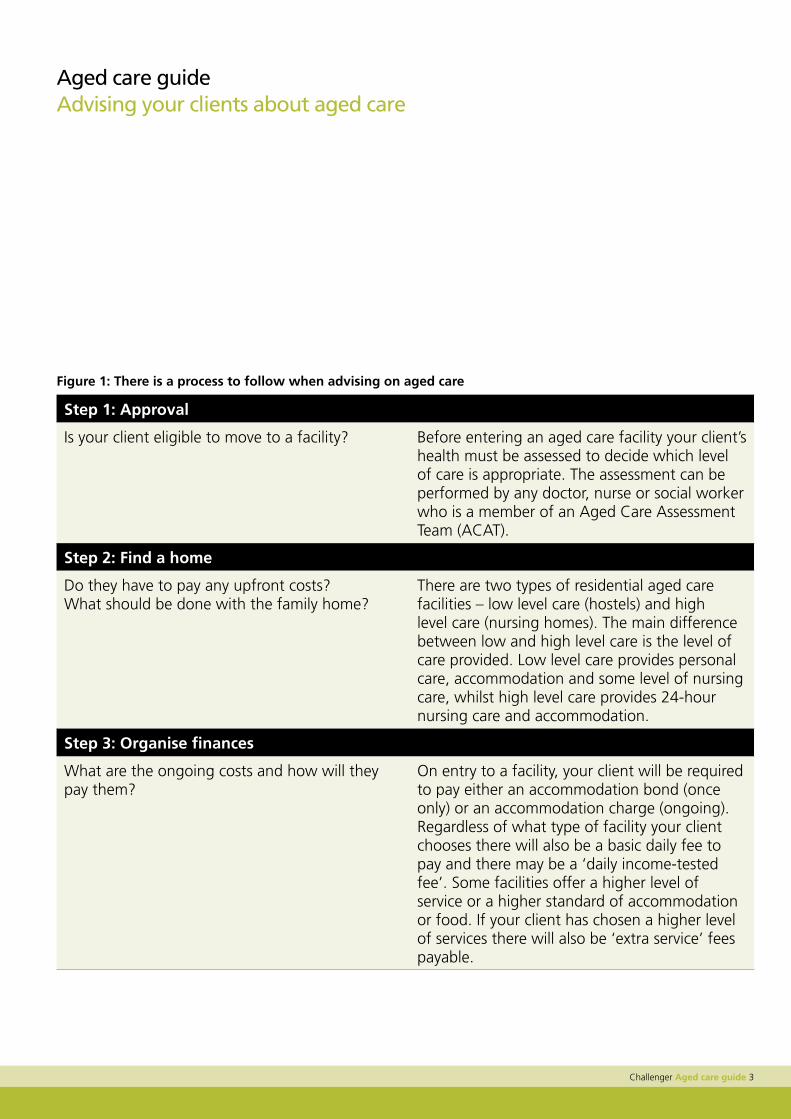

There is a process to follow when providing aged care advice to see that your client is appropriately assessed and approved, finds a home and organises their finances to suit their new circumstances (Figure 1).

It is important to carefully consider each of the following steps. Some decisions may be irreversible, and when moving to the next step could have negative consequences. This is why it’s important to become involved as early as possible.

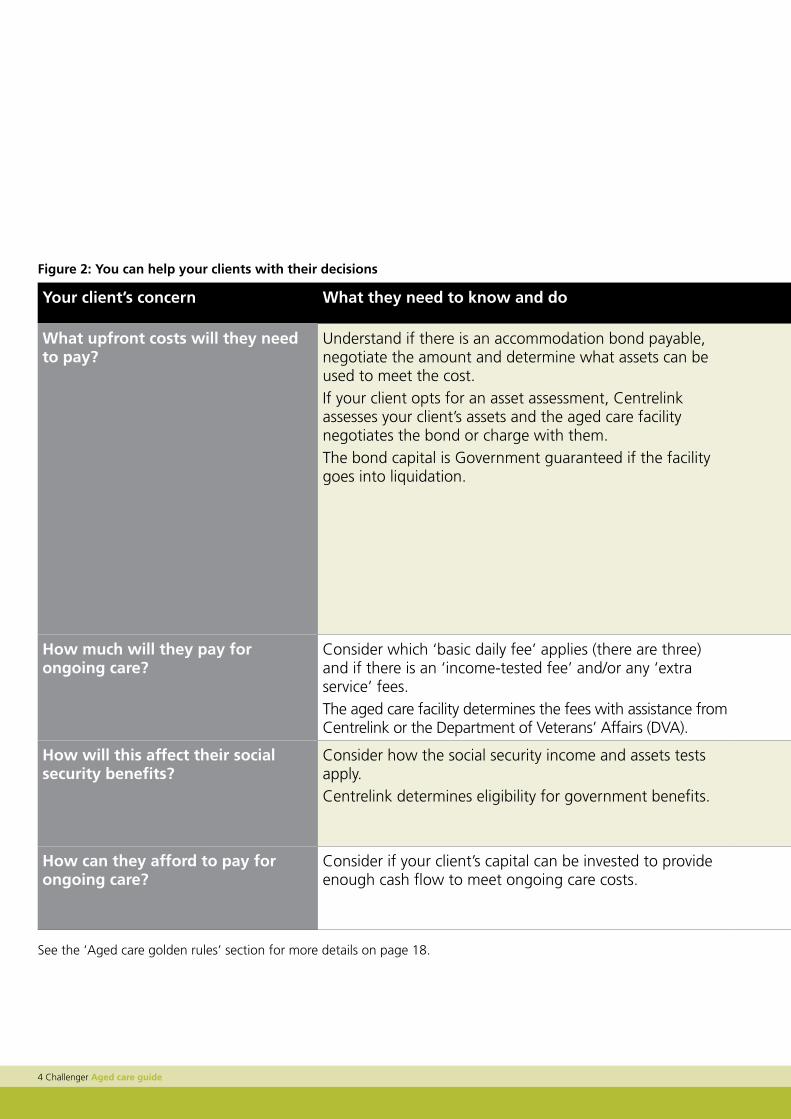

Your role as a trusted adviser will be to find a balance between your client’s objectives and concerns, and to highlight any trade-offs needed to achieve the required result (Figure 2).

Challenger Aged care guide 3

Aged care guide Advising your clients about aged care

Figure 1: There is a process to follow when advising on aged care

Step 1: Approval

Is your client eligible to move to a facility? Before entering an aged care facility your client’s health must be assessed to decide which level of care is appropriate. The assessment can be performed by any doctor, nurse or social worker who is a member of an Aged Care Assessment Team (ACAT).

Step 2: Find a home

Do they have to pay any upfront costs? What should be done with the family home?

There are two types of residential aged care facilities – low level care (hostels) and high level care (nursing homes). The main difference between low and high level care is the level of care provided. Low level care provides personal care, accommodation and some level of nursing care, whilst high level care provides 24-hour nursing care and accommodation.

Step 3: Organise finances

What are the ongoing costs and how will they pay them?

On entry to a facility, your client will be required to pay either an accommodation bond (once only) or an accommodation charge (ongoing). Regardless of what type of facility your client chooses there will also be a basic daily fee to pay and there may be a ‘daily income-tested fee’. Some facilities offer a higher level of service or a higher standard of accommodation or food. If your client has chosen a higher level of services there will also be ‘extra service’ fees payable.

4 Challenger Aged care guide

Figure 2: You can help your clients with their decisions

Your client’s concern What they need to know and do Strategy points and tips Some traps

What upfront costs will they need to pay?

Understand if there is an accommodation bond payable, negotiate the amount and determine what assets can be used to meet the cost. If your client opts for an asset assessment, Centrelink assesses your client’s assets and the aged care facility negotiates the bond or charge with them. The bond capital is Government guaranteed if the facility goes into liquidation.

Will the family home or investments need to be sold to fund the bond?Is it better to pay the entire bond by periodic payment or by lump sum, or will a combination of both be best?If assessable assets are below the minimum level (currently $43,000), no entry fee applies. It may be better that your client does not have their assets assessed.Negotiating a higher bond may increase your client’s chance of being accepted in a facility whilst also improving their social security and aged care position.If a couple, timing the move of each person’s entry to the facility may help. The bond balance is exempt from the Centrelink/DVA Assets Test and is not subject to deeming.

There may be strategies to minimise the bond. However, care is required so as not to reduce your client’s chances of being accepted into their preferred facility or to prevent unintended Centrelink consequences. If the home is kept, it is important to pay the bond at least partly by periodic payment to take advantage of the social security and aged care rules.

How much will they pay for ongoing care?

Consider which ‘basic daily fee’ applies (there are three) and if there is an ‘income-tested fee’ and/or any ‘extra service’ fees.The aged care facility determines the fees with assistance from Centrelink or the Department of Veterans’ Affairs (DVA).

Keeping the home and paying the bond at least partly by periodic payment can assist in maximising the Age Pension and lowering fees. Some investments are treated more favourably for social security and aged care Income Test rules which may help minimise fees.

The rental income from the family home (if kept) will count for the social security and aged care income test if the bond is not paid at least partly by periodic payment.

How will this affect their social security benefits?

Consider how the social security income and assets tests apply. Centrelink determines eligibility for government benefits.

Keeping the home and paying the bond at least partly by periodic payment can assist in maximising the Age Pension and lowering fees. Some investments are treated more favourably for social security and aged care income test rules which may help minimise fees.

The rental income from the family home (if kept) will count for the social security and aged care income test if the bond is not paid at least partly by periodic payment.

How can they afford to pay for ongoing care?

Consider if your client’s capital can be invested to provide enough cash flow to meet ongoing care costs.

Cash flow requirements must be taken into account when selecting investment options. There are income streams available that can provide cash flow and are also treated favourably for social security and aged care.

Some investments may not produce enough cash flow to pay for fees and other expenses.

See the ‘Aged care golden rules’ section for more details on page 18.

Challenger Aged care guide 5

Figure 2: You can help your clients with their decisions

Your client’s concern What they need to know and do Strategy points and tips Some traps

What upfront costs will they need to pay?

Understand if there is an accommodation bond payable, negotiate the amount and determine what assets can be used to meet the cost. If your client opts for an asset assessment, Centrelink assesses your client’s assets and the aged care facility negotiates the bond or charge with them. The bond capital is Government guaranteed if the facility goes into liquidation.

Will the family home or investments need to be sold to fund the bond?Is it better to pay the entire bond by periodic payment or by lump sum, or will a combination of both be best?If assessable assets are below the minimum level (currently $43,000), no entry fee applies. It may be better that your client does not have their assets assessed.Negotiating a higher bond may increase your client’s chance of being accepted in a facility whilst also improving their social security and aged care position.If a couple, timing the move of each person’s entry to the facility may help. The bond balance is exempt from the Centrelink/DVA Assets Test and is not subject to deeming.

There may be strategies to minimise the bond. However, care is required so as not to reduce your client’s chances of being accepted into their preferred facility or to prevent unintended Centrelink consequences. If the home is kept, it is important to pay the bond at least partly by periodic payment to take advantage of the social security and aged care rules.

How much will they pay for ongoing care?

Consider which ‘basic daily fee’ applies (there are three) and if there is an ‘income-tested fee’ and/or any ‘extra service’ fees.The aged care facility determines the fees with assistance from Centrelink or the Department of Veterans’ Affairs (DVA).

Keeping the home and paying the bond at least partly by periodic payment can assist in maximising the Age Pension and lowering fees. Some investments are treated more favourably for social security and aged care Income Test rules which may help minimise fees.

The rental income from the family home (if kept) will count for the social security and aged care income test if the bond is not paid at least partly by periodic payment.

How will this affect their social security benefits?

Consider how the social security income and assets tests apply. Centrelink determines eligibility for government benefits.

Keeping the home and paying the bond at least partly by periodic payment can assist in maximising the Age Pension and lowering fees. Some investments are treated more favourably for social security and aged care income test rules which may help minimise fees.

The rental income from the family home (if kept) will count for the social security and aged care income test if the bond is not paid at least partly by periodic payment.

How can they afford to pay for ongoing care?

Consider if your client’s capital can be invested to provide enough cash flow to meet ongoing care costs.

Cash flow requirements must be taken into account when selecting investment options. There are income streams available that can provide cash flow and are also treated favourably for social security and aged care.

Some investments may not produce enough cash flow to pay for fees and other expenses.

See the ‘Aged care golden rules’ section for more details on page 18.

6 Challenger Aged care guide

Before entering an aged care facility

Prior to entering an aged care facility, a person’s physical and mental health must be assessed by a member of an Aged Care Assessment Team (ACAT). In Victoria, these teams are known as Aged Care Assessment Service (ACAS). A person cannot enter a facility without approval from an ACAT or ACAS member.

Challenger Aged care guide 7

Aged care guide Before entering an aged care facility

Before entering careThe level of nursing care an individual needs will determine the type of aged care facility they enter. Low level care is for people who require some help, but who do not have very complex care needs. Low level care providers offer accommodation services such as meals, laundry, additional personal care as well as some nursing care if needed.

High level care is for people who need almost complete assistance with most activities of daily living (24 hour care). This may be because they are physically unable to move around, or because they have a severe dementia-type illness or other behavioural problems.

Aged Care Assessment TeamsACATs are made up of health professionals such as doctors, nurses and social workers, and may be a useful source of information for those entering a facility as well as financial advisers. In addition to conducting the approval process, they can help to arrange a place in a suitable facility and provide information on facilities in the area.

The best way to contact an ACAT is through the client’s doctor, local hospital or community health centre.

How long does an ACAT approval last?ACAT approvals for low level care are valid for 12 months from the date the ACAT member signs the form. A new assessment will be required if a person assessed as needing low level care does not move into an aged care facility within 12 months or if their care needs change significantly prior to moving into a facility. Those assessed as requiring high level care do not need to be assessed again unless their care needs change significantly.

What are extra services?To give a person more flexibility and choice, a number of low and high level care facilities offer extra services for an additional daily fee. These services may include a higher standard of accommodation, food and other services.

8 Challenger Aged care guide

Managing the entry point to aged care

One of your client’s main concerns when they enter an aged care facility will probably be whether a large upfront cost is payable and how they will afford it. Your client will pay either an accommodation bond or charge.

An accommodation bond is generally a one-off lump sum, payable by a person entering either a low level care facility or a high level care facility with extra services.

An accommodation charge is an ongoing daily cost, payable by a person entering a high level care facility without extra services.

Challenger Aged care guide 9

Aged care guide Managing the entry point to aged care

Accommodation bonds

How is the bond determined?Each resident’s accommodation bond will be negotiated with the facility at the time of entry. If a person chooses to have an asset assessment, the maximum bond is determined by their assessable assets.

If a person has an asset assessment:

• They will only be asked to pay a bond if they have assets over $43,000.

• There is no upper limit on the amount of the bond, but they must be left with $43,000 in assets after paying the bond.

This means that the more assets your client has, the higher the bond could be.

Where a person chooses not to have an asset assessment, the bond will be determined by negotiation alone.

Tip: You may be able to help clients get into their preferred facility and/or pay a lower accommodation bond by not having an asset assessment. See page 11 for more information.

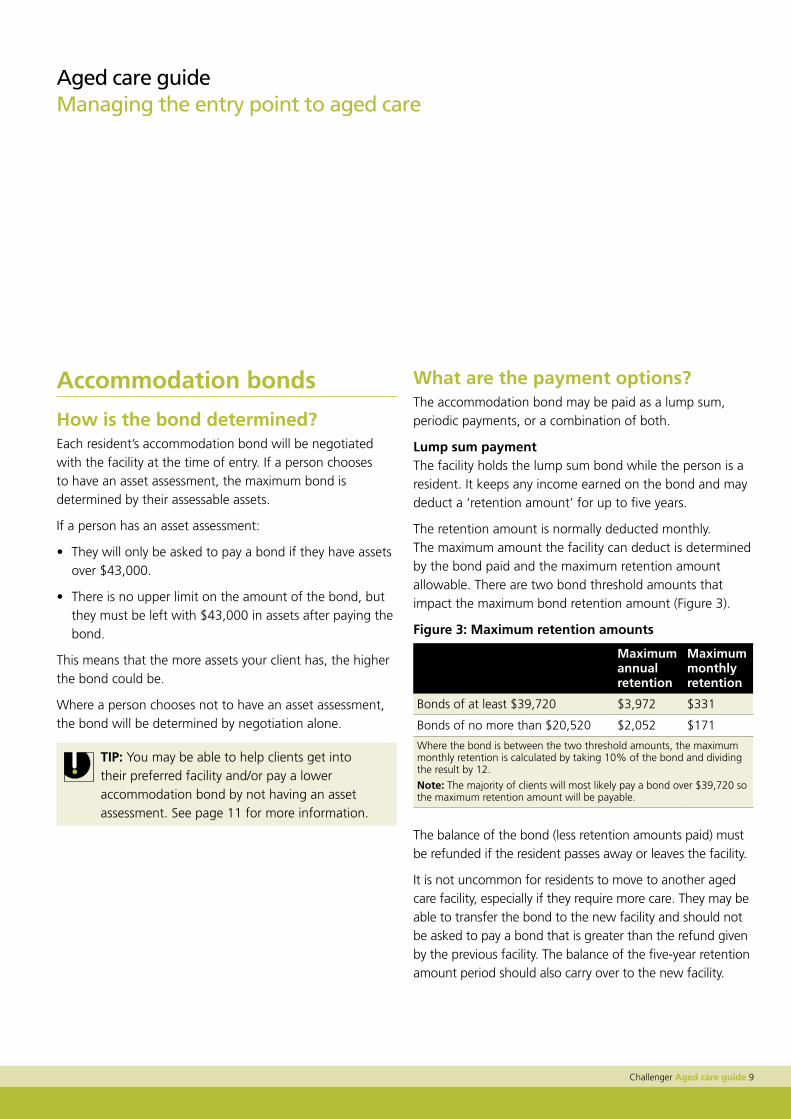

What are the payment options?The accommodation bond may be paid as a lump sum, periodic payments, or a combination of both.

Lump sum paymentThe facility holds the lump sum bond while the person is a resident. It keeps any income earned on the bond and may deduct a ‘retention amount’ for up to five years.

The retention amount is normally deducted monthly. The maximum amount the facility can deduct is determined by the bond paid and the maximum retention amount allowable. There are two bond threshold amounts that impact the maximum bond retention amount (Figure 3).

Figure 3: Maximum retention amounts

Maximum annual retention

Maximum monthly retention

Bonds of at least $39,720 $3,972 $331

Bonds of no more than $20,520 $2,052 $171

Where the bond is between the two threshold amounts, the maximum monthly retention is calculated by taking 10% of the bond and dividing the result by 12.

Note: The majority of clients will most likely pay a bond over $39,720 so the maximum retention amount will be payable.

The balance of the bond (less retention amounts paid) must be refunded if the resident passes away or leaves the facility.

It is not uncommon for residents to move to another aged care facility, especially if they require more care. They may be able to transfer the bond to the new facility and should not be asked to pay a bond that is greater than the refund given by the previous facility. The balance of the five-year retention amount period should also carry over to the new facility.

10 Challenger Aged care guide

If the resident was to move to a high care facility they may agree with the facility to have the balance of the bond refunded and pay an accommodation charge (as discussed later) or transfer the balance of the bond to the new facility.

periodic paymentIf the periodic payment option is chosen, the facility will charge interest based on the fact that it cannot earn income on the lump sum amount. The Department of Health and Ageing sets the percentage interest that a facility can charge. This charge is reset quarterly, and at 1 July 2013 is 6.82% per annum.

A resident is locked into the interest rate applicable at their time of entry. This can be a disadvantage for residents who move into facilities when interest rates are high.

Some facilities may prefer periodic payments as it provides a higher return than the facility could otherwise earn on the lump sum amount. Understanding a facility’s preferences can help you to get your clients into their desired facility.

Tip: Residents who pay at least part of their accommodation bond by periodic payment can rent out their family home and have it remain indefinitely exempt from the Centrelink/DVA Assets Test. In addition, the rental income will not be assessed for the Centrelink/DVA Income Test or the income-tested fee. See page 19 for more information.

How secure is the bond?Accommodation bond agreementsThe payment of an accommodation bond must be backed by a bond agreement. A bond agreement is a contract between a resident and the facility and must include particular details such as the date or dates that the bond is due to be paid and the interest payable if the bond is paid late.

These details must be agreed to by the resident and the facility before a bond can be paid. The bond agreement may be set out in the resident agreement but can be in a separate document.

Capital guaranteeThe accommodation bond is guaranteed by the Government, so if the facility becomes bankrupt/insolvent the Government will repay any bond (less retention amounts paid) when required. The Government requires aged care facilities to keep detailed records of bond holdings, ensure they have sufficient liquidity to repay bonds as they fall due, and provide certain financial information to residents and prospective residents.

Facilities must provide residents with information such as the bond balance and compliance with regulatory requirements, including whether bonds have been repaid on time in the past.

All providers holding bonds are required to refund bond balances:

• on the day the resident leaves the facility if a resident gives more than 14 days’ notice before leaving

• within 14 days after the resident gives notice

• if a resident dies within 14 days after being shown the grant of probate or letters of administration.

Facilities are required to pay interest for the period between when a resident leaves a facility and when the bond is actually repaid (currently 5% per annum). If a facility is late in repaying the bond, it will be required to pay a higher rate of interest equivalent to the interest paid by a resident for the time between entering a service and paying a bond to the facility (currently 6.82% per annum).

is the bond assessed for social security?The accommodation bond balance is exempt from the Centrelink/DVA Assets Test and is not subject to deeming under the Income Test because the individual is not earning income on the bond amount.

Tip: Residents may be able to increase their social security entitlement by negotiating a higher bond with a facility in return for an offset on some of the ongoing costs. If considering this strategy, it is important to remember that your client will not have access to the bond amount or earn income from it. This strategy is explored in the case study on page 27.

Challenger Aged care guide 11

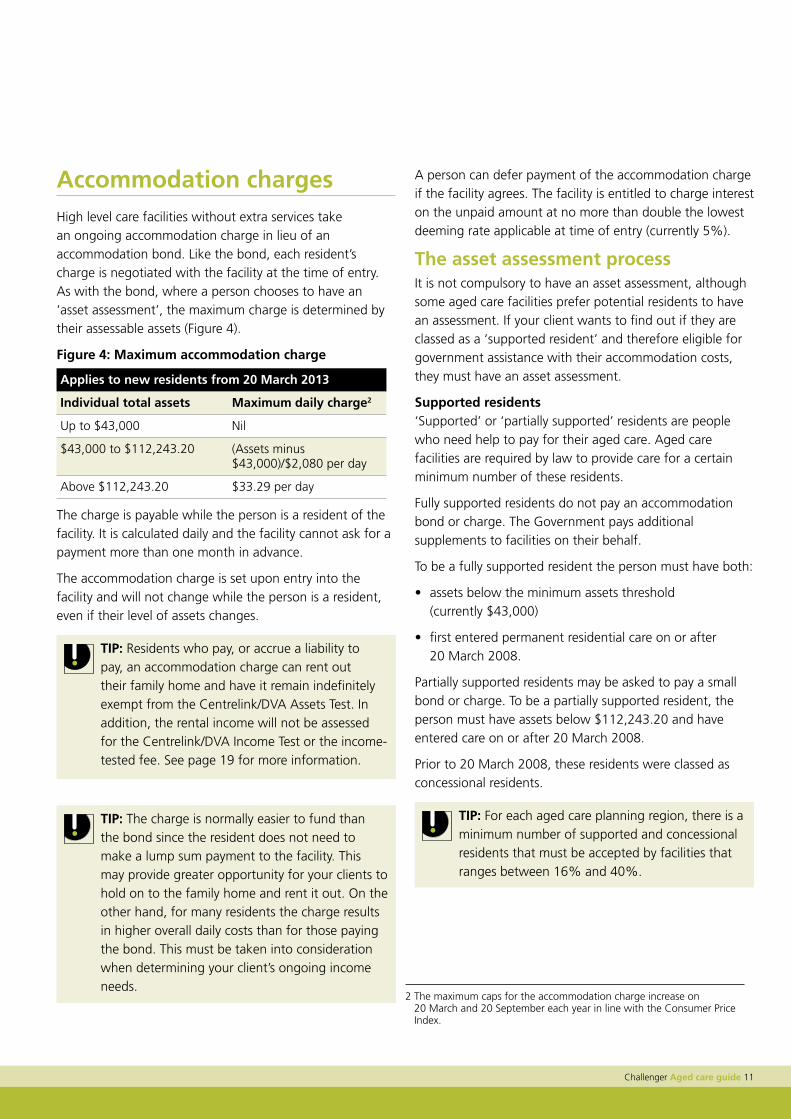

Accommodation chargesHigh level care facilities without extra services take an ongoing accommodation charge in lieu of an accommodation bond. Like the bond, each resident’s charge is negotiated with the facility at the time of entry. As with the bond, where a person chooses to have an ‘asset assessment’, the maximum charge is determined by their assessable assets (Figure 4).

Figure 4: Maximum accommodation charge

Applies to new residents from 20 March 2013

individual total assets Maximum daily charge2

Up to $43,000 Nil

$43,000 to $112,243.20 (Assets minus $43,000)/$2,080 per day

Above $112,243.20 $33.29 per day

The charge is payable while the person is a resident of the facility. It is calculated daily and the facility cannot ask for a payment more than one month in advance.

The accommodation charge is set upon entry into the facility and will not change while the person is a resident, even if their level of assets changes.

Tip: Residents who pay, or accrue a liability to pay, an accommodation charge can rent out their family home and have it remain indefinitely exempt from the Centrelink/DVA Assets Test. In addition, the rental income will not be assessed for the Centrelink/DVA Income Test or the income-tested fee. See page 19 for more information.

Tip: The charge is normally easier to fund than the bond since the resident does not need to make a lump sum payment to the facility. This may provide greater opportunity for your clients to hold on to the family home and rent it out. On the other hand, for many residents the charge results in higher overall daily costs than for those paying the bond. This must be taken into consideration when determining your client’s ongoing income needs.

A person can defer payment of the accommodation charge if the facility agrees. The facility is entitled to charge interest on the unpaid amount at no more than double the lowest deeming rate applicable at time of entry (currently 5%).

The asset assessment processIt is not compulsory to have an asset assessment, although some aged care facilities prefer potential residents to have an assessment. If your client wants to find out if they are classed as a ‘supported resident’ and therefore eligible for government assistance with their accommodation costs, they must have an asset assessment.

Supported residents‘Supported’ or ‘partially supported’ residents are people who need help to pay for their aged care. Aged care facilities are required by law to provide care for a certain minimum number of these residents.

Fully supported residents do not pay an accommodation bond or charge. The Government pays additional supplements to facilities on their behalf.

To be a fully supported resident the person must have both:

• assets below the minimum assets threshold (currently $43,000)

• first entered permanent residential care on or after 20 March 2008.

Partially supported residents may be asked to pay a small bond or charge. To be a partially supported resident, the person must have assets below $112,243.20 and have entered care on or after 20 March 2008.

Prior to 20 March 2008, these residents were classed as concessional residents.

Tip: For each aged care planning region, there is a minimum number of supported and concessional residents that must be accepted by facilities that ranges between 16% and 40%.

2 The maximum caps for the accommodation charge increase on 20 March and 20 September each year in line with the Consumer Price Index.

12 Challenger Aged care guide

Should your client have an asset assessment?Understanding accommodation bond preferences of the various facilities in your area should place you in a better position to advise your clients whether or not to undertake an asset assessment. For example, if your client has assets much higher than the average bond being charged by a facility, they may be able to negotiate a lower bond directly without having an asset assessment.

Alternatively, if completing an asset assessment will mean that a facility cannot ask for their normal bond amount because your client’s asset levels are too low, they may not accept that person in the facility.

How the assets are assessedCentrelink or DVA will carry out the asset assessment to calculate the accommodation bond or charge. A ‘Request for an Assets Assessment’ Form must be completed and returned to Centrelink or DVA.

To calculate the bond, a person’s assets are generally assessed in the same way as for Centrelink/DVA pensions. However, there are some exceptions:

• The family home may be counted as an asset in determining a bond or charge amount (see below).

• Amounts invested in a 50% Assets Test Exempt income stream (complying annuities and term allocated pensions) are non-commutable. Therefore 100% of the asset value is disregarded in calculating the bond or charge, despite 50% being assessed for social security. This relates to complying income streams purchased prior to 20 September 2007, as these products are now closed to new entrants.

• Superannuation benefits are counted regardless of the person’s age if a condition of release has been met.

When a person is a member of a couple, 50% of the combined assessable assets of the couple are assessed irrespective of the name in which the asset is held.

When an asset assessment is completed before entering a facility, it is based on assets at the time the assessment is undertaken. If completed after entry, it is based on assets at the time of entry.

This can have significant implications for members of a couple in relation to their family home.

Valuing the family home for the bond or chargeThe family home will be included as an asset when determining the bond or charge unless the person satisfies one of the following conditions at the time of assessment:

• the person’s spouse or dependent child is living in the home

• a carer eligible for an income support payment has been living in the home for the past two years

• a close relative who is eligible for an income support payment has been living in the home for the past five years.

The value of the home will be included in the calculation of the bond for the majority of single clients.

For members of a couple, the timing of an asset assessment can result in very different outcomes:

• A couple who both enter care on the same day and submit their asset assessment after they enter care will both have 50% of the value of the home assessed as an asset.

• A couple who enter care on separate days and submit their asset assessment after entry will have the home exempt for the first person to enter and half assessed against the second person.

• If a couple submits their asset assessment form before either one of them vacates the home to enter care, they may wish to consider indicating on the form that their partner lives in the home, generally exempting the home for both.

At first, it may appear that the third option would be the best strategy for a couple requiring care. However, this may at times reduce a couple’s chances of being accepted into the facility of their choice as a result of their lower asset levels. If no bond is paid, there may also be adverse implications for social security where the family home is kept, as we discuss later.

Having the home assessed may significantly impact the amount of bond or charge a person is asked to pay as the home remains the largest asset for many retirees. In addition, people with few assets other than their home could have great difficulty in paying a bond and be forced to sell it, which may in turn impact on social security entitlements. We explore the potential effects of the family home on social security on page 19 and in the case study.

Challenger Aged care guide 13

Sometimes funding the accommodation bond will require a significant change in a person’s financial assets. However, many people do not see a financial adviser until after they have sold their home, paid the bond and moved into the facility. It is important to let your clients know that you can provide assistance on how to fund the bond or look at possible strategies to reduce the bond, determine whether to submit an asset assessment and advise how to invest the proceeds from the sale of the home.

Tip: Including questions on your fact find about the age and health of the client’s parents may alert you to the need for assistance early, and prevent the sometimes unnecessary sale of the family home.

To keep or sell the family home People about to enter care are often concerned about whether they will be forced to sell the family home to fund the accommodation bond. This decision often lies with the children of the person entering care.

Many people don’t realise that there can be social security and aged care advantages to keeping the family home. We discuss this more in the ‘Aged care golden rules’ section.

When deciding what to do with the home, factors to take into account include:

• The money required (if any) to bring the home up to a rental standard.

• The commitment in time and money for ongoing maintenance and repairs – it is most likely the children will be the ones looking after the home.

• Possible capital gains tax consequences if the home is rented for more than six years.

• Land tax – this varies across each state and may apply if the home is rented.

• Tax as a result of rental income received – rental income must be included in assessable income; however, the various offsets such as the low income tax offset, the senior and pensioner tax offset and the net medical expense tax offset (refer to page 32) may apply to reduce some or all of the tax (if any).

Tip: Residents who keep and rent out their family home and pay at least part of their accommodation bond by periodic payment or accrue a liability to pay an accommodation charge will exempt their home from the Centrelink/DVA Assets Test indefinitely. In addition, the rental income will not be assessed for the Centrelink/DVA Income Test or the income-tested fee. See page 19 for more information.

14 Challenger Aged care guide

The ongoing costs

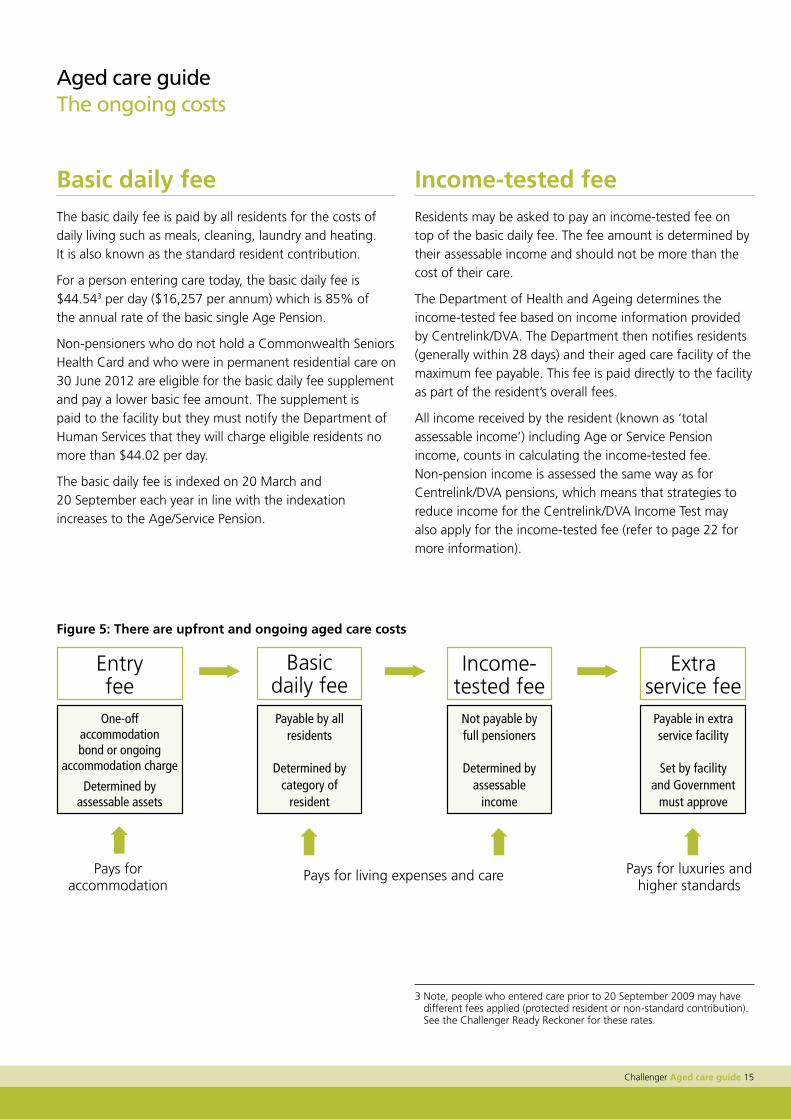

As well as considering upfront costs, your client will need to know their ongoing costs and how they will meet them (Figure 5).

It is important to understand how these fees and charges are applied and how they may be reduced, since they can be costly.

Challenger Aged care guide 15

Aged care guide The ongoing costs

Basic daily feeThe basic daily fee is paid by all residents for the costs of daily living such as meals, cleaning, laundry and heating. It is also known as the standard resident contribution.

For a person entering care today, the basic daily fee is $44.543 per day ($16,257 per annum) which is 85% of the annual rate of the basic single Age Pension.

Non-pensioners who do not hold a Commonwealth Seniors Health Card and who were in permanent residential care on 30 June 2012 are eligible for the basic daily fee supplement and pay a lower basic fee amount. The supplement is paid to the facility but they must notify the Department of Human Services that they will charge eligible residents no more than $44.02 per day.

The basic daily fee is indexed on 20 March and 20 September each year in line with the indexation increases to the Age/Service Pension.

income-tested feeResidents may be asked to pay an income-tested fee on top of the basic daily fee. The fee amount is determined by their assessable income and should not be more than the cost of their care.

The Department of Health and Ageing determines the income-tested fee based on income information provided by Centrelink/DVA. The Department then notifies residents (generally within 28 days) and their aged care facility of the maximum fee payable. This fee is paid directly to the facility as part of the resident’s overall fees.

All income received by the resident (known as ‘total assessable income’) including Age or Service Pension income, counts in calculating the income-tested fee. Non-pension income is assessed the same way as for Centrelink/DVA pensions, which means that strategies to reduce income for the Centrelink/DVA Income Test may also apply for the income-tested fee (refer to page 22 for more information).

3 Note, people who entered care prior to 20 September 2009 may have different fees applied (protected resident or non-standard contribution). See the Challenger Ready Reckoner for these rates.

➡ Basic daily feePayable by all

residents

Determined by category of

resident

Income- tested fee

Not payable by full pensioners

Determined by assessable

income

➡ ➡

Entry fee

One-off accommodation bond or ongoing

accommodation charge

Determined by assessable assets

➡

Pays for accommodation

Pays for living expenses and care

Extra service fee

Payable in extra service facility

Set by facility and Government

must approve

➡

Pays for luxuries and higher standards

Figure 5: There are upfront and ongoing aged care costs

➡ ➡

16 Challenger Aged care guide

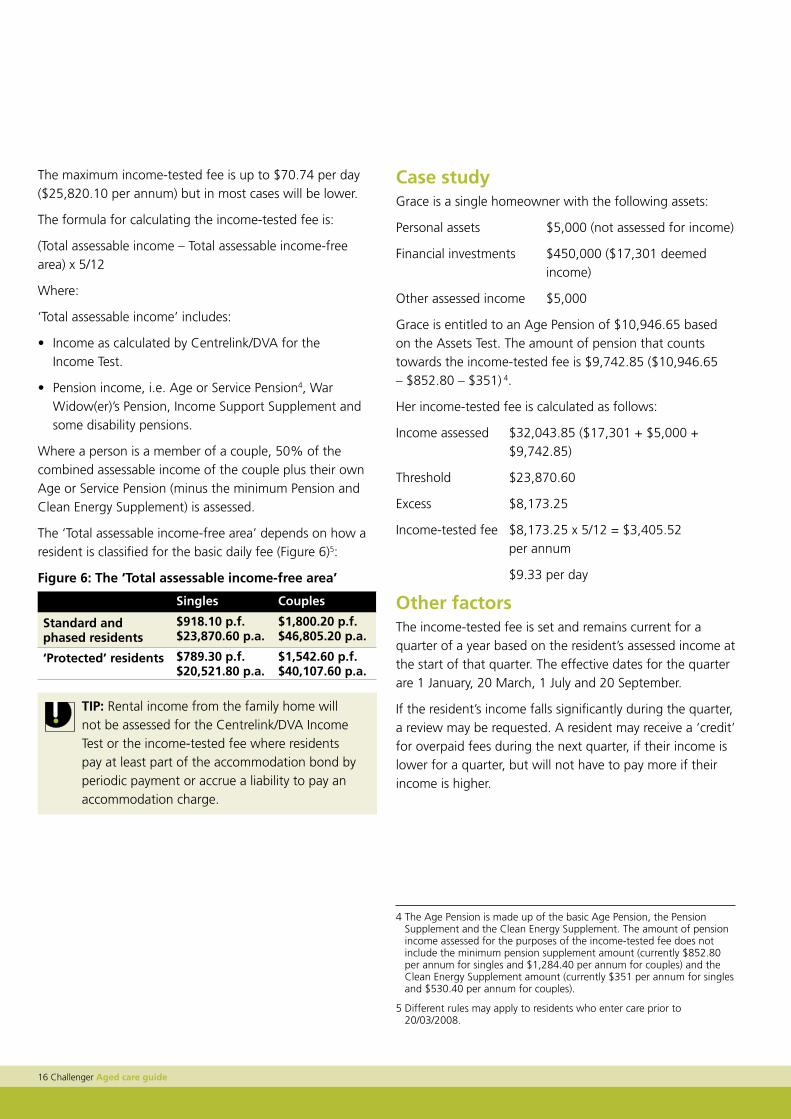

The maximum income-tested fee is up to $70.74 per day ($25,820.10 per annum) but in most cases will be lower.

The formula for calculating the income-tested fee is:

(Total assessable income – Total assessable income-free area) x 5/12

Where:

‘Total assessable income’ includes:

• Income as calculated by Centrelink/DVA for the Income Test.

• Pension income, i.e. Age or Service Pension4, War Widow(er)’s Pension, Income Support Supplement and some disability pensions.

Where a person is a member of a couple, 50% of the combined assessable income of the couple plus their own Age or Service Pension (minus the minimum Pension and Clean Energy Supplement) is assessed.

The ‘Total assessable income-free area’ depends on how a resident is classified for the basic daily fee (Figure 6)5:

Figure 6: The ‘Total assessable income-free area’

Singles Couples

Standard and phased residents

$918.10 p.f. $23,870.60 p.a.

$1,800.20 p.f. $46,805.20 p.a.

‘protected’ residents $789.30 p.f. $20,521.80 p.a.

$1,542.60 p.f. $40,107.60 p.a.

Tip: Rental income from the family home will not be assessed for the Centrelink/DVA Income Test or the income-tested fee where residents pay at least part of the accommodation bond by periodic payment or accrue a liability to pay an accommodation charge.

Case study Grace is a single homeowner with the following assets:

Personal assets $5,000 (not assessed for income)

Financial investments $450,000 ($17,301 deemed income)

Other assessed income $5,000

Grace is entitled to an Age Pension of $10,946.65 based on the Assets Test. The amount of pension that counts towards the income-tested fee is $9,742.85 ($10,946.65 – $852.80 – $351) 4.

Her income-tested fee is calculated as follows:

Income assessed $32,043.85 ($17,301 + $5,000 + $9,742.85)

Threshold $23,870.60

Excess $8,173.25

Income-tested fee $8,173.25 x 5/12 = $3,405.52 per annum

$9.33 per day

Other factorsThe income-tested fee is set and remains current for a quarter of a year based on the resident’s assessed income at the start of that quarter. The effective dates for the quarter are 1 January, 20 March, 1 July and 20 September.

If the resident’s income falls significantly during the quarter, a review may be requested. A resident may receive a ‘credit’ for overpaid fees during the next quarter, if their income is lower for a quarter, but will not have to pay more if their income is higher.

4 The Age Pension is made up of the basic Age Pension, the Pension Supplement and the Clean Energy Supplement. The amount of pension income assessed for the purposes of the income-tested fee does not include the minimum pension supplement amount (currently $852.80 per annum for singles and $1,284.40 per annum for couples) and the Clean Energy Supplement amount (currently $351 per annum for singles and $530.40 per annum for couples).

5 Different rules may apply to residents who enter care prior to 20/03/2008.

Challenger Aged care guide 17

Tip: Most non-pensioners should provide their details to Centrelink/DVA to ensure the correct income-tested fee is applied. They must complete a ‘Residential Aged Care Fee Income Assessment’ form. The maximum income-tested fee may be charged if a non-pensioner fails to provide their details.

Those with income well above the income required to incur the maximum fee do not need to complete the form, as they will be subject to the maximum fee regardless.

Eligibility for some pensions, such as a blind pension, a war widow/widower pension or a veteran’s disability pension or allowance, does not depend on a person’s income; if this is the only pension a person receives they may also have to complete the income assessment form to be charged the correct income-tested fee.

It is important to realise that an aged care facility does not receive any more money from a resident who pays an income-tested fee than one who does not – the income-tested fee simply reduces the funding the facility receives from the Government.

Extra service feeA person can choose to enter an aged care facility that offers extra services. They can enjoy a significantly higher standard of ‘hotel’ type extras in accommodation, food, and services, by paying an extra service fee.

The extra service fee is set by the facility and must be approved by the Department of Health and Ageing. It varies from one facility to another depending on the services being provided.

There is no cap on the additional fee that can be charged, so residents must be happy that the additional service warrants the cost. Facilities that offer extra services for high care residents can ask for an accommodation bond instead of an accommodation charge.

Tip: Your client may be able to negotiate a lower extra service fee in exchange for a higher accommodation bond. See page 20 for more on this strategy.

18 Challenger Aged care guide

Aged care golden rules

There are many factors to consider when moving to residential aged care and we believe the following three golden rules will assist you to help clients through the aged care process:

• evaluate whether to keep the family home

• weigh up the benefits of negotiating a higher accommodation bond

• invest for cash flow.

Challenger Aged care guide 19

Aged care guide Aged care golden rules

Evaluate whether to keep the family home

OverviewThe fate of the family home is often the decision with the greatest impact on social security. There may be significant advantages to keeping the home – in some cases it can result in a higher social security entitlement and lower income-tested fees.

StrategiesWhen a member of a couple enters an aged care facility, the family home will continue to be exempt from the Assets Test indefinitely as long as their spouse continues to live in the home.

If both members of a couple enter a facility or the resident is a single pensioner, Centrelink/DVA will continue to treat the family home as the principal place of residence for two years from the date the last person leaves the home. This means that all residents who keep their family home have at least a two-year exemption from the Centrelink/DVA Assets Test. When the two-year period has ended, the resident is considered a non-homeowner and the market value of the home becomes assessable for the Assets Test.

Using the home to extend social security means test exemptions Keeping and renting out the family home can extend the two-year exemption from the Centrelink/DVA Assets and Income Tests for:

• People who are entering a high level care facility and paying, or accruing a liability to pay, an accommodation charge. The home remains the principal residence indefinitely while these conditions apply, and is exempt from the Assets Test and rental income will not be assessed for the Income Test.

• People who are entering a low level care or extra service facility and who pay at least part of their accommodation bond by periodic payments. The home remains the principal residence and is exempt from the Assets Test and rental income will not be assessed for the Income Test unless the outstanding bond lump sum is paid to the facility.

Tip: Planning opportunities arise for your clients who can pay most of the accommodation bond by lump sum and a minimal amount via periodic payment. As long as they are renting out the family home, it will remain exempt from the Centrelink/DVA Assets and Income tests.

If the resident sells the home when they enter the facility, the proceeds are counted as an asset when they are received and they are assessed as a non-homeowner.

Other tips regarding the homeWhen renting out the family home, there is no test to check that the amount of rent is of market value. This means that the home may be rented to a family member for an amount that is well below the market rate. It is important to note, however, that there may be tax implications for receiving below market rate rents.

While the home is exempt, the resident is subject to ‘homeowner’ Assets Test thresholds. This exemption provides a great benefit for residents on Centrelink/DVA benefits as they may continue to receive the same level of Age or Service Pension (if not more) after moving into a facility while maintaining what may be their biggest asset. The option of keeping the home should always be explored first.

Beware of the trapsIf a person pays an accommodation bond by lump sum in full, any rental income from the home will count towards the Centrelink/DVA Income Test and the income-tested fee for the whole time the home is rented, and the home will count as an asset two years after they move into an aged care facility.

Also, if a person does not pay an accommodation bond or charge (as their assets are too low), they will only receive a maximum two-year exemption from the Centrelink/DVA Assets Test on the home as they do not meet both conditions above. Any rental income will also count towards the Centrelink/DVA Income Test and the income-tested fee.

Tip: For your clients with assets below $43,000 wishing to keep the family home, it may be better to negotiate a bond or charge without an asset assessment to enable them to qualify for an indefinite exemption.

20 Challenger Aged care guide

Moving from a retirement village or a granny flatThere may be occasions where your client has moved to a retirement village or had a granny flat arrangement prior to moving to an aged care facility. Here we outline the implications of this move for the family home.

Moving from a retirement village Planning opportunities are more limited when a person moves from a retirement village to an aged care facility as they generally need to sell the unit and cannot take advantage of the exemption rules that apply when keeping and renting the family home. Even if a person has kept their home after moving to a retirement village, the home cannot receive the exemption unless they live in the home right before moving to the facility. This means that the proceeds from the sale of the retirement village unit are counted as an asset when they are received and the resident is assessed as a non-homeowner.

Moving from a granny flat For social security and aged care purposes, a granny flat right or interest is a formal or informal arrangement that provides a person with a life interest in accommodation, or right to accommodation for life, upon the transfer of the legal title to their home. The granny flat rules enable a person to transfer assets without exceeding the gifting limits (currently $10,000 per financial year and $30,000 over a five-year period).

A key requirement of a granny flat arrangement is that the person with the life interest must not have any legal ownership over their home. This means if they eventually move to an aged care facility, the value of the home will not be included as an asset in determining the accommodation bond or charge.

An exception to this is if the person moves to an aged care facility within five years of creating the interest as Centrelink/DVA will apply the gifting rules if they believe the move could have been anticipated. If a person is in good health when they create the granny flat interest, however, the gifting rules are unlikely to apply regardless of the five-year rule. Creating a granny flat interest can be an effective way of reducing a future accommodation bond amount if planned well in advance.

There are some traps to be aware of including potential capital gains tax implications, stamp duty on transfer and estate planning considerations.

Weigh up the benefits of negotiating a higher accommodation bond

OverviewMany facilities are willing to negotiate lower ongoing costs in exchange for a higher accommodation bond. The discount is usually a percentage of the additional bond paid, for example, a 3% per annum discount on fees for any additional bond paid. Or they may agree to waive part or all of a fee such as the retention amount or extra service fees (if in an extra service facility).

However, facilities are not required to offer any discount on fees so the benefit will depend on the value the facility places on having the extra capital.

StrategiesIf your client’s Age or Service Pension is reduced by the Assets Test, negotiating a higher accommodation bond could increase their entitlement as the bond is Assets and Income Test exempt. This could also reduce their income-tested fees. This combination of benefits can significantly enhance the discount offered by the facility.

Tips and traps The benefit offered by this strategy may vary significantly depending on a person’s situation. The total return for those with assets well above the Assets Test, for example, will be less than those with assets just above or below the Assets Test cut-out thresholds as there may be no social security benefit.

It is also possible to pay too much bond if a person’s Age or Service Pension is no longer increasing as they are below the Assets Test reduction threshold.

It is important to look at each case individually and calculate the total return offered by the strategy versus having the funds invested elsewhere. Consideration must also be given to the fact that the person has no access to the additional bond paid while they are a resident of the facility.

We explore the strategy of paying a higher accommodation bond in the case study on page 27.

Challenger Aged care guide 21

invest for cash flowAs we’ve discussed, the option of keeping the family home should always be considered first. There are many cases, however, where the resident has sold the home prior to seeing a financial planner or is unable to keep the home. They may need to sell the home to fund an accommodation bond, for example, or may not want the burden of maintaining the home.

The effect of the sale proceeds on a resident’s aged care costs and Age or Service Pension depends on how they are invested. Even when the home is kept, the resident may have financial assets that could be invested in a better way.

The appropriate investment strategy will probably depend on which of the following goals are most important to your clients:

• eliminate or reduce income-tested aged care costs

• be Age/Service Pension friendly

• provide eligibility for the Seniors Card

• minimise Centrelink/DVA paperwork

• provide tax-effective income for seniors

• provide a known death benefit

• provide cash flow to pay costs.

StrategiesFinancial investmentsFrom a social security perspective, financial investments include cash, shares, deprived assets and short-term assets-tested income streams (with a term of five years or less).

Leaving money in a bank account or term deposit is often the default position for the elderly, because these types of investments are easily understood and are broadly considered to be safe investments.

The market value of financial investments is assessed under the Centrelink/DVA Assets Test.

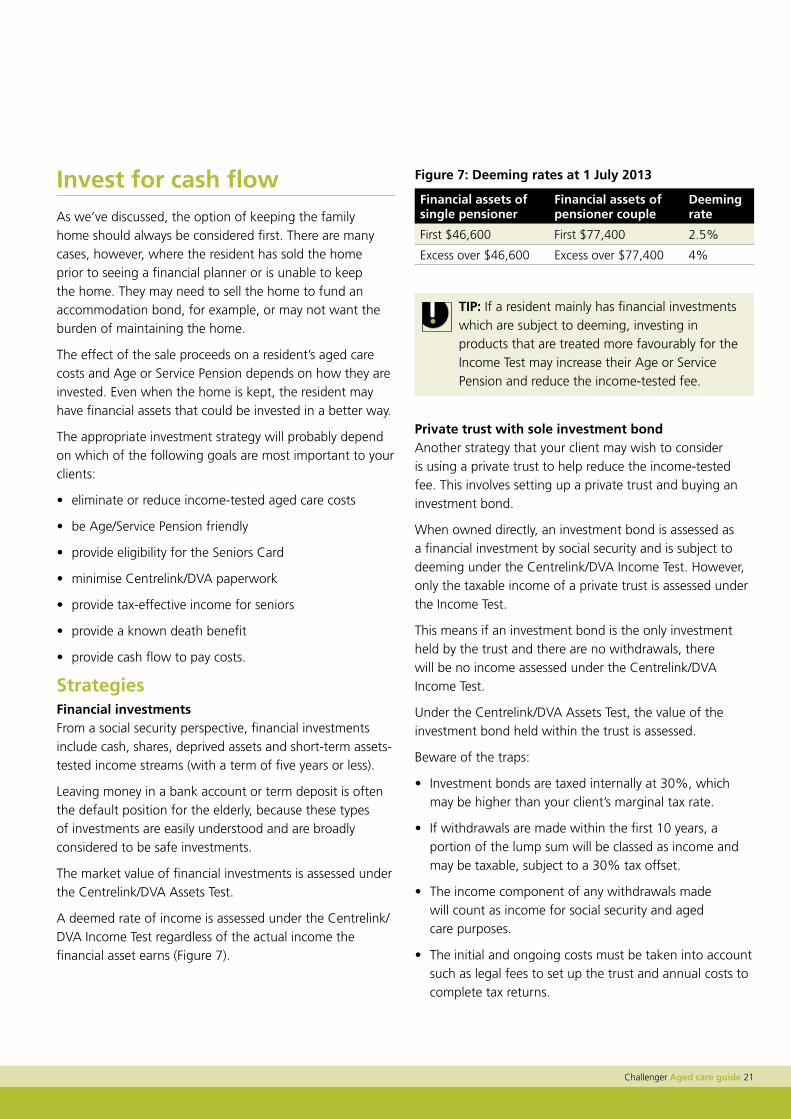

A deemed rate of income is assessed under the Centrelink/DVA Income Test regardless of the actual income the financial asset earns (Figure 7).

Figure 7: Deeming rates at 1 July 2013

Financial assets of single pensioner

Financial assets of pensioner couple

Deeming rate

First $46,600 First $77,400 2.5%

Excess over $46,600 Excess over $77,400 4%

Tip: If a resident mainly has financial investments which are subject to deeming, investing in products that are treated more favourably for the Income Test may increase their Age or Service Pension and reduce the income-tested fee.

private trust with sole investment bondAnother strategy that your client may wish to consider is using a private trust to help reduce the income-tested fee. This involves setting up a private trust and buying an investment bond.

When owned directly, an investment bond is assessed as a financial investment by social security and is subject to deeming under the Centrelink/DVA Income Test. However, only the taxable income of a private trust is assessed under the Income Test.

This means if an investment bond is the only investment held by the trust and there are no withdrawals, there will be no income assessed under the Centrelink/DVA Income Test.

Under the Centrelink/DVA Assets Test, the value of the investment bond held within the trust is assessed.

Beware of the traps:

• Investment bonds are taxed internally at 30%, which may be higher than your client’s marginal tax rate.

• If withdrawals are made within the first 10 years, a portion of the lump sum will be classed as income and may be taxable, subject to a 30% tax offset.

• The income component of any withdrawals made will count as income for social security and aged care purposes.

• The initial and ongoing costs must be taken into account such as legal fees to set up the trust and annual costs to complete tax returns.

22 Challenger Aged care guide

• Enough funds must be left outside the bond/trust structure to cover ongoing costs.

• The Centrelink/DVA paperwork required for trusts structures is quite complex and onerous.

Nil residual capital value (RCV) term annuitiesTerm annuities provide regular and known cash flow for the set term, which can be used to cover ongoing aged care costs. However, the factors outlined below must be taken into account.

Long-term annuities receive favourable Income Test treatment for social security and aged care purposes as a result of the deductible amount. To be classed as long term, annuities must have a term of at least six years (or life expectancy rounded up if it is less than five years).

Income paid from the annuity, less the deductible amount, is assessed under the Centrelink/DVA Income Test. The deductible amount is calculated as purchase price divided by the term, and reduces the income assessed for the term of the annuity.

The purchase price of the annuity is assessed under the Centrelink/DVA Assets Test when it is purchased. The asset value of the annuity, however, reduces by the deductible amount each year.

Beware of the traps:

• The amount payable upon death is unknown and may be less than the purchase price minus payments received.

• It’s also important to remember that there are early break costs upon voluntary withdrawal.

Challenger Care AnnuityThe Challenger Care Annuity (Care Annuity) is a lifetime annuity available for people who have been approved by an Aged Care Assessment Team (ACAT) as needing low level or high level residential care.

The Care Annuity is structured to provide a 100% death benefit in first 10 years and a 100% withdrawal value at end of 10 years, providing estate planning certainty for beneficiaries.

Lifetime annuities receive favourable Income Test treatment for social security and aged care purposes as a result of the deductible amount.

Income paid from the annuity less the deductible amount is assessed under the Centrelink/DVA Income Test. The deductible amount is calculated as purchase price divided by life expectancy and reduces the income assessed for the life of the annuity.

As the majority of people entering care are aged over 80, the deductible amount is generally greater than the income payments received, resulting in no income being assessed under the Centrelink/DVA Income Test.

The purchase price of the annuity is assessed under the Centrelink/DVA Assets Test when it is purchased. The asset value of the annuity, however, reduces by the deductible amount each year and ceases to have an asset value if the person lives past their life expectancy.

Beware of the traps:

• The Care Annuity can only be withdrawn during the first 10 years; however, this is subject to any applicable early break costs. Any lump sum payable upon death or voluntary withdrawal during this period will be made up of income and capital. For more information, please refer to the Challenger Care Annuity guide and the product disclosure statement (PDS). A copy of the PDS can be obtained from www.challenger.com.au.

Challenger Aged care guide 23

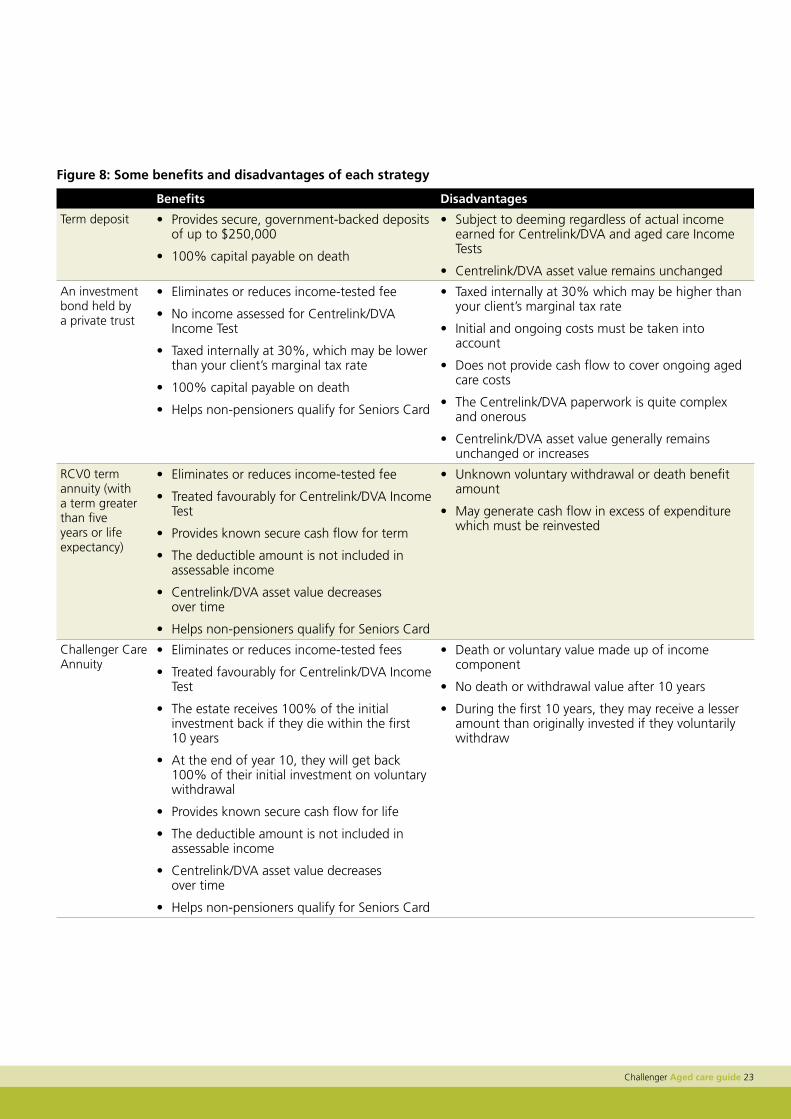

Figure 8: Some benefits and disadvantages of each strategy

Benefits Disadvantages

Term deposit • Provides secure, government-backed deposits of up to $250,000

• 100% capital payable on death

• Subject to deeming regardless of actual income earned for Centrelink/DVA and aged care Income Tests

• Centrelink/DVA asset value remains unchanged

An investment bond held by a private trust

• Eliminates or reduces income-tested fee

• No income assessed for Centrelink/DVA Income Test

• Taxed internally at 30%, which may be lower than your client’s marginal tax rate

• 100% capital payable on death

• Helps non-pensioners qualify for Seniors Card

• Taxed internally at 30% which may be higher than your client’s marginal tax rate

• Initial and ongoing costs must be taken into account

• Does not provide cash flow to cover ongoing aged care costs

• The Centrelink/DVA paperwork is quite complex and onerous

• Centrelink/DVA asset value generally remains unchanged or increases

RCV0 term annuity (with a term greater than five years or life expectancy)

• Eliminates or reduces income-tested fee

• Treated favourably for Centrelink/DVA Income Test

• Provides known secure cash flow for term

• The deductible amount is not included in assessable income

• Centrelink/DVA asset value decreases over time

• Helps non-pensioners qualify for Seniors Card

• Unknown voluntary withdrawal or death benefit amount

• May generate cash flow in excess of expenditure which must be reinvested

Challenger Care Annuity

• Eliminates or reduces income-tested fees

• Treated favourably for Centrelink/DVA Income Test

• The estate receives 100% of the initial investment back if they die within the first 10 years

• At the end of year 10, they will get back 100% of their initial investment on voluntary withdrawal

• Provides known secure cash flow for life

• The deductible amount is not included in assessable income

• Centrelink/DVA asset value decreases over time

• Helps non-pensioners qualify for Seniors Card

• Death or voluntary value made up of income component

• No death or withdrawal value after 10 years

• During the first 10 years, they may receive a lesser amount than originally invested if they voluntarily withdraw

24 Challenger Aged care guide

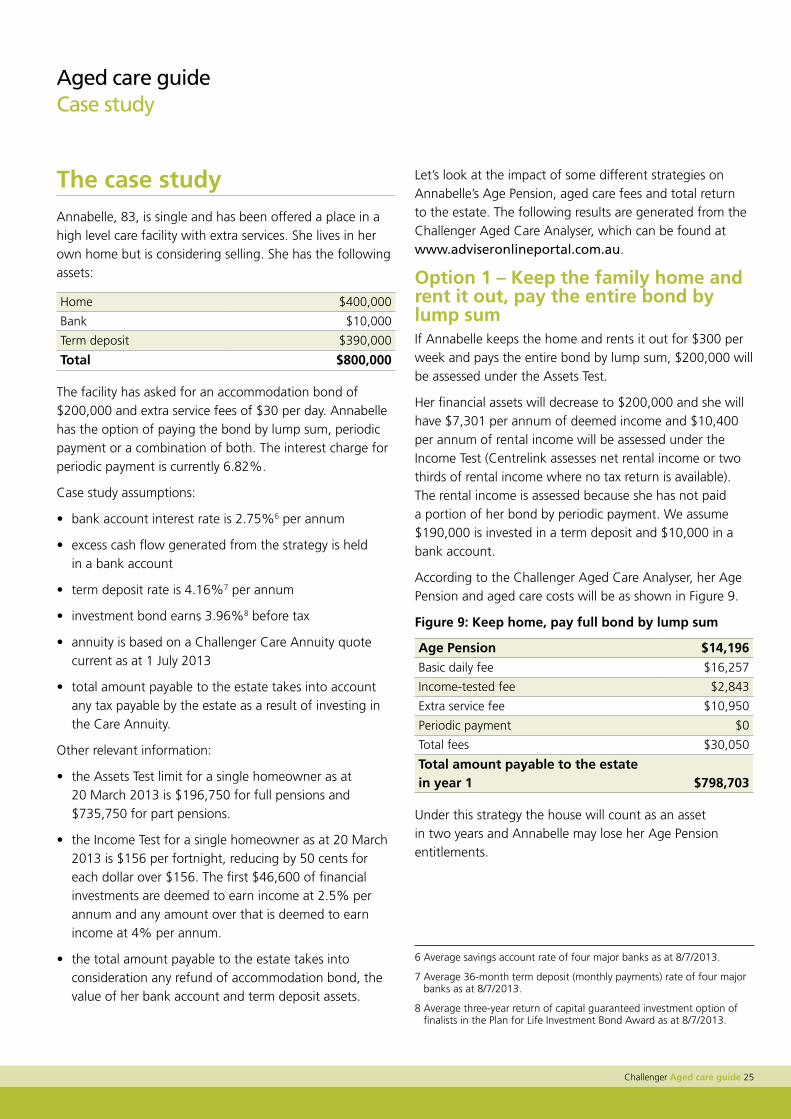

This case study shows that different types of investments can reduce the aged care costs that your client pays and maximise their social security entitlements.

Case study

Challenger Aged care guide 25

Aged care guide Case study

The case studyAnnabelle, 83, is single and has been offered a place in a high level care facility with extra services. She lives in her own home but is considering selling. She has the following assets:

Home $400,000

Bank $10,000

Term deposit $390,000

Total $800,000

The facility has asked for an accommodation bond of $200,000 and extra service fees of $30 per day. Annabelle has the option of paying the bond by lump sum, periodic payment or a combination of both. The interest charge for periodic payment is currently 6.82%.

Case study assumptions:

• bank account interest rate is 2.75%6 per annum

• excess cash flow generated from the strategy is held in a bank account

• term deposit rate is 4.16%7 per annum

• investment bond earns 3.96%8 before tax

• annuity is based on a Challenger Care Annuity quote current as at 1 July 2013

• total amount payable to the estate takes into account any tax payable by the estate as a result of investing in the Care Annuity.

Other relevant information:

• the Assets Test limit for a single homeowner as at 20 March 2013 is $196,750 for full pensions and $735,750 for part pensions.

• the Income Test for a single homeowner as at 20 March 2013 is $156 per fortnight, reducing by 50 cents for each dollar over $156. The first $46,600 of financial investments are deemed to earn income at 2.5% per annum and any amount over that is deemed to earn income at 4% per annum.

• the total amount payable to the estate takes into consideration any refund of accommodation bond, the value of her bank account and term deposit assets.

Let’s look at the impact of some different strategies on Annabelle’s Age Pension, aged care fees and total return to the estate. The following results are generated from the Challenger Aged Care Analyser, which can be found at www.adviseronlineportal.com.au.

Option 1 – Keep the family home and rent it out, pay the entire bond by lump sumIf Annabelle keeps the home and rents it out for $300 per week and pays the entire bond by lump sum, $200,000 will be assessed under the Assets Test.

Her financial assets will decrease to $200,000 and she will have $7,301 per annum of deemed income and $10,400 per annum of rental income will be assessed under the Income Test (Centrelink assesses net rental income or two thirds of rental income where no tax return is available). The rental income is assessed because she has not paid a portion of her bond by periodic payment. We assume $190,000 is invested in a term deposit and $10,000 in a bank account.

According to the Challenger Aged Care Analyser, her Age Pension and aged care costs will be as shown in Figure 9.

Figure 9: Keep home, pay full bond by lump sum

Age pension $14,196

Basic daily fee $16,257

Income-tested fee $2,843

Extra service fee $10,950

Periodic payment $0

Total fees $30,050

Total amount payable to the estate in year 1 $798,703

Under this strategy the house will count as an asset in two years and Annabelle may lose her Age Pension entitlements.

6 Average savings account rate of four major banks as at 8/7/2013.

7 Average 36-month term deposit (monthly payments) rate of four major banks as at 8/7/2013.

8 Average three-year return of capital guaranteed investment option of finalists in the Plan for Life Investment Bond Award as at 8/7/2013.

26 Challenger Aged care guide

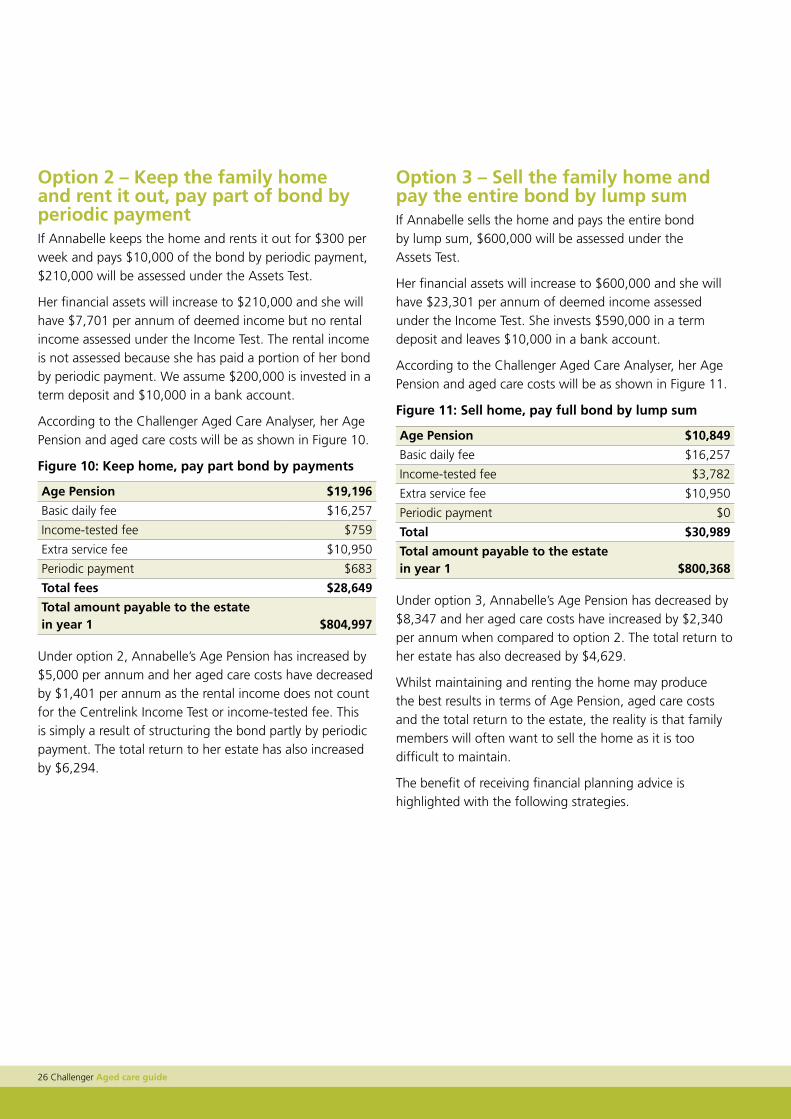

Option 2 – Keep the family home and rent it out, pay part of bond by periodic paymentIf Annabelle keeps the home and rents it out for $300 per week and pays $10,000 of the bond by periodic payment, $210,000 will be assessed under the Assets Test.

Her financial assets will increase to $210,000 and she will have $7,701 per annum of deemed income but no rental income assessed under the Income Test. The rental income is not assessed because she has paid a portion of her bond by periodic payment. We assume $200,000 is invested in a term deposit and $10,000 in a bank account.

According to the Challenger Aged Care Analyser, her Age Pension and aged care costs will be as shown in Figure 10.

Figure 10: Keep home, pay part bond by payments

Age pension $19,196

Basic daily fee $16,257

Income-tested fee $759

Extra service fee $10,950

Periodic payment $683

Total fees $28,649

Total amount payable to the estate in year 1 $804,997

Under option 2, Annabelle’s Age Pension has increased by $5,000 per annum and her aged care costs have decreased by $1,401 per annum as the rental income does not count for the Centrelink Income Test or income-tested fee. This is simply a result of structuring the bond partly by periodic payment. The total return to her estate has also increased by $6,294.

Option 3 – Sell the family home and pay the entire bond by lump sumIf Annabelle sells the home and pays the entire bond by lump sum, $600,000 will be assessed under the Assets Test.

Her financial assets will increase to $600,000 and she will have $23,301 per annum of deemed income assessed under the Income Test. She invests $590,000 in a term deposit and leaves $10,000 in a bank account.

According to the Challenger Aged Care Analyser, her Age Pension and aged care costs will be as shown in Figure 11.

Figure 11: Sell home, pay full bond by lump sum

Age pension $10,849

Basic daily fee $16,257

Income-tested fee $3,782

Extra service fee $10,950

Periodic payment $0

Total $30,989

Total amount payable to the estate in year 1 $800,368

Under option 3, Annabelle’s Age Pension has decreased by $8,347 and her aged care costs have increased by $2,340 per annum when compared to option 2. The total return to her estate has also decreased by $4,629.

Whilst maintaining and renting the home may produce the best results in terms of Age Pension, aged care costs and the total return to the estate, the reality is that family members will often want to sell the home as it is too difficult to maintain.

The benefit of receiving financial planning advice is highlighted with the following strategies.

Challenger Aged care guide 27

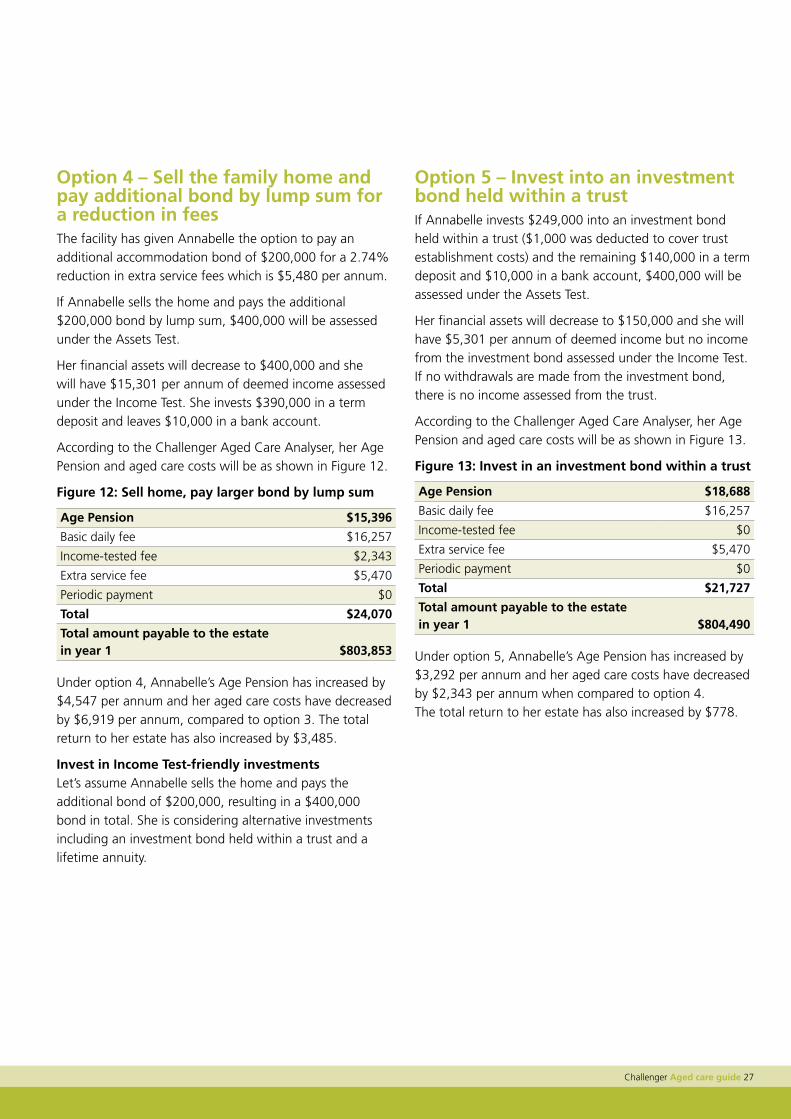

Option 4 – Sell the family home and pay additional bond by lump sum for a reduction in feesThe facility has given Annabelle the option to pay an additional accommodation bond of $200,000 for a 2.74% reduction in extra service fees which is $5,480 per annum.

If Annabelle sells the home and pays the additional $200,000 bond by lump sum, $400,000 will be assessed under the Assets Test.

Her financial assets will decrease to $400,000 and she will have $15,301 per annum of deemed income assessed under the Income Test. She invests $390,000 in a term deposit and leaves $10,000 in a bank account.

According to the Challenger Aged Care Analyser, her Age Pension and aged care costs will be as shown in Figure 12.

Figure 12: Sell home, pay larger bond by lump sum

Age pension $15,396

Basic daily fee $16,257

Income-tested fee $2,343

Extra service fee $5,470

Periodic payment $0

Total $24,070

Total amount payable to the estate in year 1 $803,853

Under option 4, Annabelle’s Age Pension has increased by $4,547 per annum and her aged care costs have decreased by $6,919 per annum, compared to option 3. The total return to her estate has also increased by $3,485.

invest in income Test-friendly investmentsLet’s assume Annabelle sells the home and pays the additional bond of $200,000, resulting in a $400,000 bond in total. She is considering alternative investments including an investment bond held within a trust and a lifetime annuity.

Option 5 – invest into an investment bond held within a trustIf Annabelle invests $249,000 into an investment bond held within a trust ($1,000 was deducted to cover trust establishment costs) and the remaining $140,000 in a term deposit and $10,000 in a bank account, $400,000 will be assessed under the Assets Test.

Her financial assets will decrease to $150,000 and she will have $5,301 per annum of deemed income but no income from the investment bond assessed under the Income Test. If no withdrawals are made from the investment bond, there is no income assessed from the trust.

According to the Challenger Aged Care Analyser, her Age Pension and aged care costs will be as shown in Figure 13.

Figure 13: invest in an investment bond within a trust

Age pension $18,688

Basic daily fee $16,257

Income-tested fee $0

Extra service fee $5,470

Periodic payment $0

Total $21,727

Total amount payable to the estate in year 1 $804,490

Under option 5, Annabelle’s Age Pension has increased by $3,292 per annum and her aged care costs have decreased by $2,343 per annum when compared to option 4. The total return to her estate has also increased by $778.

28 Challenger Aged care guide

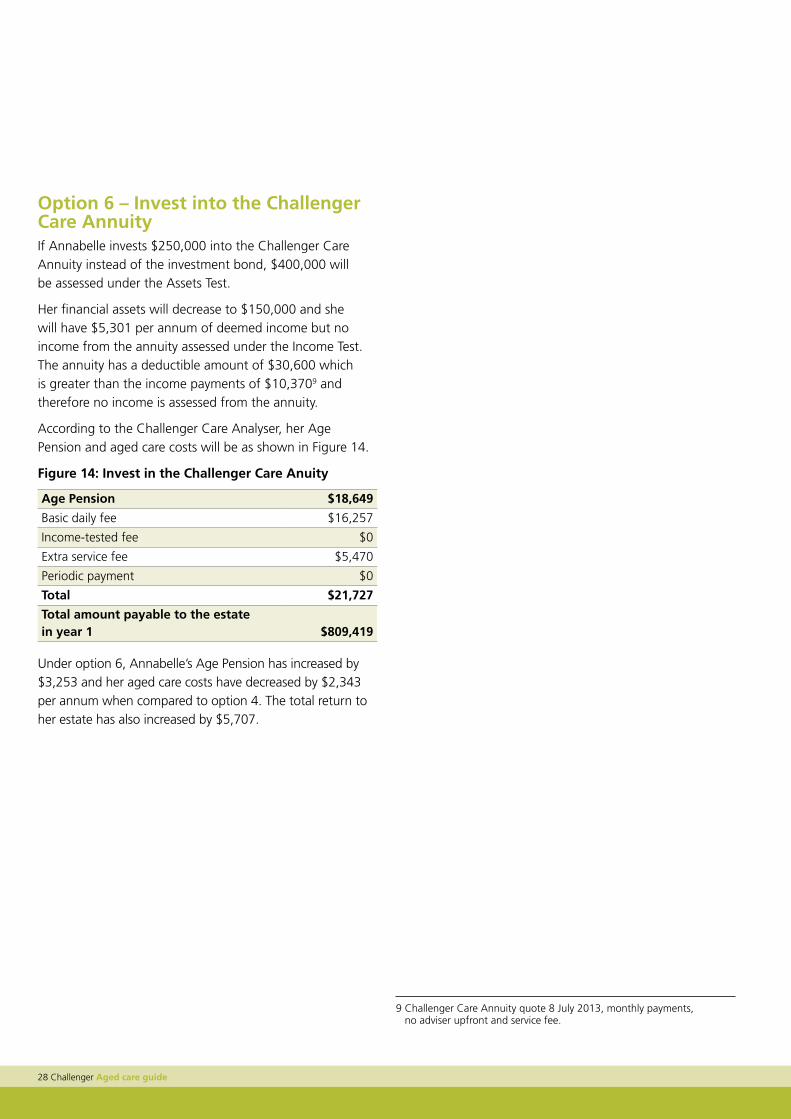

Option 6 – invest into the Challenger Care AnnuityIf Annabelle invests $250,000 into the Challenger Care Annuity instead of the investment bond, $400,000 will be assessed under the Assets Test.

Her financial assets will decrease to $150,000 and she will have $5,301 per annum of deemed income but no income from the annuity assessed under the Income Test. The annuity has a deductible amount of $30,600 which is greater than the income payments of $10,3709 and therefore no income is assessed from the annuity.

According to the Challenger Care Analyser, her Age Pension and aged care costs will be as shown in Figure 14.

Figure 14: invest in the Challenger Care Anuity

Age pension $18,649

Basic daily fee $16,257

Income-tested fee $0

Extra service fee $5,470

Periodic payment $0

Total $21,727

Total amount payable to the estate in year 1 $809,419

Under option 6, Annabelle’s Age Pension has increased by $3,253 and her aged care costs have decreased by $2,343 per annum when compared to option 4. The total return to her estate has also increased by $5,707.

9 Challenger Care Annuity quote 8 July 2013, monthly payments, no adviser upfront and service fee.

Challenger Aged care guide 29

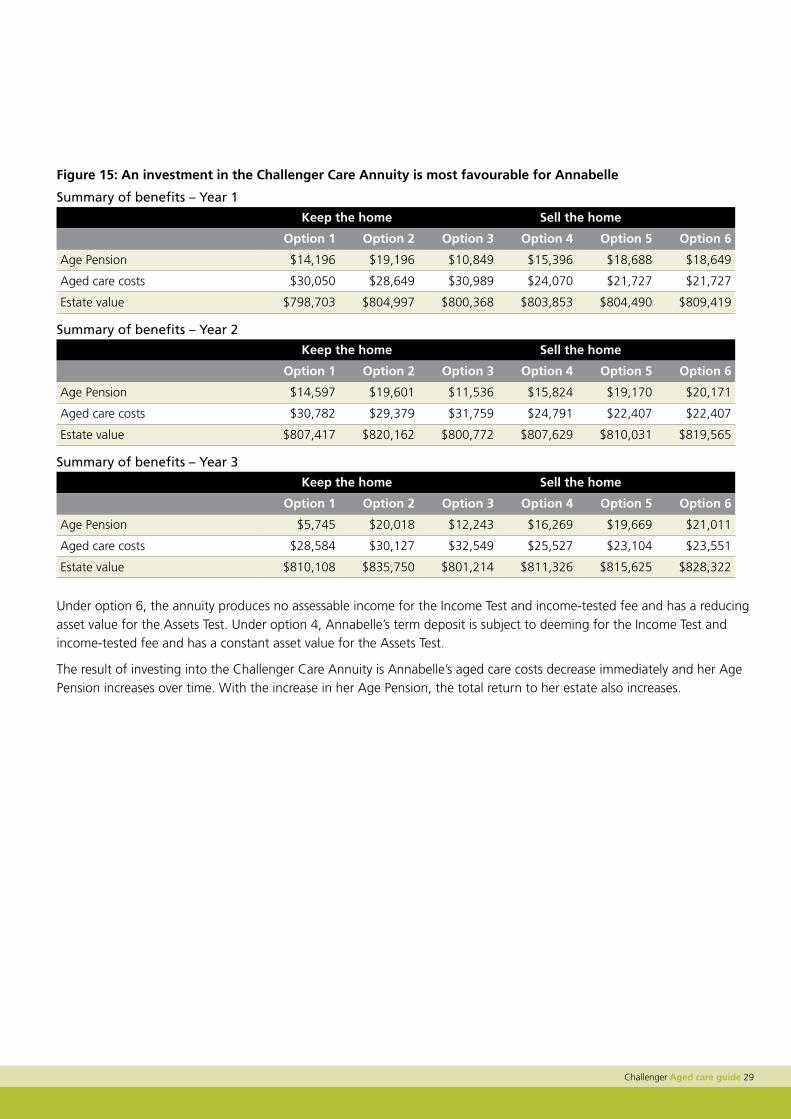

Figure 15: An investment in the Challenger Care Annuity is most favourable for Annabelle

Summary of benefits – Year 1

Keep the home Sell the home

Option 1 Option 2 Option 3 Option 4 Option 5 Option 6

Age Pension $14,196 $19,196 $10,849 $15,396 $18,688 $18,649

Aged care costs $30,050 $28,649 $30,989 $24,070 $21,727 $21,727

Estate value $798,703 $804,997 $800,368 $803,853 $804,490 $809,419

Summary of benefits – Year 2

Keep the home Sell the home

Option 1 Option 2 Option 3 Option 4 Option 5 Option 6

Age Pension $14,597 $19,601 $11,536 $15,824 $19,170 $20,171

Aged care costs $30,782 $29,379 $31,759 $24,791 $22,407 $22,407

Estate value $807,417 $820,162 $800,772 $807,629 $810,031 $819,565

Summary of benefits – Year 3

Keep the home Sell the home

Option 1 Option 2 Option 3 Option 4 Option 5 Option 6

Age Pension $5,745 $20,018 $12,243 $16,269 $19,669 $21,011

Aged care costs $28,584 $30,127 $32,549 $25,527 $23,104 $23,551

Estate value $810,108 $835,750 $801,214 $811,326 $815,625 $828,322

Under option 6, the annuity produces no assessable income for the Income Test and income-tested fee and has a reducing asset value for the Assets Test. Under option 4, Annabelle’s term deposit is subject to deeming for the Income Test and income-tested fee and has a constant asset value for the Assets Test.

The result of investing into the Challenger Care Annuity is Annabelle’s aged care costs decrease immediately and her Age Pension increases over time. With the increase in her Age Pension, the total return to her estate also increases.

30 Challenger Aged care guide

Other factors to consider

On 20 April 2012, the Government released its response to the Productivity Commission’s Inquiry into Caring for Older Australians and is committed to reforming the existing aged care system under the ‘Living Longer. Living Better – aged care reform package’. The majority of reforms are set to commence from 1 July 2014 and legislation outlining major amendments to the Aged Care Act 1997 received Royal assent on 28 June 2013.

Challenger Aged care guide 31

Aged care guide Other factors to consider

Aged care reformsSome of the measures outlined in the changes include:

• Removing the distinction between high care and low care providers.

• Everyone with assets above the relevant threshold will be required to pay a bond, or ‘accommodation payment’, either as a lump sum, periodic payments or a combination of the two. Providers will not be allowed to choose between people on the basis of how that person intends to pay for their accommodation and residents will have 28 days after they have entered care to decide how they will pay.

• A new means test for care fees which will replace the income-tested fee that takes into account a person’s income and assets above certain thresholds. The income-tested fee currently only takes into account the resident’s income. There will be an annual cap of $25,000 and lifetime cap of $60,000. This fee will be in addition to the daily basic fee and accommodation payment.

• All existing community aged care packages (Community Aged Care Packages and Extended Aged Care at Home) will be consolidated into a single program known as ‘Home Care’ packages. From 1 July 2014, older Australians may be asked to contribute to the costs of their care via a means tested Care Fee and this will be paid in addition to the Basic Fee which is currently charged.

The changes will not affect residents already in a facility as of 1 July 2014 and they will continue to be assessed under current rules.

We will provide a more detailed summary and analysis of the changes in the coming months.

Tip: The changes may result in an even bigger opportunity for financial advisers with home care packages being income tested from 1 July 2014 so it’s important to prepare for them early.

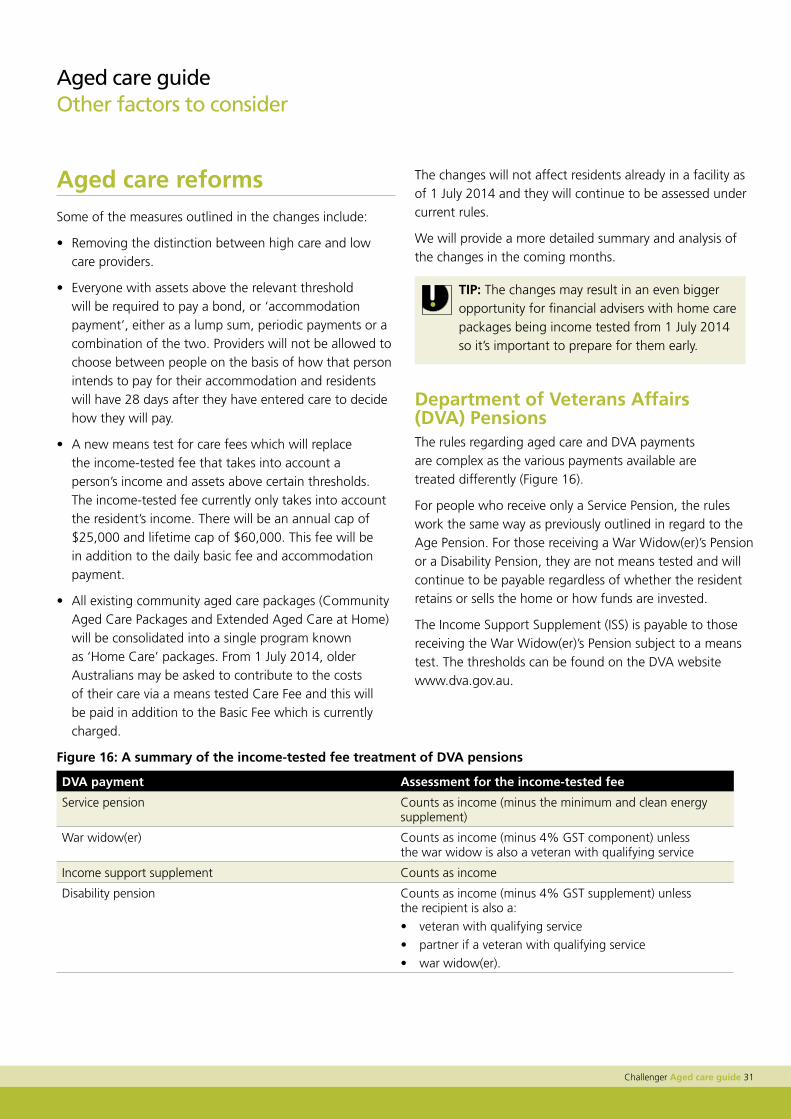

Department of Veterans Affairs (DVA) pensionsThe rules regarding aged care and DVA payments are complex as the various payments available are treated differently (Figure 16).

For people who receive only a Service Pension, the rules work the same way as previously outlined in regard to the Age Pension. For those receiving a War Widow(er)’s Pension or a Disability Pension, they are not means tested and will continue to be payable regardless of whether the resident retains or sells the home or how funds are invested.

The Income Support Supplement (ISS) is payable to those receiving the War Widow(er)’s Pension subject to a means test. The thresholds can be found on the DVA website www.dva.gov.au.

Figure 16: A summary of the income-tested fee treatment of DVA pensions

DVA payment Assessment for the income-tested fee

Service pension Counts as income (minus the minimum and clean energy supplement)

War widow(er) Counts as income (minus 4% GST component) unless the war widow is also a veteran with qualifying service

Income support supplement Counts as income

Disability pension Counts as income (minus 4% GST supplement) unless the recipient is also a:

• veteran with qualifying service

• partner if a veteran with qualifying service

• war widow(er).

32 Challenger Aged care guide

illness separated rateA couple separated by illness may be eligible for a higher rate of Age Pension. A couple is ‘separated by illness’ when one or both members move into residential aged care.

Couples in this situation will be assessed jointly under the Income and Assets Tests, but each member of the couple is eligible for the single Age Pension rate including Pension Supplement. Currently, the maximum combined annual rate for an illness separated couple is $42,036.80 per annum.

The cut-out threshold for the Assets Test increases to approximately $1,357,000 for homeowners and $1,499,500 for non-homeowners. The cut-out threshold for the Income Test increases to approximately $91,249.60 per annum.

Net medical expenses tax offsetThe government has proposed to phase out the net medical expense tax offset (NMETO) from 1 July 2013 with transitional rules for those currently claiming the offset. Importantly, the NMETO will continue to be available for out of pocket net medical expenses relating to aged care until 1 July 2019.

Also, from 1 July 2013 the net medical expense tax offset is proposed to be means tested such that a tax offset of 20% is available for taxpayers who have adjusted taxable income of $84,000 or below ($168,000 for couples) and have net medical expenses over $2,120 (2012-2013). Taxpayers with adjusted taxable income above these thresholds can claim a tax offset of 10% for net medical expenses above $5,000. These thresholds are indexed annually in line with the Consumer Price Index (CPI) and there is no upper limit of what can be claimed.

The proposed means test for the net medical expense tax offset is yet to be legislated; however, a Bill has been introduced into Parliament.

The offset is available for residents if their fees are payable to an approved care provider and cover personal or nursing care and not just accommodation. Fees that are considered medical expenses include:

• daily fees and income-tested fees

• accommodation charges

• periodic payments of accommodation bonds

• amounts retained from lump sum accommodation bond

• extra service fees.

Estate planningIt is important to ensure that appropriate legal documents such as Enduring Powers of Attorney (POA) and Enduring Powers of Guardianship are in place for situations where your client loses mental capacity. Wills should also be reviewed to ensure that ownership of assets is passed on to the intended beneficiary.

Challenger Aged care guide 33

Learn more

Challenger has a range of tools to help you work through aged care issues with clients: • ‘Aged care – what you need to know’, a flyer providing

a step-by-step approach to planning aged care with tips on where to find answers.

• ‘Managing aged care fees’, a case study comparing three strategies for someone entering aged care.

• The Challenger ‘Ready Reckoner’ is a quick reference guide displaying the latest Centrelink, tax and superannuation rates and thresholds.

• The ‘Challenger Care Annuity Adviser Guide’ provides a summary of the Care Annuity and explains its Centrelink treatment, taxation and aged care fees with examples.

• The ‘Aged Care Investment Analyser’, an Excel-based adviser tool that produces a 15-year projection for your clients to help you compare various aged care financial strategies.

34 Challenger Aged care guide

• ACATFinding a team 7

Health assessment 7

Accommodation bondAsset assessment limits 9

Assets Test assessment 10, 12

Income Test assessment 10

Negotiation 9, 20, 21

Payment options 9, 10

Retention amount 9

Security 10

Transferring to another facility 9

Whether to have an asset assessment 12

Valuing the family home 12

Accommodation chargeNegotiation 11

Versus accommodation bond 11

Valuing the family home 12

Age pensionStrategies to maximise 23, 25-29

Aged care costs (upfront)Accommodation bond 9

Accommodation charge 11

Index

Challenger Aged care guide 35

Aged care guide Index

Aged care facilitiesLow level care 3, 7

High level care 3, 7

Extra services facilities 3, 7

Aged care fees (ongoing)Basic daily fee 15

Extra service fee 17

Income-tested fee 15, 16

Aged care reformsLegislation changes from 1 July 2014 31

Basic daily feeRate 15

Indexation 15

Estate planningWills and Powers of Attorney 32

Extra service fee Fee amount 17

Ways to reduce 20, 25-29

Family homeTo keep or sell 13, 19

Impact of renting out on Assets Test 13, 19, 25-29

Impact of renting out on Income Test 13, 19, 25-29

Market value 19

Capital gains tax upon sale 13, 20

Granny flatMoving from granny flat into aged care 20

income-tested fee Calculation 15, 16

Income Test assessment 15

Strategies to reduce 21-23

illness-separated coupleCentrelink assessment 32

investing for aged careAnnuities 22, 23, 27-29

Term deposits 23, 25-29

Investment bond within a private trust 21-23, 27

Net medical expenses tax offsetFees considered medical expenses 32

Offset tax payable on rental income 13

Retirement villageMoving from retirement village into aged care 20

Supported residentsCriteria 11

Partial support 11

36 Challenger Aged care guide