cg praactices in banking secotor of bangladesh

DESCRIPTION

Corporate Governance Praactices in Banking Secotor of BangladeshTRANSCRIPT

Corporate

Governance Corporate Governance Practices of

Commercial Banks in Bangladesh

ii

Acknowledgement

At the very beginning, we would like to express my deep gratitude to almighty Allah

for giving us the strength to finish the report within the schedule time. We required

enormous time and attention in every step of it. However, it gives us a true feeling of

creation and helps me to understand my ability of work. For fear of sounding like a

vote of thanks speech, we would like to take the opportunity, to thank all of those

marvelous people who have contributed to this report. Of course, some very special

people cannot go without mentioning. At first, we express thank my heartiest

gratitude to our Course Teacher Mr. Md. Miraj Hossen, Assistant Professor, Dept. of

Management Studies, Jagannath University for his kind cooperation in preparing this

report. We are also indebted to all of respondents and for giving time and advice to

know and learn all activities of the bank and prepare this report. During the

preparation of the report. We have come to the very supportive touch of different

individuals (respondents &seniors) and friends, who lend their ideas, time and caring

guidance to amplify the report’s contents. We must say that without their help it

would be very hard for us to prepare such report. We are thankful to them with all of

our feelings.

v

Synopsis

Corporate Governance ensures to bring transparency, accountability and

professionalism in the management system of a corporate body that enhances the

credibility and acceptability to the shareholders, employees, potential investors,

customers, lenders, governments and all other stakeholders. Corporate governance

(CG) is a set of principles, which should be incorporated into every part of the

organization. Financial institutions like banks have a significant role to play in the

economy of any country. Banking sector should follow the Corporate Governance

codes for Bangladesh. Since Banks deal in public money, public confidence is of

outmost importance in this Industry. So, this paper has tried to evaluate the present

scenario of Corporate Governance practices by the commercial banks in Bangladesh.

The study has been conducted to attain some objectives. The primary objective of the

study is to evaluate the practices of Corporate Governance codes by the Commercial

Banks in Bangladesh. In this study, both the primary and secondary data were used.

The primary data relating to problems involved in Corporate Governance practice and

suggestions to remove the same were collected from 50 randomly selected

respondents of banks on the basis of a questionnaire and scheduling method. Among

them we selected Directors of the Board, executive officers etc as the internal part of

management and the stakeholders (like customers) as the external group. The

secondary data were collected through an extensive literature survey on the subject. In

order to do the study, we focus the major issues like shareholders’ rights and

disclosure of information, disclosure and transparency, effectiveness of Board of

directors etc. Four (4) hypotheses have been developed in order to identify whether

the commercial banks are complying corporate governance issues or not. And making

the study convenient an assumption was made using subjective probability technique

that 70% or more of commercial banks of Bangladesh are maintaining 90% or more

CG codes for Bangladesh (Alam, K, 2011). Only 33% of the major issue like

disclosure and transparency has met the assumption. In contrast the major issues of

CG codes namely shareholders’ rights and disclosure of information, board of

directors effectiveness are not properly exercised by the commercial banks. In this

survey, we have also found some embezzlement of commercial banks (Sonali Bank,

Agrani Bank, Bank Asia etc) in recent years. We found that this embezzlement

occurred only for not practicing good corporate governance. We have also identified

some major problems in Corporate Governance practices in the Banking Industry of

the country. The prospect of Corporate Governance practice is bright in Banking

Industry in the country as reported by the respondents if problems are removed by the

concerned management of the Banks as well as Bangladesh Bank management as the

guardian of commercial Banks. Consequently the study recommends some

approaches that are well thought out for the practice of corporate governance codes by

the private commercial banks of Bangladesh.

Table of Content

Sl Particulars Page No.

1. Title page i

2. Acknowledgement ii

3. Letter of Transmittal iii

4. Group List iv

5. Synopsis v

6. CHAPTER ONE- INTRODUCTION 1- 5

7. 1.1 Background of the Study 1

8. 1.2 Objectives of the study 1

9. 1.2.1 Primary Objective 1

10. 1.2.2 Secondary Objectives 1

11. 1.3 Methodology 2

12. 1.3.1 Sources of Data 2

13. 1.3.2 Target Population 2

14. 1.3.3 Sampling Method 2

15. 1.3.4 Questionnaire Development 2

16. 1.3.5 Research Method 2

17. 1.3.6 Measuring Instruments 2

18. 1.3.7 Data Analysis Method 2

19. 1.4 Limitation 3

20. 1.5 Hypothesis Development 3

21. 1.5.1 Hypothesis 3

22. 1.5.2 Assumption 4

23. 1.6 Literature Review 4, 5

24. CHAPTER TWO- HISTORY OF BANKING 6 - 8

25. 2.1 Short History of Banking 6

26. 2.2 Lists of commercial banks 6

27. 2.2.1 State-owned commercial banks 6

28. 2.2.2 Private commercial banks 6, 7

29. 2.2.3 Islamic Commercial Banks 7

30. 2.2.4 Foreign commercial banks 7

31. 2.3 Brief description of some commercial banks: 7

32. 2.3.1 Pubali Bank 7, 8

33. 2.3.2 National Bank Ltd. 8

34. 2.3.3 Dutch-Bangla Bank Ltd. 8

35. 2.3.4 IBBL 8

36. CHAPTER THREE- HISTORY OF BANKING 10 - 40

37. 3.1 Definition of Corporate Governance 10

38. 3.2 Principles 10, 11

39. 3.3 Pre-Requisites of Effective Corporate Governance 11, 12

40. 3.4 Corporate Governance Guidelines for Banking Sector 12 - 14

41. 3.5 Present State of CB in BD 14, 15

42. 3.5.1 Embezzlement in Banks 15

43. 3.6 Limitations 16

44. 3.7 Result and Analysis 17 - 30

45. 3.8 Testing Hypothesis 31- 40

46. 3.8.1 Hypothesis Test 1 30 - 33

47. 3.8.2 Hypothesis Test 2 33 - 35

48. 3.8.3 Hypothesis Test 3 36 - 38

49. 3.8.4 Hypothesis Test 4 38 - 40

50. CHAPTER FOUR- FINDINGS & DISCLOSURE OF INFORMATION 41 - 45

51. 4.1 Findings 41, 42

52. 4.2 Problems 43

53. 4.3 Conclusion 43, 44

54. 4.4 Recommendation 44, 45

55. Closing Part 46 - 60

56. Reference 46, 47

57. Appendix 48 - 60

58. Questionnaire 48 - 54

59. List of Respondent 55, 56

60. List of Table 56 – 60

ACRONYMS

SL.NO. ACRONYMS ABBREVIATION

1 ARCG Asian Roundtable on Corporate Governance

2 AGM Annual General Meeting

3 BEI Bangladesh Enterprise Institute

4 BIS Bank Of International Settlement

5 BOD Board Of Directors

6 CEO Chief Executive Officer

7 CG Corporate Governance

8 CSR Corporate Social Responsibility

9 CSE Chittagong Stock Exchange

10 DSE Dhaka Stock Exchange

11 MIS Management Information System

12 RAFT Responsibility, Accountability, Fairness,

Transparency

13 RJSC Registrar of Joint Stock Company

14 SEC Securities Exchange Commission

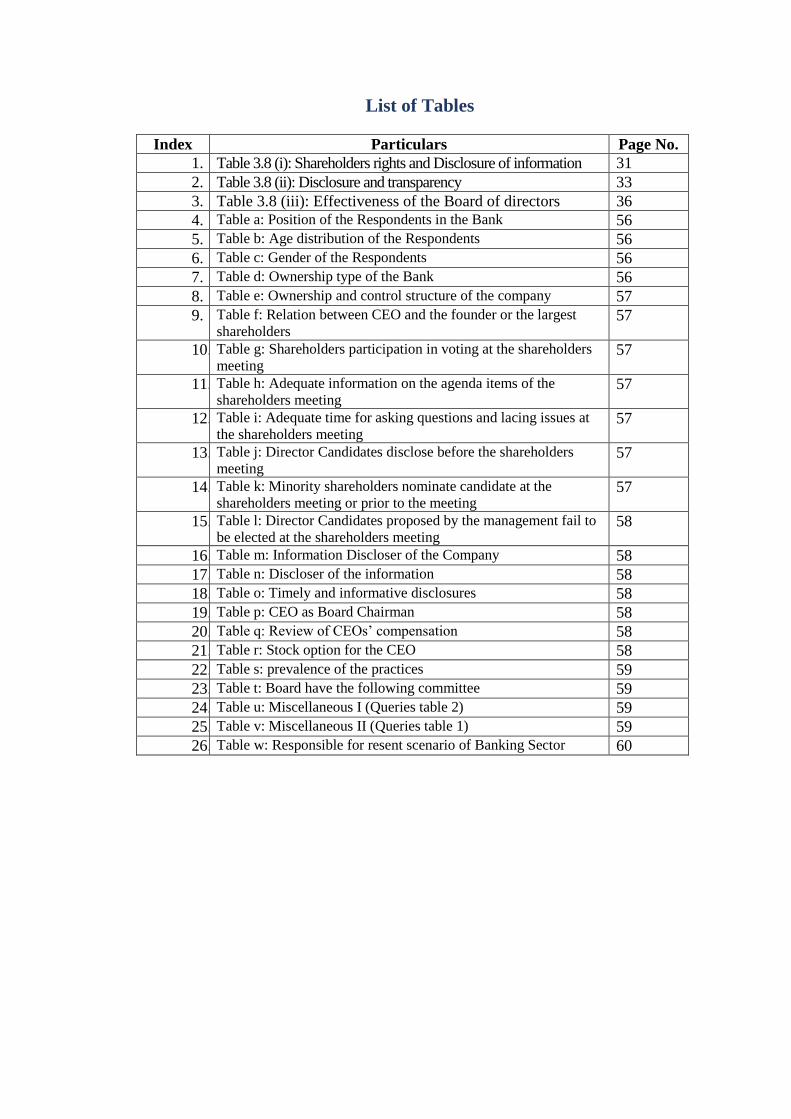

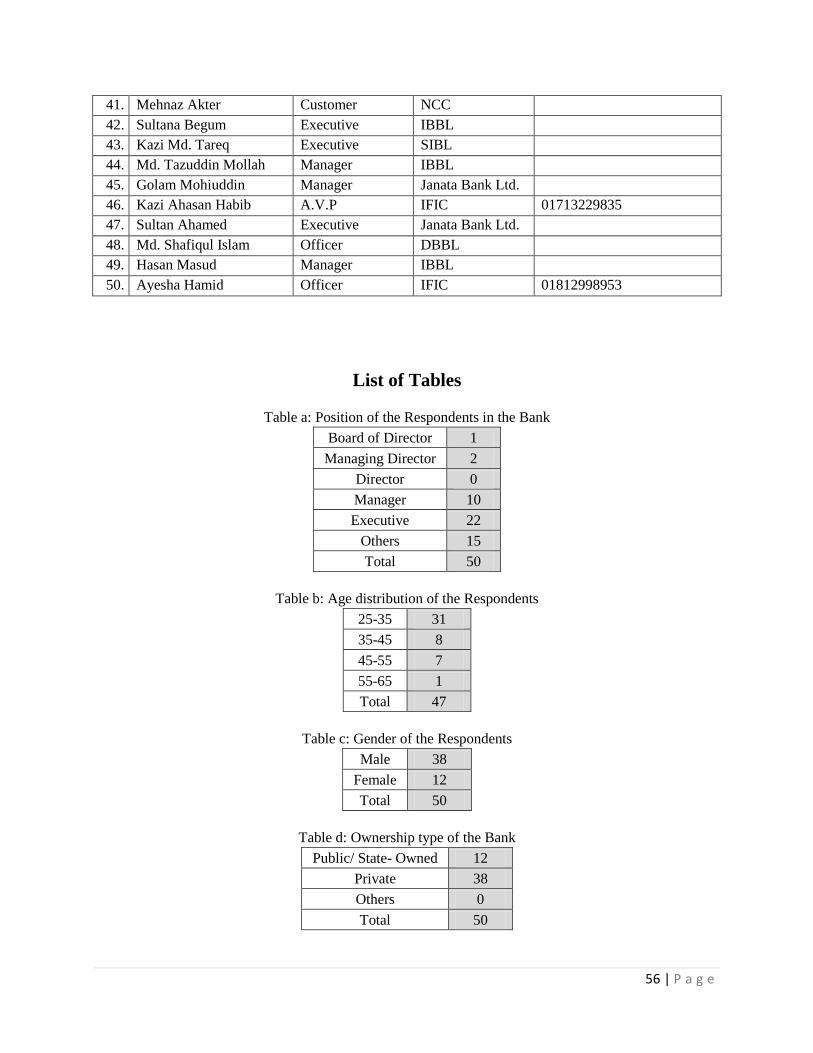

List of Tables

Index Particulars Page No.

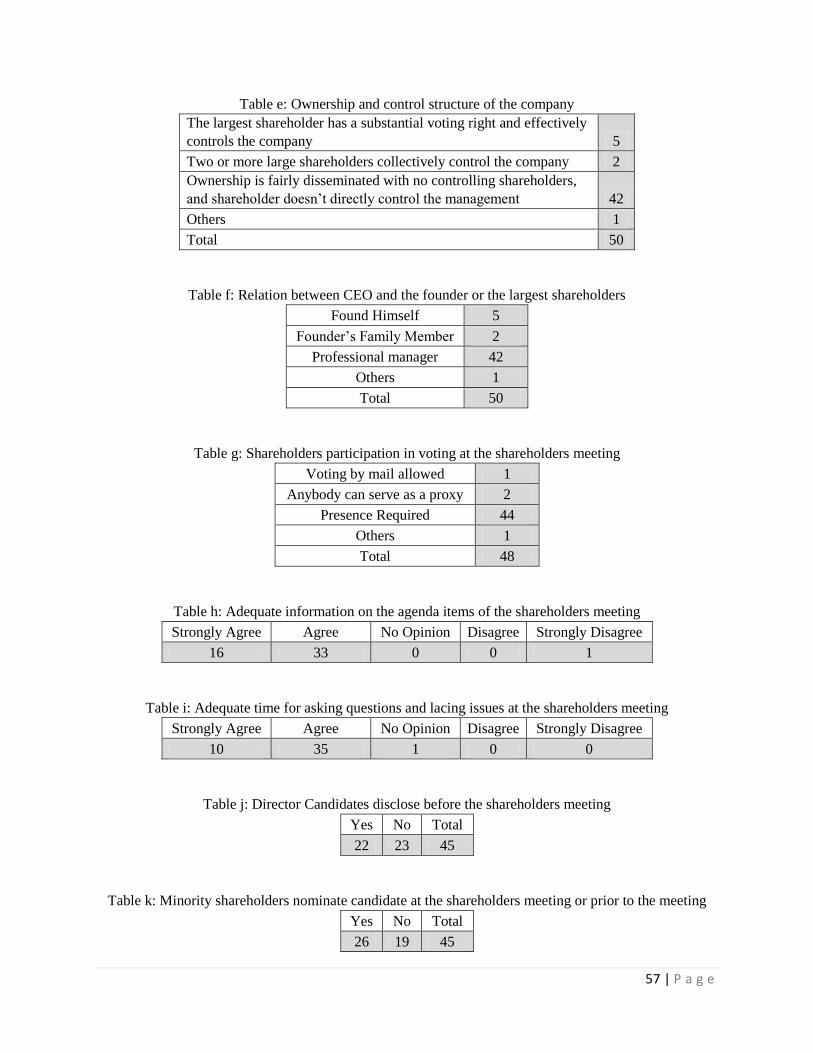

1. Table 3.8 (i): Shareholders rights and Disclosure of information 31

2. Table 3.8 (ii): Disclosure and transparency 33

3. Table 3.8 (iii): Effectiveness of the Board of directors 36

4. Table a: Position of the Respondents in the Bank 56

5. Table b: Age distribution of the Respondents 56

6. Table c: Gender of the Respondents 56

7. Table d: Ownership type of the Bank 56

8. Table e: Ownership and control structure of the company 57

9. Table f: Relation between CEO and the founder or the largest

shareholders 57

10. Table g: Shareholders participation in voting at the shareholders

meeting 57

11. Table h: Adequate information on the agenda items of the

shareholders meeting 57

12. Table i: Adequate time for asking questions and lacing issues at

the shareholders meeting 57

13. Table j: Director Candidates disclose before the shareholders

meeting 57

14. Table k: Minority shareholders nominate candidate at the

shareholders meeting or prior to the meeting 57

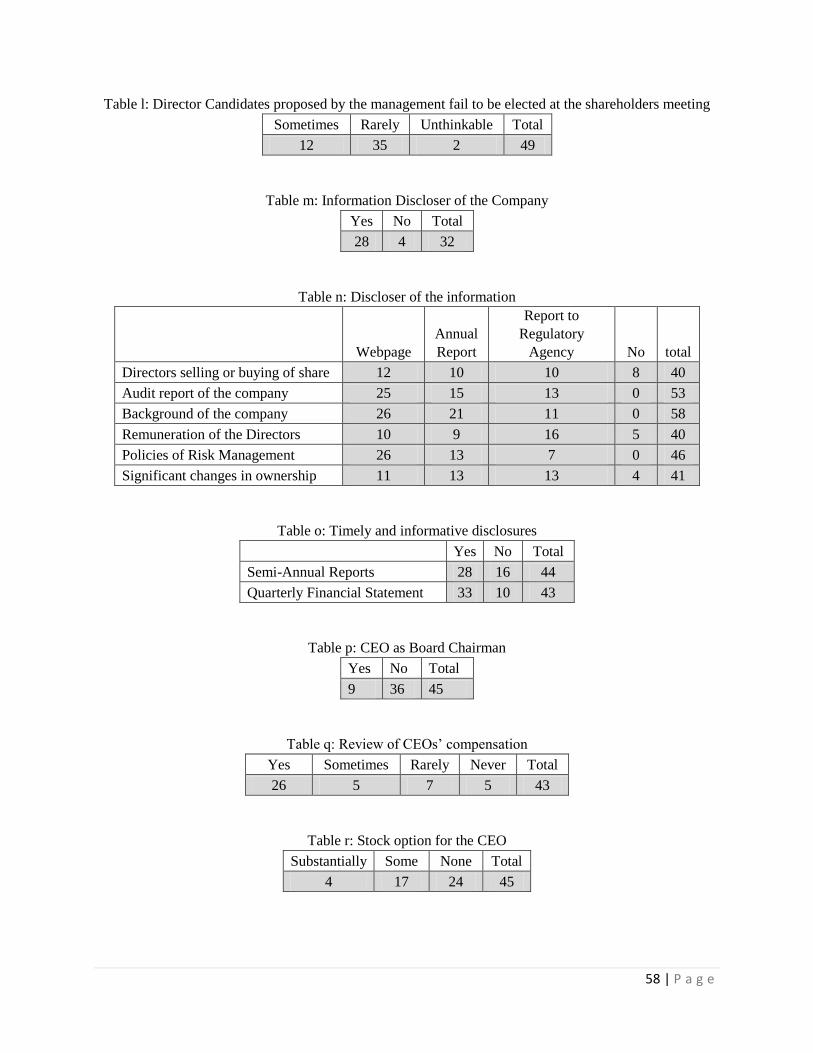

15. Table l: Director Candidates proposed by the management fail to

be elected at the shareholders meeting 58

16. Table m: Information Discloser of the Company 58

17. Table n: Discloser of the information 58

18. Table o: Timely and informative disclosures 58

19. Table p: CEO as Board Chairman 58

20. Table q: Review of CEOs’ compensation 58

21. Table r: Stock option for the CEO 58

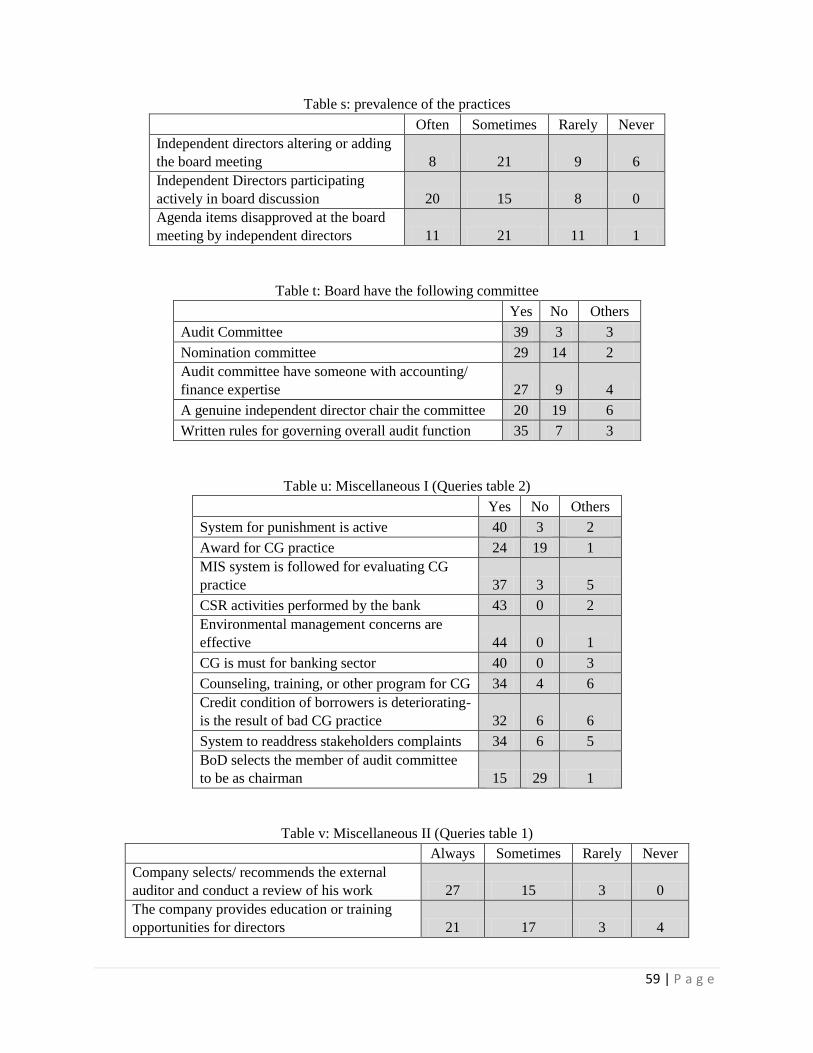

22. Table s: prevalence of the practices 59

23. Table t: Board have the following committee 59

24. Table u: Miscellaneous I (Queries table 2) 59

25. Table v: Miscellaneous II (Queries table 1) 59

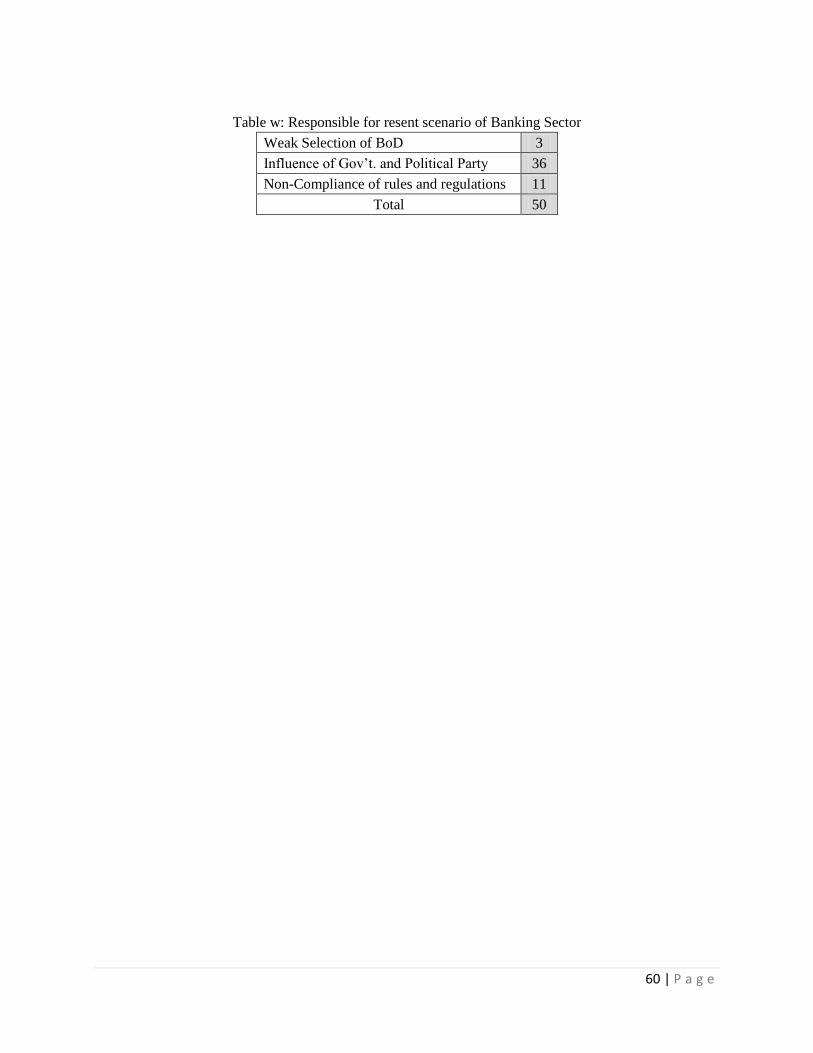

26. Table w: Responsible for resent scenario of Banking Sector 60

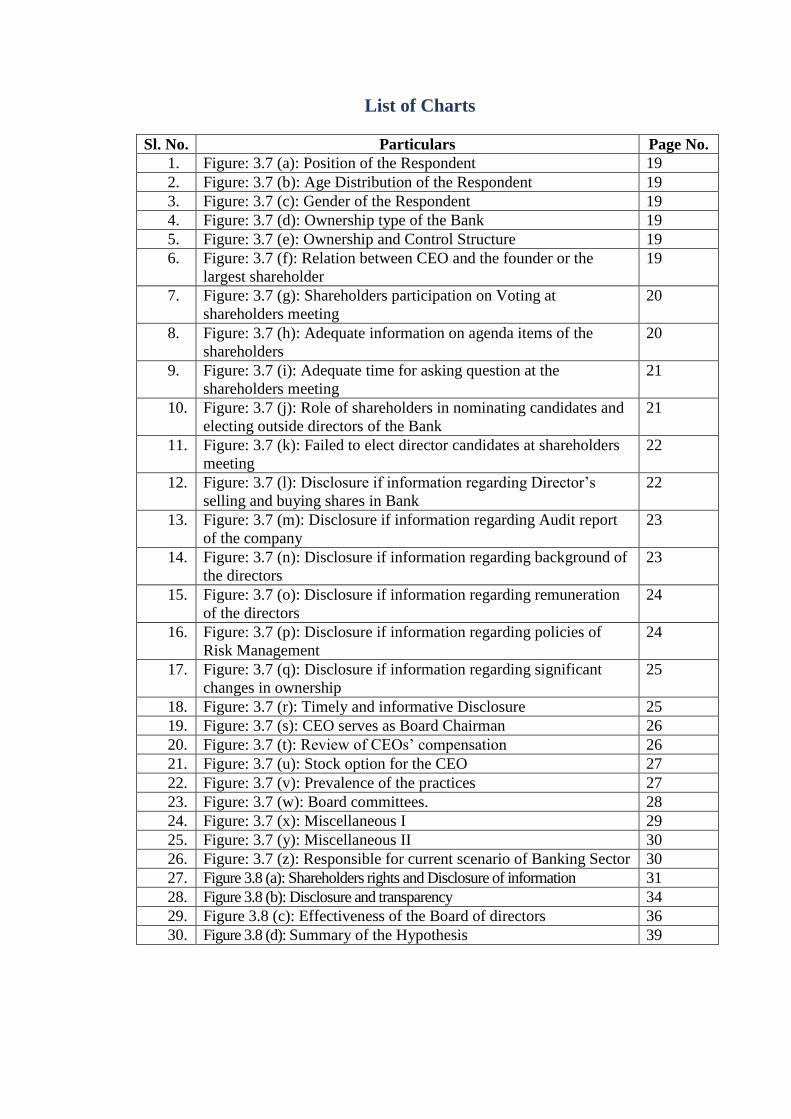

List of Charts

Sl. No. Particulars Page No.

1. Figure: 3.7 (a): Position of the Respondent 19

2. Figure: 3.7 (b): Age Distribution of the Respondent 19

3. Figure: 3.7 (c): Gender of the Respondent 19

4. Figure: 3.7 (d): Ownership type of the Bank 19

5. Figure: 3.7 (e): Ownership and Control Structure 19

6. Figure: 3.7 (f): Relation between CEO and the founder or the

largest shareholder

19

7. Figure: 3.7 (g): Shareholders participation on Voting at

shareholders meeting

20

8. Figure: 3.7 (h): Adequate information on agenda items of the

shareholders

20

9. Figure: 3.7 (i): Adequate time for asking question at the

shareholders meeting

21

10. Figure: 3.7 (j): Role of shareholders in nominating candidates and

electing outside directors of the Bank

21

11. Figure: 3.7 (k): Failed to elect director candidates at shareholders

meeting

22

12. Figure: 3.7 (l): Disclosure if information regarding Director’s

selling and buying shares in Bank

22

13. Figure: 3.7 (m): Disclosure if information regarding Audit report

of the company

23

14. Figure: 3.7 (n): Disclosure if information regarding background of

the directors

23

15. Figure: 3.7 (o): Disclosure if information regarding remuneration

of the directors

24

16. Figure: 3.7 (p): Disclosure if information regarding policies of

Risk Management

24

17. Figure: 3.7 (q): Disclosure if information regarding significant

changes in ownership

25

18. Figure: 3.7 (r): Timely and informative Disclosure 25

19. Figure: 3.7 (s): CEO serves as Board Chairman 26

20. Figure: 3.7 (t): Review of CEOs’ compensation 26

21. Figure: 3.7 (u): Stock option for the CEO 27

22. Figure: 3.7 (v): Prevalence of the practices 27

23. Figure: 3.7 (w): Board committees. 28

24. Figure: 3.7 (x): Miscellaneous I 29

25. Figure: 3.7 (y): Miscellaneous II 30

26. Figure: 3.7 (z): Responsible for current scenario of Banking Sector 30

27. Figure 3.8 (a): Shareholders rights and Disclosure of information 31

28. Figure 3.8 (b): Disclosure and transparency 34

29. Figure 3.8 (c): Effectiveness of the Board of directors 36

30. Figure 3.8 (d): Summary of the Hypothesis 39

Background of the study

Objectives

Methodology

Limitations

Hypothesis Development

Literature Review

Chapter: One

Introductory Issues

1 | P a g e

1.1 Background of the Study

Corporate governance is the set of processes, customs, policies, laws and institutions

affecting the way a corporation is directed, administered or controlled. It can be defined

as a combination of fairness, precision, accountability and sustainability of corporate

behavior. It is a key factor to achieve the improved performance of an organization. It

is a fundamental element to safeguard the interests of shareholders and stakeholders.

For continuous and sustainable growth of an organization, there is no alternative to

effective Corporate Governance.

The positive effect of corporate governance on commercial banking sectors ultimately

is a strengthened economy, and hence good corporate governance is a tool for socio-

economic development.

Commercial Banks are critically important for industrial expansion, the Corporate

Governance (CG) of firms, and capital allocation. When banks efficiently mobilize and

allocate funds, this lowers the cost of capital to firms, boosts capital formation, and

stimulates productivity growth. Thus, the functioning of banks has ramifications for the

operations of firms and the prosperity of nations.

Effective Corporate Governance practices are essential to achieving and maintaining

public trust and confidence in the banking system, which are critical to the proper

functioning of the banking sector and economy as a whole.

As we know banking sector has been performing an essential role in strengthening any

economy. Poor Corporate Governance may contribute to bank failures, which can pose

significant public costs and consequences due to their potential impact on any

applicable deposit insurance systems and the possibility of broader macroeconomic

implications, such as contagion risk and impact on payment systems. In addition, poor

Corporate Governance can lead markets to lose confidence in the ability of a bank to

properly manage its assets and liabilities, including deposits, which could in turn trigger

a bank run or liquidity crisis.

1.2 Objectives of the study

1.2.1 Primary Objective

To evaluate the practices of Corporate Governance codes by the Commercial Banks of

Bangladesh.

1.2.2 Secondary Objectives

i. To see the corporate governance guidelines in Bangladesh.

ii. Assessing the accountability of commercial banks in Bangladesh to the

stakeholders.

iii. Evaluating how far the current practice of corporate governance passes the

test of fairness in case of banks.

iv. To know whether corporate governance system in Bangladesh is transparent

for all stakeholders of commercial banks.

v. To find out challenges and recommends some measures to improve the

quality of present issues of corporate governance of commercial banks in

Bangladesh.

2 | P a g e

1.3 Methodology

The following are the bases that have been followed to conduct the study:

1.3.1 Sources of Data

i. Primary Source

Primary data have been collected through conducting questionnaire and

scheduling method.

ii. Secondary Source

Secondary data have been collected from different journals, books,

banks’ websites and banks’ annual report.

1.3.2 Target Population

The target populations of this study are the shareholders, stakeholders (customers,

investors, employees Etc.), managers and executives of different commercial banks in

Bangladesh.

1.3.3 Sampling Method

Random sampling method is used as a sampling method. Under which convenient

technique has been used to gather primary data. And sample size has been determined

50 respondents of commercial banks in Bangladesh.

1.3.4 Questionnaire Development

The questionnaire consists of both open and close ended questions. The questionnaire

has been developed based on the corporate governance codes for Bangladesh.

1.3.5 Research Method

To do this study a questionnaire has been developed to collect information about

corporate governance practiced by the commercial banks in Bangladesh. The

questionnaire has been divided into different sections such as company profile,

shareholders’ rights and disclosure, public disclosure and transparency, effectiveness

of the board, function of the board, and effectiveness of the independent directors. The

questionnaire was made semi-structured to allow for in depth interviews with key

individuals of the companies.

1.3.6 Measuring Instruments

Scales Include5 point Likert scales. Where 5= strongly agree, 4=Agree, 3=No opinion,

2=Disagree, 1= strongly disagree.

1.3.7 Data Analysis Method

In this step, each element of the major issues of corporate governance has been

tabulated and analyzed. For some analysis here, percentage system has been used. It

has been presented in terms of tables, figures, and graphs as well as written scripts. For

the processing and analyzing numerical data, means, standard deviations and z tests

have been used in the study.

3 | P a g e

1.4 Limitation

There were some limitations of the study among which non availability of data was the

most, especially for the non-listed companies. Another limitation was least amount of

disclosure regarding Corporate Governance. Corporate Social Responsibility (CSR)

activities of the banks were very limited, as well as the disclosure regarding CSR.

Non availability of data

Least amount of disclosure regarding Corporate Governance

The sample size was relatively small as compared to the total population.

Absence of credible data and relevant information on the real CG concerns in

Bangladesh.

Comprehensive access to information was a difficult task because of time

limitation.

Unwillingness to provide confidential information especially by state owned

commercial bank.

Unawareness of customers about the CG practice in their respective banks.

1.5 Hypothesis Development

1.5.1 Hypothesis

i. Hypothesis- 1

H0 = The state of affairs of Shareholder Rights and Disclosure of Information

is meeting the CG codes in the commercial banks.

H1 = The state of affairs of Shareholder Rights and Disclosure of Information

is not meeting the CG codes in the commercial banks.

ii. Hypothesis- 2

H0 = The state of affairs for Disclosure and Transparency is being met the CG

codes by the commercial banks.

H1 = The state of affairs for Disclosure and Transparency is not being met the

CG codes by the commercial banks.

iii. Hypothesis- 3

H0 = The state of affairs of Effectiveness of the Board of directors is meeting

the CG codes in the commercial banks.

H1 = The state of affairs of Effectiveness of the Board of directors is not meeting

the CG codes in the commercial banks.

iv. Hypothesis- 4

H0 = The CG codes are practiced by the commercial banks in Bangladesh as

per the assumption.

H1 = The CG codes are not practiced by the commercial banks in Bangladesh

as per the assumption.

4 | P a g e

1.5.2 Assumption

An assumption has been taken to conduct the survey that 70% or more

of the commercial banks in Bangladesh are satisfying with 90% or more issues

of the corporate governance codes. Conformity of corporate governance codes

for each issue is determined when 70% or more banks have satisfied with that

assumption. The probability has been taken based on subjective probability

technique.

1.6 Literature Review

In the area of corporate governance practices of banks, three strands of literature are

found. First strand focuses on how the corporate governance practices in banks differ

from those in non-banking firms (Prowse, 1997; Furfine, 2001; Morgan, 2002; Macey

and O‟Hara, 2003). Banks have two related characteristics that inspire a separate

analysis of the corporate governance of banks (Furfine, 2001). First, banks are generally

more obscure than non-financial firms. Although information asymmetries plague all

sectors, evidence suggests that these informational asymmetries are larger with banks

(Furfine, 2001).

From the perspective of banking, loan quality is not readily observable and can be

hidden for long periods. Therefore, Morgan (2002) found that bond analysts disagree

more over the bonds issued by banks than by non-financial firms. The comparatively

severe difficulties in acquiring information about bank behavior and monitoring

ongoing bank activities hinder traditional corporate governance mechanisms (Levine,

2004).

The second strand of literature looks at how better governance practices in banks can

help their financial development and growth (Levine, 1997; Bushman and Smith,

2003). Bushman and Smith discussed economics-based research focused primarily on

the governance role of financial accounting information and propose future research

ideas. As presented in their study, a framework that isolates three channels through

which financial accounting information can affect the investments, productivity, and

value-added of firms namely the use of financial accounting information by managers

and investors, the use of financial accounting information in corporate control

mechanisms and the use of financial accounting information to reduce information

asymmetries among investors. The third strand looks at corporate governance practices

in banks from the perspective of its impact on performance and efficiency of the banks

themselves (Jensen and Meckling, 1976; Hovey et al, 2003).

Andres and Vallelado (2008) have examined the corporate governance in banking: the

role of the board of directors. They pointed out that bank board composition and size

are related to directors‟ ability to monitor and advice management, and that larger and

not excessively independent board might prove more efficient in monitoring and

advising functions, and create more value. Kutubi (2011) has examined board of

director‟s size, independence and performance: an analysis of private commercial

banks in Bangladesh. This study has examined the impact of board size and the

independent directors on the performance of the local private commercial banks in

Bangladesh. The study has found that statistically significance positive relationship

existed between the proportions of the independent directors and the performance of

the banks.

5 | P a g e

Hossain (2011) highlighted the corporate governance practices in Bangladesh. The

study has pointed out that good corporate governance has implication for company

behavior towards employees, shareholders, customers & banks. He has suggested that

improving corporate governance can provide significant rewards to both individual

companies and countries.

Rashid et al (2010) have examined board composition and firm performance from

Bangladesh perspective. The study has also examined the influence of corporate board

composition in the form of representation of outside independent directors on firms‟

economic performance in Bangladesh. The finding of the study has provided an insight

to the regulators in this quest for harmonization of internal corporate governance

practices. Rashid et al (2009) have made an overview on corporate governance in banks

in Bangladesh. The study has identified six specific corporate governance

characteristics in relation to current corporate governance practices in Bangladesh

namely legal and regulatory frame work, weak institutional control, pre-dominant of

individual investors, limited transparence & weak disclosure practices etc.

History

List of commercial Banks

Brief description of some Banks

Chapter: Two

Commercial Banking Sector

in Bangladesh at a glance

6 | P a g e

2.1 Short History of Banking

The banking system at independence (1971) consisted of two branch offices of the

former State Bank of Pakistan and 17 large commercial banks, two of which were

controlled by Bangladeshi interests and three by foreigners other than west Pakistanis.

There were 14 smaller commercial banks. Virtually all banking services were

concentrated in urban areas. The newly independent government immediately

designated the Dhaka branch of the State Bank of Pakistan as the central bank and

renamed it Bangladesh Bank. The bank was responsible for regulating currency,

controlling credit and monetary policy, and administering exchange control and the

foreign exchange reserves. The Bangladesh government initially nationalized the entire

domestic banking system and proceeded to reorganize and rename the various banks.

Foreign-owned banks were permitted to continue doing business in Bangladesh.

2.2 Lists of commercial banks

2.2.1 State-owned commercial banks

State-owned are functioning as nationalist. Here is the list -

□ Sonali Bank □ Janata Bank

□ Agrani Bank □ Rupali Bank

2.2.2 Private commercial banks

Private Banks are the highest growth sector due to the dismal performances

of government banks (above). They tend to offer better service and products.

Here is the list -

AB Bank Limited

Bangladesh Commerce Bank Limited

Bank Asia Limited

BRAC Bank Limited

Dhaka Bank Limited

Dutch Bangla Bank Limited

Eastern Bank Limited

Farmers Bank Limited

IFIC Bank Limited

Jamuna Bank Limited

Meghna Bank Limited

Mercantile Bank Limited

Midland Bank Limited

Modhumoti Bank Limited

Mutual Trust Bank Limited

National Bank Limited

NCC Bank Limited

NRB Commercial Bank Limited

NRB Global Bank Ltd

One Bank Limited

Prime Bank Limited

Pubali Bank Limited

7 | P a g e

South Bangla Agriculture and Commerce Bank Ltd

Southeast Bank Limited

Standard Bank Limited

The City Bank Limited

The Premier Bank Limited

Trust Bank Limited

United Commercial Bank Ltd

Uttara Bank Limited

2.2.3 Islamic Commercial Banks

There are 8 Islamic Commercial Banks:

Al-Arafah Islami Bank Limited

Export Import Bank of Bangladesh Limited

First Security Islami Bank Limited

ICB Islamic Bank

Islami Bank Bangladesh Limited

Shahjalal islami bank Limited

Social Islami Bank Limited

Union Bank Limited

2.2.4 Foreign commercial banks

10 foreign commercial banks are operating in Bangladesh. These are:

Bank Alfalah

Citibank NA

Commercial Bank of Ceylon

Habib Bank Limited

HSBC (The Hong Kong & Shanghai Banking Corporation Ltd.)

National Bank of Pakistan

Standard Chartered Bank

State Bank of India

Woori Bank

ICICI Bank

2.3 Brief description of some commercial banks:

There are brief discretion of some commercial banks in Bangladesh.

2.3.1 Pubali Bank

PUBALI BANK LIMITED is the largest Commercial Bank in Private Sector in

Bangladesh. It provides mass banking services to the customers through its branch

network all over the country. This Bank has been playing a vital role in socio-economic,

industrial and agricultural development as well as in the overall economic development

of the country since its inception through savings mobilization and investment of funds.

During the last 5 years the growth rate of bank’s earnings is more than 25% on average.

The Bank was initially emerged in the Banking scenario of the then East Pakistan as

Eastern Mercantile Bank Limited at the initiative of some Bangalee entrepreneurs in

the year 1959 under Bank Companies Act 1913. After independence of Bangladesh in

8 | P a g e

1972 this Bank was nationalized as per policy of the Government and renamed as Pubali

Bank. Subsequently due to changed circumstances this Bank was denationalized in the

year 1983 as a private bank and renamed as Pubali Bank Limited. The Government of

the People’s Republic of Bangladesh handed over all assets and liabilities of the then

Pubali Bank to the Pubali Bank Limited. Since then Pubali Bank Limited has been

rendering all sorts of Commercial Banking services as the largest bank in private sector

through its branch network all over the country.

2.3.2 National Bank Ltd.

National Bank Limited has been licensed by the Government of Bangladesh as a

Scheduled commercial bank in the private sector in pursuance of the policy of

liberalization of banking and financial services and facilities in Bangladesh. In view of

the above, the Bank within a period of 25 years of its operation achieved a remarkable

success and met up capital adequacy requirement of Bangladesh Bank.

National Bank Limited established as the first private sector Bank fully owned by

Bangladeshi entrepreneurs. NBL was the first domestic bank to establish agency

arrangement with the world famous Western Union in order to facilitate quick and safe

remittance of the valuable foreign exchanges earned by the expatriate Bangladeshi

nationals. NBL was also the first among domestic banks to introduce international

Master Card in Bangladesh.

2.3.3 Dutch-Bangla Bank Ltd.

Dutch-Bangla Bank Limited (DBBL) is Bangladesh’s most innovative and

technologically advanced bank. DBBL stands to give the most innovative and

affordable banking products to Bangladesh. Amongst banks, DBBL is the largest donor

in to social causes in Bangladesh. It stands as one of the largest private donors involved

in improving the country. DBBL is proud to be associated with helping Bangladesh as

well as being a leader in the country’s banking sector

Dutch-Bangla Bank believes in its uncompromising commitment to fulfill its customer

needs and satisfaction and to become their first choice in banking. Taking cue from its

pool esteemed clientele, Dutch-Bangla Bank intends to pave the way for a new era in

banking that upholds and epitomizes its vaunted marques “Your Trusted Partner”

DBBL was the first bank in Bangladesh to be fully automated. The Electronic-Banking

Division was established in 2002 to undertake rapid automation and bring modern

banking services into this field. Full automation was completed in 2003 and hereby

introduced plastic money to the Bangladeshi masses. DBBL had pursued the mass

automation in Banking as a CSR activity and never intended profitability from this

sector.

2.3.4 IBBL

Islami Bank Bangladesh Limited is a Joint Venture Public Limited Company engaged

in commercial banking business based on Islamic Shari'ah with 63.09% foreign

shareholding having largest branch network ( total 293 Branches) among the private

sector Banks in Bangladesh. It was established on the 13th March 1983 as the first

Islamic Bank in the South East Asia.

It is listed with Dhaka Stock Exchange Ltd. and Chittagong Stock Exchange Ltd.

Authorized Capital of the Bank is Tk. 20,000.00 Million and Paid-up Capital is Tk.

16,099.90 million having 33,686 shareholders as on 30th September 2014.

Definition of CG

Principles of CG

Pre-requisites for CG practice

CG Guidelines for Banking Sector

Present states of CG in BD

Limitations

Result/ Findings

Chapter: Three

Theoretical Issues

Hypothesis testing

9 | P a g e

3.1 Definition of Corporate Governance

Corporate Governance (CG) is probably the widest control mechanism used for

efficient utilization of corporate resources. It can be defined as an organizational

control devise, which is a hybrid of internal and external control mechanisms

with a view to achieving efficient utilization of corporate resources. It is a network

among various corporate players such as shareholders, managers, employees,

leaders, governments, suppliers and consumers for increasing the value of the

firm. Different authors view the meaning of corporate governance differently. For

example:

One school of thoughts describes corporate governance as a “system” by which

companies are directed and controlled (Cadbury and Greenbury Report, 1992).

That the fundamental concern of corporate governance is to ensure the

conditions whereby a firm’s directors and mangers are held accountable,

ensure better and effective protection to all stakeholders.

The World Bank define that the framework of corporate governance should be

based on four pillars such as Responsibility, Accountability, Fairness and

Transparency (RAFT).

There are some variables on which the corporate governance framework

established. Those are Responsibility, Accountability, Fairness and Transparency.

Corporate governance from the view point of commercial banks:

Effective corporate governance practices are essential to achieving and maintaining the

public trust and confidence in the banking system, as a result they are critical to the

proper functioning of the banking sector and economy as a whole. However, little

attention has being given to corporate governance of banking sector especially in

developing economies.

According to Hambrick et al. (2008), not only do the constituents of banking

sector stand to gain or lose due the quality and nature of corporate governance

therein, but the entire national systems can be propelled or stymied as well. “The

health of the economy is closely related to the soundness of its banking sector”

(Katrodia, 2012).

Handley-Schachler et al. (2007) posited that banks require different and more

extensive corporate governance arrangements.

Arun and Turner (2004) also argued that the unique nature of the bank both in

the developed or developing world requires a broad view of corporate

governance to be adopted for banks.

According to Bank for International Settlements (2010) effective corporate

governance practices are essential to achieving and maintaining the public trust

and confidence in the banking system, hence critical to the proper functioning

of the banking sector and economy as a whole.

10 | P a g e

However, Arun and Turner (2004) stated that:

The corporate governance of banks in developing economies is important for several

reasons.

First, banks have an overwhelmingly dominant position in developing-economy

financial systems, and are extremely important engines of economic growth....

Second, as financial markets are usually underdeveloped, banks in developing

economies are typically the most important source of finance for the majority

of firms.

Third, as well as providing a generally accepted means of payment, banks in

developing countries are usually the main depository for the economy’s savings.

Fourth, many developing economies have recently liberalized their banking

systems through privatization/disinvestments and reducing the role of economic

regulation. Consequently, managers of banks in these economies have obtained

greater freedom in how they run their banks.”

3.2 Principles

Key elements of good corporate governance principles include honesty, trust and

integrity, openness, performance orientation, responsibility and accountability, mutual

respect, and commitment to the organization.

Of importance is how directors and management develop a model of governance that

aligns the values of the corporate participants and then evaluate this model periodically

for its effectiveness. In particular, senior executives should conduct themselves

honestly and ethically, especially concerning actual or apparent conflicts of interest,

and disclosure in financial reports.

Commonly accepted principles of corporate governance include:

i. Rights and equitable treatment of shareholders: Organizations should

respect the rights of shareholders and help shareholders to exercise those

rights. They can help shareholders exercise their rights by effectively

communicating information that is understandable and accessible and

encouraging shareholders to participate in general meetings.

ii. Interests of other stakeholders: Organizations should recognize that they

have legal and other obligations to all legitimate stakeholders.

iii. Role and responsibilities of the board: The board needs a range of skills

and understanding to be able to deal with various business issues and have

the ability to review and challenge management performance. It needs to be

of sufficient size and have an appropriate level of commitment to fulfill its

responsibilities and duties. There are issues about the appropriate mix of

executive and non-executive directors.

iv. Integrity and ethical behavior: Ethical and responsible decision making is

not only important for public relations, but it is also a necessary element in

risk management and avoiding lawsuits. Organizations should develop a

11 | P a g e

code of conduct for their directors and executives that promotes ethical and

responsible decision making. It is important to understand, though, that

reliance by a company on the integrity and ethics of individuals is bound to

eventual failure. Because of this, many organizations establish Compliance

and Ethics Programs to minimize the risk that the firm steps outside of

ethical and legal boundaries.

v. Disclosure and transparency: Organizations should clarify and make

publicly known the roles and responsibilities of board and management to

provide shareholders with a level of accountability. They should also

implement procedures to independently verify and safeguard the integrity

of the company’s financial reporting. Disclosure of material matters

concerning the organization should be timely and balanced to ensure that all

investors have access to clear, factual information.

Issues involving corporate governance principles include:

Internal controls and internal auditors.

The independence of the entity’s external auditors and the quality of their

audits.

Oversight and management of risk.

Oversight of the preparation of the entity’s financial statements.

Review of the compensation arrangements for the chief executive officer

and other senior executives.

The resources made available to directors in carrying out their duties.

The way in which individuals are nominated for positions on the board.

3.3 Pre-Requisites of Effective Corporate Governance:

The effectiveness of Corporate Governance in Bangladesh depends on the major Key

Corporate Performances which are nothing but the pre-requisites. These are as follows:

Effective corporate governance requires a clear understanding of the

respective roles of the board

The selection, compensation and evaluation of a well-qualified and ethical

CEO is the single most important function of the board

A corporation should have a code of conduct with effective reporting and

enforcement mechanisms.

A substantial majority of directors of the board of publicly owned

corporation should be independent of management.

Every publicly owned corporation should have an audit committee

Audit committee meetings should be held frequently

An effective internal control system should be in existence at all

corporations

Ensure corporate ethical behavior;

The some special nature of banks makes their corporate governance more complex

because:

12 | P a g e

Depositors are protected by the deposit insurance fund. Because

depositor losses after bank failure are made good by the insurance

fund, depositors are insensitive to the riskiness of the bank. As a

result, banks have an incentive to take excessive risks to boost their

profits.

Many banks are too important to be allowed to fail, and hence

shareholders may believe that they have a tacit government guarantee.

As a result, shareholders may tolerate excessive risk.

Bank assets are hard to evaluate. Even when shareholder rights are

protected, investors may struggle to understand precisely how their

capital is deployed and the bank may be taking on more risk than they

realize.

The objective is what distinguishes bank corporate governance from

other areas of corporate governance because of the potential social

costs that banking can have on the broader economy". It may not be

practical or desirable to expose bank directors to the full costs of their

mistakes, but, in general, good governance should, like good

regulations oblige bankers to consider the wider, external, costs that

their risk-taking could inflict upon third parties.

3.4 Corporate Governance Guidelines for Banking Sector

Banks in developing countries are faced with high risk of sharking as a result of heavy

government ownership, lack of prudential regulation, weak legal protection and

presence of special interest groups (Arun, T.G. and J. Turner (2003), However, there is

an argument that active role by regulators may cause problems as well, as regulators

may not have a convincing or sufficient motivation to monitor the banks as they do not

have much at stake in case of bank failures. Recently, the financial markets of

developing economies have experienced rapid changes due to the growth of wider range

of financial products. As a result of this, banks have been involved with high risk

activities such as trading in financial markets and different off balance sheet activities

more than ever before (Greuning, H. and S. Bratanovic (2003),) which necessitate an

added emphasis on quality of corporate governance of banks in developing economies.

Asian Roundtable on Corporate Governance (ARCG) Task force developed the Policy

Brief on Corporate Governance of Banks in Asia (June 2006). The main issues and

priorities for reforms in CG of banks in Asia that were identified are:

The responsibility of individual board members– fiduciary duties of bank’ board

members need of skill, personal abilities, training programs on integrity and

professionalism.

The roles or functions of the board– guiding, approving and overseeing

strategies or policies rather than being immersed in day-to-day operations.

Creating clear accountability line and internal control system. Sufficient flows

of information and managerial support.

The composition of the board–banks is more encouraged to have independent

directors than other firms. Separation between Chairman and CEO.

13 | P a g e

The committees of the board–audit committee, the Risk Management

Committee, The Governance Committee with combined responsibilities of

Nomination, remuneration, succession planning, training, performance

evaluation, etc.

Preventing abusive related party transactions– inspection of the existing

firewall. Creation of specialized committee to monitor and approve related part

transaction. Publicly disclose such transaction.

Bank holding companies and groups of companies holding banks–a bank’s

parent company should not impede the full exercise of the CG of the bank within

the banking group.

Disclosure–effort on convergence into international standards on accounting,

etc. should be encouraged.

Bank’s autonomy in relation to the state–state as owner should respect the legal

corporate structures of State Owned Commercial Banks

Bank’s monitoring of the CG structure of its corporate borrowers–Extent to

which banks should assess or monitor CG of their corporate borrowers or seek

to improve it.

Actually the principle legal instrument for enforcing governance in Bangladesh is the

Companies Act 1994 which is administered by Registrar of Joint Stock Company

(RJSC) and the Ministry of Commerce. SEC is concerned with publicly limited

companies only, the number of which is very insignificant. Close monitoring of leading

companies is a disincentive for going public as there is a perception that this will create

and raise unnecessary difficulties for companies to supply information as and when

requested.

i. Corporate Governance in the Financial Institutions (FIs) as bank

The need for a competent financial sector is important to stimulate and support

economic growth through efficient resource allocation. Good CG practices are essential

to the effectiveness, competitiveness and safety and soundness of financial institutions.

ii. Streamlining the Guidelines with the Code of Corporate Governance

A Code of CG has been published by BEI can be streamlined to reduce duplication and

resources to comply with CG requirements for the FIs.

iii. Protection of depositors

Given the special nature of banking institutions, a broad view of CG where regulation

of banking activities is required to protect depositors. In developed economies,

protection of depositors in a deregulated environment is typically provided by a system

of prudential regulation, but in developing economies such protection is undermined by

the lack of well-trained supervisors, inadequate disclosure requirements, the cost of

raising bank capital and the presence of distributional cartels.

iv. Improvements in prudential regulation

Liberalization policies need to be gradual, and should be dependent upon improvements

in prudential regulation. Bangladesh needs to expend resources enhancing the quality

of their financial reporting systems, as well as the quantity and quality of bank

supervisors. 50 Given that bank capital plays such an important role in prudential

regulatory systems, it is necessary to improve investor protection laws, increase

financial disclosure and impose fiduciary duties upon bank directors so that banks can

raise the equity capital required for regulator y purposes. A further reason as to why

14 | P a g e

this policy needs implemented is the growing recognition that the CG of banks has an

important role to play in assisting supervisory institutions to perform their tasks,

allowing supervisors to have a working relationship with bank management, rather than

adversarial one.

v. Political determinants of Corporate Governance

CG of financial institutions, particularly banking sector, in Bangladesh is severely

affected by political considerations. Given the trend towards privatization of

government-owned banks in Bangladesh, there is a need for the managers of such banks

to be granted autonomy and be gradually introduced to the CG practices of the private

sector prior to divestment.

vi. Role of the shareholders

Where there has only been partial divestment and government have not relinquished

any control to other shareholders, it may prove very difficult to divest further ownership

stakes unless CG is strengthened

3.5 Present State of CB in BD

As in many developing countries, banks play a vital role in Bangladesh economy, as

the dominant financier for the industrial and commercial activities. The sector

witnessed decreasing profitability, increasing non-performing assets, provision and

capital shortfalls, eroded credit discipline, rampant corruption patronized by political

quarters, low recovery rate, inferior asset quality, managerial weaknesses, excessive

interference from government and owners, weak regulatory and supervisory role etc.

(Hassan, 1994; USAID, 1995).Internal control system along with accounting and audit

qualities are believed to have been substandard (World Bank, 1998; Raquib, 1999;

CPD, 2001). Many of the problems have been attributed to lack of sound corporate

governance among the banks. The reports by the Banking Reform Commission (1999)

and BEI (2003) raises serious concerns on the banking sector and criticize the quality

of governance that prevails in the banking sector in Bangladesh.

Corporate governance practices in Bangladesh are quite absent in most companies and

organizations as well as in commercial banks. In fact, Bangladesh has lagged behind its

neighbors and the global economy in corporate governance because of following

reasons:

Motivation to disclose information and improve governance practices by banks

is felt negatively. There is neither any value judgment nor any consequences for

corporate governance practices.

The current system in Bangladesh does not provide sufficient legal, institutional

and economic motivation for stakeholders to encourage and enforce corporate

governance practices.

Failure in most of the constituents of corporate governance is witness in

Bangladesh.

Poor bankruptcy laws

No push from the international investor community

Limited or no disclosure regarding related party Transactions

15 | P a g e

Weak regulatory system

General meeting scenario

Lack of shareholder active participations

3.5.1 Embezzlement in Banks:

Agrani Bank, a state-owned commercial bank, was found involved in showing inflated

profit through ‘window-dressed’ accounting during the year 2012. According to the

inspection report, Agrani Bank showed an operating profit of Tk 1314.61 crore for the

year 2012, ended December 31, producing fictitious accounts. The bank has incurred a

net loss of Tk 1185.06 crore instead of the profit.

The bank did not abide by the central bank’s set provisioning guidelines and

keep the required provisioning amount of Tk 1719.66 crore against its all

account during the year 2012.

“The profit was calculated without keeping required provisioning against its

classified loan, investment and provisioning against the central bank’s

prescribed rate,” added the report.

That means, the bank has a net shortfall of Tk 1672.11 crore provisioning

against its classified loan during the year.

According to Bangladesh Bank, loans of Tk 31,500 crore have so far been written off

as of March 2014.

The banks are taking opportunity of writing off bad loans as a ploy to cover up their

corruptions and mismanagements. The state-owned four commercial banks are ahead

in writing off bad loans. According to Bangladesh Bank data, four state-owned banks

have written off loans of Tk 15,228 crore until March 2014 since 2002.Of the amount,

the share of Sonali Bank stood at Tk 5,850 crore, Agrani Bank Tk 5,011 crore, Janata

Bank Tk 3,348 crore and Ruplai Bank Tk 1,019 crore. Twenty-seven of the 39 private

banks waived bad loans of Tk 12,517 crore and four state-owned specialised banks

waived Tk 3, 261 crore.

The failure of Sonali Bank, Ruposhi Bangla Branch to prevent the fraudulent

misappropriation of Tk. 3,607 crores by Hallmark Group (Tk. 2,668 crores) and others

is the biggest scandal in the banking industry.

In recent times, several such frauds –

i. Misappropriation of Tk. 622 coroes by one Nurunnabi in Chittagong in 2007

through a false local letter of credit.

ii. Embezzlement of Tk. 596 crores withdrawn without cheque from Oriental

Bank in 2006.

Several other related incidents need to be recalled as rude reminders of indifference to

serious matters. The writing off of bank loans and interest charges of the defaulters

against hundred percent provisioning makes the default rate lower but definitely gives

raise to moral hazard in addition to encouraging further default by the mighty.

16 | P a g e

3.6 Limitations

Why any of these corporate governance mechanisms could not prevent or detect the

massive amount of fund embezzlement?

The prospect of political influence and collusion between top management and

branch level employees cannot be completely ruled out.

The current board, albeit constituted in conformity with the corporate

governance guidelines issued by the Bangladesh Bank, is largely dominated by

political appointees.

Political appointments to boards of state-owned commercial banks are not

uncommon in Bangladesh, and given the socio-political context of the country,

the incorporation of politically linked directors are perhaps understandable.

These directors, although in charge of a very substantial amount of public fund,

would not possibly devote the amount of time they otherwise would have, had

there been personal stakes involved.

The absence of protection for whistleblowers appears to be a fundamental

problem for the smooth functioning of the audit committees in Bangladesh. A

corruption of this extent is likely to involve a large number of persons, and it is

likely that at least one person (if not more) in the chain would be worried and

disgusted about this. If the bank could ensure protection and anonymity of this

person, he or she could have approached the audit committee and reported the

matter to it. However, with no whistleblower protection in place, it is unlikely

that this would happen.

The role of the auditors in this entire scam remains mysterious.

The central bank should also investigate why the external and internal auditors

who regularly audited the bank failed to perform their responsibilities.

Overall, the Sonali Bank case demonstrates that despite having all the corporate

governance mechanisms as suggested by the corporate governance guidelines issued by

the Bangladesh Bank, it was possible to misappropriate a significant amount of public

money.

17 | P a g e

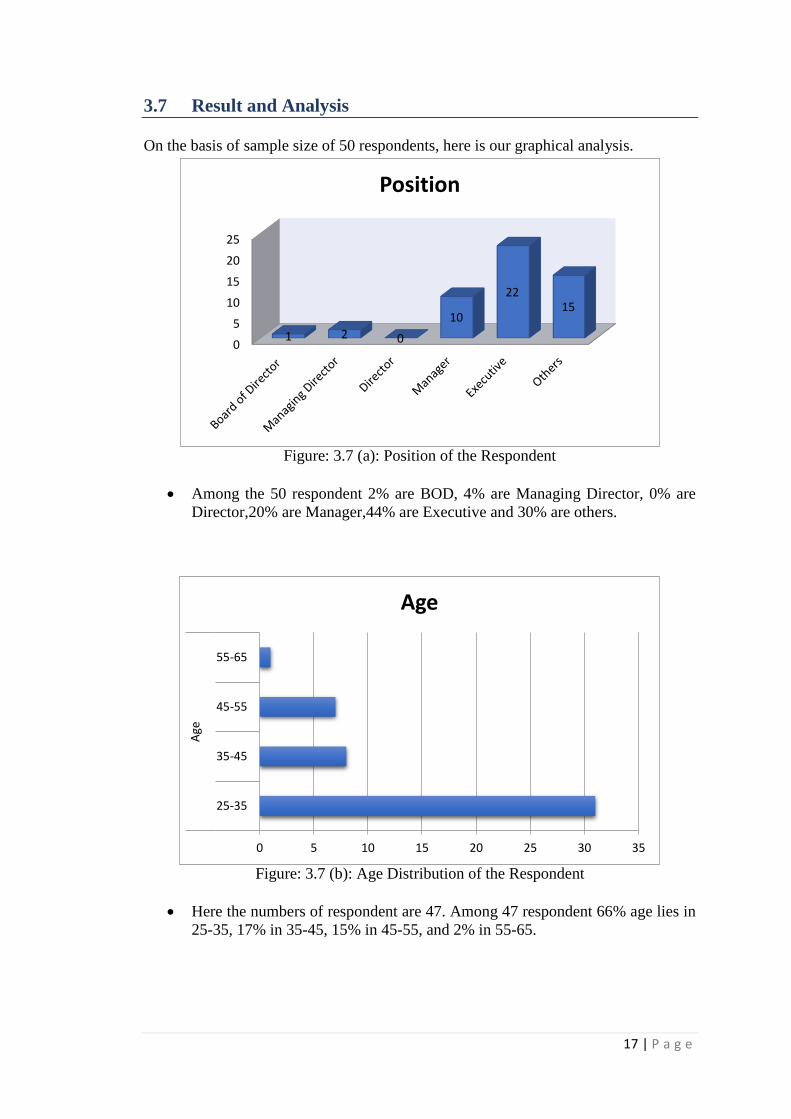

3.7 Result and Analysis

On the basis of sample size of 50 respondents, here is our graphical analysis.

Figure: 3.7 (a): Position of the Respondent

Among the 50 respondent 2% are BOD, 4% are Managing Director, 0% are

Director,20% are Manager,44% are Executive and 30% are others.

Figure: 3.7 (b): Age Distribution of the Respondent

Here the numbers of respondent are 47. Among 47 respondent 66% age lies in

25-35, 17% in 35-45, 15% in 45-55, and 2% in 55-65.

0

5

10

15

20

25

1 2 0

10

2215

Position

0 5 10 15 20 25 30 35

25-35

35-45

45-55

55-65

Age

Age

18 | P a g e

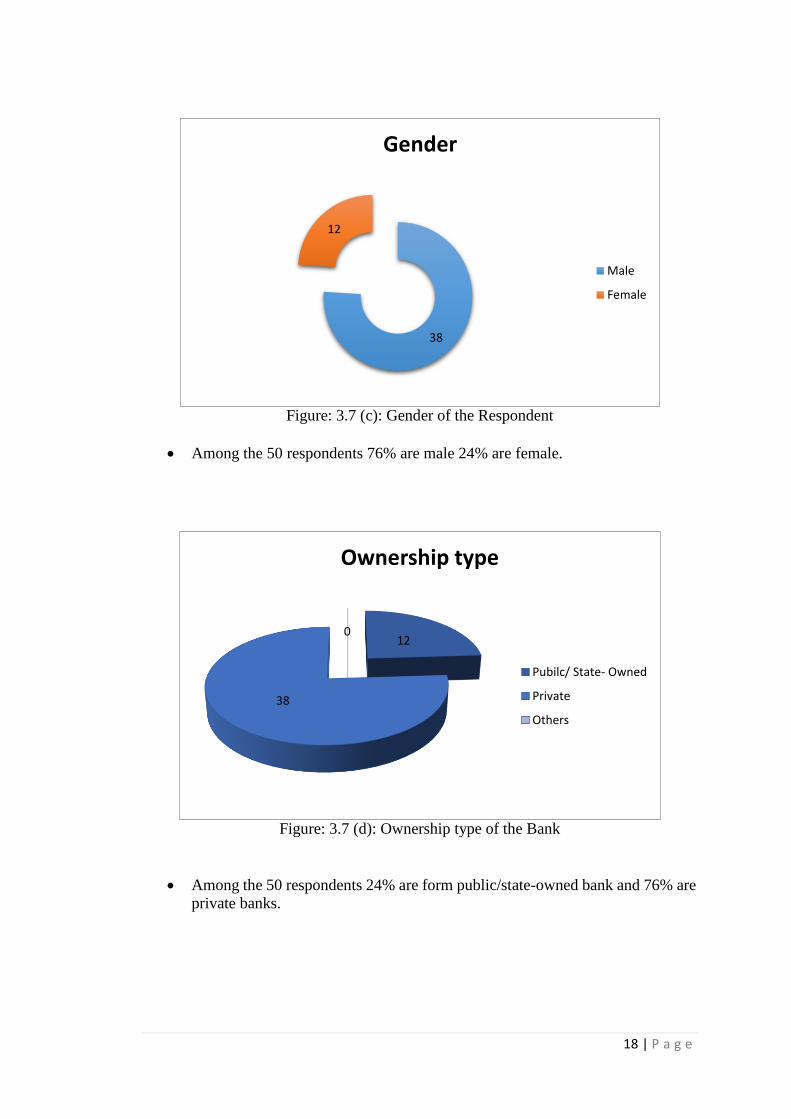

Figure: 3.7 (c): Gender of the Respondent

Among the 50 respondents 76% are male 24% are female.

Figure: 3.7 (d): Ownership type of the Bank

Among the 50 respondents 24% are form public/state-owned bank and 76% are

private banks.

38

12

Gender

Male

Female

12

38

0

Ownership type

Pubilc/ State- Owned

Private

Others

19 | P a g e

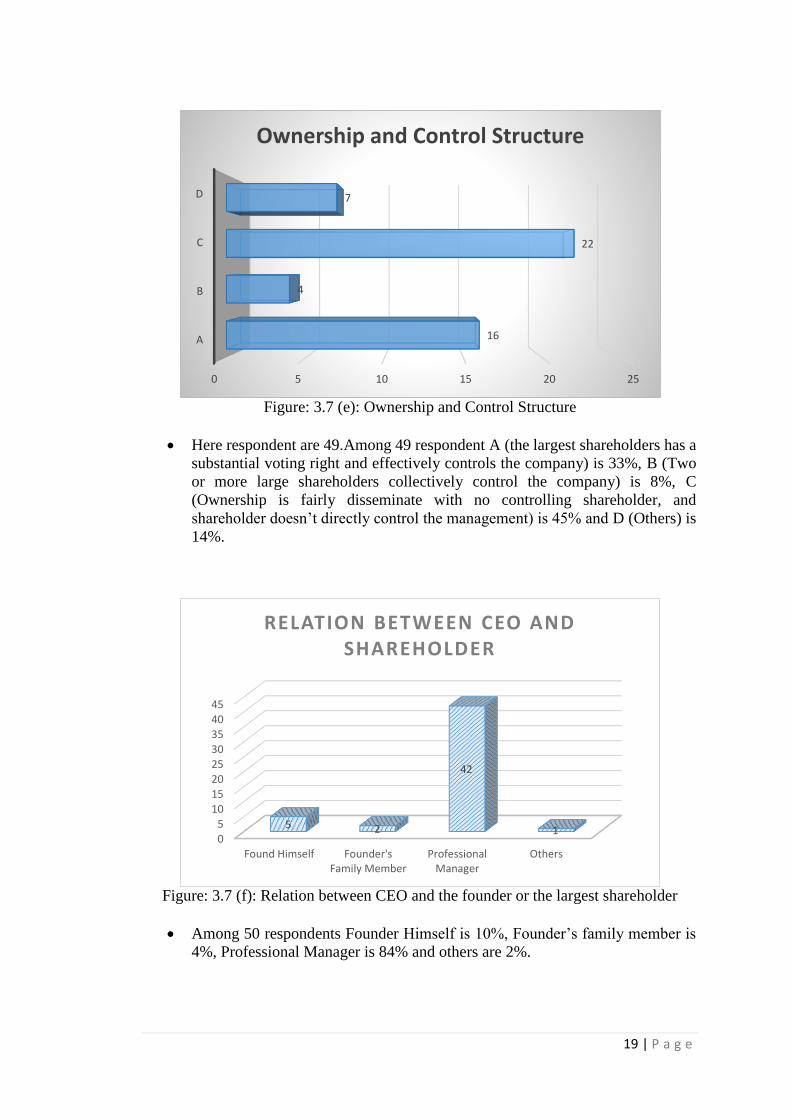

Figure: 3.7 (e): Ownership and Control Structure

Here respondent are 49.Among 49 respondent A (the largest shareholders has a

substantial voting right and effectively controls the company) is 33%, B (Two

or more large shareholders collectively control the company) is 8%, C

(Ownership is fairly disseminate with no controlling shareholder, and

shareholder doesn’t directly control the management) is 45% and D (Others) is

14%.

Figure: 3.7 (f): Relation between CEO and the founder or the largest shareholder

Among 50 respondents Founder Himself is 10%, Founder’s family member is

4%, Professional Manager is 84% and others are 2%.

0 5 10 15 20 25

A

B

C

D

16

4

22

7

Ownership and Control Structure

05

1015202530354045

Found Himself Founder'sFamily Member

ProfessionalManager

Others

5 2

42

1

RELATION BETWEEN CEO AND SHAREHOLDER

20 | P a g e

Figure: 3.7 (g): Shareholders participation on Voting at shareholders meeting

Here the respondents are 48. Among 48 respondents 2% said that Voting by

mail is allowed, 4% said anyone can serve as a proxy, 92% told Presence

requires for voting and Other option is ticked by 2%.

Figure: 3.7 (h): Adequate information on agenda items of the shareholders

Here respondents are 50 among them 32% strongly agree that shareholders provide

adequate information, 66% agree about the terms, and 2% strongly disagreed about the

term.

0

5

10

15

20

25

30

35

StronglyAgree

Agree No Opinion Disagree StronglyDisagree

16

33

0 0 1

ADEQUATE INFORMATION ON AGENDA ITEMS OF THE

SHAREHOLDERS

1 2

44

10

5

10

15

20

25

30

35

40

45

50

Voting by mail Anybody can proxy Presence Requires Others

Participation on Voting

21 | P a g e

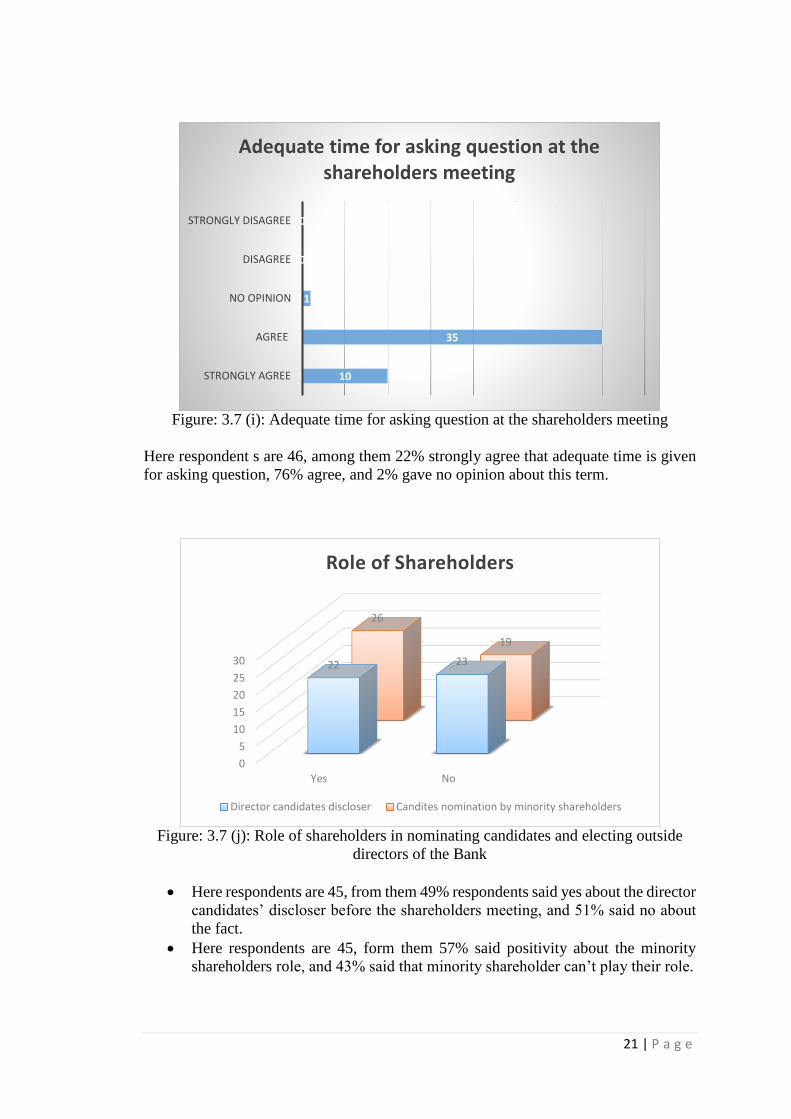

Figure: 3.7 (i): Adequate time for asking question at the shareholders meeting

Here respondent s are 46, among them 22% strongly agree that adequate time is given

for asking question, 76% agree, and 2% gave no opinion about this term.

Figure: 3.7 (j): Role of shareholders in nominating candidates and electing outside

directors of the Bank

Here respondents are 45, from them 49% respondents said yes about the director

candidates’ discloser before the shareholders meeting, and 51% said no about

the fact.

Here respondents are 45, form them 57% said positivity about the minority

shareholders role, and 43% said that minority shareholder can’t play their role.

0

5

10

15

20

25

30

Yes No

22 23

26

19

Role of Shareholders

Director candidates discloser Candites nomination by minority shareholders

10

35

1

0

0

STRONGLY AGREE

AGREE

NO OPINION

DISAGREE

STRONGLY DISAGREE

Adequate time for asking question at the shareholders meeting

22 | P a g e

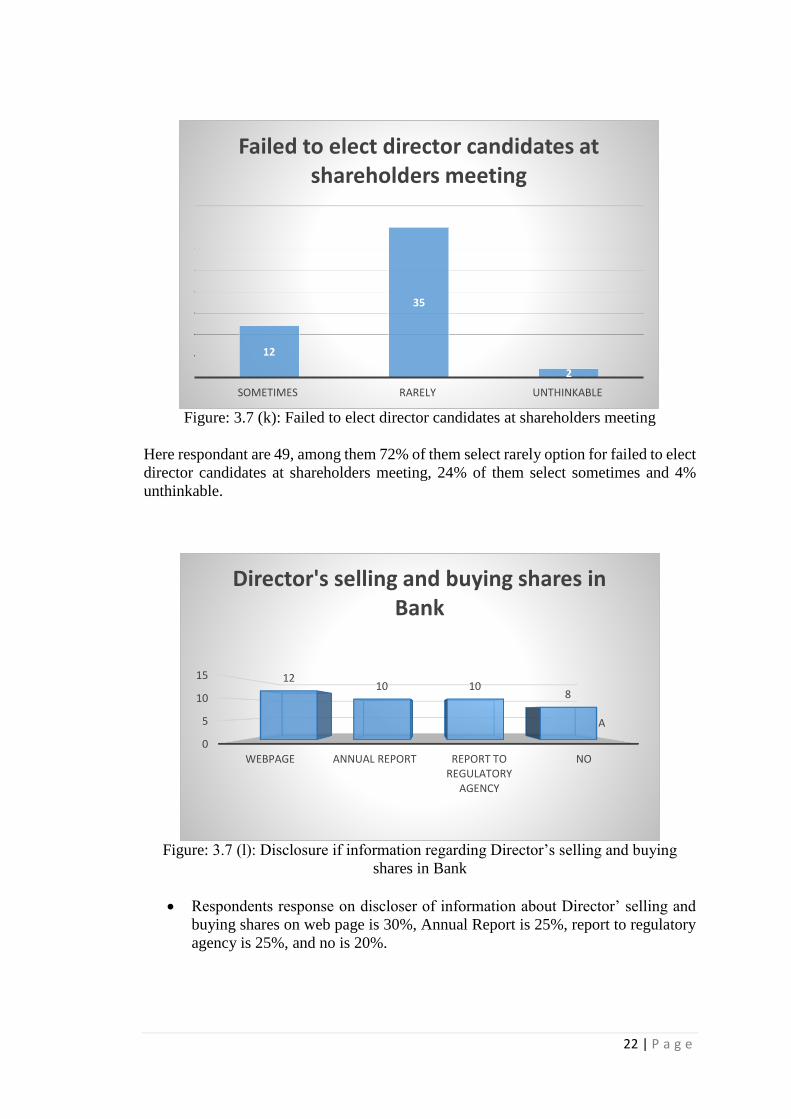

Figure: 3.7 (k): Failed to elect director candidates at shareholders meeting

Here respondant are 49, among them 72% of them select rarely option for failed to elect

director candidates at shareholders meeting, 24% of them select sometimes and 4%

unthinkable.

Figure: 3.7 (l): Disclosure if information regarding Director’s selling and buying

shares in Bank

Respondents response on discloser of information about Director’ selling and

buying shares on web page is 30%, Annual Report is 25%, report to regulatory

agency is 25%, and no is 20%.

A

0

5

10

15

WEBPAGE ANNUAL REPORT REPORT TO REGULATORY

AGENCY

NO

1210 10

8

Director's selling and buying shares in Bank

12

35

2

SOMETIMES RARELY UNTHINKABLE

Failed to elect director candidates at shareholders meeting

23 | P a g e

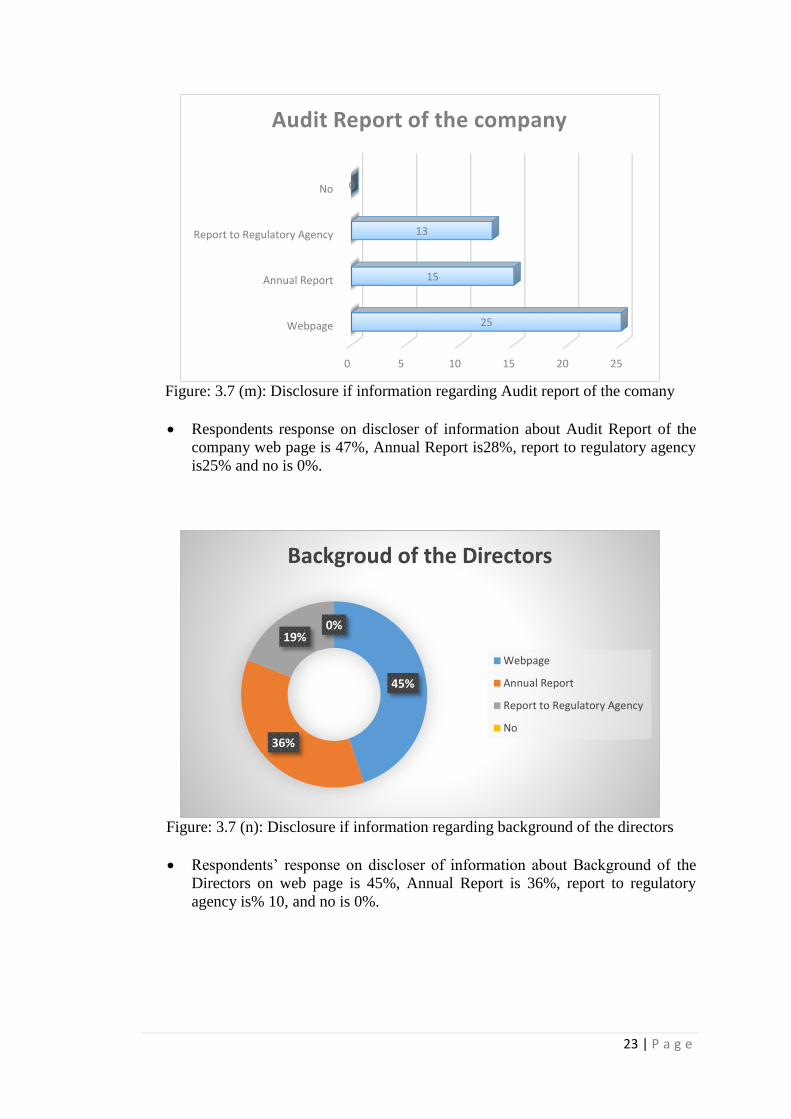

Figure: 3.7 (m): Disclosure if information regarding Audit report of the comany

Respondents response on discloser of information about Audit Report of the

company web page is 47%, Annual Report is28%, report to regulatory agency

is25% and no is 0%.

Figure: 3.7 (n): Disclosure if information regarding background of the directors

Respondents’ response on discloser of information about Background of the

Directors on web page is 45%, Annual Report is 36%, report to regulatory

agency is% 10, and no is 0%.

45%

36%

19%0%

Backgroud of the Directors

Webpage

Annual Report

Report to Regulatory Agency

No

0 5 10 15 20 25

Webpage

Annual Report

Report to Regulatory Agency

No

25

15

13

0

Audit Report of the company

24 | P a g e

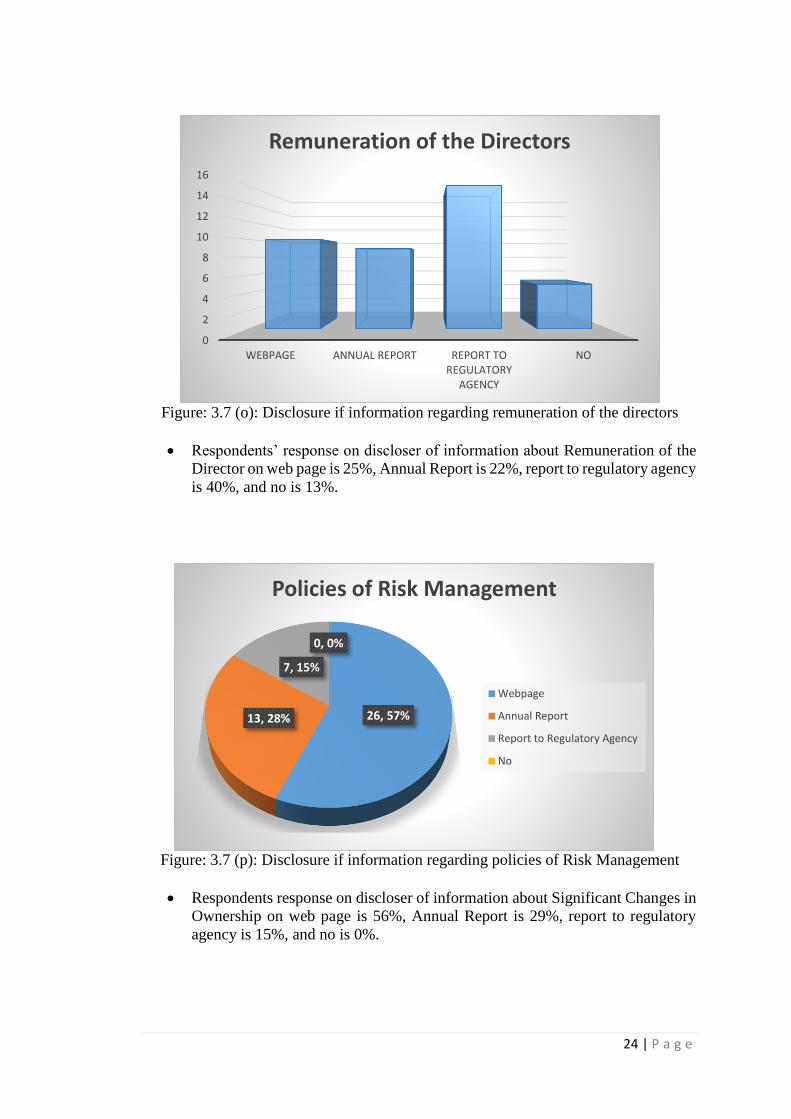

Figure: 3.7 (o): Disclosure if information regarding remuneration of the directors

Respondents’ response on discloser of information about Remuneration of the

Director on web page is 25%, Annual Report is 22%, report to regulatory agency

is 40%, and no is 13%.

Figure: 3.7 (p): Disclosure if information regarding policies of Risk Management

Respondents response on discloser of information about Significant Changes in

Ownership on web page is 56%, Annual Report is 29%, report to regulatory

agency is 15%, and no is 0%.

0

2

4

6

8

10

12

14

16

WEBPAGE ANNUAL REPORT REPORT TO REGULATORY

AGENCY

NO

Remuneration of the Directors

26, 57%13, 28%

7, 15%

0, 0%

Policies of Risk Management

Webpage

Annual Report

Report to Regulatory Agency

No

25 | P a g e

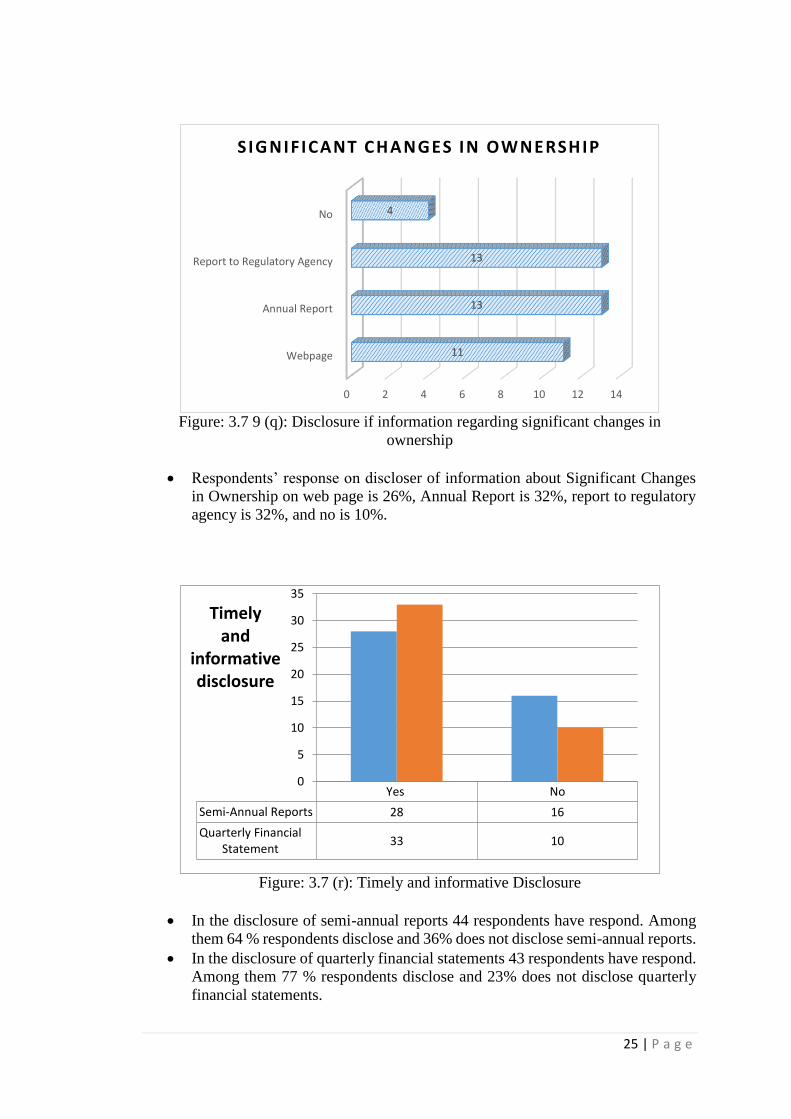

Figure: 3.7 9 (q): Disclosure if information regarding significant changes in

ownership

Respondents’ response on discloser of information about Significant Changes

in Ownership on web page is 26%, Annual Report is 32%, report to regulatory

agency is 32%, and no is 10%.

Figure: 3.7 (r): Timely and informative Disclosure

In the disclosure of semi-annual reports 44 respondents have respond. Among

them 64 % respondents disclose and 36% does not disclose semi-annual reports.

In the disclosure of quarterly financial statements 43 respondents have respond.

Among them 77 % respondents disclose and 23% does not disclose quarterly

financial statements.

Yes No

Semi-Annual Reports 28 16

Quarterly FinancialStatement

33 10

0

5

10

15

20

25

30

35

Timelyand

informativedisclosure

0 2 4 6 8 10 12 14

Webpage

Annual Report

Report to Regulatory Agency

No

11

13

13

4

SIG NIFICANT CHANGES IN OWNERSHIP

26 | P a g e

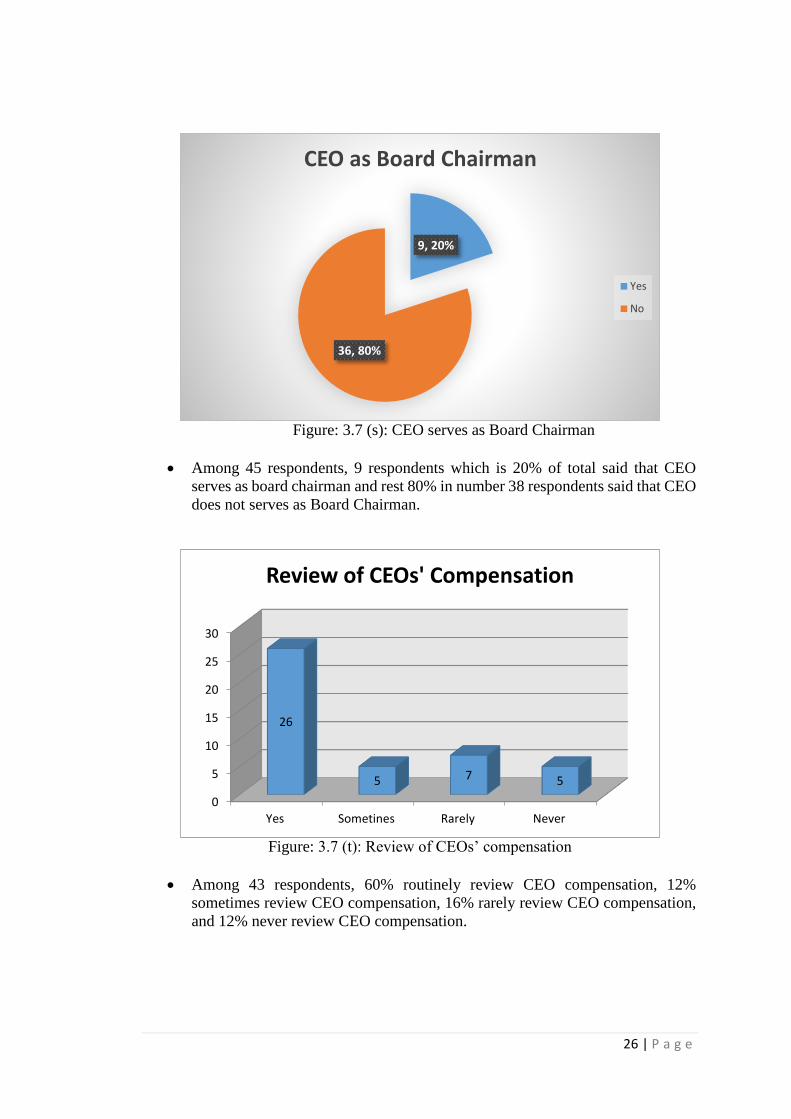

Figure: 3.7 (s): CEO serves as Board Chairman

Among 45 respondents, 9 respondents which is 20% of total said that CEO

serves as board chairman and rest 80% in number 38 respondents said that CEO

does not serves as Board Chairman.

Figure: 3.7 (t): Review of CEOs’ compensation

Among 43 respondents, 60% routinely review CEO compensation, 12%

sometimes review CEO compensation, 16% rarely review CEO compensation,

and 12% never review CEO compensation.

9, 20%

36, 80%

CEO as Board Chairman

Yes

No

0

5

10

15

20

25

30

Yes Sometines Rarely Never

26

5 7 5

Review of CEOs' Compensation

27 | P a g e

Figure: 3.7 (u): Stock option for the CEO

Among 45 respondents, 9% says that Banks Provide substantial Stock option

for CEO, 38% says that banks provide some or little stock option for CEO, and

53% says that banks provide no stock option for CEO.

Figure: 3.7 (v): Prevalence of the practices

Among 44 respondents, response on a (independent directors altering or adding

the board meeting agenda) often 18%, sometimes 48%, rarely 20%, never 14%.

Among 43 respondents, response on b (independent directors’ participation

actively in board discussion) often 47%, sometimes 34%, rarely 19% and never

0%.

Among44 respondents, response on c (agenda items disapproved at the board

meeting by independent directors) often 25%, sometimes 48%, rarely 25% and

never 2%.

0 5 10 15 20 25

Substantially

Some

None

4

17

24

Stock Option of CEO

0

5

10

15

20

25

Often Sometimes Rarely Never

8

21

9

6

20

15

8

0

11

21

11

1

Prevalence of the practices

a

b

c

28 | P a g e

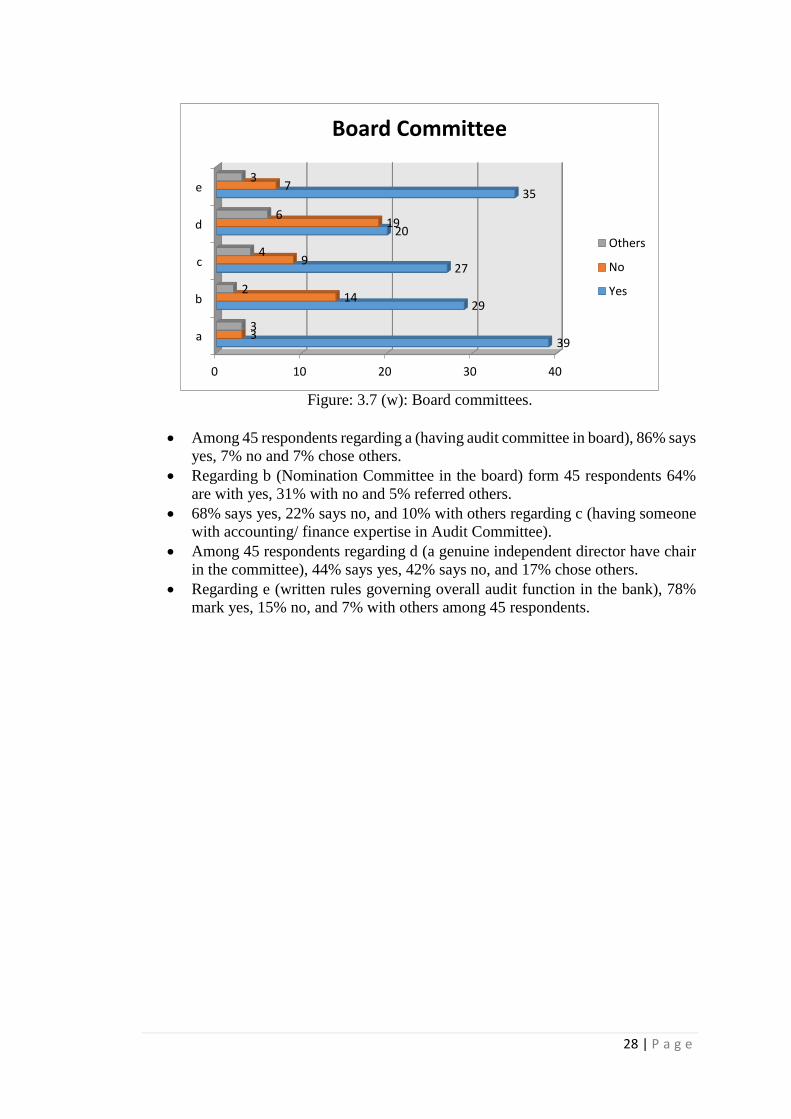

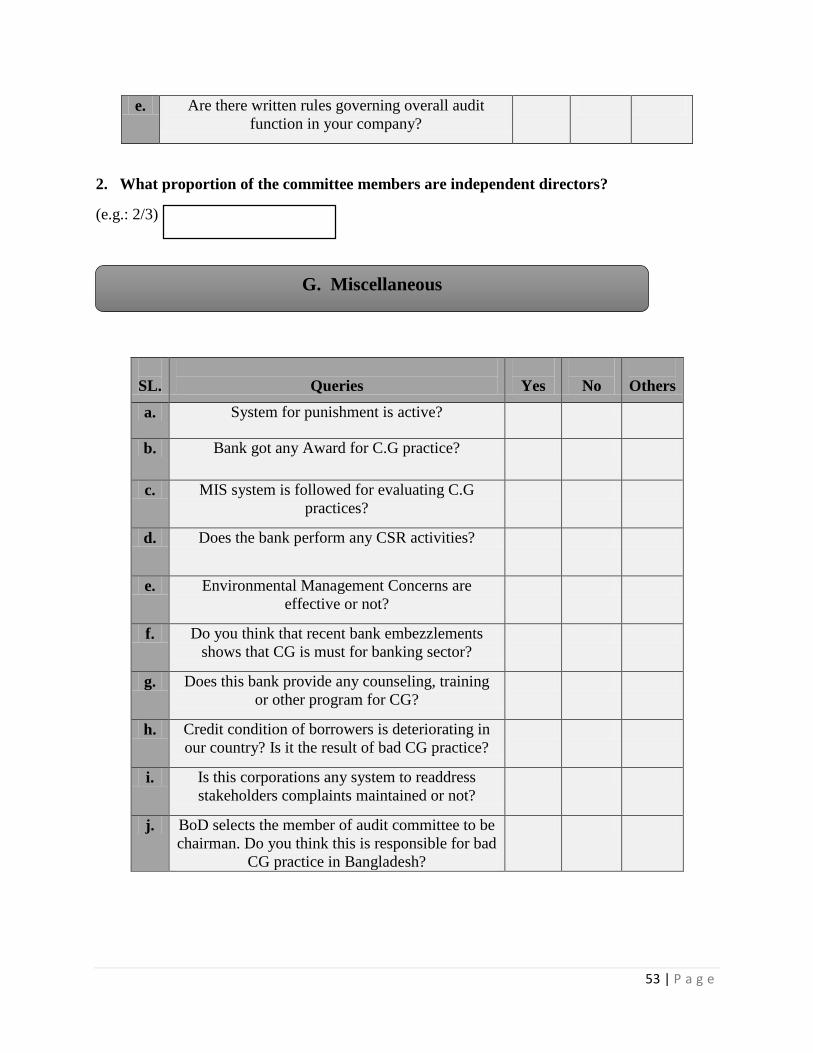

Figure: 3.7 (w): Board committees.

Among 45 respondents regarding a (having audit committee in board), 86% says

yes, 7% no and 7% chose others.

Regarding b (Nomination Committee in the board) form 45 respondents 64%

are with yes, 31% with no and 5% referred others.

68% says yes, 22% says no, and 10% with others regarding c (having someone

with accounting/ finance expertise in Audit Committee).

Among 45 respondents regarding d (a genuine independent director have chair

in the committee), 44% says yes, 42% says no, and 17% chose others.

Regarding e (written rules governing overall audit function in the bank), 78%

mark yes, 15% no, and 7% with others among 45 respondents.

0 10 20 30 40

a

b

c

d

e

39

29

27

20

35

3

14

9

19

7

3

2

4

6

3

Board Committee

Others

No

Yes

29 | P a g e

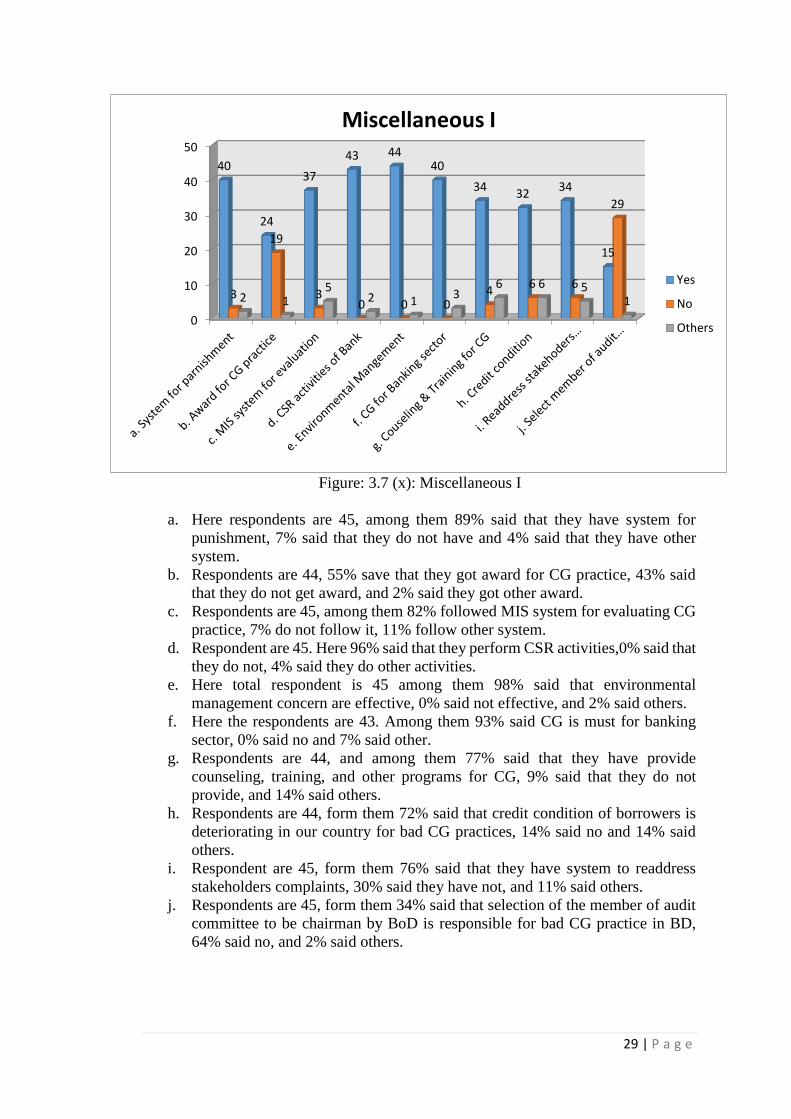

Figure: 3.7 (x): Miscellaneous I

a. Here respondents are 45, among them 89% said that they have system for

punishment, 7% said that they do not have and 4% said that they have other

system.

b. Respondents are 44, 55% save that they got award for CG practice, 43% said

that they do not get award, and 2% said they got other award.

c. Respondents are 45, among them 82% followed MIS system for evaluating CG

practice, 7% do not follow it, 11% follow other system.

d. Respondent are 45. Here 96% said that they perform CSR activities,0% said that

they do not, 4% said they do other activities.

e. Here total respondent is 45 among them 98% said that environmental

management concern are effective, 0% said not effective, and 2% said others.

f. Here the respondents are 43. Among them 93% said CG is must for banking

sector, 0% said no and 7% said other.

g. Respondents are 44, and among them 77% said that they have provide

counseling, training, and other programs for CG, 9% said that they do not

provide, and 14% said others.

h. Respondents are 44, form them 72% said that credit condition of borrowers is

deteriorating in our country for bad CG practices, 14% said no and 14% said

others.

i. Respondent are 45, form them 76% said that they have system to readdress

stakeholders complaints, 30% said they have not, and 11% said others.

j. Respondents are 45, form them 34% said that selection of the member of audit

committee to be chairman by BoD is responsible for bad CG practice in BD,

64% said no, and 2% said others.

0

10

20

30

40

50

40

24

37

43 4440

3432

34

15

3

19

30 0 0

46 6

29

2 15

2 13

6 6 51

Miscellaneous I

Yes

No

Others

30 | P a g e

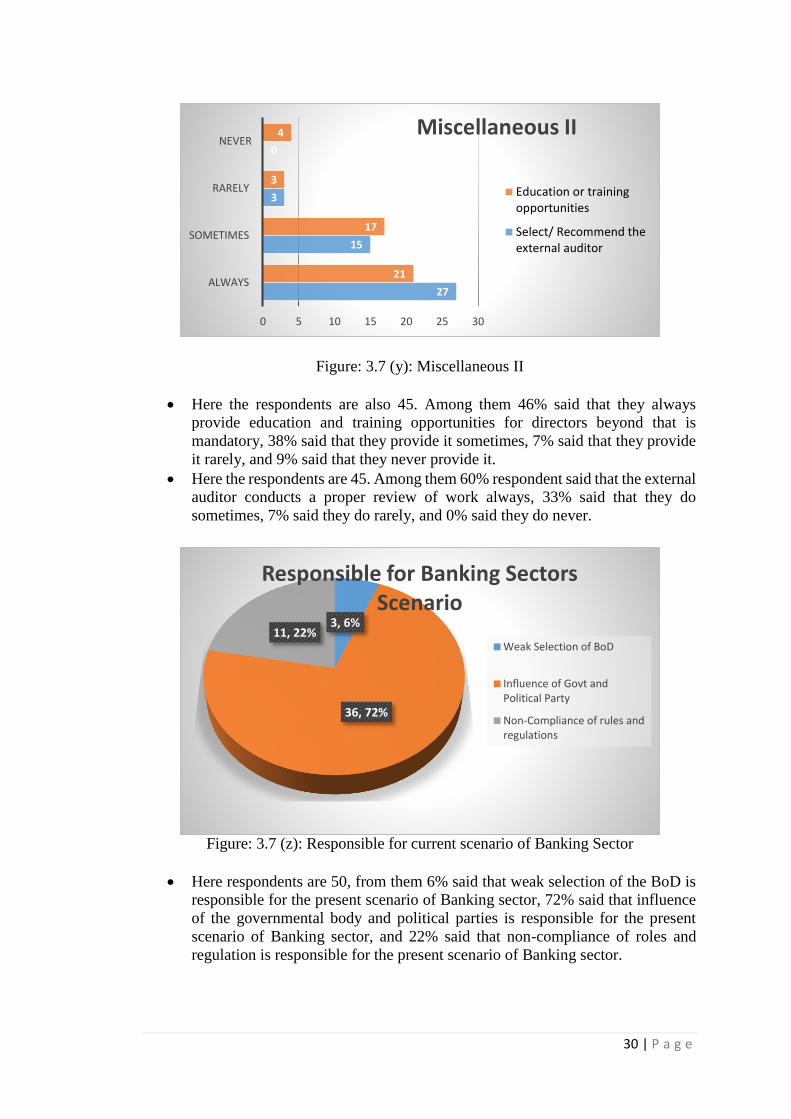

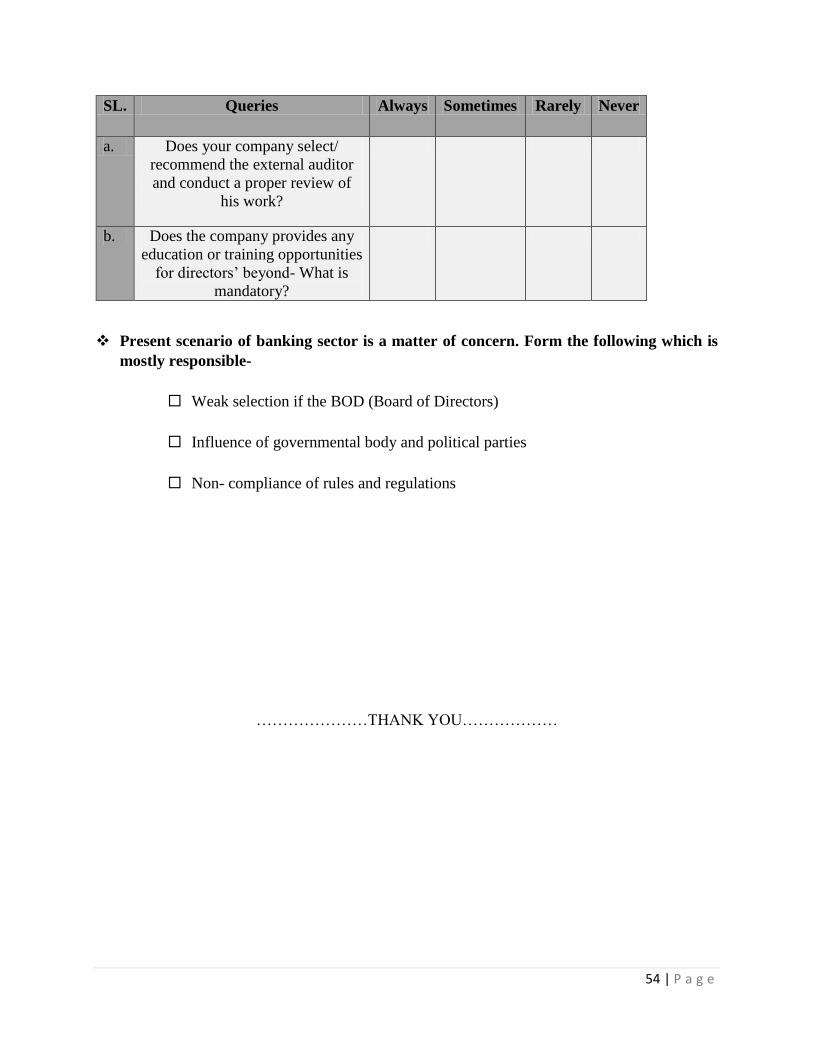

Figure: 3.7 (y): Miscellaneous II

Here the respondents are also 45. Among them 46% said that they always

provide education and training opportunities for directors beyond that is

mandatory, 38% said that they provide it sometimes, 7% said that they provide

it rarely, and 9% said that they never provide it.

Here the respondents are 45. Among them 60% respondent said that the external

auditor conducts a proper review of work always, 33% said that they do

sometimes, 7% said they do rarely, and 0% said they do never.

Figure: 3.7 (z): Responsible for current scenario of Banking Sector

Here respondents are 50, from them 6% said that weak selection of the BoD is

responsible for the present scenario of Banking sector, 72% said that influence

of the governmental body and political parties is responsible for the present

scenario of Banking sector, and 22% said that non-compliance of roles and

regulation is responsible for the present scenario of Banking sector.

27

15

3

0

21

17

3

4

0 5 10 15 20 25 30

ALWAYS

SOMETIMES

RARELY

NEVERMiscellaneous II

Education or trainingopportunities

Select/ Recommend theexternal auditor

3, 6%

36, 72%

11, 22%

Responsible for Banking Sectors Scenario

Weak Selection of BoD

Influence of Govt andPolitical Party

Non-Compliance of rules andregulations

31 | P a g e

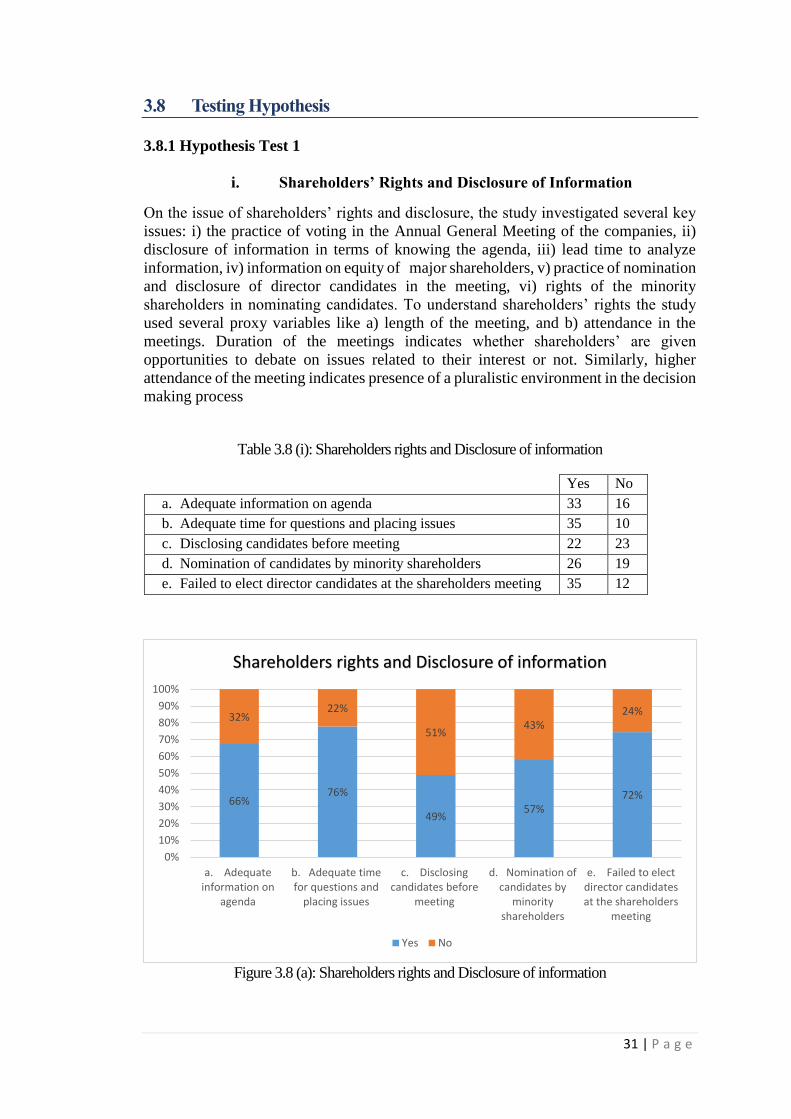

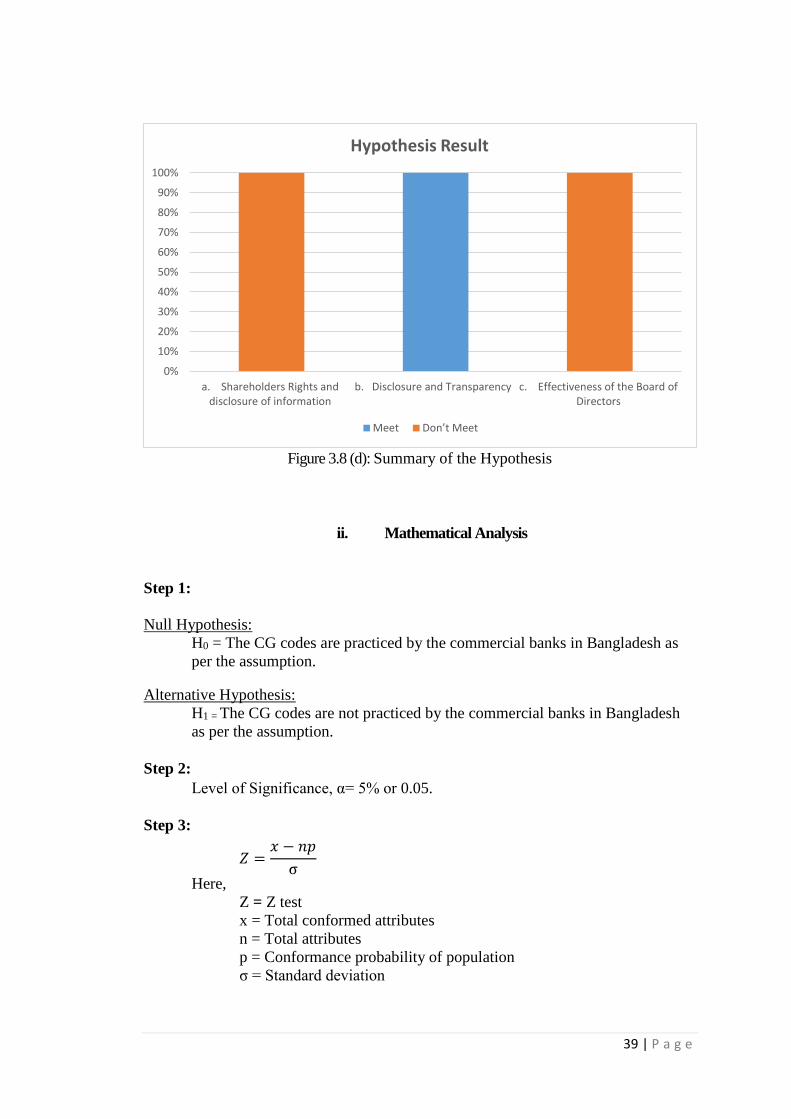

3.8 Testing Hypothesis

3.8.1 Hypothesis Test 1

i. Shareholders’ Rights and Disclosure of Information

On the issue of shareholders’ rights and disclosure, the study investigated several key

issues: i) the practice of voting in the Annual General Meeting of the companies, ii)

disclosure of information in terms of knowing the agenda, iii) lead time to analyze

information, iv) information on equity of major shareholders, v) practice of nomination

and disclosure of director candidates in the meeting, vi) rights of the minority

shareholders in nominating candidates. To understand shareholders’ rights the study

used several proxy variables like a) length of the meeting, and b) attendance in the

meetings. Duration of the meetings indicates whether shareholders’ are given

opportunities to debate on issues related to their interest or not. Similarly, higher

attendance of the meeting indicates presence of a pluralistic environment in the decision

making process

Table 3.8 (i): Shareholders rights and Disclosure of information

Yes No

a. Adequate information on agenda 33 16

b. Adequate time for questions and placing issues 35 10

c. Disclosing candidates before meeting 22 23

d. Nomination of candidates by minority shareholders 26 19

e. Failed to elect director candidates at the shareholders meeting 35 12

Figure 3.8 (a): Shareholders rights and Disclosure of information

66%76%

49%57%

72%

32%22%

51%43%

24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

a. Adequateinformation on

agenda

b. Adequate timefor questions and

placing issues

c. Disclosingcandidates before

meeting

d. Nomination ofcandidates by

minorityshareholders

e. Failed to electdirector candidatesat the shareholders

meeting

Shareholders rights and Disclosure of information

Yes No

32 | P a g e

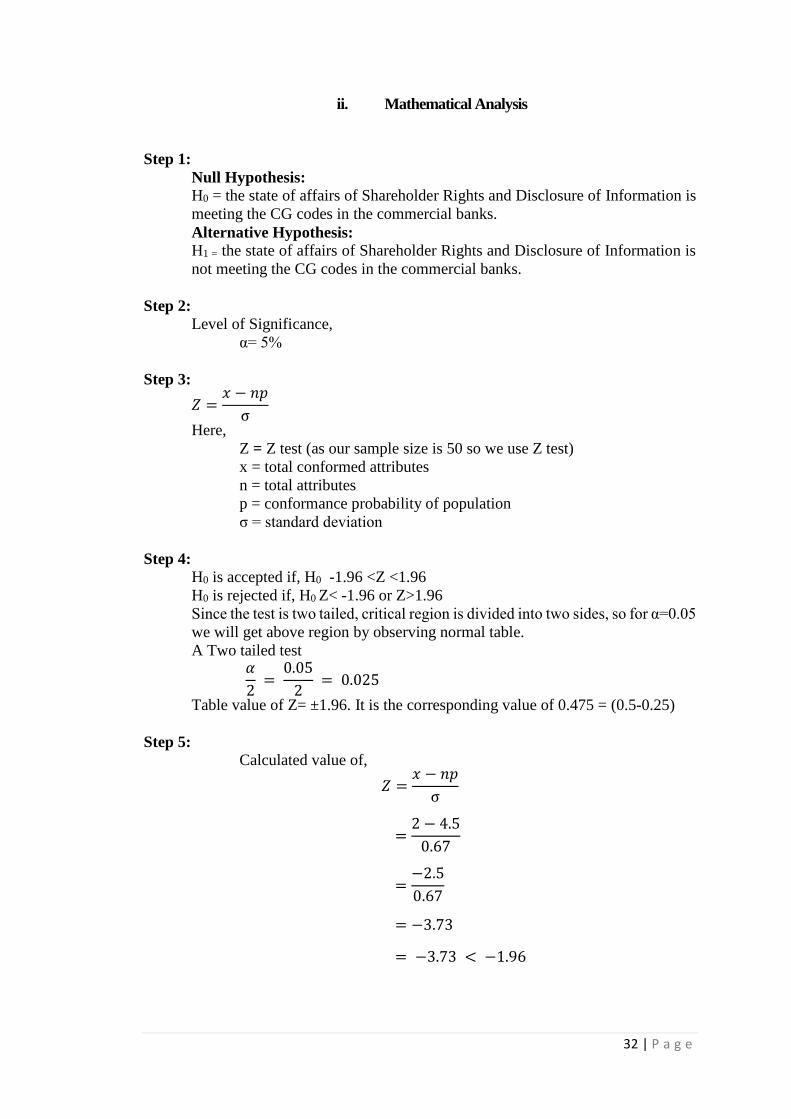

ii. Mathematical Analysis

Step 1:

Null Hypothesis:

H0 = the state of affairs of Shareholder Rights and Disclosure of Information is

meeting the CG codes in the commercial banks.

Alternative Hypothesis:

H1 = the state of affairs of Shareholder Rights and Disclosure of Information is

not meeting the CG codes in the commercial banks.

Step 2:

Level of Significance,

α= 5%

Step 3:

𝑍 =𝑥 − 𝑛𝑝

σ

Here,

Z = Z test (as our sample size is 50 so we use Z test)

x = total conformed attributes

n = total attributes

p = conformance probability of population

σ = standard deviation

Step 4:

H0 is accepted if, H0 -1.96 <Z <1.96

H0 is rejected if, H0 Z< -1.96 or Z>1.96

Since the test is two tailed, critical region is divided into two sides, so for α=0.05

we will get above region by observing normal table.

A Two tailed test 𝛼

2 =

0.05

2 = 0.025

Table value of Z= ±1.96. It is the corresponding value of 0.475 = (0.5-0.25)

Step 5:

Calculated value of,

𝑍 =𝑥 − 𝑛𝑝

σ

=2 − 4.5

0.67

=−2.5

0.67

= −3.73

= −3.73 < −1.96

33 | P a g e

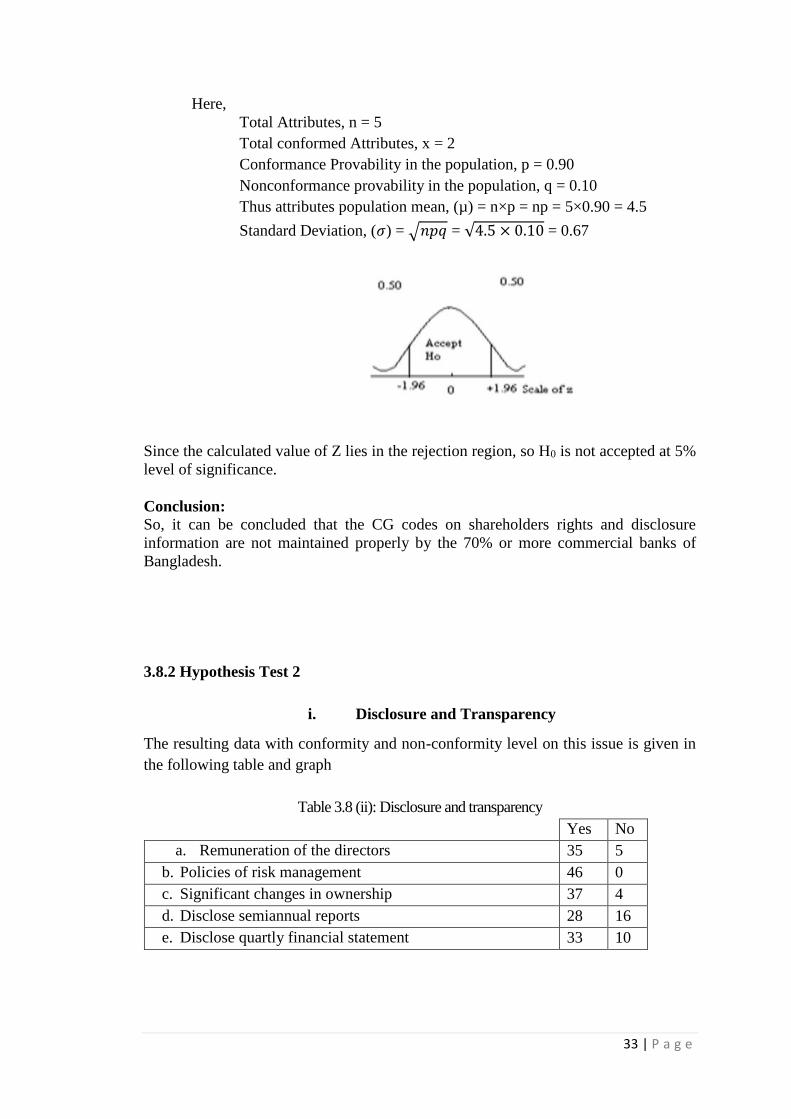

Here,

Total Attributes, n = 5

Total conformed Attributes, x = 2

Conformance Provability in the population, p = 0.90

Nonconformance provability in the population, q = 0.10

Thus attributes population mean, (µ) = n×p = np = 5×0.90 = 4.5

Standard Deviation, (𝜎) = √𝑛𝑝𝑞 = √4.5 × 0.10 = 0.67

Since the calculated value of Z lies in the rejection region, so H0 is not accepted at 5%

level of significance.

Conclusion:

So, it can be concluded that the CG codes on shareholders rights and disclosure

information are not maintained properly by the 70% or more commercial banks of

Bangladesh.

3.8.2 Hypothesis Test 2

i. Disclosure and Transparency

The resulting data with conformity and non-conformity level on this issue is given in

the following table and graph

Table 3.8 (ii): Disclosure and transparency

Yes No

a. Remuneration of the directors 35 5

b. Policies of risk management 46 0

c. Significant changes in ownership 37 4

d. Disclose semiannual reports 28 16

e. Disclose quartly financial statement 33 10

34 | P a g e

Figure 3.8 (b): Disclosure and transparency

ii. Mathematical Analysis

Step 1:

Null Hypothesis:

H0 = the state of affairs for Disclosure and Transparency is being met the CG

codes by the commercial banks.

Alternative Hypothesis:

H1 = the state of affairs for Disclosure and Transparency is not being met the CG

codes by the commercial banks.

Step 2:

Level of Significance,

α= 5%

Step 3:

𝑍 =𝑥 − 𝑛𝑝

σ

Here,

Z = Z test

x = total conformed attributes

n = total attributes

p = conformance probability of population

σ = standard deviation

Step 4:

H0 is accepted if H0 if -1.96 <Z <1.96

H0 is rejected if H0 Z< -1.96 or Z>1.96

Since the test is two tailed, critical region is divided into two sides, so for α=0.05

we will get above region by observing normal table.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

a.Remunerationof the directors

b. Policies ofrisk

management

c. Significantchanges inownership

d. Disclosesemiannual

reports

e. Disclosequartly financial

statement

87.5%100%

90%

64%77%

12.5%0

10%

36%23%

Disclosure and transparenacy

Yes No

35 | P a g e

A Two tailed test 𝛼

2 =

0.05

2 = 0.025

Table value of Z= ±1.96. It is the corresponding value of 0.475 = (0.5-0.25)

Step 5:

Calculated value of,

𝑍 =𝑥 − 𝑛𝑝

σ

=4 − 4.5

0.67

=−0.5

0.67

= −0.75

= −1.96 < −0.75 < 1.96 Here,

Total Attributes, n = 5

Total conformed Attributes, x = 4

Conformance Provability in the population, p = 0.90

Nonconformance provability in the population, q = 0.10

Thus attributes population mean, (µ) = n×p = np = 5×0.90 = 4.5

Standard Deviation, (𝜎) = √𝑛𝑝𝑞 = √4.5 × 0.10 = 0.67

Since the calculated value of Z lies in the acceptance region, so H0 is accepted at 5%

level of significance.

Conclusion:

So, it can be concluded that the CG codes on disclosure and transparency are maintained

properly by the 70% or more commercial banks of Bangladesh.

36 | P a g e

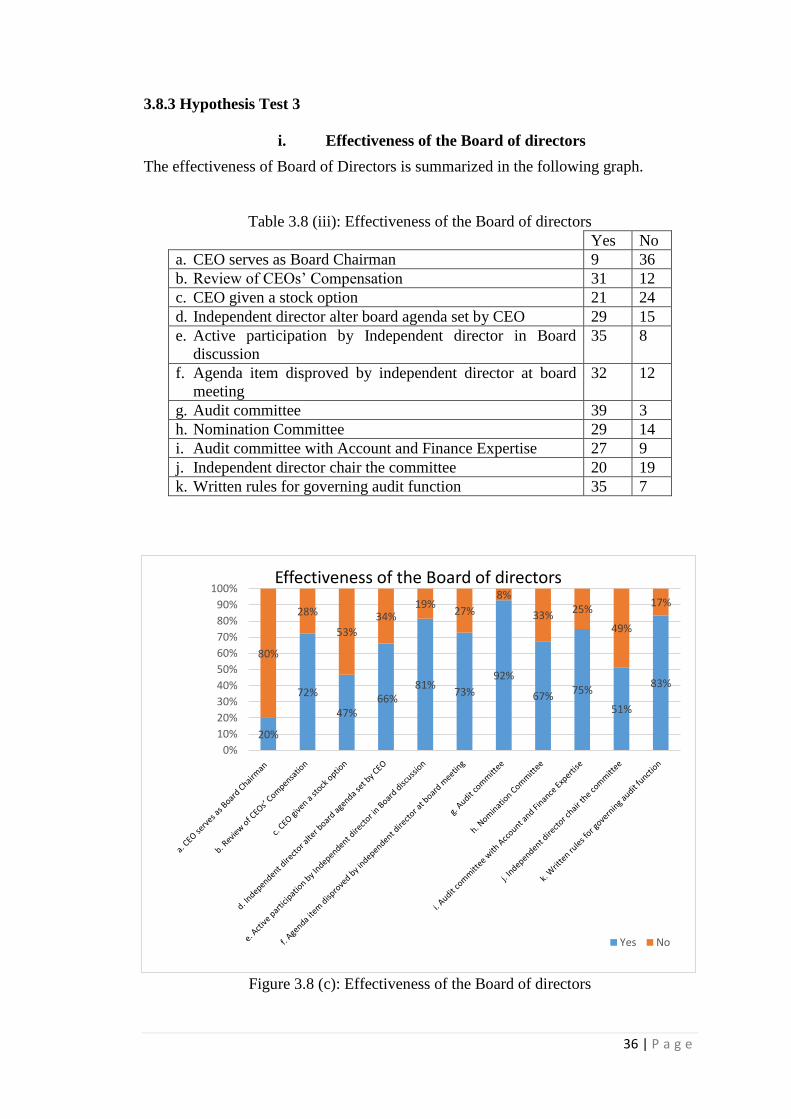

3.8.3 Hypothesis Test 3

i. Effectiveness of the Board of directors

The effectiveness of Board of Directors is summarized in the following graph.

Table 3.8 (iii): Effectiveness of the Board of directors

Yes No

a. CEO serves as Board Chairman 9 36

b. Review of CEOs’ Compensation 31 12

c. CEO given a stock option 21 24

d. Independent director alter board agenda set by CEO 29 15

e. Active participation by Independent director in Board

discussion

35 8

f. Agenda item disproved by independent director at board

meeting

32 12

g. Audit committee 39 3

h. Nomination Committee 29 14

i. Audit committee with Account and Finance Expertise 27 9

j. Independent director chair the committee 20 19

k. Written rules for governing audit function 35 7

Figure 3.8 (c): Effectiveness of the Board of directors

20%

72%

47%66%

81%73%

92%

67%75%

51%

83%

80%

28%

53%

34%19%

27%

8%

33%25%

49%

17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Effectiveness of the Board of directors

Yes No

37 | P a g e

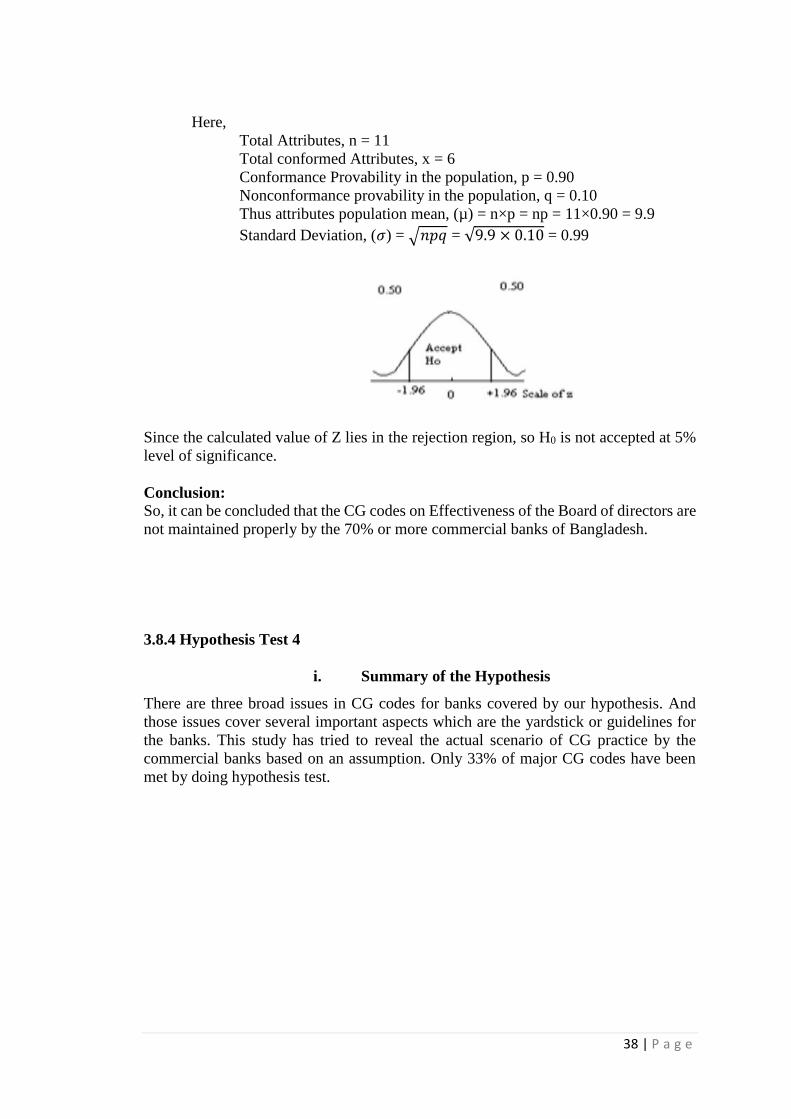

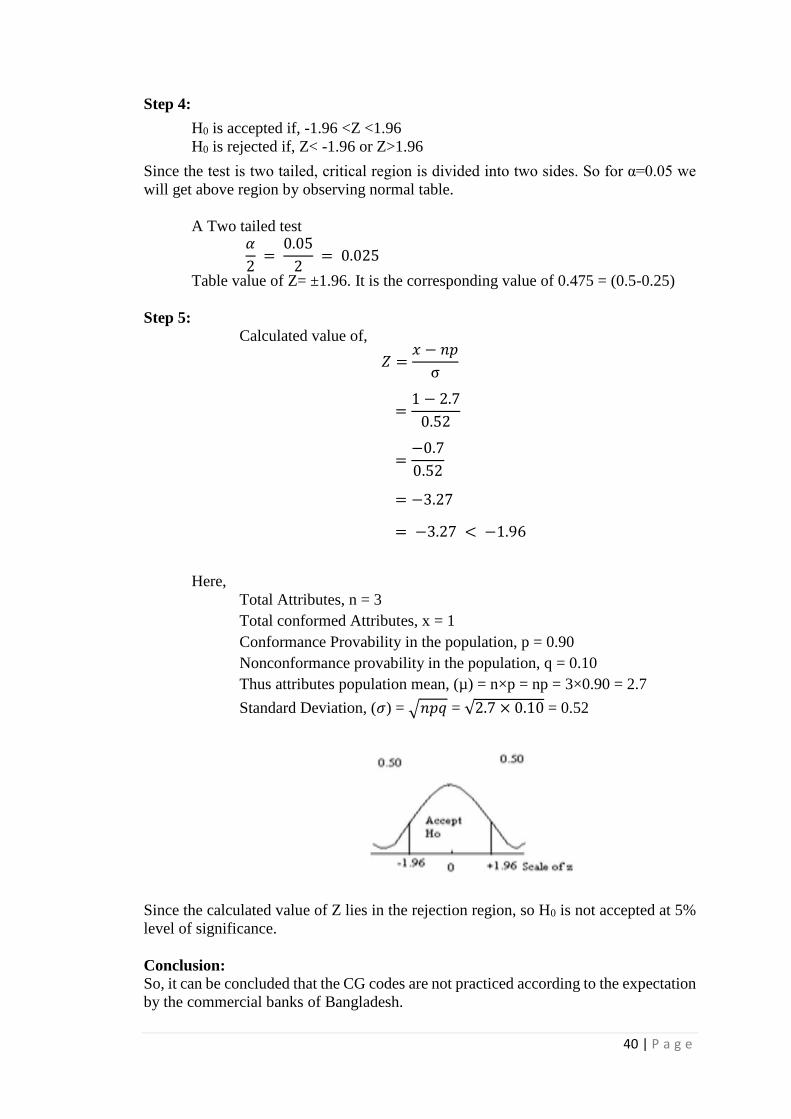

ii. Mathematical Analysis

Step 1:

Null Hypothesis:

H0 = The state of affairs of Effectiveness of the Board of directors is meeting

the CG codes in the commercial banks.

Alternative Hypothesis:

H1 = The state of affairs of Effectiveness of the Board of directors is not meeting

the CG codes in the commercial banks.

Step 2:

Level of Significance, α= 5% or 0.05.

Step 3:

𝑍 =𝑥 − 𝑛𝑝

σ

Here,

Z = Z test

x = total conformed attributes

n = total attributes

p = conformance probability of population

σ = standard deviation

Step 4:

H0 is accepted if, -1.96 <Z <1.96

H0 is rejected if, Z< -1.96 or Z>1.96