cfo 221015 slide deck - financial mutuals

TRANSCRIPT

CFO NETWORK22ND OCTOBER 2015

!

CFO NETWORKHOST: JAMES BRENNAN, RATHBONES

TODAY’S CHAIR: MARTIN SHAW, AFM

!

TODAY’S AGENDA

ORSA: practical experiences and regulatory feedback, Mick Campbell, Deloitte

Working together to solve governance and operational challenges, Peter Bernie, Charles Taylor

AFM update, Martin Shaw, AFM

Bond Market Update, Noelle Cazalis, Rathbones

Solvency 2 calculation and reporting tools, Omar Ripon, Moore Stephens and Bo Orskov Koldenberg, Asseco

Solvency 2: accounting changes in UK GAAP and iFRS , Paul Bennett, Mazars

CFO NETWORK22ND OCTOBER 2015

!

PRECISE. PROVEN. PERFORMANCE.

Moore Stephens Solvency II engineDemonstration of calculation and reporting tool for Pillars 1- 3

Agenda

• Introduction to Moore Stephens SII engine • Demo of SII engine

Speakers

• Omar Ripon – Moore Stephens Partner– [email protected]– 020 7651 1151

• Bo Ørskov Koldenborg – Asseco Partner– [email protected]– +45 29 20 49 60

•

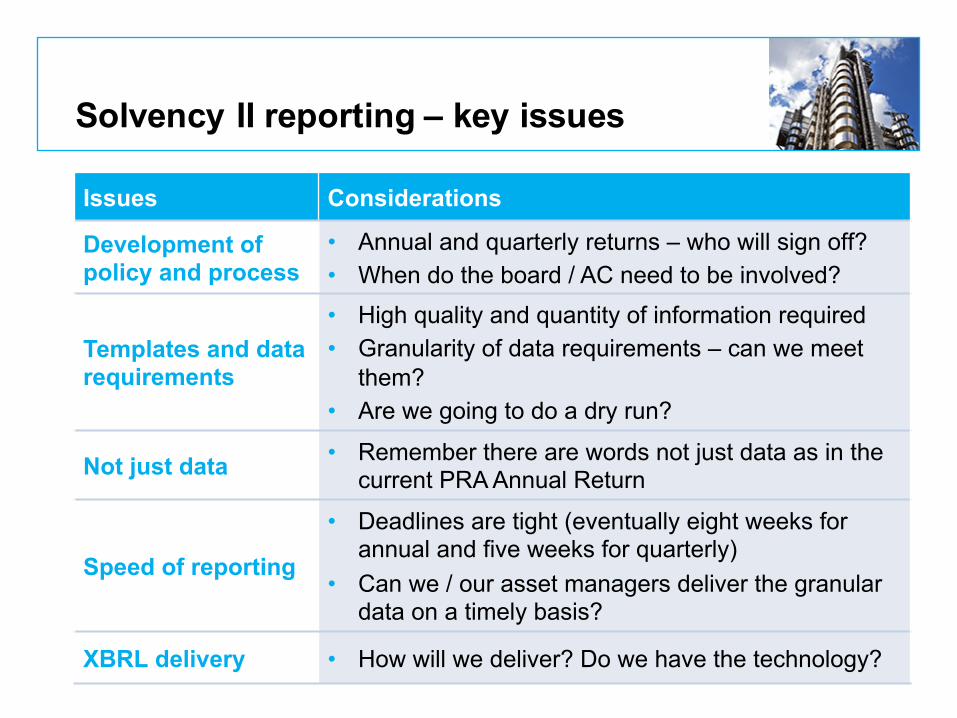

Solvency II reporting – key issues

Issues Considerations

Development of policy and process

• Annual and quarterly returns – who will sign off?• When do the board / AC need to be involved?

Templates and data requirements

• High quality and quantity of information required• Granularity of data requirements – can we meet

them?• Are we going to do a dry run?

Not just data • Remember there are words not just data as in the current PRA Annual Return

Speed of reporting

• Deadlines are tight (eventually eight weeks for annual and five weeks for quarterly)

• Can we / our asset managers deliver the granular data on a timely basis?

XBRL delivery • How will we deliver? Do we have the technology?

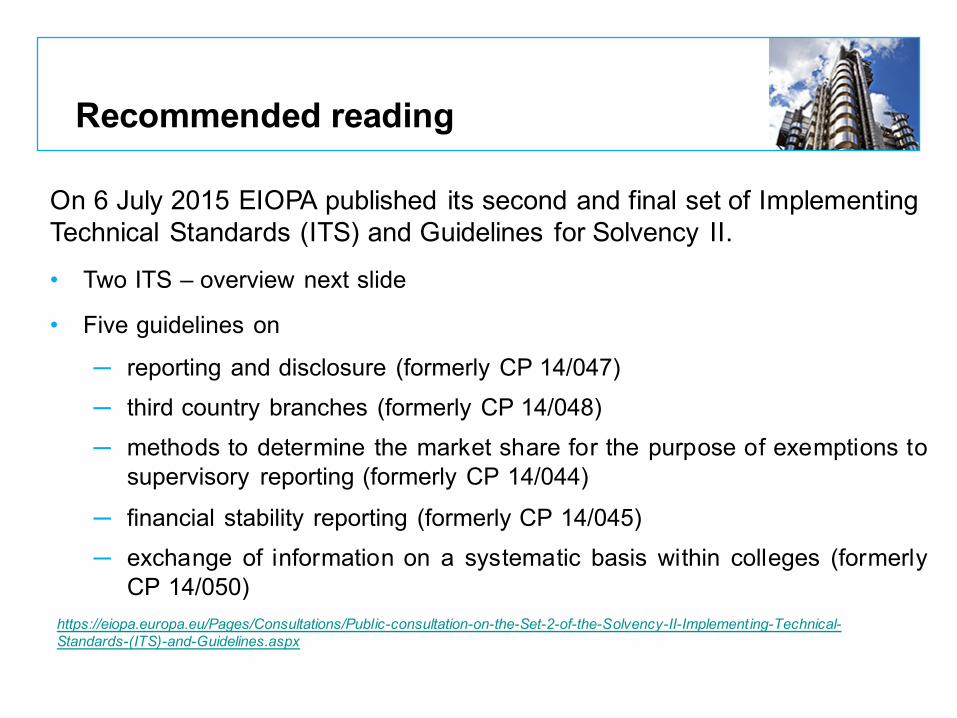

Recommended reading

On 6 July 2015 EIOPA published its second and final set of Implementing Technical Standards (ITS) and Guidelines for Solvency II.

• Two ITS – overview next slide

• Five guidelines on

─ reporting and disclosure (formerly CP 14/047)─ third country branches (formerly CP 14/048)─ methods to determine the market share for the purpose of exemptions to

supervisory reporting (formerly CP 14/044)

─ financial stability reporting (formerly CP 14/045)─ exchange of information on a systematic basis within colleges (formerly

CP 14/050)https://eiopa.europa.eu/Pages/Consultations/Public-consultation-on-the-Set-2-of-the-Solvency-II-Implementing-Technical-Standards-(ITS)-and-Guidelines.aspx

Pillar 3 – second set of ITS – July 2015

FormerCP ITS Key features

CP-14/052

Regular supervisory reporting

• The ITS sets out the templates to be submitted by (re)insurance undertakings and participating (re)insurance undertakings or insurance holding companies to NCAs. It defines:

• solo reporting• group reporting (general) and the reporting of risk concentration and

intra-group transactions in particular• a list of information to be reported• the templates and LOGs as annexes for:

─ day-1 reporting, ─ quarterly submissions; and─ annual submissions

CP-14/055

Public disclosure: procedures, formats and templates

Defines the procedures, formats and templates for public disclosure by (re)insurance undertakings and participating (re)insurance undertakings or insurance holding companies for the SFCR on a regular basis and on ad-hoc reporting following a major development which affects significantly the relevance of the information previously disclosed.

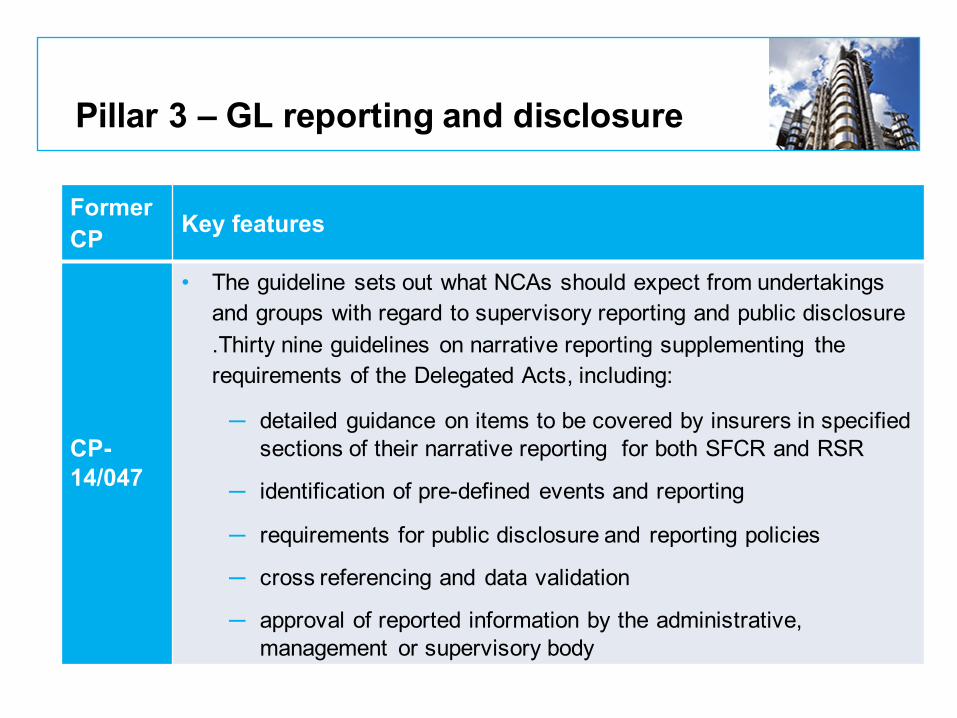

Pillar 3 – GL reporting and disclosure

FormerCP Key features

CP-14/047

• The guideline sets out what NCAs should expect from undertakings and groups with regard to supervisory reporting and public disclosure.Thirty nine guidelines on narrative reporting supplementing the requirements of the Delegated Acts, including:

─ detailed guidance on items to be covered by insurers in specified sections of their narrative reporting for both SFCR and RSR

─ identification of pre-defined events and reporting

─ requirements for public disclosure and reporting policies

─ cross referencing and data validation

─ approval of reported information by the administrative, management or supervisory body

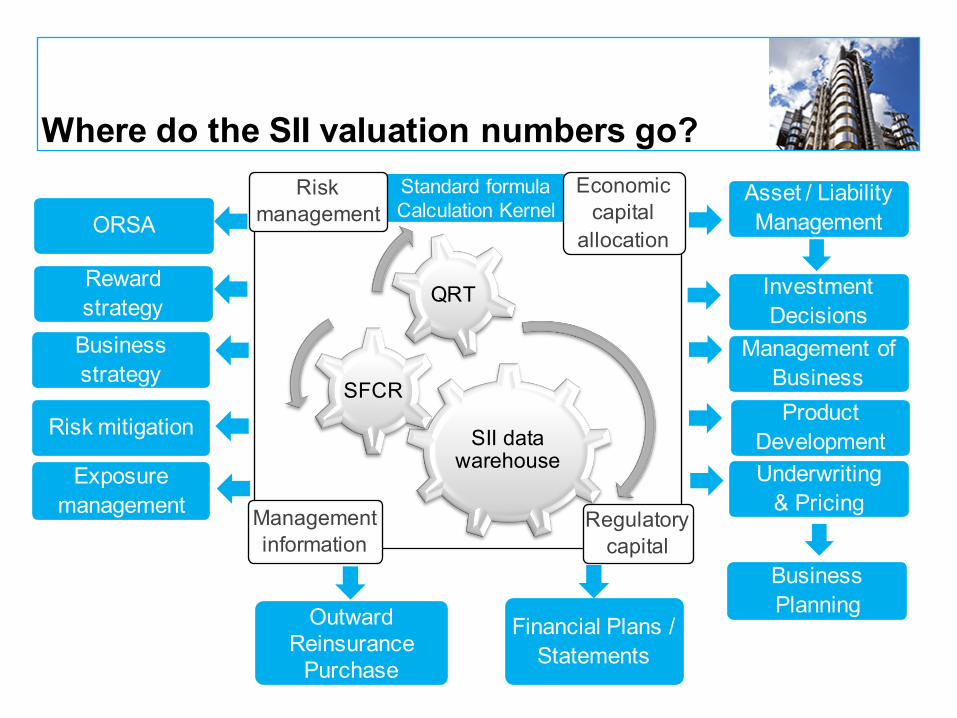

SII data warehouse

SFCR

QRT

Standard formula Calculation Kernel

Risk management

Management information

Economic capital

allocation

Regulatory capital

ORSA

Rewardstrategy

Business strategy

Risk mitigation

Exposure management

Outward Reinsurance

Purchase

Asset / Liability Management

Investment Decisions

Management of BusinessProduct

DevelopmentUnderwriting

& Pricing

Business Planning

Financial Plans / Statements

Where do the SII valuation numbers go?

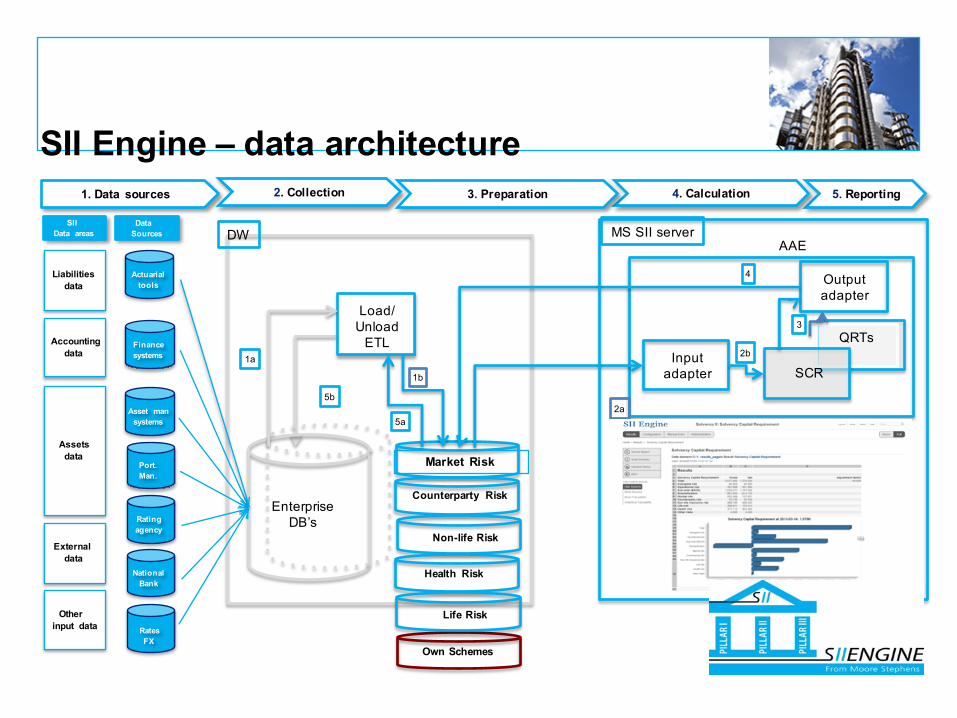

SII Engine – data architecture

SII Data areas

Assetsdata

Accountingdata

Liabilitiesdata

Externaldata

Otherinput data

Data Sources

Actuarialtools

Financesystems

Asset mansystems

Port.Man.

NationalBank

Ratingagency

RatesFX

1. Data sources 5. Reporting4. Calculation3. Preparation2. Collection

Load/Unload

ETL

EnterpriseDB’s

AAE

Inputadapter

Outputadapter

QRTs

SCR1a

3

5b

4

1b

5a2a

2b

MS SII serverDW

Market Risk

Counterparty Risk

Non-life Risk

Health Risk

Own Schemes

Life Risk

1410/28/15

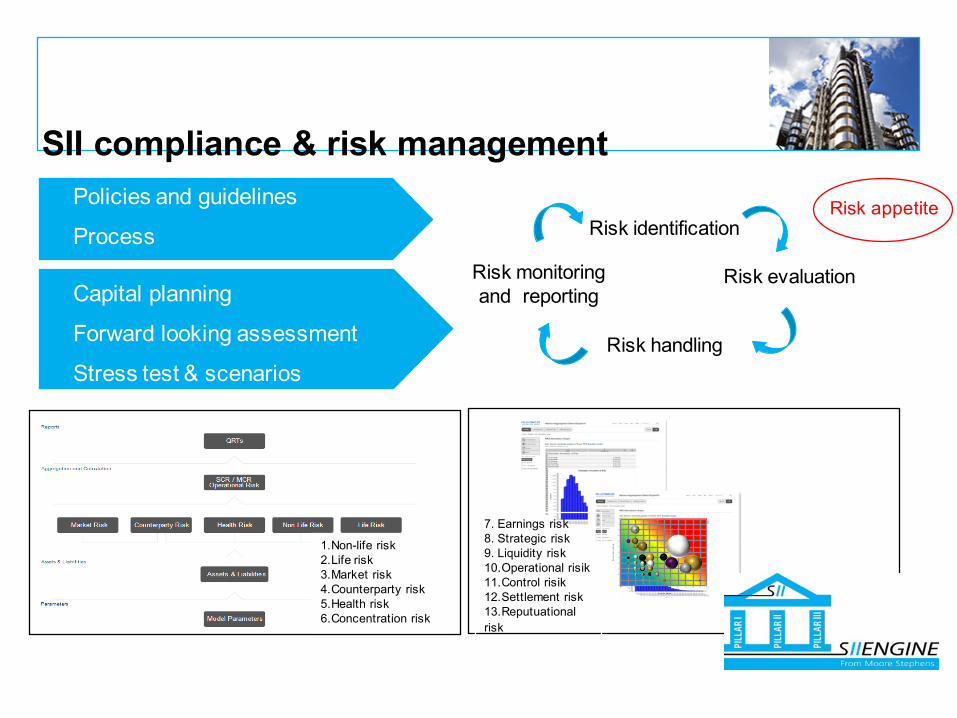

SII compliance & risk management

Risk identification

Risk evaluation

Risk handling

Risk monitoring and reporting

Risk appetite

0

1

2

3

4

5

6

7

8

9

1 0

1 1

1 2

0 1 2 3 4 5 6 7 8 9 1 0 1 1 1 2

Øk

on

om

isk

om

fan

g

S a n d s y n lig h ed

144

7. Earnings risk8. Strategic risk9. Liquidity risk10.Operational risik11.Control risik12.Settlement risk13.Reputuational risk

• Policies and guidelines

• Process

• Capital planning

• Forward looking assessment

• Stress test & scenarios

1.Non-life risk2.Life risk3.Market risk4.Counterparty risk5.Health risk6.Concentration risk

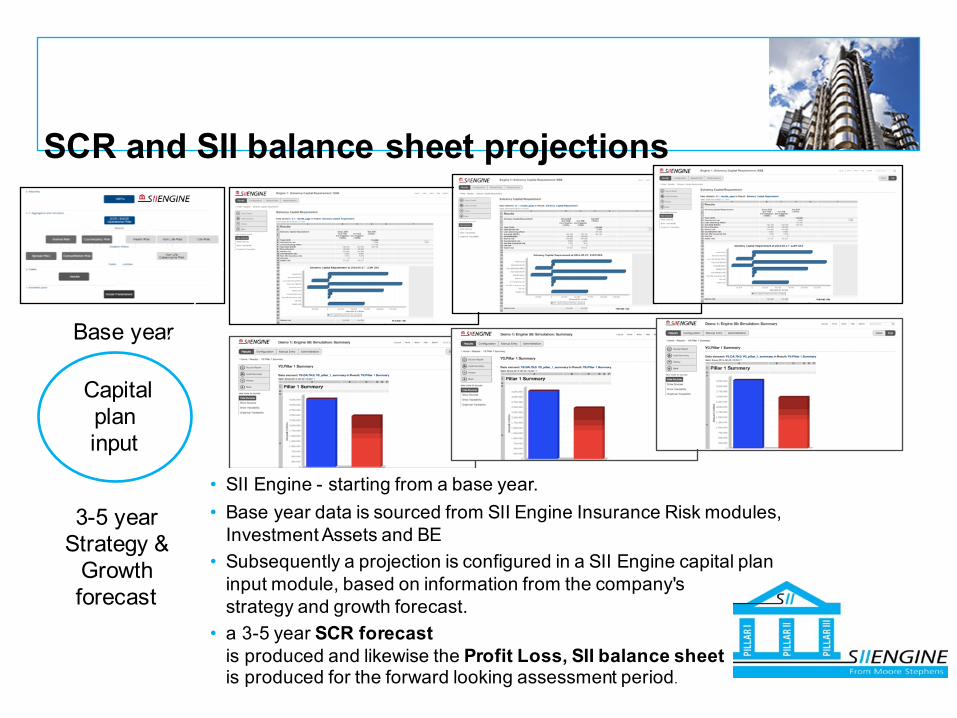

SCR and SII balance sheet projections

15

Base year

3-5 year Strategy &

Growth forecast

• SII Engine - starting from a base year.• Base year data is sourced from SII Engine Insurance Risk modules,

Investment Assets and BE • Subsequently a projection is configured in a SII Engine capital plan

input module, based on information from the company's strategy and growth forecast.

• a 3-5 year SCR forecastis produced and likewise the Profit Loss, SII balance sheetis produced for the forward looking assessment period.

Capital plan input

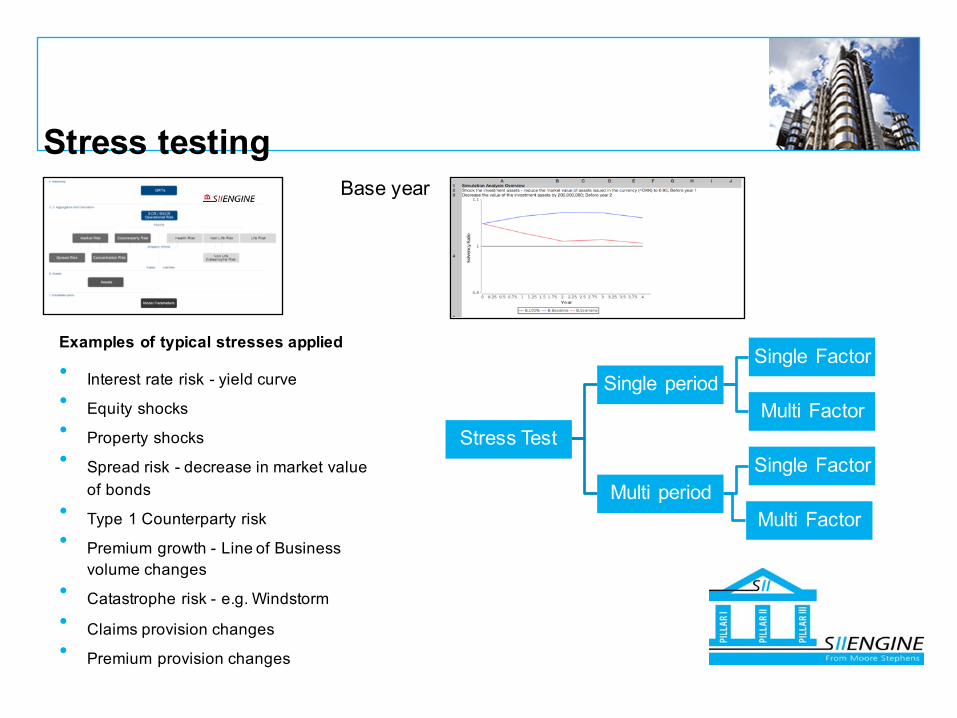

Stress testing

1610/28/15 www.assco.dk

Base year

Stress Test

Single period Single Factor

Multi Factor

Multi period Single Factor

Multi Factor

Examples of typical stresses applied

• Interest rate risk - yield curve• Equity shocks• Property shocks• Spread risk - decrease in market value

of bonds• Type 1 Counterparty risk• Premium growth - Line of Business

volume changes• Catastrophe risk - e.g. Windstorm• Claims provision changes• Premium provision changes

Custom reporting

1710/28/15

MI

• All risks• Company relevant risks• Risk per risk group or

risk driver• Top 10 risks• Risk maps

• Realised vs. Risk appetite

• Historic comparisons• Reports per risk

ambassador or risk owner

Variables can be customised to client specific requirements.

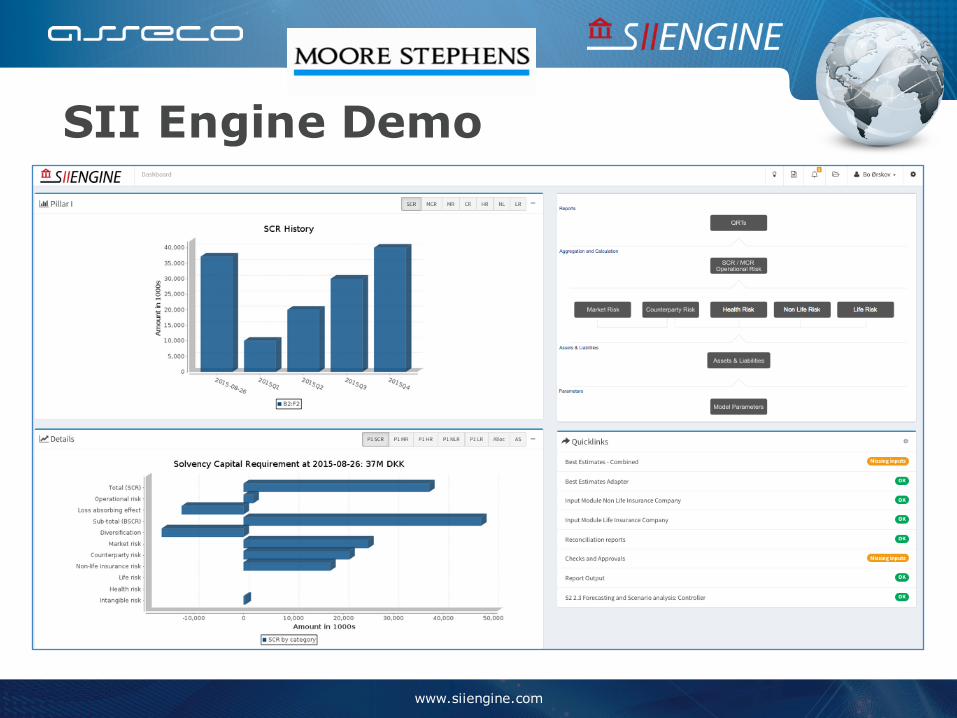

www.siiengine.com

SII Engine Demo

Bo Ørskov Koldenborg

1910/28/15 www.siiengine.com

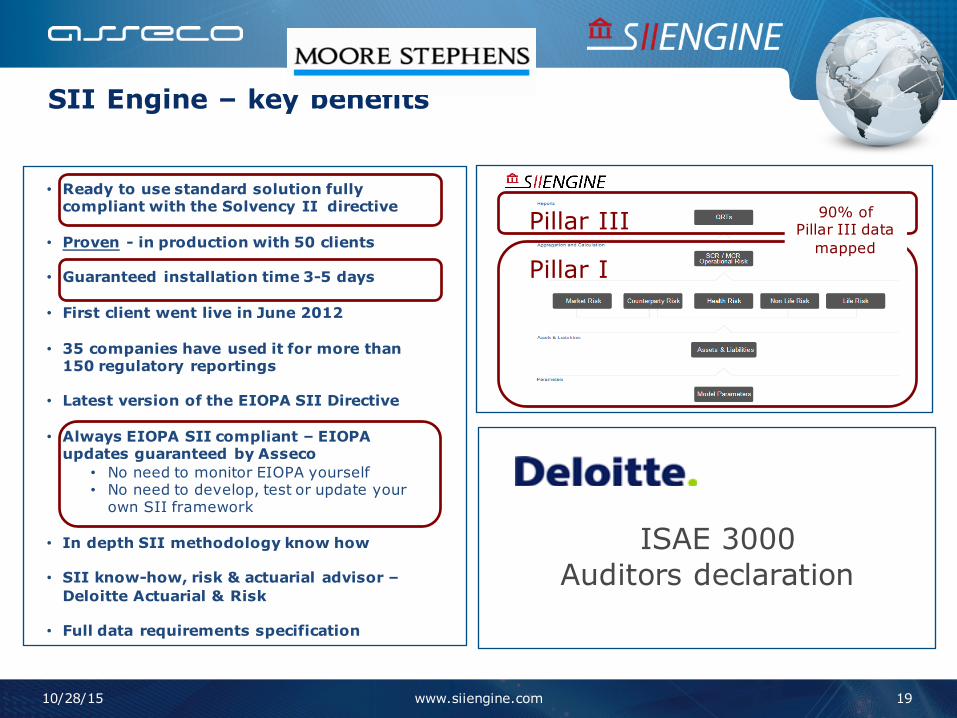

SII Engine – key benefits

• Ready to use standard solution fullycompliant with the Solvency II directive

• Proven - in production with 50 clients

• Guaranteed installation time 3-5 days

• First client went live in June 2012

• 35 companies have used it for more than150 regulatory reportings

• Latest version of the EIOPA SII Directive

• Always EIOPA SII compliant – EIOPA updates guaranteed by Asseco

• No need to monitor EIOPA yourself• No need to develop, test or update your

own SII framework

• In depth SII methodology know how

• SII know-how, risk & actuarial advisor –Deloitte Actuarial & Risk

• Full data requirements specification

Pillar I

Pillar III 90% of Pillar III data

mapped

ISAE 3000 Auditors declaration

2010/28/15 www.siiengine.com

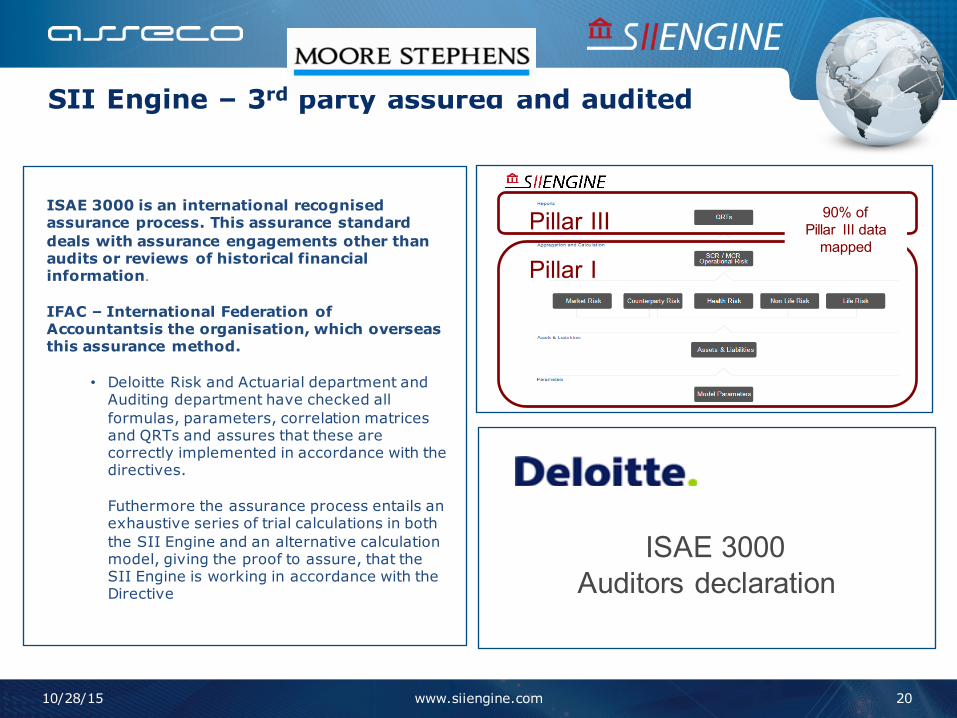

SII Engine – 3rd party assured and audited

ISAE 3000 is an international recognisedassurance process. This assurance standard deals with assurance engagements other thanaudits or reviews of historical financialinformation.

IFAC – International Federation of Accountantsis the organisation, which overseasthis assurance method.

• Deloitte Risk and Actuarial department and Auditing department have checked all formulas, parameters, correlation matrices and QRTs and assures that these arecorrectly implemented in accordance with the directives.

Futhermore the assurance process entails an exhaustive series of trial calculations in boththe SII Engine and an alternative calculationmodel, giving the proof to assure, that the SII Engine is working in accordance with the Directive

Pillar I

Pillar III 90% of Pillar III data

mapped

ISAE 3000 Auditors declaration

SII Engine Non-life and Health NSLT

21

www.asseco.dk

SII Data areas

Assetsdata

Accountingdata

Liabilitiesdata

External data

Other input data

Data Sources

Insurance systems

Financesystems

Asset mansystems

EDW

NationalBank

Ratingagency

RatesFX

1. Data sources 4. Reporting3. Calculation2. Collection and Preparation

Load/Unload

ETL

Outputadapter

Data Mart

Market Risk

Counterparty Risk

Health Risk

Own schemas

Life Risk

Claims prov. Cash flows

NL BE & Run offs

Send to Regulator in XBRL

Premium prov. Cash flows

NL BE

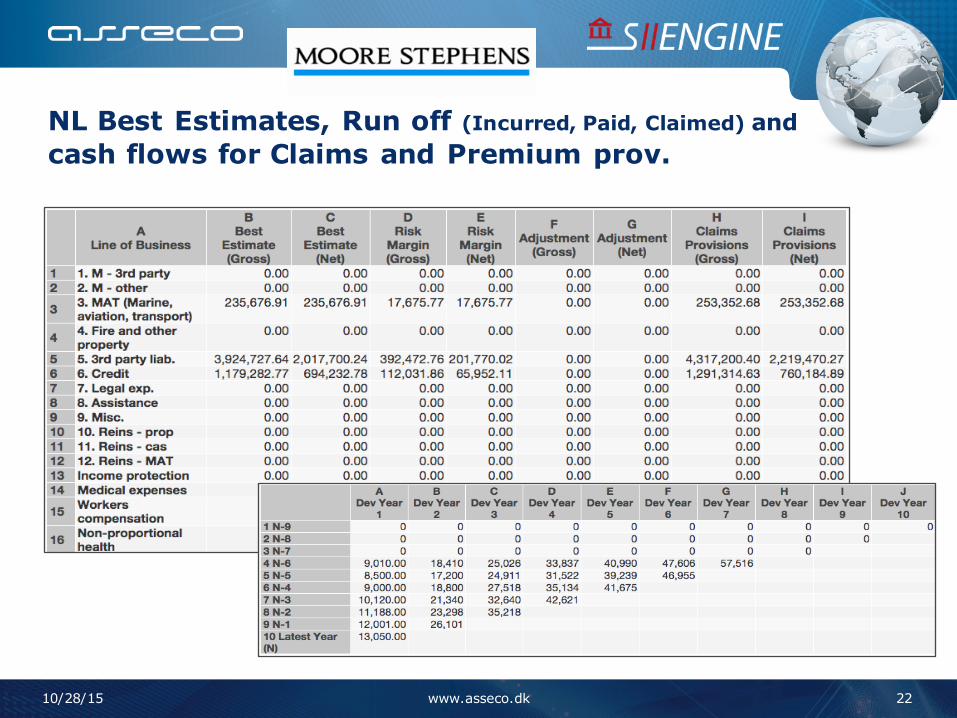

NL Best Estimates, Run off (Incurred, Paid, Claimed) and cash flows for Claims and Premium prov.

2210/28/15 www.asseco.dk

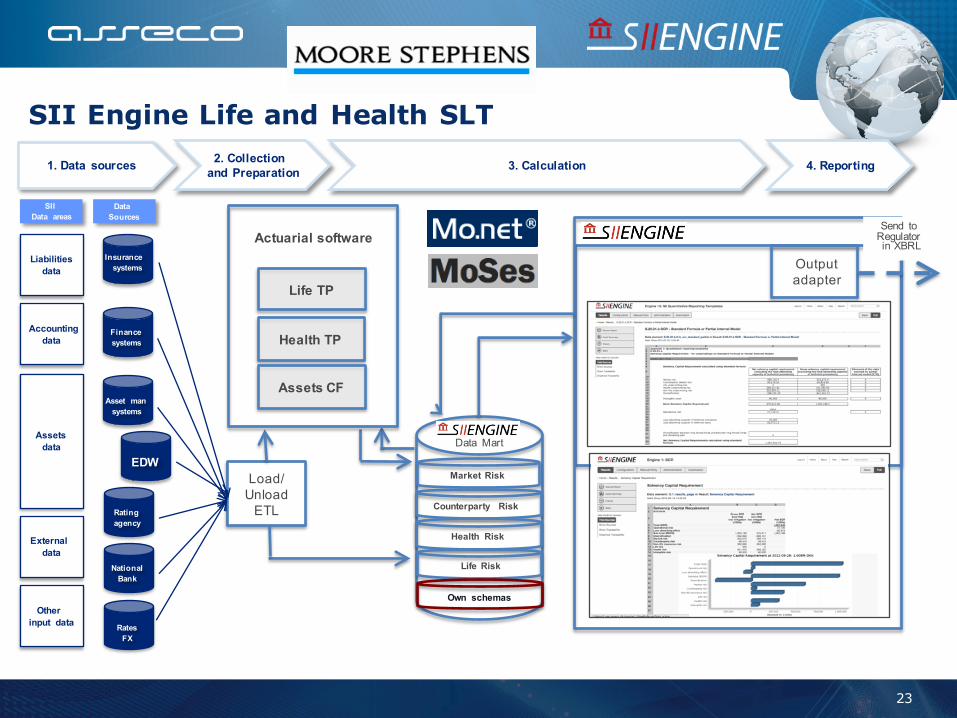

SII Engine Life and Health SLT

23

www.asseco.dk

SII Data areas

Assetsdata

Accountingdata

Liabilitiesdata

External data

Other input data

Data Sources

Insurance systems

Financesystems

Asset mansystems

EDW

NationalBank

Ratingagency

RatesFX

1. Data sources 4. Reporting3. Calculation2. Collection and Preparation

Load/Unload

ETL

Actuarial software

Outputadapter

Data Mart

Market Risk

Counterparty Risk

Health Risk

Own schemas

Life Risk

Health TP

Assets CF

Life TP

Send to Regulator in XBRL

www.siiengine.com

SII Engine Demo

Open forum

Employers’ support

• Questions?

• Observations?

CFO NETWORK22ND OCTOBER 2015

!

SolvencyIIandGAAPintheUK- AccountingandOthertopicalissues

22October2015

Agenda• Using Solvency II for Accounts purposes

• Other topical issues

§ Using UK GAAP for Solvency II

§ Update on IFRS 4 Phase II and UK GAAP

§ The Audit of Solvency II Pillar III reporting

USING SOLVENCY II FOR ACCOUNTS PURPOSES

29

Background

• For accounting periods beginning on or after 1 January 2015 UK insurers will prepare their accounts § using FRS 102 and FRS 103; or § IFRS and in particular IFRS 4 Phase I

• Solvency II is effective from 1 January 2016• Both IFRS 4 Phase I and FRS 103 (which replicates much of IFRS 4 Phase I) allow

an insurer to continue using the accounting policies used prior to adoption of new standard

• Old UK GAAP for life insurers was based on PRA regulatory requirements that will no longer apply post 1 January 2016 § MSSB and realistic capital regime

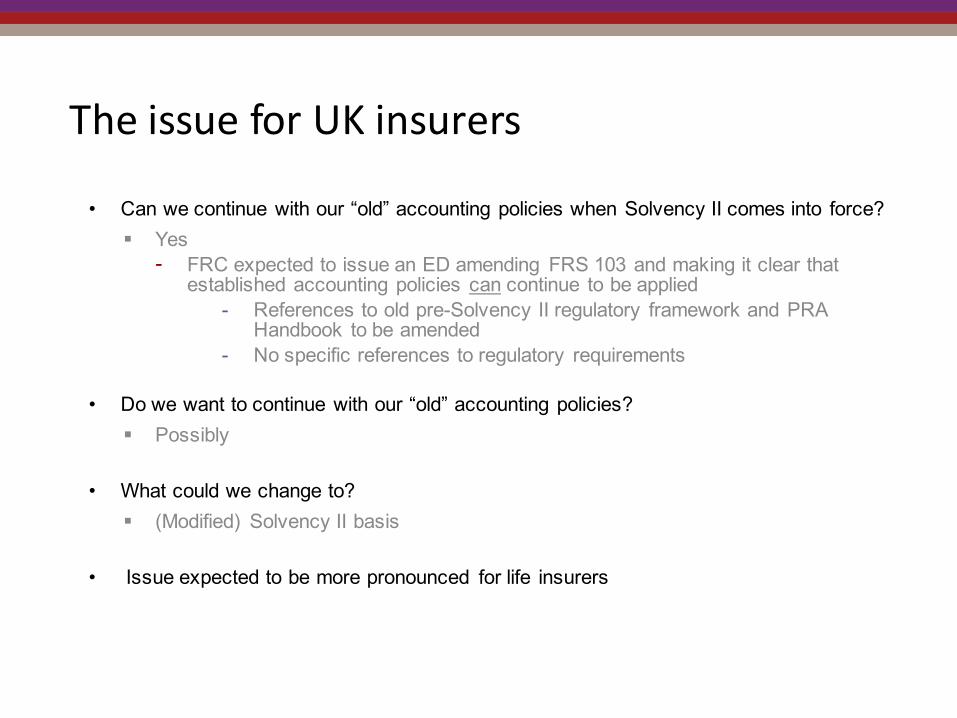

TheissueforUKinsurers

• Can we continue with our “old” accounting policies when Solvency II comes into force? § Yes- FRC expected to issue an ED amending FRS 103 and making it clear that

established accounting policies can continue to be applied- References to old pre-Solvency II regulatory framework and PRA

Handbook to be amended - No specific references to regulatory requirements

• Do we want to continue with our “old” accounting policies?§ Possibly

• What could we change to? § (Modified) Solvency II basis

• Issue expected to be more pronounced for life insurers

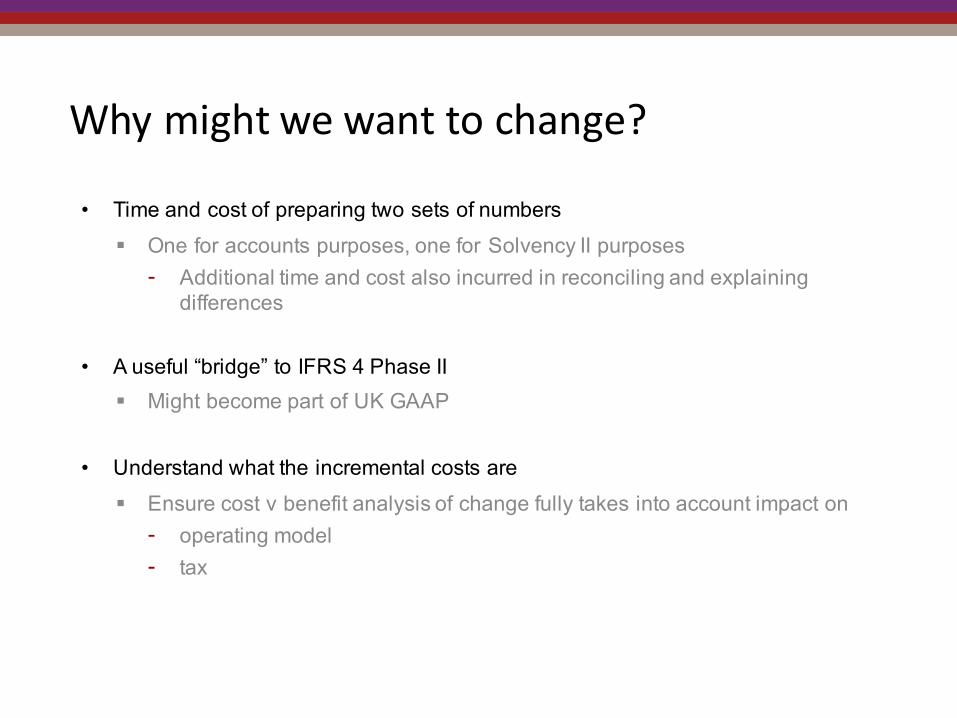

Whymightwewanttochange?

• Time and cost of preparing two sets of numbers§ One for accounts purposes, one for Solvency II purposes- Additional time and cost also incurred in reconciling and explaining

differences

• A useful “bridge” to IFRS 4 Phase II§ Might become part of UK GAAP

• Understand what the incremental costs are§ Ensure cost v benefit analysis of change fully takes into account impact on- operating model- tax

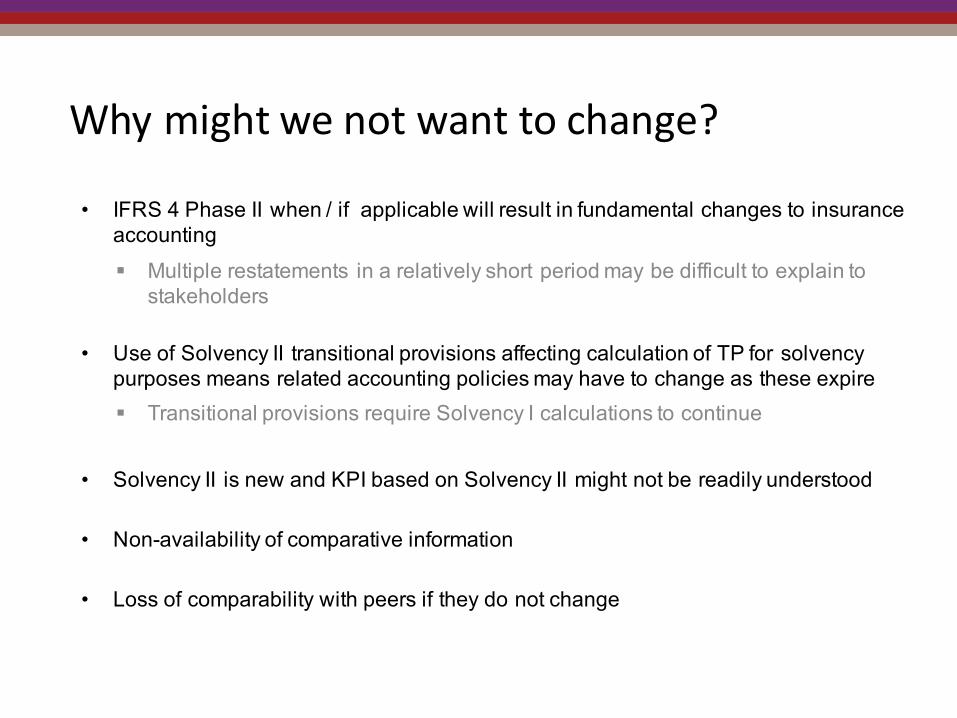

Whymightwenotwanttochange?

• IFRS 4 Phase II when / if applicable will result in fundamental changes to insurance accounting§ Multiple restatements in a relatively short period may be difficult to explain to

stakeholders

• Use of Solvency II transitional provisions affecting calculation of TP for solvency purposes means related accounting policies may have to change as these expire§ Transitional provisions require Solvency I calculations to continue

• Solvency II is new and KPI based on Solvency II might not be readily understood

• Non-availability of comparative information

• Loss of comparability with peers if they do not change

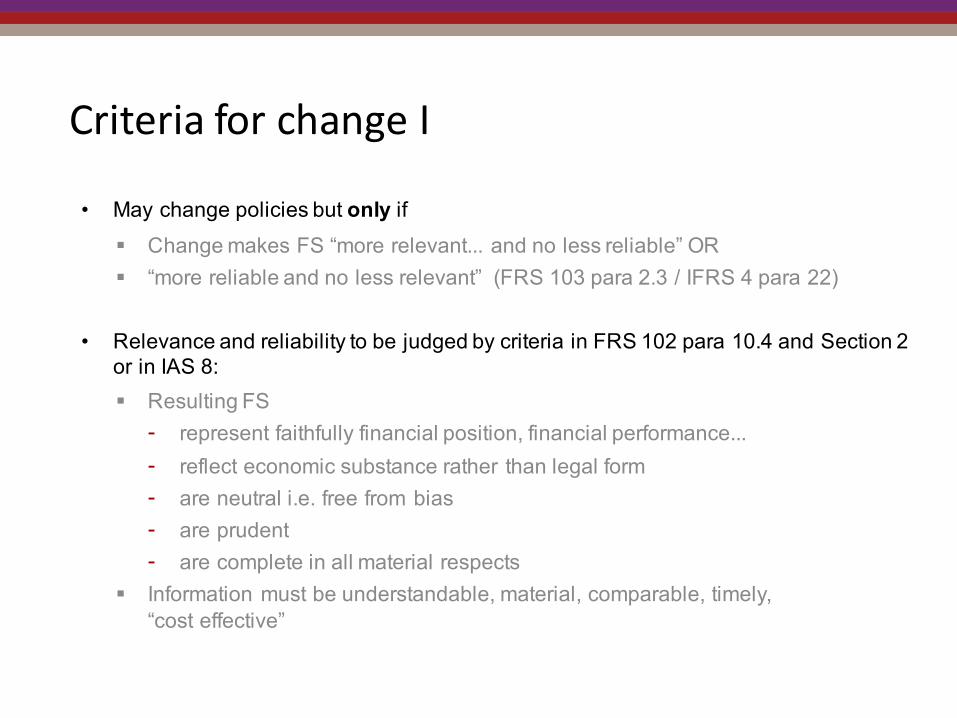

CriteriaforchangeI

• May change policies but only if § Change makes FS “more relevant... and no less reliable” OR§ “more reliable and no less relevant” (FRS 103 para 2.3 / IFRS 4 para 22)

• Relevance and reliability to be judged by criteria in FRS 102 para 10.4 and Section 2 or in IAS 8: § Resulting FS- represent faithfully financial position, financial performance...- reflect economic substance rather than legal form- are neutral i.e. free from bias- are prudent - are complete in all material respects

§ Information must be understandable, material, comparable, timely,“cost effective”

CriteriaforchangeII

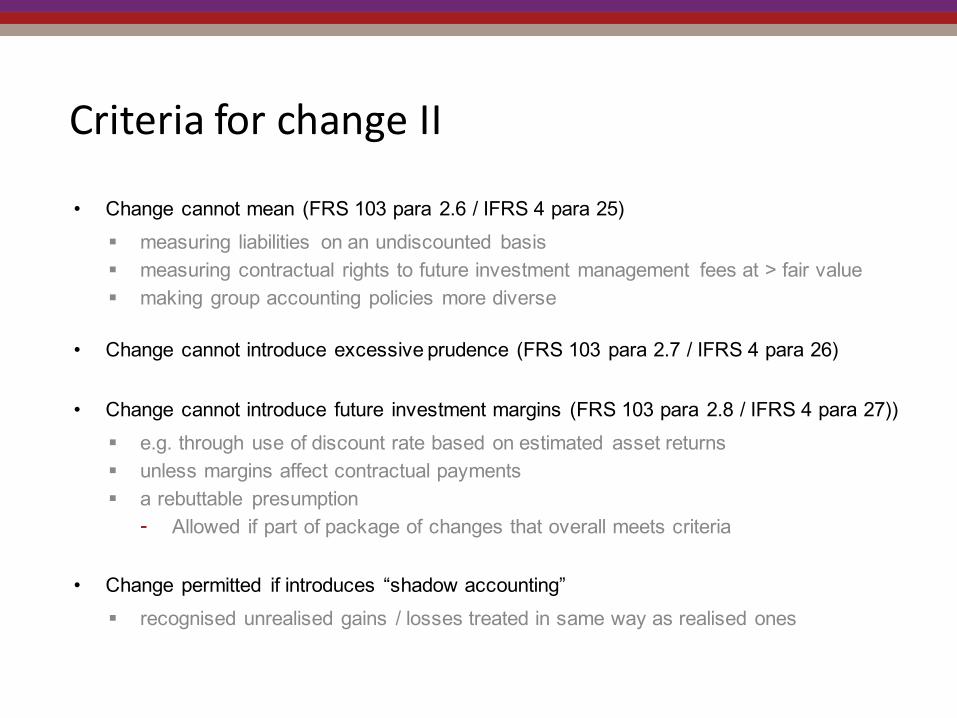

• Change cannot mean (FRS 103 para 2.6 / IFRS 4 para 25)§ measuring liabilities on an undiscounted basis§ measuring contractual rights to future investment management fees at > fair value§ making group accounting policies more diverse

• Change cannot introduce excessive prudence (FRS 103 para 2.7 / IFRS 4 para 26)

• Change cannot introduce future investment margins (FRS 103 para 2.8 / IFRS 4 para 27))§ e.g. through use of discount rate based on estimated asset returns§ unless margins affect contractual payments§ a rebuttable presumption- Allowed if part of package of changes that overall meets criteria

• Change permitted if introduces “shadow accounting”§ recognised unrealised gains / losses treated in same way as realised ones

CriteriaforchangeIII

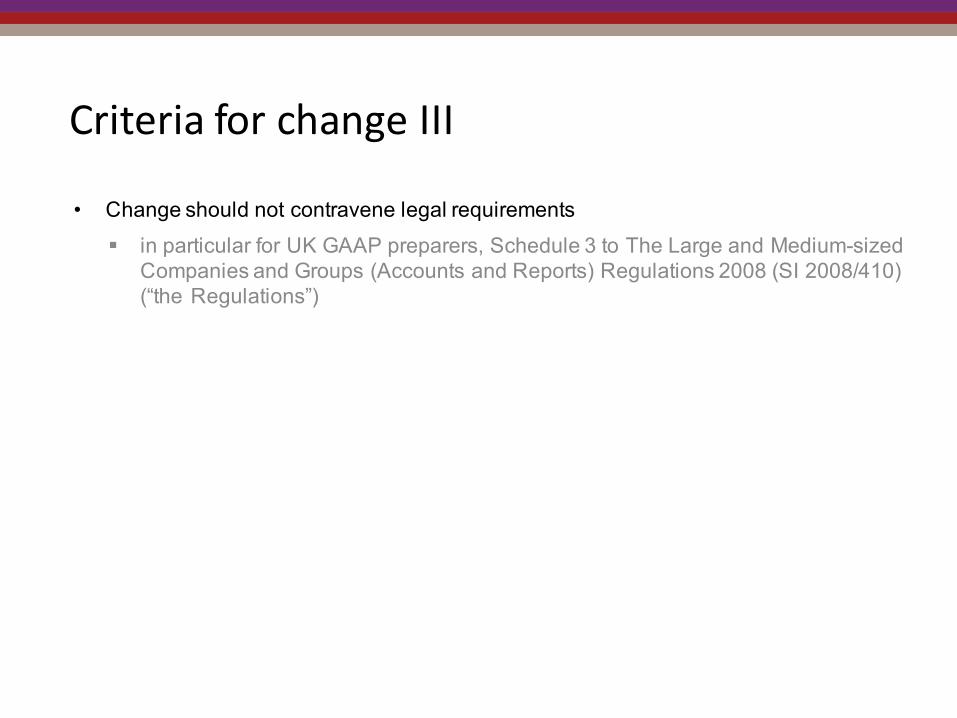

• Change should not contravene legal requirements§ in particular for UK GAAP preparers, Schedule 3 to The Large and Medium-sized

Companies and Groups (Accounts and Reports) Regulations 2008 (SI 2008/410) (“the Regulations”)

CouldwechangetoSolvencyII?

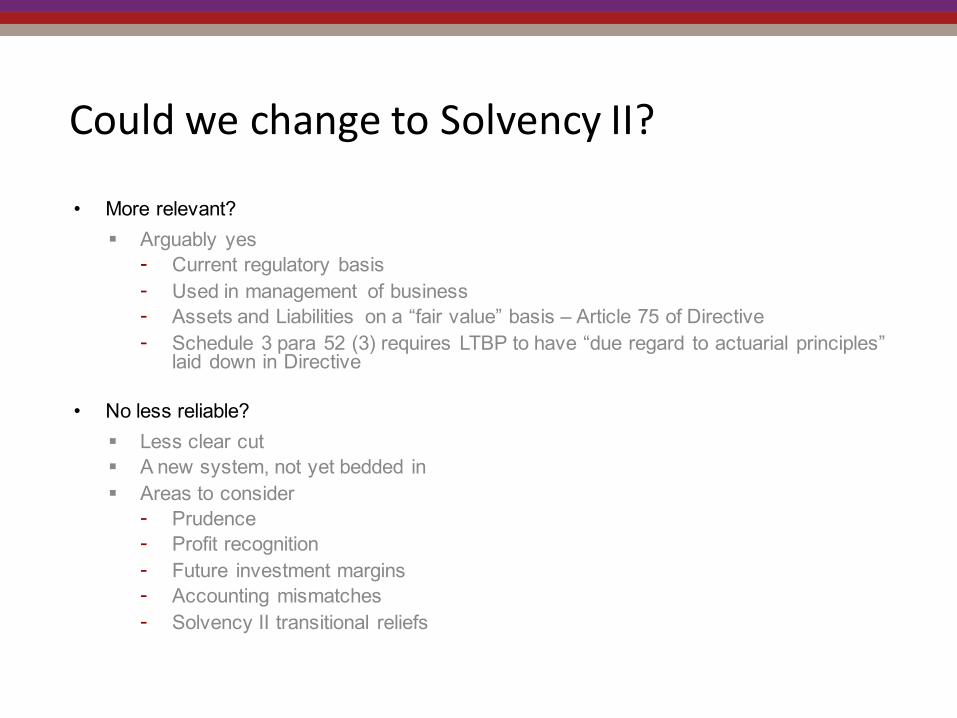

• More relevant? § Arguably yes- Current regulatory basis- Used in management of business- Assets and Liabilities on a “fair value” basis – Article 75 of Directive- Schedule 3 para 52 (3) requires LTBP to have “due regard to actuarial principles”

laid down in Directive

• No less reliable? § Less clear cut§ A new system, not yet bedded in § Areas to consider- Prudence- Profit recognition- Future investment margins- Accounting mismatches- Solvency II transitional reliefs

Prudence

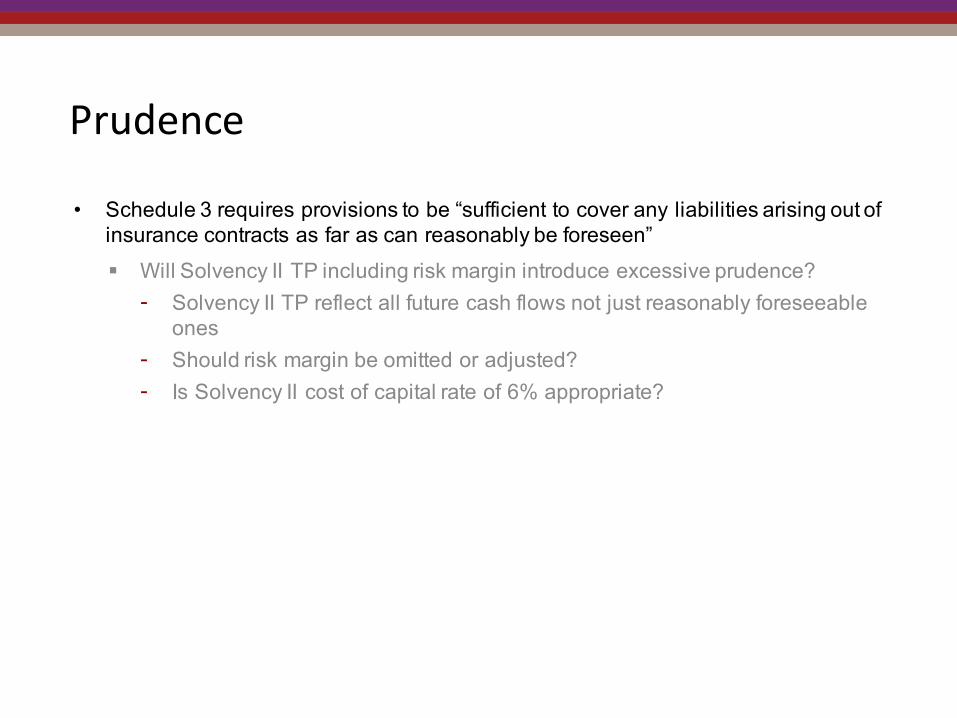

• Schedule 3 requires provisions to be “sufficient to cover any liabilities arising out of insurance contracts as far as can reasonably be foreseen” § Will Solvency II TP including risk margin introduce excessive prudence? - Solvency II TP reflect all future cash flows not just reasonably foreseeable

ones- Should risk margin be omitted or adjusted? - Is Solvency II cost of capital rate of 6% appropriate?

Profitrecognition

• No P&L focus in Solvency II, no profit deferral mechanism § Day 1 profits can be recognised § Not consistent with general principles of FRS 102 - % completion method or

IFRS 15 § IFRS 4 Phase II will not allow recognition of Day 1 profits § Consistency of approach needed re contract boundaries for BS and P&L account

• Less of an issue for mutuals than for insurers with shareholders

Futureinvestmentmargins

• Standard approach under Solvency II is to discount using appropriate risk free rate but § matching adjustment or volatility adjustment use rates based on returns on assets

held

Accountingmismatches

• Will change increase volatility of results or mismatches between assets and liabilities?

• Will changes in asset strategies as a result of Solvency II increase accounting mismatches if liabilities are not accounted for on a Solvency II basis as well?

SolvencyIItransitionalreliefs

• The unwinding of transitional reliefs may make consistency and comparability difficult to achieve

Other

• There are no deferred acquisition costs under Solvency II• Unless a life insurer already uses, or elects to use, the “realistic” value of liabilities in

its FS, FRS 103 para 3.8 states that except in certain circumstances “acquisition costs shall be deferred”

• Some accounting amendment may be necessary to Solvency II TP to gross them up for deferrable acquisition costs§ Similar to adjustment currently made under MSSB

Considerationforgeneralinsurers

• Same link does not exist between solvency requirements and accounting requirements as existed for life insurers

• Accounting basis for general insurance less “broken” than that for life insurance§ Premium allocation approach expected to be available to general insurers under

IFRS 4 Phase II is more like old UK GAAP than Solvency II§ may be better to move straight to IFRS 4 Phase II basis

• Schedule 3 para 54 (1) restricts the use of discounting§ in particular, “the expected average interval between the date for the settlement

of claims being discounted and the accounting date must be at least four years” • Treatment of non-proportional reinsurance (may also impact some life insurers)

§ Solvency II rules, as currently understood, effectively write off the cost of any reinsurance purchased before the year even if inwards policies yet to be written would be protected in due course

§ Under old UK GAAP an asset would be recognised.

Summary

• Using Solvency II as the basis for the preparation for accounts may be a viable option for some insurers

• Arguments for and against need to be carefully weighed and discussions held with all interested stakeholders

• If a change is being considered, early consultations with the auditor are strongly recommended!

OTHER TOPICAL ISSUES

46

UsingUKGAAPforSolvencyII

• PRA SS38/15 Solvency II: consistency of UK generally accepted accounting principles with the Solvency II Directive

§ sets out the PRA’s expectations of firms wanting to use UK GAAP for the recognition and valuation of assets and liabilities for Solvency II purposes

§ identifies those UK treatments which the PRA considers to be consistent, in full or in part, with Article 75 of the Directive

IFRS4PhaseII• Basic building blocks approach generally accepted

§ unbiased estimate of future cash flows§ risk margin§ contractual service (profit) margin§ discount for time value of money

• Final standard delayed by continuing deliberations over performance reporting particularly in respect of contracts with a discretionary participation feature

• Another ED expected in 2016

• 3 – 4 year transition period between final standard and mandatory effective date§ EU approval

• FRC’s position re introduction into UK GAAP unchanged§ No firm decision taken – wait and see what final standard looks like and any implementation

issues

AuditofSolvencyIIPillarIIIreporting

• EIOPA position § audit a good thing but not our problem!

• UK – transitional audits ref to 31 December 2014

• PRA consultation paper due in November 2015 on audit requirements iro live reporting from 1 January 2016

• FRC to redraft PN20 Audit of Insurers in the United Kingdom§ gap period expected to arise between due date for first audited annual QRTs

and issue date of revised PN20

• Cost of audit proposals expected to be an issue!

QUESTIONS?

50 Titre de la présentation

Contact details

• Ray Tidbury: § Tel: 020 7063 4447§ [email protected]

• Paul Bennett§ Tel: 020 7063 4452§ [email protected]

This presentation has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained herein without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information it contains. To the greatest extent permitted by law, Mazars LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting or refraining to act, in reliance on the information contained in this presentation or for any decision based on it.

CFO NETWORK22ND OCTOBER 2015

!

CFO NetworkORSA –practical experience and regulatory feedbackMick Campbell22 October 2015

Content

§ Key points from the final guidelines

§ Industry approaches to developing the ORSA

§ Practical uses of the ORSA

§ Regulatory feedback

§ ORSA – a look ahead….

54

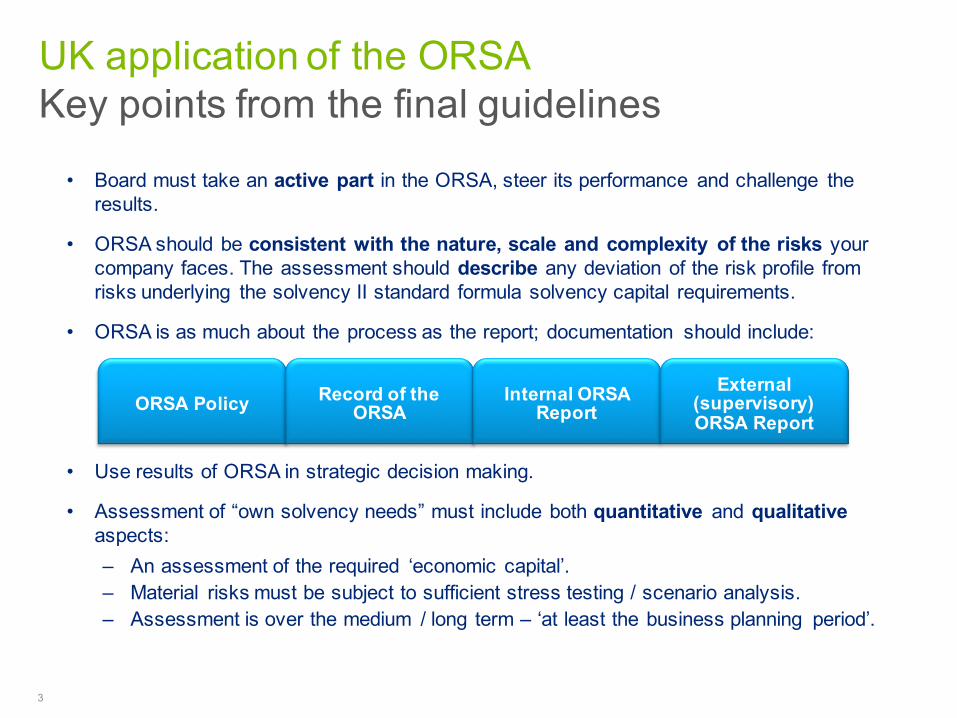

• Board must take an active part in the ORSA, steer its performance and challenge the results.

• ORSA should be consistent with the nature, scale and complexity of the risks your company faces. The assessment should describe any deviation of the risk profile from risks underlying the solvency II standard formula solvency capital requirements.

• ORSA is as much about the process as the report; documentation should include:

• Use results of ORSA in strategic decision making.

• Assessment of “own solvency needs” must include both quantitative and qualitativeaspects:‒ An assessment of the required ‘economic capital’.‒ Material risks must be subject to sufficient stress testing / scenario analysis.‒ Assessment is over the medium / long term – ‘at least the business planning period’.

ORSA Policy Record of the ORSA

Internal ORSA Report

External (supervisory) ORSA Report

Key points from the final guidelinesUK application of the ORSA

3

ORSA report – Industry approachesTiming and frequency

§ 85% of firms expect to produce their formal ORSA annually

§ The majority (75%) also use regular Risk MI (or similar) to support the annual ORSA report.

Q1 Q2 Q3 Q4

Regular Risk ReportingRegular Risk Reporting Regular Risk Reporting Regular Risk Reporting

• Most firms anticipate more frequent reports will be used to communicate risk and solvency MI

• Two thirds of the firms will be aligning the production of the ORSA report with their annual planning process

• 15% finalise ORSA report at Y/E

• Some firms may have annual planning processes aligned to Y/E

4

Monthly Risk Reporting

Monthly Risk Reporting

Monthly Risk Reporting

Monthly Risk Reporting

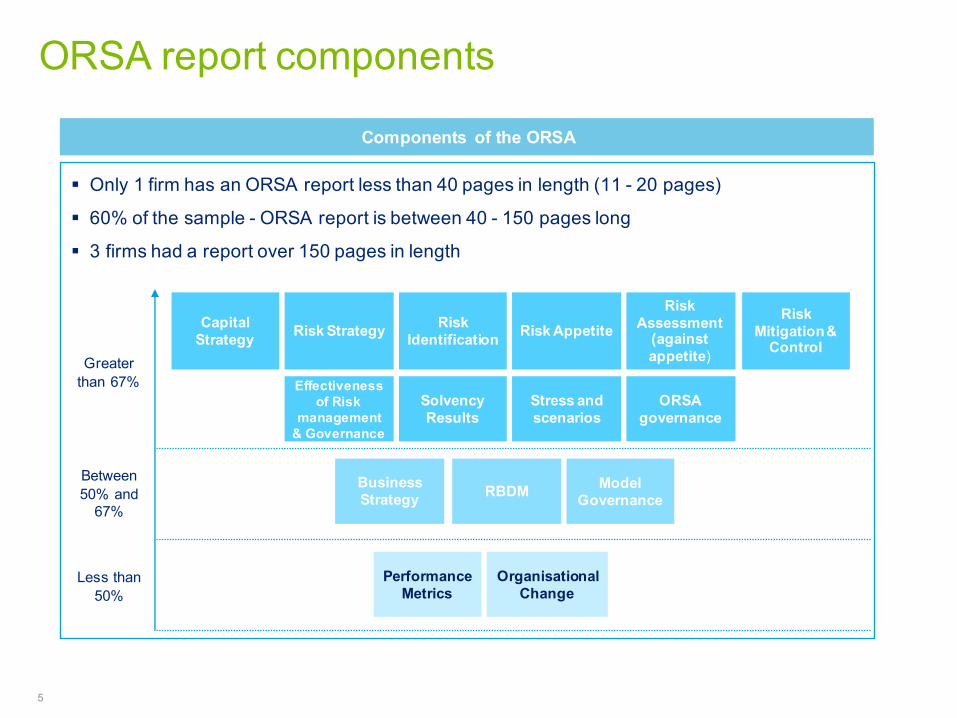

ORSA report components

Components of the ORSA

§ Only 1 firm has an ORSA report less than 40 pages in length (11 - 20 pages)

§ 60% of the sample - ORSA report is between 40 - 150 pages long

§ 3 firms had a report over 150 pages in length

Greater than 67%

Between 50% and

67%

Less than 50%

Capital Strategy Risk Strategy Risk

Identification Risk AppetiteRisk

Assessment (against appetite)

Risk Mitigation &

Control

Effectiveness of Risk

management & Governance

Solvency Results

Stress and scenarios

ORSA governance

RBDM Model Governance

Business Strategy

Performance Metrics

Organisational Change

5

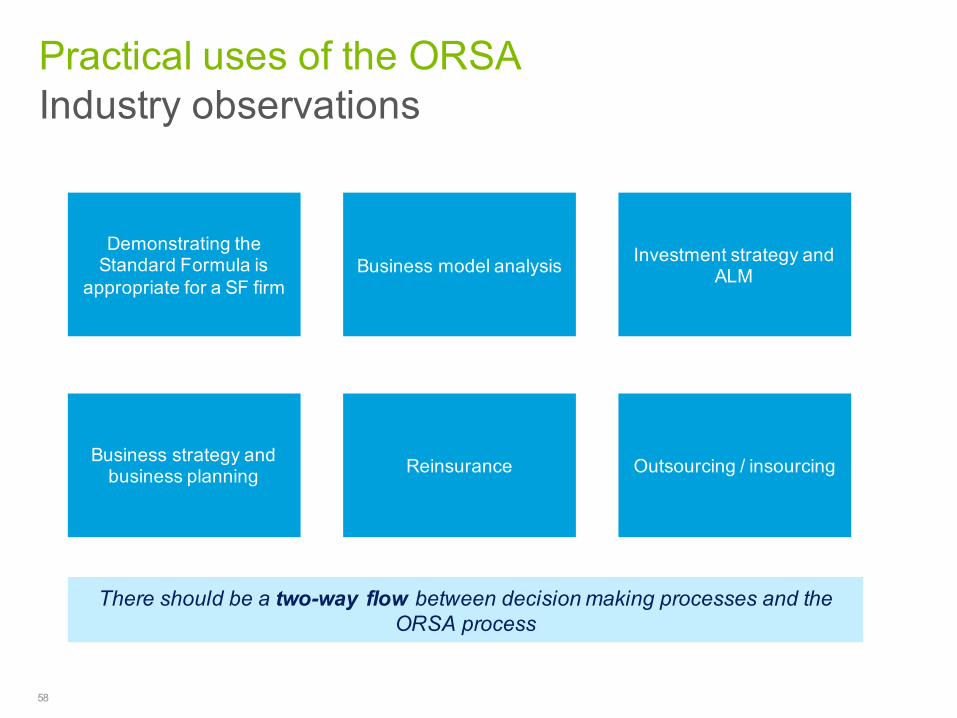

Practical uses of the ORSAIndustry observations

58

Business strategy and business planning Reinsurance Outsourcing / insourcing

Demonstrating the Standard Formula is

appropriate for a SF firmBusiness model analysis Investment strategy and

ALM

There should be a two-way flow between decision making processes and the ORSA process

Regulatory feedback regarding the ORSA

Key areas of feedback

The following areas have attracted comment from the PRA:• Structure of the report (e.g. length and contents);• ORSA policy;• Supporting evidence regarding Board sign-off and use of ORSA

in decision making;• Lack of linkage to business strategy;• Lack of linkage of risks to appetite and tolerances;• Lack of detail on future capital and solvency positions;• Stress and scenario testing; and• IM and SF firm uses.

Focus on stress testing

Stress testing should provide the link from risk identification to capital management and be:• Forward looking;• Widely applied e.g. through stress tests, scenario analysis,

sensitivity testing and reverse stress testing;• Proportionate to the firm and its risks;• Link to other parts of the process (strategy, risks and solvency);• Assess capital implications;• Result in agreed management actions; and• Evidence management and the Board have understood

assumptions and challenged output.

7

A look ahead……

60

ORSA

• More scrutiny from firms and the regulators of individual component parts of the ORSA rather than the process as a whole

• Demonstrating and evidencing ORSA use to inform decision making

• Embedding the ORSA across the business

• An increased level of engagement and direction from the Board regarding ORSA development

CFO NetworkORSA –practical experience and regulatory feedbackMick Campbell22 October 2015

Contact details:Mick CampbellTel: +44 141 314 5899Mobile: +44 7900 607 601Email: [email protected]

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and i ts network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2015 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

CFO NETWORK22ND OCTOBER 2015

!

Association of Financial MutualsOctober 2015

66

Overview

1. Speaker2. Mutual insurers3. The Strike Club4. Issues 5. Options for a partner6. Charles Taylor plc7. Impacts of choosing Charles Taylor8. Challenges9. Questions and discussion

67

Speaker

AccountantWorking for financial mutuals since 1988Experience in non-life insuranceUntil March 2015, working for small management companyFrom March 2015, working for Charles Taylor plcFinance director, MSUKI, The Strike Club020 7767 [email protected]

68

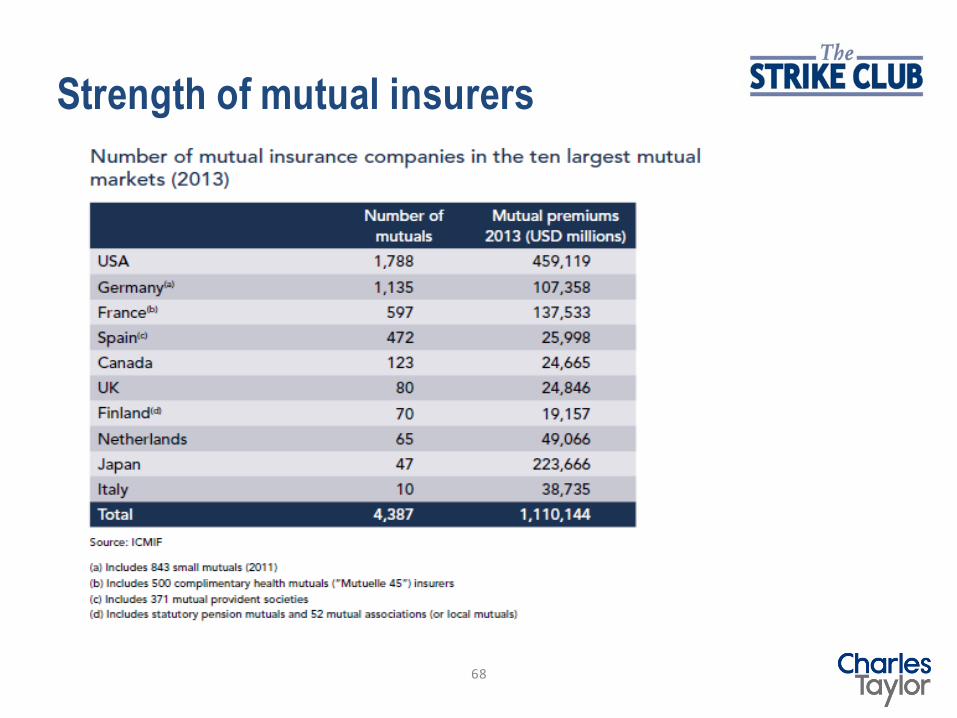

Strength of mutual insurers

69

The Strike Club

Mutual insurance company started in 1957Specialist marine delay risks insurer (2015 premium of £25m) Management carried out by independent management company

with 19 staff, mostly long-servingSuccession and recruitment issuesOperations, governance, compliance & documentation

OK for Solvency I, not OK for Solvency IIIncreasingly spending too much on ‘what to do’ consultants

70

Issues

The Board wanted the insurer to stay independentThe Board and managers wanted to retain loyal staffHowever implementing Solvency II

without sharing the costslikely to prove very difficult, if not impossible,within a reasonable budget

71

Options for working with a partner

Managers could contract with a partner to provide services

complex in a regulated environment

Managers could set up a JV with a partner

JV would be a new regulated entity

Managers could merge / be taken over option chosen - signed fixed price end-to-end management agreement toaddress governance and operations

72

Charles Taylor plc

Providing professional services to insurance clients since 1884

Listed on the London Stock Exchange since 1996

Over 1,200 permanent staff in 67 offices across 27 countries

Provides services through three businesses, principally fee-based:

Management Services (end-to-end management of insurance co’s)

Adjusting Services (loss adjusting & marine average adjusting)

Insurance Support Services (stand-alone services to life

and non-life insurers)

Owns insurers (with main focus on servicing life insurers in run-off)

73

CT’s life company insurance services

Outsourced insurance services for major international life insurance companies,

covering every aspect of life company operations:

either chosen from a full menu of services (for both insurers writing new

business and for run-off insurers)

or a complete turnkey solution for run-off insurers

Full range of unitised pricing services that some life companies require

Services applicable to a wide range of life companies, from smaller mutual and

specialist life offices, up to larger unit linked insurers

74

Impact for the insurance company

Remained independentCombined existing management with new resources to

enhance operationsCompliant with legal & regulatory requirementsFixed price management feeCost reductions achieved for several general expenses

from shared services & economies of scale

75

Impact for the staff

Two Charles Taylor people have moved across to our teamTwo new people have been recruitedOf the nineteen people working a year ago:

one part-timer left before takeovertwo people have retiredsixteen continue working

The message has been:‘Charles Taylor wants to retain experienced people’

76

Impact for Solvency II

The business has gained experienced people to fill specificgaps and access to key shared services:

actuarialcomplianceinternal auditITinternal auditreinsurancerisk management

77

Impact – practical flexibilityBy 2014, the insurer had already chosen Moore Stephens to implement various work streams, so Charles Taylor has been working with Omar Ripon and his team to develop and refine:

data and MI for the ORSAthe ORSA itselfSolvency Financial Condition ReportReport to SupervisorsSCR governance & risk managementdisclosure & reporting

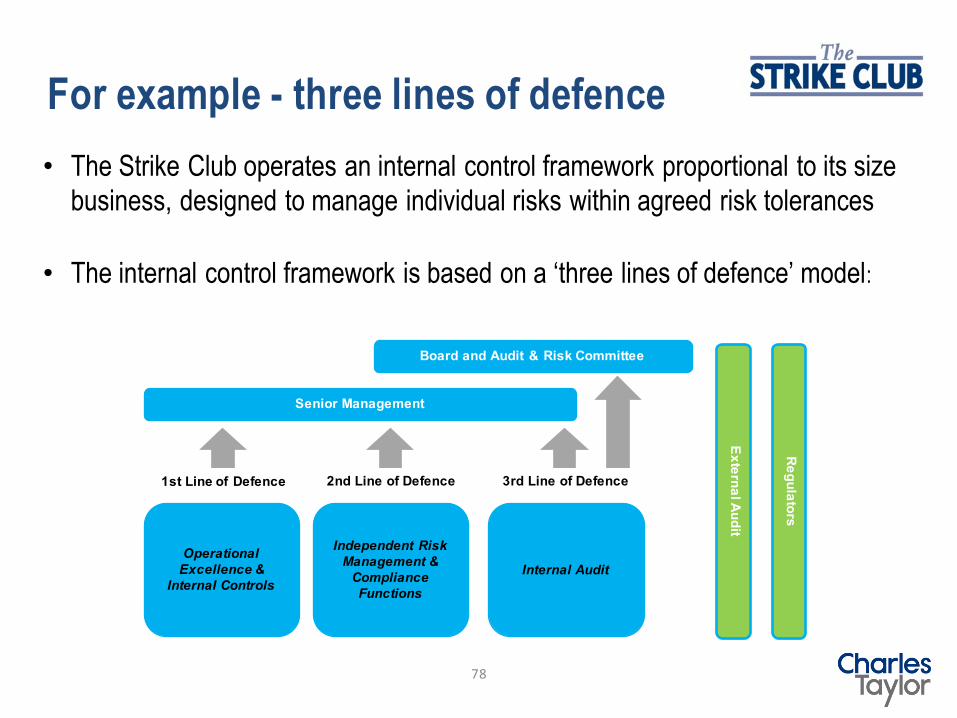

For example - three lines of defence• The Strike Club operates an internal control framework proportional to its size

business, designed to manage individual risks within agreed risk tolerances

78

Board and Audit & Risk Committee

Senior Management

Operational Excellence &

Internal Controls

Independent Risk Management &

Compliance Functions

Internal Audit

1st Line of Defence 3rd Line of Defence2nd Line of Defence

External Audit

Regulators

• The internal control framework is based on a ‘three lines of defence’ model:

79

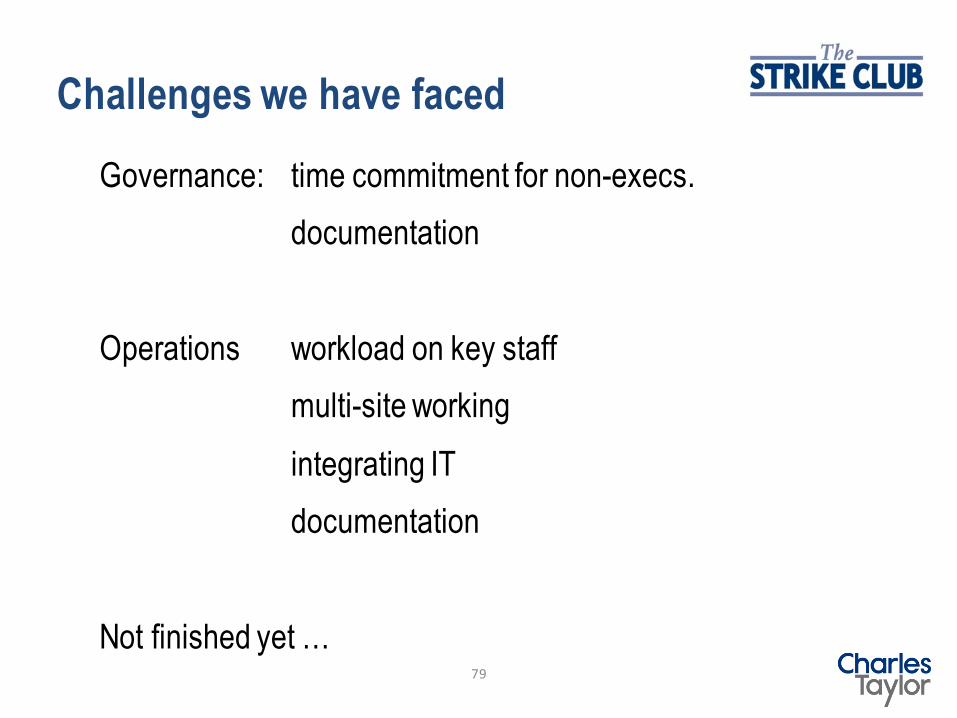

Challenges we have faced

Governance: time commitment for non-execs. documentation

Operations workload on key staffmulti-site working integrating ITdocumentation

Not finished yet …

Questions and discussion

CFO NETWORK22ND OCTOBER 2015

!