cfa institute research challenge · cfa institute research challenge hosted by cfa society sydney...

TRANSCRIPT

CFA Institute Research Challenge

Hosted by CFA Society Sydney

The University of Sydney

Blackmores Limited (ASX:BKL) 24 September 2012|Consumer Health Australia

Journey to the East

• We initiate coverage on Blackmores (BKL) with a strong Buy recommendation and a $37.73 12 month price target. Blackmores is a market leader in natural healthcare, with a strong presence in the Vitamins and Dietary Supplements (VDS) sector, operating throughout Australia, New Zealand and Asia. Moving forward significant earnings growth is expected as the group exploits favourable demographic and social trends throughout all regions.

• The Asian growth engine. Sales and NPAT in Asia grew 20% and 35% respectively in FY12, with the segment contributing 26% of the Group’s profits. FY13 will see Blackmores strengthen its presence in Asia with new product launches, increased marketing activity and entry into Mainland China. Forecasted growth throughout FY13-‐16 is expected to stand at a CAGR of 15.3%, 11.5% and 23.6% for Thailand, Malaysia and ‘Other Asia’ (inclusive of China, Hong Kong, Singapore and South Korea) respectively.

• Across all regions significant growth from new product launches is expected. In particular, development of the recently acquired FIT-‐BioCeuticals will see Blackmores gain a foothold in the growing Practitioner market. The forthcoming on-‐the-‐go range will widen Blackmores’ distribution channels reducing their reliance on supermarkets and pharmacies.

• FY12 marked the tenth consecutive year of record sales and profit for Blackmores. Persevering against retail headwinds, the group experienced 11% growth in sales to $262m and 2% growth in NPAT to $27.3m in FY12. As the group continues its growth strategy, particularly expansion into China, profit and sales are expected to continue escalating accordingly. Revenue is forecast to grow from $327m in FY13 to $408m in FY16. Likewise, NPAT is forecast to grow from $31m in FY13 to $40m in FY16.

• The valuation of $37.73, derived using Discounted Cash Flow and multiples analyses, affirms the view that Blackmores is perfectly positioned to ride the growing VDS trend in Asia whilst leveraging their strong brand equity in the domestic market. Growth potential is immense, with China and South Korea, Blackmores’ newest regions, being the largest VDS markets in Asia.

• Key risks to the target price include operational risks concerning Asian expansion – trade tariffs, regulatory differences and varying consumer tastes. The latter two, however, also provide upside risk if Blackmores can exploit favourable conditions. Volatile exchange rates and raw input prices in addition to the strong Australian dollar expose Blackmores to further downside risk.

Rating: BUY Target Price: $37.73 Upside: 19.79%

Stock Data Price at 24/09/12: $31.50 Intrinsic Value: $37.73 52 Week High (AUD): $31.50 52 Week Low (AUD): $25.25 Average Price (LTM): $28.12 Market Cap (AUD mn): $528.63 Shares Outstanding (mn) 16.8 Daily Volume (LTM average): 7.00 K Float: 67.7% Source: BKL Data; Capital IQ Key Financial Data FY12 end Debt/Equity 53.3% Net Debt/Equity 39.4% Dividend Yield 4.2% EV/EBITDA 11.8x Diluted P/E 18.6x Source: BKL Data Relative Performance (%) S&P/ASX 200 -‐1m 7.1 -‐3m 12.3 -‐12m (5.5) S&P/ASX 200 Healthcare -‐1m 1.6 -‐3m 7.8 -‐12m (27.5) Source: BKL Data; Capital IQ BKL Share Price (LTM, AUD)

Source: Capital IQ

This report is published for educational purposes only by students competing in the CFA Institute Research Challenge.

BKL Key Financial Estimates Year ending 30 June AUD mn 2011A 2012A 2013E 2014E 2015E 2016E Revenue $235.3 $261.6 $326.7 $353.2 $381.1 $408.1 EBITDA $46.1 $47.2 $55.2 $59.2 $63.4 $67.5 Net Income $27.3 $27.4 $31.5 $34.2 $37.3 $40.2 FCFF $19.7 $14.9 $18.9 $29.2 $31.8 $34.9 Per Share (AUD) Basic EPS $1.63 $1.66 $1.87 $2.04 $2.22 $2.39 Dividends (DPS) $1.24 $1.27 $1.42 $1.55 $1.68 $1.82 Returns ROA 17.0% 16.3% 15.3% 15.7% 15.9% 16.1% ROE 36.2% 33.6% 30.3% 30.4% 30.2% 29.9% Source: SURG Estimates; Capital IQ

24.00

25.00

26.00

27.00

28.00

29.00

30.00

31.00

32.00

Sep-‐2011 Dec-‐2011 Mar-‐2012 Jun-‐2012 Sep-‐2012

Sydney University Research Group 1

Company Overview Blackmores Ltd (ASX:BKL) – founded in 1932 and based in Sydney – is the second largest player in the Australian consumer health industry with a 9% market share and a market capitalisation of $528.6 million. Blackmores takes a natural, holistic approach to health care with a range of consumer products in the vitamin, supplement, sports nutrition and weight management segments. As a brand, Blackmores commands an 18.8% share in the VDS sector making it the market leader. Key products including the Performance Multi range, Eco Krill Oil, Executive B Stress Formula and Pregnancy and Breast-‐Feeding Gold lead the company’s extensive 141 product range. In July 2012 the firm diversified its product portfolio with the acquisition of FIT-‐BioCeuticals. This deal gave Blackmores a foothold in the growing healthcare practitioner-‐only market with a new range of products complementary to their existing lines. FIT-‐BioCeuticals continues to operate as a standalone business. Geographic segments: • Australia – Blackmores’ core segment, contributing 76.9% of revenue. Blackmores’

products are distributed in supermarkets, pharmacies and health food stores– Coles, Woolworths and Chemist’s Warehouse contribute 57.0% of the groups Australian revenue

• Thailand – Blackmores’ longest established and best performing Asian market. The company currently enjoys the title of number 1 most trusted VDS brand. Success has been due to the growing trend toward calcium supplements and also the company’s vitamin segmentation strategy, in particular vitamins for kids.

• Malaysia – contributes 5.8% of the firm’s total revenue. Blackmores is currently the number 2 most trusted VDS brand in Malaysia after Amway Nutrile. Vitamin C and other immune defence VDS drive sales in the region.

• New Zealand – operation is via an agency agreement. Only 1.9% of revenue stems from New Zealand.

• Other Asia – This segment comprises of Singapore, Hong Kong, Taiwan, South Korea and China, and accounts for 5.1% of sales. Substantial growth is forecast particularly from South Korea and Mainland China. The company entered Mainland China at the end of FY12 and will expand its presence during FY13.

Industry Overview Australia Growing vitamins and dietary supplements (VDS) industry The VDS industry has seen 64% current value growth since CY06. In CY11 the industry grew 7%, bringing it to a total value of $1.4 billion. Underpinning growth in this market is Australia’s ageing population, growing obesity and a trend of increasing health and wellbeing awareness. In CY12, Australia’s baby boomers reached retirement pushing the number of retired Australians to a forecasted 17% higher than CY11. Over 61% of

80%

90%

100%

110%

120%

130%

140%

150%

Sep 2011

Oct 2011

Nov 2011

Dec 2011

Jan 2012

Feb 2012

Mar 2012

Apr 2012

May 2012

Jun 2012

Jul 2012

Aug 2012

Blackmores Limited (ASX:BKL) -‐ Share Pricing

S&P/ASX 200 Index (^XJO) -‐ Index Value

76.9%

9.4%

5.8% 5.1% 1.9%

Figure 3: Revenue by Geographic Segment

Australia

Thailand

Malaysia

Other Asia

New Zealand

Source: BKL Data

CFA Institute Research Challenge 24.09.2012

0%

5%

10%

15%

20%

25%

50

100

150

200

250

300

2008 2009 2010 2011 2012

Figure 1: Sales and EBITDA margin (AUD mn)

Sales EBITDA Margin Source: BKL Data

Figure 2: BKL relative performance LTM

Source: Capital IQ

Figure 4: Blackmores Australasian Operations (Blue)

CFA Institute Research Challenge 24.09.2012 CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 2

Australians are either overweight or obese, making Australia one of the most obese nations in the world. In essence, the industry is riding a demographic wave. As such, consumers have been increasingly turning to VDS products as a means of filling the gaps in their nutritional intake. The ageing population will continue to place emphasis on maintaining mobility and brain health, as well as boosting immune systems. As the leading brand in this sector for Australia, Blackmores’ revenues and profit margins are expected to reap the benefits of this trend. Multiple distribution channels VDS products are sold through a number of channels, including pharmacies, grocery stores, health food stores and direct-‐to-‐consumer. Store-‐based retailing accounts for the dominant share of VDS retailing in Australia, with 87%. Within this channel, supermarkets have seen their share of retail distribution grow as consumers appreciate the convenience of one stop shopping and the lower unit prices, with a current value share of 31%. Chemists/pharmacies and other health food specialists accounted for the remaining 39% and 20% value share respectively. Blackmores has a well-‐established presence within all these channels, with 7,500 points of distribution. Fragmented market Vitamins currently face little competition from fresh or fortified food and drinks in Australia. However, the market is fragmented with a number of large suppliers, including Blackmores, Sanofi-‐Aventis, Herron Pharmaceuticals, Pharmacare (Nature’s Way), Wyeth Australia, Swisse and Bayer (penta-‐vite). This has created a competitive environment and limits the potential for growth in the Australian market. Retail headwind Uncertainty in the global economy, pressures of a rising cost of living and low consumer confidence could potentially hold back domestic revenues. Overall retail value grew moderately by only 2.0% in FY11, similar to growth in FY10 but substantially poorer than earlier years of the review period where growth ranged from 4.0% to 6.0%. However, Blackmores’ strong branding does put them ahead of the curve as consumers continually seek value and price-‐quality. Grocery retail growth has slowed to 2.8% in FY11, with health specialist retail slowing to 5.3%, from 7.3% in CY09. However, Blackmores’ revenue streams has shown a slight level of resilience to the down swing in the retail sector, growing at 9.1% in FY11 and maintaining a solid 11.2% in FY12. Prospects for retail throughout the forecast period are bleak and the increasing trend towards online shopping may exacerbate this. We feel that Blackmores’ current presence online will put them in good stead to make the transition if such is needed. Blackmores has one of Australia’s largest online communities of over 360,000 members and recently launched country websites for China, South Korea and Thailand. Blackmores’ free Naturopathic Advisory Service has been operating for 20 years and supports over 53,000 contact points per year. Asia Large and growing market Blackmores’ expansion into the Asian market, and in particular China, is an important driver of revenue throughout the forecast period. Growth in value within these industries has been historically sound at 6.0%, 11.0%, 5.0% and 20.0% for Malaysia, South Korea, Hong Kong and Thailand respectively, and is forecast to continue at this pace throughout the forecast period. Sound structure with multiple channels of distribution Asia has a wide range of distribution channels including, pharmacies, grocery stores, health food stores, department stores, drugstores, specialty stores, hospitals, direct selling, home shopping and online. As Blackmores has the intention of continuing production in Australia, this will strongly favour their expansionary distribution strategy. China Although forecasts have recently been revised down, discretionary spending is increasing with disposable incomes as China’s strong GDP growth continues. The World Bank maintains a forecast of 8.2% for CY12, and continues to project strong single digit growth until CY15. The VDS industry has continually seen solid growth, reaching a size of approximately A$11.0 billion in CY11. Like Australia, the key products in demand are dietary supplements, which have been driven by well-‐established health awareness, far-‐reaching customer service and an effective public health system. Multivitamins have continually dominated this category with 73% of total value sales and value growth of 9% in CY11. Paediatric and single vitamins registered more robust value growth than multivitamins in CY11 at 11%.

Geography Market Size (US$ mn) China 10,668.1 South Korea 3,304.5 Taiwan 1,890.6 Australia 1,521.2 Thailand 1,007.2 Hong Kong 504.9 Singapore 467.7 Malaysia 456.4 New Zealand 186.8

Figure 5: Blackmores Australian Distribution Channels by Revenue

Source: BKL Data

Source: Euromonitor

Table 1: Global Vitamin and Dietary Supplements (VDS) Market Sizes in 2011

Sydney University Research Group 3

CFA Institute Research Challenge 24.09.2012

Like Australia, the Chinese VDS industry is fragmented with a high amount of competition from the top 10 players. The leading brands, such as Infinitus (China) Co Ltd, hold a distinctive market positioning by marketing a wide range of products and targeting middle and high-‐end consumers through product differentiation, tailored to specific needs. China’s booming Internet retailing has remained a niche market within the VDS

industry, however, competitive pricing and convenience have resulted in strong growth throughout CY11/12. China currently holds 1st place for number of Internet users at approximately 513 million. We see this as favouring Blackmores’ integration into China given their strong online foundations and networks.

Competitive Positioning Vitamins and dietary supplements market in Australia Australia market leader Blackmores is the brand leader in the highly concentrated Australian VDS market. Its set apart by its operations and a reputation for quality, beyond the required TGA standards. Blackmores has seen steady brand share of 18.9% in FY10 and 18.8% in FY11, consistent with the brand growth of competitors. Blackmores’ Australian VDS strategy has been to retain market share through continual renovation of SKUs and increased product segmentation in high growth areas. High growth areas High growth areas include paediatrics, multivitamins and Vitamin D with CY11-‐16 CAGRs of 4.2%, 5.1% and 5.9% respectively. Blackmores is well positioned for growth in paediatrics with four SKUs compared to ten SKUs for main competitor Nature’s Way and relatively little competition from single product competitors Herron, Bioglan and Centrum. Blackmores is also innovating in multivitamins, being the first mover in “bulk” products such as Executive B and planned on-‐the-‐go vitamins and supplements. Pet care and nutraceuticals Blackmores has strategically positioned itself for growth in the pet care and nutraceuticals market. PAW, a natural alternative to mainstream pet care products, is located in a viable niche market of medicated grooming products and pet health supplements. Under Blackmores’ direction, PAW’s sales have increased 129% to $3.2m in FY12, and is expected to grow by 10.5% and 8.0% over CY11-‐16 on the back of pet humanisation trends. The acquisition of FIT-‐BioCeuticals also gives Blackmores a foothold in the practitioner-‐only channel and leverages FIT-‐BioCeutical’s existing relationship with doctors, practitioners and natural health professionals, providing a combined depth of experience of over 100 professionals. Vitamins and dietary supplements market in Asia Thailand and Malaysia – Vitamin market Blackmores is well positioned as a strong competitor within the vitamin market of Thailand, Malaysia, Hong Kong and Singapore. In Thailand, Blackmores brand share has increased from 10.8% to 13.3% over the FY08-‐11 to currently hold the second highest vitamin brand share after Amway’s Nutrilite. In Malaysia, brand share in vitamins has increased from 6.7% to 7.5% over the FY08-‐11. Blackmores faces smilar competitive pressures in both regions from market leader Amway and its Nutrilite range and Cerebos and its “Brand’s” products. In both markets Blackmores has focused on product segmentation with over 31 products in Thailand and 58 in Malaysia. Blackmores’ push into the pharmaceuticals, such as Watsons, also means that it does not directly compete with Amway and its focus on vitamins means it does not directly compete with Cerebos’ nutritive drinks. Distribution channels Blackmores’ competitive position is related to its clever geographic footprint, designed to tap into the specificities of each market. Blackmores has chosen some of the fastest growing channels in each region. In South Korea Blackmores is sold through the dominant TV home shopping sales channel which saw growth of 23% in FY11 and taps into South Korea’s gift culture. In Hong Kong, Blackmores’ partnership with Eu Yan Sang is designed to take advantage the local popularity of Traditional Chinese Medicine. In China Blackmores’ use of the official retailer section of online platform Taobao and single store Shanghai’s No. 1 Pharmacy represents a way to test the market before fully committing resources to a country-‐wide expansion.

CFA Institute Research Challenge 24.09.2012

Figure 7: Historical market share of top 5 VDS Brands in Thailand

Source: Euromonitor

Figure 8: Historical market share of top 5 VDS Brands in Malaysia

Source: Euromonitor

Source: Euromonitor

Figure 6: Australian VDS Market Share by Brand

Sydney University Research Group 4

Product quality Blackmores’ Australia based production signals quality and differentiates it from major competitors; Blackmores’ products are complementary goods meaning production must comply with TGA guidelines. This, together with the continually evolving research on the benefits of complementary medicines, provides a high amount of credibility to the VDS industry. Further, the necessary compliance with these TGA standards also extends to the exported VDS products from Australia, reinforcing the quality, and hence competitive positioning, of Blackmores in the Asian market.

Company Strategy Product Innovation & Diversification In order to consolidate market position within Australia, Blackmores continues to aggressively diversify product offerings and increase levels of new product development, with the introduction of over 102 new products in FY12. The recent acquisition of FIT-‐BioCeuticals positions Blackmores to achieve substantial growth to revenues and NPAT through leveraging resources and knowledge. We identify that Blackmores will achieve these targets through broadening their customer base by incorporating the practitioner only segment, diversifying itself from traditional retailing activities. FIT-‐BioCeuticals is the practitioner segment leader in the market, with 1 in 4 Australian adults visiting natural health practitioners each year Blackmores’ strategy is to capture this growing market. Potential for cross selling within the practitioner market also extends the channels by which Blackmores can grow its core brand revenues. This will allow Blackmores to affirm itself as the largest Australian natural healthcare brand. Blackmores’ Australian strategy also involves a focus on product development as they seek to be ‘innovators’ or ‘fast followers’ within the VDS market. Competition in the Australian VDS market is tightening, seen through stable proportions of market share over several years. Figure 9 displays the lack of market share growth for recognised VDS brands. This tightening has led Blackmores to intensify product segmentation and development with 55 improved products in FY12 compared to 21 in FY11. This 162% increase in new product offerings reflects Blackmores’ strategy of deep product segmentation in order to increase current market share. Historical data demonstrates a strong positive trend between sales growth and product development, with 3.1% and 10.7% growth in sales for FY11 and FY12 respectively, reaffirming the success of their strategy. Additional gains are also recognised when benchmarked to key competitors due to the unique position of Blackmores in consumer minds, as it is distinguished as providing superior quality products. Asia – Expand distribution and increasing product awareness Economic conditions are strong within the Asian markets, with an average of 5.6% GDP growth in all of Blackmores Asian operating countries. Thus, Blackmores’ strategy is to leverage this through increased market share by expanding their Asian distribution and increasing product awareness. Specifically, Blackmores employees Ian Thorp as a brand embassidor and has incorporated the ‘Blackmores Sydney Running Festival brand champaign’ in Thailand. Blackmores will continue to leverage off their high quality reputation and strategically form partnerships with local healthcare companies and retail distributors. Emulating its relationship with that of Eu Yan Sang Ltd. in Singapore is vital for its penetration plans into China. Figure 11 displays companies of strategic significance for Blackmores in the Asian markets. Partnering with dominant Traditional Chinese Medicine (TCM) companies and healthcare retailers will create substantial revenue enhancement by establishing product awareness in the region. Alliances will also create a distinct position for Blackmores among other Western companies as it connects Asian consumers between Western and Eastern natural health forms and will improve prospects of achieving targets of 20% sales growth.

Investment Summary Structural growth within the industry We forecast NPAT to grow by 44.4% to A$40.2 million in FY16, from the current A$27.8 million, driven by expansion into Asian markets, ageing populations in Asia and Australia, product innovation and growing sales in the grocery and discount pharmacy channels. Blackmores’ footprint expansion continues with 26 new products in 3QFY12 and entry into the Chinese retail market on track for 1QFY13. However, domestic profit margins are expected to be flat throughout the forecast period. The fragmented market will put high

Source: BKL Data

Figure 11: Asian Strategic Partners

Figure 10: Blackmores New Product Development Strategy

CFA Institute Research Challenge 24.09.2012

Source: Euromonitor

Figure 9: Changes in Australian VDS Brand Market Share

Sydney University Research Group 5

amounts of pricing pressure on the grocery and discount pharmacy channels as upstart competitors, such as Swisse, seek market share.

Asia Growth Engine Collectively, Asian revenue grew by 20.0% in FY12 to a total of A$53.0 million. NPAT grew 35.0% to A$7.2 million, representing 26.0% of the Group’s profit. We forecast Blackmores’ Asian revenues to grow at strong double-‐digit rates throughout the forecast period as a result of increased market share through new products, strong marketing and increased investment support. Notably, Thailand and Malaysia experienced robust revenue growth of 21.0% and 12.5% respectively throughout FY12. We remain positive on the growth outlook for these regions, with expected top line FY13-‐16 CAGR of 16.5% and 11.8%, and expect strong growth out of smaller markets, such as Korea and Hong Kong, of top line CAGR of 23.6%. In FY12, Blackmores’ tripled its distribution points in Asia and launched in both Taobao, China’s largest e-‐commerce platform and in China’s largest pharmacy, Shanghai No. 1 Pharmacy. High brand equity Blackmores is currently the most visible and trusted vitamin and supplement brand in Australia, winning Reader’s Digest Most Trusted Brand Survey for 4 consecutive years. In the same survey for, Blackmores was rated the number one trusted VDS brand in Thailand and number two in Malaysia in 2012. Blackmores also has a strong position in Google page ranks for health related product and service searches, Blackmores is searched for directly over 50,000 times per month and also has strong positioning in searches for vitamins, detox and fish-‐oil, where it is ranked two after Wikipedia.org.

Industry Growth The VDS industry is a continually growing segment of the Consumer Health market with CAGR CY11-‐2016 of 2.6% and 5.2% for Australia and China respectively. Within the industry Blackmores has maintained the highest percentage value with respect to Brand, consistently between 18.0% and 19.0% from FY08 to FY11. Although Blackmores’ share of retail value has plateaued, the industry will continue to be driven by the ageing population, obesity and increasing healthcare awareness.

Balance sheet remains sound Blackmores’ balance sheet remains robust and retains meaningful capacity for growth with solid forecasted gearing metrics of net debt/EBITDA of 1.17x and interest cover of 13.62x for FY13. This provides a strong financial base for expansion and growth and the means to absorb adverse shocks throughout Blackmores’ expansion into Asia through either organic or inorganic means. Blackmores is trading at a current PE multiple of 19.0x, which is one of the highest in the industry, suggesting strategic acquisition for growth would be EPS accretive.

Acquisition of FIT-‐BioCeuticals We see the acquisition of FIT-‐BioCeuticals as a sound strategic and financial fit for four key reasons: 1) increased offerings in the practitioner channel and a reduction in Blackmores’ reliance on the competitive supermarket channel; 2) a deepening and widening of Blackmores’ extensive product offerings; 3) creation of value through a sharing of sourcing and R&D and an opportunity to leverage Blackmores’ warehousing and distribution capabilities in the long term; 4) the addition of an unparalleled depth of expertise via the addition of 100 qualified healthcare professionals including doctors, pharmacists and naturopaths.

Figure 14: BKL share price and volume LTM

Source: BKL Data; Capital IQ

CFA Institute Research Challenge 24.09.2012

Figure 12: Blackmores’s historic and forecast NPAT and NPAT margin

Source: Capital IQ; SURG Estimates

Figure 13: Historic VDS Industry Growth

Source: Euromonitor

Sydney University Research Group 6

Valuation Our final price of $37.73 per share intrinsic value estimate was derived by two methods – a discounted cash flow analysis and multiples analysis for the consolidated entity, with weightings of 70% and 30% respectively. The 70% weighting attached to the DCF method reflects the models ability to explicitly describe risk and also account for the high growth opportunities that Blackmore’s currently have in the Asian markets, as well as dealing with the more mature revenues that Blackmore’s experiences in the Australian market. Discounted Cash Flow (DCF) Valuation The DCF valuation produced an intrinsic value per share of $38.33, derived by discounting back future FCFF by the WACC calculated for Blackmore’s. The assumptions for the model are outlined below. Revenues: Individual revenues for each geographic segment of Blackmores’ operations were modelled with different growth rates independently, as this allows for a appropriate representation of the unique growth opportunities in each region. By proportion, the total revenue is dominated by the contribution of the Australian segment revenue. Due to Blackmores’ long-‐standing presence in the Australian market, it is felt that they are approaching a mature stage of operations in this region. As such, revenues were forecast to slowly decline to 3.5% over the 10 year forecast. Other important regions include Blackmores’ Thai operations and their operations throughout ‘Other Asia’. These divisions were forecast to continue the strong growth that they have seen previously over the past five years as Blackmores increases its presence before declining over the proceeding five years. FIT-‐BioCeuticals was forecast as a separate entity throughout the forecast period at a steady rate of 4%.The long term growth rate was determined as 2.15%. This growth rate was derived from the averages of GDP growth, inflation rates and population growth throughout the Asia Pacific region. Inventories: Although Blackmores’ Sydney warehouse is currently operating at capacity, their WA warehouse is operating at only approximately 25%. It is evident that as the aggressive expansion throughout Asia continues, so too will the inventory account. This was modelled as a gradual increase in the account over the forecast horizon with respect to sales. Accounts Receivable: Currently, Blackmores’ receivables are dominated by their three largest clients, Woolworths Limited, Chemists Warehouse, and Wesfarmers Limited which comprise approximately 57% of the account. Given the current economic stability that exists in Australia, in conjunction with the conglomerate nature of the firms, accounts receivable was forecast as maintaining its historical average with respect to sales. Non-‐Cash Charges: Amortization was modelled during the forecast horizon as a function of the intangibles account. This is felt to be consistent with the increased research and development being carried out by Blackmore’s as part of their Blackmore’s Institute initiative. Depreciation is forecasted as a function of PPE due to the historically strong correlation between the accounts. Capital Expenditure: Capital Expenditure was modelled to be increasing year on year throughout the forecast horizon until growth slowed in the final years. During the growth years, capital expenditure per year is approximately $7.5m. This is consistent with the expenditure required to fund the aggressive expansion by Blackmore’s throughout Asia. Change in Net Working Capital: Throughout the forecast horizon, net working capital increases proportionally year on year. This is intuitive due to the requirements for inventory and accounts receivable as Blackmores’ expands. Per year, net working capital increases on average $6.2m. It should be noted that in FY13, there is a sharp increase in working capital due to the increased inventory and accounts receivable from the acquisition of FIT-‐BioCeuticals. Capital Structure: Over the past decade, Blackmore’s has had a highly varied capital structure, as determined by their Net D/E ratio. Over this period, the figure averages out to approximately 30%. As it becomes increasingly complex to model changing capital structure during the forecast period, the average was taken as a conservative figure to use when determining the Weighted Average Cost of Capital for Blackmore’s. Although the debt funded acquisition of FIT-‐BioCeuticals pushed the net gearing ratio up to 78.91%, it is expected that Blackmores will attempt to pay off debt early to attempt to minimise

WACC and Terminal Value Shares Outstanding (A$m) 16.78

Current Share Price $31.50

Market Capitalisation (A$m) $528.63

Total Debt (A$m) $86.00

Current D/E Ratio 78.91%

Target D/E Ratio 30.00%

Common equity weighting 76.92%

Debt weighting 23.08%

Cost of debt 5.36%

Tax Rate 30.00%

Tax-‐adjusted cost of debt 3.75%

Risk-‐free rate 5.00%

Beta 0.62

Market Risk Premium 6.50%

Cost of equity 9.01%

WACC 7.80%

Terminal Growth Rate 2.15%

Terminal Value (A$m) $942.94

PV(Terminal Value) (A$m) $445.07

Methodology Method Value

Weighting Per Share

DCF Analysis 70% $38.33 Consolidated Multiples 30% $36.33

Target Price Strong Buy $37.73

CFA Institute Research Challenge 24.09.2012 CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 7

Table 2: Valuation Method Triangulation

Table 3: WACC and Terminal Value Calculations

Source: SURG Estimates

Source: Capital IQ; SURG Estimates

financial risk while simultaneously taking on operational risk through their Asian expansion. Key takeaways from the DCF analysis • Although Blackmores is breaking into the Asian markets rapidly, revenue is still

supported largely by Australian operations. At present, Australian operations still account for ~77% of their revenue streams. By the end of the forecast horizon, this figure is still ~60%, a very healthy amount. This can be seen as a key indicator of the strong financial base that Blackmore’s is currently growing from, indicative of stability even in the event of poor performance in more risky geographies, where competition is tougher and different regulatory risks exist.

• Even with the conservative revenue growth profiles used for expansions such as Thailand, there is still significant underlying value within the Blackmore’s operations that has not yet been fully realised by the market.

To ensure prudency in our financial model, we performed several sensitivity analyses on the reasonable ranges of WACC, terminal growth rates, cost of equity and cost of debt. In addition, a Monte Carlo Simulation was carried out on the revenue growth profiles of each geographic segment. The DCF value still held a strong value with a range between $35.99 and $40.76, with 90% confidence. Additionally, the sensitivity analyses of factors including WACC and terminal growth rate indicated a high level of robustness in the financial model, with reasonable target prices across a range of inputs. Relative Valuation Consolidated entity value In order to complete this analysis a median NTM EV/EBITDA and NTM P/E multiples was applied. The comparables cover the functions of Blackmores’, including production, manufacturing, distribution and marketing. Of significance is the commonality of the firms operating in Asian markets. This has been identified as a crucial factor as the Asian region is forecast to shape growth prospects for Blackmores with the complementary health sector growing by c.10% annually and earnings from Asia accounting for 26% of Group profits in FY12 up from 20% in FY11. Both pharmaceuticals and VDS companies were used when performing the multiples analysis. The growing acceptance of complementary medicines has caused VDS to be perceived as on par to pharmaceuticals and consequently firms within the industries are becoming similar with regard to revenues and costs. This is captured by a consistency between gross margins between the comparables chosen. Figure 15 demonstrates the similarity in average firm gross margins across both the VDS and pharmaceutical companies. Further, a crucial driver in the comparable company selection was the market positioning of each company. The comparables are either market leaders or strategically placed to capture gains in a turbulent environment. This is considered to be analogous to the positioning of Blackmores’ in Australia and Asia respectively. Determination of Value As a consolidated entity, the relative valuation yielded an implied share price of $37.66 and $35.00 when applying a NTM EV/EBITDA and NTM P/E multiples respectively. The median of 12.4x and 18.3x were multiplied by calendarised NTM EBITDA and NTM NPAT. This accounts for the forecasts by SURG for FY13 and the reported FY12 figures. In order to fully realise the future value Blackmores’ will deliver, the utilisation of forward looking estimates was vital. A clear upside potential is seen for Blackmores’ share price. Weighting each multiple valuation at 50% a final relative value of $36.33 was computed. A clear buy presenting a 15.3% upside on the current share price

Financial Analysis Sales: Growth driven by Asian expansion and new product development. Australia: We expect steady revenue growth in the domestic market, with 6.5% and 6.25% in FY13 and FY14 respectively. Short-‐term growth will be driven by new product offerings from the FIT-‐BioCeuticals acquisition and product segmentation. Growth is expected to slow in the medium-‐term to 5.5% by FY16 with the Company’s consolidation strategy dampened by increasing competition in the VDS sector. With a conservative domestic

Company EV/EBITDA P/E Amway Malaysia 12.4 18.3 Australian Pharmaceutical Group

4.9 8.2

Balchem 14.1 25.4

Cerebos Pacific 8.5 -‐ EBOS Group 9.3 12.5 Glenmark Pharmaceuticals 14.2 18.2

Raffles Medical 18.2 23.6 Schiff Nutrition International 17.0 24.1

Sigma Pharmaceuticals 8.7 14.9

USANA Health Sciences 6.1 9.7

Vitamin Shoppe 13.9 24.1

Median 12.4 18.3

EV/EBITDA P/E

Calendarised EBITDA NTM 56.11

Calendarised NPAT NTM

32.10 EV 695.72

Less: Net Debt 63.74 Equity Value 631.98 587.40

SOI 16.78 16.78 Equity Value Per Share $37.66 $35.00 Average Value Per Share $36.33

Source: SURG EstimatesSource: Euromonitor

Figure 16: Forecast non-‐Australian segment revenueFigure 15: Gross Margins of VDS

and Pharmaceutical Industries

CFA Institute Research Challenge 24.09.2012

Table 4: Comparables’ Multiple Values

Table 5: Blackmores Relative Valuation

Source: Capital IQ

Source: Capital IQ; SURG Estimates

Sydney University Research Group 8

strategy, the company will focus on strengthening its position in emerging Asian markets. The greatest opportunities lie in China and South Korea – the largest VDS markets in Asia.

China and South Korea: These two markets hold great potential for Blackmores and we forecast solid sales growth, reflected by a 23.7% CAGR in revenue for the ‘Other Asia’ segment from FY12 to FY16. This translates to an increase from $13.4m to $31.3m. We acknowledge the risks involved in these assumptions and have built these into a Monte Carlo simulation (appendix 7).

Thailand and Malaysia: Historically, Thailand and Malaysia have been highly successful markets for Blackmores with 21.0% and 16.6% CAGRs for FY10-‐11. We expect this trend to continue with new product launches and increased marketing activity, leveraging their strong brand equity in the region. Sales in Thailand and Malaysia are forecast to reach $45.8m and $23.6m respectively by FY16, representing 16.8% and 11.8% CAGR.

Free Cash Flows FCFF are negative in FY13 due to inflated working capital and CAPEX arising from the acquisition of FIT-‐BioCeuticals. Beyond this, FCFF will grow over the forecast horizon with increasing sales. Working capital requirements are forecast to increase from $71.0m in FY12 to $108.2m in FY16 as the company increases inventories in their Perth warehouse, catering to forecast increased sales in Asia. CAPEX requirements are also forecast to increase. These increases will be offset by the company’s EBIT, which is forecast to grow from $42.7m in FY12 to $60.5m in FY16. This accounts for the overall increase in FCFF. Dividend policy will consume a portion of the company’s FCFF with the payout ratio forecast to remain constant at 76.0%. This translates to dividends of $30.5m by FY16. Remaining FCFF will be used for debt obligations and investment in future growth.

Financing and Balance Sheet At the end of FY12 Blackmores’ net debt position was position $34.1m. Accounting for the Company’s $40m acquisition of FIT-‐BioCeuticals, Blackmores’ net debt is currently at $74.1m. Net debt is then expected to decrease to $45.4m by FY16, in line with the approximate historical capital structure of 30%, as Blackmores pays off its debt, resulting in a net debt to equity ratio of 38%. This places Blackmores in a favourable position, with enough room to finance further product development and growth in Asia. Additionally, Blackmores has a current Altman Z score of 6.37, placing it well into the “safe zone”, indicating the company is not in immediate danger of financial distress. 55.6% of Blackmores’ debt is fixed rate in FY12.

Investment Risks Product risk -‐ Blackmores’ strategy is growth through product segmentation, innovation and expansion. The Blackmores brand launched 102 new products and 43 renovations globally in FY12. However, a greater number of products can lead to a mismatch between product design and consumer preference, leading to lower than expected sales. Additionally, some of the fastest growing products in Asian markets are super foods and traditional medicines that Blackmores have not historically dealt with. Competition from tonics, bottled nutritive drinks and super foods -‐ In Thailand tonics and bottled nutritive drinks outperformed over CY11 with the highest current value growth rate of 32%. Major players, Cerebos and Scotch, are benefiting from strong performance in this segment, which could expose Blackmores to margin pressure if competitors subside their other businesses. Super foods are also popular in Asia and Blackmores may be entering into markets where it currently does not have the expertise, scope, or experience to compete.

2012A 2013E 2014E 2015E 2016E

2012A 2013E 2014E 2015E 2016E

Profitability Ratios EBITDA Margin 18.03% 16.89% 16.75% 16.65% 16.54% ROA 16.30% 13.97% 14.51% 15.02% 15.47%

EBIT Margin 16.31% 14.84% 14.83% 14.83% 14.82% ROE 33.60% 33.53% 33.55% 33.56% 33.29% NPAT Margin 10.46% 9.63% 9.70% 9.77% 9.84%

Solvency Ratios Total Debt/Equity 53.31% 85.26% 73.49% 63.07% 53.89% Net Debt/EBITDA 0.72x 1.17x 0.98x 0.82x 0.67x

Net Debt/Equity 39.45% 68.55% 56.88% 46.59% 37.65% Interest Coverage 14.5x 13.62x 15.18x 17.05x 19.31x Market Ratios

CAPEX Ratios

DPS $1.27 $1.42 $1.55 $1.68 $1.82 CAPEX/Revenues 2.09% 9.57% 2.05% 1.92% 1.81% Basic EPS $1.66 $1.87 $2.04 $2.22 $2.39 D&A/CAPEX 90.11% 21.41% 93.99% 94.66% 95.29%

Figure 17: Forecast EBITDA, EBIT and FCFF

Source: SURG Estimates

Table 6: Key Financial Ratios

Source: SURG Estimates

CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 9

Figure 11: Forecast non-‐Australian segment revenue

Source: SURG Estimates

Margin erosion -‐ The VDS market is seeing increasing pricing pressure. Low cost competitors like Swisse have increased vitamin market share from 1.2% to 1.6% over CY08 to CY11 by offering a lower cost alternative to higher cost Blackmores and Sanofi-‐Aventis. Major distributors like Woolworths, Coles and Chemist Warehouse have also put increasing pressure on suppliers in a bid to compete with each other. In FY12 Blackmores’ promotions and other rebates line items rose 42% reflecting growth in grocery and discount channels through discounts and promotions. Continued price competition poses a threat to the premium that Blackmores’ leadership commands. Restricted Asian sales models -‐ Blackmores’ employs a distribution/retail partnership in Hong Kong, Thailand, China and Singapore. However this method of distribution ignores the fast growing direct selling channel with market shares of approximately 49%, 33%, 52% and 23% in the aforementioned countries. International brands are often stocked together in local distributors such as Watsons leading to increased competition for the firm as compared to the direct selling model. Blackmores may also appear less differentiated as opposed to firms like GNC, which operates stores within stores. In South Korea, Blackmores’ strategy is focused on direct selling via home shopping. CJ Cheil Jedang Corp has begun competing in store-‐based retail channels at lower prices than direct sellers; hence this may be a venue that poses competition to the Group. Online risk -‐ Given current trends in retail we expect consumers may begin seeking vitamins and dietary supplements online as well. In CY11 online retailers of vitamin and dietary supplements in Australia saw their share of sales increase. Blackmores and its competitors currently lack direct sales to consumers via their websites although products are available via third parties. However, Blackmores is well placed for online sales with an online community of over 360,000 members. Financial risks: Fluctuations of exchange rates -‐ Blackmores is exposed to exchange rate risk and has approximately 60% of its cost of sales denominated in US Dollars and 23% of revenues from foreign countries (9% Thailand, 6% Malaysia, 5% Other Asia, 2% New Zealand, 1% Other). On the basis of five years of average monthly data, we estimate that the USD to AUD exchange rate has the most significant coefficient of variation of 12.97%. However, Blackmores has hedged exchange rate risk via to the opening of the USD bank account to utilise the natural hedge between intercompany receipts from Asia and USD exposure on purchases of raw materials. Blackmores also sources many of its ingredients in the countries in which it operates which acts as a natural hedge. Operative risks: Increase in raw materials and marketing costs -‐ Raw materials account for approximately 35% of Blackmore’s total costs. Hence, their fluctuation has a moderate impact on profitability as Blackmores does not explicitly hedge commodity risk. Additionally, marketing expenses account for 11.33% of total costs. Blackmores has encountered heavy marketing by major players in Thailand and by Swisse in Australia. Blackmores will also assumedly incur new marketing expenses in Mainland China where competitors often employ high profile athletes to represent their brands. Product defects -‐ Defects and product recalls may affect Blackmores’ image, cause a negative impact on revenues, and lead to the intrusion of regulators. For example, in 2003 the Therapeutic Goods Administration (TGA) suspended Pan Pharmaceutical’s license leading to the collapse of the company.

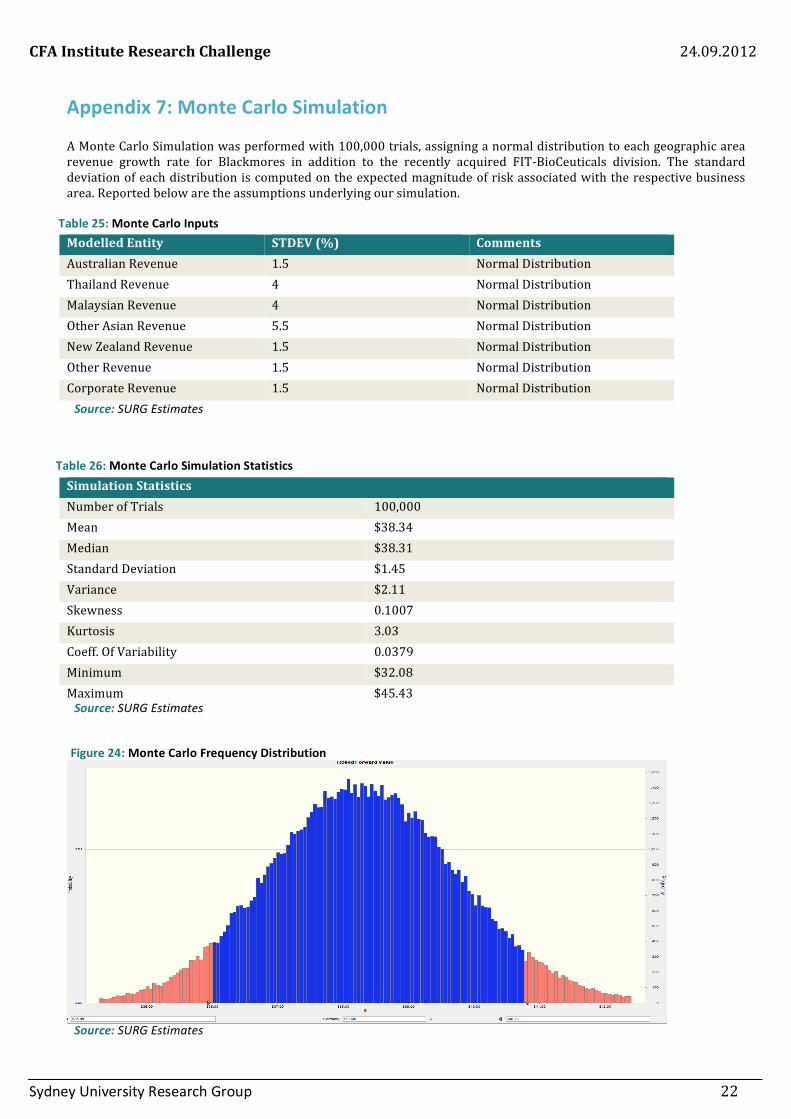

Monte Carlo Simulation Given the substantial growth opportunities that Blackmores has throughout Asia that presents substantial value creation opportunities, we conducted Monte Carlo simulation using prudent volatility estimates with respect to each geographic operation. The end result is a distribution on the target price with a standard deviation of $1.45 around the $38.34 mean. This gives a target range between $35.99 and $40.76 with 90% confidence. The greatest contributor to the risk profile was felt to be due to the operations in the greater Asia region, including Hong Kong, Taiwan, Singapore, South Korea and China. Details on the Monte Carlo Simulation can be found in appendix 7.

Sydney University Research Group 10

Appendices

Appendix 1: Pro-‐forma Financial Statements Income Statement (AUD $m) 12 months 12 months 12 months 12 months 12 months For the Fiscal Period Ending Jun-‐30-‐2012 Jun-‐30-‐2013 F Jun-‐30-‐2014 F Jun-‐30-‐2015 F Jun-‐30-‐2016F Revenues Australia Revenue $222.32 $236.77 $251.57 $266.66 $281.33 Australian Revenue Growth 10.73% 6.50% 6.25% 6.00% 5.50% Thailand Revenue $24.62 $29.77 $35.28 $40.92 $45.83 Thailand Revenue Growth 21.01% 20.90% 18.50% 16.00% 12.00% Malaysia Revenue $15.08 $17.27 $19.34 $21.47 $23.61 Malaysian Revenue Growth 12.54% 14.50% 12.00% 11.00% 10.00% Other Asia Revenue $13.37 $16.72 $20.89 $26.12 $31.34 Other Asia Revenue Growth 25.42% 25.00% 25.00% 25.00% 20.00% New Zealand Revenue $4.95 $5.16 $5.37 $5.59 $5.81 New Zealand Revenue Growth 13.50% 4.43% 4.00% 4.00% 4.00% Other Revenue $2.47 $2.47 $2.47 $2.47 $2.47 Other Revenue Growth 76.41% 0.00% 0.00% 0.00% 0.00% Corporate Revenue -‐$21.20 -‐$23.05 -‐$25.01 -‐$27.09 -‐$29.07 Corporate Revenue Growth 35.03% 8.73% 8.50% 8.31% 7.31% FIT-‐BioCeuticals Revenue $40.00 $41.60 $43.26 $44.99 $46.79 FIT-‐BioCeuticals Revenue Growth -‐ 4.00% 4.00% 4.00% 4.00% Total Revenues $261.61 $326.70 $353.17 $381.13 $408.12 Operating Expenses $215.20 $271.51 $294.00 $317.69 $340.60

EBITDA $47.17 $55.19 $59.17 $63.44 $67.52 EBITDA Margin 18.03% 16.89% 16.75% 16.65% 16.54% Depn & Amortization -‐$4.92 -‐$6.69 -‐$6.80 -‐$6.92 -‐$7.03

EBIT $42.67 $48.50 $52.37 $56.52 $60.49 EBIT Margin 16.31% 14.84% 14.83% 14.83% 14.82% Finance Costs -‐$2.93 $4.29 $4.20 $4.13 $4.00 Finance Costs/Total IBLs 6.38% 5.36% 5.36% 5.36% 5.36% Earnings Before Taxes $39.97 $44.94 $48.92 $53.21 $57.36

Taxes $11.39 $13.48 $14.68 $15.96 $17.21 Income Tax Expense/Revenues 4.35% 4.13% 4.16% 4.19% 4.22% Net Income (Loss) $27.81 $31.46 $34.24 $37.25 $40.15 Net Profit Margin 10.63% 9.63% 9.70% 9.77% 9.84% Dividends -‐$21.31 -‐$23.91 -‐$26.02 -‐$28.31 -‐$30.51 Dividend Payout Ratio 76.65% 76.00% 76.00% 76.00% 76.00% Retained Earnings $6.49 $7.55 $8.22 $8.94 $9.64

CFA Institute Research Challenge 24.09.2012

Table 7: Pro-‐forma Income Statement

Source: SURG Estimates

Sydney University Research Group 11

Partial Balance Sheet (AUD $m) 12 months 12 months 12 months 12 months 12 months

as of Jun-‐30-‐2012 Jun-‐30-‐2013 F Jun-‐30-‐2014 F Jun-‐30-‐2015 F Jun-‐30-‐2016 F Current Assets

Cash & Cash Equivalents $11.96 $16.26 $16.95 $18.29 $19.59 Trade Debtors $53.70 $65.63 $70.95 $76.57 $81.99 Inventories $31.79 $39.20 $42.38 $45.74 $48.97 Non Current Assets Net PP&E $65.92 $91.00 $92.00 $93.00 $94.00 Intangibles (Inc. Goodwill)

$2.91 $3.27 $3.53 $3.81 $4.08

Current Liabilities

Trade Payables $14.20 $17.97 $19.42 $20.96 $22.45 Other Creditors and Accruals $19.88 $23.52 $25.43 $27.44 $29.38

Non Current Liabilities

Long Term Debt $46.00 $80.00 $75.00 $70.00 $65.00 Annual Leave & Long Service Leave Accrued $.91 $1.01 $1.11 $1.21 $1.31

Equity Total Shareholder's Equity $86.28 $93.83 $102.05 $110.99 $120.62

CFA Institute Research Challenge 24.09.2012

Table 8: Pro-‐forma Partial Balance Sheet

Source: SURG Estimates

Sydney University Research Group 12

Consolidate Market Position

Product Development Diversify Product Offerings

Strengthen Operations in Asia

Strong Partnerships

Connect East & West Natural Medicine

Innovative market relevant products

Create product awareness

Appendix 2: Strategic Analysis

CFA Institute Research Challenge 24.09.2012

Figure 18: Blackmores Australian Strategy Figure 19: Blackmores Asian Strategy

Strengths • Established and trusted brand name with 80 years experience – reiterated by a new marketing campaign • Number 1 recognised retail vitamin brand in Thailand and number 2 in Malaysia. • Growth driven CEO, spurred by a long sighted remuneration strategy • Highly efLicient supply chain with customers dealing directly with the warehouse facility

Weaknesses • Lack of well deLined and unique operational strategy • Asian expansion has been with existing product lines – There has been limited product development tailored to speciLic consumer tastes in the differing markets • Limited distribution channels/partners – Coles, Woolworths and Chemist Warehouse comprise 57% of Australian sales

Opportunities • Further expansion in Asia – geographically (into Mainland China) and with new product launches and distribution partnerships. • Development of a direct online retail platform • Organic growth prospects from newly acquired pet care and practitioner-‐only segments.

Threats • Increasing domestic competition in VDS sector and sports nutrition • Increasing marketing activity from competitors -‐ especially Swisse and Nature’s Own • With the rise of discount chemists, retailers may demand lower prices from Blackmores to avoid contracting their own proLit margins.

SWOT

Figure 20: Blackmores SWOT Analysis

Source: SURG Estimates

Source: SURG Estimates

Source: SURG Estimates

Sydney University Research Group 13

Rivalry Amongst Existing Competitors • Competition is fierce and competitive

advantage often comes down to marketing effort and brand awareness.

• Product differentiation can be easily emulated by competitors

Threat of Substitutes • Overall threat of is low, with the

major being Traditional Chinese Medicine (TCM).

• Threat from over-‐the-‐counters medications is low as they are often taken in addition to vitamins and dietary supplements.

Threat of New Entrants • Barriers to entry are strong with high

CAPEX requirements for new firms. • Scale advantages and industry

experience of incumbents make entry difficult.

Bargaining Power of Suppliers • Bargaining power of

suppliers is weak. Blackmores does not require highly specialised inputs.

Bargaining Power of Buyers • With no direct selling

channels, Blackmores competes for limited shelf space giving the retailers (buyers) significant bargaining power.

• 3 buyers contribute 57% of revenue

Figure 21: Porter’s 5 Forces Analysis for Blackmores Australian Operations

CFA Institute Research Challenge 24.09.2012

Rivalry Amongst Existing Competitors • Competition is fierce and

competitive advantage often comes down to marketing effort and brand awareness.

• Blackmores is a relatively small player and must compete with large, well-‐established domestic brands

Threat of Substitutes • Moderate threat with popularity

of Traditional Chinese Medicines (TCM)

Bargaining Power of Suppliers • Bargaining power of

suppliers is weak. Blackmores does not require highly specialised inputs.

Bargaining Power of Buyers • With no direct selling

routes, Blackmores competes for limited shelf space giving the retailers (buyers) significant bargaining power.

• Costs of switching between Asian distributors are moderate due to the complexity of foreign business negotiations.

Threat of New Entrants • Barriers to green-‐field entry are

strong with high CAPEX requirements and differing regulatory constraints

• High threat of entrants from existing companies pursuing an Asian expansion strategy looking to capitalise on growth in the region.

Figure 22: Porter’s 5 Forces Analysis for Blackmores Asian Operations

Source: SURG Estimates

Source: SURG Estimates

Sydney University Research Group 14

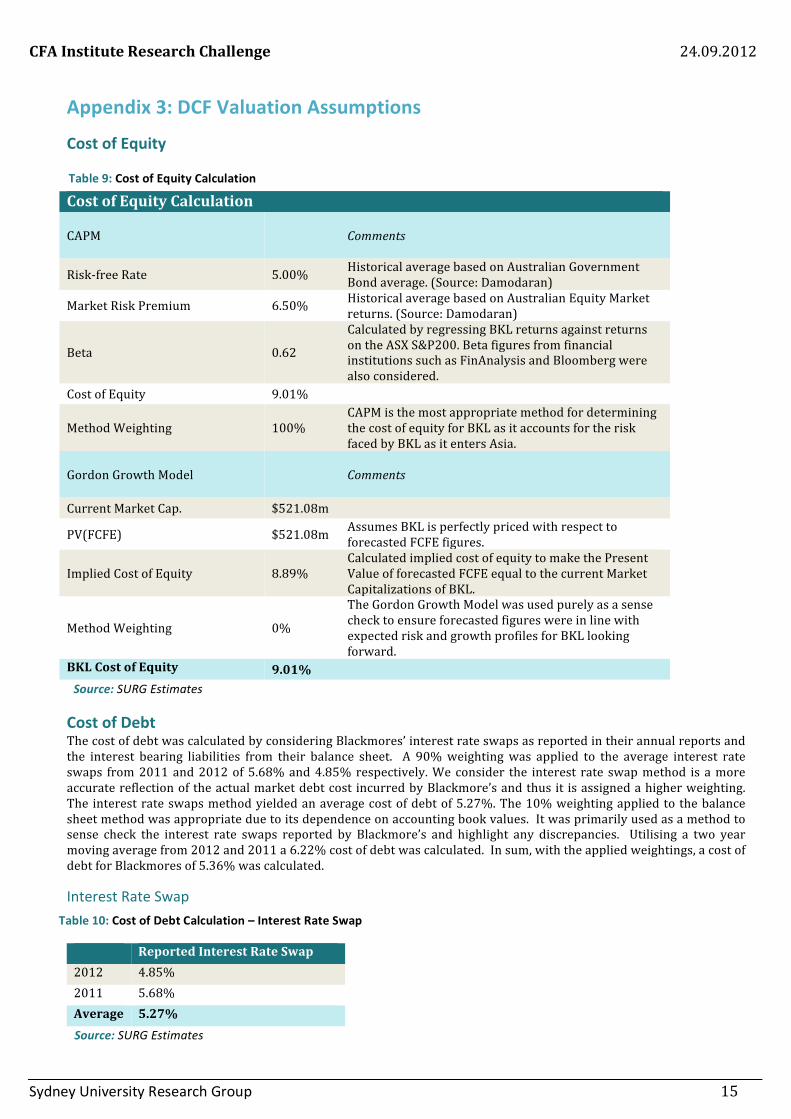

Appendix 3: DCF Valuation Assumptions

Cost of Equity Cost of Equity Calculation CAPM

Comments

Risk-‐free Rate 5.00% Historical average based on Australian Government Bond average. (Source: Damodaran)

Market Risk Premium 6.50% Historical average based on Australian Equity Market returns. (Source: Damodaran)

Beta 0.62

Calculated by regressing BKL returns against returns on the ASX S&P200. Beta figures from financial institutions such as FinAnalysis and Bloomberg were also considered.

Cost of Equity 9.01%

Method Weighting 100% CAPM is the most appropriate method for determining the cost of equity for BKL as it accounts for the risk faced by BKL as it enters Asia.

Gordon Growth Model

Comments

Current Market Cap. $521.08m

PV(FCFE) $521.08m Assumes BKL is perfectly priced with respect to forecasted FCFE figures.

Implied Cost of Equity 8.89% Calculated implied cost of equity to make the Present Value of forecasted FCFE equal to the current Market Capitalizations of BKL.

Method Weighting 0%

The Gordon Growth Model was used purely as a sense check to ensure forecasted figures were in line with expected risk and growth profiles for BKL looking forward.

BKL Cost of Equity 9.01%

Cost of Debt The cost of debt was calculated by considering Blackmores’ interest rate swaps as reported in their annual reports and the interest bearing liabilities from their balance sheet. A 90% weighting was applied to the average interest rate swaps from 2011 and 2012 of 5.68% and 4.85% respectively. We consider the interest rate swap method is a more accurate reflection of the actual market debt cost incurred by Blackmore’s and thus it is assigned a higher weighting. The interest rate swaps method yielded an average cost of debt of 5.27%. The 10% weighting applied to the balance sheet method was appropriate due to its dependence on accounting book values. It was primarily used as a method to sense check the interest rate swaps reported by Blackmore’s and highlight any discrepancies. Utilising a two year moving average from 2012 and 2011 a 6.22% cost of debt was calculated. In sum, with the applied weightings, a cost of debt for Blackmores of 5.36% was calculated.

Interest Rate Swap Reported Interest Rate Swap 2012 4.85% 2011 5.68% Average 5.27%

CFA Institute Research Challenge 24.09.2012

Source: SURG Estimates

Source: SURG Estimates

Table 9: Cost of Equity Calculation

Table 10: Cost of Debt Calculation – Interest Rate Swap

Sydney University Research Group 15

Balance Sheet interest Bearing Liabilities 2011 2012 Interest Expense 2.37 2.93 Total IBL 40 45 Implied Cost of Debt 5.93% 6.51% 2 Year Average 6.22%

Cost of Debt Calculation Cost of Debt Weighting Weighted Cost of Debt Interest Rate Swap Method 5.27% 90% 4.74% IBL Method 6.22% 10% 0.62% Total Cost of Debt 5.36%

WACC WACC and Terminal Value Assumptions Comments Shares Outstanding (mn) 16.78 Current Share Price (24/09/12) $31.50 Market Capitalisation ($m) $528.63 Total Debt ($m) $86.00 Current D/E Ratio 76.92% Target D/E Ratio 30.00% Optimal gearing ratio estimated

for BKL looking forward Common Equity Weighting 76.92% Debt Weighting 23.08% Cost of Debt 5.36% Tax Rate 30.00% Tax-‐Adjusted Cost of Debt 3.75% Cost of Equity 9.01% WACC 7.80%

Terminal Growth Rate 2.15% Long Term growth rate estimates. See appendix 4

CFA Institute Research Challenge 24.09.2012

Source: SURG Estimates

Source: SURG Estimates

Source: SURG Estimates

Table 11: Cost of Debt Calculation – IBL Method

Table 12: Cost of Debt Triangulation

Table 13: WACC and Terminal Value Calculation

Sydney University Research Group 16

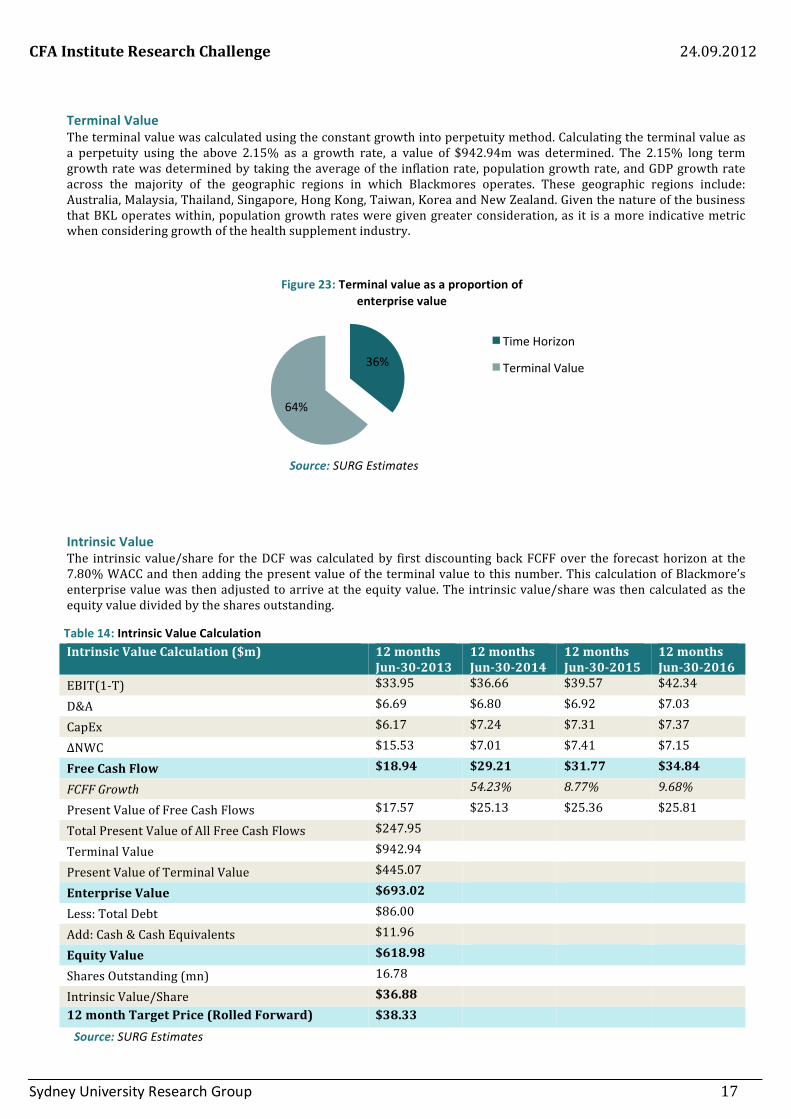

Terminal Value The terminal value was calculated using the constant growth into perpetuity method. Calculating the terminal value as a perpetuity using the above 2.15% as a growth rate, a value of $942.94m was determined. The 2.15% long term growth rate was determined by taking the average of the inflation rate, population growth rate, and GDP growth rate across the majority of the geographic regions in which Blackmores operates. These geographic regions include: Australia, Malaysia, Thailand, Singapore, Hong Kong, Taiwan, Korea and New Zealand. Given the nature of the business that BKL operates within, population growth rates were given greater consideration, as it is a more indicative metric when considering growth of the health supplement industry.

Intrinsic Value The intrinsic value/share for the DCF was calculated by first discounting back FCFF over the forecast horizon at the 7.80% WACC and then adding the present value of the terminal value to this number. This calculation of Blackmore’s enterprise value was then adjusted to arrive at the equity value. The intrinsic value/share was then calculated as the equity value divided by the shares outstanding. Intrinsic Value Calculation ($m) 12 months

Jun-‐30-‐2013 12 months Jun-‐30-‐2014

12 months Jun-‐30-‐2015

12 months Jun-‐30-‐2016

EBIT(1-‐T) $33.95 $36.66 $39.57 $42.34

D&A $6.69 $6.80 $6.92 $7.03

CapEx $6.17 $7.24 $7.31 $7.37

ΔNWC $15.53 $7.01 $7.41 $7.15

Free Cash Flow $18.94 $29.21 $31.77 $34.84

FCFF Growth 54.23% 8.77% 9.68%

Present Value of Free Cash Flows $17.57 $25.13 $25.36 $25.81

Total Present Value of All Free Cash Flows $247.95

Terminal Value $942.94

Present Value of Terminal Value $445.07

Enterprise Value $693.02

Less: Total Debt $86.00

Add: Cash & Cash Equivalents $11.96

Equity Value $618.98

Shares Outstanding (mn) 16.78

Intrinsic Value/Share $36.88 12 month Target Price (Rolled Forward) $38.33

CFA Institute Research Challenge 24.09.2012

36%

64%

Time Horizon

Terminal Value

Source: SURG Estimates

Source: SURG Estimates

Figure 23: Terminal value as a proportion of enterprise value

Table 14: Intrinsic Value Calculation

Sydney University Research Group 17

Appendix 4: Terminal Growth Rate We identify three critical factors that will determine the long-‐term growth prospects of Blackmores. Population growth, GDP growth and inflation will impact how Blackmores progresses into perpetuity due to their inherent links to the success of the business. By assuming a stable growth model, a terminal value growth rate was found by taking an average of and triangulating population, GDP and inflation rates from 2000 through 2011. These measures were analysed across the countries of Blackmores’ operations.

Population Growth Rates Population growth rate was considered as the primary driver of Blackmores’ long-‐term growth rate. As the company is linked to consumer demand, it is unable to grow at a rate greater than that of the population. This represents an upper bound for Blackmores’ growth and is subsequently given a triangulation weighting of 50%. A key aspect of the population growth rate is that it encompasses the aging and slowing population growth. With a greater proportion of populations aged over 65, Blackmores’ growth prospects will be largely influenced by an ability to provide goods to this segment.

Population Growth 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Average Australia 1.20% 1.35% 1.22% 1.22% 1.16% 1.32% 1.48% 1.52% 2.00% 2.09% 1.70% 1.40% 1.47% Malaysia 2.36% 2.32% 2.27% 2.20% 2.09% 1.97% 1.85% 1.73% 1.65% 1.61% 1.60% 1.58% 1.94% Thailand 1.19% 1.17% 1.16% 1.12% 1.05% 0.96% 0.86% 0.77% 0.69% 0.64% 0.60% 0.57% 0.90% Singapore 1.73% 2.70% 0.91% -1.48% 1.25% 2.35% 3.13% 4.17% 5.32% 3.02% 1.77% 0.82% 2.14% Hong Kong 0.88% 0.74% 0.44% -0.20% 0.78% 0.44% 0.64% 1.00% 0.75% 0.37% 0.91% 0.45% 0.60% Taiwan 0.81% 0.80% 0.78% 0.65% 0.64% 0.63% 0.61% 0.30% 0.24% 0.23% 0.21% 0.19% 0.51% Korea 0.84% 0.74% 0.56% 0.50% 0.38% 0.21% 0.33% 0.33% 0.31% 0.29% 0.26% 0.23% 0.42%

NZ 0.59% 0.59% 1.74% 1.97% 1.49% 1.13% 1.22% 1.04% 0.96% 1.09% 1.20% 0.88% 1.16%

Average Population Growth Rate 1.14%

GDP Growth Rates GDP growth rates are another factor impacting Blackmores’ long-‐term growth. Considering GDP provides a suitable proxy for the limit to long-‐term growth Blackmores can achieve into perpetuity. Averaging the GDP growth rates experienced by the countries of Blackmores’ operations reflects a relevant measure to which Blackmores can grow. Data was averaged from 2000 to 2011 and assigned a 25% weighting in the total growth rate calculation.

GDP Growth 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Average

Australia 4.00% 2.10% 3.90% 3.30% 4.20% 3.00% 3.10% 3.60% 3.80% 1.40% 2.30% 1.90% 3.05%

Malaysia 8.90% 0.50% 5.40% 5.80% 6.80% 5.30% 5.80% 6.50% 4.80% -‐1.60% 7.20% 3.70% 4.93%

Thailand 4.80% 2.20% 5.30% 7.10% 6.30% 4.60% 5.10% 5.00% 2.50% -‐2.30% 7.80% 1.80% 4.18%

Singapore 9.10% -‐1.20% 4.20% 4.60% 9.20% 7.40% 8.70% 8.80% 1.50% -‐0.80% 14.50% 4.90% 5.91%

Hong Kong 8.00% 0.50% 1.80% 3.00% 8.50% 7.10% 7.00% 6.40% 2.30% -‐2.70% 7.00% 2.60% 4.29%

Taiwan 4.92% -‐3.22% -‐4.60% 6.80% 2.56% 7.04% 3.83% 5.25% -‐7.31% 9.31% 5.67% 3.61% 2.82%

Korea 8.50% 4.00% 7.20% 2.80% 4.60% 4.00% 5.20% 5.10% 2.30% 0.30% 6.20% 3.10% 4.44%

NZ 2.60% 3.60% 4.90% 4.30% 3.80% 3.30% 0.80% 3.00% -‐1.50% -‐0.50% 0.23% 1.50% 2.17%

Average GDP Growth Rate 3.97%

CFA Institute Research Challenge 24.09.2012

Table 15: Historic Population Growth

Table 16: Historic GDP Growth

Source: IMF

Source: IMF

Sydney University Research Group 18

Inflation Rate Inflation rate is an important metric to include in the long-‐term growth rate as it provides a factor for adjusting nominal growth. It determines the real growth, which Blackmores can achieve. Utilising a method of averaging inflation rates across the countries of Blackmores’ operations accounts for inflationary distortions upon Blackmores’ long-‐term growth. In reflection of the weighting assigned to GDP growth, a 25% weighting was also applied to the inflation rate averages

Inflation Rate 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Average Australia 2.56% 4.38% 3.00% 2.77% 2.34% 2.67% 3.54% 2.33% 4.35% 1.82% 2.85% 3.42% 3.00% Malaysia 1.70% 1.50% 1.90% 1.10% 1.30% 3.00% 3.80% 4.30% 5.40% 0.60% 1.70% 2.20% 2.38% Thailand 2.10% 1.60% 0.60% 1.80% 2.80% 4.50% 5.10% 2.20% 5.50% -‐0.90% 3.30% 3.81% 2.70% Singapore 1.40% 1.50% -‐0.40% 0.50% 1.70% 0.40% 1.00% 2.10% 6.50% 0.60% 2.80% 5.20% 1.94% Hong Kong 3.70% -‐1.60% 3.00% -‐2.60% -‐0.30% 0.90% 2.20% 2.00% 4.30% -‐0.50% 4.50% 5.30% 1.74% Taiwan 1.30% 0.50% -‐0.20% -‐0.30% 1.70% 2.30% 1.00% 1.80% 3.50% -‐0.90% 1.00% 1.60% 1.11% Korea 2.30% 2.50% 2.80% 3.60% 3.60% 2.80% 2.20% 2.50% 4.70% 2.80% 3.00% 4.32% 3.09% NZ 2.40% 2.60% 2.70% 1.80% 2.40% 3.00% 3.80% 2.40% 4.00% 2.10% 2.60% 2.70% 2.71% Average Inflation Rate 2.33%

Triangulating Long-‐Term Growth To determine a final long-‐term growth rate, the average rates of population growth, GDP growth and inflation for Blackmores’ countries of operation were triangulated. Population growth average was assigned 50%, GDP growth 25% and inflation 25%. A long-‐term growth rate was computed to be 2.15%. This is an appropriate measure as it lies below consensus GDP growth making it a reasonable long-‐term growth rate for Blackmores.

Terminal Growth Rate Rate Triangulated Weight

Population Growth 1.14% 0.5 Economic Growth (GDP) 3.97% 0.25 Inflation 2.33% 0.25 Terminal Growth Rate 2.15%

CFA Institute Research Challenge 24.09.2012

Table 17: Historic Inflation Rate

Table 18: Terminal Growth Triangulation

Source: IMF

Source: IMF; SURG Estimates

Sydney University Research Group 19

Appendix 5: Multiples Analysis

Appendix 6: Sum Of The Parts Analysis

Relative Valuation Asia Company Name/Exchange/Ticker EV/EBITDA P/E CCM Duopharma Biotech Berhad (KLSE: CCMDIO) 7.7 12.1 China Nuokang Bio-‐Pharmaceutical Inc. (NasdaqGM:NKBP) 12.3 25.4 Estechpharma Co. Ltd. (KOSE: A041910) 10.0 14.9 Eu Yan Sang International Ltd. (SGX:E02) 10.6 14.4 Goangdong Taiantang Pharmaceutical Co. Ltd 21.4 29.3 Ilsung Pharmaceuticals Co. Ltd. (KOSE: A003120) 18.3 2.7 Sinphar Pharmaceutical Co. Ltd. 21.4 41.9 Shanghai No 1 Pharmacy Co (SHSE:600833) 28.0

44.0

Median 15.30

20.13

Company Name/Exchange/Ticker EV/EBITDA P/E Amway Malaysia Holdings Ltd. (KLSE:AMWAY) 12.4 18.3 Australian Pharmaceutical Industries Limited (ASX:API) 4.9 8.2 Balchem Corp. (NasdaqGS:BCPC) 14.1 25.4 Cerebos Pacific Limited (SGX:C20) 8.5 -‐ EBOS Group Ltd. (NZSE: EBO) 14.2 12.5 Glenmark Pharmaceuticals Ltd. (BSE: 532296) 18.2 18.2 Raffles Medical Group Ltd. (SGX:R01) 8.7 23.6 Schiff Nutrition International Inc. (NYSE:SHF) 6.1 24.1 Sigma Pharmaceuticals Ltd. (ASX:SIP) 13.9 14.9 USANA Health Sciences Inc. (NYSE:USNA) 12.4 9.7 Vitamin Shoppe, Inc. (NYSE:VSI) 4.9 24.1 Median 12.4 18.3

Blackmores EV/EBITDA P/E Calendarised EBITDA NTM 56.11 Calendarised NPAT NTM 32.10

EV 695.72 Less: Net Debt 63.74 Equity Value 631.98 587.40

SOI 16.78 16.78 Equity Value per Share $37.66 $35.00

Average Value per Share $36.33

Blackmores EV/EBITDA P/E Calendarised EBITDA

LTM 10.19

Calendarised NPAT NTM 5.83 EV 155.89

Less: Net Debt 15.39 Equity Value 140.50 117.18

SOI 16.78 16.78 Equity Value per Share $8.37 $6.98

Average Value per Share $7.68

CFA Institute Research Challenge 24.09.2012 CFA Institute Research Challenge 24.09.2012

Table 19: Comparables’ Multiples

Table 20: Blackmores Implied Value

Table 21: Asian Comparables’ Multiples

Table 22: Blackmores Implied Value

Source: Capital IQ

Source: Capital IQ; SURG Estimates

Source: Capital IQ

Source: Capital IQ; SURG Estimates

Sydney University Research Group 20

Source: Capital IQ

Australia and NZ Company Name/Exchange/Ticker EV/EBITDA P/E AnsellLtd. (ASX:ANN) 12.0 14.8 Australian Pharmaceutical Industries Limited (ASX:API) 6.4 9.5 Coca-‐Cola Amatil Limited (ASX:CCL) 13.9 17.3 CSL Ltd. (ASX:CSL) 15.4 19.3 Domino's Pizza Enterprises (ASX:DMP) 16.2 22.0 Metcash Limited (ASX:MTS) 8.5 11.2 Ramsay Healthcare (ASX:RHC) 10.8 20.8 Sigma Pharmaceuticals Ltd. (ASX:SIP) 9.7 14.6 Treasury Wine Estates (ASX:TWE) 12.5 20.9 Sonic Healthcare Ltd. (ASX: SHL) 10.8 15.4 Median 11.40 16.32 Multiples Assumptions and Findings Calendarisation – The EBITDA and NPAT figures were calculated as at 23/09/12 to account for both FY13F estimates by SURG and the reported figures for FY12A. Use of Median – The median was utilised as it removed the noise of potential outliers in the comparable company set. It provides a truer depiction of the multiple values. Consolidated Entity Valuation – Both NTM EV/EBITDA and NTM P/E ratios were considered with a 50% weighting each towards the relative valuation. A 12.4x NTM EBITDA multiple based on the median of comparable companies was used. An 18.3x NTM P/E multiple based on the median of comparable companies was used. Sum-‐of-‐the-‐Parts Valuation – The sum-‐of-‐the-‐parts relative valuation was used a method to determine the level of value divided between Asian operations and Australian operations. This was not included in the final relative valuation. As a substantial level of Blackmores’ value is realised when operating as a whole, incorporating a sum-‐of-‐the-‐parts relative valuation significantly deteriorates the value of Blackmores’. The company’s distinctiveness regarding market position, brand equity, broad operations and geographic exposure is undermined when considering sum-‐of-‐the-‐parts as true value cannot be accurately reflected. The LTM EV/EBITDA multiple was used and a calendarised EBITDA LTM figure. For Asia the operations a price of $8.37 was determined and for Australian/NZ operations a price of $22.88 was found. This combined provides a share price of $31.25. Utilising the NTM P/E multiple and a NTM NPAT calendarised figure, Asian operations were valued at $6.98 and Australian/NZ operations were valued at $24.70. This produces a combined share price of $31.68. Asian Operations – A LTM EV/EBITDA median multiple of 15.3x was applied. A NTM P/E median multiple of 20.1x was applied.. Australian/NZ Operations – A LTM EV/EBITDA median multiple of 11.4x was applied. A NTM P/E median multiple of 16.3 was applied.

Blackmores EV/EBITDA P/E Calendarised EBITDA LTM 38.82 Calendarised NPAT NTM 25.43

EV 442.56 Less: Net Debt 58.65 Equity Value 383.91 414.45

SOI 16.78 16.78 Equity Value per Share $22.88 $24.70

Average Value per Share $23.79

CFA Institute Research Challenge 24.09.2012

Table 24: Blackmores Implied Value Table 23: Australian/NZ Comparables’ Multiples

Source: Capital IQ

Source: Capital IQ; SURG Estimates

Sydney University Research Group 21

Appendix 7: Monte Carlo Simulation A Monte Carlo Simulation was performed with 100,000 trials, assigning a normal distribution to each geographic area revenue growth rate for Blackmores in addition to the recently acquired FIT-‐BioCeuticals division. The standard deviation of each distribution is computed on the expected magnitude of risk associated with the respective business area. Reported below are the assumptions underlying our simulation. Modelled Entity STDEV (%) Comments Australian Revenue 1.5 Normal Distribution Thailand Revenue 4 Normal Distribution Malaysian Revenue 4 Normal Distribution Other Asian Revenue 5.5 Normal Distribution New Zealand Revenue 1.5 Normal Distribution Other Revenue 1.5 Normal Distribution Corporate Revenue 1.5 Normal Distribution

Simulation Statistics Number of Trials 100,000 Mean $38.34 Median $38.31 Standard Deviation $1.45 Variance $2.11 Skewness 0.1007 Kurtosis 3.03 Coeff. Of Variability 0.0379 Minimum $32.08 Maximum $45.43

CFA Institute Research Challenge 24.09.2012

Table 25: Monte Carlo Inputs

Table 26: Monte Carlo Simulation Statistics

Figure 24: Monte Carlo Frequency Distribution

Source: SURG Estimates

Source: SURG Estimates

Source: SURG Estimates

Sydney University Research Group 22

Appendix 8: Target Price Sensitivity Analysis (DCF)

Triangulation DCF Consolidated Multiples Price 50.00% 50.00% $37.33

60.00% 40.00% $37.53

70.00% 30.00% $37.73 80.00% 20.00% $37.93

Cost of Equity

$37.73 4.36% 4.86% 5.36% 5.86% 6.36%

Cost of

Debt

8.01% $44.18 $43.50 $42.83 $42.19 $41.57

8.51% $41.26 $40.67 $40.10 $39.54 $39.00

9.01% $38.75 $38.23 $37.73 $37.25 $36.77

9.51% $36.57 $36.11 $35.67 $35.24 $34.82

10.01% $34.66 $34.25 $33.86 $33.47 $33.10

Terminal Growth

$37.73 1.15% 1.65% 2.15% 2.75% 3.25%

WACC

6.80% $39.80 $42.01 $44.69 $48.79 $53.27

7.30% $36.96 $38.75 $40.87 $44.05 $47.41

7.80% $34.56 $36.02 $37.73 $40.24 $42.84

8.30% $32.49 $33.70 $35.10 $37.13 $39.18

8.80% $30.69 $31.71 $32.87 $34.53 $36.18

Source: SURG Estimates

Source: SURG Estimates

Source: SURG Estimates

Table 27: Target price sensitivity to cost of equity and cost of debt

Table 28: Target price sensitivity to terminal growth rate and WACC

Table 29: Scenario Manager for Valuation Method Weightings

CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 23

Appendix 9: Target Price Sensitivity Analysis (Multiples)

EV/EBITDA

$37.66 11.86 12.13 12.4 12.67 12.95

Equity Value

(AUDm)

600.38 $35.78 $35.78 $35.78 $35.78 $35.78

616.18 $36.72 $36.72 $36.72 $36.72 $36.72

631.98 $37.66 $37.66 $37.66 $37.66 $37.66

647.78 $38.60 $38.60 $38.60 $38.60 $38.60

663.58 $39.55 $39.55 $39.55 $39.55 $39.55

P/E

$30.46 17.11 17.68 18.3 18.84 19.44

Equity Value

(AUDm)

558.03 $33.26 $33.26 $33.26 $33.26 $33.26

572.72 $34.13 $34.13 $34.13 $34.13 $34.13

587.40 $35.01 $35.01 $35.01 $35.01 $35.01

602.09 $35.88 $35.88 $35.88 $35.88 $35.88

616.77 $36.76 $36.76 $36.76 $36.76 $36.76

CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 24

Table 30: Price sensitivity to Equity Value and EV/EBITDA multiple

Table 31: Price sensitivity to Equity Value and P/E

Source: SURG Estimates

Source: SURG Estimates

Appendix 10: FIT-‐BioCeuticals Organic growth through FIT-‐BioCeuticals Business Overview FIT-‐BioCeuticals is an Australian based nutraceutical company with offices in Australia, New Zealand and the US, operating in the traditional naturopath, pharmacist, direct-‐to-‐consumer channel and the health food store channel. Within the traditional naturopath, pharmacist and health food store channel FIT-‐BioCeuticals has four key brands, BIOCeuticals (vitamins and supplements), Hall Drug Technologies (prescriptive drug range), IsoWhey (weight-‐loss range) and BioEngineered (sports/performance range). FIT-‐BioCeuticals main product lines include its BIOCeuticals and IsoWhey. BIOCeutical products are high efficacy neutraceuticals aimed at the symptoms of deficiencies, imbalances and toxicities, whilst IsoWhey products are a high protein, low carb, low fat meal replacement system with protein shakes, snack bars, vitamin supplemented snack bars and confectionary substitutes. Strategic Fit of FIT-‐BioCeuticals Channel Diversification FIT-‐BioCeuticals leads the market within the practitioner channel for its product category. The company was first to be accepted as a member of Medicines Australia out of Australia’s nutraceutical companies. Thus, the acquisition gives Blackmores’ a foothold in the practitioner channel and the opportunity to leverage existing relationships from both businesses into developing, marketing and selling new products. Increased product offering FIT-‐BioCeuticals’ large portfolio of products both complement and supplement BKL’s current product offerings. For example, the acquisition will add to BKL a range of weight loss supplement products, which are currently sold both direct to the consumer and through the traditional pharmacy and health food channels. Potential sourcing and R&D synergies There is a high level of commonality between the base components of both Blackmores and FIT-‐BioCeuticals product portfolios, including research, development and marketing of products. Therefore, there is an opportunity for a sharing of sourcing for key ingredients, research and development costs. However, with the intention of FIT-‐BioCeuticals remaining as a standalone company, these synergies are limited in the short to medium term. Increased experience and knowledge FIT-‐BioCeuticals, combined with Blackmores, will provide an unparalleled depth of expertise with over 100 doctors, naturopaths and pharmacists. This reinforces Blackmores position Australia’s largest natural health company and their position as market leader. EPS accretion The deal is estimated to be approximately 5% EPS accretive from an estimated $2.0 million increase in NPAT for FY13. This is driven by revenue growth within the broader VDS market, along with continued product investment delivering slight increases in margins.

CFA Institute Research Challenge 24.09.2012

Sydney University Research Group 25

Disclosures: Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue. Position as a officer or director:

The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject company. Market making:

The author(s) does not act as a market maker in the subject company’s securities. Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with CFA Society Sydney, CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.

CFA Institute Research Challenge