certification of appraisal -...

TRANSCRIPT

CERTIFICATION OF APPRAISAL

Each person signing below certifies to the best of their personal knowledge and belief:

1. The statements of fact contained in this report are true and correct.

2. The reported analyses, opinions, and conclusions are limited only by the reported

assumptions and limiting conditions, and are our personal, impartial, and unbiased

professional analyses, opinions, and conclusions.

3. We have no present or prospective interest in the property that is the subject of this report,

and no personal interest with respect to the parties involved.

4. We have no bias with respect to the property that is the subject of this report or to the parties

involved with this assignment.

5. The engagement for this assignment was not contingent upon developing or reporting

predetermined results.

6. Our compensation for completing this assignment is not contingent upon the development or

reporting of a predetermined value or direction in value that favors the cause of the client, the

amount of the value opinion, the attainment of a stipulated result, or the occurrence of a

subsequent event directly related to the intended use of this appraisal.

7. The reported analyses, opinions, and conclusions were developed, and this report has been

prepared, in conformity with the requirements of the Code of Professional Ethics & Standards

of Professional Appraisal Practice of the Appraisal Institute, which include the Uniform

Standards of Professional Appraisal Practice.

8. Adam Zimmerman has made a personal inspection of the property that is the subject of this

report.

9. No one has provided significant real property appraisal assistance to the person(s) signing

this report.

10. We have experience in appraising properties similar to the subject and are in compliance with

the Competency Rule of USPAP.

11. The appraiser(s) has not provided any appraisal related services at the subject property

during the previously 36 months.

12. The use of this report is subject to the requirements of the Appraisal Institute relating to review

by its duly authorized representatives.

13. As of the date of this report, Adam Zimmerman has completed the standards and ethics

requirements for candidates of designation of the Appraisal Institute.

14. The appraisal assignment was not based on a requested minimum value, a specific valuation,

or the approval of a loan.

HILCO REAL ESTATE APPRAISAL, LLC

Adam Zimmerman

Vice President

MS Certified General Appraiser #TG-3679

AERIAL PHOTO

EXECUTIVE SUMMARY Location: The site is located at 7276 Casino Strip Resort Blvd. in

Robinson, Tunica County County, MSA 38664.

Property Description: The subject property is considered a limited service hotel,

operating under the Days Inn brand. The property offers 66

guestrooms and was built in 1994. The subject site is comprised

of one, 1.50-acre parcel.

Assessor’s Parcel Number(s): 3104180000000100

Interest Appraised: Fee Simple, Going Concern

Date of Value(s): January 23, 2018

Date of Inspection: January 29, 2018

Ownership:

Jasveer S Brar

Highest and Best Use Opinion

If Vacant: Future Hotel or Commercial development

As Improved: Current use as a hotel

Site & Improvements

Zoning: None, Tunica County

Land Area: 1.50 acres – Assessor’s Parcel Map

Number of Stories: 2

Year Built: 1994

Type of Construction: Masonry: 2 story hotel

Gross Building Area: 35,720 SF

Number of Rooms: 66 rooms

Amenities: Breakfast room

Parking:

84 spaces

EXECUTIVE SUMMARY

EXTRAORDINARY ASSUMPTIONS & HYPOTHETICAL CONDITIONS

The value conclusion is subject to the general assumptions and limiting conditions and certifications. In

addition, the following extraordinary assumptions and hypothetical conditions, if any, are summarized

below, which might affect the assignment results. Any changes from these assumptions may affect market

value and we reserve the right to revise our analysis. Use of these extraordinary assumptions may have

affected the assignment results.

Extraordinary Assumptions

The square footages of the building area and other information such as parking count were obtained from

the Harris County Records and assumed accurate. We reserve the right to amend our value conclusion if

these assumptions are later proven incorrect.

It is our understanding that the subject is currently in violation of its franchise agreement and has been

removed from the Choice Hotel's web site. We also understand that the subject needs a PIP (Property

Improvement Plan) to remove it from non-performing status. We do not know the PIP amount, but estimate

it could exceed $500,000, given the subject's below brand standards. We recommend a review of any PIP

information provided by Choice Hotels.

We were not provided signicant financials. We estimated the subject's ADR and Occupancy by using

market based data such as an STR Trend report. We did present an Income Capitalization Analysis

(ERRM) as a general valuation tool, but projecting ADR, Occupancy, Rev Par and operating expenses

as well as selecting discount rates and cap rates without knowing any current or historical operating

income and expenses, any required capital expenditures, or understanding the franchise agreement is

highly speculative. We assume the subject is underperforming based on its market share, but we are

uncertain as to the amount of capital needed (without understanding financials, condition and spending

requirements) to stabilize the hotel. We were unable to complete a reliable penetration analysis. If full

recent financials become available, we reserve the right to modify our analysis.

We assume the property is and will continue to be managed by a competent management group, typically

provided for similar hotels.

We estimated (by allocation) the value of the FF&E. We do not know the current condition of the FF&E

(Case and soft goods) and have estimated depreciation based on similar aged hotel valuations we have

completed.

Hypothetical Conditions

None

TABLE OF CONTENTS

INDTRODUCTION ................................................................................................................. 1

REGIONAL ANALYSIS .......................................................................................................... 5

NEIGHBORHOOD ANALYSIS ............................................................................................... 8

SITE DESCRIPTION ........................................................................................................... 14

IMPROVEMENTS DESCRIPTION ...................................................................................... 16

REAL ESTATE TAXES ........................................................................................................ 21

ZONING ............................................................................................................................... 21

HOTEL MARKET ANALYSIS ............................................................................................... 22

HIGHEST AND BEST USE .................................................................................................. 31

VALUATION PROCESS ...................................................................................................... 33

INCOME CAPITALIZATION APPROACH............................................................................ 36

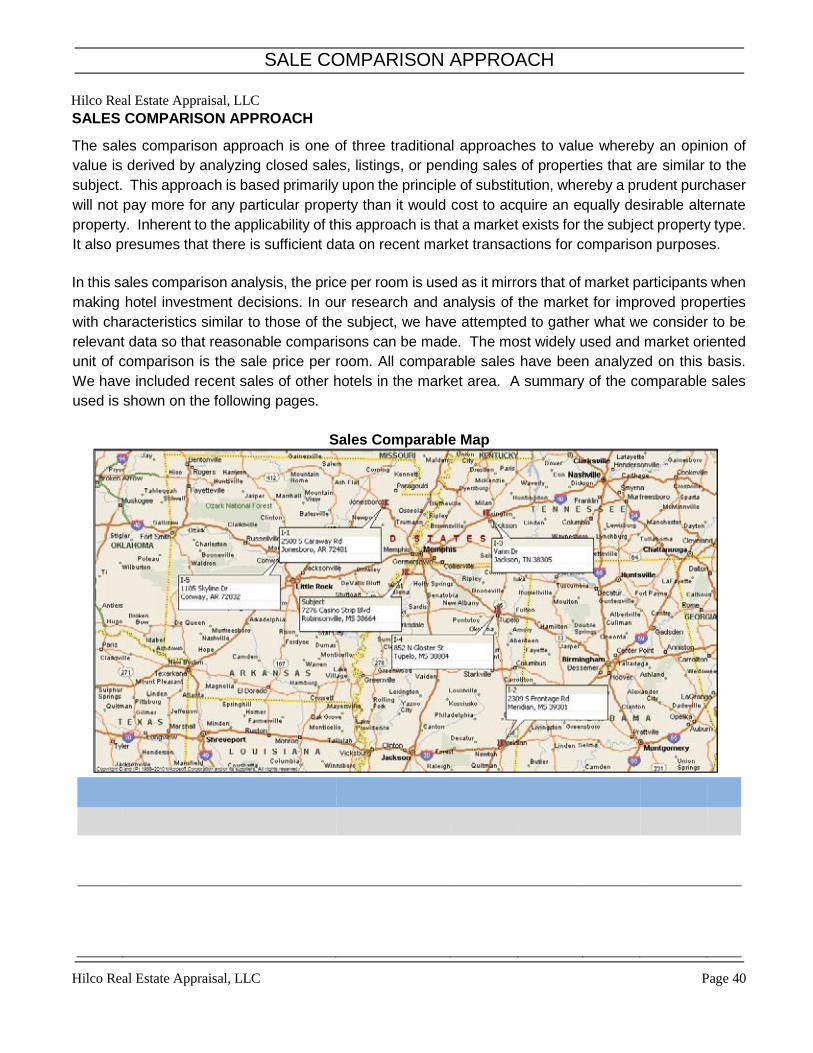

SALES COMPARISON APPROACH ................................................................................... 40

RECONCILIATION AND FINAL VALUE OPINION .............................................................. 46

ASSUMPTIONS AND LIMITING CONDITIONS .................................................................. 49

ADDENDA ITEMS

INTRODUCTION

Hilco Real Estate Appraisal, LLC Page 1

INDTRODUCTION Identification of Subject Property

Property Description: The subject property is a limited-service Days Inn hotel that opened in

1994 as a Knights Inn and was converted to a Days Inn in 2008. The

property features 66 rooms. The hotel offers complimentary hot

breakfast. Situated on a 1.50 acre site, the property is located in the

Tunica Resort Hotel Market.

Address: 7276 Casino Strip Resort Blvd., Robinson,

Tunica County County, MSA, 38664

Assessor’s Parcel No.: 3104180000000100

Description of Property Interest Appraised

Interest Appraised: Fee Simple, Going Concern Interest

Property Ownership and Three Years Sales History

Current Ownership:

Management/Franchise

Agreements:

Sale History:

The subject is currently owned by Jasveer S Brar

The subject is franchised under the Days Inn brand. We were not

provided a copy of the franchise agreement. The subject may be in

violation of the agreement.

There have been no other transactions that we are aware of in the last

three years. In addition, to the best of our knowledge, the property is not

currently on the market for sale.

Intended Use and Users of the Appraisal

This appraisal is to be used by the Client, Three River Planning & Development District, for mortgage

lending purposes. The intended user(s) is Three River Planning & Development District. All others

reading or relying on this appraisal report are considered unintended users of this appraisal. The

appraisal cannot be used for any other reason including appealing tax assessments, litigation, settling

an estate, etc. Should anyone other than the client read or rely on this report, no fiduciary obligation is

owed by the appraisers to that party. Any additional work will be billed at an hourly rate, for expert

witness testimony, preparation for testimony, and any other work deemed necessary.

INTRODUCTION

Hilco Real Estate Appraisal, LLC Page 2

Dates of Inspection and Valuation

The value conclusion reported herein is as of January 23, 2018, corresponding with the date of

inspection, January 29, 2018, by Adam Zimmerman.

Property Rights Appraised

Per our agreement for services, we are appraising the Fee Simple, Going Concern interest.

The following definition is from the Dictionary of Real Estate Appraisal, Sixth Edition (2015), published

by the Appraisal Institute.

Fee Simple Interest: Absolute ownership unencumbered by any other interest or estate, subject only to

the limitations imposed by the governmental powers of taxation, eminent domain, police power, and

escheat.

With respect to the subject property, the property rights valued include all items of personal property,

including furniture, fixtures, and equipment, and licenses and agreements required to operate the

property and related facilities. The “business assets” or business component is an integrated constituent

of value and includes “tangible and intangible resources that are employed by a business enterprise in

its operations.”

Scope of the Appraisal

The scope of an appraisal is defined as “the amount and type of information researched and the analysis

applied in an assignment” (USPAP). The scope of this assignment involves:

• Research and analysis sufficient to form a credible opinion of value,

• Presentation of our research, analysis and final opinions in a report format.

In fulfillment of our agreement for services and the professional requirements noted below, our appraised

value is based on a combination of primary and secondary data research. The depth of our research

and analysis is based on the significance of each issue to the appraisal. The results of our research

and analysis are described throughout the following report. In summary, during the course of this

assignment, we:

• Requested subject property information and reviewed the information that was made available

to us. Researched public source and vendor service based subject information. Conducted an

appraisal inspection of the subject property, made field notes and took photographs.

• Drove the subject’s local area to assess development trends, transportation patterns, quality and

condition of improvements, access to services, adverse influences, etc.

• Gathered published information on key economic, social, governmental and environmental

factors in the region and local area that influence the subject’s value.

• Researched the subject’s zoning designation and key development restrictions.

• Formed an opinion of the subject’s Highest and Best Use, and determined which approaches to

value were applicable and/or necessary.

INTRODUCTION

Hilco Real Estate Appraisal, LLC Page 3

• Investigated and selected the most relevant and reliable improved sales for use in the Sales

Comparison Approach.

• Investigated and selected the most relevant and reliable rent comparables, expense data and

investment rates for use in the Income Capitalization Approach.

• Considered the input gathered from our interviews of buyers, sellers, brokers, property

developers and public officials, as applicable in each approach. Concluded a final opinion of

value after reconciling the indications from the approaches employed.

Additionally, this appraisal assignment was prepared to conform to the applicable professional

requirements set forth under:

• The most recent edition of the Uniform Standards of Professional Appraisal Practice (USPAP).

• The current Code of Professional Ethics of the Appraisal Institute

• The Financial Institutions Reform, Recovery and Enforcement Act of 1989 (FIRREA), Title XI

Regulations.

• Three River Planning & Development District’s guidelines and required scope of work.

Definition of Market Value

The most probable price which a property should bring in a competitive and open market

under all conditions requisite to a fair sale, the buyer and seller, each acting prudently and

knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this

definition is the consummation of a sale as of a specified date and the passing of title from

seller to buyer under conditions whereby:

1. Buyer and seller are typically motivated;

2. Both parties are well informed or well advised, and acting in what they consider their own best

interest;

3. A reasonable time is allowed for exposure in the open market;

4. Payment is made in terms of cash in US dollars or in terms of financial arrangements

comparable thereto; and

5. The price represents the normal consideration for the property sold unaffected by special or

creative financing or sales concessions granted by anyone associated with the sale.1

Definitions of Other Key Terms

Definitions of key appraisal terms are included in the glossary in the addenda.

Significant Appraisal Assistance or Contribution

No other individuals have provided significant real property appraisal assistance to the persons signing

this report in the form of property inspection, research and general report preparation.

1 Source: OCC, 12 CFR Part 34, Subpart C-Appraisals, 34.42 Definitions (g)

INTRODUCTION

Hilco Real Estate Appraisal, LLC Page 4

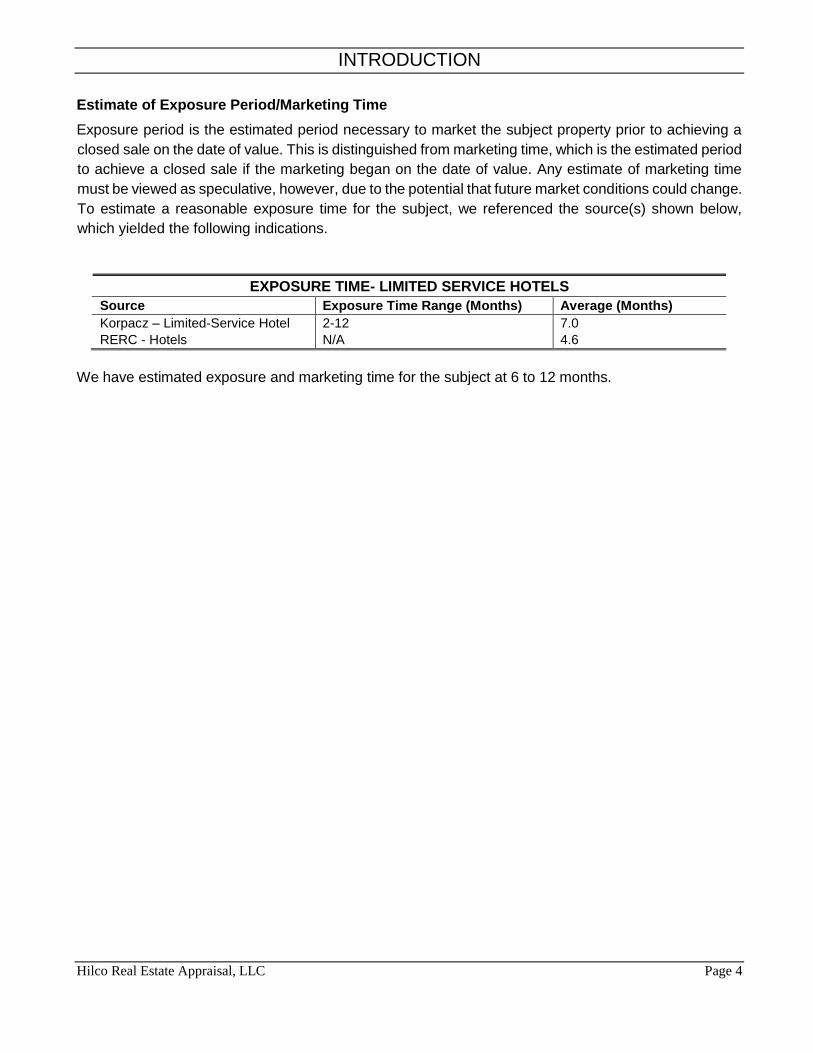

Estimate of Exposure Period/Marketing Time

Exposure period is the estimated period necessary to market the subject property prior to achieving a

closed sale on the date of value. This is distinguished from marketing time, which is the estimated period

to achieve a closed sale if the marketing began on the date of value. Any estimate of marketing time

must be viewed as speculative, however, due to the potential that future market conditions could change.

To estimate a reasonable exposure time for the subject, we referenced the source(s) shown below,

which yielded the following indications.

EXPOSURE TIME- LIMITED SERVICE HOTELS

Source Exposure Time Range (Months) Average (Months)

Korpacz – Limited-Service Hotel

RERC - Hotels 2-12 N/A

7.0 4.6

We have estimated exposure and marketing time for the subject at 6 to 12 months.

Hilco Real Estate Appraisal, LLC Page 5

REGIONAL ANALYSIS

The Memphis–Forrest City Combined Statistical Area, TN–MS–AR (CSA) is the commercial and cultural

hub of The Mid-South or Ark-Miss-Tenn. The census defined combined statistical area covers ten

counties in three states – Tennessee, Mississippi, and Arkansas. As of census 2010 the MSA had a

population of 1,324,108. The Forrest City Micropolitan area was added to the Memphis area in 2012 to

form the Memphis–Forrest City Combined Statistical area and had a population of 1,369,548 according

to census estimates. The greater Mid-South area as a whole has a population of 2.4 million according

to 2013 census estimates. This area is covered by Memphis local news channels and includes the

Missouri Bootheel, Northeast Arkansas, West Tennessee, and North Mississippi

RELATIVE EMPLOYMENT PERFORMANCE (JAN 2007=100)

REGIONAL ANALYSIS

Regional Map

MOODY’S ANALYTICS / Précis® U.S. Metro / December 2017

MOODY'S ANALYTICS / Book / Copyright © 2018, Moody's Analytics, Inc. All Rights Reserved.

UNITED STATES

14

EMPLOYMENT GROWTH RATE

2016-2018 2016-2021

1.4%

0.9%

GROSS DOMESTIC PRODUCT

2016-2018 2016-2021

2.6% 2.1% Source: Moody’s Analytics

STRENGTHS & WEAKNESSES ANALYSIS STRENGTHS

» Very productive workforce. » Labor market attracts skilled and unskilled

immigrants. » High innovation and entrepreneurship. » Mobile labor force, flexible labor system.

WEAKNESSES » Many labor market nonparticipants. » Large budget, current account deficits. » Skewed income and wealth

distribution. » Polarized and fractured

political system.

The sweeping changes to the tax code negoti- cause insurance premiums to increase, knocking ated by the Trump administration and Republi- 13 million off insurance rolls. Also, the expiracan Congress will significantly impact the near- tion of the individual tax cuts in 2025 results in a term economic outlook. The $1.5 trillion, 10-year higher tax liability for the two-thirds of taxpayers tax cut will juice-up growth through the remain- making less than $75,000 a year. der of this decade, but will result in meaningfully Individuals in high-tax states in the Northeast weaker growth at the start of the next decade. and California are also at risk of paying more Longer run, the cuts will add little to the econo- in taxes as the legislation scales back the demy but will add significantly to the government’s ductions for state and local income, sales, and deficits and debt load. property taxes. This is even more likely for home-

Winners and losers. Businesses are the owners in these areas who have large mortgages, biggest winners of the tax cuts. Larger C-corpo- since the legislation limits the mortgage interest rations are the beneficiaries of $650 billion in tax deduction to mortgage debt less than $750,000. cuts over the next decade, as their top marginal Overheating threat. The deficit-financed rate is permanently reduced from 35% to 21% tax cuts will act like fiscal stimulus, temporarily (see Chart 1). Cash-rich multinational firms en- pumping up growth. Based on simulations of the joy a much lower tax rate on earnings repatri- Moody’s Analytics macro model, the tax legislaated from overseas and the move from a global tion will lift real GDP growth by 0.4 percentage taxation system to a territorial one. Smaller S- point in 2018 and 0.2 percentage point in 2019. corporations and other pass-through entities Without tax cuts, the economy was set to grow will enjoy a lower marginal rate, giving them a by 2.5% per annum through the remainder of $250 billion tax break through 2025 when this the decade, but with the cuts, growth will be cut expires along with the rest of the tax cuts 2.9% per annum.

for individuals. The problem is that the economy is arguably High-income and wealthy households are also already operating beyond full employment.

The winners. Of the $1.1 trillion in tax cuts going to in- unemployment rate is just over 4%, well below dividuals over the next decade, more than three- most estimates of the full-employment unemquarters goes to taxpayers who make more than ployment rate, including the Moody’s Analytics $200,000 a year in taxable income. For context, estimate of 4.5% (see Chart 2). Even without this group accounts for just over one-twentieth tax cuts, unemployment was set to fall below of all taxpayers. Wealthy households also benefit 4%, but with them it could fall into the low-3% from a doubling of the estate tax exemption, and range. a rarefied group of private equity managers will Wage and price pressures have been largely continue to benefit from the special tax treat- dormant, but this will not last, and the Federal ment of carried interest. Reserve will have little choice but to normal-

Lower-income taxpayers struggling to hold on ize monetary policy more aggressively. Fed to their health insurance will likely be hurt. They policymakers are currently anticipating three benefit from the doubling of the standard deduc- 0.25-point rate hikes in 2018 and about the tion under the law. But the legislation ends the same in 2019, but four rate hikes each year now individual mandate for health insurance, which seems more likely.

the Congressional Budget Office concludes will (Continued next page)

CURRENT EMPLOYMENT TRENDS % CHANGE YR AGO, 3-MO MA

Nov 16 May 17 Nov 17 Total 1.7

1.5 1.4 Construction 3.2 2.6 2.8 Manufacturing -0.2 0.4 1.3 Trade 1.2 0.4 0.1 Trans/Utilities 1.8 1.6 1.7 Information 0.6 -1.3 -2.5 Financial Activities 2.1 2.1 1.8 Prof & Business Svcs. 2.8 3.2 2.7 Edu & Health Svcs. 2.6 2.3 2.0 Leisure & Hospitality 2.5 2.0 1.7 Other Services 1.5 1.1 1.3 Government 1.1 0.7 0.1

FORECAST RISKS

SHORT TERM LONG TERM UPSIDE

» Low energy prices and rising wages act as tailwinds for consumer spending.

» Long-term interest rates remain low for much longer, fueling housing’s recovery and spurring more business investment.

DOWNSIDE » Weak global demand and high dollar detract from

exports longer than expected. » Household formation remains subdued, hurting

the housing recovery.

MOODY’S

RATING Aaa

2011 2012 2013 2014 2015 2016 INDICATORS 2017 2018 2019 2020 2021 2022 15,021 15,355 15,612 16,013 16,472 16,716 Gross domestic product (C09$ bil) 17,098 17,585 17,966 18,145 18,588 19,059

1.6 2.2 1.7 2.6 2.9 1.5 % change 2.3 2.8 2.2 1.0 2.4 2.5

MOODY’S ANALYTICS / Précis® U.S. Metro / December 2017

MOODY'S ANALYTICS / Book / Copyright © 2018, Moody's Analytics, Inc. All Rights Reserved.

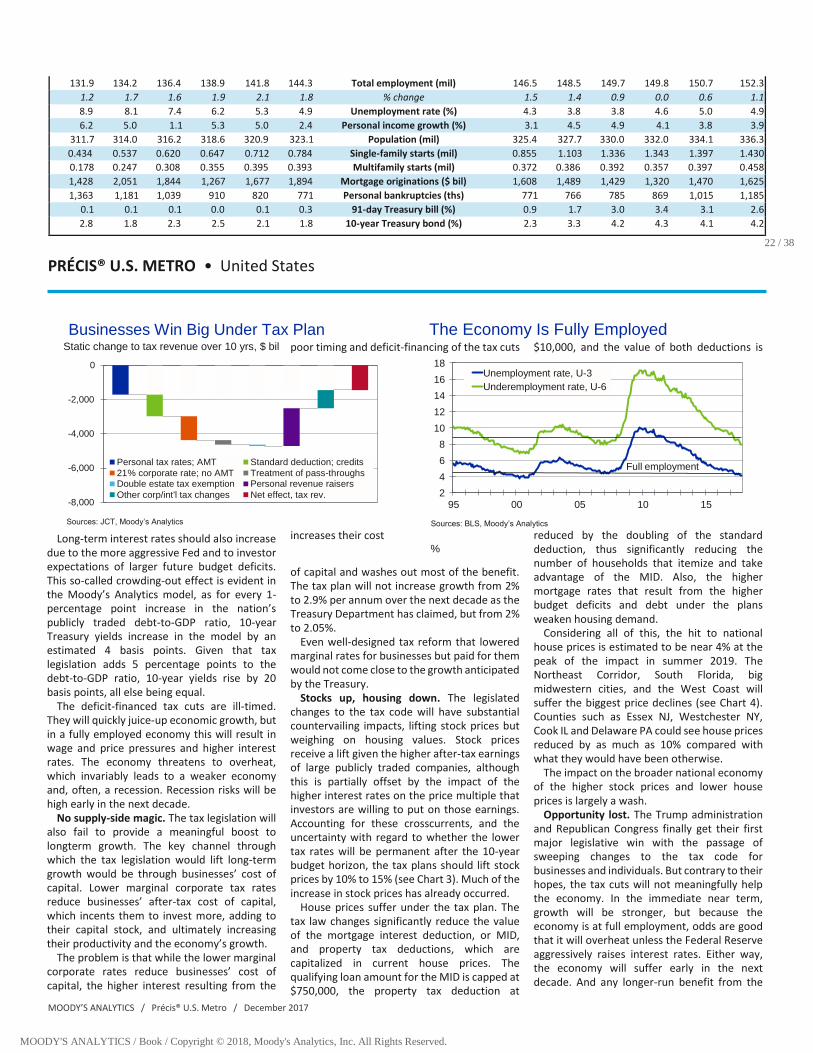

131.9 134.2 136.4 138.9 141.8 144.3 Total employment (mil) 146.5 148.5 149.7 149.8 150.7 152.3 1.2 1.7 1.6 1.9 2.1 1.8 % change 1.5 1.4 0.9 0.0 0.6 1.1 8.9 8.1 7.4 6.2 5.3 4.9 Unemployment rate (%) 4.3 3.8 3.8 4.6 5.0 4.9 6.2 5.0 1.1 5.3 5.0 2.4 Personal income growth (%) 3.1 4.5 4.9 4.1 3.8 3.9 311.7 314.0 316.2 318.6 320.9 323.1 Population (mil) 325.4 327.7 330.0 332.0 334.1 336.3 0.434 0.537 0.620 0.647 0.712 0.784 Single-family starts (mil) 0.855 1.103 1.336 1.343 1.397 1.430 0.178 0.247 0.308 0.355 0.395 0.393 Multifamily starts (mil) 0.372 0.386 0.392 0.357 0.397 0.458 1,428 2,051 1,844 1,267 1,677 1,894 Mortgage originations ($ bil) 1,608 1,489 1,429 1,320 1,470 1,625 1,363 1,181 1,039 910 820 771 Personal bankruptcies (ths) 771 766 785 869 1,015 1,185 0.1 0.1 0.1 0.0 0.1 0.3 91-day Treasury bill (%) 0.9 1.7 3.0 3.4 3.1 2.6 2.8 1.8 2.3 2.5 2.1 1.8 10-year Treasury bond (%) 2.3 3.3 4.2 4.3 4.1 4.2

22 / 38

PRÉCIS® U.S. METRO • United States

Businesses Win Big Under Tax Plan The Economy Is Fully Employed Static change to tax revenue over 10 yrs, $ bil

Long-term interest rates should also increase due to the more aggressive Fed and to investor expectations of larger future budget deficits. This so-called crowding-out effect is evident in the Moody’s Analytics model, as for every 1-percentage point increase in the nation’s publicly traded debt-to-GDP ratio, 10-year Treasury yields increase in the model by an estimated 4 basis points. Given that tax legislation adds 5 percentage points to the debt-to-GDP ratio, 10-year yields rise by 20 basis points, all else being equal.

The deficit-financed tax cuts are ill-timed. They will quickly juice-up economic growth, but in a fully employed economy this will result in wage and price pressures and higher interest rates. The economy threatens to overheat, which invariably leads to a weaker economy and, often, a recession. Recession risks will be high early in the next decade.

No supply-side magic. The tax legislation will also fail to provide a meaningful boost to longterm growth. The key channel through which the tax legislation would lift long-term growth would be through businesses’ cost of capital. Lower marginal corporate tax rates reduce businesses’ after-tax cost of capital, which incents them to invest more, adding to their capital stock, and ultimately increasing their productivity and the economy’s growth.

The problem is that while the lower marginal corporate rates reduce businesses’ cost of capital, the higher interest resulting from the

poor timing and deficit-financing of the tax cuts

increases their cost %

of capital and washes out most of the benefit. The tax plan will not increase growth from 2% to 2.9% per annum over the next decade as the Treasury Department has claimed, but from 2% to 2.05%.

Even well-designed tax reform that lowered marginal rates for businesses but paid for them would not come close to the growth anticipated by the Treasury.

Stocks up, housing down. The legislated changes to the tax code will have substantial countervailing impacts, lifting stock prices but weighing on housing values. Stock prices receive a lift given the higher after-tax earnings of large publicly traded companies, although this is partially offset by the impact of the higher interest rates on the price multiple that investors are willing to put on those earnings. Accounting for these crosscurrents, and the uncertainty with regard to whether the lower tax rates will be permanent after the 10-year budget horizon, the tax plans should lift stock prices by 10% to 15% (see Chart 3). Much of the increase in stock prices has already occurred.

House prices suffer under the tax plan. The tax law changes significantly reduce the value of the mortgage interest deduction, or MID, and property tax deductions, which are capitalized in current house prices. The qualifying loan amount for the MID is capped at $750,000, the property tax deduction at

$10,000, and the value of both deductions is

reduced by the doubling of the standard deduction, thus significantly reducing the number of households that itemize and take advantage of the MID. Also, the higher mortgage rates that result from the higher budget deficits and debt under the plans weaken housing demand.

Considering all of this, the hit to national house prices is estimated to be near 4% at the peak of the impact in summer 2019. The Northeast Corridor, South Florida, big midwestern cities, and the West Coast will suffer the biggest price declines (see Chart 4). Counties such as Essex NJ, Westchester NY, Cook IL and Delaware PA could see house prices reduced by as much as 10% compared with what they would have been otherwise.

The impact on the broader national economy of the higher stock prices and lower house prices is largely a wash.

Opportunity lost. The Trump administration and Republican Congress finally get their first major legislative win with the passage of sweeping changes to the tax code for businesses and individuals. But contrary to their hopes, the tax cuts will not meaningfully help the economy. In the immediate near term, growth will be stronger, but because the economy is at full employment, odds are good that it will overheat unless the Federal Reserve aggressively raises interest rates. Either way, the economy will suffer early in the next decade. And any longer-run benefit from the

Sources: JCT, Moody’s Analytics

-8,000

-6,000

-4,000

-2,000

0

Personal tax rates; AMT Standard deduction; credits 21 % corporate rate; no AMT Treatment of pass-throughs Double estate tax exemption Personal revenue raisers Other corp/int'l tax changes Net effect, tax rev. 2

4 6 8

10 12 14 16 18

95 00 05 10 15

Unemployment rate, U-3 Underemployment rate, U-6

Sources: BLS, Moody’s Analytics

Full employment

MOODY’S ANALYTICS / Précis® U.S. Metro / December 2017

MOODY'S ANALYTICS / Book / Copyright © 2018, Moody's Analytics, Inc. All Rights Reserved.

lower marginal tax rates will be washed away by the fallout from the bigger budget deficits and government debt load. Good tax reform is

difficult to do, and the tax plan set to pass into law does not get it done.

Mark Zandi

December 2017

Plan Boosts After-Tax Corporate Earnings Add to S&P EPS from lower corporate tax rate, $

House Prices Are Hit Under Tax Plan % change in FHFA HPI due to tax plan

Sources: S&P, Moody’s Analytics Sources: IRS, Moody’s Analytics

23 / 38

RELATIVE EMPLOYMENT PERFORMANCE (JAN 2007=100)

SOUTH

Source: Moody’s Analytics

EMPLOYMENT GROWTH RATE

2016-2018 2016-2021

1.8%

1.2%

GROSS DOMESTIC PRODUCT

2016-2018 2016-2021

2.7% 2.6%

STRENGTHS & WEAKNESSES ANALYSIS STRENGTHS

» Lower costs, including taxes, attract businesses and households.

» Above-average population growth in some states drives household spending.

WEAKNESSES » Workforce quality still lags in many places, and

per capita incomes are low. » Globalization in manufacturing erodes the

South’s competitive advantage.

Recent Performance. Following a rough jobs—the state’s unemployment rate dropped hurricane season, the major economies of the to below 4% in September, the lowest level in South are starting to recover. After Harvey hit a decade, even as hourly wages climbed to a Texas in late August and Irma hit Florida in Sep- record high. A longer-term concern is that retember, total employment in the region fell. The tiree havens along Florida’s Gulf Coast south of rebound began in October, after Congress ap- Tampa would lose their luster if baby boomers proved an initial $15 billion relief package for considering retirement were to shy away from Texas. Later in the month, lawmakers autho- these hurricane-prone areas. However, the likerized a second installment amounting to $36.5 lihood is that this will not occur unless the patbillion, which will be distributed among Florida, tern of hurricanes becomes more frequent and Puerto Rico and California as well as Texas. De- damaging. Much the same is true of South Carspite the weather-related setback, regional job olina, where the storm affected tourism only growth in the South over the past year has been temporarily. Further, Georgia was unaffected the fastest among the four regions, with manu- by the storms and as a result will continue to facturing and professional services leading the grow at an above-average pace, maintaining its way. Because these industries pay well, growth position as a leader in the region. Core profesin high-wage jobs in the South has outpaced sional services, especially in Atlanta; distribu-

that in the West. tion; and homebuilding will lead the way. North Energy exploration. The oil patch is set to Carolina’s performance has been matching

accelerate. In addition to the rebuilding efforts the national average in 2017, reflecting that is on the Gulf Coast that will lift residential and has reached full employment and is on a trend commercial construction in Texas and Louisiana, growth path. the uptrend in oil prices that

CURRENT EMPLOYMENT TRENDS % CHANGE YR AGO, 3-MO MA

Nov 16 May 17 Nov 17 Total 1.9

2.0 1.7

Construction 3.4 3.3 3.5 Manufacturing -0.0 1.3 1.9 Trade 1.2 0.6 0.6 Trans/Utilities 2.3 2.2 2.0 Information -0.6 -1.7 -2.3 Financial Activities 2.0 2.3 2.2

0 2 4 6 8

10 12 14 16

30 29 28 27 26 25 24 23 22 21 20 New corporate tax rate

>-2 -2 to -4 -4 to -6 <-6

U.S. avg=-4

MOODY’S ANALYTICS / Précis® U.S. Metro / December 2017

MOODY'S ANALYTICS / Book / Copyright © 2018, Moody's Analytics, Inc. All Rights Reserved.

Prof & Business Svcs. 2.4 3.1 2.7 began in August will Stimulus elsewhere in the South. In the reboost drilling throughout the subregion. Since gion’s midsection, Tennessee has been slowing reaching a trough in the middle of August, West but should get a temporary boost as demand Texas Intermediate has risen by about $15 per rises to replace motor vehicles destroyed by hurbarrel to $57, the highest level since early 2015. ricane flooding. Kentucky and Alabama, whose Internal political struggles in Saudi Arabia, rising performance has been steadier, will similarly tension between that nation and Iran, and pos- benefit. In Virginia, the likelihood of increased sible new U.S. sanctions on Iran together imply federal defense spending should lift militarythat prices will not quickly fall back. Active drill related industries in Northern Virginia and rigs have begun to rise in the fourth quarter in Virginia Beach. Texas, Louisiana and Oklahoma following a Having weathered the hurricanes, the three-month downtrend. South should remain the near-term regional

Southeast growth is steady. Because Ir- leader as the oil patch rebounds. Texas will ma’s impact on the Southeast was less damag- vie with the Southeast for the regional lead. ing than Harvey’s on Texas, steady growth there Longer term, the South will derive support should continue. After dipping in August prior from demographics, the energy industry, to the storm, the labor force in Florida actu- and low business costs. ally rebounded later in September. These ad- Ed Friedman ditional

workers had no trouble finding decent December 2017

Edu & Health Svcs. 2.9 2.7 2.2 Leisure & Hospitality 3.0 2.1 1.6 Other Services 1.9 1.8 2.5 Government 1.3 0.8 0.8

FORECAST RISKS

SHORT TERM LONG TERM UPSIDE

» Stronger than expected rebound in the oil patch lifts entire region.

» Low costs enable some reshoring of manufacturing.

DOWNSIDE » In-migration to the Southeast rebounds less

than anticipated. » Decline in U.S. vehicle sales slows growth in the

Mid-South auto-producing states.

COST OF

DOING BUSINESS 97%

2011 2012 2013 2014 2015 2016 INDICATORS 2017 2018 2019 2020 2021 2022 4,600.3 4,703.7 4,812.9 4,929.8 5,080.1 5,128.9 Gross regional product (C09$ bil) 5,250.6 5,422.1 5,581.6 5,672.2 5,863.6 6,061.6

44,016 44,844 45,705 46,745 47,830 48,714 Total employment (ths) 49,597 50,448 51,048 51,236 51,722 52,461 1.4 1.9 1.9 2.3 2.3 1.8 % change 1.8 1.7 1.2 0.4 0.9 1.4 8.7 7.7 6.9 5.9 5.2 5.0 Unemployment rate (%) 4.4 3.7 3.8 4.5 4.9 4.9 6.6 5.0 1.0 6.1 4.8 1.8 Personal income growth (%) 3.5 5.1 5.4 4.6 4.9 5.0 108,690 109,857 110,919 112,135 113,430 114,670 Population (ths) 116,044 117,500 118,973 120,419 121,841 123,309 594.0 654.6 588.8 713.0 818.3 778.8 Net migration (ths) 951.0 1,040.8 1,066.7 1,050.1 1,037.7 1,096.1 216,101 263,641 315,269 328,063 362,601 389,925 Single-family permits (#) 419,333 497,173 600,604 628,810 656,505 665,990 83,519 141,025 152,063 165,732 182,944 177,061 Multifamily permits (#) 161,862 131,441 137,025 136,360 165,732 189,804 267 266 275 289 306 326 House price (1980Q1=100) 347 362 368 372 379 388 372 522 503 367 470 525 Mortgage originations ($ mil) 466 443 430 396 433 475 4,753.0 5,438.8 5,787.9 6,163.4 6,475.1 6,530.1 New vehicle registrations (ths) 6,070.1 6,315.5 6,251.7 6,046.0 6,149.8 6,570.7 455,228 406,310 370,059 340,879 310,963 294,152 Personal bankruptcies (#) 289,257 282,700 288,351 307,962 361,590 436,014

20 / 38

Hilco Real Estate Appraisal, LLC Page 6

REGIONAL ANALYSIS

As additional supporting documentation for the previously presented information, the following items are

retained in our files: 1.) a User’s Guide related to the previously presented statistical and economic

information; 2.) a Five-Year Forecasted Employment Growth Rankings for all MSAs within the U.S.; 3.)

the Forecast Assumptions related to projections presented on the preceding pages; 4.) Employment

Growth Rankings for all MSAs within the U.S.; 5.) Population Growth Rankings for all MSAs within the

U.S.; 6.) Absolute Change in Employment & Population projections for all MSAs within the U.S.; 7.) Risk-

Adjusted Return for each MSA within the U.S.

Key Comparisons and Projections

The following information is taken from the previously presented economic and statistical data provided

by Economy.com as of December 2017. Robinsonville,, MS is in Tunica County, MS which is part of

the Memphis MSA as determined by Economy.com.

UNITED STATES SOUTH

Total Employment

146,400,000 49,600,000

Employment Change %

1.5 1.8

Unemployment Rate %

4.4 4.6

Personal Income Growth

3.8 4.0

Strengths

• Very productive workforce. • Lower costs, including taxes,

attract businesses and

households.

• Labor market attracts skilled and unskilled immigrants.

• High innovation

and entrepreneurship. • Mobile labor force, flexible

labor system.

•

Above-average population

growth in some states drives

related household spending.

Weaknesses

• Many labor market

nonparticipants. • Workforce quality still lags in

many places, and per capita

incomes are low.

Page 7

• Large budget,

current account deficits.

• Skewed income and wealth

distribution. • Polarized and fractured

political system

•

Globalization in manufacturing

erodes the South’s competitive

advantage.

REGIONAL ANALYSIS

National Outlook

“Regardless of what is happening around the globe—and a lot seems to be happening—the U.S.

economy continues to plug away. The U.S. economic expansion is eight years old and counting, and

growth remains remarkably stable.

Real GDP growth ebbs and flows on a quarterly basis, but that seems mostly due to the Bureau of

Economic Analysis’ problems measuring GDP. Abstracting from the quarterly ups and downs, it has

been growing at a 2% annualized pace since the expansion began, and that is what it likely grew during

the first half of this year.

Job growth has been equally unwavering. There have been months with soft employment gains and

others with strong gains, but this too can be chalked up mostly to measurement issues and transitory

events, like weather. Looking through monthly noise, job additions have averaged just under 200,000

per month since job gains resumed—about the size of gains enjoyed so far this year.

A boring economy is exactly what global investors hope for, and one reason they have been bidding up

asset prices. Stock prices are at record highs, credit spreads in the bond market are narrow, and

capitalization rates in real estate markets are low. There are other reasons for the investor euphoria—

easy global monetary policy quickly comes to mind—but investors are feasting on businesses’ steadyas-

she-goes revenue growth, costs, and profitability. A better global economy and more stable dollar mean

that the U.S. trade deficit, which had been a significant drag on U.S. growth, is leveling off and soon may

even improve a bit. It is a pleasant surprise how quickly the weight on the U.S. economy from global

trade has lifted.

The economy continues to expand at a pace above its potential, and any remaining unused labor and

other capacity is quickly being put to use. But this bears close watching, the outlook for inflation and

interest rates are particularly difficult to get right.” (Precis: Metro December 2017 Moody's Analytics

Economy.com)

South Region Outlook

“The South will be the near-term regional leader as the oil patch rebounds. Texas will vie with the

Southeast for the lead within the region. Longer term, the South will derive support from demographics,

the energy industry, and low business costs.” (Precis: Metro December 2017 Moody's Analytics

Economy.com)

NEIGHBORHOOD ANALYSIS

Hilco Real Estate Appraisal, LLC Page 8

Hilco Real Estate Appraisal, LLC

NEIGHBORHOOD ANALYSIS

Location

Casino gambling's effect on the local economy has spurred population growth in unincorporated parts

of the county outside Tunica proper. Since 1990, the town's name has been popularly associated with

several casinos located near the Mississippi River. However, the current group of casinos is located

from the community of Tunica Resorts, 10 miles north of the town of Tunica, and extending to the DeSoto

County line.

Neighborhood Map

Page 9

Tunica Resorts was originally named "Robinsonville", but the name was changed in 2005 to eliminate

confusion over the location of the casinos, which have always used the name "Tunica" as an identifier.

The success of these gaming houses in northern Tunica County came at the expense of the area's first

group of casinos in the early 1990s, located just northwest of Tunica proper, in an area known as Mhoon

Landing. This now comprises the current census-designated place of North Tunica. These casinos were

closed or moved as larger resorts opened closer to Memphis to attract its larger residential base.

Unlike the area including casinos along Mississippi's Gulf Coast region, Tunica was not in the path of

Hurricane Katrina. As a result, some of the regular Gulf Coast customer traffic from casinos drifted

northward to Tunica County while repairs and reconstruction were underway in the Gulf Coast locations.

Though the casinos lie outside the town limits, the benefits of tax revenue generated have also aided

the town. Major improvements to the public school system and downtown district are among the most

NEIGHBORHOOD ANALYSIS

visible aspects. Long-term effects include major highway improvements on U.S. Route 61 and a

muchdiscussed potential expansion of Tunica Municipal Airport.

Transportation/Access/Visibility

According to the U.S. Census Bureau, the county has a total area of 481 square miles, of which 455

square miles is land and 26 square miles is water.

Major highways

Interstate 69

U.S. Route 61

Mississippi Highway 3

Mississippi Highway 4

Airports

Memphis International Airport is a civil-military airport seven miles southeast of downtown Memphis in

Shelby County, Tennessee, United States.

Memphis International Airport is home to the FedEx Express global hub, which processes many of the

company's packages. Nonstop FedEx destinations from Memphis include cities across the continental

United States, Canada, Europe, the Middle East, Asia, and South America. From 1993 to 2009, Memphis

had the largest cargo operations of any airport worldwide. MEM dropped to the second position in 2010,

NEIGHBORHOOD ANALYSIS

Hilco Real Estate Appraisal, LLC Page 10

just behind Hong Kong; however, it remains as the busiest cargo airport in the United States and in the

Western Hemisphere.

As of 2016, MEM had a count of over 4 million passengers, up slightly from 2015. The airport was

previously a hub for Northwest Airlines and later Delta Air Lines. As of June 2017, MEM averaged 83

passenger flights per day on all of the airlines serving the city. In recent years the airport added several

new airlines, including Air Canada, Allegiant Air, Frontier Airlines, and Southwest Airlines, which has

increased competition among carriers. Since Delta's departure as a hub operation, average round trip

prices have also declined. The July–September 2014 quarter alone saw a 4.7% decline from the quarter

a year earlier.

The 164th Airlift Wing of the Tennessee Air National Guard is based at the co-located Memphis Air National

Guard Base, operating C-17 Globemaster III transport aircraft.

Hilco Real Estate Appraisal, LLC

Land Use Patterns

The dominant land uses in the neighborhood are commercial and vacant land which are centered around

Casino Strip Blvd. and US 61. The subject property is just west of US 61. The subject’s immediate area

is mostly under developed and with vacant land available for new construction.

The subject is part of the Tunica Resort Corridor Casino and hotels, competing mainly with hotels

clustered near the casinos and US 61. The surrounding neighborhoods are mostly agricultural, as well

as residential neighborhood throughout the local area. .

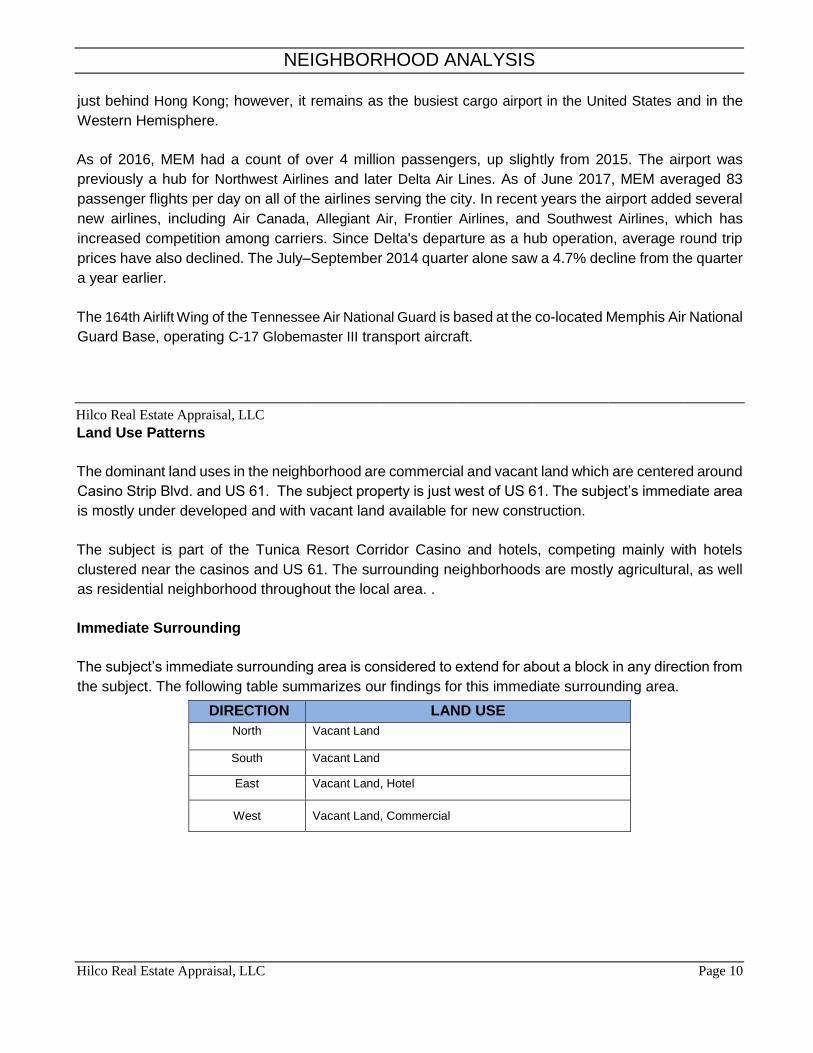

Immediate Surrounding

The subject’s immediate surrounding area is considered to extend for about a block in any direction from

the subject. The following table summarizes our findings for this immediate surrounding area.

DIRECTION LAND USE

North Vacant Land

South Vacant Land

East Vacant Land, Hotel

West Vacant Land, Commercial

NEIGHBORHOOD ANALYSIS

Hilco Real Estate Appraisal, LLC Page 11

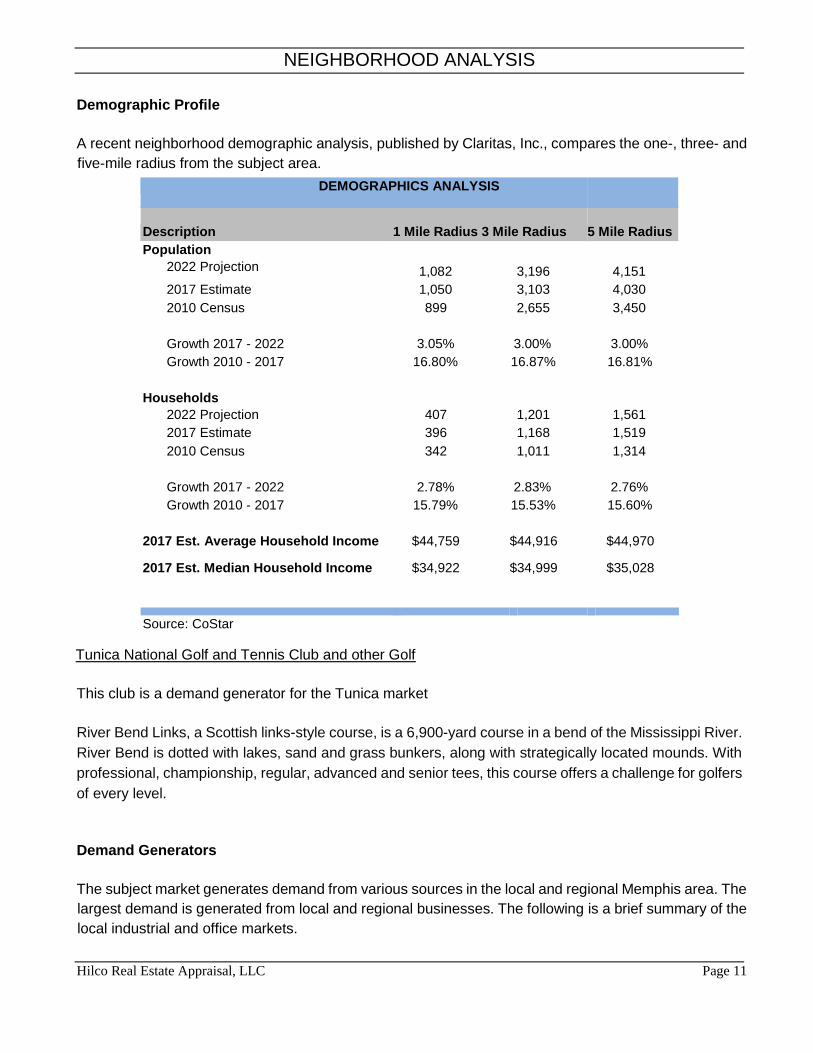

Demographic Profile

A recent neighborhood demographic analysis, published by Claritas, Inc., compares the one-, three- and

five-mile radius from the subject area.

DEMOGRAPHICS ANALYSIS

Description 1 Mile Radius 3 Mile Radius 5 Mile Radius

Population 2022 Projection 1,082 3,196 4,151

2017 Estimate 1,050 3,103 4,030

2010 Census 899 2,655 3,450

Growth 2017 - 2022 3.05% 3.00% 3.00%

Growth 2010 - 2017 16.80% 16.87% 16.81%

Households 2022 Projection 407 1,201 1,561

2017 Estimate 396 1,168 1,519

2010 Census 342 1,011 1,314

Growth 2017 - 2022 2.78% 2.83% 2.76%

Growth 2010 - 2017 15.79% 15.53% 15.60%

2017 Est. Average Household Income $44,759 $44,916 $44,970

2017 Est. Median Household Income $34,922 $34,999 $35,028

Source: CoStar

Tunica National Golf and Tennis Club and other Golf

This club is a demand generator for the Tunica market

River Bend Links, a Scottish links-style course, is a 6,900-yard course in a bend of the Mississippi River.

River Bend is dotted with lakes, sand and grass bunkers, along with strategically located mounds. With

professional, championship, regular, advanced and senior tees, this course offers a challenge for golfers

of every level.

Demand Generators

The subject market generates demand from various sources in the local and regional Memphis area. The

largest demand is generated from local and regional businesses. The following is a brief summary of the

local industrial and office markets.

NEIGHBORHOOD ANALYSIS

Hilco Real Estate Appraisal, LLC Page 12

Office Market Overview

The Memphis Office market ended the fourth quarter 2017 with a vacancy rate of 12.2%. The vacancy

rate was up over the previous quarter, with net absorption totaling a positive 316,197 square feet in the

fourth quarter. Rental rates ended the four quarter at $17.45, a decrease over the previous quarter. A

total of 888,375 square feet delivered to the market, with 531,559 square feet still under construction at

the end of the quarter.

Total Office Submarket Statistics Year-End 2017

Market

Existing Inventory Vacancy YTD Net

Absorption YTD

Deliveries Under

Const SF Quoted

Rates

# Blds Total RBA Direct SF Total SF Vac % 385 Corridor 349 7,630,530 719,932 745,177 9.8% 53,897 122,112 9,400 $18.30 Airport 262 6,681,143 1,408,237 1,408,237 21.1% 55,192 0 0 $13.77 DeSoto County 356 2,122,219 130,394 137,594 6.5% (36,150) 800 0 $15.89 Downtown 277 10,680,656 1,708,982 1,714,753 16.1% (76,556) 45,000 328,000 $17.15 East 551 13,760,854 1,307,413 1,339,584 9.7% 5,389 163,805 159,909 $20.77 Fayette County 55 408,675 15,317 15,317 3.7% (7,017) 0 0 $14.07 Marshall County 20 209,212 1,038 1,038 0.5% (1,038) 0 0 $0.00 Midtown 408 4,555,617 369,761 369,761 8.1% 461,595 552,258 0 $15.35 North 247 2,160,947 174,657 174,657 8.1% (67,816) 0 0 $15.74 Northeast 291 4,425,695 513,547 514,797 11.6% (73,047) 0 34,250 $16.95 Tate County 42 154,135 7,250 7,250 4.7% (5,950) 0 0 $12.37 Tipton County 45 191,710 21,963 21,963 11.5% 7,698 4,400 0 $8.25 Tunica County 20 74,219 0 0 0.0% 0 0 0 $0.00 Totals 2,923 53,055,612 6,378,491 6,450,128 12.2% 316,197 888,375 531,559 $17.45 Source: CoStar Property®

The subject’s submarket, highlighted in yellow, is the smallest market in Memphis with limited data.

Other Regional Demand Generators

In addition to commercial corporate demand, the subject market wide generates a significant demand

from meeting and group business, and leisure travelers. The meeting and group demand is generated

by corporate businesses in addition to sports, teams, weddings, reunions, and religious meetings. The

subject is located less than 30 miles from the Memphis International Airport. The following are a few

highlights of the local attractions/facilities in this market.

Blues Hall of Fame Museum

Opened in May of 2015, the Blues Hall of Fame Museum is a Memphis gem for both serious blues fans

and casual visitors. With robust exhibits and in-depth history, the museum exposes, educates, and

entertains visitors with all that is blues culture while highlighting our over 400 inductees in five key

categories: Performer, Individual, Album, Single, and Literature.

National Civil Rights Museum

The National Civil Rights Museum is a complex of museums and historic buildings in Memphis,

Tennessee; its exhibits trace the history of the Civil Rights Movement in the United States from the 17th

NEIGHBORHOOD ANALYSIS

Hilco Real Estate Appraisal, LLC Page 13

century to the present. The museum is built around the former Lorraine Motel, where Rev. Martin Luther

King, Jr. was assassinated on April 4, 1968. Two other buildings and their adjacent property, also

connected with the King assassination, have been acquired as part of the museum complex.

The museum re-opened in 2014 after renovations that increased the number of multi-media and

interactive exhibits, including numerous short movies to enhance features. The museum is owned and

operated by the Lorraine Civil Rights Museum Foundation, based in Memphis. The Lorraine Motel is

owned by the Tennessee State Museum and leased long term to the Foundation to operate as part of the

museum complex.

COLLEGES & UNIVERSITIES

Colleges and universities located in the city include the University of Memphis, including University of

Memphis Cecil C. Humphreys School of Law, Rhodes College, Christian Brothers University, Memphis

College of Art, LeMoyne–Owen College, Baptist College of Health Sciences, Memphis Theological

Seminary, Harding School of Theology, Embry–Riddle Aeronautical University, Worldwide (Memphis

Campus), Reformed Theological Seminary (satellite campus), William R. Moore College of Technology,

Southern College of Optometry, Southwest Tennessee Community College, Tennessee Technology

Center at Memphis, Visible Music College, Mid-America Baptist Theological Seminary, and the University

of Tennessee Health Science Center. Memphis also has campuses of several forprofit post-secondary

institutions, including Concorde Career College, ITT Technical Institute, Remington College, Vatterott

College, and University of PhoenixHealth Care.

Conclusion

The subject property is located within the Tunica Resort and is part of the Casino hotel corridor. Regional

and local access is good. The subject property is compatible to the adjacent uses. The regional has

been affected by the most recent hurricane and new Casinos entering the outside of the immediate

market. Revenues appear to be declining.

Hilco Real Estate Appraisal, LLC Page 14

SITE DESCRIPTION

SITE DESCRIPTION

The subject site is comprised of one rectaangular-shaped interior shaped parcel, located along the south

side of Casino Strip Resort Blvd. in Robinsonville, MS.

TAX MAP

Shape: Irregular

Topography: The subject is generally level at curb grade.

Land Area: The hotel site sits on 1.50 acres, or 65,340 square foot. The land area is based on the

assessor’s parcel map. It is noted that we relied on this information

and assume that it is accurate. We reserve the right to amend the

land area should this assumption be determined to be incorrect.

Zoning: None

Frontage, Access, Visibility: The subject site is comprised of one rectaangular-shaped interior shaped

parcel, located along the south side of Casino Strip Resort Blvd. in

Robinsonville, MS. The access and visibility is considered

Hilco Real Estate Appraisal, LLC Page 15

average, with access provided by curb cuts on Casinoa Strip Road

and Commercial Road.

SITE DESCRIPTION

Soil Conditions: For the purposes of our analysis, we have assumed that no soil

conditions exist. We are not qualified to render a technical opinion

regarding soil conditions. Therefore, it is assumed that the load-

bearing capacity is sufficient to support any reasonably probable

improvements.

Utilities All necessary and typical public utilities are assumed to be installed

to the subject sites.

Land Use Restrictions: The appraisers were not provided with a title report. The

appraisers have assumed that no easements or encroachments

affecting value have been created in the intervening years. In the

performance of the appraisal, the appraisers were not made aware

of any other easements or encroachments that would have an

adverse effect on the subject site, other than typical utility

easements. However, it is suggested that a legal opinion be

obtained to ensure that no adverse easements or encroachments

exist.

Drainage: Drainage is via flow gutters. During our inspection of the site, we

observed no drainage problems and assume that none exist.

Flood Hazard: The subject is located in an X flood zone which is outside the 500

year floodplain boundaries as noted by the map panel # 280236

0085 D dated August 16, 2008.

Hazardous Substances: There were no hazardous substances observed or discovered

during our routine appraisal investigation. The subject was

appraised as if no hazardous substances are present. However,

we are not trained to perform technical environmental inspections.

If the client is concerned about this issue, we recommend the

services of a professional engineer for this purpose.

Overall Functionality:

The subject site has a typical shape, size and utility for the local

area. No significant issues that would currently limit the utility of

the site were discovered. The subject site is appraised “As-Is”, fully

functional for its highest and best use.

IMPROVEMENTS DESCRIPTION

Hilco Real Estate Appraisal, LLC Page 16

IMPROVEMENTS DESCRIPTION

The subject property is a limited-service Days Inn hotel that opened in 1994 as a Knights Inn and was

converted to a Days Inn in 2008. The property features 66 rooms. The hotel offers complimentary hot

breakfast. Situated on a 1.50 acre site, the property is located in the Tunica Resort Hotel Market.

The following is a description of the subject’s improvements and basic construction features based on

our inspection.

Infrastructure and Site Improvements

The hotel is a 2-story, interior corridor, limited-service hotel. The guestrooms are located on floors 1

through 2. The lobby is located at the front building, along with the breakfast seating. Parking surrounds

the buildings to the south, east and west.

Number of Rooms Guestroom Configuration

66 Rooms

66 Total

Seating Capacity Food & Beverage Facilities C omments

20 Breakfast Area

Indoor Meeting & Banquet Facilities Square Footage C omments

Total 0

Amenities & Services

Complimentary Breakfast

FACILITIES SUMMARY

( Estimated )

IMPROVEMENTS DESCRIPTION

Hilco Real Estate Appraisal, LLC Page 17

The following table summarizes the general construction characteristics of the improvements. We have

estimated certain items below including construction materials, based on our knowledge of other

prototypical construction.

BUILDING SUMMARY - GENERAL CONSTRUCTION

Property Type Limited-Service

Guest Room Corridors Interior Corridor

Foundation Concrete slab, with cast-in-place perimeter and interior colums

and grade beams

Structure/Exterior Walls Masonry + Frame

Roof Pitched Shingles Composite Membrane Cover

Electrical Assumed to comply with City building codes Plumbing Assumed to

comply with City building codes

Windows Anodized aluminum with fixed insulated glazing. Single Pane

Exterior Doors Metal.

Elevators One

Life Safety Systems Fire Sprinklers and smoke detectors

Ceilings Textured and/or painted gypsum board or suspended

acoustical tile.

Floors Common areas have a combination of ceramic tile and carpet

flooring. Guestrooms are assumed to have commercial grade

carpet and ceramic tiles.

Interior walls Walls are generally textured and painted drywall or vinyl wall

covering on gypsum board

HVAC Roof-mounted Individual systems

Parking 84 parking spaces

Actual Age 24 years Effective Age 20 years

Total Economic Life 50 years Remaining

Economic Life 30 years

Overall Condition Average

Source: Property management; Hilco Real Estate Appraisal, LLC

The hotel's exterior was in average condition upon inspection, and no major problems were observed.

IMPROVEMENTS DESCRIPTION

Hilco Real Estate Appraisal, LLC Page 18

Lobby Area

The lobby is located at the entrance of the hotel, through two double glass doors, one automatic. The

front desk immediately greets the guests to the left, and there are seats for waiting. The lobby appeared

in average condition

Restaurant/Lounge/Breakfast Buffet Areas

The hotel offers a free hot breakfast buffet. This area is sit up to about 15 guests. There is a small

kitchenette at the back with a cooler.

Guestrooms

The hotel features queen/queen or king guestroom

configurations, about 350 square foot of living area. The

rooms offer typical amenities for this product type, including a mini refrigerator, and microwave (first floor

rooms only). There are 2 handicap rooms available in both King configurations.

We inspected three guestrooms. The guestroom is furnished

with a table and chairs. The guest bath is has a shower/tub

combo. The bedroom includes nightstands, lighting, and a

either a flat screen television or older model. In room

amenities include high-speed internet access.

The corridors are adequate and functional, adequate width

permitting the

passage of

housekeeping

carts.

Recreational

Facilities

The subject does not feature any recreational facilities.

IMPROVEMENTS DESCRIPTION

Hilco Real Estate Appraisal, LLC Page 19

Back-of-the-House

The subject property is served by the necessary back-of-the-house space, such as administrative offices

and laundry facilities (one commercial washer and two dryers).

Utilities

All utilities are available to site.

Functional Utility

The existing improvements appear to offer a typical limited

service hotel with regard to layout, construction materials and

overall design. In general it is typical of hotel of this size and

competitive with other similar brands. In general, the

improvements are considered adequately functional in terms of utility.

ADA Compliance

The Americans with Disabilities Act (ADA) became effective January 26, 1992. We have not made, nor

are we qualified by training to make, a specific compliance survey and analysis of this property to

determine whether or not it is in conformity with the various detailed requirements of the ADA. It is

possible that a compliance survey and a detailed analysis of the requirements of the ADA could reveal

that the property is not in compliance with one or more of the requirements of the Act. If so, this fact could

have a negative effect upon the value of the property. Since we have not been provided with the results

of a survey, we did not analyze the results of possible non-compliance.

Furniture, Fixtures and Equipment (Personal Property) The

subject’s FF&E are detailed later in the report.

Environmental Issues

We did not observe any potentially hazardous materials such as lead paint, asbestos, urea formaldehyde

foam insulation, or other potentially hazardous construction materials on or in the improvements.

However, it is noted that we did not search for such materials and are not qualified to detect such

materials. The existence of said hazardous materials (if any) may have an effect on the value of the

property. Therefore, for the purpose of this appraisal, we have specifically assumed that the property is

not affected by any hazardous materials that may be present on or in the improvements. We strongly

recommend that a qualified environmental engineering firm be retained by the Client prior to making a

business decision.

Deferred Maintenance

Deferred maintenance is curable, physical deterioration that should be corrected immediately. While the

immediacy of need is inherent and exists, it does not necessarily suggest inadequate maintenance in the

past. Our limited observation of the property indicated no significant items of deferred maintenance in

the common area.

IMPROVEMENTS DESCRIPTION

Hilco Real Estate Appraisal, LLC Page 20

Capital Expenditures

Our analysis specifically assumes that the hotel will require ongoing refurbishments in order to maintain

and upkeep to current standards, as well as its RevPAR position in this market, as forecast in this report.

In order to ensure that the subject property is maintained in a competitive position throughout the holding

period, we have deducted a reserve for replacement equal to 4.0% of total revenues per year. This is in-

line with the requirements from the market. The reserve is assumed to be adequate to fund all future

capital expenditures.

Conclusion

The existing improvements maintain average overall design and functional utility. Furthermore, there

were no signs of major deferred maintenance upon limited inspection and we are unaware of any major

planned capital improvements (exclusive of a required PIP that has not been completed). Consequently,

there are no known factors that could be considered to adversely impact the marketability of the

improvements.

Hilco Real Estate Appraisal, LLC Page 21

REAL ESTATE TAXES

REAL ESTATE TAXES

The site and improvements are identified by the Tunica County Assessor’s Office as parcel number:

3104180000000102

All property, real and personal, is appraised at true value then assessed at a percentage of true value

according to its type and use. Assessment ratios are 10%, 15%, and 30%. All ad valorem taxes are

assessed by local taxing authorities except that the Tax Commission assesses all public service

corporations (railroads, pipelines, electric power and light companies, private railcars, telephone and

telegraph companies, and other such companies) and provides to the tax assessor uniform assessment

schedules for motor vehicle and mobile homes. All ad valorem taxes are collected by the local county

and/or municipal tax collectors. Ad valorem taxes are payable on or before February 1 of the following

year of assessment except on motor vehicles which are paid at the time they are registered for road and

bridge privilege taxes. Mobile homes must be registered within 7 days of either purchase or movement

into the state and the ad valorem taxes are to be paid within 90 days.

The following presents a summary of the subject’s 2017 assessment (market value and effective tax rate)

and tax liability:

Assessor’s ID No. 3104180000000100

Land $75,000

Improvements

Total

$1,607,420

$1,682,420

Effective Tax Rate

Total Taxes

0.015248

$25,653

Thus, the subject’s 2017 total tax liability is $25,652.70. The real property assessed value is $252,363 with

a 15 percent ratio, implying a market value of $1,682,420.

In the forthcoming Income Capitalization Approach, we have forecast the subject’s assessment and

corresponding real estate tax liability to increase and stabilize at a two percent increased amount or

$26,000 as rounded.

ZONING

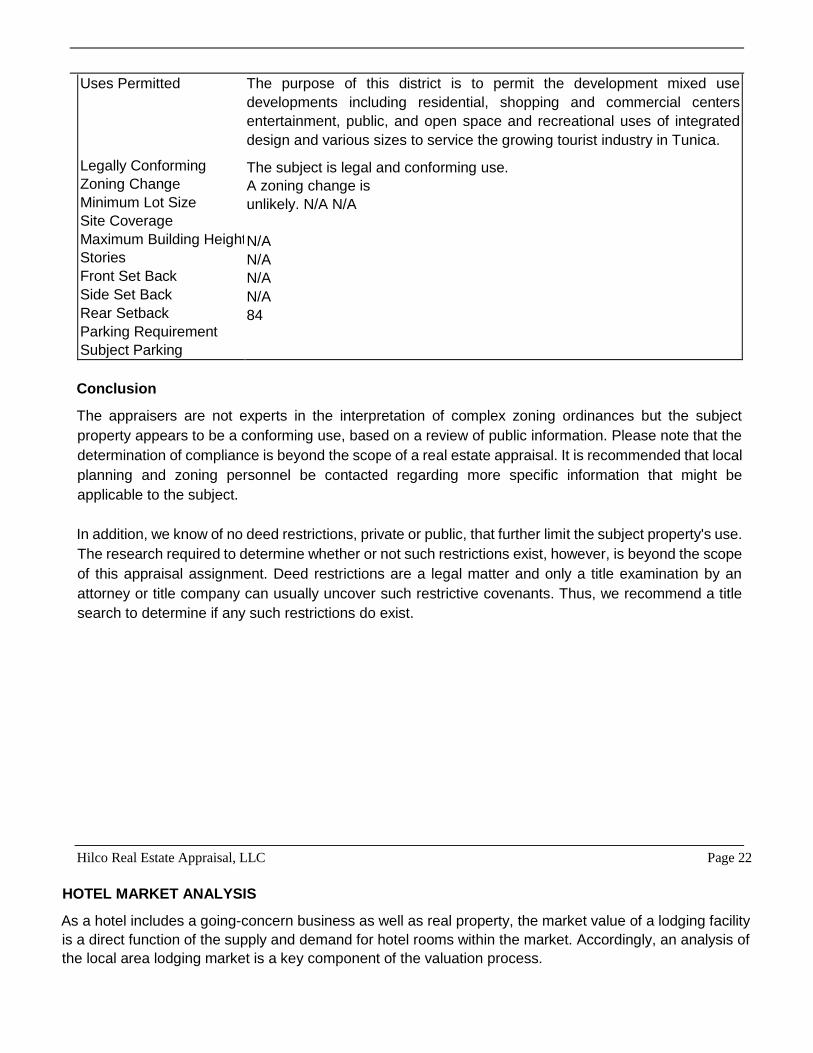

ZONING

The applicable zoning information for the subject is summarized as follows:

ZONING SUMMARY

Current Zoning None

Uses Permitted

Legally Conforming

Zoning Change

Minimum Lot Size

Site Coverage

Maximum Building Height 5

Stories

Front Set Back

Side Set Back

Rear Setback

Parking Requirement

Subject Parking

The purpose of this district is to permit the development mixed use

developments including residential, shopping and commercial centers

entertainment, public, and open space and recreational uses of integrated

design and various sizes to service the growing tourist industry in Tunica.

The subject is legal and conforming use.

A zoning change is

unlikely. N/A N/A

N/A

N/A

N/A

N/A

84

Conclusion

The appraisers are not experts in the interpretation of complex zoning ordinances but the subject

property appears to be a conforming use, based on a review of public information. Please note that the

determination of compliance is beyond the scope of a real estate appraisal. It is recommended that local

planning and zoning personnel be contacted regarding more specific information that might be

applicable to the subject.

In addition, we know of no deed restrictions, private or public, that further limit the subject property's use.

The research required to determine whether or not such restrictions exist, however, is beyond the scope

of this appraisal assignment. Deed restrictions are a legal matter and only a title examination by an

attorney or title company can usually uncover such restrictive covenants. Thus, we recommend a title

search to determine if any such restrictions do exist.

Hilco Real Estate Appraisal, LLC Page 22

HOTEL MARKET ANALYSIS

As a hotel includes a going-concern business as well as real property, the market value of a lodging facility

is a direct function of the supply and demand for hotel rooms within the market. Accordingly, an analysis of

the local area lodging market is a key component of the valuation process.

HOTEL MARKET ANALYSIS

Hilco Real Estate Appraisal, LLC Page 23

Presented in this section is a discussion on the subject’s competitive market and the historical and projected

performance of the subject. The national market overview is taken directly from Marcus & Millichap’s Mid-

Year 2017 Hotel Research Report.

National Market Overview

The U.S. hospitality sector has recorded increases in

occupancy and revenue metrics during the year ending in June

as room demand remained healthy. Employment growth

nationwide and the rising median household income will

support travel in the near future. Both domestic and

international travel continue to rise, further benefiting room

demand. Potential headwinds do exist including the growing

construction pipelines in many major markets that may place

downward pressure on occupancy, the average daily rate and

RevPAR this year and into 2018. During the last 12-month

period, hiring in office-using sectors rose 2.4 percent

nationwide as 734,000 workers were added to staffs. Healthy

job growth and a tight employment rate of 4.4 percent bolstered medium household incomes by 2.8 percent

during this time. The rising incomes may spur additional leisure travel while increased jobs may further

business travel. Domestic and international passenger travel in the United States rose 3.8 percent during

2016. In particular, international travel provides hotel operators opportunities for stronger demand drivers

as passengers more than doubled in the last three years. Texas and California have more than 20,000

rooms each that are expected to break ground in the next 12 months. The increased supply may place

downward pressure on occupancy in the coming years.

Investors increasingly targeting hotels as demand drivers improve.

Hotel operations that spur revenue growth have kept buyers active in this sector. Transaction velocity rose

roughly 10 percent nationwide as demand picked up for

properties in many of the country’s smaller markets. On

average, hotel assets changed hands for nearly $100,000

per key, down slightly year over year as fewer properties in

upper chain scales changed hands. Among chain scales,

lower-tier hotels garnered significant investor attention.

Trades increased considerably for economy and upper

midscale assets during the previous four quarters. Demand

for upscale assets held steady with the majority of trades in

HOTEL MARKET ANALYSIS

Hilco Real Estate Appraisal, LLC Page 24

Marriott and Hilton branded properties. Several regions posted significant increases in transaction volume

during the last 12 months. The Carolinas and the Central Midwest region led the nation, with the Mid Atlantic,

Mid South and Southwest regions following. In prior years, coastal regions typically led sales volume. Sales

velocity picked up for independent properties during the year ending in June as buyers widened their

acquisition expectations. The increased demand for soft brand hotels may further intensify bidding for their

properties moving forward as visitors seek experience oriented hotels.

Hotel construction pipeline on the rise.

Roughly 111,000 rooms in more than 950 hotel projects were completed nationwide during the last 12

months up to June. Moving forward, nearly 187,000 rooms are under development and an additional

222,000 are expected to break ground in the next four quarters. The growing supply additions may place

downward pressure in occupancy over the coming year. The metros of Houston and New York City received

the largest number of rooms as 4,200 and 5,400 rooms were completed within July to June, respectively.

Hilton Worldwide and Marriott International boosted their inventory during the last 12 months. Both

companies averaged between 27 percent and 28 percent increases of new hotel rooms over all supply

additions. Among chain scales, the bulk of new completions were in the upscale and upper midscale

segments with a combined total of 77,000 rooms. Roughly 10,500 unaffiliated rooms were also constructed

during this time.

Occupancy climbs amid healthy room demand.

Since last June, demand for hotel rooms continued

to outpace supply growth, lifting occupancy in the

United States 50 basis points to 73.4 percent at the

end of the second quarter. First half occupancy rose

40 basis points from the same time period last year

to 65.3 percent. Large markets

that

demonstrated significant occupancy increases from

last year include Norfolk-Virginia Beach, Orlando and Atlanta. On the other hand, mounting supply pressures

in metros including Dallas, Houston and Nashville weighed on vacancy improvement in the last 12 months.

Nearly all hotel chain scales posted occupancy improvements over the year ending in June. Economy chains

boasted the greatest improvement with occupancy increasing 90 basis points to 65.4 percent. The upscale

segment posted the only occupancy decrease as the rate ticked down 20 basis points year over year to

80.5 percent. Based on location, occupancy in properties in proximity to major thoroughfares climbed 100

basis points during the previous four quarters to 66.6 percent. Room demand in these hotels typically comes

from travelers passing by. The highest occupancy rate remains in urban hotels at 80.4 percent, up 50 basis

points year over year.

Room demand drives increases in revenue metrics.

HOTEL MARKET ANALYSIS

Hilco Real Estate Appraisal, LLC Page 25

Rising occupancy nationwide is driving growth in revenue metrics. During the year ending in the second

quarter, the average daily rate advanced 2.1 percent to $129.12. The increase in ADR and occupancy

generated a 2.8 percent rise in RevPAR during this time to $94.73. ADR and RevPAR in independent hotels

outperformed all other chain scales, rising 2.7 percent and 3.9 percent, respectively. Economy hotels

followed as strong occupancy improvement and a 2.2 percent increase in ADR drove a 3.5 percent climb in

RevPAR during the last 12 months. Despite higher occupancy in urban areas, suburban hotels outperformed

their counterparts in ADR and RevPAR growth during the previous four quarters. ADR in urban hotels rose

0.3 percent while RevPAR inched up 0.9 percent during this time. In the suburbs, ADR climbed 2.3 percent

and RevPAR posted a 2.8 percent advance. Major markets with RevPAR growth near or above 10 percent

include Norfolk- Virginia Beach, Orlando, and San Diego.

2017 National Forecast

The U.S. economy has proved resilient throughout this cycle, hurdling numerous obstacles ranging from a

federal government shutdown to financial markets’ susceptibility to periodic bouts of volatility. Events abroad

also periodically weigh on the outlooks of U.S. business and consumers, and the effects of the Brexit vote

have clearly yet to entirely play out. However, a decline in travel from the U.K. and countries in the Euro

zone could become more evident in bookings at U.S. hotels in the coming months. Against the backdrop of

a choppy pattern of domestic economic growth and international uncertainty, the U.S. hotel sector will post

modest gains in all key performance measures this year. Room demand will grow 2.0 percent in 2016 to

offset an increase in construction, yielding a 30-basis-point rise in annual occupancy to 65.8 percent.

Revenue measures will gain traction through the peak summer travel season and early fall, with ADR and

RevPAR forecast to gain 4.1 percent and 4.5 percent, respectively. Over the near term, rising completions

will slow occupancy growth and further compress gains in RevPAR.

The unanticipated outcome of the Brexit vote disrupted the Federal Reserve’s campaign to normalize

monetary policy. As expected, the central bank did not elect to raise its short-term lending benchmark at its

July meeting, and prospects of a rate increase in September have also diminished. A flight-to-safety bid into

the 10-year U.S. Treasury in the days following the out-come in the U.K. lowered the yield on the 10year to

the mid1 percent range and reduced the 10-year Treasury swap rate.

Spreads on CMBS widened in the wake of Brexit but retraced to near pre-vote levels in the ensuing days.

CMBS lenders continue to compete with local, regional and large national banks in the hotel sector. The

minimum loan threshold starts at $5 million, and rates begin at roughly 325 basis points above the 10-year

U.S. Treasury swap rate for top brands in the largest markets, and select well-sponsored transactions in

secondary markets. Terms are five or 10 years, and leverage is capped at 70 percent.

Banks continue to monitor the concentration of hotel loans on their books as demand in some segments of

the economy wanes. Local and regional banks will loan a maximum of $10 million for hotel transactions,

while large national banks can provide up to $30 million. Leverage on senior debt can reach 65 percent for

the best transactions. Loan terms vary from three to seven years at rates that typically range from 250 to

300 basis points above the corresponding U.S. Treasury yield or the U.S. prime rate. Non-recourse financing

is also provided to qualified borrowers in select circumstances.

HOTEL MARKET ANALYSIS

Hilco Real Estate Appraisal, LLC Page 26

SUPPLY & DEMAND ANALYSIS

The subject property is located in the Tunica Resort market. The subject is a 66-room, limited-service hotel

that caters mainly to the leisure hotel demand. The subject competes with other flagged and independent

properties near the Tunica Casino Corridor. The subject property competes directly with six other hotels in

the market, as shown below. A 2017 estimate, historical performance and a summary description of the

competitive hotels are outlined in the following pages.

2017 Competitive Hotel Supply

Year Property Open

No. Rooms