cerca practitioner survey report fta fedstate e-file symposium may 3, 2000

TRANSCRIPT

CERCA Practitioner Survey Report

FTA FedState E-File Symposium

May 3, 2000

Agenda

• Survey Methodology

• Executive Summary

• Profiles

• Factors Influencing E-filing

• Future Trends

• Recommendations

Survey Methodology

• September 1999, CERCA commissioned Mellman Group to survey 579 tax practitioners by telephone

• Sample was obtained using an IRS listing of tax preparers

• Selection criteria of tax practitioners – Prepared and filed tax

returns in TY98

– Used tax software to prepare the majority of tax returns

– Must be aware of the e-filing program

Objectives

• Examine current and future e-file market & ways to increase tax practitioner e-file – Profile e-filers to assess current and future

market – Understand how and why practitioners’ use e-

file– Explore incentives, barriers, and other factors

that could impact future of e-file

Executive Summary

• E-file market significant and can be expected to grow significantly next tax year– 33% e-filed in TY98– 28% expect to join in TY99

• E-filers believe in the program – 97% of 1998 filers plan to e- file again in 1999 – Also plan to file more returns than last year

Executive Summary

• Great potential to expand the market – 33% currently e- file less than 50% their returns

Customer demand and cost-benefit analysis driving practitioners’ decisions on e-filing Don’t e-file because clients are not interested

and benefit not worth the additional effort

Executive Summary

• Some current e-filers put off by transmission fees, time investment, and cumbersome application process

• But 37% would e-file business returns

• Key benefits as incentives to e-file – Tax credits for clients– Ability to electronically access client account

status at IRS

Market Definition

• Almost all practitioners aware of e-filing (1% unaware)

• Nearly 60% of e-filers are “heavy” filers --using e-filing for over half of their returns

• About 25% e-filers file over 80% of eligible federal returns electronically

• Average e-filer filed 45% of their eligible federal returns electronically

Market Definition

• Fewer state returns e-filed– Typical e-filer files 29% of eligible state returns

• Compared to the 45% of federal returns

– 15% e-file over 80% of their state returns– 72% e-file less than half of eligible state returns

E-file Profiles

• More likely to be tax preparers than CPAs– Over 40% of e-filers were tax preparers– 30% of e-filers were CPAs vs. 50% non-e-filers

Segments who e-file more than 50% eligible returns: 56% practitioners <10 years experience– 38% with 10-20 years experience – 27% with over 20 years experience

E-filer Profiles

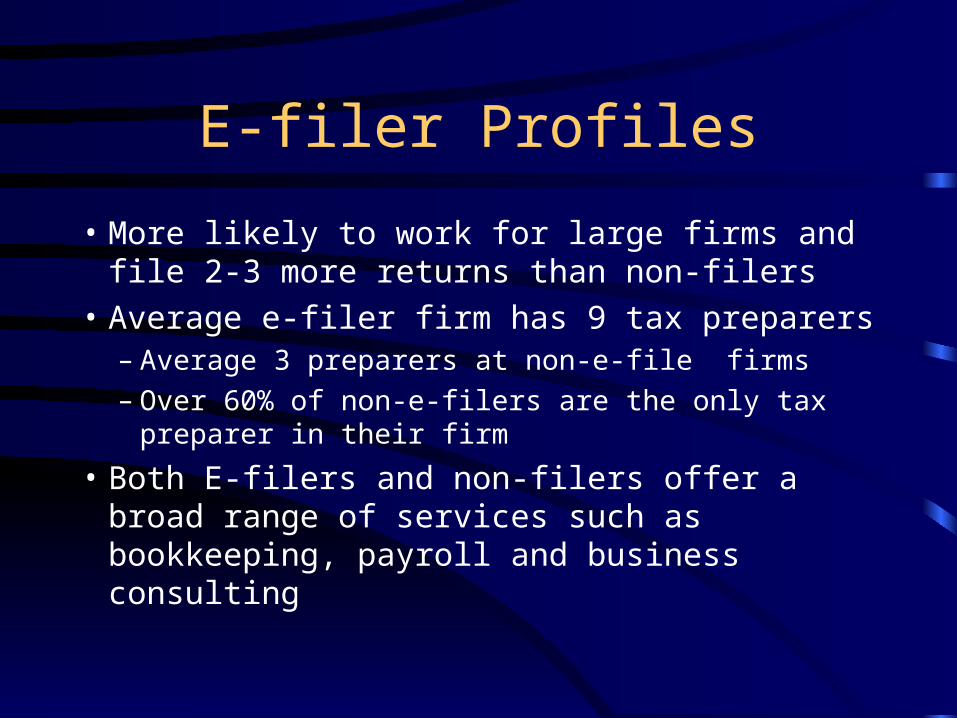

• More likely to work for large firms and file 2-3 more returns than non-filers

• Average e-filer firm has 9 tax preparers – Average 3 preparers at non-e-file firms– Over 60% of non-e-filers are the only tax preparer in

their firm

• Both E-filers and non-filers offer a broad range of services such as bookkeeping, payroll and business consulting

Heavy E-filers

• Heavy e-filers tend to focus more on individual tax returns– 26% filed more than

500 1040’s in TY98

– 50% filed more than 190 1040’s

• Only 5% non-e-filers filed >500 1040’s

• Heavy e-filers tend to– Not charge a separate

fee (20%) and include the fee in their tax prep charge (44%)

– Offer RALS (66%) and,

– Offer other bank refund products

Proportion of EligibleReturns Filed

E-filers(n=303)

Least ExperiencedPractitioners

(n=63)

MostExperiencedPractitioners

(n=90)RATE OF FEDERAL E-FILING

Average 46% 62% 35% 1%-30% 43% 22% 58% 31% - 50% 12% 13% 10% 51%-100% 38% 56% 27%RATE OF STATE E-FILING

Average 29% 40% 25% 0% 44% 38% 38% 1%-30% 21% 15% 32% 31% - 50% 7% 8% 4% 51%-100% 25% 32% 17%

Market Definition

E-file ServicesService Offered Tax Practitioners

(e-filed TY98)(n=138)

Heavy E-filers(e-filed TY98)

(n=166)

Light E-filers(e-filed TY98)

(n=116)OFFERED E-FILING

To most clients 73% 93% 66% Only if refund expected 25% 7% 32%CHARGED FEE FOR FEDERAL E-FILING?

Yes 45% 34% 57% No 16% 20% 10% Include in tax prep fee 37% 44% 33%CHARGED FEE FORSTATE E-FILING?

(n=73) (n=82) (n=81)

Yes 41% 48% 47% No 37% 43% 31% Include in tax prep fee 19% 9% 20%OFFERED RALS?

Yes 34% 66% 21% No 66% 34% 79%OFFERED OTHER BANK REFUND PRODUCTS?

Yes 28% 53% 14% No 71% 45% 84%

To E-File or Not -- Key Factors

Education is Key

• Reasons given for not e-filing point to the need for a campaign to educate taxpayers and practitioners about electronic filing process– Highlight possible improvements in the

program

Value Proposition?

• Non-e-filers cite insufficient value for clients compared to the increased cost in time and effort to the practitioner and clients’ lack of interest as their top two reasons for not filing – Cited by over 50% non-filers

Information Crucial

• Lack of information and discomfort with security issues are significant barriers– ~40% non-e-filers unsure of participation

criteria– ~40% uncomfortable sending taxpayer data

electronically

Costs & Cumbersome Procedures

• E-file transmission fees were the second most frequently cited reason not to e-file by e-filers

• Similar numbers of both e-filers and non-e-filers agree that the ERO application process and procedures are too cumbersome

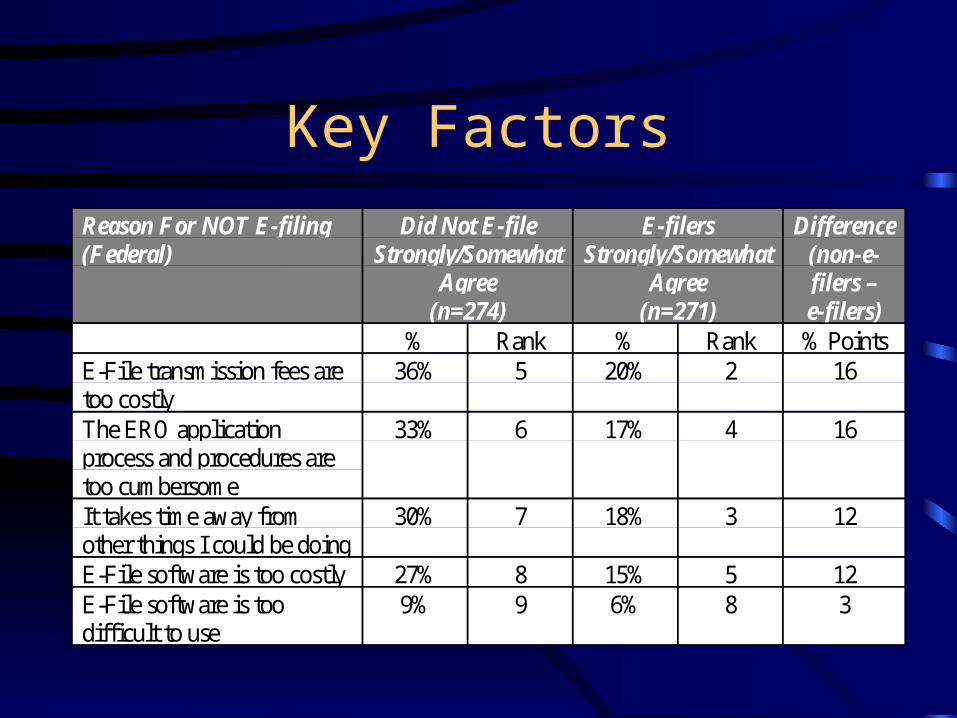

Key FactorsReason For NOT E-filing(Federal)

Did Not E-fileStrongly/Somewhat

Agree(n=274)

E-filersStrongly/Somewhat

Agree(n=271)

Difference(non-e-filers –e-filers)

% Rank % Rank % PointsThe benefit to my clients isnot worth my effort

54% 1 14% 6 40

My clients are not interestedin E-Filing when I offer it tothem

50% 2 32% 1 18

I am not sure what thecriteria is for me toparticipate in IRS E-Fileprogram

38% 3 4% 10 34

I am not comfortablesending taxpayer dataelectronically

37% 4 6% 7 31

Key Factors

Reason For NOT E-filing(Federal)

Did Not E-fileStrongly/Somewhat

Agree(n=274)

E-filersStrongly/Somewhat

Agree(n=271)

Difference(non-e-filers –e-filers)

% Rank % Rank % PointsE-File transmission fees aretoo costly

36% 5 20% 2 16

The ERO applicationprocess and procedures aretoo cumbersome

33% 6 17% 4 16

It takes time away fromother things I could be doing

30% 7 18% 3 12

E-File software is too costly 27% 8 15% 5 12E-File software is toodifficult to use

9% 9 6% 8 3

Key FactorsReason For NOT E-filing(Federal)

Did Not E-fileStrongly/Somewhat

Agree(n=274)

E-filersStrongly/Somewhat

Agree(n=271)

Difference(non-e-filers –e-filers)

% Rank % Rank % PointsI am concerned I might losemy Circular 230/EROprivileges if IRS does notaccept me as an ERO

6% 10 5% 9 1

I am concerned aboutpossible suspension and/orincreased visits by IRS CIDafter being approved

6% 11 3% 12 3

I am concerned aboutincreasing the likelihood ofan audit by IRS

6% 12 4% 11 2

I do not have a modem 5% 13 -- 13 5

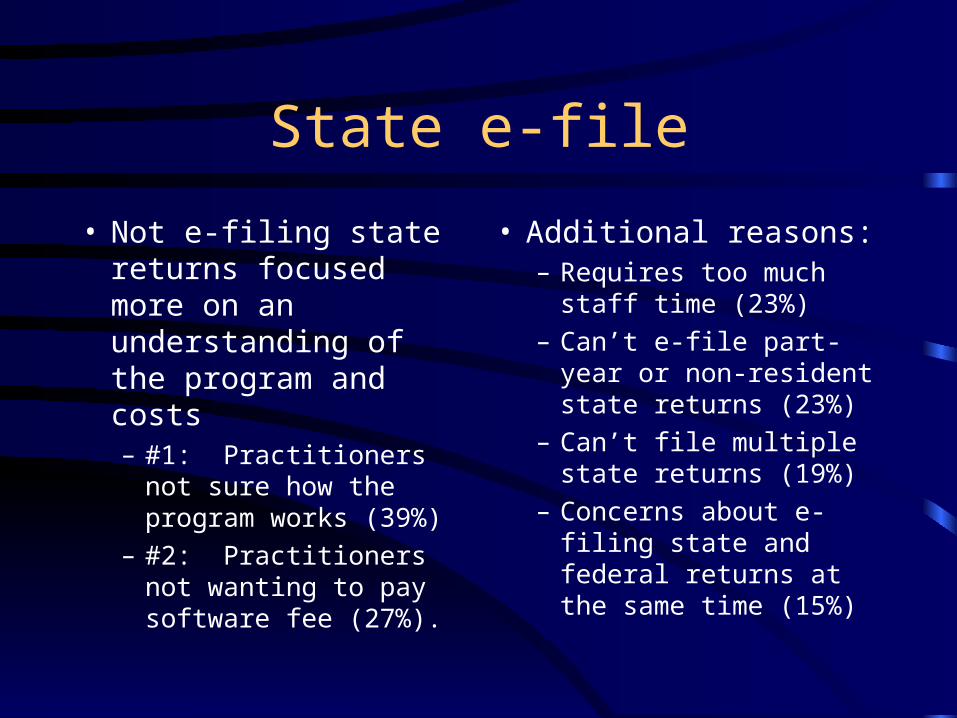

State e-file

• Not e-filing state returns focused more on an understanding of the program and costs– #1: Practitioners not

sure how the program works (39%)

– #2: Practitioners not wanting to pay software fee (27%).

• Additional reasons:– Requires too much staff

time (23%)– Can’t e-file part-year or

non-resident state returns (23%)

– Can’t file multiple state returns (19%)

– Concerns about e-filing state and federal returns at the same time (15%)

E-file Increase is Coming

Significant e-file increase for TY99

• Over 60% likely to e-file for TY99– >40% “almost certain” to do so

• Significant increase over 30% currently filing

– 42% who did not e-file in TY98 likely to e-file in TY99

Current e-filers will file more

• 97% will e-file again in 1999 – 90% responded “almost certain” – 61% plan file more returns– 38% will file the same number– None plan to file fewer returns

Why e-file more?

• Customer demand is the leading reason current e-filers plan to e-file more – >50% indicated e-file increase cited increased

customer demand as reason– 25% cited increase in their own base of clients– >10% cited increased comfort with the process– 2% expect to file more refund due returns.

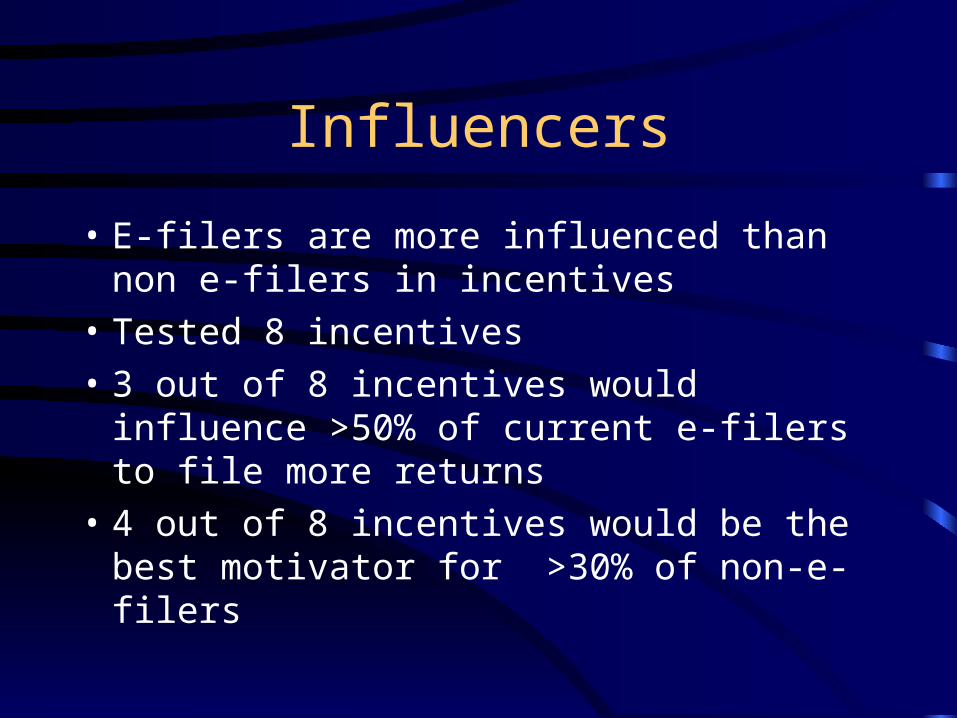

Influencers

• E-filers are more influenced than non e-filers in incentives

• Tested 8 incentives

• 3 out of 8 incentives would influence >50% of current e-filers to file more returns

• 4 out of 8 incentives would be the best motivator for >30% of non-e-filers

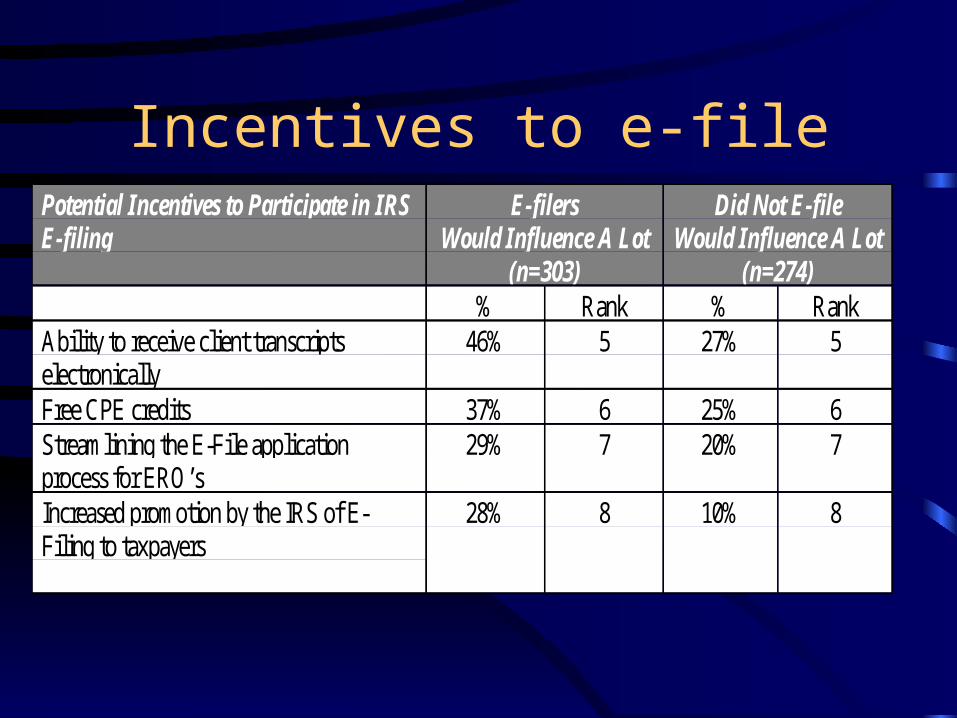

Incentives to e-filePotential Incentives to Participate in IRSE-filing

E-filersWould Influence A Lot

(n=303)

Did Not E-fileWould Influence A Lot

(n=274)% Rank % Rank

To be able to electronically access accountstatus for your clients at the IRS

56% 1 39% 1

To be able to electronically correspondwith the IRS about your clients accounts

56% 2 34% 3

A tax credit on your clients return if E-Filed

54% 3 36% 2

To be able to file Power of Attorneysand/or tax information authorizationselectronically

47% 4 34% 4

Incentives to e-filePotential Incentives to Participate in IRSE-filing

E-filersWould Influence A Lot

(n=303)

Did Not E-fileWould Influence A Lot

(n=274)% Rank % Rank

Ability to receive client transcriptselectronically

46% 5 27% 5

Free CPE credits 37% 6 25% 6Streamlining the E-File applicationprocess for ERO’s

29% 7 20% 7

Increased promotion by the IRS of E-Filing to taxpayers

28% 8 10% 8

Frequent e-file Program of Interest

• 33% overall practitioners interested – 11% of those “very” interested– Marginally rises to 38% if criteria is % eligible

returns e-filed

• 45% overall practitioners very disinterested

• 53% e-filers interested in such a program– 26% of those are “very” interested – 33% of e-filers “very” disinterested

Business e-file Important

• Overall, 37% who currently prepare business returns would e-file them– 60% would not, including 49% not at all likely

• 55% current e-filers would e-file– 58% heavy e-filers say they would e-file,

including• 49% of those with < 10 years experience

• 43% of tax preparers

Recommendations

• Continue and increase information to practitioners of e-file ease and benefits

• Continue and increase taxpayer education of e-file ease and benefits

• Reduce procedural barriers

• Provide incentive structure