central europe investor relations conference 2 july 2001

DESCRIPTION

Central Europe Investor Relations Conference 2 July 2001. Herman Agneessen s Member of the EC. Central Europe. Mission Statement Acquisitions to date Guiding management concepts Financial Results Financial Objectives SWOT analysis Asset Quality Efficiency initiatives Current IPB status. - PowerPoint PPT PresentationTRANSCRIPT

Central Europe

Investor Relations Conference2 July 2001

Herman AgneessensMember of the EC

2

Central Europe

Mission Statement

Acquisitions to date

Guiding management concepts

Financial Results

Financial Objectives

SWOT analysis

Asset Quality

Efficiency initiatives

Current IPB status

To

pic

s

Central Europe Mission Statement

Create a second home market

In future EU member-countries

For bankinsurance activities

On a segmented basis

In KBC’s 4 activitity areas

4

Kredyt bankAgropolisaWarta

CSOBCSOB Poijst'ovnaPatria

K&H BankK&H LifeArgosz

5

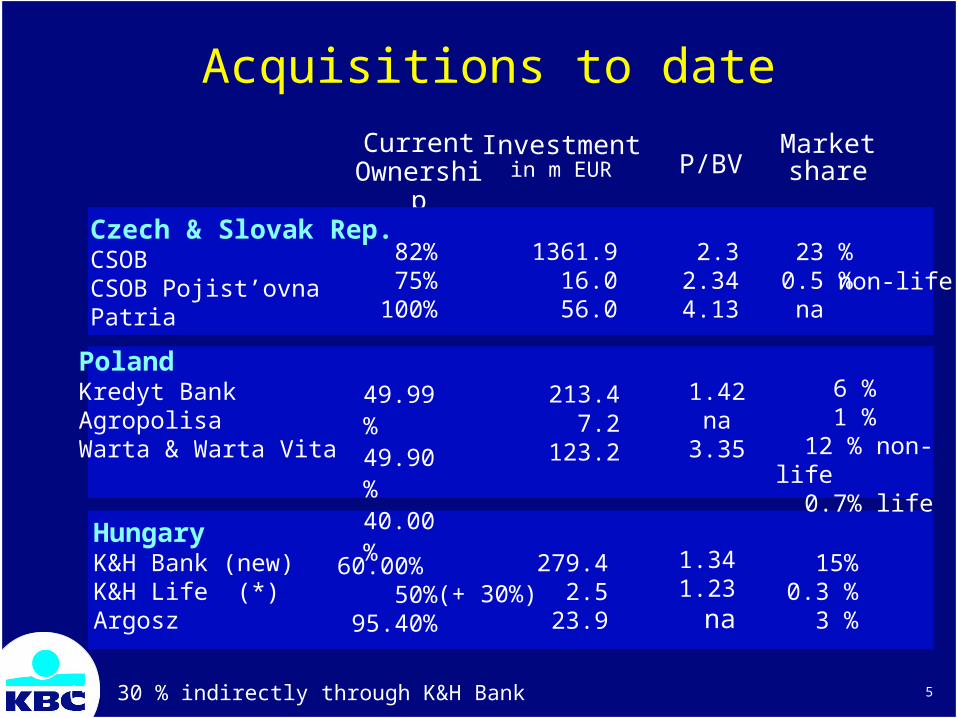

Acquisitions to date

PolandKredyt BankAgropolisaWarta & Warta Vita

HungaryK&H Bank (new)K&H Life (*)Argosz

49.99%49.90%40.00%

60.00% 50%

95.40%

CurrentOwnership

213.47.2

123.2

279.42.5

23.9

Investmentin m EUR

6 % 1 % 12 % non-life 0.7% life

15%0.3 %

3 %

Market share P/BV

1.42na

3.35

1.341.23

na

(*) 30 % indirectly through K&H Bank

Czech & Slovak Rep.CSOBCSOB Pojist’ovnaPatria

82%75%

100%

1361.916.056.0

23 %0.5 %

na

2.32.344.13

non-life

(+ 30%)

Central Europe

Total investment : EUR 2,084 million

banking EUR 1,911 million

insurance EUR 173 million

7

Guiding management conceptsCareful balance between autonomy and control

Branding policy : customer identification

Strong local management input

Strict central control requirements Credit/insurance risks, market risks, operational integrity Internal audit & compliance principles KBC reporting standards

Maximisation of synergies IT, payment systems, operational efficiency Bankinsurance, markets & asset management know-how “best group practices”

8

Financial results 1Q01

m EUR Y2000 1Q01

CSOB 116.1 78.7

K&H Bank 3.8 0.2

Kredyt Bank 46.8 15.5

p.m. Patria n/a 0.2

Stand alone results banks

9

Financial results 1Q01- Banking

Net profit (m EUR)

Share in group profit

Return on alloc. equity

Share in alloc. equity

Cost/Income ratio

60.0

16.9%

44.4%

10.1%

59.4%

40.0

11.9%

29.0%

10.1%

59.4%

30.5

9.7%

16.6%

8.7%

59.3%

External (1)

External (2)Normalized Internal(3)

(1) external: after minorities and funding cost(2) ext. normalized: excluding 20 m EUR except. loan loss recoveries(3) internal : including FGBR and amortization of goodwill over 20 yrs

10

Financial results 1Q01

m EUR Y2000 1Q01

CSOB Poijst'ovna -1.6 +1.0

K&H Life -0.2 -0.04

Argosz +0.05 +0.2

Warta -7.2 +0.03

Stand alone results insurance

11

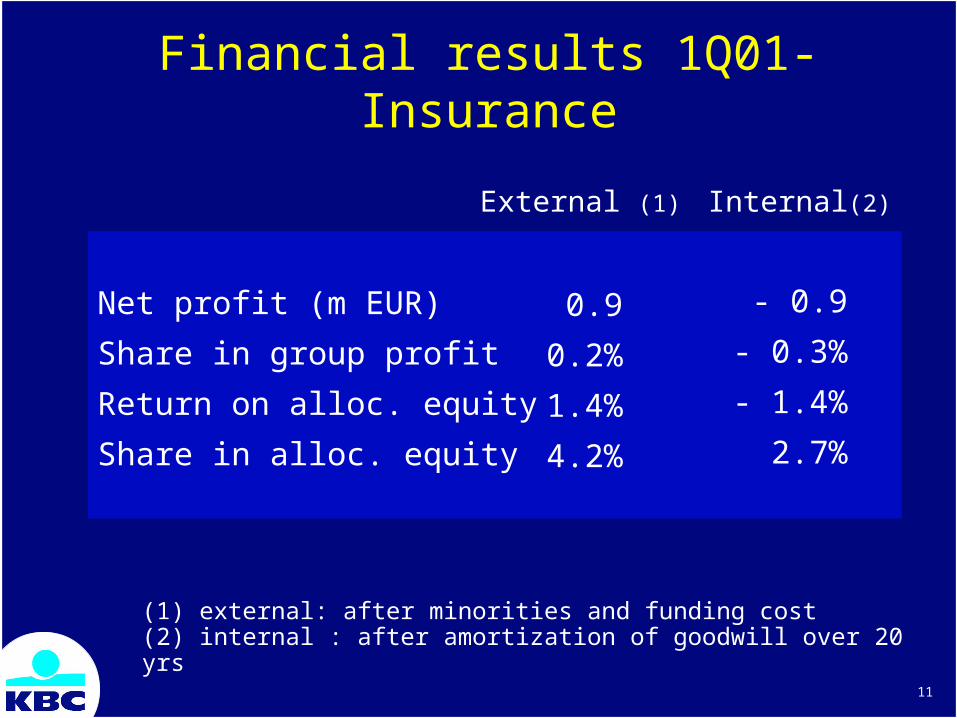

Financial results 1Q01- Insurance

Net profit (m EUR)

Share in group profit

Return on alloc. equity

Share in alloc. equity

0.9

0.2%

1.4%

4.2%

- 0.9

- 0.3%

- 1.4%

2.7%

External (1) Internal(2)

(1) external: after minorities and funding cost(2) internal : after amortization of goodwill over 20 yrs

12

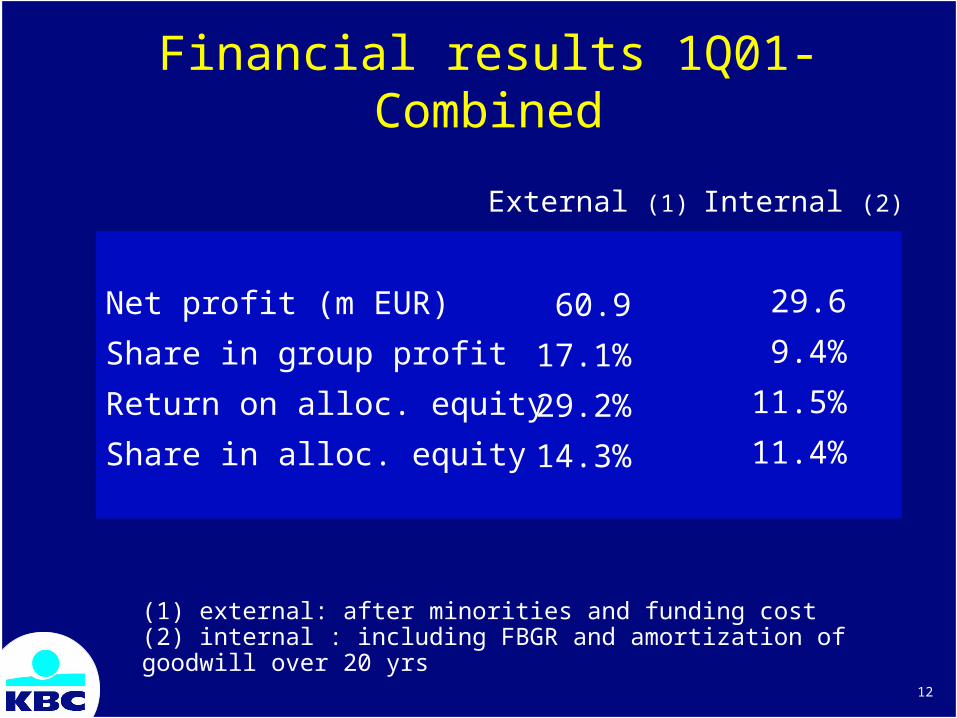

Financial results 1Q01- Combined

Net profit (m EUR)

Share in group profit

Return on alloc. equity

Share in alloc. equity

60.9

17.1%

29.2%

14.3%

29.6

9.4%

11.5%

11.4%

External (1) Internal (2)

(1) external: after minorities and funding cost(2) internal : including FBGR and amortization of goodwill over 20 yrs

13

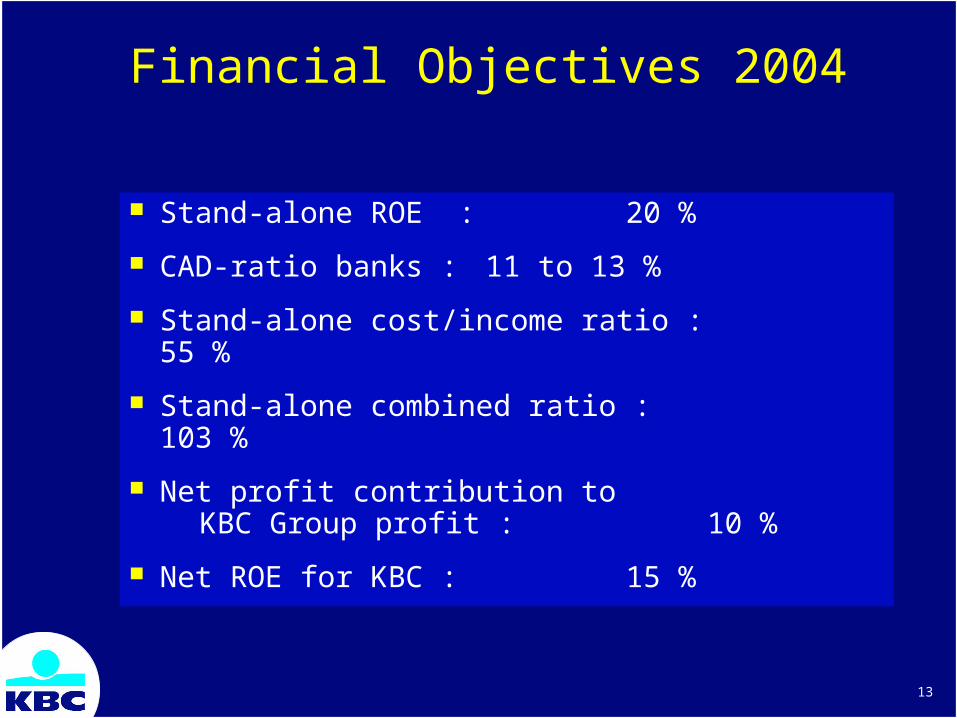

Financial Objectives 2004

Stand-alone ROE : 20 %

CAD-ratio banks : 11 to 13 %

Stand-alone cost/income ratio : 55 %

Stand-alone combined ratio : 103 %

Net profit contribution to KBC Group profit : 10 %

Net ROE for KBC : 15 %

14

KBC’s major strenghts in CE

Strong banking franchises at competitive cost

Strong insurance franchise in Poland, …. perhaps also in Czech Republic

Good to strong local management teams

Segmentation already introduced

Early entrant in integrated bankinsurance

Positive profit potential outlook

Eu-joining of chosen countries well underway

15

KBC’s major weaknesses in CE

Mostly inadequate IT-infrastructures

Insufficient customer orientation

Insufficient productivity & efficiency levels

Unequal risk-awareness & asset quality levels

Insufficient existing product offerings

Critical mass not available in all countries

Banks insufficiently strong in retail

16

KBC’s major opportunities in CE

Above average (western) growth outlook Country GDP as such Country GDP because of eu-joining GDP per capita Savings ratio Customer switch to higher value added products

Policy of combining local brand & local management with strong shareholder resp. know-how provider

Largely undeveloped SME / Asset Management / bankassurance markets - areas of KBC expertise

Domestic capital markets waiting to be developed

17

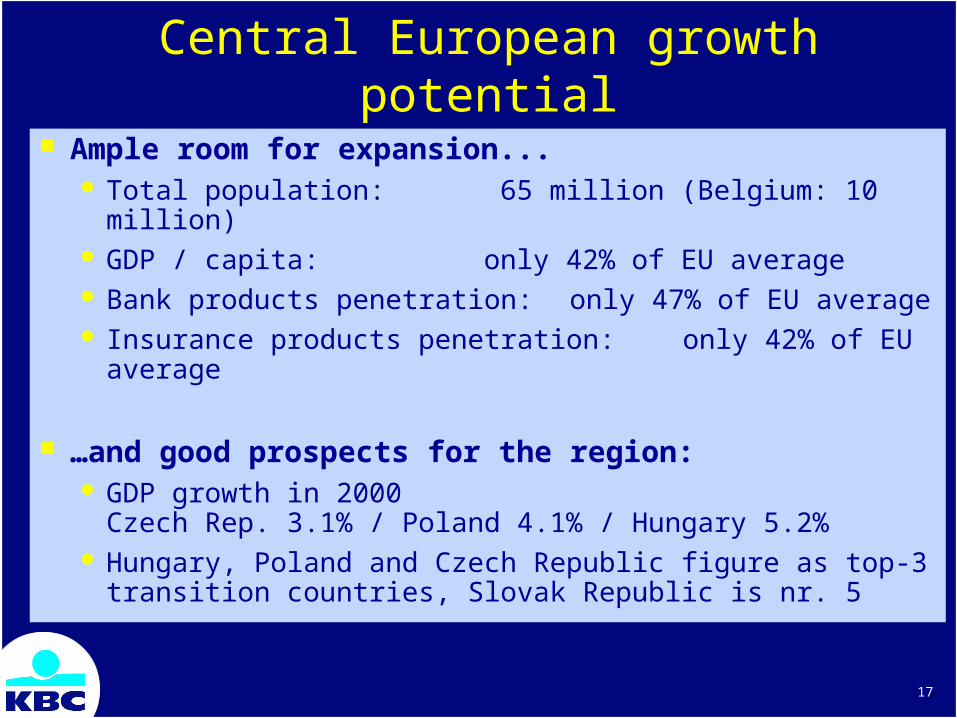

Central European growth potential

Ample room for expansion... Total population: 65 million (Belgium: 10 million) GDP / capita: only 42% of EU average Bank products penetration: only 47% of EU average Insurance products penetration: only 42% of EU average

…and good prospects for the region: GDP growth in 2000

Czech Rep. 3.1% / Poland 4.1% / Hungary 5.2% Hungary, Poland and Czech Republic figure as top-3 transition

countries, Slovak Republic is nr. 5

18

KBC’s major threats The competition has woken up ! IT-renewal is a major challenge Large-scale employee education is a must Change management must be concluded

successfully Bank-mergers in czech republic and hungary Network expansion in slovak and polish banks Implementation of integrated bankinsurance concept New IT = new processes = “rationalizing yourself away” Productivity increase requirements Ensure adequate customer orientation Need to significantly enlarge existing product-offerings Develop & control new products in an untested environment

19

Current Bank Asset Quality

% watch31.12.00

% NPL31.12.00

% watch31.3.01

% NPL31.3.01

CSOB "new" 9.0% 1.7% 11.5% 2.0%

CSOB "historic" 100.0% 87.7% 95.8% 78.7%

K&H 11.0% 3.6% 5.8% 2.1%

KB corporate 11.9% 5.7% 14.8% 5.2%

KB consumers 5.0% - . 4.8% - .

KBC Bank cons. 2.9% 1.7% 2.2% 1.5%

20

Efficiency initiatives - CSOB (CR only)

.

8 901

7 997 (-10.1%)

6 597 (- 25.9%)

2.2 m EUR

15.1 m EUR

CSOB + IPB staff June 2000 :

CSOB + IPB staff now :

CSOB + IPB staff Dec. 2001 :

Estimated lay-off costs :

Est. recurrent savings p.a. :

21

Efficiency initiatives - K&H Bank

K&H+AAM staff 30/08/00 : 5.174

K&H+AAM staff 31/05/01 : 4.468 (- 13.7 %)

K&H+AAM staff 31/12/01 : 3.939 (- 24.9 %)

K&H+AAM staff 31/12/02 : 3.400 (- 34.3 %)

K&H+AAM staff 31/12/03 : 3.000 (- 42.0 %)

estimated lay-off costs : 10.0 m EUR

est. recurrent savings p/a : 11.4 m EUR

22

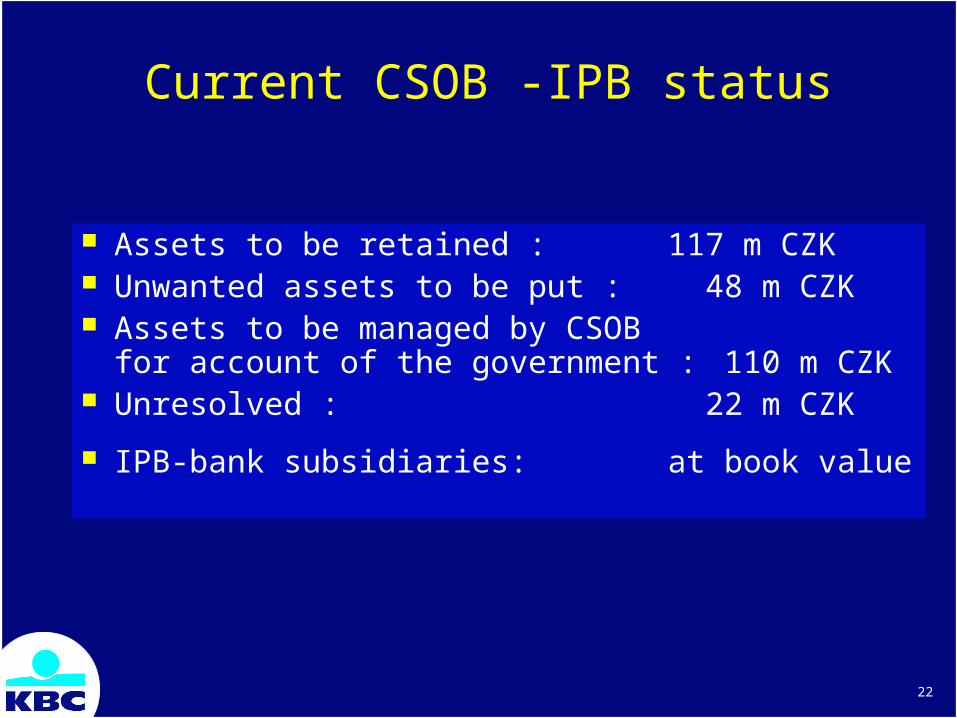

Current CSOB -IPB status

Assets to be retained : 117 m CZK Unwanted assets to be put : 48 m CZK Assets to be managed by CSOB

for account of the government : 110 m CZK Unresolved : 22 m CZK

IPB-bank subsidiaries: at book value

23

Remaining CSOB / IPB issues

IPB Pojistovna : ownership

Pension fund : ownership

37 % IT affiliate PVT : modalities

Central Europe

Investor Relations Conference2 July 2001

Herman AgneessensMember of the EC

25

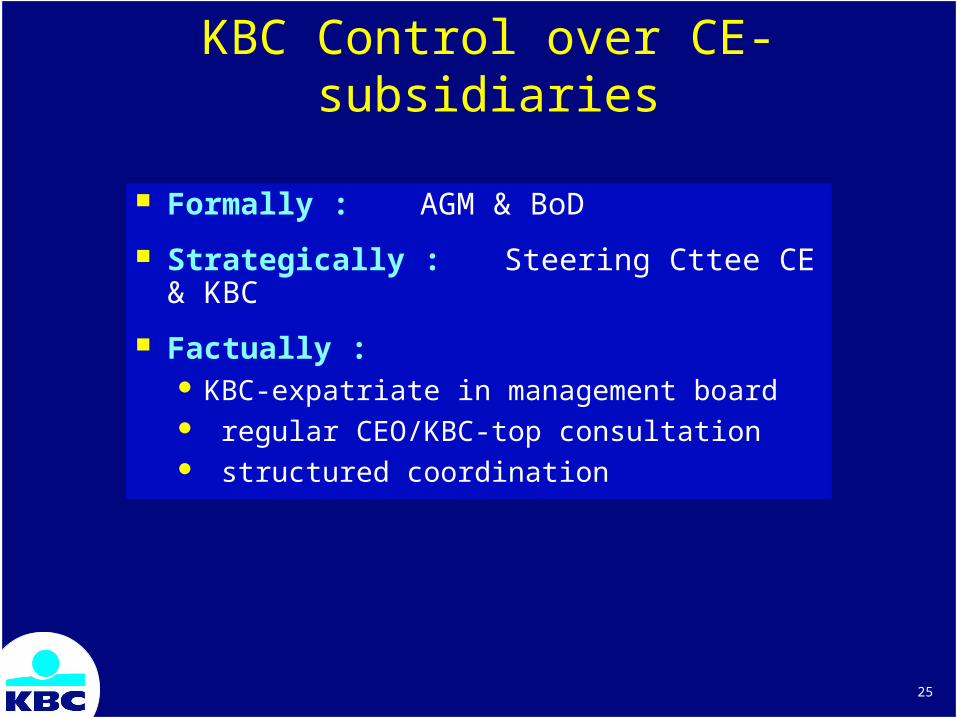

KBC Control over CE-subsidiaries

Formally : AGM & BoD

Strategically : Steering Cttee CE & KBC

Factually : KBC-expatriate in management board regular CEO/KBC-top consultation structured coordination

26

KBC-control : structured coordination

Full-time regional KBC CE-coordinators for : Overall coordination Market activities Internal Audit Market Risk Management Retail bankinsurance Information technology

27

KBC-control : structured coordination

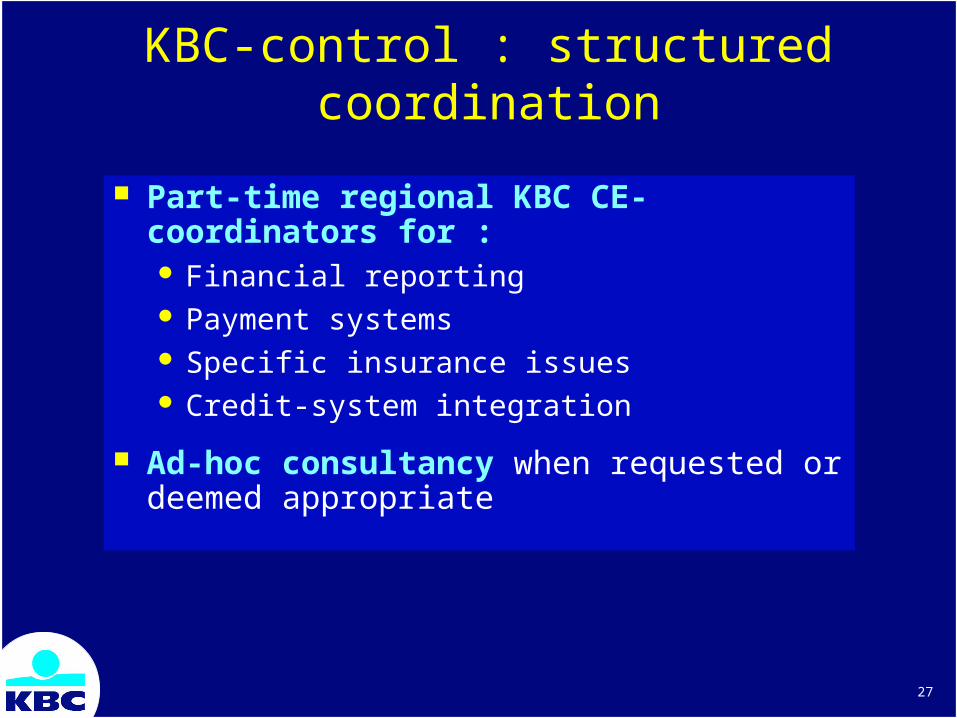

Part-time regional KBC CE-coordinators for : Financial reporting Payment systems Specific insurance issues Credit-system integration

Ad-hoc consultancy when requested ordeemed appropriate

Central Europe

Investor Relations Conference2 July 2001

Herman AgneessensMember of the EC