central bank independence in resource-rich economies - hoda selim

TRANSCRIPT

ARE CENTRAL BANKS OF ARABCOMMODITY EXPORTERS

INDEPENDENT? DOES IT MATTER?

Hoda Selim, Economic Research Forum (ERF)

Presentation for the conference on

Monetary and Fiscal Institutions in Resource-Rich Arab Economies

November 4-5, 2015Kuwait city, Kuwait

MOTIVATION

Arab central banks are exposed to oil price shocks

Monetary policy operates in a volatile context:

Pressures on the real exchange rate Pro-cyclical capital flows and risks of asset

price bubbles

Monetary policy operates in an uncertain context which complicates the forecasting of growth and its role in macro stabilization.

They have less developed institutions (central banks) and a low stock of credibility that could affect policy effectiveness.

2

Provide a comparative analysis of current central bank legislations in oil rich-Arab economies and Chile (copper-exporter).

To what extent are Arab central banks independent? transparent ? accountable?

Does CBI matter for macro outcomes in all Arab commodity exporters?

OBJECTIVE

3

I. Country coverage

II.Measuring independence

III.Independence of Arab monetary institutions: An answer from legislations

IV.Central banks and macro outcomes: was it independence?

V.Concluding remarks

OUTLINE

4

I. Country coverage

II.Measuring independence

III.Independence of Arab monetary institutions: An answer from legislations

IV.Central banks and macro outcomes: was it independence?

V.Concluding remarks

OUTLINE

5

COUNTRY COVERAGE

Oil-dependent Arab economies are divided into 2 groups: High rent/capita: GCC (close to US$ 74,000) Low rent per capita: Algeria, Sudan and Yemen: (US$

642) Chile: US$ 2,529

Source: Calculated by the authors based on data from the World Development Indicators and national statistical offices.No old data for Qatar and UAE.

Natural resource rent per capita (current US$)

26,0

68

5,38

9

3,82

8

11,3

89

27

0 0 102.

3

223,

096

89,5

76

92,4

83

17,0

31

13,9

54

12,6

04

1,55

0.2

154.

4

222.

4

2,52

9

0

50,000

100,000

150,000

200,000

250,000

Qat

ar

Kuw

ait

UAE

Sau

di A

rabi

a

Om

an

Bah

rain

Alg

eria

Sud

an

Yem

en

Chi

le

1970s/1980s 2013

6

I. Country coverage

II.Measuring independence

III.Independence of Arab monetary institutions: An answer from legislations

IV.CBI and macro outcomes

V.Concluding remarks

OUTLINE

7

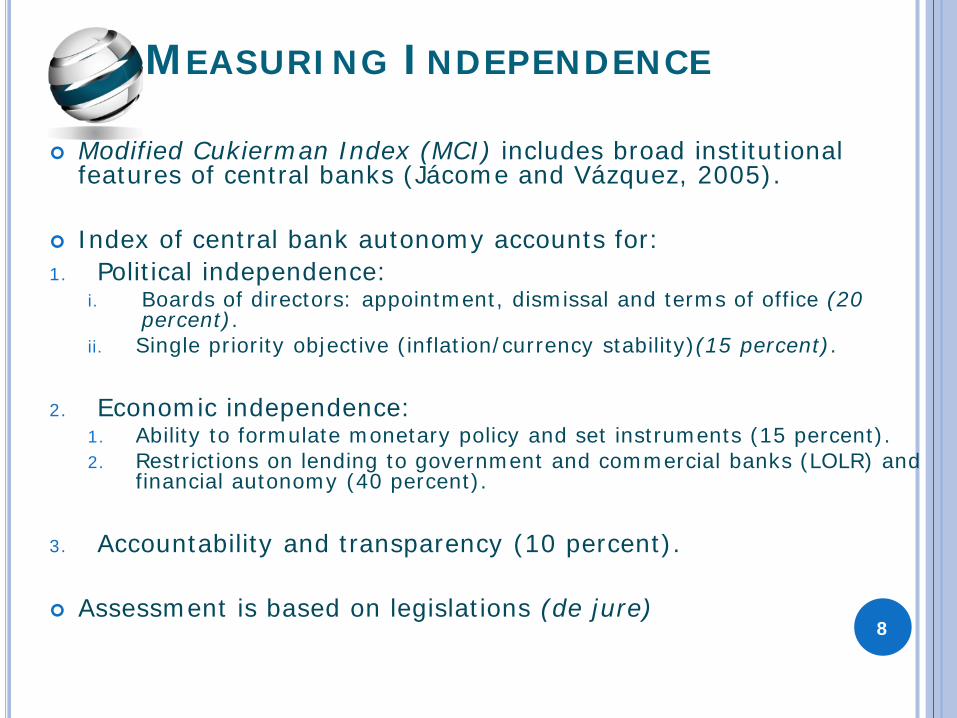

MEASURING INDEPENDENCE

Modified Cukierman Index (MCI) includes broad institutional features of central banks (Jácome and Vázquez, 2005).

Index of central bank autonomy accounts for:1. Political independence:

i. Boards of directors: appointment, dismissal and terms of office (20 percent).

ii. Single priority objective (inflation/currency stability)(15 percent).

2. Economic independence:1. Ability to formulate monetary policy and set instruments (15 percent).2. Restrictions on lending to government and commercial banks (LOLR) and

financial autonomy (40 percent).

3. Accountability and transparency (10 percent).

Assessment is based on legislations (de jure)8

I. Country coverage

II.Measuring independence

III.Independence of Arab monetary institutions: An answer from legislations

IV.Central banks and macro outcomes: was it independence?

V.Concluding remarks

OUTLINE

9

CBI: AN ANSWER FROM LEGISLATIONS

I. Political Independence

CBC is the most politically independent: Double-veto process for appointment and dismissal of governor and board members, thus providing credibility and stability beyond the political cycle.

These processes in the majority of Arab central banks are strongly influenced by the government.

Legal central bank independence: political independence

Source: constructed by the authors based on central bank legislations

00.20.40.60.8

11.2

Bahr

ain

Kuw

ait

Om

an

Qat

ar

KSA

UAE

Alge

ria

Suda

n

Yem

en

Chile

Central bank boards Central bank primary objective

10

CBI: POLITICAL INDEPENDENCE

A closer look at Arab central bank boards

Governors’ terms of office are usually shorter than that of the executive governments, responsible for the appointment One exception is Kuwait: 5-year term for governor vs. 4-year term for FM

Governors and board members are appointed by the executive without the involvement of the legislature.

Dismissal does not require the approval of the legislature or the ruling of an independent tribunal. SAMA: dismissal could be arbitrary.

11

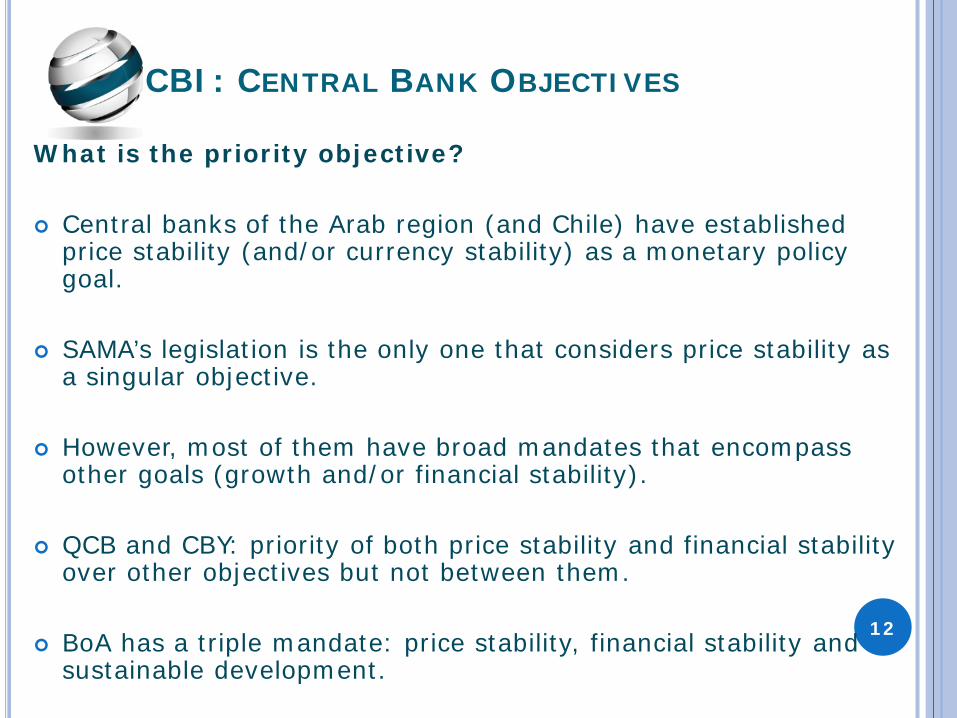

CBI: CENTRAL BANK OBJECTIVES

What is the priority objective?

Central banks of the Arab region (and Chile) have established price stability (and/or currency stability) as a monetary policy goal.

SAMA’s legislation is the only one that considers price stability as a singular objective.

However, most of them have broad mandates that encompass other goals (growth and/or financial stability).

QCB and CBY: priority of both price stability and financial stability over other objectives but not between them.

BoA has a triple mandate: price stability, financial stability and sustainable development.

12

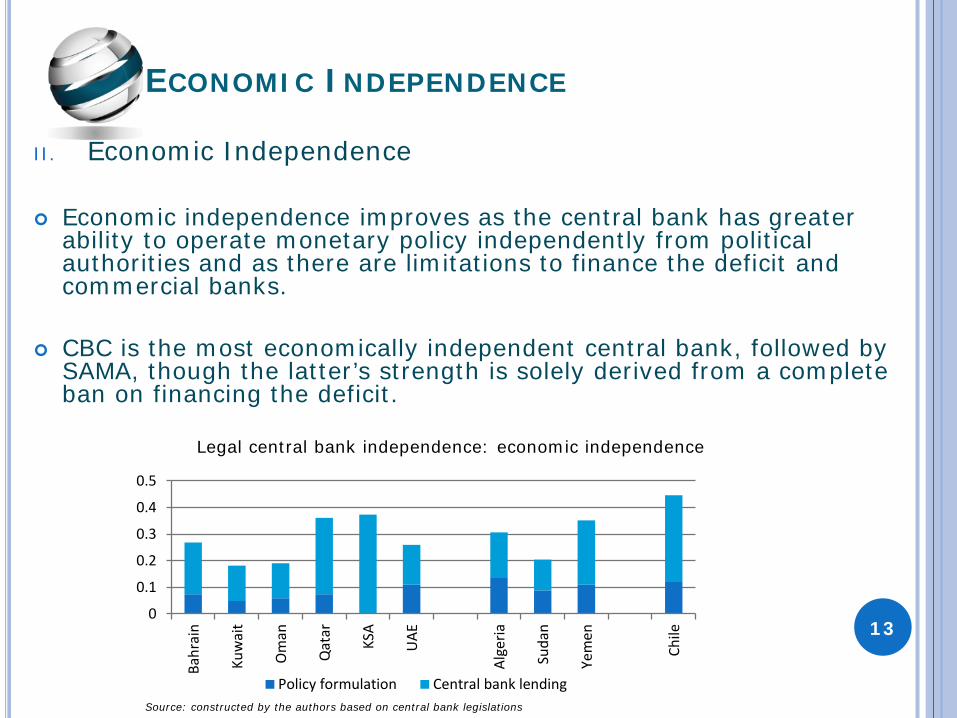

ECONOMIC INDEPENDENCE

II. Economic Independence

Economic independence improves as the central bank has greater ability to operate monetary policy independently from political authorities and as there are limitations to finance the deficit and commercial banks.

CBC is the most economically independent central bank, followed by SAMA, though the latter’s strength is solely derived from a complete ban on financing the deficit.

Legal central bank independence: economic independence

Source: constructed by the authors based on central bank legislations

0

0.1

0.2

0.3

0.4

0.5

Bahr

ain

Kuw

ait

Om

an

Qat

ar

KSA

UAE

Alge

ria

Suda

n

Yem

en

Chile

Policy formulation Central bank lending

13

CBI: GOAL VS. INSTRUMENT INDEPENDENCE

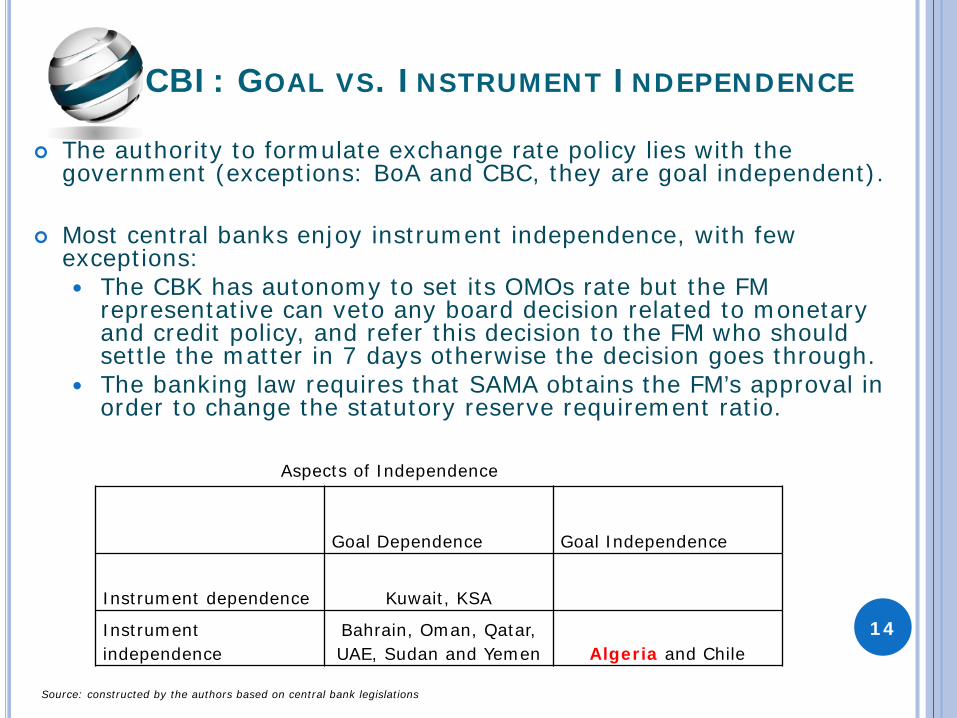

The authority to formulate exchange rate policy lies with the government (exceptions: BoA and CBC, they are goal independent).

Most central banks enjoy instrument independence, with few exceptions: The CBK has autonomy to set its OMOs rate but the FM

representative can veto any board decision related to monetary and credit policy, and refer this decision to the FM who should settle the matter in 7 days otherwise the decision goes through.

The banking law requires that SAMA obtains the FM’s approval in order to change the statutory reserve requirement ratio.

Goal Dependence Goal Independence

Instrument dependence Kuwait, KSA

Instrument independence

Bahrain, Oman, Qatar, UAE, Sudan and Yemen Algeria and Chile

Aspects of Independence

Source: constructed by the authors based on central bank legislations

14

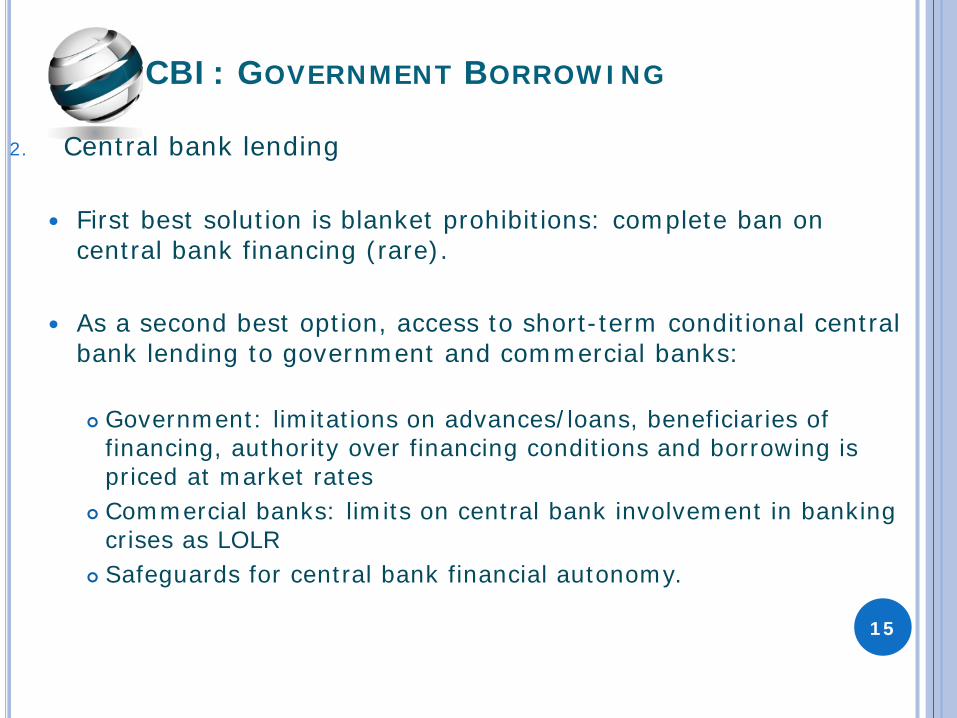

2. Central bank lending

First best solution is blanket prohibitions: complete ban on central bank financing (rare).

As a second best option, access to short-term conditional central bank lending to government and commercial banks:

Government: limitations on advances/loans, beneficiaries of financing, authority over financing conditions and borrowing is priced at market rates

Commercial banks: limits on central bank involvement in banking crises as LOLR

Safeguards for central bank financial autonomy.

CBI: GOVERNMENT BORROWING

15

Blanket prohibitions are present for SAMA and CBC. Conditional government borrowing is allowed in others

The limits hover around 10% of some definition of revenue: QCB (5% of average revenue of past 3 years) vs. CBB and CBY (at 25% of expenditure/revenue).

Repayment takes up to longer than a year, going up to two years for the CBUAE vs. 90 days for the CBO.

CBI: GOVERNMENT BORROWING

0.000.200.400.600.801.00

Bah

rain

Kuw

ait

Om

an

Qat

ar

KSA

UAE

Alg

eria

Sud

an

Yem

en

Chi

legovernment credit index LOLR Financial autonomy

Legal central bank independence: central bank lending

Source: constructed by the authors based on central bank legislations

16

Interest conditions are often negotiated with the government. In UAE, interest-free financing.

Central bank advances benefit the governments except in Bahrain where they are extended to public corporations after the approval of the FM.

SAMA and CBC are prohibited from holding public debt.

QCB and CBY are restricted to purchasing debt in the secondary market.

Other central banks are allowed to purchase public in the primary market.

CBI: BORROWING CONDITIONS

Central Bank negotiated with

governmentBelow market

ratesNo legal

provisions

Bahrain, Qatar

Kuwait, Algeria, Sudan and Yemen

UAE (interest-free) Oman

Loan conditions

Source: constructed by the author based on central bank legislations

17

LOLR: The provision of emergency liquidity is present in all legislations

(except SAMA’s). Such function is not always tied to illiquid financial institutions

(CBB, CBK and QCB).

The CBC has two liquidity facilities to banks: one is tied to emergency liquidity for a period of 90 days to banks with “difficulties arising out of a temporary liquidity shortage.” However, the second credit facility may be providing finance for bank restructuring.

Financial autonomy:

The legislations of the CBK and SAMA do not allow the government to capitalize the central banks.

Law does not state that CBK has a financial autonomy and the CBK board’s decisions on regulations related to financial and administrative issues require the approval of the FM.

CBI: LOLR AND FINANCIAL AUTONOMY

18

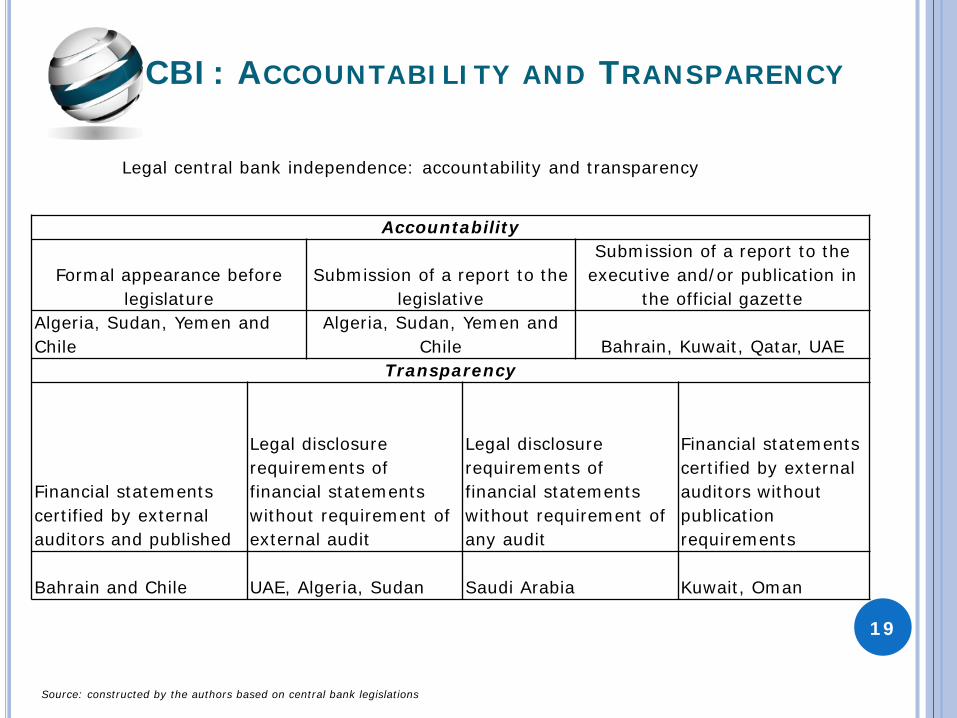

CBI: ACCOUNTABILITY AND TRANSPARENCY

Accountability

Formal appearance before legislature

Submission of a report to the legislative

Submission of a report to the executive and/or publication in

the official gazetteAlgeria, Sudan, Yemen and Chile

Algeria, Sudan, Yemen and Chile Bahrain, Kuwait, Qatar, UAE

Transparency

Financial statements certified by external auditors and published

Legal disclosure requirements of financial statements without requirement of external audit

Legal disclosure requirements of financial statements without requirement of any audit

Financial statements certified by external auditors without publication requirements

Bahrain and Chile UAE, Algeria, Sudan Saudi Arabia Kuwait, Oman

Legal central bank independence: accountability and transparency

Source: constructed by the authors based on central bank legislations

19

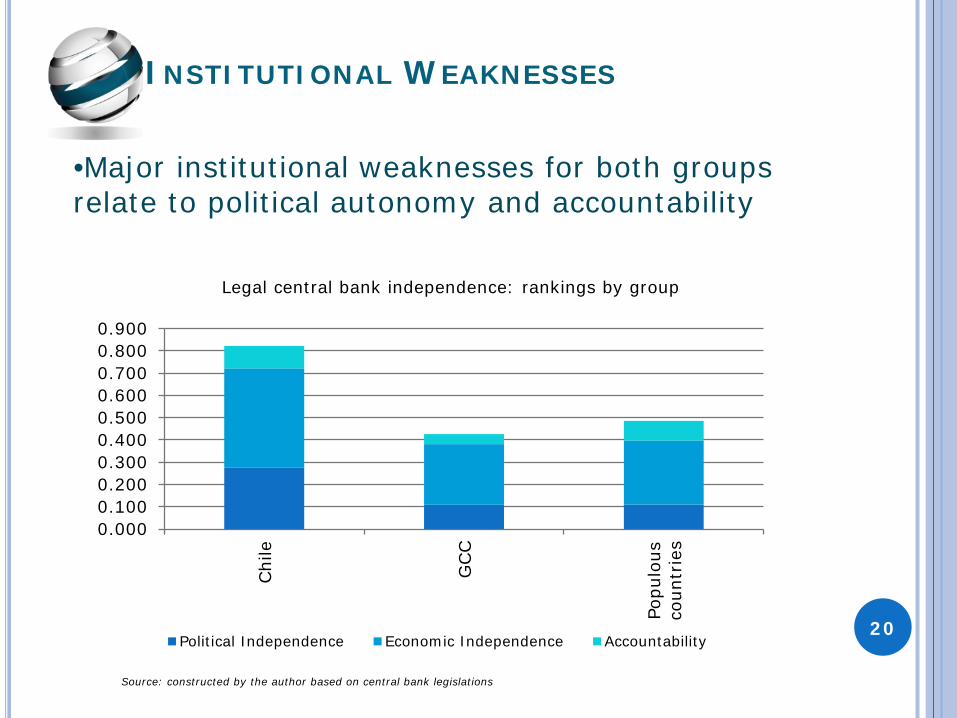

INSTITUTIONAL WEAKNESSES

•Major institutional weaknesses for both groups relate to political autonomy and accountability

0.0000.1000.2000.3000.4000.5000.6000.7000.8000.900

Chi

le

GCC

Popu

lous

coun

trie

s

Political Independence Economic Independence Accountability

Legal central bank independence: rankings by group

Source: constructed by the author based on central bank legislations

20

CBI: AN ANSWER FROM LEGISLATIONS

0.0000.1000.2000.3000.4000.5000.6000.7000.8000.900

Chile KSA

Yem

en

Qat

ar

Alge

ria

Bahr

ain

Suda

n

UAE

Om

an

Kuw

ait

Political Independence Economic Independence Accountability

•CBI is not uniform across Arab commodity exporters

•Central banks in the populous group benefit from more economic autonomy and accountability than their GCC counterparts

Legal central bank independence: rankings

Source: constructed by the author based on central bank legislations

21

IT IS ALL ABOUT INSTITUTIONS

•Low political independence of central bank boards is associated with overall weak political institutions.

BHR

KWT

OMN, QAT, UAE, YMN

SAU

DZASDN

Chile

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0 2 4 6 8

CB b

oard

s

FH scores

Source: constructed by the author based on central bank legislations and Freedom House scores

Freedom house scores and index for central bank board independence

22

I. Country coverage

II.Measuring independence

III.Independence of Arab monetary institutions: An answer from legislations

IV.Central banks and macro outcomes: was it independence?

V.Concluding remarks

OUTLINE

23

• Independent central banks in theory should be more successful in achieving their objectives.

• Yet, central banks have been associated with by more favourable outcomes (low inflation, currency stability, fiscal surpluses and financial stability) in the GCC even though the populous group are more slightly independent in de jureterms.

• So does CBI matter?

CBI AND MACRO OUTCOMES

24

Data: Author’s calculations based on WEO

PRICE STABILITY

•Compatible with legal mandate, low inflation in the GCC (exchange peg)

•Inflation seems like a structural problem in the poorer economies.

•Chile’s performance greatly improved in the 1990s.

1.7 3.5 2.1 3.8 1.5 4.49.7

39.9

17.911.1

0.05.0

10.015.020.025.030.035.040.045.0

Level Volatility

Long-term inflation: level and volatility

25

Data: Author’s calculations based on WEO

CURRENCY STABILITY

•Exchange rate pegs have been an anchor to inflationary expectations in the GCC

•Exchange rates in the poorer economies went through several adjustments and are volatile.

0.0

0.1 0.3

-0.1

0.3

-0.1

10.8

63.6

20.08.9

-10.00.0

10.020.030.040.050.060.070.0

er variation

Long-term exchange rate variations

26

Data: Author’s calculations based on WEO

GCC COUNTRIES ESCAPED FINANCIAL CRISIS

•Credit booms in Bahrain and UAE, driven by real estate investments during 2004-08 which moderated afterwards but no severe financial crisis.

-2.00-1.000.001.002.003.004.005.006.007.008.00

2004

-200

8

2009

-201

3

2004

-200

8

2009

-201

3

2004

-200

8

2009

-201

3

2004

-200

8

2009

-201

3

2004

-200

8

2009

-201

3

2004

-200

8

2009

-201

3

2003

-200

8

2004

-201

3

Bahrain Kuwait Oman Qatar SaudiArabia

UAE Chile

Credit to GDP Change in private credit/GDP ratio (pp)

Credit markets in the GCC and Chile

27

Data: Author’s calculations based on WEO

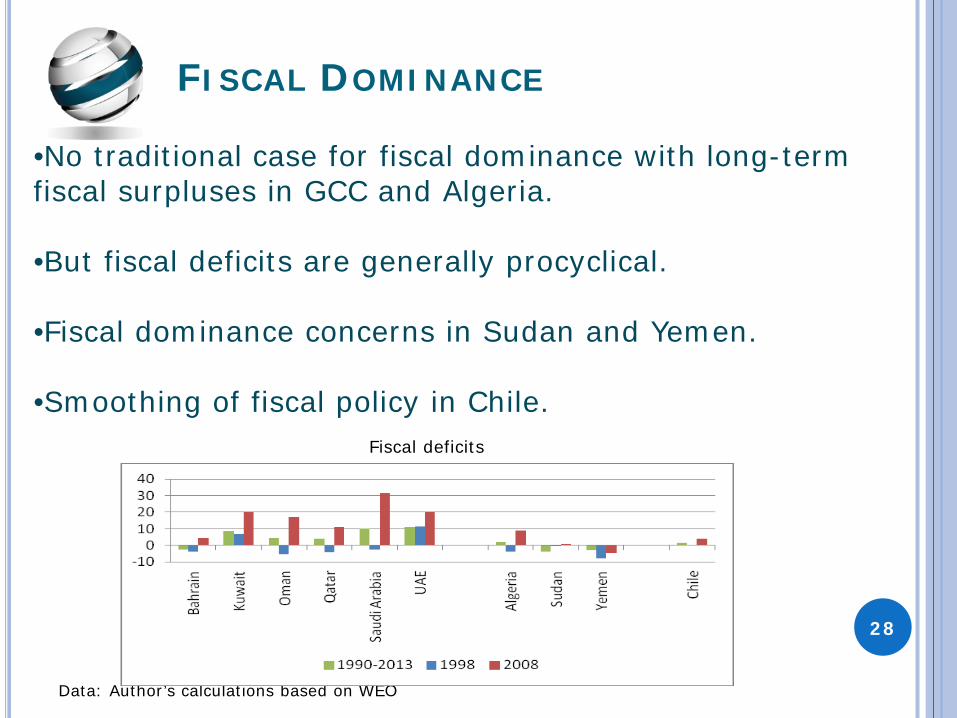

FISCAL DOMINANCE

•No traditional case for fiscal dominance with long-term fiscal surpluses in GCC and Algeria.

•But fiscal deficits are generally procyclical.

•Fiscal dominance concerns in Sudan and Yemen.

•Smoothing of fiscal policy in Chile.Fiscal deficits

28

The GCC has better outcomes because of many other underlying factors:

1. The exchange rate peg GCC imports credibility from the US$ and benefits from a stable US$ economy, which boosts de facto credibilty even without de jure independence.

2. The sheer amount of GCC wealth which translate into massive amount of reserve accumulation sustains the peg and fiscal surpluses do not put pressure on monetary policy in the traditional sense and generally insulates the effects of shocks.

3. The GCC has benefited from relative political stability which have contributed to macro stability.

DOES CBI MATTER IN ARAB COUNTRIES?

29

CBI matters :

For delivering better incomes in a context of overall strong domestic institutions (Chile vs. Arab world).

If good legislations are actually implemented (Yemen).

When monetary policy has a domestic anchor: If and when the peg is abandoned in the GCC and if the currency union leads to the creation of a supranational central bank.

During difficult times: oil busts and pressure on public finances

During good times: need to implement countercyclical policies.

DOES CBI MATTER IN ARAB COUNTRIES?

30

Elements for a reform agenda:

1. Introduce political reforms to support wide-ranging macro-institutional reform and therefore improve the management of natural resources

2. Strengthen political autonomy of central banks to untie monetary policy horizons from politicians

3. Set rigorous accountability and transparency procedures to bolster the credibility of monetary policy

4. Countercyclical fiscal policy and fiscal rules to smooth fiscal spending and promote fiscal discipline (SWF).

5. Prioritize central bank objectives in order to insure policy inconsistencies during implementation.

CONCLUDING REMARKS

31