central america macro watch april 20, 2006. agenda external financial conditions economic growth and...

TRANSCRIPT

Central America Macro Watch

Central America Macro Watch

April 20, 2006April 20, 2006

Agenda

• External Financial Conditions

• Economic Growth and Outlook

• The Real Exchange Rate and Inflation

• Effects of Oil Price Increases

• The MDRI Initiative and its Impact

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 F 2006 F

Net Capital Capital Account FDI Portfolio Other investments Errors and Omissions

Capital Flows, CAC-7Capital Flows, CAC-7(US$ Billion)(US$ Billion)

Capital Flows have kept on increasing, and have hovered Capital Flows have kept on increasing, and have hovered steadily…steadily…

Source: BoPs (April 2006), WEO(Sep 2005). Includes errors and omissions.

CAC 7 = Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras, Nicaragua and Panama

Argentinean Crisis

Russian Crisis

Asian Crisis

Total FlowsDominican

Crisis

Capital Flows, LAC 7 & CAC 7(index 1997=100)

...in contrast with LAC7 countries...in contrast with LAC7 countries

Source: BoPs (April 2006), WEO(Sep. 2005).

CAC 7 = Costa Rica, Dominican Republic , El Salvador, Guatemala, Honduras, Nicaragua and PanamaLAC 7 = Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela* Total Capital Flows include errors and omissions.

Asian Crisis

Russian Crisis

Argentinean Crisis

Dominican Crisis

-20

0

20

40

60

80

100

120

140

1997 1998 1999 2000 2001 2002 2003 2004 2005 F 2006 F

(In

de

x 1

99

7=

10

0)

CAC7 LAC7

External Financial ConditionsSpreads over US Treasury Bills (basis points)

Source: Bloomberg

The CAC7 Sovereign Spreads are from JP Morgan’s Latin Eurobond Index and include Costa Rica, El Salvador, Guatemala and Panama. The index shown above is an average weighted by market capitalization.

This is reflected in lower spread volatility in Central This is reflected in lower spread volatility in Central America...America...

Enron Effect

BanInter Intervention

Sovereign Spread CAC7 Excl. Dominican Rep.

EMBI+ Excl. Argentina

0

100

200

300

400

500

600

700

800

900

1000

Apr

-02

Jun-

02

Aug

-02

Oct

-02

Dec

-02

Feb

-03

Apr

-03

Jun-

03

Aug

-03

Oct

-03

Dec

-03

Feb

-04

Apr

-04

Jun-

04

Aug

-04

Oct

-04

Dec

-04

Feb

-05

Apr

-05

Jun-

05

Aug

-05

Oct

-05

Dec

-05

Feb

-06

GDP at Constant Prices(index 1997=100, regional averages)

...higher GDP growth in the region......higher GDP growth in the region...

Source: WEO (Sep. 2005).

LAC7= Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela

CAC 7 = Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras, Nicaragua and Panama

Asian CrisisRussian Crisis

Argentinean Crisis

CAC 7

LAC 7

60

70

80

90

100

110

120

130

140

150

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Index 1

99

7=

10

0

....and most of all in real exchange rate stability.....and most of all in real exchange rate stability.CAC7– Bilateral Real Exchange Rate Index (1997=100)

LAC7= Argentina, Brazil, Chile, Colombia, México, Peru and Venezuela

CAC 7 = Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras, Nicaragua and Panama

The bilateral real exchange rate is the regional average.

Source: IFS, WEO (Sep. 2005) and own estimates.

Argentinean Crisis

Russian Crisis

Asian Crisis BanInter

Intervention

50

100

150

200

Jan

-97

Jul-9

7

Jan

-98

Jul-9

8

Jan

-99

Jul-9

9

Jan

-00

Jul-0

0

Jan

-01

Jul-0

1

Jan

-02

Jul-0

2

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

(In

de

x 1

99

7=

10

0)

CAC7 LAC7 CAC7 (Excl. Dom Rep)

Source: WEO (Sep-05), BoPs (April-2006)Source: WEO (Sep-05), BoPs (April-2006)

CAC 7 = Costa Rica, Dominican Rep., El Salvador, Guatemala, Honduras, Nicaragua and Panama

Current Account Balance & Remittances, CAC7Current Account Balance & Remittances, CAC7(% of GDP)(% of GDP)

Although remittances have financed a big share of the Although remittances have financed a big share of the current account deficit...current account deficit...

-6.2% -6.4%

-7.8%

-6.8%

-5.7% -5.7%

-4.8%-4.4%

-5.0%-4.7%

-10.3%-11.0%

-13.0%-12.5%

-11.8%

-12.9%-13.2%

-13.7%-14.1%

-13.6%

-16.0%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005F 2006F

CA CA w/o Remittances

Source: BoPs (April 2006), WEO (Sep-05). Source: BoPs (April 2006), WEO (Sep-05).

CAC 7 = Costa Rica, Dominican Rep., El Salvador, Guatemala, Honduras, Nicaragua and Panama

Capital Flows and Remittances, CAC-7Capital Flows and Remittances, CAC-7(US Dollar Billion)(US Dollar Billion)

...they have been growing steadily, and apparently isolated ...they have been growing steadily, and apparently isolated from economic cycles.from economic cycles.

0

2

4

6

8

10

12

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

F

2006

F

Net Capital Flows Remittances

There is a strong link between the regional cycle and that of There is a strong link between the regional cycle and that of the US, due to large tradable sectors integrated to the US...the US, due to large tradable sectors integrated to the US...

Source: WEO (Sep. 2005), EIU (Mar 2006), BCN (NIC) and MEF (PAN).

CAC 7 USA

CAC 7 = Costa Rica, Dominican Rep., El Salvador, Guatemala, Honduras, Nicaragua and Panama

GDP at Constant Prices (Annual Growth, in percent)

Argentinean Crisis

Russian Crisis

Asian Crisis

Mexican Crisis

-1

0

1

2

3

4

5

6

7

81

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

F

20

06

F

CAC 7 = Costa Rica, Dominican Rep., El Salvador, Guatemala, Honduras, Nicaragua and Panama

GDP Growth, CAC7 (in percent, 2005E vs. 2006F)

Following lower growth expectations in the US, somewhat Following lower growth expectations in the US, somewhat lower growth is forecasted for 2006lower growth is forecasted for 2006

Source: EIU Country Reports (Mar 2006)

CRI

DOM

SLV

GTM HON

NIC

PAN

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

-10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0

GDP growth in 2005E

GD

P g

row

th in

20

06

F

Inflation and the Real Inflation and the Real Exchange RateExchange Rate

Source: Central Banks, WEO (Sep-2005), EIU (March-2005)

CAC7 – Inflation Rate (%)CAC7 – Inflation Rate (%)

The region has experienced a sustained increase in inflation. The region has experienced a sustained increase in inflation. What drives this process? What drives this process?

0

2

4

6

8

10

12

14

16

CRI SLV GTM HON NIC PAN

%

2002 2003 2004 2005

0

5

10

15

20

25

30

35

40

45

50

55

DOM

Do

min

ica

n R

ep

ub

lic (

%)

In many cases, an important policy objective is to ensure In many cases, an important policy objective is to ensure real exchange rate stability...real exchange rate stability...CAC7– Bilateral Real Exchange Rate Index (1997=100)

LAC7= Argentina, Brazil, Chile, Colombia, México, Peru and Venezuela

CAC 7 = Costa Rica, Dominican Republic, El Salvador, Guatemala, Honduras, Nicaragua and Panama

The bilateral real exchange rate is the regional average.

Source: IFS, WEO (Sep. 2005) and own estimates.

Argentinean Crisis

Russian Crisis

Asian Crisis BanInter

Intervention

50

100

150

200

Jan

-97

Jul-9

7

Jan

-98

Jul-9

8

Jan

-99

Jul-9

9

Jan

-00

Jul-0

0

Jan

-01

Jul-0

1

Jan

-02

Jul-0

2

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

(In

de

x 1

99

7=

10

0)

CAC7 LAC7 CAC7 (Excl. Dom Rep)

Source: IFS. Own estimates.

CAC7 – Bilateral Real Exchange Rate with the US CAC7 – Bilateral Real Exchange Rate with the US (1997=100)(1997=100)

75

100

125

150

175

Jan-

97

May

-97

Sep

-97

Jan-

98

May

-98

Sep

-98

Jan-

99

May

-99

Sep

-99

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

Costa Rica Dominican Rep. El Salvador Guatemala Honduras Nicaragua Panama

1616Source: BoPs (April 2006), Central Banks, WEO (Sep-05)Source: BoPs (April 2006), Central Banks, WEO (Sep-05)

Remittances by Country Remittances by Country (% of GDP)

The substantial increase of remittances has been a source of The substantial increase of remittances has been a source of potential real exchange rate appreciation.potential real exchange rate appreciation.

0%

5%

10%

15%

20%

25%

CRI DOM SLV GTM HON NIC PAN

2001 2002 2003 2004 2005

270% increase

85% increase

1717

* General Government Balances include grants. Source: WEO (Sep-05), Central Banks, IMF Country Reports

Non-Financial Public Sector Balance (% of GDP)*

Fiscal deficit financing is large in many cases...Fiscal deficit financing is large in many cases...

-9.0%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

CRI DOM SLV GTM HON NIC PAN

2001 2002 2003 2004 2005F

• Regional average for 2005: -2.2% of GDP

CAC 7 – Central Bank Debt (% of GDP)

Source: Central Banks. Information for Costa Rica and Honduras as of Feb-2006

……in an effort to keep inflation at bay and stabilize the real in an effort to keep inflation at bay and stabilize the real exchange rate, Central Banks sterilize the associated monetary exchange rate, Central Banks sterilize the associated monetary

expansion...expansion...

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

CRI DOM SLV GTM HON NIC

2001 2002 2003 2004 2005 Mar 2006

• Regional average for 2005: 8.4% of GDP

Source: Central Banks and IMF.

CAC 7 –Net Central Bank Losses (2003-2005, % of GDP)

...at a high quasi-fiscal cost. ...at a high quasi-fiscal cost.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

CRI DOM GTM HON NIC

2003 2004 2005

• Regional average for 2005: 1.4% of GDP

2005 Average

An example of Likely Deviation from Equilibrium RER by An example of Likely Deviation from Equilibrium RER by 2004: Guatemala2004: Guatemala

3.2

3.6

4.0

4.4

4.8

5.2

86 88 90 92 94 96 98 00 02 04

A c tu a l Equilibrium REER P Equilibrium REER T

• However, strong real appreciation has taken place in 2005-2006 (11% )

Effects of Oil Price Effects of Oil Price IncreasesIncreases

Oil Price BehaviorOil Price Behavior

Spot Price Crude WTI Cushing. Source: Bloomberg.

343%

0

10

20

30

40

50

60

70

80Ja

n-9

7

Jul-9

7

Jan

-98

Jul-9

8

Jan

-99

Jul-9

9

Jan

-00

Jul-0

0

Jan

-01

Jul-0

1

Jan

-02

Jul-0

2

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Oil

Pri

ce

- U

S$

/Ba

rre

l

Fuel Imports as a Share of Total ImportsFuel Imports as a Share of Total Imports

0%

5%

10%

15%

20%

25%

30%

35%

40%

Costa Rica Dom Republic El Salvador Guatemala Honduras Nicaragua Panama

2002 2003 2004 2005

Note: Excludes maquila or free zone imports. Source: Central Banks.

Average (2005)

Note: The Fund’s September 2005 World Economic Outlook (WEO) now envisages world oil prices averaging US$54.1/bbl in 2005 and US$61.8/bbl in 2006, some 17 percent and 40 percent higher, respectively, than projected in the April 2005 WEO.

Source: Singh, Anoop. Global Context and Regional Outolook for Latin America and the Caribbean. IMF. October 2005.

LAC: Oil price impact on economic activity and Inflation(in % )

Net oil Exporters

South America

Central America

The Caribbean

Latin America and the Caribbean

3.0%

2005 2006 2005 2006

Inflation Growth

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

-0.5%

-1.0%

-1.5%

Estimates of the impact of the change of WEO oil price assumptions in the LAC Region

Note: Preliminary results.

* Average change in Oil Prices estimated between 2004 and 2005 for the Spot Prices of the West Texas Intermediate.** Forecast based on annual growth rate of Oil Prices from IMF.Source: Central Banks, Bloomberg, and BoPs (April 2006); own estimates.

Effect of an increase in the Price of Oil over the Effect of an increase in the Price of Oil over the Real Exchange RateReal Exchange Rate

CRI DOM SLV GTM HND NIC PAN

Net Oil Imports (US$ million, 2004) 582 1449 460 910 637 377 511Oil Price Increase 2004-2005 (%)* 37.7%Oil Price Increase 2004-2006 (%)** 57.3%

Oil Imports Increase 2004-2005 As a share of GDP 2005 1.1 2.5 1.0 1.3 3.0 2.8 1.3 As a share of Imports 2004 3.1 8.3 2.9 3.8 5.1 5.9 3.8Oil Imports Increase 2004-2006 As a share of GDP 2005 1.7 3.8 1.6 1.9 4.6 4.3 2.0 As a share of Imports 2004 4.7 12.6 4.4 5.7 7.8 9.0 5.8

Change in REER required (2004-2005) 7.7 20.8 7.3 9.4 12.9 14.7 9.6 Number of Standard Deviations 4.2 1.1 4.4 1.4 4.4 5.7 10.3Change in REER required (2004-2006) 11.7 31.6 11.0 14.3 19.6 22.4 14.5

Number of Standard Deviations 6.4 1.7 6.7 2.2 6.7 8.7 15.7

So far, given favorable financing conditions, the oil shock So far, given favorable financing conditions, the oil shock has been absorbed without major RER effects. But things has been absorbed without major RER effects. But things could be different in the absence of foreign financingcould be different in the absence of foreign financing

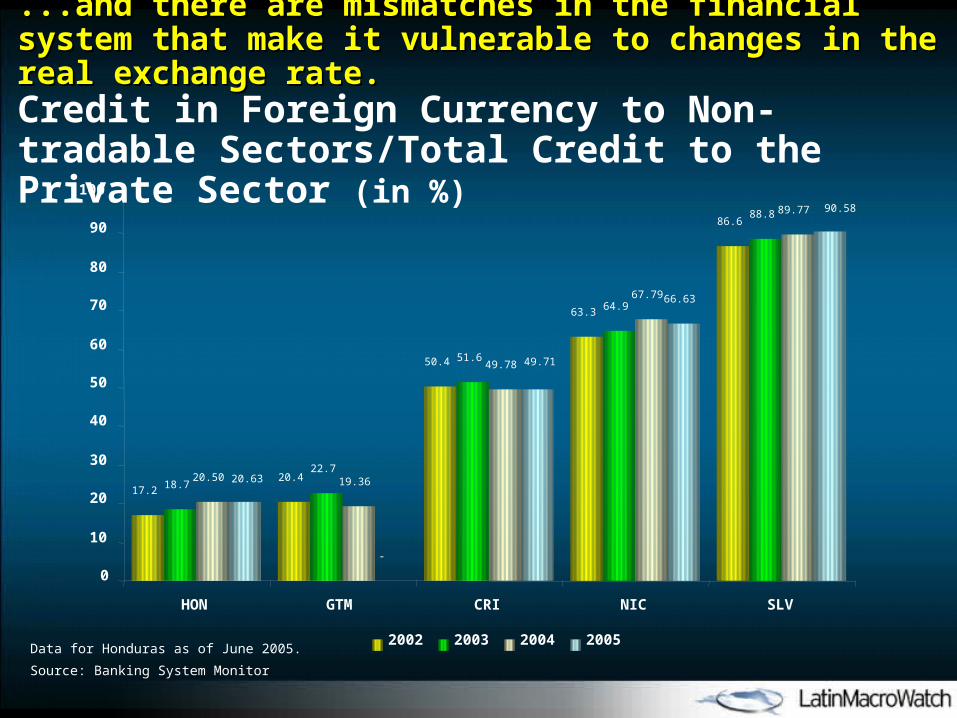

Data for Honduras as of June 2005.

Source: Banking System Monitor

...and there are mismatches in the financial system that make ...and there are mismatches in the financial system that make it vulnerable to changes in the real exchange rate.it vulnerable to changes in the real exchange rate.

Credit in Foreign Currency to Non-tradable Sectors/Total Credit to the Private Sector (in %)

17.220.4

50.4

63.3

86.6

18.7

22.7

51.6

64.9

88.8

20.50 19.36

49.78

67.79

89.77

-

66.63

49.71

20.63

90.58

0

10

20

30

40

50

60

70

80

90

100

HON GTM CRI NIC SLV

2002 2003 2004 2005

Note: The ratio dB/de measures changes in total debt in percentage points of GDP (B) that would occur when the real exchange rate (e) variation of 100%

Source: Central Banks, Finance Ministries and IMF. Own estimates.Source: Central Banks, Finance Ministries and IMF. Own estimates.

Financial Exposure of the NFPS - dB/de (2004)

On the other hand, the public sector in some countries is On the other hand, the public sector in some countries is heavily exposed to RER depreciation.heavily exposed to RER depreciation.

CAC 7 LAC 7

0%

20%

40%

60%

80%

100%

120%N

IC

UR

U

PA

N

HN

D

SLV

PE

R

BO

L

JA

M

AR

G

CO

L

DO

M

CR

I

GT

M

BR

A

ME

X

VE

N

CH

L

Lo

w E

xp

osu

reH

igh

Exp

osu

re

Multilateral Debt Reduction Multilateral Debt Reduction InitiativeInitiative

Multilateral Debt Relief Initiative (MDRI)

• Coverage: HIPC countries that have reached, or will eventually reach, their completion point, plus non-HIPC countries with a GDP per capita at or below US$380.

• Relief: 100 % of debt with three multilateral institutions: IMF, IDA, and ADF.

• Amount: About US$50 billion in nominal terms (outstanding stocks as of Dec-2004).

• Qualifying IADB members: Bolivia, Guyana, Honduras and Nicaragua.

• Allocation: In contrast to HIPC initiative, there is no specific allocation for social expenditure increases.

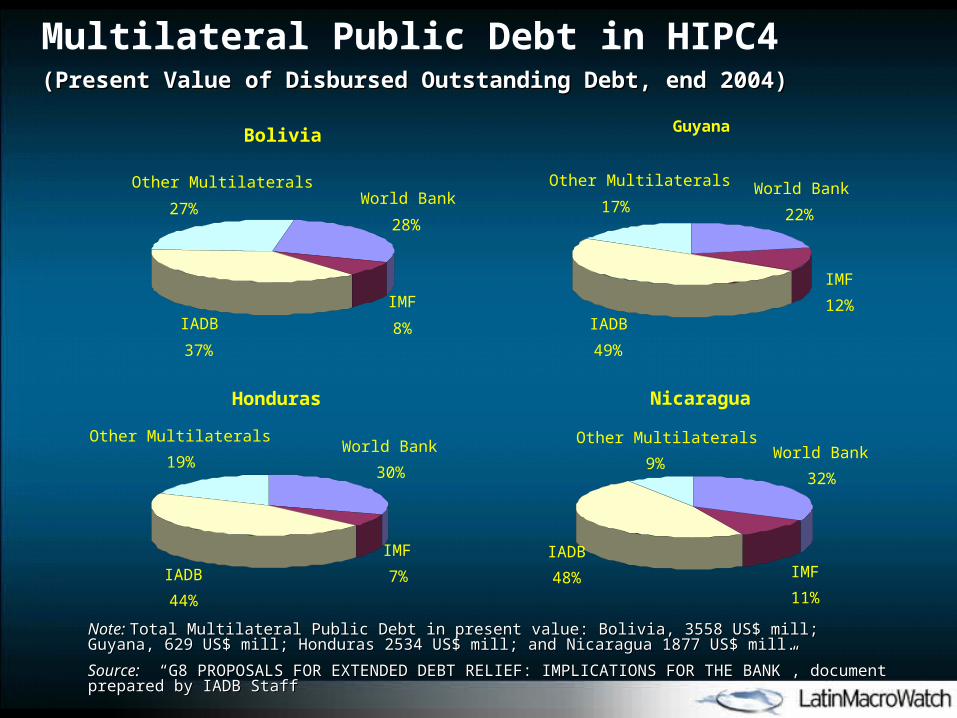

Multilateral Public Debt in HIPC4(Present Value of Disbursed Outstanding Debt, end 2004)(Present Value of Disbursed Outstanding Debt, end 2004)

Note: Note: Total Multilateral Public Debt in present value: Bolivia, 3558 US$ mill; Guyana, 629 US$ mill; Honduras Total Multilateral Public Debt in present value: Bolivia, 3558 US$ mill; Guyana, 629 US$ mill; Honduras 2534 US$ mill; and Nicaragua 1877 US$ mill.2534 US$ mill; and Nicaragua 1877 US$ mill.

Source:Source: “ “G8 PROPOSALS FOR EXTENDED DEBT RELIEF: IMPLICATIONS FOR THE BANKG8 PROPOSALS FOR EXTENDED DEBT RELIEF: IMPLICATIONS FOR THE BANK”, document ”, document prepared by IADB Staffprepared by IADB Staff

Bolivia

World Bank

28%

IMF

8%IADB

37%

Other Multilaterals

27%

Guyana

World Bank

22%

IMF

12%IADB

49%

Other Multilaterals

17%

Honduras

World Bank

30%

IMF

7%IADB

44%

Other Multilaterals

19%

Nicaragua

World Bank

32%

IMF

11%

IADB

48%

Other Multilaterals

9%

Impact of HIPC & MDRI: NPV of Public Debt as a share of GDP(2004, in %)

SourceSource: “: “G8 PROPOSALS FOR EXTENDED DEBT RELIEF: IMPLICATIONS FOR THE BANKG8 PROPOSALS FOR EXTENDED DEBT RELIEF: IMPLICATIONS FOR THE BANK”, document ”, document prepared by IADB Staff. Own calculationsprepared by IADB Staff. Own calculations

Ratio of Present Value of External Public Debt to GDP in 2004, in percent

0

20

40

60

80

100

Guyana Honduras Nicaragua Bolivia

Outstanding After HIPC After MDRI After IADB "MDRI"

15%27%

32%38%

SourceSource: GDF and IMF. Own calculations: GDF and IMF. Own calculations

0

5

10

15

20

25

Bolivia Guyana Honduras Nicaragua

Outstanding After HIPC After MDRI After IADB "MDRI"

1.4%3.3%

1.6% 1.7%

Impact of HIPC & MDRI: Amortization of Multilateral Public Debt to Reserves Ratio(2004, in %)

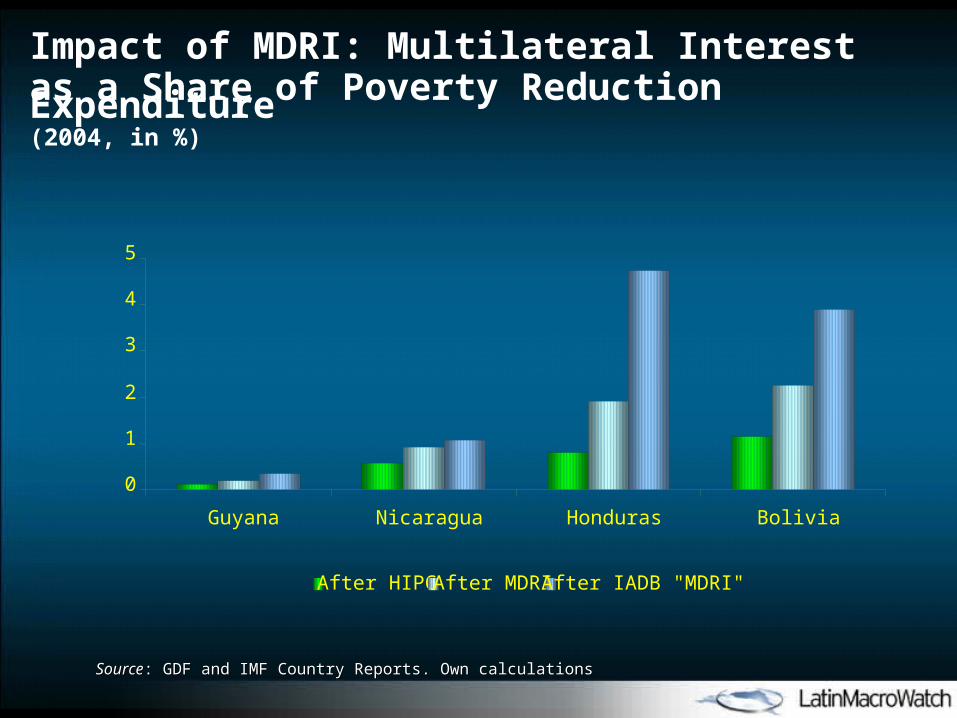

SourceSource: GDF and IMF Country Reports. Own calculations: GDF and IMF Country Reports. Own calculations

0

1

2

3

4

5

Guyana Nicaragua Honduras Bolivia

After HIPC After MDRI After IADB "MDRI"

Impact of MDRI: Multilateral Interestas a Share of Poverty Reduction Expenditure(2004, in %)

Central America Macro Watch

Central America Macro Watch

April 20, 2006April 20, 2006