cencosud: without limits to dream carrefour colombia: an

TRANSCRIPT

March 1st, 2015

Cencosud: Without l imits to dream

“The Colombian purchase is a unique opportunity we can't let go" -‐Horst Paulmann, founder and President, Cencosud

Carrefour Colombia: An Opportunity Arises

Juan Manuel Parada felt restless. As the newly appointed CFO of Cencosud, he had just received a report

that could change the course of the company. It contained information on Carrefour, the world’s second-‐

largest retailer and competitor of Cencosud. Looking to cut costs and debt, due to the difficult economic

situation in Europe, Carrefour was contemplating whether to sell its Colombian operations. Present in

Colombia since 1998, Carrefour operates 72 hypermarkets, 16 convenience stores and 4 cash and carry

stores in the country. Although Cencosud had no current plans to grow through acquisitions in Colombia,

this deal would allow them to penetrate the market in a way that wouldn’t have been possible via organic

growth. Furthermore, Carrefour stores share a similar format to Cencosud stores, which would make

them a good fit with Cencosud’s current operations.

Juan Manuel worried that disclosing this information to the board could lead Horst Paulmann, Founder

and President of Cencosud, to make a hasty decision. This could be Juan Manuel’s first acquisition and he

didn’t want it to be a value-‐destroying one. Carrefour’s Colombian operations represented a large asset

that would require Cencosud to undertake more debt than usual. He needed time, to put together a

valuation but knew he didn’t have much. Since he had this report, it meant that other competitors also

did. He needed to reach a conclusion fast or risk Wal-‐Mart and Falabella beating them to the punch.

The Fuqua School of Business at Duke University

2

Competitive Landscape

Retail industry and major players in Chile

The retail industry in Chile is highly competitive and developed, and has grown significantly in the last 20

years through the consolidation of strong local players and with little presence of international players.

Financial services associated to the retail business, including credit cards and loyalty programs, are strong

in Chilean retail, and have been determinant for the success of local players, and at the same time, have

been an important reason of the failure of international players trying to set foot in the Chilean retail

industry. Giant retailers JCPenney, Home Depot, and Carrefour are some examples.

The Chilean retail industry can be divided into three main categories: department stores, supermarkets,

and home improvement. The total retail market as of 2011 is valued near $25 billion and has experienced

a sharp growth in the past years, motivated by high GDP growth rates, 5.8% and 5.8% in 2010 and 2011,

respectively. Market projections show the growth in food retail to be 7.3% and 3.5% for the apparel retail

in the 2013 – 2018 periodI. This is in line with the healthy economy of Chile, which has presented

consistent growth in-‐hand with a stable political environment, wide access to credit, and solid growth

projections for coming years.

The two dominant retail players in Chile, with activities in all the three retail categories, are Falabella and

Cencosud. These two conglomerates face competition in the department stores and home improvement

categories from smaller and local players, with a more focused approach in a particular segment.

However, in the supermarket segment, the two dominant players compete against giant Wal-‐Mart. In

addition, Falabella and Cencosud face competition from SMU, a group formed from a series of mergers

between 12 smaller regional supermarket chains. Please refer to Exhibit 1 that contains a table

summarizing the main characteristics of the largest retail players in Chile.

Chilean Consolidation and diversification

The period between the years 1990 and 2005 is referred as the “golden years” for the retail industry in

ChileII. Leading players developed a consolidation and high growth strategy that was executed both via

acquisitions and organic growth. Big technological improvements made a significant difference in terms

of cost efficiency, and positioned the principal players a huge step ahead of the rest of the competitors.

The incorporation of code bars and laser readers by 1991 was vital to improve stocking and inventory

The Fuqua School of Business at Duke University

3

efficiency, and also the development of distribution centers that solved logistic issues for the chains that

were expanding within the countryIII.

By the mid-‐90s in the supermarket segment, “Lider”, now Wal-‐Mart, followed a strategy leaned to

organic growth. Santa Isabel, acquired by Cencosud in 2003, acquired smaller regional chains Multimarket

and Marmentini Letelier. By 2004, Falabella entered the supermarket arena by acquiring Supermercados

San Francisco, later on rebranded as Tottus, now with 64 stores in Chile and PeruIV.

In the Department Stores segment, Cencosud made a key consolidation move in April 2005. The company

acquired Falabella’s main competitor, Almacenes Paris, for $950 million. This acquisition allowed

Cencosud to enter the department store and retail financial services businessesV.

The home improvement is the most fragmented of the three segments, however we have seen huge

resources devoted by the big players in order to consolidate their presence in this business. Cencosud

formed “Easy” by 1993 and followed an organic growth strategy with a combination of small acquisitions

of some of the Chilean assets of The Home Depot and ProTerra in 2000. On the other hand, Falabella took

an aggressive move in 2003 by acquiring Sodimac, the leader in this segment, a transaction valued in $2.5

billionVI. To further consolidate, Falabella acquired Imperial in 2008.

As conclusion, in this 1990 – 2005 period we can observe that the largest Chilean players were filing the

market rapidly and diversifying their presence in the retail industry to its three segments. The evident

growth strategy in order to continue having such successful rates was to tap other markets in Latin

America. However, there they would face other country risk, market dynamics, competitors and

particularities from each the markets.

Latin American players

Argentina Efforts to rebuild credit following the financial and political crises of 1999-‐2002 had a positive impact on

consumer expenditure and, consequently, retail sales in ArgentinaVII. However continuous economic and

political issues, and rising inflation rates challenged the development of the retail sector, especially for

foreign companies. Nevertheless, three main players in the supermarket segment, Carrefour, Cencosud

and Wal-‐Mart, are foreign. The total food retail market for 2011 was valued at $33 billionVIII.

Both the department store and the home improvement segments are not well developed in Argentina

due to consumer’s preferences to shop in smaller local and specialized storesIX. Falabella is the only

The Fuqua School of Business at Duke University

4

significant department store with an income of $511 million in 2011. The group is also present with

Sodimac and competes against Easy (Cencosud) in the home improvement segment.

Brazil Brazil is the world’s third-‐biggest grocery market, next only to America and China, with strong players

operating in the market, both foreign and domesticX. The food retail market in Brazil for 2011 had total

sales for $128 billionXI. Global retailers such as Wal-‐Mart compete against domestic market leaders like

Pão de Açúcar. In terms of market share, Pão de Açúcar has of about 18% of the market; the French

retailer has about 14.5% and Walmart 12%XII. Competition is expected to intensify in the next few years as

the supermarket penetration remains low at 40%, significantly lower than the 70% penetration achieved

in Chile.XIII

Strong local players such as Casa Bahia, Lojas Americanas, and Companhia Hering characterize the

department stores segment in Brazil. The apparel retail market in Brazil had $37 billion in sales for

2011XIV.

Colombia Since the beginning of the new century, the Colombian market has been expanding very rapidly. Growth

in personal income and changes in purchasing habits led Colombia to become one of the most attractive

markets in the region.XV Market researchers expect the food retail in Colombia to grow 6.7% CAGR (see

Exhibit 2 for projections) in the 2013-‐2018 periodXVI. International players mainly make up the retail

industry, and given its high growth potential market researchers expect this trend to continue. For the

coming years, market researchers expect a good environment for international investment in Colombia

because of GDP expansions above Latin America’s average, a controlled inflation, decreasing

unemployment rates and a healthy financial system.

Grupo Exito, who owns 61% of the market share, dominates the supermarket segment, Carrefour follows

with 19%, Olimpica, with 15%, and La 14, with 5%. Total food retail market was $58.2 billion in 2011XVII.

The two main department stores are the Chileans Falabella and La Polar. Finally, Chilean players Falabella

and Cencosud, with their respective brands Sodimac and Easy, also dominate the home improvement

segment XVIII.

Mexico Mexico is a hybrid country, where new, world-‐class retail development shares the street with an

estimated 2.3 million single-‐shop stores and traditional markets. Still, it is a very attractive market due to

The Fuqua School of Business at Duke University

5

its large and growing middle class populationXIX. Food retail in Mexico is a market with total sales of $151

billion in 2011XX with the major players being WalMex, Organizacion Soriana, Chedraui and ComerciXXI.

The department store segment, especially in the apparel component has experimented moderate growth

in recent years, however it is expected to growth slightly in the 2011 – 2016 period at a 2.9% CAGRXXII.

The main department stores players are Liverpool, Suburbia, Sears and El Palacio del Hierro.

Peru Retail industry prospects in Peru are very attractive. Real wages in Peru are expected to growth twice the

average of Latin America’sXXIII. This, combined with the lowest penetration of “developed” retail, makes

the country tempting to new players. The three main players in the supermarket segment are Wong,

acquired by Cencosud in 2007 for $468 million, Supermercados Peruanos, and Falabella’s Tottus.

Chilean’s Falabella and Ripley dominate the department stores segment. Finally, Sodimac followed by

local Maestro leads the home improvement segment.

Cencosud: A leader is born

In 1976 Horst Paulmann, a German immigrant, opened the first hypermarket “Jumbo” in the south of

Chile. Little did he know that five decades later his company would be recognized as one of the largest

and most prestigious retail conglomerates in Latin America. With over 800 stores, 25 shopping centers,

4.2 million credit cards issued and 130,000 employees in 5 countries1, Cencosud is a force to be reckoned

with. It has acquired over ten companies in the past. The company offers more than 450 thousand

products through diversified business segments and 15 brand names present in 5 countries (Exhibit 3

shows a breakdown of brands by country). Additionally, it had a very strong financial performance in 2011

with $15.6billion in revenues and an EBITDA of $1.287 billion that has increased by more than 3x since

2005XXIV.

Cencosud: Multi-‐Format Strategy Cencosud currently operates five lines of business (Exhibit 4 specifies revenue and EBITDA breakdown

by business line):

1. Supermarkets: Its most relevant business division with over 720 stores across 4 countriesXXV.

They have a quality-‐service and quality-‐price strategy that helps them segment customers. It

holds brands such as “Jumbo”, “GBarbosa”, and “Disco” that are well known and have high

customer recognition.

1 As of December 31, 2011

The Fuqua School of Business at Duke University

6

2. Home improvement: Founded in 1993, it is the second most important business division with

over 80 stores in Argentina, Chile, and Colombia. Stores offer products and services oriented to

improve and/or maintain home. Its main brand is “Easy”.

3. Department stores: In 2005 Cencosud began its participation in this industry by acquiring

Chilean department store chain Almacenes Paris. The division is primarily focused in Chile. Stores’

main activity is the retail sale of clothing, appliances, electronics and technology. By the end of

2011 the company successfully completed a phase of its ambitious expansion cycle with the

acquisition of Johnson department stores in Chile.

4. Shopping centers: With over 20 shopping centers in Chile, Argentina, and Peru the shopping

center division represents 2% of revenues. Cencosud seeks to promote flow of consumers

through additional stores by having “Jumbo” and “Easy” as anchors in its shopping malls.

Cencosud’s desire to ensure that their customers have a superior shopping experience has led to

the creation of its Costanera Center, the tallest building in Latin America, expected to open in the

second quarter of 2012.

5. Financial Services: Encompasses mainly credit card and consumer finance operations, as well

as insurance. With over 4.2 million credit cards issued, this business segment represents 3% of

revenues. The main objective is to strengthen the relationship with clients by offering a more

complete service and generating greater added value from the synergies that exist between all

subsidiariesXXVI.

Cencosud: Business Strategy

The company’s business strategy resides in leveraging the competitive advantages of all business lines to

provide consumers with exceptional shopping experiences. To accomplish this Cencosud focuses on five

key pointsXXVII:

1. Continue developing a multi-‐format and multi-‐brand strategy: this allows Cencosud to offer a

wide range of products and brands associated with different shopping experiences therefore

achieving consumer loyalty as well as benefiting from synergies between the different business

units.

2. Centralize efforts in continuing to increase margins: focus on operational efficiency and

rationalization of distribution capacity making use of the increasing economies of scale to obtain

favorable buying conditions.

The Fuqua School of Business at Duke University

7

3. Continue organic growth and new acquisitions: Take advantage of its well-‐known brand portfolio

and reputation to continue with its aggressive plan of organic growth, leveraging significant

opportunities to expand their presence in Peru and Brazil.

4. Obtain synergies through the integration of our acquisitions: Achieved synergies and cost savings

by integrating acquisitions with operations in Chile and Argentina.

5. Improve service commitment and customer satisfaction: Given the highly competitive nature of

the retail business Cencosud is looking to attract and retain customers through combination of

quality products, good service, reasonable prices and attractive shopping environment. In order

to anticipate customer demand, the company plans to improve its information technology

systems, databases and CRM.

International expansion Cencosud’s geographic diversification campaign has allowed the firm to ensure its growing participation

in Latin America. Organic growth in neighbor countries plus a sequence of key acquisitions positioned the

firm, 3 decades later, as one of the most prestigious and profitable retailers in the region (Exhibit 5

provides a timeline from 1976 to 2012). After this period of continued growth, the company maintains

international operations in Argentina, Brazil, Colombia and Peru (Exhibit 6 presents Cencosud’s

revenues by country).

1982 – 2001: Organic growth in Argentina During this period, and despite Argentina’s continued economic and political challenges, Cencosud

underwent an aggressive growth plan in the country. The company’s expansion plan in Argentina started

in 1982 when the company opened the first hypermarket, Jumbo, an almost 100,000 square-‐foot facility.

The country was experiencing triple-‐digit inflation, but Buenos Aires had more inhabitants than all of Chile

and thus, represented a good business opportunity to boost international revenues. XXVIII

In 1988, Cencosud recognized the value of a multi-‐format strategy and a multi-‐brand strategy (Exhibit 7

provides Cencosud brands and their market position) and inaugurated its first shopping center,

Unicenter, a 987,811 square-‐foot facility of rentable space. XXIX The success of Unicenter plus the

desirable economic conditions remaining in Argentina, where inflation had ended, led Cencosud to focus

most of the company’s international growth in Argentina. Between 1993 and 2001, the firm opened 10

commercial centers, 8 in Buenos Aires, 1 in the province of Neuquen and 1 in the city of Mendoza.XXX

The Fuqua School of Business at Duke University

8

2002 – 2006: Acquisitions in Argentina In 2002, the company started its acquisition process by taking over four Home Depot stores and

converting them into Easy stores. This move represented a big step for Cencosud, who took loans from 4

different banks to pay the $90 million acquisition. XXXI

Argentina’s currency problems forced foreign investors, such as Wal-‐Mart and Casino, to freeze further

expansion in Argentina. Cencosud took advantage of the static business environment and in 2004

acquired Disco, the nation second largest supermarket chain, which accounted for 19.2% of the market

share. XXXII

By early 2006, as the Argentine recession was threatening to slow down Cencosud’s growth, the firm

started looking into alternative markets to continue its expansion process in Latin America.

2007 – 2011: Expansion to Colombia, Peru and Brazil Cencosud decided to enter the Colombian market in 2007 through a joint venture with giant French

retailer Casino. Cencosud hold a 70% stake in this partnership and Casino the remaining 30%. The

rationale behind this strategic alliance, called Easy Colombia, was two-‐fold. First, Cencosud wanted to

take advantage of Casino’s local market knowledge. And second, both parties wanted to set a framework

to potentially enter other markets in Latin America.XXXIII

The same year, the company entered the Peruvian market, when it acquired Grupo Wong, the top

operator of supermarkets and shopping centers. The $500 million acquisition allowed Cencosud to

become the largest supermarket operator in the country.

Expansion in Brazil helped Cencosud to position the firm as a regional retail powerhouse. Growth came in

large part from a steady acquisition campaign, which cost the company over $2 billion. XXXIV In 2008 the

firm purchased the GBarbosa chain and two years later the firm added Perini, Mercantil Rodrigues, Super

Familia and Bretas supermarket chains, which allowed the firm to double its presence in Brazil.XXXV

Recently, in 2011, the company acquired the Cardoso supermarket chain and took over Prezunic in Rio de

Janeiro. This last move allowed Cencosud to become the fourth largest supermarket chain in Brazil, after

Pão de Açúcar, Carrefour Brazil and Wal-‐Mart Brazil.

Looking ahead: Growth in current markets vs. untapped markets Cencosud has been considering the idea of expanding into new markets. Mexico represent an attractive

destination for Cencosud due to its growing middle class, a retail sector that is expected to grow by 12%

by 2014 and a population of 110 million people. XXXVI However, it has also proved to be one of the most

challenging markets in Latin America for the retail sector. Many multinational players, like Carrefour, have

The Fuqua School of Business at Duke University

9

been unsuccessful in exploring the Mexican market, where the $49.4 billion WalMex, the largest grocery

store chain in the country, rests strong and dominates.XXXVII Additionally, entering the Mexican market

would require a significant investment for Cencosud. Another market Cencosud is considering is Panama.

The country has become one of the fastest and best managed markets. While the country population

doesn’t reach the 3.5 million people, a US dollar-‐based economy and the rapid growth in infrastructure

and real state might position Panama as a very attractive destination for Cencosud.XXXVIII

At the same time, penetration of the retail sector in Brazil, Colombia and Peru remains low.2 While the

company understands additional acquisitions will be required to consolidate its presence in these markets

and close the gap with local competitors, Cencosud has to be careful when choosing its next step. Should

they continue pursuing its aggressive diversification strategy and expand into new markets, or should

they consolidate its market position in Peru, Colombia and Brazil?

Carrefour Colombia

Carrefour is a French multinational retailer headquartered in Boulogne Billancourt, France, in Greater

Paris. It’s one of the largest hypermarket chains in the world (with 1,452 hypermarkets at the end of

2011), the fourth largest retail group in the world in terms of revenue (after Wal-‐Mart, Tesco and Costco),

and the third in profit (after Wal-‐Mart and Tesco). In 1973 it began its international expansion by opening

its first hypermarket in Spain, under the store Pryca banner. Later on 1975, Carrefour arrived to Latin

America by opening a hypermarket in Brazil.

The still undergoing European crisis damaged Carrefour’s European operations. Carrefour has struggled in

recent years with lower sales and strategic mistakes. Analysts attribute its poor performance to

overreliance on its outdated hypermarkets and to fierce competition in Western Europe. The newly

appointed CEO, George Plassat, has a three-‐year plan where he will prioritize lowering the company's

financial costs and review the company's operations in some markets.

Carrefour Colombia (see Exhibit 8 for financial information) proved to be a successful venture, since its

arrival in Colombia in 1997 the company operates 72 hypermarkets, 16 convenience stores and 4 cash

and carry store with some 400,000 sqm of sales area, representing revenues over $2 billion, establishing

itself as the second largest supermarket chain in Colombia with a market share of some 17%XXXIX.

2 As of December 2011

The Fuqua School of Business at Duke University

10

Cencosud and the Colombian market

Although Cencosud has displayed a longtime interest in growing its presence in Colombia, the firm has

not been successful in penetrating the market. In 2006, Cencosud offered to buy 25% of Almacenes Exito

(Colombia’s food retailer). However, the offer didn’t go through and Almacenes Exito remained in the

hands of the Casino Group and the Toro Family. The next year, Cencosud secured a joint venture

agreement with the Casino Group to develop Cencosud’s home improvement stores in Colombia.

However, the partnership has been unsuccessful in growing the number of stores due to real state

unavailability in urban areas. On June of this year, the Company manifested its interest of expanding its

business in Colombia, but they explicitly mentioned that there were no acquisition plans in this country

for the nearest future.

Principal players interested in the transaction

After several months of work, on September 2010, Credit Suisse distributed invitations to strategic

participants to take part in the sales process of Carrefour Colombia. This meant that the process was

going to be a very competitive one. Cencosud knew its rivals, Wal-‐mart and Falabella, were interested in

growing its operations in the Colombian market. Cencosud understood that, if they finally decide to go

ahead with the acquisition, they would have to bear some additional risks in order to beat its competitors

and secure its offer.

Going forward Juan Manuel was at a crossroads. The acquisition of Carrefour Colombia was certainly a unique

opportunity for Cencosud to penetrate the growing Colombian market (Exhibit 9 details growth

perspectives in the Colombian market). It would allow them to enter the supermarket sector, but also, by

acquiring real state in urban areas, they could grow the home improvement and shopping center

segments.

However, Juan Manuel recognized certain risks. This transaction would represent the largest acquisition

in the history of Cencosud. Although the firm has proved to be an extraordinary supermarket operator,

this acquisition would stress Cencosud debt levels and would probably require a capital increase. Also,

Cencosud could not continue operating with the Carrefour brand. The firm would have to invest in a

massive marketing campaign to introduce Cencosud brands, Jumbo and Maxi, to the Colombian market.

As the company did not have any experience in rebranding, he was concerned about the results.

The Fuqua School of Business at Duke University

11

Juan Manuel had a few options and needed to act fast. Should he start a very thorough due diligence

process to make sure the acquisition was the best move for Cencosud, and then disclose his findings to

the board? Should he reach out immediately to Mr. Paulmann and explain why he believed Cencosud had

to acquire Carrefour Colombia before its competitors? Or, should he decide not to participate in the sales

process and wait for another opportunity once he acquires more experience in his role as CFO? With

these questions in mind, Juan Manuel knew that his restlessness was justified.

The Fuqua School of Business at Duke University

12

Exhibit 1: Chi lean main retai l p layers

Exhibit 2: Project ions Of Food Retai l in Colombia

Year $ Billion COP billion € Billion % Growth 2013 68.7 128,503.2 51.7 6.4% 2014 73.1 136,614.1 55.0 6.3% 2015 78.0 145,888.3 58.7 6.8% 2016 83.3 155,717.1 62.7 6.7% 2017 88.9 166,208.6 66.9 6.7% 2018 94.8 177,311.6 71.4 6.7% CAGR: 2013–18 6.7%

Exhibit 3: Brand Portfol io by CountryXL

Company Supermarkets Department Stores

Home Improvement

Sales 2011(in $ million)

EBITDA 2011(in $ million)

Market Cap. 2011

(in $ million)

Total Square Feet 2011

Latam Footprint 2011

Other brands in Latammarkets

$15,749 $1,436 $13,107 27.6 millionChile, Argentina,Peru, Brazil, Colombia

$10,633 $1,591 $18,710 18.9 millionChile, Peru, Argentina, Colombia

NA NA $5,394 $531 $3,172 7.5 million Chile

NA NA $2,474 $221 $1,845 3.9 million Chile, Peru

NA NA $344 N.M. $278 2.0 million Chile, Colombia

NA NA $471 $46 $235 0.9 million Chile

The Fuqua School of Business at Duke University

13

Exhibit 4: Revenue and EBITDA breakdown by business segmentXLI

74%

12%

9%

2% 3%

Revenue By Business Segment

Supermarkets

Home Improvement

Department Stores

Shopping center

Financial Services

55%

12%

6%

14%

13%

EBITDA by Business Segment

Supermarkets

Home Improvement

Department Stores

Shopping center

Financial Services

The Fuqua School of Business at Duke University

14

Exhibit 5: Cencosud t imel ineXLII

Exhibit 6: Cencosud’s revenues by country in 2011

Source: Cencosud 2011 Annual Report.

The Fuqua School of Business at Duke University

15

Exhibit 7: Cencosud Formats, Market Posit ion and BrandsXLIII

The Fuqua School of Business at Duke University

16

Exhibit 8: Carrefour Colombia F inancial Information (a l l f igures in COP$ ‘000)

Income Statement

REVENUES $3,959,771,118COST OF GOODS SOLD $3,172,582,701GROSS MARGIN $787,188,417ADMINISTRATIVE EXPENSES $364,924,341SALES EXPENSES $332,795,906OPERATIONAL INCOME $89,468,170NON OPERATIONAL INCOME $95,701,140NON OPERATIONAL EXPENSES $120,728,888INTEREST EXPENSE $32,087,528PROFIT BEFORE TAXES $64,440,422TAXES $19,148,431NET PROFIT $45,291,991

DEPRECIATION EXPENSE $141,593,791

The Fuqua School of Business at Duke University

17

Balance Sheet

CASH%AND%CASH%EQUIVALENTS $9,685,803SAVINGS%ACCOUNTS $50,503,730SUBTOTAL $60,189,533SHORT%TERM%INVESTMENTS $542,478,532ACCOUNTS%RECEIVABLE $80,720,041TRADE%AND%OTHER%RECEIVABLES $22,959,804SHORT%TERM%PROMISES%OF%SALE $23,019,262DEPOSITS $1,129,824OTHR%SHORT%TERM%PROMISES%OF%SALE $59,804,073INCOME%RECEIVABLE $296,206TAX%ADVANCES $42,541,929SHORT%TERM%CLAIMS $8,032,351RECEIVABLES%FROM%EMPLOYEES $54,476OTHER%RECEIVABLES $1,244,915DOUBTFUL%ACCOUNTS $8,046,552SHORTDTERM%PROVISIONS $8,046,551SUBTOTAL%SHORT%TERM%DEBTORS $239,802,882OUTSOURCED%GOODS $378,528,221INTRANSIT%INVENTORIES $10,704,918PROVISIONS $26,204,794INVENTORY%SUBTOTAL $363,028,345PREPAID%EXPENSES $7,765,767DEFERRED%SUBTOTAL $7,765,767TOTAL%CURRENT%ASSETS $1,213,265,059INVESTMENTS $37,084PROMISES%OF%SALE $22,283,624VARIOUS%DEBTORS $29,632,708SUBTOTAL%LONG%TERM%DEBTORS $51,916,332PROPERTY,%PLANT%AND%EQUIPMENT $1,839,467,700COMMERCIAL%CREDIT $92,092,956RIGHTS $141,074,209ACCUMULATED%DEPRECIATION $20,373,286SUBTOTAL%INTANGIBLES $212,793,879DEFERRED%CHARGES $218,167,045ACCUMULATED%DEPRECIATION $69,282,873SUBTOTAL%DEFERRED $148,884,172ART%AND%CULTURE%PROPERTY $18,094SUBTOTAL%OTHER%ASSETS $18,094FIXED%ASSETS $535,765,945SUBTOTAL%VALUATIONS $535,765,945TOTAL%NONCURRENT%ASSETS $2,788,883,206TOTAL%ASSETS $4,002,148,265

The Fuqua School of Business at Duke University

18

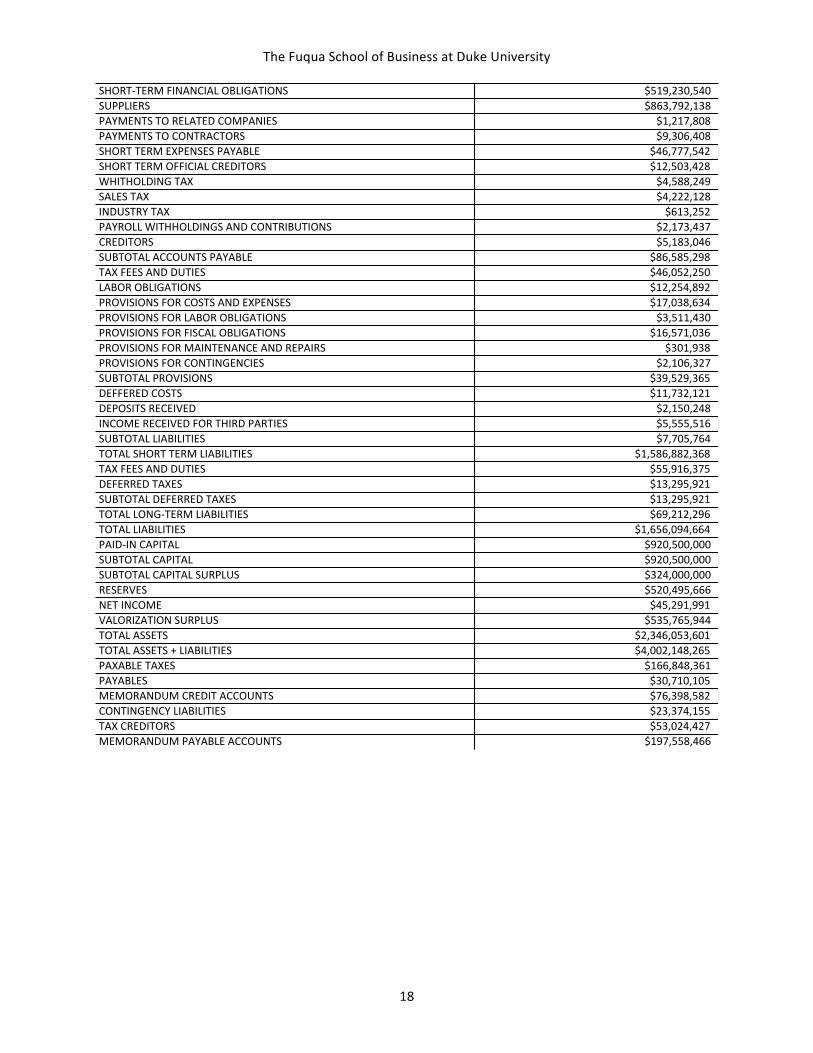

SHORT&TERM)FINANCIAL)OBLIGATIONS $519,230,540SUPPLIERS $863,792,138PAYMENTS)TO)RELATED)COMPANIES $1,217,808PAYMENTS)TO)CONTRACTORS $9,306,408SHORT)TERM)EXPENSES)PAYABLE $46,777,542SHORT)TERM)OFFICIAL)CREDITORS $12,503,428WHITHOLDING)TAX $4,588,249SALES)TAX $4,222,128INDUSTRY)TAX $613,252PAYROLL)WITHHOLDINGS)AND)CONTRIBUTIONS $2,173,437CREDITORS $5,183,046SUBTOTAL)ACCOUNTS)PAYABLE $86,585,298TAX)FEES)AND)DUTIES $46,052,250LABOR)OBLIGATIONS $12,254,892PROVISIONS)FOR)COSTS)AND)EXPENSES $17,038,634PROVISIONS)FOR)LABOR)OBLIGATIONS $3,511,430PROVISIONS)FOR)FISCAL)OBLIGATIONS $16,571,036PROVISIONS)FOR)MAINTENANCE)AND)REPAIRS $301,938PROVISIONS)FOR)CONTINGENCIES $2,106,327SUBTOTAL)PROVISIONS $39,529,365DEFFERED)COSTS $11,732,121DEPOSITS)RECEIVED $2,150,248INCOME)RECEIVED)FOR)THIRD)PARTIES $5,555,516SUBTOTAL)LIABILITIES $7,705,764TOTAL)SHORT)TERM)LIABILITIES $1,586,882,368TAX)FEES)AND)DUTIES $55,916,375DEFERRED)TAXES $13,295,921SUBTOTAL)DEFERRED)TAXES $13,295,921TOTAL)LONG&TERM)LIABILITIES $69,212,296TOTAL)LIABILITIES $1,656,094,664PAID&IN)CAPITAL $920,500,000SUBTOTAL)CAPITAL $920,500,000SUBTOTAL)CAPITAL)SURPLUS $324,000,000RESERVES $520,495,666NET)INCOME $45,291,991VALORIZATION)SURPLUS $535,765,944TOTAL)ASSETS $2,346,053,601TOTAL)ASSETS)+)LIABILITIES $4,002,148,265PAXABLE)TAXES $166,848,361PAYABLES $30,710,105MEMORANDUM)CREDIT)ACCOUNTS $76,398,582CONTINGENCY)LIABILITIES $23,374,155TAX)CREDITORS $53,024,427MEMORANDUM)PAYABLE)ACCOUNTS $197,558,466

The Fuqua School of Business at Duke University

19

Exhibit 9: Growth Perspectives for the Colombian Market

The Fuqua School of Business at Duke University

20

Bibliography

1. Carrefour Group Site. History. http://www.carrefour.com/content/history 2. The Wall Street Journal. “Carrefour Loss Narrows”. NADYA MASIDLOVER.

http://www.wsj.com/articles/SB10000872396390444914904577620680509686036 3. The Wall Street Journal. “Carrefour Names CEO for Retail Turnaround”. Passsariello, Masidlover and

Landauro. January 31, 2012. http://www.wsj.com/articles/SB10001424052970204740904577192192183472350

4. Reuters. “Carrefour faces tough choices to fund revival”. Aug 22, 2012.http://www.reuters.com/article/2012/08/22/carrefour-‐funding-‐idUSL6E8IV4HE20120822

Sources

I Market Line – Chile food and apparel retail II “La historia del Retail en Chile”. http://archivosuai.eclass.cl/comunidad/articulo/45296/la-‐historia-‐del-‐retail-‐en-‐chile III Ibid. IV Falabella Conference – Citibank, NYC, March 2012. V Cencosud Presentation – 2008. VI Economia y Negocios. http://www.economiaynegocios.cl/noticias/noticias.asp?id=27645 VII Argentina Retail Report Q3 2011 – Research and Markets. VIII Market Line – Argentina food retail. IX CorpResearch – Retail Sector Report. X Thomas White International. http://www.thomaswhite.com/global-‐perspectives/retail-‐sector-‐in-‐brazil-‐riding-‐the-‐wave-‐of-‐middle-‐class-‐growth-‐and-‐consumer-‐credit-‐boom/ XI Market Line – Brazil food retail. XII Thomas White International. http://www.thomaswhite.com/global-‐perspectives/retail-‐sector-‐in-‐brazil-‐riding-‐the-‐wave-‐of-‐middle-‐class-‐growth-‐and-‐consumer-‐credit-‐boom/ XIII ADVFN, “With Brazil Acquisition, Chile Cencosud Flexes Its Muscle”, 2011, http://www.advfn.com/nyse/StockNews.asp?stocknews=WMT&article=44834315 XIV Market Line – Brazil apparel retail. XV My EIU, “Cencosud leads Chilean incursion into Colombian market”, October 2012, http://country.eiu.com/article.aspx?articleid=181377802&Country=Chile&topic=Economy&oid=1391538923&flid=1579732542 XVI Market Line – Colombia Food Retail XVII Market Line – Colombia food retail XVIII CorpResearch – Retail Sector Report. XIX PwC Mexico retail sector report XX Market Line – Mexico food retail. XXI CorpResearch – Retail Sector Report. XXII Market Line – Mexico food retail XXIII Ibid. XXIV Cencosud Annual Report 2011, http://www.cencosud.com/wp-‐content/files_mf/memoria201142.pdf XXV Cencosud Report. “Roadshow Presentation”, June 2012, http://www.cencosud.com/wp-‐content/files_mf/6.enginvestorpresentationjune201237.pdf XXVI Cencosud. “Financial Retailing”, http://www.cencosud.com/en/unidades-‐de-‐negocio/retail-‐financiero/ XXVII Cencosud Annual Report 2011. “Business Strategy”, http://www.cencosud.com/wp-‐content/files_mf/memoria201142.pdf XXVIII Funding Universe http://www.fundinguniverse.com/company-‐histories/cencosud-‐s-‐a-‐history/ XXIX Funding Universe http://www.fundinguniverse.com/company-‐histories/cencosud-‐s-‐a-‐history/ XXX Funding Universe http://www.fundinguniverse.com/company-‐histories/cencosud-‐s-‐a-‐history/

The Fuqua School of Business at Duke University

21

XXXI Funding Universe http://www.fundinguniverse.com/company-‐histories/cencosud-‐s-‐a-‐history/ XXXII Progressive Grocer, “Cencosud Reaches Agreement to Acquire Disco From Ahold”, November 2003, http://www.progressivegrocer.com/node/64253?sort_order=ASC XXXIII Business Wire, “Casino Announces Its Intention to Enter into a Joint Venture with Cencosud to Develop The DIY (Do-‐It-‐Yourself) and Home Improvement Retail Business in Colombia”, May 2007, http://www.businesswire.com/news/home/20070502005473/en/Casino-‐Announces-‐Intention-‐Enter-‐Joint-‐Venture-‐Cencosud#.VN0aDy79yRg XXXIV Merger Market report, “Clash of the Titans”, September 2012 XXXV Bloomberg, “Cencosud Climbs on Purchase of Brazilian Grocery Chain”, October 2010, http://www.bloomberg.com/news/articles/2010-‐10-‐18/chile-‐s-‐cencosud-‐buys-‐brazil-‐retailer-‐bretas-‐in-‐biggest-‐deal-‐in-‐five-‐years XXXVI ATKearney Report, “2011 Global Retail Development Index”, 2011 XXXVII Merger Market report, “Clash of the Titans”, September 2012 XXXVIII ATKearney Report, “2011 Global Retail Development Index”, 2011 XXXIX Santander Investment research department XL Cencosud Report. “Roadshow Presentation”, June 2012, http://www.cencosud.com/wp-‐content/files_mf/6.enginvestorpresentationjune201237.pdf XLI Ibid XLII Ibid XLIII Ibid