ceat ceat ltd. rpg house worli, mumbai 400030, india · worli, mumbai 400030, india +91 22 24930621...

TRANSCRIPT

CEAT

November 19, 2018

CEAT LTD.

RPG House

463 Dr. Annie Besant Road,

Worli, Mumbai 400030, India

+91 22 24930621

CIN: L25100MH1958PLC011041

www.ceat.com

BSE limited,

Corporate Service Department,

1st Floor, P.J. Towers,

The National Stock Exchange of India Limited,

Exchange Plaza, 3cd Floor,

Plot No. C/1, "G" Block,

Dalal Street, Bandra Kurla Complex,

Mumbai 400 001 Band ra East,

Mumbai 400 051

Security Code: 5001178 Symbol: CEATLTD

Sub: Investor conference participation - Disclosure under Reg. 30

Dear Sir/Madam,

Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements)

Regulations, 2015 read with Part A of Schedule III and Company's Policy on Determination of

Materiality of Events, please find below details of the investors conference which will be

participated by the Company along with the presentation to be made at the same:

Date Particulars

November 19, 2018 Conference arranged by !DFC

Kindly take the same on record and acknowledge receipt.

Thanking you,

Sincerely,

For CEAT Limited

Encl. A/a

location

Grand Hyatt, Kalina, Mumbai

An®Rr'GCompany

An Group Company

Q2 FY19 – Investor Presentation

This presentation may include statements which may constitute forward-looking statements. All statements that address expectations or projections about thefuture, including, but not limited to, statements about the strategy for growth, business development, market position, expenditures, and financial results, areforward looking statements. Forward looking statements are based on certain assumptions and expectations of future events. The Company cannot guaranteethat these assumptions and expectations are accurate or will be realized. The actual results, performance or achievements, could thus differ materially fromthose projected in any such forward-looking statements.

The information contained in these materials has not been independently verified. None of the Company, its Directors, Promoter or affiliates, nor any of its ortheir respective employees, advisers or representatives or any other person accepts any responsibility or liability whatsoever, whether arising in tort, contractor otherwise, for any errors, omissions or inaccuracies in such information or opinions or for any loss, cost or damage suffered or incurred howsoever arising,directly or indirectly, from any use of this document or its contents or otherwise in connection with this document, and makes no representation or warranty,express or implied, for the contents of this document including its accuracy, fairness, completeness or verification or for any other statement made orpurported to be made by any of them, or on behalf of them, and nothing in this document or at this presentation shall be relied upon as a promise orrepresentation in this respect, whether as to the past or the future. The information and opinions contained in this presentation are current, and if not statedotherwise, as of the date of this presentation. The Company undertake no obligation to update or revise any information or the opinions expressed in thispresentation as a result of new information, future events or otherwise. Any opinions or information expressed in this presentation are subject to changewithout notice.

This presentation does not constitute or form part of any offer or invitation or inducement to sell or issue, or any solicitation of any offer to purchase orsubscribe for, any securities of CEAT Limited (the “Company”), nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on inconnection with, any contract or commitment therefore. Any person/ party intending to provide finance / invest in the shares/businesses of the Company shalldo so after seeking their own professional advice and after carrying out their own due diligence procedure to ensure that they are making an informeddecision. This presentation is strictly confidential and may not be copied or disseminated, in whole or in part, and in any manner or for any purpose. No personis authorized to give any information or to make any representation not contained in or inconsistent with this presentation and if given or made, suchinformation or representation must not be relied upon as having been authorized by any person. Failure to comply with this restriction may constitute aviolation of the applicable securities laws. The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possessionthis presentation comes should inform themselves about and observe any such restrictions. By participating in this presentation or by accepting any copy of theslides presented, you agree to be bound by the foregoing limitations.

Disclaimer

Section 1: RPG Group Overview

Section 3: Operational & Financial Overview

Section 2: Business Overview

5-6

19-26

8-17

Table of Contents

Section 1: RPG Group Overview

KEC International

World leader in Power

TransmissionEPC space

CEAT

One of India’s leading

manufacturer of automobile tyres

ZensarTechnologies

Softwareservices provider spread across 20

countries,400+ customers.

RPG Life Sciences

Pharma company with

wide range medicines in

global generics and synthetic

APIs.

Raychem RPG

Engineering products and

servicescatering to

infrastructure segment

of the economy.

Harrisons Malayalam

One of India’s largest plantation companies with tea, rubber and

other agro products.

RPG Enterprises was founded in 1979. The group currently operates in various

industries - Infrastructure, Technology, Life Sciences, Plantations and TyreManufacturing. The group has a history of business dating back to 1820 AD in

banking, textiles, jute and tea. The Group grew in size and strength with several

acquisitions in the 1980s and 1990s. CEAT became a part of the RPG Group in 1982,which is now one of India’s fastest growing conglomerates with 20000+ employees,

presence in 100+ countries and annual gross revenues of ~$3 Bn.

RPG Group: Powered by Passion, Driven by Ethics

UNLEASHTALENT

TOUCHLIVES

OUTPERFORM

AND☺

5

FY14-18 CAGR: EBITDA 8.0% PAT 11.7%

Note:1) ROCE is calculated by taking EBIT*(1-ETR) divided by Capital Employed2) ROE is calculated by taking PAT divided by Net-worth3) Market Cap updated till 18th July 2018

FY14-18CAGR: 4.9%

RPG Group: Key Financials

6

17,94919,183 19,271 20,052

21,766

FY14 FY15 FY16 FY17 FY18

Gross Total Income (Rs Cr.)

1,630 1,668

2,014 2,0452,218

663 739879

980 1,031

FY14 FY15 FY16 FY17 FY18

EBITDA PAT

3,8074,611

5,260

6,066

6,925

17.4%16.0% 16.7% 16.2% 14.9%

12.1% 10.6% 11.6% 12.3% 12.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

FY14 FY15 FY16 FY17 FY18

Net Worth ROE ROCE

19,260

4,442

7,182

6,260

0

5,000

10,000

15,000

20,000

25,000

30,000

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18

Market Cap

Group CEAT KEC Zensar

Section 4: Business OverviewSection 2: Business Overview

Harsh Vardhan GoenkaChairman, Non Executive Director

Anant Vardhan GoenkaManaging Director

Arnab BanerjeeWhole -Time Director

Atul C. ChokseyNon Executive

Independent Director

Hari L. MundraNon Executive

Non Independent Director

Mahesh S. GuptaNon Executive

Independent Director

Paras K. ChowdharyNon Executive

Independent Director

Punita LalNon Executive

Independent Director

Ranjit PanditNon Executive

Independent Director

S. DoreswamyNon Executive

Independent Director

Vinay BansalNon Executive

Independent Director

Board of Directors

Haigreve KhaitanNon Executive

Independent Director

8

Pierre E. CohadeNon Executive

Non Independent Director

Anant Goenka

Managing Director Chief Financial Officer

Arnab Banerjee

Executive Director- Operations

Tom Thomas

Executive Director - Projects & Chief Mentor Technology

Dilip Modak Chandrashekhar Ajgaonkar

Senior Vice President- Manufacturing

Senior Vice President- Quality Based Management

Kumar Subbiah

9

Leadership Team

Milind Apte

Senior Vice President- Human Resources

Peter Becker

Senior Vice President- R&D and Technology

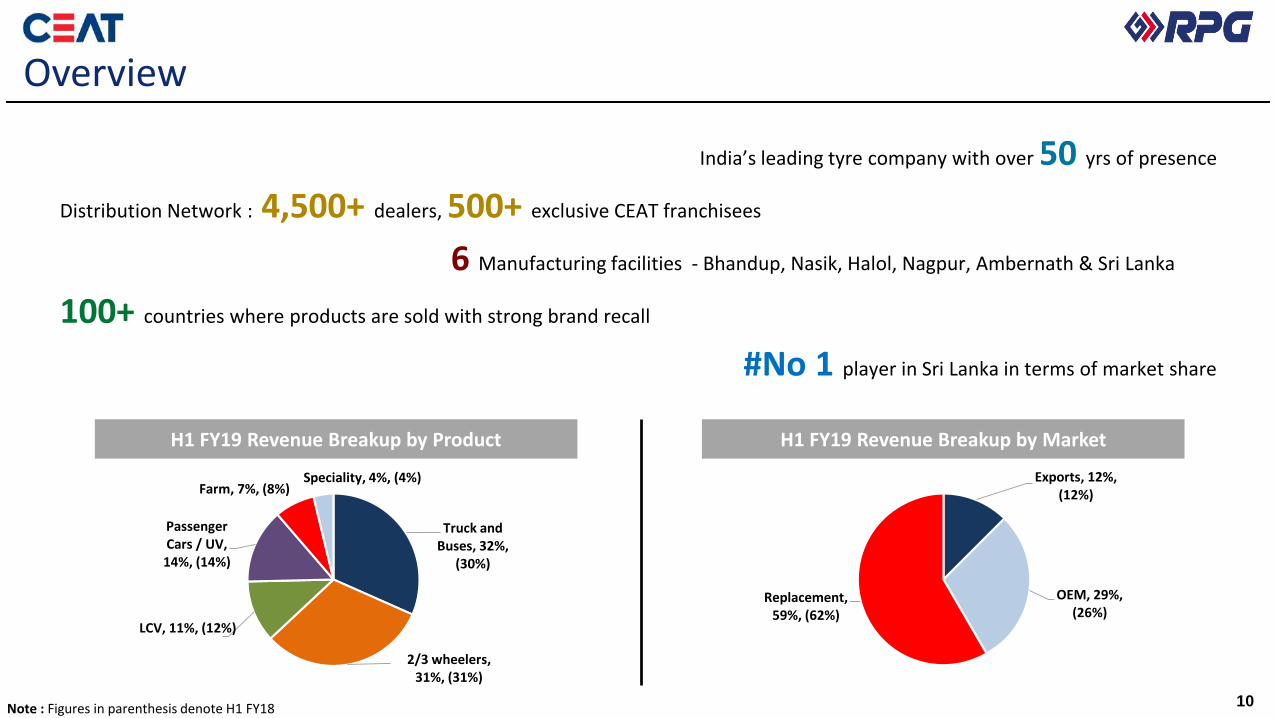

India’s leading tyre company with over 50 yrs of presence

Distribution Network : 4,500+ dealers, 500+ exclusive CEAT franchisees

6 Manufacturing facilities - Bhandup, Nasik, Halol, Nagpur, Ambernath & Sri Lanka

100+ countries where products are sold with strong brand recall

#No 1 player in Sri Lanka in terms of market share

H1 FY19 Revenue Breakup by Product H1 FY19 Revenue Breakup by Market

10

Overview

Note : Figures in parenthesis denote H1 FY18

Exports, 12%, (12%)

OEM, 29%, (26%)

Replacement, 59%, (62%)

Truck and Buses, 32%,

(30%)

2/3 wheelers, 31%, (31%)

LCV, 11%, (12%)

Passenger Cars / UV, 14%, (14%)

Farm, 7%, (8%)Speciality, 4%, (4%)

11

Strategy

Differentiated Products1

Strong Brand2

Extensive Distribution3

Deep OEM Partnerships4

World Class R&D5

Expanding Global Reach6

✓ Two wheelers

✓ Passenger cars & Utility vehicles

Profitable growth

✓ Off Highway Tyres

✓ Passenger Segments

Domestic Market

International Market

12

Differentiated Products1

Key developments

▪ Focus on OEM, recent entriesin new models – Ashok LeylandDost, Mahindra E Alpha, BajajNew Platina, Honda Cliq, AshokLeyland Stag and Partner, TorkT6X, Hero Motocorp Achiever150, Renault Kwid, HimalayanABS (Royal Enfield), The AceDeluxe – Cleveland Cycleworks

▪ Recent entries into OEM’sexisting models – Bajaj Pulsar150, Honda (Livo, Shine andDream Yuga), Bajaj Pulsar 160,Tata Motors TBR, AL PartnerLCV, Escort Tractors, Wagon R,Zylo, Daimler Truck Radials,Suzuki Gixxer, RE Classic,Yamaha FZ, Volvo etc.

▪ Platforms like Fuelsmart, Gripp,Mileage X3, SecuraDrive etc.

New Entries and Supplier to OEM’s

13

Strong Brand2

CEAT became the official tyre partner of Torino FC, an elite Serie A football club based in Italy

CEAT’s SecuraDrive platformtargeting Superior Control at Higher Speed

No. of CEAT Shoppes

▪ 4,500+ dealers

▪ 500+ CEAT Franchisees (Shoppes + Hubs)

▪ 280+ two-wheeler distributors

▪ Developed Multi Brand Outlet / Shop in Shop model over last 2 years.

Over 400 outlets so far

▪ Launched CEAT Bike Shoppes in Bangalore and Kolkata

Distribution Network

14

Extensive Distribution

District coverage

3

Shoppe Shop in Shop (SIS)

Multi Brand Outlet (MBO) Bike Shoppe

212

464

601

FY12 FY15 FY18

102

~350

FY12 FY18

15

Deep OEM Partnerships4

16

World Class R&D5

▪ State of the art R&D facility at Halol plant

▪R&D focussed on development of breakthrough

products, alternate materials, green tyres &

smart tyres

▪Partnerships with global institutes and

technology partners

Breakthrough Products

▪ “Puncture Safe” tyres for Two Wheelers – India’s 1st Self Sealing tyre

▪ “FuelSmarrt Tyres” for Passenger Cars – Reduced rolling resistance, less fuel consumption and more savings

▪ “Milaze Tyres” for SUV segment– Higher mileage up to 1,00,000 kilometers

Expanding Global Reach

▪ Exports to 90+ Countries in 7 clusters

▪ Sri Lanka: Manufacturing facility and Leadership position in the market and with 50+% market share

▪ Focused product and distribution strategy for select clusters and countries

Far East 1 Cluster

Africa

Cluster

LATAM

Cluster

Middle East

Cluster

Europe Cluster

US Cluster

Emerging markets

Key Export Clusters

Far East 2 Cluster

6

Section 5: Operational & Financial Overview

Section 3: Operational & Financial Overview

19

Q2 FY19 Operational Highlights

OEM Model EntryManufacturing Excellence

Ace Deluxe Cleveland CycleworksCEAT’s Nagpur plant awarded the

British Safety Council’s ‘Sword of Honor’

Q2 FY19 v/s Q1 FY19 (Q-o-Q)

▪ Net revenue from operations increased by 2.8% at INR

1,755 Crs from INR 1,706 Crs

▪ Gross margins remained flattish at 39.3%

▪ EBITDA stood at INR 165 Crs compared to INR 181 Crs;

margins at 9.4% from 10.6%

▪ PAT stood at INR 63 Crs compared to INR 71 Crs

▪ Debt / equity at 0.34x compared to 0.28x

20

Consolidated: Q2 FY19 Financial Highlights

Q2 FY19 v/s Q2 FY18 (Y-o-Y)

▪ Net revenue from operations increased by 15.2% at INR

1,755 Crs from INR 1,523 Crs

▪ Gross margins contracted marginally to 39.3% from 39.4%

▪ EBITDA stood at INR 165 Crs compared to INR 181 Crs;

margins at 9.4% from 11.9%

▪ PAT stood at INR 63 Crs compared to INR 73 Crs

▪ Debt / equity at 0.34x compared to 0.41x

Rev

en

ue

gro

wth

Mar

gin

tre

nd

s

21

Consolidated: Financial Trends

NoteFY16 onwards the figures are per IND AS; Other financial figures are as per IGAAP as published in previous periodsFY16 onwards the Company’s investment in Sri Lanka JV is accounted using Equity method under IND AS which was earlier consolidated using proportionate consolidation methodFY16 onwards the EBITDA includes profit from Sri Lanka JVEBITDA does not include Non- operating income

5,508 5,705 5,447 5,722 6,231

1,706 1,755

FY 14 FY15 FY16 FY17 FY18 Q1 FY19 Q2 FY19

Net Sales (Rs Cr)

658 680 809

685 638

181 165

11.9% 11.9%

14.9%

12.0%10.2% 10.6%

9.4%

FY 14 FY15 FY16 FY17 FY18 Q1 FY19 Q2 FY19

EBITDA (Rs Cr)

EBITDA to NetSales %

PAT

tre

nd

s

NotesFY16 onwards the figures are per IND AS; Other financial figures are as per IGAAP as published in previous periods 22

Consolidated: Financial Trends

271 317

438 361

233

71 63

4.9%5.6%

8.0%

6.3%

3.7%4.2%

3.6%

0.0 %

1.0 %

2.0 %

3.0 %

4.0 %

5.0 %

6.0 %

7.0 %

8.0 %

9.0 %

-

50

100

150

200

250

300

350

400

450

500

FY 14 FY15 FY16 FY17 FY18 Q1 FY19 Q2 FY19

PAT (Rs Cr)

PAT to Net Sales%

23

Consolidated: Q2 FY19 Financials

NotesFigures are as per IND AS Company’s investment in Sri Lanka JV is accounted using Equity method under IND AS which was earlier consolidated using proportionate consolidation methodEBITDA includes profit from Sri Lanka JVEBITDA does not include Non- operating income

Parameter Q2 FY18 Q1 FY19 Q2 FY19 QoQ YoY

Net Revenue from operations 1,523 1,706 1,755 3% 15%

Raw Material 923 1,035 1,065 3% 15%

Gross margin 600 671 690 3% 15%

Gross margin % 39.4% 39.3% 39.3% Flattish -8 bps

Employee Cost 111 119 142 19% 28%

Other Expenses 314 377 389 3% 24%

EBITDA 181 181 165 -9% -9%

EBITDA % 11.9% 10.6% 9.4% -118 bps -249 bps

Finance Cost 24 20 19 -9% -22%

Depreciation 41 46 48 4% 17%

Operating PBT 117 114 99 -14% -15%

Exceptional expense 8 2 2 -13% -75%

Non-Operating income 6 4 3 -11% -49%

PBT 115 116 100 -13% -13%

PAT 73 71 63 -12% -14%

De

bt

bre

aku

pLe

vera

ge r

atio

s

Total Debt (INR Cr)

1174 775 663 872

24

Consolidated: Leverage / coverage Profile

NoteFY16 onwards the figures are per IND AS; Other financial figures are as per IGAAP as published in previous periodsCompany’s investment in Sri Lanka JV is accounted using Equity method under IND AS which was earlier consolidated using proportionate consolidation methodEBITDA includes profit from Sri Lanka JV; EBITDA does not include Non- operating incomeFor Debt / EBTIDA, quarterly EBITDA has been annualisedFor debt break-up, we have reclassified Current Maturities of Long Term Debt under Long Term debt

924 755 943

658 680809

685638

181 165

1.8 1.1 0.81.3 1.4

1.0 1.43.8

5.2

8.5 8.4

6.6

8.9 8.9

0

100

200

300

400

500

600

700

800

900

FY 14 FY 15 FY 16 FY 17 FY18 Q1 FY19 Q2 FY19

EBITDA (Rs Cr)

Debt / EBITDA(x)

EBITDA /Interest (x)

597

27234

58196 106

363

577

503630

866676

649

5811.14

0.460.32 0.38 0.33 0.28 0.34

FY 14 FY 15 FY 16 FY 17 FY18 Q1 FY19 Q2 FY19

LT Debt (Rs Cr)

ST Debt (Rs Cr)

D/E

NotesFinancials are as per IND ASEBITDA does not include Non- operating income 25

Standalone: Q2 FY19 Financials

Parameter Q2 FY18 Q1 FY19 Q2 FY19 QoQ YoY

Net Revenue from operations 1,512 1,674 1,718 3% 14%

Raw Material 920 1,028 1,058 3% 15%

Gross margin 592 646 660 2% 12%

Gross margin % 39.2% 38.6% 38.4% -15 bps -72 bps

Employee 105 110 132 19% 25%

Other Expenses 306 362 372 3% 22%

EBITDA 182 174 157 -10% -14%

EBITDA % 12.1% 10.4% 9.1% -127 bps -293 bps

Finance Cost 23 15 13 -16% -45%

Depreciation 41 41 44 5% 7%

Operating PBT 118 118 100 -15% -15%

Exceptional expense 1 2 2 -13% 256%

Non-Operating income 8 6 12 118% 46%

PBT 125 121 111 -8% -12%

PAT 83 78 75 -3% -10%

▪ Market Price (October 25): INR 1,049/share

▪ Face Value : INR 10/share

▪ Market Cap (October 25): INR 4,244 Cr

Shareholding Pattern as onSep 30, 2018 Market Information

Source : Capitaline. The above data is updated till 24th October, 2018

26

Equity Shareholding & Price trends

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

Oct/17 Nov/17 Dec/17 Jan/18 Feb/18 Mar/18 Apr/18 May/18 Jun/18 Jul/18 Aug/18 Sep/18 Oct/18

Close Price (Rs) Total Volume

Y O UT H A N K