cdl customer interactive_session_nigeria_2013_macroeconomic_update

TRANSCRIPT

CDL INVESTORS FORUM2013 NIGERIA MACRO-ECONOMIC UPDATES

25TH APRIL 2013

Outline

I The Global Economy 3

II Nigeria Political Updates 4

III Nigeria Macro-economic updates 5

IV Outlook on Inflation 7

V Exchange Rate 9

VI Monetary Policy Rate 11

VII Budget 2013 Crude Oil Estimates 12

VIII JP Morgan Effect on FGN Debt Instruments 13

IX Outlook for the rest of the year 15

X CDL Chronology 16

Global Economy – Key Issues Developed Economies

US Markets hit new records

Japan embarks on ambitious inflation bid

ECB cuts rate to record low of 0.5%

Emerging Markets BRICS aims to set up

devt’ bank to rival the World Bank

If only India will get its politics right

Mixed signals from China

MENA, Sub-Saharan Africa Oil, oil and more oil Ghana in bid to ensure

bond price transparency The Kenyan Anti-climax North Africa in post-

revolution blues Sudan and South Sudan:

“On oil we stand”

Commodities Is Gold fading? IEA & OPEC lower oil

demand forecasts OPEC aims to trim

supply to firm up prices Analysts forecast oil to

remain around $98 - $105 pb in 2013

Nigeria Political Updates… Early kick-off for 2015

In-house politicking within ruling party ahead of 2015

Nigerian Governors’ Forum becomes battle ground

Focus gradually shifts from economic reforms to politics

EIU Latest Ranking: Nigeria is classified as a Hybrid Regime on 120th position below Sierra-Leone, Libya, Haiti and Pakistan

Opposition Parties in Merger Deal A Kenyan inspired model Three (3) APCs emerge Early punts favour ACN faction

within the group (Broom emblem, Fashola, etc.)

Echoes from SDP – NRC era

PDP; 58.9%

APC; 39.8%

Others; 1.3%

A retrospective view of 2011 Presidential elections with a united opposition

Source: CDL Research

1

Nigeria Macroeconomic Updates

The PIB still stuck in the National Assembly!

Power Sector Reforms going well for now

GDP rebasing has been postponed for the umpteenth time

Banking reforms perceived to be successful

CBN Governor opts for single term

Nigeria’s improving economic profile (MINT, Global X Funds, Barclays Bond Index)

Nigeria to raise $1 billion Eurobond to finance power and other infrastructure in June 2013 … NOI

A fumbling and wobbling naira?

2013 Fiscal Scenarios

Scenario I Scenario II Scenario III

Oil Price (USD) 90 100 110

Benchmark Oil Price ($pb) 79 79 79

FGN Debt / GDP 18% 17.5% 17%

Average FX Rate (N/$) 166 – 168 160 – 162 156 – 158

Inflation 15% 9.73% 12%

Official FX Reserves $47.5 b $50 b $55 b

Real GDP Growth 5% 7% 7 – 8%

Monetary Policy Rate 11.75% 12% 12.25%

Sources: Agusto & Co, NBS, CDL Research

Outlook on Inflation

Source: FDHL, NBS

Assumptions on Inflation

The CBN in-house forecasts suggest that the rate of change in headline prices between March and August 2013 will average 9.6% and range between 8.8 – 10% – with the trough being in March.

This implies that the inflation rate may accelerate in the months to come especially as the food planting season kicks off.

CBN will continue to pursue managed tightening monetary policies However we still expect inflation to close the year in single digit,

broadly in line with the NBS’s 9.73% forecast for 2013. Pump price of petrol to remain at N97/l in 2013. Budget 2013

adequately caters for the fuel subsidy No wage pressures in 2013 fiscal year The new tariff regime on Rice & Sugar and imported food inflation

Import duty and levy on raw sugar will be 10% and 50% respectively Refined sugar will attract 20% duty and 60% levy Rice: 10% import duty and 100% levy will be applied to both brown and

polished rice.)

Exchange Rate: How’s the Naira doing?

-

500,000,000.00

1,000,000,000.00

1,500,000,000.00

2,000,000,000.00

2,500,000,000.00

3,000,000,000.00 FX Dd & Ss by CBN

Amount Offered (US$) Total Sold (US$)

FX SS drops on JPMorgan effect

3

Source: FDHL

Nigerian Naira Proving Resilient For Now…

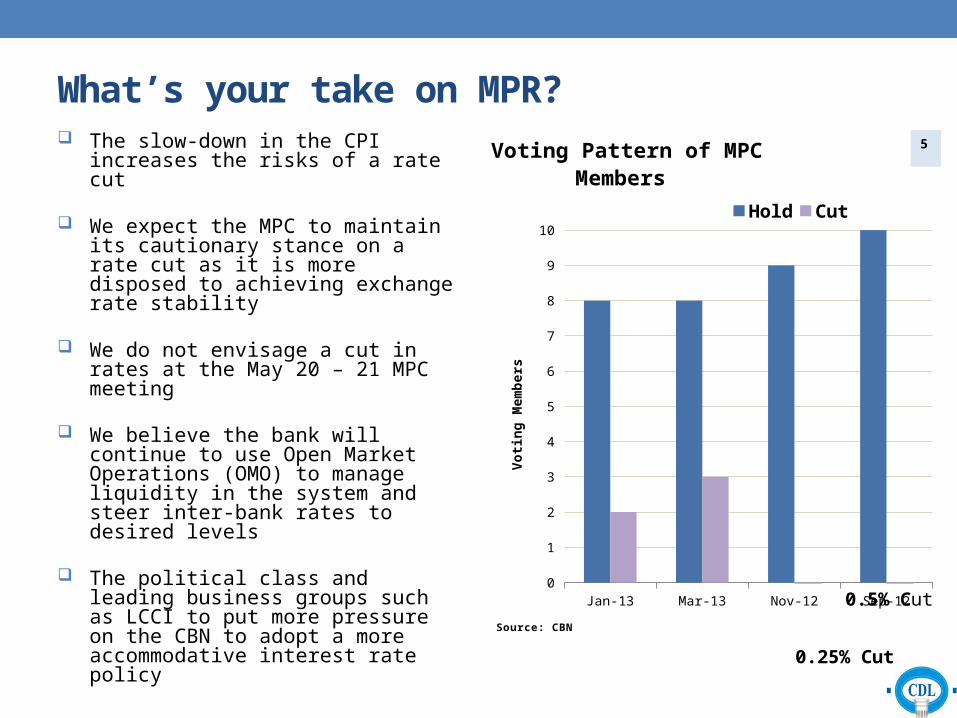

What’s your take on MPR? The slow-down in the CPI increases

the risks of a rate cut

We expect the MPC to maintain its cautionary stance on a rate cut as it is more disposed to achieving exchange rate stability

We do not envisage a cut in rates at the May 20 – 21 MPC meeting

We believe the bank will continue to use Open Market Operations (OMO) to manage liquidity in the system and steer inter-bank rates to desired levels

The political class and leading business groups such as LCCI to put more pressure on the CBN to adopt a more accommodative interest rate policy

Sep-12 Nov-12 Jan-13 Mar-130

1

2

3

4

5

6

7

8

9

10

0.25% Cut

0.5% Cut

Voting Pattern of MPC Members

Hold Cut

Vo

tin

g M

emb

ers

5

Source: CBN

Budget 2013 estimates… Can Nigeria achieve 2.53mbd in oil production in 2013?

Source: CBN Economic Reports

Bond Market – The JP Morgan Effect

Treasury Bills Market

Outlook for the rest of the year

The widening of yields on bonds and treasury bills will present good re-entry levels for FPIs

AMCON bonds to become secondary market trading instruments (Q3, 2013) as appointment of market makers in the offing

IMF call on AMCON to dampen initial appetite for the bonds amongst FPIs

AMCON to exit the three nationalised banks (Q3 – Q4 2013) The success (near to medium term) of the Power Sector Reforms

may be hinged on Transmission (still under pseudo-state control)Oil theft and vandalisation may continue to stymie Nigeria’s crude oil

outputBig Ticket Loan Syndications (Dangote Cement - $3.5b, MTN - $1.8b,

Indorama - $0.8b, Accurgas - $0.225b) kick start credit market Flurry of capital raising by Tier 2 Banks in bid to join syndication clubs

2006 2006 2007 20121996

Commenced operations with N200m in SHF

Net profit crossed the N1b mark

Moved into CDL HOUSE

Appointed PDMM in May-06 by DMO

Appointed Money Market Maker by CBN

CDL’s SHF crossed the N25B threshold

N25b

2012

CDL CHRONOLOGY

Important Risk Warnings and Disclaimers

Consolidated Discounts Limited (CDL) is regulated by the Central Bank of Nigeria (CBN).

USE OF THIS PUBLICATION FOR THE PURPORSE OF MAKING INVESTMENT DECISION EXPOSES YOU TO RISK OF LOSS.

Reception of this publication does not make you a client or provide you with the protection afforded to clients of CDL.

All information is provided for information purposes only. Every effort is made to ensure that all information given in this publication is accurate, but no responsibility can be accepted by CDL Research or the Consolidated Discounts Limited Group, their agents or employees, for any errors or for any loss arising from use of this publication or the information contained herein. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of CDL Research and the Consolidated Discounts Limited Group.

© CDL 2013. All rights reserved. Consolidated Discounts Limited67 MarinaLagos.Tel: +234-1-2778218

www.cdlnigeria.com