cd equisearch p pvt ltd - business...

TRANSCRIPT

CD Equisearch P

Equities Derivatives Commoditie

Shriram Transport Finance Company Ltd.

No. of shares (crore) 22.7

Mkt cap (Rs crs) 21502

Current price (Rs)(08/7/2015) 948

Price target (Rs) 1082

52 week H/L (Rs.) 1287/761

Book value (Rs.)(FV. 10) 408

P/BV (16e/17e) 2.1/1.9

P/E (16e/17e) 17.1/14.9

Beta 1.1

EPS Growth ( FY15/16e/17e) -24.3/22.5/14.3

ROE ( FY15/16e /17e) 11.1/12.3/12.6

Daily Volume (avg. weekly) 59750

BSE Code 511218

NSE Code SRTRANSFIN

Bloomberg SHTF IN

Reuters SRTR.BO

Shareholding pattern % Promoters 26.1

MFs / Banks / FIs 4.2

Foreign 51.4

Govt. Holding 0.00

Non-Promoter Corp. 12.1

Total Public 6.2

Total 100.0

As on March 31, 2015

Recommendation

Accumulate

Analyst

Priyanka Somani

Phone: + 91 (33) 4488 0043

E- mail: [email protected]

Figures in Rs crs

Net Interest Income

Non Interest Income

Pre-Provision Profits

Net Profit

EPS

EPS growth (%)

Pvt Ltd

ities Distribution of Mutual Funds Dis

Ltd.

14.3

6

SRTRANSFIN

FY13 FY14 FY15

3719.38 3751.54 4193.44

237.64 526.44 311.52

3057.62 3216.46 3304.93

1463.43 1357.94 1028.44

64.50 59.85 45.33

11.5 -7.2 -24.3

Company Background

Shriram Transport Finance Company Ltd

NBFC with strong competitive advantage in pre

vehicle (CV) financing (especially 5-12 year old vehicles).

Quarterly Highlights

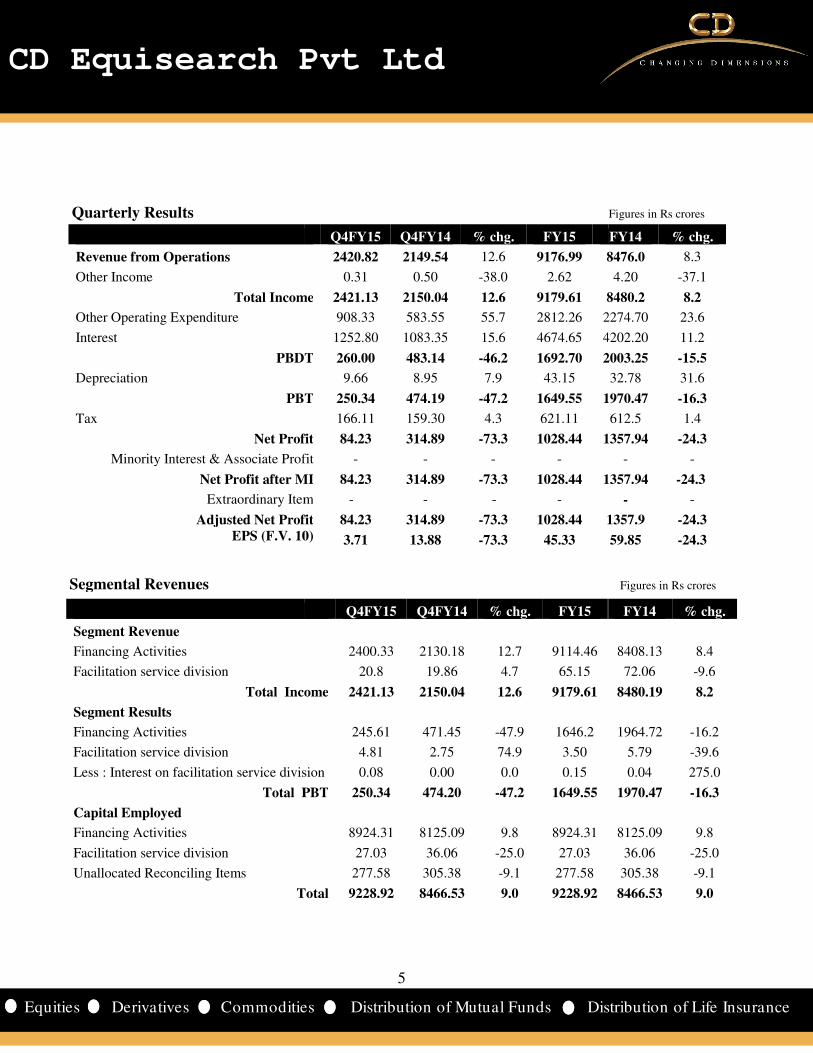

• On a consolidated basis, STFC reported a total income of Rs 2421 crores

in Q4 FY15 versus Rs 2150 crores in Q4 FY14 which is a growth of

12.6%.The finance cost for the quarter grew by 15

crores (Rs 1083.35 in Q4 FY14). The net profit for the quarter declined

by 73.3% to Rs 84.23 crore from Rs 314.89

equipment finance subsidiary.

• On a standalone basis, STFC reported a total income of Rs 2310.69

crores in Q4 FY15 versus Rs 2005.37 crores in Q4 F

growth of 15.23%. The finance cost for the quarter grew by 16.75% to Rs

1184.30 crores (Rs 1014.38 in Q4 FY14).The net profit for the quarter

increased by 7.4% to Rs 316.73 crore from Rs 294.96 crore in Q4 FY14.

• Shriram Equipment Finance Company Limited, a subsidiary of

reported a net loss of Rs 237.13 crores in Q4 FY15 versus a net profit of

Rs 16.48 crores in Q4 FY14 as a result of higher provisioning for NPAs.

The assets under management declined from Rs 3418.39 crores in Q4

FY14 to Rs 2998.58 crores in Q4 FY15 (a de growth

• We believe that the commercial vehicle cycle has bottomed out and

second half of FY16 will witness a pickup in demand. We have revised

our EPS estimates of FY16 from Rs 68.72 to Rs 55.5 (refer to o

previous report dated Jan 7, 2015). Our FY17 EPS target is projected at

Rs 63.43.

• The stock currently trades at 2.1x FY16e book v

and 1.9x FY17e book value (14.9x FY17e

that the stock is reasonably valued, though asset quality concerns with

respect to equipment finance business remain

‘Accumulate’ with a target of Rs 1082 (previous target 1237

been achieved subsequent to our report dated Jan 7, 2015) based on 2.2

FY17e BV (17x FY17e EPS), within a time horiz

July 09, 2015

istribution of Life Insurance

FY16e FY17e

4440.25 5085.22

458.70 500.00

3615.64 4128.66

1259.43 1439.18

55.50 63.43

22.5 14.3

(STFC) is one of India’s leading

NBFC with strong competitive advantage in pre-owned commercial

12 year old vehicles).

STFC reported a total income of Rs 2421 crores

in Q4 FY15 versus Rs 2150 crores in Q4 FY14 which is a growth of

The finance cost for the quarter grew by 15.6% to Rs 1252.80

crores (Rs 1083.35 in Q4 FY14). The net profit for the quarter declined

Rs 84.23 crore from Rs 314.89 in Q4 FY14 due to the loss in

On a standalone basis, STFC reported a total income of Rs 2310.69

crores in Q4 FY15 versus Rs 2005.37 crores in Q4 FY14 which is a

ce cost for the quarter grew by 16.75% to Rs

1184.30 crores (Rs 1014.38 in Q4 FY14).The net profit for the quarter

increased by 7.4% to Rs 316.73 crore from Rs 294.96 crore in Q4 FY14.

Shriram Equipment Finance Company Limited, a subsidiary of STFC,

reported a net loss of Rs 237.13 crores in Q4 FY15 versus a net profit of

Rs 16.48 crores in Q4 FY14 as a result of higher provisioning for NPAs.

The assets under management declined from Rs 3418.39 crores in Q4

(a de growth of 12.3%).

We believe that the commercial vehicle cycle has bottomed out and

up in demand. We have revised

from Rs 68.72 to Rs 55.5 (refer to our

, 2015). Our FY17 EPS target is projected at

x FY16e book value (17.1x FY16e EPS)

Y17e EPS). At current levels, we feel

valued, though asset quality concerns with

uipment finance business remain. We recommend

(previous target 1237, which had

been achieved subsequent to our report dated Jan 7, 2015) based on 2.2x

e EPS), within a time horizon of 9-12 months.

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

FY12 FY13 FY14 FY15 FY16e

Source: CD Equisearch , STFC

Recommendation

Financials

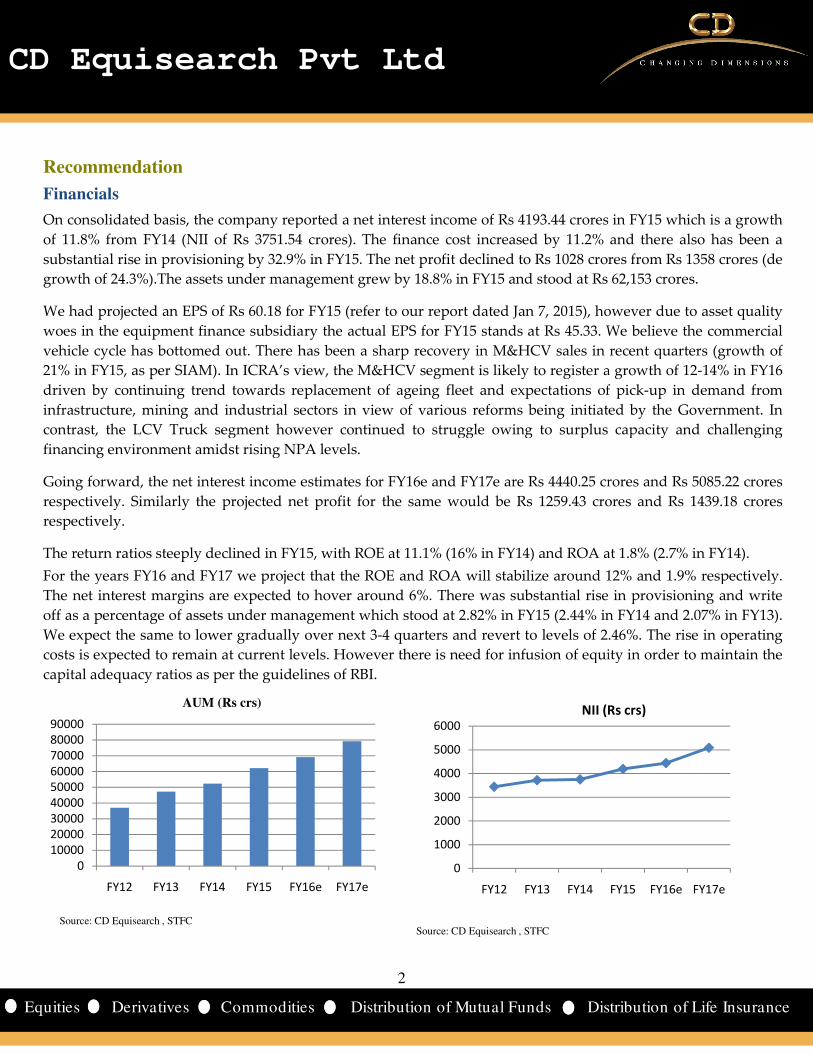

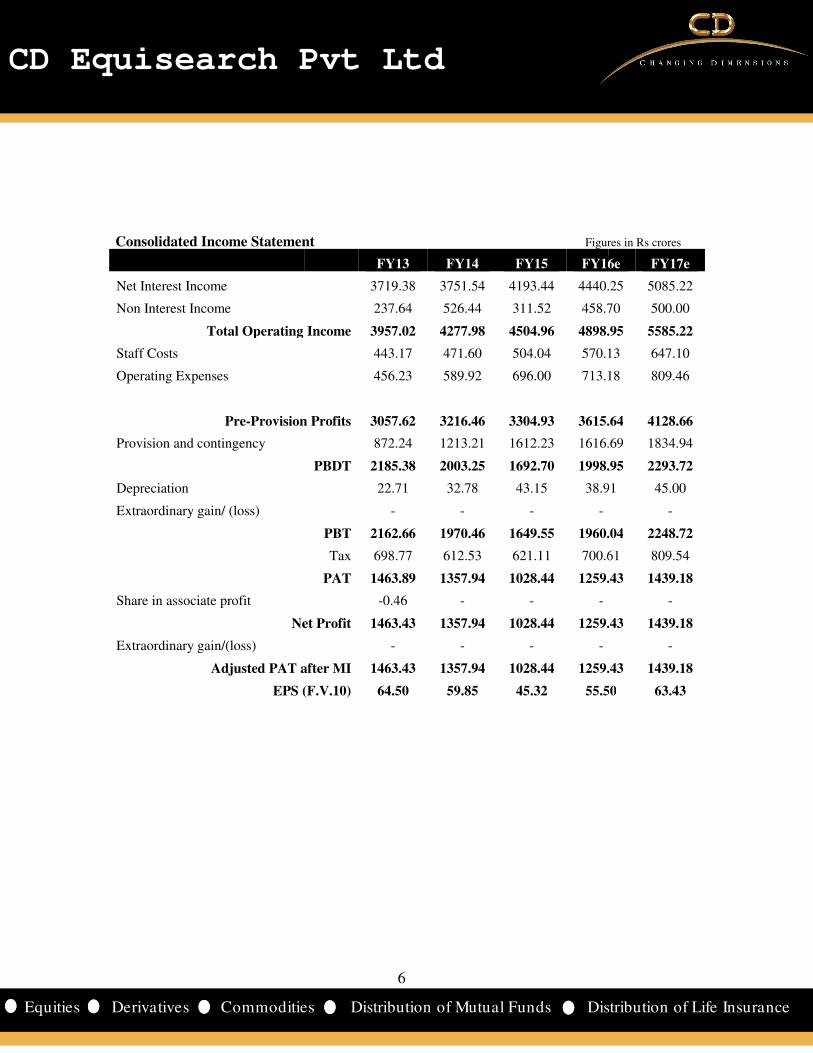

On consolidated basis, the company reported a net interest income of Rs 4193.44 crores in F

of 11.8% from FY14 (NII of Rs 3751.54 crores).

substantial rise in provisioning by 32.9% i

growth of 24.3%).The assets under management grew by 18.8

We had projected an EPS of Rs 60.18 for FY15 (refer to our report dated Jan

woes in the equipment finance subsidiary the actual EPS for FY15 stands at Rs 45.33. We believe the commercial

vehicle cycle has bottomed out. There has been a

21% in FY15, as per SIAM). In ICRA’s view, the M&HCV segment is likely to regi

driven by continuing trend towards replacement of ageing fleet and expectations of pick

infrastructure, mining and industrial sectors in view of various reforms being initiated by the Government. In

contrast, the LCV Truck segment however continued to struggle owing to surplus capacity and challenging

financing environment amidst rising NPA levels.

Going forward, the net interest income estimates for FY16e and FY17e are Rs 4440.25 crores and Rs 5085.22 crores

respectively. Similarly the projected net profit for the same would be Rs 1259.43 crores and Rs 1439.18 crores

respectively.

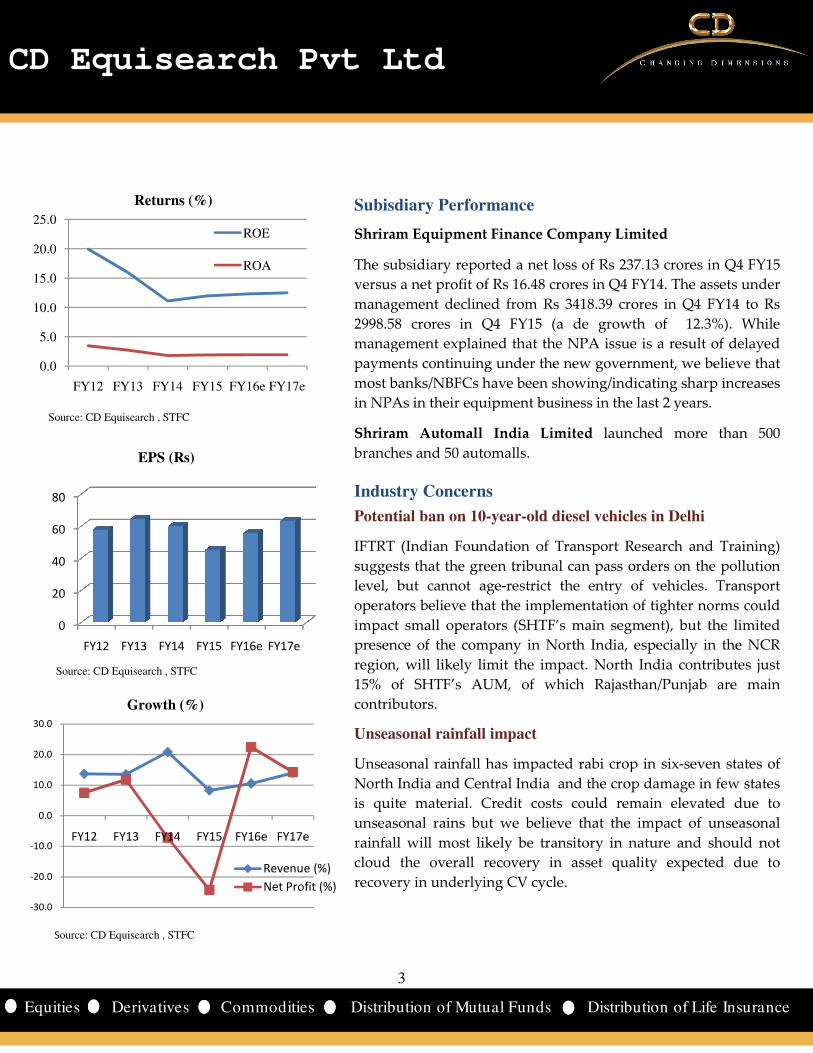

The return ratios steeply declined in FY15,

For the years FY16 and FY17 we project that the ROE and ROA will stabilize around 12% and 1.9% respectively.

The net interest margins are expected to hover around 6%. There was substantial ris

off as a percentage of assets under management which stood at 2.82% in FY15 (2.44% in FY14 and 2.07% in FY13).

We expect the same to lower gradually over next 3

costs is expected to remain at current levels. However there is need for infusion of equity in order to maintain the

capital adequacy ratios as per the guidelines of RBI.

AUM (Rs crs)

2

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

FY16e FY17e

, the company reported a net interest income of Rs 4193.44 crores in F

.54 crores). The finance cost increased by 11.2% and there also has been a

32.9% in FY15. The net profit declined to Rs 1028 crores from Rs 1358 crores (de

sets under management grew by 18.8% in FY15 and stood at Rs

We had projected an EPS of Rs 60.18 for FY15 (refer to our report dated Jan 7, 2015), however due to asset quality

woes in the equipment finance subsidiary the actual EPS for FY15 stands at Rs 45.33. We believe the commercial

here has been a sharp recovery in M&HCV sales in recent quarters

. In ICRA’s view, the M&HCV segment is likely to register a growth of 12

driven by continuing trend towards replacement of ageing fleet and expectations of pick

sectors in view of various reforms being initiated by the Government. In

contrast, the LCV Truck segment however continued to struggle owing to surplus capacity and challenging

rising NPA levels.

est income estimates for FY16e and FY17e are Rs 4440.25 crores and Rs 5085.22 crores

respectively. Similarly the projected net profit for the same would be Rs 1259.43 crores and Rs 1439.18 crores

The return ratios steeply declined in FY15, with ROE at 11.1% (16% in FY14) and ROA at 1.8% (2.7% in FY14).

For the years FY16 and FY17 we project that the ROE and ROA will stabilize around 12% and 1.9% respectively.

The net interest margins are expected to hover around 6%. There was substantial rise in provisioning and write

under management which stood at 2.82% in FY15 (2.44% in FY14 and 2.07% in FY13).

We expect the same to lower gradually over next 3-4 quarters and revert to levels of 2.46%. The

expected to remain at current levels. However there is need for infusion of equity in order to maintain the

capital adequacy ratios as per the guidelines of RBI.

0

1000

2000

3000

4000

5000

6000

FY12 FY13 FY14

Source: CD Equisearch , STFC

NII (Rs

2

CD Equisearch Pvt Ltd

istribution of Life Insurance

, the company reported a net interest income of Rs 4193.44 crores in FY15 which is a growth

The finance cost increased by 11.2% and there also has been a

n FY15. The net profit declined to Rs 1028 crores from Rs 1358 crores (de

% in FY15 and stood at Rs 62,153 crores.

7, 2015), however due to asset quality

woes in the equipment finance subsidiary the actual EPS for FY15 stands at Rs 45.33. We believe the commercial

sales in recent quarters (growth of

ster a growth of 12-14% in FY16

driven by continuing trend towards replacement of ageing fleet and expectations of pick-up in demand from

sectors in view of various reforms being initiated by the Government. In

contrast, the LCV Truck segment however continued to struggle owing to surplus capacity and challenging

est income estimates for FY16e and FY17e are Rs 4440.25 crores and Rs 5085.22 crores

respectively. Similarly the projected net profit for the same would be Rs 1259.43 crores and Rs 1439.18 crores

with ROE at 11.1% (16% in FY14) and ROA at 1.8% (2.7% in FY14).

For the years FY16 and FY17 we project that the ROE and ROA will stabilize around 12% and 1.9% respectively.

e in provisioning and write

under management which stood at 2.82% in FY15 (2.44% in FY14 and 2.07% in FY13).

4 quarters and revert to levels of 2.46%. The rise in operating

expected to remain at current levels. However there is need for infusion of equity in order to maintain the

FY15 FY16e FY17e

NII (Rs crs)

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

0.0

5.0

10.0

15.0

20.0

25.0

FY12 FY13 FY14 FY15 FY16e FY17e

ROE

ROA

Source: CD Equisearch , STFC

Returns (%)

0

20

40

60

80

FY12 FY13 FY14 FY15 FY16e FY17e

Source: CD Equisearch , STFC

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

FY12 FY13 FY14 FY15 FY16e FY17e

Revenue (%)

Net Profit (%)

Source: CD Equisearch , STFC

EPS (Rs)

Growth (%)

3

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

FY17e

FY17e

Revenue (%)

Net Profit (%)

Subisdiary Performance

Shriram Equipment Finance Company Limited

The subsidiary reported a net loss of Rs 237.13 crores in Q4

versus a net profit of Rs 16.48 crores in Q4 FY14. The assets

management declined from Rs 3418.39 crores in Q4 FY14 to

2998.58 crores in Q4 FY15 (a de growth of 12.3%).

management explained that the NPA i

payments continuing under the new government, we believe that

most banks/NBFCs have been showing/indicating sharp increases

in NPAs in their equipment business in the last 2 years.

Shriram Automall India Limited launched more t

branches and 50 automalls.

Industry Concerns

Potential ban on 10-year-old diesel vehicles in Delhi

IFTRT (Indian Foundation of Transport Research and Training)

suggests that the green tribunal can pass orders on

level, but cannot age-restrict the entry of vehicles. Transport

operators believe that the implementatio

impact small operators (SHTF’s main segment),

presence of the company in North India, especially in the NC

region, will likely limit the impact. North India contributes just

15% of SHTF’s AUM, of which Rajasthan/Punjab are main

contributors.

Unseasonal rainfall impact

Unseasonal rainfall has impacted rabi crop in six

North India and Central India and the c

is quite material. Credit costs could remain

unseasonal rains but we believe that the impact of

rainfall will most likely be transitory in nature a

cloud the overall recovery in asset quality expec

recovery in underlying CV cycle.

3

CD Equisearch Pvt Ltd

istribution of Life Insurance

Shriram Equipment Finance Company Limited

loss of Rs 237.13 crores in Q4 FY15

versus a net profit of Rs 16.48 crores in Q4 FY14. The assets under

Rs 3418.39 crores in Q4 FY14 to Rs

a de growth of 12.3%). While

management explained that the NPA issue is a result of delayed

payments continuing under the new government, we believe that

most banks/NBFCs have been showing/indicating sharp increases

in NPAs in their equipment business in the last 2 years.

launched more than 500

old diesel vehicles in Delhi

(Indian Foundation of Transport Research and Training)

een tribunal can pass orders on the pollution

he entry of vehicles. Transport

operators believe that the implementation of tighter norms could

small operators (SHTF’s main segment), but the limited

company in North India, especially in the NCR

. North India contributes just

Rajasthan/Punjab are main

Unseasonal rainfall has impacted rabi crop in six-seven states of

and the crop damage in few states

rial. Credit costs could remain elevated due to

t we believe that the impact of unseasonal

likely be transitory in nature and should not

sset quality expected due to

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

Valuations

The poor show of results (due to higher NPA

correction in the price of the stock post Q4 FY15

has already got on the path of recovery.

achievable. Asset under management is expected to touch

respectively in the years FY16 and FY17. The upgrade in credit ratings

the funding costs substantially, going forward.

Instruments/Facility

Long Term Bank Facilities

Non-Convertible Debentures

Subordinated Debentures

Fixed Deposits Programme

The company has announced amalgamation of

itself. We believe that the asset quality concerns in the same is expected to persist over next 2

led us to lower our financial targets with reference to our previous

income target for the year FY16 is lowered from Rs 4590.25 to Rs 4440.25

from Rs 68.72 to Rs 55.5 on account of higher provisioning and contingency though the pre pro

has not changed substantially (previous target Rs 3765 crore and current target Rs 3615.64 crore for FY16).

The stock currently trades at 2.1x FY16e book

At current levels, we feel that the stock is reasonably

equipment finance business remain. We recommend ‘Accumulate’ with

(17x FY17e EPS), within a time horizon of 9

Cross Sectional Analysis

Asset Financing NBFCs Equity*

M&M Financial Services 114

Sundaram Finance 111

Cholamandalam Inv 144

Shriram Transport Fin. 227

Source: STFC, CD Equisearch

*Rs in crores, the companies in the matrix are not directly comparable as their loan book/asset under management

4

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

oor show of results (due to higher NPAs in the equipment finance subsidiary) in Q4

Q4 FY15 results .The commercial vehicle cycle we feel has bottomed out and

We feel that AUM growth of 11.2% for FY16e and 14.6

achievable. Asset under management is expected to touch Rs 70000 (approx) crore and Rs 80000 crore

respectively in the years FY16 and FY17. The upgrade in credit ratings by CRISIL in July 2015

going forward.

Upgraded Rating Previous Rating

CRISIL AA+/Stable CRISIL AA/Positive

CRISIL AA+/Stable CRISIL AA/Positive

CRISIL AA+/Stable CRISIL AA/Positive

FAAA/Stable FAA+/Positive

announced amalgamation of its equipment finance subsidiary (which is wholly owned by it) with

itself. We believe that the asset quality concerns in the same is expected to persist over next 2

led us to lower our financial targets with reference to our previous report (dated January 7, 2015). The net interest

d from Rs 4590.25 to Rs 4440.25. We have lowered the EPS target of FY16

from Rs 68.72 to Rs 55.5 on account of higher provisioning and contingency though the pre pro

has not changed substantially (previous target Rs 3765 crore and current target Rs 3615.64 crore for FY16).

x FY16e book value (17.1x FY16e EPS) and 1.9 x FY17e book value (14.9x FY17e

we feel that the stock is reasonably valued, though asset quality concerns with respect to

We recommend ‘Accumulate’ with a target of Rs 1082 based on 2.2x FY17 BV

(17x FY17e EPS), within a time horizon of 9-12 months.

FV CMP Mcap* IO* ROE(%)

2 280 15925 6061 15.3

10 1568 17420 4294 15.3

10 696 10005 3715 14.0

10 948 21502 9180 11.1

, the companies in the matrix are not directly comparable as their loan book/asset under management weights to various sectors differ.

4

CD Equisearch Pvt Ltd

istribution of Life Insurance

FY15 has caused adequate

The commercial vehicle cycle we feel has bottomed out and

We feel that AUM growth of 11.2% for FY16e and 14.6% for FY17e is

crore and Rs 80000 crore (approx)

by CRISIL in July 2015 is expected to lower

Previous Rating

CRISIL AA/Positive

CRISIL AA/Positive

CRISIL AA/Positive

FAA+/Positive

its equipment finance subsidiary (which is wholly owned by it) with

itself. We believe that the asset quality concerns in the same is expected to persist over next 2-3 quarters which has

report (dated January 7, 2015). The net interest

. We have lowered the EPS target of FY16

from Rs 68.72 to Rs 55.5 on account of higher provisioning and contingency though the pre provision profit target

has not changed substantially (previous target Rs 3765 crore and current target Rs 3615.64 crore for FY16).

FY17e book value (14.9x FY17e EPS).

valued, though asset quality concerns with respect to

a target of Rs 1082 based on 2.2x FY17 BV

ROE(%) P/BV P/E

15.3 2.7 17.5

15.3 4.6 30.3

14.0 3.2 22.5

11.1 2.3 20.9

weights to various sectors differ.

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

Quarterly Results

Segment Revenue

Financing Activities

Facilitation service division

Total Income

Segment Results

Financing Activities

Facilitation service division

Less : Interest on facilitation service division

Total PBT

Capital Employed

Financing Activities

Facilitation service division

Unallocated Reconciling Items

Total

Segmental Revenues

Revenue from Operations

Other Income

Total Income

Other Operating Expenditure

Interest

PBDT

Depreciation

PBT

Tax

Net Profit

Minority Interest & Associate Profit

Net Profit after MI

Extraordinary Item

Adjusted Net Profit

EPS (F.V. 10)

5

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

Q4FY15 Q4FY14 % chg. FY15

2400.33 2130.18 12.7 9114.46

20.8 19.86 4.7 65.15

Total Income 2421.13 2150.04 12.6 9179.61

245.61 471.45 -47.9 1646.2

4.81 2.75 74.9 3.50

division 0.08 0.00 0.0 0.15

Total PBT 250.34 474.20 -47.2 1649.55

8924.31 8125.09 9.8 8924.31

27.03 36.06 -25.0 27.03

277.58 305.38 -9.1 277.58

Total 9228.92 8466.53 9.0 9228.92

Q4FY15 Q4FY14 % chg. FY15

2420.82 2149.54 12.6 9176.99 8476.0

0.31 0.50 -38.0 2.62

Total Income 2421.13 2150.04 12.6 9179.61 8480.2

908.33 583.55 55.7 2812.26 2274.70

1252.80 1083.35 15.6 4674.65 4202.20

PBDT 260.00 483.14 -46.2 1692.70 2003.25

9.66 8.95 7.9 43.15

PBT 250.34 474.19 -47.2 1649.55 1970.47

166.11 159.30 4.3 621.11

Net Profit 84.23 314.89 -73.3 1028.44 1357.94

Minority Interest & Associate Profit - - - -

Net Profit after MI 84.23 314.89 -73.3 1028.44 1357.94

Extraordinary Item - - - -

Adjusted Net Profit 84.23 314.89 -73.3 1028.44 1357.9

EPS (F.V. 10) 3.71 13.88 -73.3 45.33

5

CD Equisearch Pvt Ltd

istribution of Life Insurance

Figures in Rs crores

FY14 % chg.

8408.13 8.4

72.06 -9.6

8480.19 8.2

1964.72 -16.2

5.79 -39.6

0.04 275.0

1970.47 -16.3

8125.09 9.8

36.06 -25.0

305.38 -9.1

8466.53 9.0

Figures in Rs crores

FY14 % chg.

8476.0 8.3

4.20 -37.1

8480.2 8.2

2274.70 23.6

4202.20 11.2

2003.25 -15.5

32.78 31.6

1970.47 -16.3

612.5 1.4

1357.94 -24.3

- -

1357.94 -24.3

- -

1357.9 -24.3

59.85 -24.3

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

Net Interest Income

Non Interest Income

Total Operating Income

Staff Costs

Operating Expenses

Pre-Provision Profits

Provision and contingency

Depreciation

Extraordinary gain/ (loss)

Share in associate profit

Net Profit

Extraordinary gain/(loss)

Adjusted PAT after MI

EPS (F.V.10)

Consolidated Income Statement

Rs in crores

6

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

FY13 FY14 FY15 FY16e

3719.38 3751.54 4193.44 4440.25

237.64 526.44 311.52 458.70

Total Operating Income 3957.02 4277.98 4504.96 4898.95

443.17 471.60 504.04 570.13

456.23 589.92 696.00 713.18

Provision Profits 3057.62 3216.46 3304.93 3615.64

872.24 1213.21 1612.23 1616.69

PBDT 2185.38 2003.25 1692.70 1998.95

22.71 32.78 43.15 38.91

- - - -

PBT 2162.66 1970.46 1649.55 1960.04

Tax 698.77 612.53 621.11 700.61

PAT 1463.89 1357.94 1028.44 1259.43

-0.46 - - -

Net Profit 1463.43 1357.94 1028.44 1259.43

- - - -

Adjusted PAT after MI 1463.43 1357.94 1028.44 1259.43

EPS (F.V.10) 64.50 59.85 45.32 55.50

Consolidated Income Statement Figures in Rs crores

6

CD Equisearch Pvt Ltd

istribution of Life Insurance

FY16e FY17e

4440.25 5085.22

458.70 500.00

4898.95 5585.22

570.13 647.10

713.18 809.46

3615.64 4128.66

1616.69 1834.94

1998.95 2293.72

38.91 45.00

-

1960.04 2248.72

700.61 809.54

1259.43 1439.18

-

1259.43 1439.18

-

1259.43 1439.18

55.50 63.43

Figures in Rs crores

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

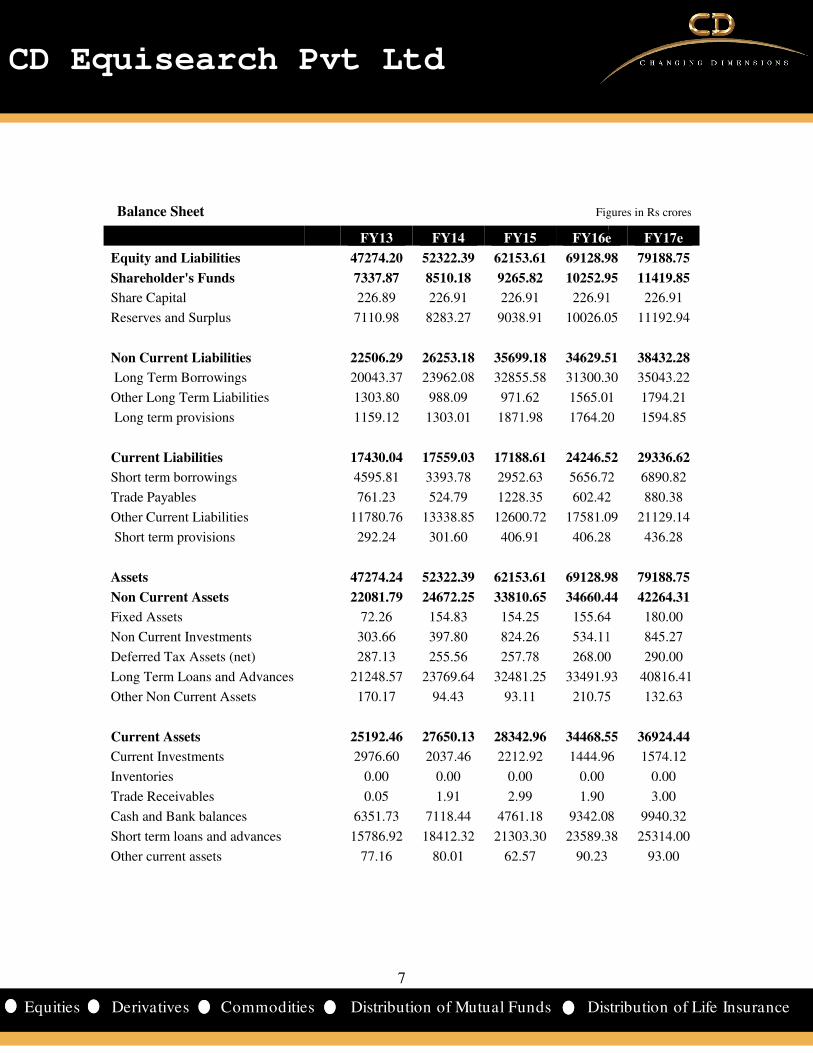

Equity and Liabilities

Shareholder's Funds

Share Capital

Reserves and Surplus

Non Current Liabilities

Long Term Borrowings

Other Long Term Liabilities

Long term provisions

Current Liabilities

Short term borrowings

Trade Payables

Other Current Liabilities

Short term provisions

Assets

Non Current Assets

Fixed Assets

Non Current Investments

Deferred Tax Assets (net)

Long Term Loans and Advances

Other Non Current Assets

Current Assets

Current Investments

Inventories

Trade Receivables

Cash and Bank balances

Short term loans and advances

Other current assets

Balance Sheet

7

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

FY13 FY14 FY15 FY16e

47274.20 52322.39 62153.61 69128.98

7337.87 8510.18 9265.82 10252.95

226.89 226.91 226.91 226.91

7110.98 8283.27 9038.91 10026.05

22506.29 26253.18 35699.18 34629.51

20043.37 23962.08 32855.58 31300.30

1303.80 988.09 971.62 1565.01

1159.12 1303.01 1871.98 1764.20

17430.04 17559.03 17188.61 24246.52

4595.81 3393.78 2952.63 5656.72

761.23 524.79 1228.35 602.42

11780.76 13338.85 12600.72 17581.09

292.24 301.60 406.91 406.28

47274.24 52322.39 62153.61 69128.98

22081.79 24672.25 33810.65 34660.44

72.26 154.83 154.25 155.64

303.66 397.80 824.26 534.11

287.13 255.56 257.78 268.00

21248.57 23769.64 32481.25 33491.93

170.17 94.43 93.11 210.75

25192.46 27650.13 28342.96 34468.55

2976.60 2037.46 2212.92 1444.96

0.00 0.00 0.00 0.00

0.05 1.91 2.99 1.90

6351.73 7118.44 4761.18 9342.08

15786.92 18412.32 21303.30 23589.38

77.16 80.01 62.57 90.23

Balance Sheet Figures in Rs crores

7

CD Equisearch Pvt Ltd

istribution of Life Insurance

FY16e FY17e

69128.98 79188.75

10252.95 11419.85

226.91 226.91

10026.05 11192.94

34629.51 38432.28

31300.30 35043.22

1565.01 1794.21

1764.20 1594.85

24246.52 29336.62

5656.72 6890.82

602.42 880.38

17581.09 21129.14

406.28 436.28

69128.98 79188.75

34660.44 42264.31

155.64 180.00

534.11 845.27

268.00 290.00

33491.93 40816.41

210.75 132.63

34468.55 36924.44

1444.96 1574.12

0.00

3.00

9342.08 9940.32

23589.38 25314.00

93.00

Figures in Rs crores

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

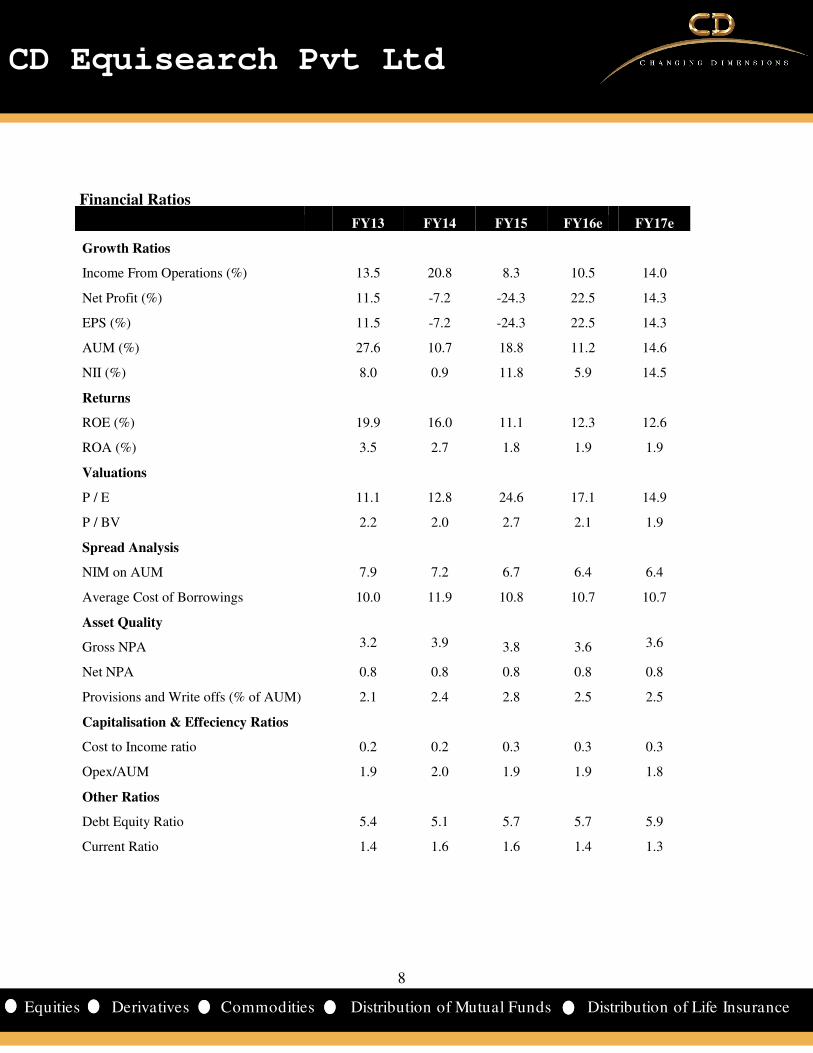

Growth Ratios

Income From Operations (%)

Net Profit (%)

EPS (%)

AUM (%)

NII (%)

Returns

ROE (%)

ROA (%)

Valuations

P / E

P / BV

Spread Analysis

NIM on AUM

Average Cost of Borrowings

Asset Quality

Gross NPA

Net NPA

Provisions and Write offs (% of AUM)

Capitalisation & Effeciency Ratios

Cost to Income ratio

Opex/AUM

Other Ratios

Debt Equity Ratio

Current Ratio

Financial Ratios

8

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

FY13 FY14 FY15 FY16e

13.5 20.8 8.3 10.5

11.5 -7.2 -24.3 22.5

11.5 -7.2 -24.3 22.5

27.6 10.7 18.8 11.2

8.0 0.9 11.8 5.9

19.9 16.0 11.1 12.3

3.5 2.7 1.8 1.9

11.1 12.8 24.6 17.1

2.2 2.0 2.7 2.1

7.9 7.2 6.7 6.4

10.0 11.9 10.8 10.7

3.2 3.9 3.8 3.6

0.8 0.8 0.8 0.8

2.1 2.4 2.8 2.5

0.2 0.2 0.3 0.3

1.9 2.0 1.9 1.9

5.4 5.1 5.7 5.7

1.4 1.6 1.6 1.4

8

CD Equisearch Pvt Ltd

istribution of Life Insurance

FY17e

14.0

14.3

14.3

14.6

14.5

12.6

1.9

14.9

1.9

6.4

10.7

3.6

0.8

2.5

0.3

1.8

5.9

1.3

CD Equisearch Pvt Ltd

Equities Derivatives Commoditie

DISCLOSURE & DISCLAIMER: CD Equisearch Private Limited (hereinafter referred to as India Limited, Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX Stock Exchange Limited). CD Equi is also registered as Depository Participant withAdvisor. The associates of CD Equi are engaged in activities relating to NBFCBroking, Real Estate, etc. CD Equi has applied for registration under SEBI (Research Analysts) R

• No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

• CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more t

percent/material conflict of interest in the subject company(s)

• CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve months.

• CD Equi/its research analysts has not served as

has not been engaged in market making activity of the company covered by analysts This document is solely for the personal information of the recipient and must not be singularly used ainvestment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an invethe securities of the companies referred to in this document (including the merits and risks involved) and should consult theown advisors to determine the merits and risks of such an investment. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true but we do not represent that it is accurate or complete and it should not be relied on asuch, as this document is for general guidance only. CD Equi or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in threport. CD Equi has not independently verified all the information contained within this document. Accordingly, we cannot testify nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While, CD Equi endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or other reasons that prevent us from doing so. This document is being supplied to you solely for your information and its contents, information or data mayredistributed or passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liabloss or damage that may arise from or in connection with the use of this information.CD Equisearch Private Limited (CIN: U67120WB1995PTC071521)Registered Office: 37, Shakespeare Sarani, 1st Floor, Kolkata Corporate Office: 10, Vasawani Mansion, 2nd Floor, Dinshaw Wachha Road, Churchgate, Mumb2283 0652/0653; Fax: +91(22) 2283, 2276 Website: www.cdequi.com; Email: [email protected] Regn No.: NSE-CM: INB230781137, NSE-FOINF010781133, MCX-SX-CM: INB-260781134, MCX180-2002

9

CD Equisearch Pvt Ltd

ities Distribution of Mutual Funds Dist

CD Equisearch Private Limited (hereinafter referred to as ‘CD Equi’) is a Member registered with National Stock Exchange of India Limited, Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX Stock Exchange Limited). CD Equi is also registered as Depository Participant with CDSL and AMFI registered Mutual Fund Advisor. The associates of CD Equi are engaged in activities relating to NBFC-ND - Financing and Investment, Commodity

CD Equi has applied for registration under SEBI (Research Analysts) Regulations, 2014. Further, CD Equi hereby declares that

No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more t

percent/material conflict of interest in the subject company(s).

CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the

CD Equi/its research analysts has not served as an officer, director or employee of company covered by analysts and

has not been engaged in market making activity of the company covered by analysts.

This document is solely for the personal information of the recipient and must not be singularly used ainvestment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an invethe securities of the companies referred to in this document (including the merits and risks involved) and should consult theown advisors to determine the merits and risks of such an investment.

ysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a

t has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true but we do not represent that it is accurate or complete and it should not be relied on aguidance only. CD Equi or any of its affiliates/group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in thrified all the information contained within this document. Accordingly, we cannot

testify nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

a reasonable basis the information discussed in this material, there may be regulatory compliance or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information and its contents, information or data mayredistributed or passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liabloss or damage that may arise from or in connection with the use of this information.

Private Limited (CIN: U67120WB1995PTC071521) Floor, Kolkata – 700 017; Phone: +91(33) 4488 0000; Fax: +91(33) 2289 2557Floor, Dinshaw Wachha Road, Churchgate, Mumbai

[email protected] FO: INF230781137, NSE-CD: INE230781135, BSE-CM: INB010781133, BSE

260781134, MCX-SX-FO: INF260781134, MCX-SX-CD: INE260781137, DP: IN

9

CD Equisearch Pvt Ltd

istribution of Life Insurance

) is a Member registered with National Stock Exchange of India Limited, Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX

CDSL and AMFI registered Mutual Fund Financing and Investment, Commodity

egulations, 2014. Further, CD Equi hereby declares that –

No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more than one

CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the

an officer, director or employee of company covered by analysts and

This document is solely for the personal information of the recipient and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved) and should consult their

ysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a

t has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true but we do not represent that it is accurate or complete and it should not be relied on as guidance only. CD Equi or any of its affiliates/group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this rified all the information contained within this document. Accordingly, we cannot

testify nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

a reasonable basis the information discussed in this material, there may be regulatory

This document is being supplied to you solely for your information and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liable for any

700 017; Phone: +91(33) 4488 0000; Fax: +91(33) 2289 2557; ai – 400 020; Phone: +91(22)

CM: INB010781133, BSE-FO: CD: INE260781137, DP: IN-DP-CDSL-