cc power point presentation

TRANSCRIPT

What your health care team needs to knowabout Covered California.

Covered California

Agenda

www.thecmafoundation.org

• Overview of ACA

• Overview of Covered CA

• Health Exchange Plans

• What Physician Practices Need to Know

• Question and Answer Session

The Fine Print

www.thecmafoundation.org

Covered California has provided funding to educate physicians and their health care teams about health insurance reform and the new marketplace, Covered California.

This presentation will not discuss contract reimbursement rates.

Nothing in this presentation is intended to suggest that a physician should or should not contract with any plan, and decisions whether to contract with a plan must be made based on the specific individual situation of the physician.

• Network Adequacy Issues

– Provider directories

– Specialists and referrals

• Exchange / Mirrored Plans

– Names of Networks

– 2015 Names

• Grace Period Clarification

• Other practice management issues

Issues to be Addressed

Regulatory Response

In June, the DMHC opened an investigation regarding the accuracy of the Anthem Blue Cross and Blue Shield provider directories and whether they have violated any California laws.

The final report will be issued in the beginning of November prior to open enrollment.

Ultimately, CMA’s goal for the DMHC’s investigation is• better education to patients and physicians on the fact that the networks

are different from their larger commercial networks; and• the requirement that the plans take steps to confirm the adequacy of

their networks and the accuracy of their directories.

www.thecmafoundation.org

Covered California’s Response

In 2015, Covered California will hold health plans accountable for consumers. Specifically, health plans must:

www.thecmafoundation.org

1. Have sufficient clinicians (physicians, hospitals, other) to meet needs of enrollees2. Each enrollee receives a preventive, wellness visit annually3. Identify and proactively manage “at-risk” enrollees4. Determine enrollees’ health status…5. Promote the use of best practice models for continuity of care & care coordination6. Be transparent about plan performance at the point of enrollment, standard

measures of prevention, access and clinical effectiveness7. Be certified by the National Committee for Quality Assurance

Health Insurance Statusof Californians Under Age 65

www.chcf.org/aca411

Overview of the ACA

Insurance Market Reforms Guaranteed issue

– Ignores pre-existing conditions

– Health status

– No gender-based premiums

Guaranteed renewal– Health insurance cannot be dropped if sick

– No lifetime or annual caps on dollar value of services

Individual Mandate– Required to have public or private health insurance or pay

penalty

Overview of the ACA

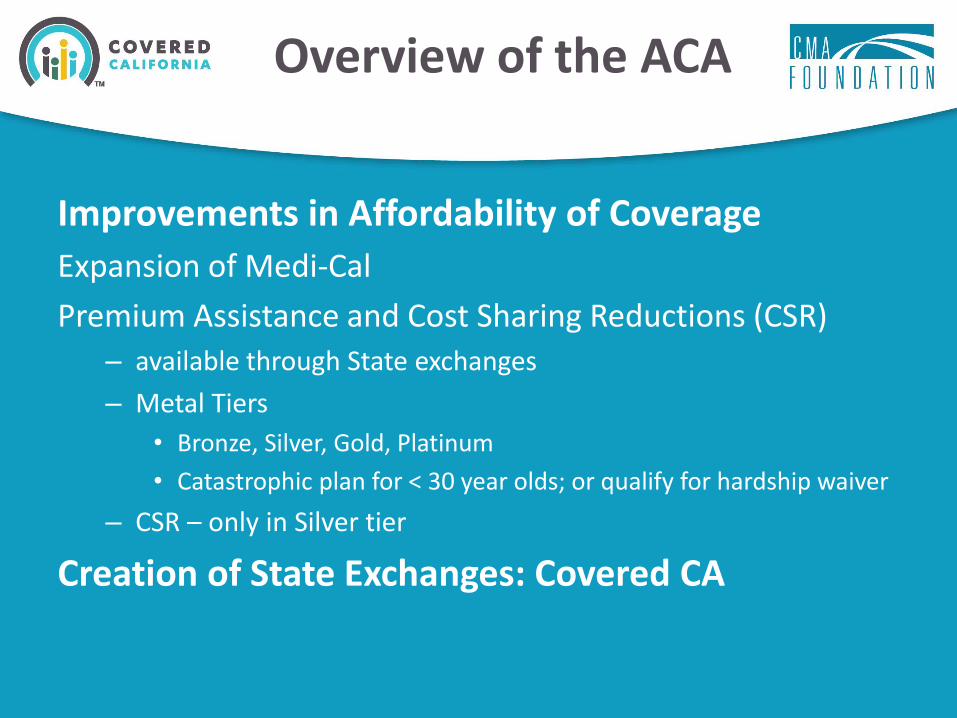

Improvements in Affordability of Coverage

Expansion of Medi-Cal

Premium Assistance and Cost Sharing Reductions (CSR)

– available through State exchanges

– Metal Tiers

• Bronze, Silver, Gold, Platinum

• Catastrophic plan for < 30 year olds; or qualify for hardship waiver

– CSR – only in Silver tier

Creation of State Exchanges: Covered CA

Covered California

An “active purchaser” model which allows it to negotiate with insurers, decide which insurers can offer health plans through the exchange and set criteria for participating plans.

Behaves similarly to that of a large employer - negotiating and purchasing health coverage on behalf of its employees.

Contracted with ten Knox-Keene licensed health plans in 2014 to create a marketplace through which enrollees select a plan.

– Health plans contract directly with providers and the terms of those contracts are propriety to each plan.

www.thecmafoundation.org

www.cmafoundation.org

Covered California

Purchased through health insurance website or insurance broker

No Covered CA Logo

Mirror Plan Exchange PlanPremium Assistance & Cost Sharing Reductions

Identical ProductsIdentical Benefits

Identical Provider Networks

Purchased through Cov CA website or Cov CA Certified Insurance Agentor Certified Enrollment Counselor

Covered CA Logo

The Covered CA MarketplaceSacramento County San Francisco County Los Angeles County San Diego County

Anthem

Blue Shield

Kaiser Permanente

Western Health Advantage

Anthem

Blue Shield

Chinese Community Health Plan

Health Net

Kaiser Permanente

Anthem

Blue Shield

Health Net

Kaiser Permanente

L.A. Care Health

Plan

Anthem

Blue Shield

Health Net

Kaiser Permanente

Molina Healthcare

Sharp Health Plan

Medi-Cal Medi-Cal Medi-Cal Medi-Cal

The place to shop for health insurance.

Covered CA Enrollment as of April 17, 2014= 1,395,929

Subsidy-Eligible 88%

Unsubsidized 12%

Making Care More Premium Assistance

Eligibility is based on:

Number of People in Your

Household

Annual Household Income

1 $0 - $16,105

2 $0 - $21,708

3 $0 - $27,311

4 $0 - $32,913

5 $0 - $38,516

$16,106 - $46,680

$21,709 - $62,920

$27,312 - $79,160

$32,914 - $95,400

$38,517 - $111,640

Eligible for Premium Assistance

Eligible forMedi-Cal

Medi-Cal Expansion

New eligible population

Adults whose incomes are ≤ 138% of FPL

– No longer child-linked

– Eliminates asset tests

Uses Modified Adjusted Gross Income (MAGI) to determine eligibility

Expansion is in addition to the approximately 7 million Californians already insured through Medi-Cal.

Medi-Cal Enrollment as of Mar. 31, 2014

1,100,000 650,000 180,0000

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Enrolled Medi-Cal transitions from LowIncome Health Program (LIHP)

Express Lane

= 1.9 Million

2015Standard Bene�ts for Individuals

Bronze Silver* Gold Platinum

Deductible $5,000 Medical and drugs

$2,000 Medical None None

Primary Care Visit Copay

$60 (Three visits per year) $45 $30 $20

Generic Medication Copay

$15 $15 $15 $5

Emergency Room Copay $300 $250 $250 $150

Maximum Out-of-Pocket for Individual $6,250 $6,250 $6,250 $4,000

Maximum Out-of-Pocket for Family $12,500 $12,500 $12,500 $8,000

Copays are not subject to any deductible and count toward the annual out-of-pocket maximum.Blue corners indicate bene�ts that are subject to deductibles.

* Lower cost sharing is available on a sliding scale.

or less or less or less or less

Annual Income $16,106 – $17,504 $17,505 – $23,339 $23,340 – $29,174 $29,175 – $46,680

Deductible None $500 $1,500 Medical

$2,000 Medical

Primary Care Visit Copay $3 $15 $40 $45

Generic Medication Copay $3 $5 $15 $15

Emergency Room Copay $25 $75 $250 $250

Maximum Out-of-Pocket for Individual $2,250 $2,250 $5,200 $6,250

Maximum Out-of-Pocket for Family $4,500 $4,500 $10,400 $12,500

2015| SINGLE

SILVER PLAN (Eligible for Premium Assistance)

Copays are not subject to any deductible and count toward the annual out-of-pocket maximum.

Individuals Enrolled Across Metal Levelas of May 19, 2014

Minimum Coverage 1% Minimum Coverage 2% Minimum Coverage 2% Minimum Coverage 1%

Bronze , 26%

Bronze , 35%Bronze , 31%

Bronze , 28%

Silver , 62%

Silver , 54%Silver , 55% Silver , 63%

Gold , 6% Gold , 5%Gold , 6%

Gold , 5%Platinum , 5% Platinum , 4% Platinum , 6% Platinum , 3%

64,924 Enrollees 26,671 Enrollees 33,715 Enrollees

Individuals Enrolled Across Health Planas of May 19, 2014

Kaiser , 17.3%Kaiser , 21.2%

Kaiser , 46.1%

Anthem , 30.5%

Anthem , 60.4%Anthem , 16.1%

Anthem , 61.9%

Blue Shield , 27.3%

Blue Shield , 10.8%

Blue Shield , 22.7%Blue Shield , 29.7%

Health Net, 18.9%

Health Net, 4.6%

Health Net, 4.8%

Health Net, 8.5%Valley Health Plan, 2.9%

83% - premium assistance 89% - premium assistance84% - premium assistance

Understanding the Grace Period

Applies to subsidized patients for non- payment or premium delinquency

Health Plans are required to:

– Identify patient’s coverage as suspended or inactive the 2nd & 3rd month of delinquency

– Notify physicians who have submitted claims on patient in previous 2 months, as well as the patient’s assigned PCP

Understanding the Grace Period

Indicate suspension upon patient eligibility verification the first day of the second month

– Blue Shield – “Suspended”

– Anthem Blue Cross – “Suspended pending investigation”

– Health Net – “Delinquent”

Understanding the Grace Period

Best Practices: ALWAYS CHECK ELIGIBILITY– Verify as close to the time of service, every time a

patient comes in for service

– Print “eligibility screen” from health plan website

– Treat the situation as any other patient who has had a lapse in coverage

For non-emergent services, patient can choose to either pay cash for that visit or re-schedule their appointment.

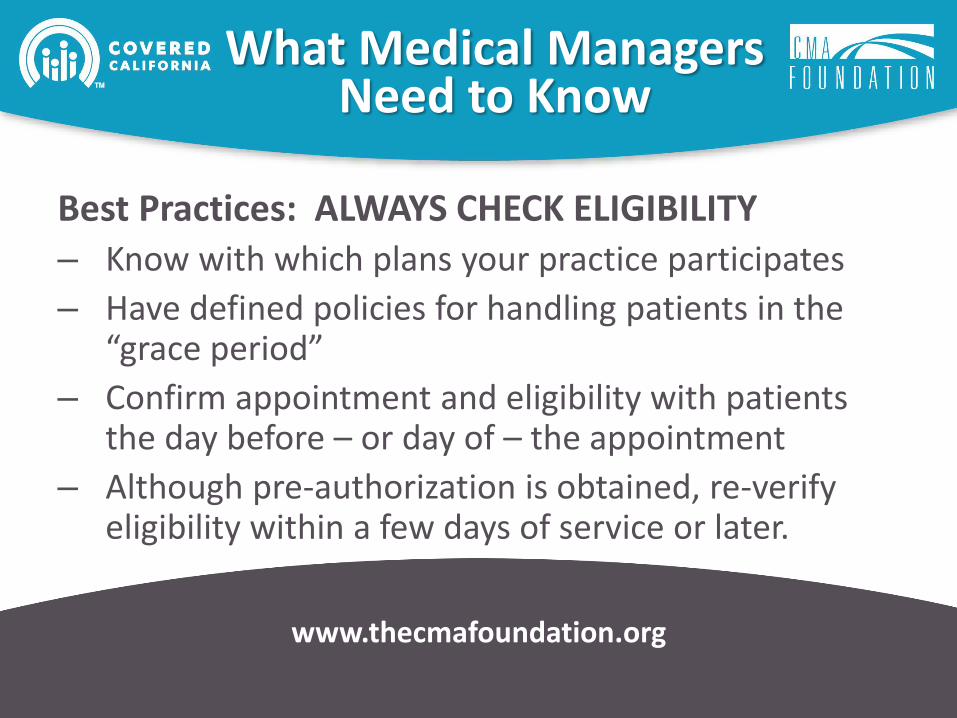

What Medical Managers Need to Know

Best Practices: ALWAYS CHECK ELIGIBILITY– Know with which plans your practice participates

– Have defined policies for handling patients in the “grace period”

– Confirm appointment and eligibility with patients the day before – or day of – the appointment

– Although pre-authorization is obtained, re-verify eligibility within a few days of service or later.

www.thecmafoundation.org

What Medical Managers Need to Know

Anthem Blue Cross

Network Relations – (855) 238-0095 or [email protected]

Blue Shield of California

Provider Services – (800) 258-3091

Health Net of California Provider Services –(800) 641-7761 or [email protected]

Valley Health Plan Provider Relations –(408) 885-2221, option #1

www.thecmafoundation.org

Network Adequacy Concerns

www.thecmafoundation.org

Specific detailed complaints:– Department of Managed Health Care (DMHC)

https://wpso.dmhc.ca.gov/contactform/– Covered California [email protected]– Office of Patient Advocacy [email protected]– CMA at [email protected]

Refer Patients to DMHC HMO Help Line: 1-888-466-2219

Special Enrollment –Qualifying Events

Consumers have 60 days after the qualifying event to enroll in a new plan or change health plans

Second EnrollmentNov 15, 2014 – Feb 15, 2015

Minimal Changes in 2015:– Adult dental plans will be offered through Covered CA– Children’s Health Plans will bundle medical plans with dental

plans– No changes in the Standard Benefit Design until 2016– Health plans formularies linked to the Covered CA website

Information after October 1st– Plan names will be the same (mirrored and exchange)– Adjustment in premium assistance as plan costs change

CMAF Resource PageCovered CA FAQs

www.thecmafoundation.org

http://www.thecmafoundation.org/Programs/Covered-California