cashless campuses going cashless in universities &...

TRANSCRIPT

CASHLESS CAMPUSES

APRIL 2015

GOING CASHLESS IN UNIVERSITIES & COLLEGESWHY IT MATTERS, WHAT IT LOOKS LIKE, HOW TO DO IT.

CONTENTS

02

References

What to look for/pitfalls to avoid when choosing a vendor

The hurdles & how to get over them

Summary of benefits for stakeholders

What does a cashless campus look like?

Universities & the commercial imperative

Universities & the student experience

Students & the payment experience

Notes & coins: past their sell-by date?

Summary

27

24

21

18

13

12

10

08

05

03

SUMMARY

The following points are collated from the At a glance summaries at the end of each section:

03

01 07

05 11

03 09

02 08

06 12

04 10

Cash costs a lot of money for businesses to manage – and consumers don’t love it either

Cash is less suitable for students and can diminish their financial inclusion

Consumers prefer a choice of payment options

A better student experience enables institutions to attract and retain more students

Cashless technology is widely available but businesses may be slow to adopt

A students financial and technological experience affects their overall experience

Fast and easy payment methods influence purchasing habits

Cash is dirty, which is a particular worry in food-service settings

Young people are less likely to carry cash or to know how much cash they have

Not everyone has a bank account

Cashless suits universities and colleges well, but rarely extends beyond catering

Students expect institutions to invest in their experience beyond tuition

04

14

13 21

18

25

16

23

20

27

15

22

19

26

17

24

There is growing pressure for universities and colleges to save money

Support with financial management can be of value to international students

Institutions can choose between closed and open loop systems

‘Cashless’ doesn’t mean no cash at all

Information, consultation and negotiation are crucial for achieving stakeholder buy-in

Institutions must find increasingly innovative ways to deliver efficiencies

Going cashless offers significant benefits for the institution and its staff, UK and international students, parents/guardians,and third-party suppliers

Multiple payment methods are available, but smartcards will give way to mobile phones in future

Knowing what you’re looking for, and the questions to ask, will help you to choose the right vendor and assure a successful solution.

At the same time, they must compete more intensively and in a global market

Cashless systems can be invaluable even for transactions which don’t involve money

One non-cash method can pay for goods and services across campus — and beyond

A good cashless solution vendor will help the institution to get over any hurdles they encounter

Going cashless can deliver both cost savings and an enhanced student experience

Institutions tend to have unnecessary worries about going cashless

The United Kingdom leads the world in financial services2 and yet, when it comes to moving beyond cash, we are far less advanced than countries like Sweden — where four out of five purchases are now made electronically3. Even Kenya has been ‘thundering along the cutting edge’ of cashless payments4.

The writing is on the wall around the globe: cash will continue to decline in importance, driven by both human determination and technological advances. In a 2012 US survey of internet experts, 65% of respondents said that, by 2020, “cash and credit cards will have mostly disappeared from many of the transactions that occur in advanced countries”5. David Wolman, author of 2013 book The End of Money, went so far as to call cash “an anachronism.”6

Consumers & businesses both predict the demise of cash

For consumers, cash can be difficult to access (and around 3% of ATMs still charge a fee for dispensing cash7). It offers less control over finances, and can lead to diminished financial inclusion8. It’s unhygienic, too: Danish banknotes were found to be contaminated with an average of 40,000 bacteria, including staphylococci and faecal bacteria9, and staphylococci were found on 94% of all US banknotes10. 16% of UK consumers think banknotes will have died out by 2025.11

Cash is also a burden for businesses, since it’s more expensive to insure, count, store, manage, and transport. It’s risky: it attracts crime (including violent crime) and it’s open to fraud. In 2014, around 430,000 counterfeit banknotes, with a face value of £8.1million, were taken out of circulation in the UK12, and an estimated 5% of all £1 coins are counterfeit13. Cash is also prone to higher levels of error: 52% of UK businesses said that cash involves more accounting inaccuracies than any other payment method they use14. Indeed, cash is one of the most expensive means of payment available15, costing UK businesses £17.8bn a year16.

Furthermore, cash is slow — and at busy times in retail environments, slow processes lose sales and damage the brand. A single cash transaction requires getting the money out of a wallet/pocket, counting it, handing it over, waiting while the sum offered is checked, receiving any change, checking the change, and putting it away (compare this to a contactless payment, which takes about a second).

Technology is replacing cash

The technology already exists to transform the way we receive and spend money, enabling both consumers and businesses to reduce their dependence on cash while making life easier, more secure and less expensive for everyone. Tokenised online payment, such as Amazon Payments and PayPal, is already part of everyday life. Another method, ‘contactless’, grew 255% in the UK in the year to December 201417, getting a high-profile boost when Transport for London began accepting contactless EMV (Europay, MasterCard & Visa) cards as alternatives to Oyster cards18.

“Physical currency is a bulky, germ-smeared, carbon-intensive, expensive medium of exchange.”1 — David Wolman, The End of Money, 2012

NOTES & COINS: PAST THEIR SELL-BY DATE?

05

This white paper examines the significance and benefits of cashless operation in the further- and higher-education sectors. It explores what a cashless campus might look like; how it can benefit the various stakeholders; and how barriers to adoption can be addressed. It also suggests an approach to selecting a successful cashless system.

06

In March 2015, Facebook announced that its instant messaging app will permit users to send money to each other as easily as they send messages and photos. Other free person-to-person (P2P) payment methods already include Snapchat and PayPal’s Venmo19.

Apple’s new smartwatch enables payment simply by waving the arm at the till; according to the Economist, “the firm’s new contactless payment service… already accounts for two of every three dollars spent in America by gesturing with a smartphone or a card”. Meanwhile, Google has acquired the Softcard mobile-payment service20. And Deloitte predicts that in-store mobile payments will increase by more than 1,000% worldwide in 201521.

Yet businesses are nervous about dispensing with cash

Despite the availability of technology and systems, businesses haven’t embraced cashless operations as fast as one might expect. Adoption may be hindered by concerns about investment, vendor selection, and system implementation/management. It may simply be a question of cold feet. Sometimes, there’s a sense that cash is cheap to transact: after all, cash payments cost an average of 2p to process, versus 8p for debit-card payments and 33p for credit cards23(and chip & pin fraud costs the UK economy around £450m every year24). But businesses often forget the significant add-on costs involved in receiving, counting, insuring, storing, reconciling and transporting cash.

Cashless in the further/higher education sectors

Despite all this, certain contexts lend themselves particularly well to going cashless. For example, further and higher education appears ideally suited:

• Studentsandstaffrepresentadiscretesetofcustomers,regularlygatheringtogetherinonelocation

• Studentsaregenerallyalreadytechnology-savvyandearlyadopters;they’reover40%morelikelytohaveasmartphonethan the overall UK population25, and phones are ideal for identity verification and transaction processing in a cashless environment

• Thenaturalsenseofcommunity,coupledwithbrandloyaltytotheinstitution,canhelptocatalyseuptakeofthesystem

• Studentsarepredisposedtoengagewithdiscounts,promotionsandloyaltyrewards,whichcanhelpachievearapidsystem launch.

However, only a small minority of colleges and universities have transitioned to cashless. Even those which have adopted cashless systems often limit them to a single function, such as catering, rather than moving to a fully integrated ‘cashless campus’.

Both universities and colleges are required to check that students meet the criteria set out in immigration rules, and are fearful of the kind of publicity generated by the 2012 London Met visa debacle. Further education colleges have been slower to adopt cashless (largely because they don’t have the kind of budgets which universities have); however, under new legislation in September 2014 they were collectively tasked with administering and monitoring the provision of free meals for around 103,000 14-18-year-olds. A cashless campus system, incorporating a catering and student attendance system, respectively, makes compliance with these regulations considerably easier and more cost-efficient.

“Hard cash is increasingly becoming currency non grata... Airlines won’t take it for in-flight snacks.”22 — Huff Post Money, 2012

07

“An average smartphone today has more computing power than all of NASA had in 1969... Placing this at a consumer’s fingertips has driven phenomenal opportunities in m-commerce.”26 — Global Payments, 2014

At a glance:

1. Cash costs a lot of money for businesses to manage – and consumers don’t love it, either

2. Cash is dirty, which is a particular worry in food-service settings

3. Cashless technology is widely available but businesses may be slow to adopt

4. Cashless suits universities and colleges well, but rarely extends beyond catering.

“Young people especially will be quick to adopt [contactless]. They’re already living in the digital world and paying small amounts by card.”27 — Nils Ragnar Løvhaug, 2014

STUDENTS &THE PAYMENT EXPERIENCE

The payment experience matters

Consumers in general don’t only care about what they’re buying: they care about how they pay for it too. They want choice and flexibility, and they’ll vote with their feet if they don’t get it, with 31% of consumers more likely to shop at places which offer a range of payment methods28 and 41% of consumers admitting that fast and easy payments influence their purchasing29.

47% of UK customers are likely to use e-wallets, and 50% of shoppers want to access services by mobile devices30. (In fact, the mobile phone will only increase in importance, whether used to make payments or to verify the identity of the bearer.) And it’s worth remembering that around two million people in the UK don’t have a bank account31, and a billion people across the globe (over 14% of the world’s population) don’t have a bank account — but do have a mobile phone32.

Cash can be problematic for students

The UK’s Payments Council, representing the payments industry, says that the heaviest users of cash are older adults and those in socio-economic groups D and E33— providing a strong indication (if any were needed) that it’s socially mobile young people who have the highest propensity to reject cash in favour of other payment methods. A study by the British Retail Consortium found that the use of cash had declined by 14% over five years, while debit cards had grown by 11%; “This phenomenon is particularly pronounced among young people who are keen to use new payment technologies,” they said34.

Individuals aged 18-34 are four times more likely to carry a phone than cash35, highlighting the growing importance of the mobile phone as a replacement for all or part of the wallet. Furthermore, 2015 research from Visa indicates that 75% of 16-24 year olds in the UK “would feel comfortable using information such as fingerprint scans, facial recognition or retina scanning in place of traditional passcodes36”.

Not only do students tend to be more technology-savvy, but cash can be more problematic for them. To begin with, young people tend not to know how much cash they have37. Also, their purchasing patterns are often concentrated in one area, on and around campus, and can reflect odd hours; therefore, accessing an ATM (and one which is loaded and functioning) may not always be easy, free or safe.

Most students are living on a tight budget, and may not always have cash on them. Using cash to pay for goods and services can drain a bank account: paying for a £4.99 meal, for example, necessitates withdrawing at least £10 from an ATM, i.e. more cash than immediately required. And since cash doesn’t provide a neat record of transactions/balances (unless receipts are carefully kept and regularly tallied — and we’re talking about students, here), it can be all too easy to slide unknowingly into an overdraft situation, which is one of the reasons why using cash can lead to lower levels of financial inclusion38. The Gates Foundation has invested $500million in mobile phone based financial management; the programme’s director claims that “cash is the enemy of the poor39”.

08

Payment and the university brand experience

Consumers are also looking for a consistent brand experience41: a single way to interact with a brand, across all touch points, in a way which feels familiar and relevant. In the university context, this becomes a critical point both for the student and the institution.

Brand-aware students need to make a wide variety of online and offline purchases from multiple suppliers — not just the institution (from catering to the library and laundry) but also its suppliers and partners, plus peripheral organisations such as bus companies.

It would make sense for universities and colleges, therefore, to make things easier for students by providing a unified, fast, easy, cashless way to pay for almost everything, both on campus and even beyond. For the university or college, this strengthens the student experience and provides peace of mind for parents (and perhaps even bank managers).

09

“Technology can [help] people keep track of their spending… Prepaid cards… can be a useful tool to help people manage their money more effectively.”40 — Financial Inclusion Commission, 2015

At a glance:

5. Consumers prefer a choice of payment options

6. Not everyone has a bank account

7. Fast and easy payment methods influence purchasing habits

8. Cash is less suitable for students and can diminish their financial inclusion

9. Young people are less likely to carry cash or to know how much cash they have.

10

“The most successful campuses will create a ubiquitous-use environment where the student doesn’t have to think ‘card or mobile?’ …but instead can simply leverage their mobile for the full gamut of activities on campus.”42 — Jeff Staples, Blackboard Transact, 2015

UNIVERSITIES &THE STUDENT EXPERIENCE

Students increasingly see themselves as consumers of, rather than simply participants in, higher education43. Those who are very conscious of paying for the experience become more conscious of what they’re paying for. That sense of being a consumer means continually weighing up the perceived value of goods and services versus the price paid for them, and this extends beyond tuition. Finance, therefore, is an important component of the student experience. In a 2013 UK survey, “students spoke as often about immediate financial concerns, such as money for food, rent and transport, as about tuition fees and student loans44”.

The same survey suggests that students expect institutions to take on responsibility, oversight and partnership for things as varied as accommodation, transport, spaces, cheap/healthy food options, and social activities. It says that students also “focus on functional aspects of IT infrastructure, including ease and reliability of accessing resources and quality of wireless internet”, and that they value a sense of community and belonging, and a high-quality environment.

In other words, students expect institutions to invest in wider aspects of student life, including inclusion, all supported by the latest technology. Students have a loud collective voice in this highly competitive market, of which universities are only too aware. The Times Higher Education Student Experience Survey, for example, takes into account a much broader student experience than the learning-oriented NSS survey.

The student experience affects retention and recruitment

Student retention – preventing students from dropping out – is of growing concern to institutions45, but improving the broad student experience can help to cut withdrawal rates and is ‘pivotal’ to the ability to attract students46.

11

Attracting international students

The government is concerned that the UK isn’t attracting enough international students, who make a significant contribution to the economy47. Certainly, British universities see the recruitment of international students as lucrative and highly competitive. While international students’ perception of student satisfaction doesn’t necessarily drive their choice of institution, it does have a bearing on their decisions48.

Furthermore, once they have arrived in the UK, international students can face particular challenges with regard to paying for goods and services. For example:

• AccessingaUKbankaccount

• Easeofreceivingmoneysentbyparents

• Languagedifficulties

• Problemswithunderstandingcurrencyconversions,calculatingandcountingchange,etc

• Lackofparentaloversightonspending.

At a glance:

10. A student’s financial and technological experience affects their overall experience

11. Students expect institutions to invest in their experience beyond tuition

12. A better student experience enables institutions to attract and retain more students

13. Support with financial management can be of value to international students.

UNIVERSITIES & THE COMMERCIAL IMPERATIVE

Universities have worked hard in recent years to deliver value for money, meeting successive CSR efficiency targets and saving over £1 billion from 2011-201450. However, there is no let-up in the demand for further cost savings, with continuous cuts to public funding; increasing mobility of a more discerning domestic student population, willing to look to cheaper overseas institutions; increased competition for international students; and the constant demand for a better student experience.

Furthermore, the removal of the ‘cap’ on student places in 2015 is likely to lead to higher costs and an increase in the number of stu-dents with low prior attainment51 — which means that universities will have to save money even as they drive up their student satisfac-tion (and reputation) in order to attract and retain a higher calibre of student.

Finding new efficiencies is a growing challenge. Cost savings from asset-sharing, improved estate management and better energy efficiency have been some of the ‘low-hanging fruit’ which have delivered returns — but finding new sources of savings can be chal-lenging, demanding increasingly innovative solutions52. Leveraging technology to go cashless represents one such innovative step.

“Delivering efficiency and value for money is an absolute operational priority… universities must work in ever smarter and more innovative ways.”49 — Chair, UUK Efficiency Task Group, 2015

12

“Universities and colleges must face the reality that, although they exist primarily as places of learning, they also need to behave as businesses.”53 — Chris Davies, Global Payments, 2014

At a glance:

14. There is growing pressure for universities and colleges to save money

15. At the same time, they must compete more intensively and in a global market

16. Institutions must find increasingly innovative ways to deliver efficiencies

17. Going cashless can deliver both cost savings and an enhanced student experience.

WHAT DOES A CASHLESS CAMPUSLOOK LIKE?

‘Cashless’, although a commonly used term, is actually a misnomer. It’s unlikely that campuses will go entirely cashless in the foreseeable future, but for our purposes we’ll use the term ‘cashless’ to indicate ‘a lot less cash’.

Under a fully integrated cashless system, a single common payment mechanism provides access to goods and services right across the campus (and even beyond), incorporating products and services such as the learning environment, library, common amenities, catering, security, shops (on campus and online), on and off campus transport, and much more. At the time of payment, the purchaser must prove their identity.

The system

In simple terms, a cashless system involves:

• Anaccountforeachuser.Afterloggingin,theycanseetheirtransactionsandbalances,andcanperformaccountandcard management functions.

• Apaymentmechanismforusers,linkedtotheiraccount.Thiscouldbeviathechipinasmartcard(whichcouldevenbe the institution’s existing student card; smartcards can invariably already support an e-payment system). Beyond cards, payment mechanisms will increasingly include mobile phones or even a smart watches, key fobs or bracelets. The mechanism is issued/made available to students and staff, with temporary access provided to visitors, delegates, contractors and others.

• Amechanismforverifyingtheuser’sidentityateachtransaction.Thisisdonewithproximity/smartcardscarryingadigital key, or ‘ID tokens’ via mobile phones for contactless methods*, or with biometrics – such as fingerprints or retina scans.

• Paymentterminalsfordebitinguseraccounts.Thesecouldbeateachrequiredpointofsale–anythingfromarestauranttill to a vending machine, a library printer, a laundromat washing machine, online consumables shops, and much more.

• Theabilitytoaddfundstotheaccount.Fundscanbeaddedeitherbythecardholderorthirdpartiessuchasparentsorthe institution (for example, when paying out bursaries). This can be done online, for example via PayPal, debit/credit card, bank transfer or standing order, or in person using kiosks around the campus (which will accept cash), just as Oyster cards can be topped up at London Underground stations.

• Atransactionengine(apowerfulrelationaldatabase)whichwillmanagetheentireprocess.

*Mobile-phone identification can use near field communication (NFC), offering very-short-range wireless communications of up to 10cm for Android, Blackberry and Windows Mobile; or Bluetooth, offering up to 50m wireless communication, on the above platforms plus iPhone (using Apple Pay)

13

Choosing a payment mechanism

Some banks are keen to promote the use of their own EMV cards in student settings, either under their own name or white-labelled with the institution’s own brand. Getting into the institutions provides access to the next generation of higher earners while also delivering revenue (because EMV-compliant terminals are expensive, and every transaction carries a fee).

But Richard Poynder of Smartex, the UK association for smart technology, points out that universities and students are less enthusiastic about using EMV cards. Magnetic stripes are typically reserved for bank use and can’t be used for other purposes. From a management perspective, there are delays with clearing funds and replacing cards. The university has less control, and they may balk at the bank’s overt branding – not just the logo, but because of distrust of banks. Students almost certainly already have at least one contactless EMV card (why add yet another?), and there are difficulties with how to load funds onto those cards. Plus, who owns the card itself, or the data about the cardholder and their transactions?

According to Poynder, “The slow migration over the last 15 years by the 163 UK universities from magnetic-striped campus cards to smart contactless cards has provided opportunities for the latter to be used as the relatively secure, portable token to authorise and authenticate on campus payments. Increasingly, universities are attempting to support many functions with a single campus card per student or staff member.”

14

Adapted from Use by Universities of EMV Contactless-Enabled Payment Cards on Campus, Smartex, 201554

* Open loop and closed loop systems are explained in the next section

Info/options

- Chip & PIN/contactless open-loop* credit/debit cards- Prepaid cards

- Payment apps

- Proprietary (often provided by catering system suppliers, but occasionally independent system providers), OR- White-label or closed loop* EMV (chip & pin) cards- Prepaid cards.

- This open loop* system is rarely seen on the high street

Payment mechanism

Standard consumer smartcards

Mobile phones

University-operated closed-loop* cashless payment systems using plastic cards

sQuid

2010

200

400

600

800

52.9

02011

101.1

163.1

235.4

325.2

431.1

563.4

721.4

2012 2013 2014 2015 2016 2017

Your phone will be your wallet

In future, it is highly likely that the mobile phone will dominate in this area; after all, there are now 4.6 billion of them in use worldwide, out of a population of 7 billion56. The author of The End of Money, David Wolman, claims that “Phones are the solution to getting financial services to the masses.57”

The global volume of mobile phone enabled financial transactions is growing dramatically – and it’s not unusual for developing countries to be more ahead of the UK in this area. The volume is expected to more than double between 2014 and 2017, rising from US$325 billion to US$721 worldwide:

15

“Universities see smartphones as the main form factor for the future… they believe that these will change the game entirely.”55 — Richard Poynder, Smartex, 2015

Statista: Global mobile payment transaction volume from 2010 to 201758

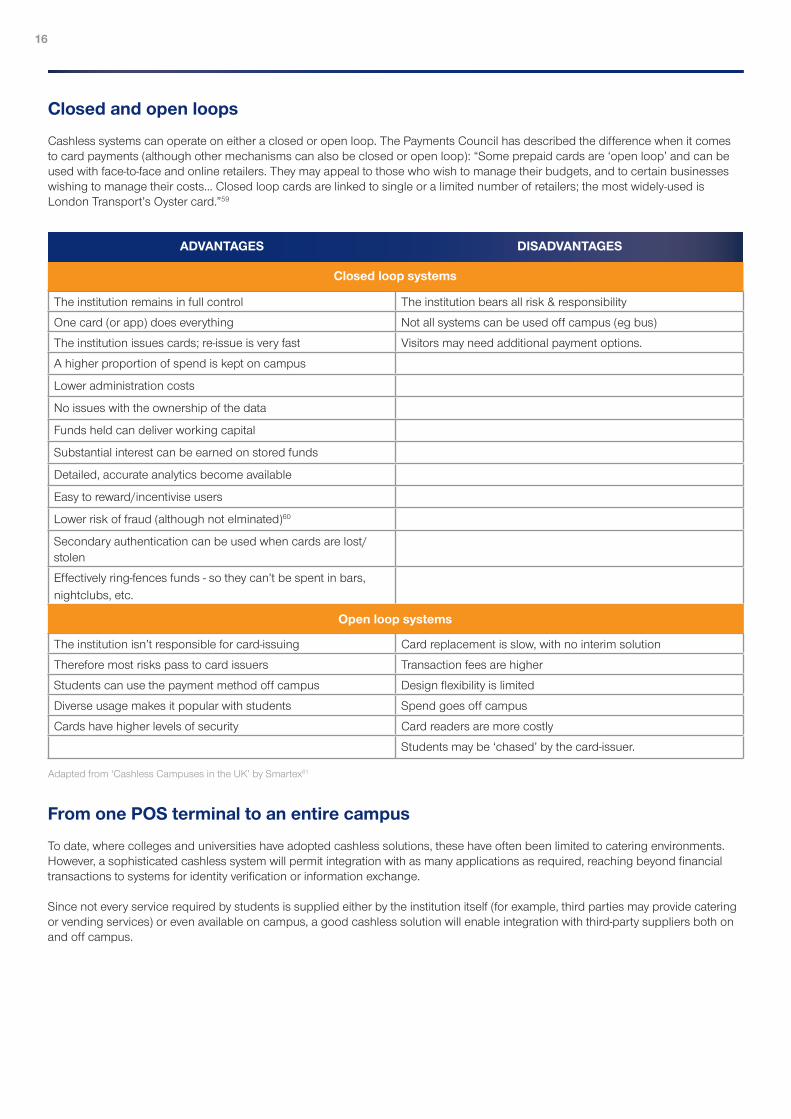

Closed and open loops

Cashless systems can operate on either a closed or open loop. The Payments Council has described the difference when it comes to card payments (although other mechanisms can also be closed or open loop): “Some prepaid cards are ‘open loop’ and can be used with face-to-face and online retailers. They may appeal to those who wish to manage their budgets, and to certain businesses wishing to manage their costs… Closed loop cards are linked to single or a limited number of retailers; the most widely-used is London Transport’s Oyster card.”59

From one POS terminal to an entire campus

To date, where colleges and universities have adopted cashless solutions, these have often been limited to catering environments. However, a sophisticated cashless system will permit integration with as many applications as required, reaching beyond financial transactions to systems for identity verification or information exchange.

Since not every service required by students is supplied either by the institution itself (for example, third parties may provide catering or vending services) or even available on campus, a good cashless solution will enable integration with third-party suppliers both on and off campus.

16

The institution isn’t responsible for card-issuing Card replacement is slow, with no interim solution

Therefore most risks pass to card issuers Transaction fees are higher

Students can use the payment method off campus Design flexibility is limited

Diverse usage makes it popular with students Spend goes off campus

Cards have higher levels of security Card readers are more costly

Students may be ‘chased’ by the card-issuer.

The institution remains in full control The institution bears all risk & responsibility

One card (or app) does everything Not all systems can be used off campus (eg bus)

The institution issues cards; re-issue is very fast Visitors may need additional payment options.

A higher proportion of spend is kept on campus

Lower administration costs

No issues with the ownership of the data

Funds held can deliver working capital

Substantial interest can be earned on stored funds

Detailed, accurate analytics become available

Easy to reward/incentivise users

Lower risk of fraud (although not elminated)60

Secondary authentication can be used when cards are lost/stolen

Effectively ring-fences funds - so they can’t be spent in bars, nightclubs, etc.

Adapted from ‘Cashless Campuses in the UK’ by Smartex61

Open loop systems

Closed loop systems

ADVANTAGES DISADVANTAGES

17

At a glance:

18. ‘Cashless’ doesn’t mean no cash at all

19. One non-cash method can pay for goods and services across campus — and beyond

20. Multiple payment methods are available, but smartcards will give way to mobile phones in future

21. Institutions can choose between closed and open loop systems

22. Cashless systems can be invaluable even for transactions which don’t involve money.

Liberating data

Crucially, the transaction engine also delivers detailed management information. No longer must important information be held in hard-to-access silos spread across campus: it can now be held in one place and used to inform decision-making, enhance student engagement, increase income and cut costs.

Detailed, user-level information can be used to deliver targeted promotions – not just for marketing purposes but for public health and other issues related to student and staff wellbeing.

On campus Bursary distribution

Catering Visitor & contractor security (signing in & out)

Vending Cleaner sign-in/sign-out

Laundrettes Security patrol check-ins

Consumables - IT, stationery, art supplies, etc Door access control

Institution’s online store Security tracking for students walking alone

Bookstores Room booking (sports halls, class/meeting rooms)

Mini-markets Student attendance registration

Ticketing - events, etc. Examinee validation

Library fines Equipment sign-out

Copying, printing, binding, etc. Proof of age

Fee payments - accomodation, exams, etc. Locker access

Parking Computer access

University-operated buses/shuttles Voting

Off campus Students’ union & society membership

Partner retailers (e.g. university bookshops) Leisure scheme management

Local transport fares (e.g. buses) Marketing & reward/loyalty campaigns

Financial transactions

On Campus

Off Campus

Non-financial applications

EXAMPLE APPLICATIONS FOR A ONE CARD CASHLESS SYSTEMS

SUMMARY OF BENEFITSFOR STAKEHOLDERS

Benefits for the institution

• Simpleradministrationbecauseonesystemcandoitall(orasmuchofitasrequired)

• Greatlyreducedcostsofreceiving,counting,insuring,storing,reconciling,transportingandreconcilingcash

• Reducedriskarisingfromrobbery,theft,fraudandcounterfeiting

• FewerEMVmerchantterminalsmeansareductioninPOSandtransactioncosts

• Operatingcostsarereduced:oneuniversityestimatedsaving8%bygoingcashless

• Aclosedloopsystemwillkeepspendoncampus,andmayboostrevenuebyupto20%62

• Aclosedloopsystemwillcutthecostoftransactions(merchantservices)

• Studentfundsheldinaclosedloopsystem(whichcouldamounttohundredsofthousandsofpoundsatatimeforlarger institutions) can support cash flow and earn substantial interest

• Significantlyfastertransactionsleadtogreaterthroughput,helpingtokeeppeople(andspend) moving at peak times

• Sincestudentshavingcashonthemisnolongeranissue,libraryfinesarepaidsooner

• Stockmanagementissimplified

• Securityisenhancedthroughphysicalandelectronicaccesscontrol,guardpatrolcheck-ins,etc

• Financialreportsandadministrationcanbeautomated

• Datacanbemovedoutofsilos,centralisedandcross-referenced–andthenusedtoinformpolicy and decision-making

• Compliancewithvisaregulationsbecomeseasierthankstotheeaseofmonitoringphysicalattendanceatlectures

• Collegesfinditeasiertoachievecompliancewithfreemealprovisionforunder-18s

• Studentengagementisenhancedthroughon-cardbrandinganddiscounts/rewards

• Thereisgreatercontroloverthebatch-creditingofbursaries

• Bursarypaymentscanbeadministeredeasilyandthespendcontrolledsoitiskeptoncampus • Departmentalfundscanbering-fenced;codescanbeassignedtoparticulartypesofspend,withbudgetscontrolledwithin overall limits and limits per code

• Staffminimisetheirinvolvementinhigh-volume,low-costtransactions

• Student,staff,visitorandpartner/supplierexperiencesareallimproved

18

• Contactwithstudentsthroughtheironlineaccountdeliversacommunicationopportunity

• Cashlesssystemsminimisetheneedtoprintreceipts–savingtimeandothercosts

• Itsupportsthegreenagenda:cashusesupnaturalresourcesandrequiresfuelfortransportation.

Benefits for UK students

• Onefast,easysystemcanaccessawiderangeofgoodsandservices,onorevenoffcampus

• Studentsbenefitfromdiscounts,rewardsandpre-loadedcreditsofferedbytheinstitutiontoincentivisetake-up

• There’snoneedtogolookingforfunctioningATMstoaccessfunds;thesecanbedistant,expensiveandasecurityrisk (especially at night)

• There’snoneedforuserstoworryaboutholdingcashorhowmuchisheld;there’snoneedtoweighupwhichmethodto use when paying

• Fundscanbeloadedtotheaccountquicklyandconveniently—atkiosksoncampus,oronlinebystudentsand/ortheir parents

• Studentshavegreatercontrolovertheirfinances:there’snoneedtowithdrawmorecashthanisimmediatelyneeded;trans action histories are viewable online; it’s easier to avoid overdrafts

• Fastertransactionsavoidwastingtimeinqueuesandarrivinglateforlectures

• Usershavelesstocarryaround(noneedforwalletstobebulkedoutwithcards,heavycoins,etc)

• It’squickandeasytoblocklostorstolensmartcardsandimmediatelysetupanalternativepaymentsystem(andtounblock cards again)

• Bullyingisreduced,andstudentswhoqualifyforfreemealsarediscreetlyidentified.

Additional benefits for international students

• AccessingaUKbankaccountandbank-issuedEMVcardscanbecomplicatedandslow:university-issuedcontactless cards/mobile phone apps can be provided quickly

• There’snoneedtoworrywhetheroverseasEMVcardswillwork,ortogetthemunblocked

• Ithelpstoavoidinitiallanguageandcurrencydifficultiesduringtransactions(egunderstandingPOSstaff,counting change, etc.)

• It’squickandeasyforparentstocredittheaccountusingarangeofpaymentoptions

• ManyEuropeanstudentsexpectcashless,becausetheymayhavehaditathighschool,andmanycounties(e.g.theFar East) are ahead of us on mobile-phone and contactless payments

• ItavoidsoverseasstudentsbringinglargeamountsofcashwiththemtotheUK.

19

Benefits for parents/guardians

• Itprovidesafastwaytodeliverfundstostudents,especiallyinurgentsituations(thusalsodeliveringpeaceofmind)

• Themoresophisticatedcashlesssystemsallowstudentstochoosewhethertheirparentscanviewtheirtransactionhistories and balances.

Additional benefits for staff

• Lesstimeiswastedqueuingforprint,refreshmentsetc

• Meetingsandclassesaremorelikelytostarton-timeasaresult

• Staffaresaferbecausetheyhandlelesscash,lessoften

• Tediouscash-managementtimeisreduced

• Staffproductivityisimproved

• Staffabsenteeismwilldecreasewherebacteria-ladenbanknoteshadbeencausinginfection.

Benefits for third-party suppliers (e.g. catering contractors)

• Closedloopsystemshelptokeepspendoncampus

• University-ledpromotions&discountsencouragespendoncampus

• Stockmanagement,administrationandcash-handlingaresimplified,lesscostlyandmoresecure

• Moreaccuratestock/incomereportingbecomespossible.

At a glance:

23. Going cashless offers significant benefits for the institution and its staff; UK and international students; parents/guardians; and third-party suppliers.

20

THE HURDLES & HOW TOGET OVER THEM

Institutions have been slower than expected to adopt cashless systems, whether for a single function (such as catering) or a fully integrated campus. There can be uncertainty about making the transition — but it’s much more straightforward than some institutions might think.

21

Cost of implementation

Introducing new technology can sound expensive, but institutions often forget about two key things: (a) the real cost of cash, which they could be saving, and (b) the additional benefits of going cashless. Colleges and universities should assess the amount of employee time spent counting, ordering, reconciling and banking cash; the cost of securely storing it (in safes etc); the cost of errors and counterfeits; the cost of bank charges; the cost of cash collection/transportation fees; the cost and hassle of providing floats around campus; the cost of insuring cash; and more. Then there are the benefits (such as from cash flow and interest earned) to be accrued from holding funds within the cashless system: at one institution, these averaged £1.5m at any one time. It may be more difficult to assign a financial value to efficiency savings and the benefit of enhanced access to data, etc., but these should nevertheless be taken into account before drawing up a comprehensive cost/benefit analysis.

Implementing a cashless campus doesn’t have to be done all at once. A phased implementation may make the transition easier, spread the cost, and help to get individual modules through under departmental spending thresholds.

The cost of integrating the new cashless system with existing systems needn’t be high. A simple interface to one third-party module (such as a vending system) should take a good vendor just a few days; a campus-wide integration will take a few weeks.

Then there’s the opportunity cost. Not going ahead with a cashless campus only delays the inevitable: cash is on its way out. Real savings and revenues can be realised now by going cashless, and while it’s difficult to put a value on enhancements to the student and staff experiences, the competitive advantage is there nonetheless.

It’s worth pointing out that although around 100 UK universities have moved to smartcards, only about 20% of them have enabled the card to be used for payment and/or in multiple schemes. This means that, for 80% of them, their existing investment in smart technology already isn’t delivering its potential returns.

Internal stakeholders need buy-in

Although stakeholders worry about technological problems with their solution, in truth technology is rarely an issue and it is human concerns which need more attention. Some people will struggle with the concept of going cashless. Communicating the inevitability of the demise of cash, as well as the real practical and financial benefits of going cashless, will be invaluable. Also, a phased implementation will seem less overwhelming and enables each phase to be tested before moving onto the next.

The work around going cashless mostly resides within the IT department, but has significant links to estates, catering, laundry, transport, sports, finance, the library, and more. Going cashless involves a lot of people at many levels, and faculties will need to work well together — which is not necessarily a given. Similarly, the IT department needs to be on-board and enthusiastic about the project. Consultation, involvement and communication are therefore critically important.

Those who will be customer-facing, and worried about how they’ll handle cashless transactions in general plus any teething problems in the first weeks, will also need training and reassurance. Ideally, key people driving the transition should be alongside these teams during the launch phase.

Some people may be resistant to going cashless because they may have personally overseen the introduction of an existing system, perhaps even recently. They may have worked hard on a lengthy and complex tender process, and have carefully negotiated supplier agreements. They won’t want to see their project scrapped — and it needn’t be, as long as the chosen cashless vendor can integrate with existing systems.

Third-party contractors have systems already in place

Colleges and universities may initially feel ‘locked-in’ by suppliers; the classic example would be the third-party catering contractor. Many institutions have these, and they involve substantial contracts dealing with very large numbers of transactions. The catering provider may be resistant to change, whether they have their own cashless operation or not, especially with any ‘not invented here’ solution. They may even claim that functionality would be lost in the transition (although this is extremely unlikely). However, with the right vendor and system, there’s no technical reason why full integration can’t be achieved. Institutions may want to consider their timing vis à vis existing contracts. If there are three years to run on a catering contract, consider whether to do it now, or wait. Contract renewal could be made contingent on integrating to the new cashless system. Or, at worst, you could choose to scrap the contract and pay the penalties — although, when it comes down to it, most catering contractors would far rather change their POS system than lose a lucrative contract.

Management & responsibility

Going cashless can feel like a big change, so it will need strong project management as well as project ambassadors (in IT, finance, estates and the faculties, for example) who are well-informed and enthusiastic about the change. Going cashless typically involves consultation and negotiation not only with internal stakeholders but also external ones (such as catering companies); a good vendor will be willing and able to handle a proportion of this for you, using their experience to achieve your goals effectively and within a shorter timeframe. High-level endorsement, from within the senate, will help to drive the project through.

Availability of whole-solution vendors

Most institutions who have started to go cashless have so far limited themselves to a couple of schemes only, such as catering and/or print and copy. To some extent, this has been driven by the fact that most vendors can’t offer more than that. Clearly, however, universities and colleges will increasingly demand more from vendors in order to keep pace with the available technology, changing market demand and the expectations of students.

As a result, it’s critically important not only to choose a vendor which can offer cashless across a very wide range of applications but also one with solid experience of doing so (and there are relatively few of these). As a result of the low number of well-integrated cashless campuses and the small number of more sophisticated, experienced vendors, there is only a relatively small number of UK reference sites at present — but this is changing.

22

Not everyone has a bank account/UK bank account

Some institutions are concerned about going cashless because – as we’ve seen – not everyone has a bank account, and therefore this impacts on the ability to load funds into student accounts in the cashless system. However, UK students must have a bank account if they receive student finance; even if they don’t, their parents’ bank account/s can be used. For international students who may not have a UK bank account, or may experience delays getting one, their parents overseas can load funds into the account (so you should check how many top-up options are offered by your vendor shortlist). Furthermore, international students who bring large amounts of cash with them can top up with cash at kiosks around campus.

Ensuring scheme take-up

Plan your cashless launch campaign very carefully so that you get rapid uptake among students and staff. Ensure that users understand the many benefits of going cashless, and that they will be incentivised and rewarded for adopting the new system. SMS messages from the institution offer an effective way to send offers to students; for example to boost quiet periods in catering outlets, eg 20% off coffee before 10am, or to alert students to PC availability.

Other offers could include £5 preloaded onto every new account; discounted laundromat-use at off-peak times whenever cashless is used; free account credits on users’ birthdays; rewards when a certain number of transactions have been reached on an account; rewards for healthy living (eg use of the sports hall); etc.

If you’ve chosen an open-loop system, which enables users to spend off-campus, your university-operated outlets will be competing with external third-party outlets — all the more reason to find ways to motivate users to spend in your own outlets.

23

At a glance:

24. Institutions tend to have unnecessary worries about gong cashless

25. Information, consultation and negotiation are crucial for achieving stakeholder buy-in

26. A good cashless solution vendor will help the institution to get over any

WHAT TO LOOK FOR & PITFALLS TO AVOID WHEN CHOOSING A VENDOR

Institutions will want to talk to multiple vendors to find the right solution for them. Here’s a starting list of issues to consider and questions to ask.

Can the vendors integrate the whole campus — or even beyond?

Cashless campus solutions are more attractive to users if they work at more than one outlet, so the broader your system, the better your user buy-in will be. This, in turn, helps to keep as much spend as possible on campus.

Some vendors offer only one or two cashless ‘modules’, such as catering and/or copy/print. The fact that e-payments will increasingly replace cash means that you need to think medium to long term, not short term — or your investment will rapidly show up its limitations. Look for a wide range of modules within the system (such as vending, laundromats, access control, room-booking, etc - see the chart on page 17). You should also check that the system can integrate easily with third-party e-payment systems, such as any provided by a catering contractor and external systems such as local transport providers.

Your ideal vendor will offer you the choice of taking you cashless using only their own solution, from the ground up, or providing core elements of the system and then integrating with existing and/or third-party systems.

How ‘open’ is the vendor?

Your vendor should use common standards to facilitate integration and to help future-proof your solution: avoid proprietary technology or systems which can’t use a choice of protocols in important areas. Alarm bells should ring if the system can’t integrate easily to Windows POS systems, or doesn’t use a common database format, for example. Look for a system which uses SOAP (Simple Object Access Protocol) to assure easy integration between the cashless and other systems.

Mobile-phone apps used for verification or payment should run on the major mobile platforms, including Android, iOS and Windows Mobile. And a good cashless system will handle most major payment providers (eg Worldpay, Streamline, Sage Pay, GlobalPAY, PayPal, EMV cards, etc).

Do you want an open or closed loop system?

Decide whether you’re looking for a closed loop or open loop system (see comparison chart on page 16). Your potential vendors will need to support what you’re looking for.

How scalable is the system?

The capacity of your cashless system will depend in turn on the capacity of your server/s and your network, plus the load you place upon the system. If your cashless solution isn’t scalable, it will grind to a halt when you hit a critical size, and you’ll need to do significant redevelopment work.

Look for a scalable system which can grow with your solution and with your institution, and ask potential system vendors to identify any likely bottlenecks on your campus and what may need to be done to address them. You should be able to add as many users and as many transactions, at as many points and outlets, via as many third-party system integrations, as you need.

How secure is the system?

Ensure that all parts of the solution are password protected and that they run on websites served over HTTPS. All transactions should require user-identity verification involving ID tokens — whether RFID in a smartcard, NFC in a mobile phone, or biometrics (such as fingerprints or retina scans). You should ensure that these protocols are already supported by your vendor’s system, or that there are definite plans to do so. Check also that the software development kit (SDK) is fully secure.

24

Where will your server be?

Will the system be held in-house, or hosted? On campus servers are managed by the institution, while hosted solutions will be managed by the vendor. You may want to consider the differences when it comes to security and system administration, and to look at hire costs and costs per transaction. Another factor may be staff capacity and buy-in within the IT function.

Can the system work with pre-existing & external data?

Ask how easily the vendors’ systems will link to databases such as your student record system. To what extent can the links between them be automated? Will the cashless system automatically access information about new and departed students, and adapt permissions accordingly — and can the data exchanges be scheduled to avoid manual intervention?

Can you still support some cash & EMV payments?

No ‘cashless’ campus systems are, as yet, entirely cashless. To begin with, some applications (such as laundromats and vending machines) may be best running dual cash/cashless payment methods. Additionally, for higher-value purchases (such as accommodation fees or expensive textbooks), users may prefer to use EMV credit cards. Senior senate staff may wish to use EMV cards when entertaining VIP guests in on campus restaurants. Therefore, check that your vendor can accommodate all the payment methods you want.

How many user-identification options are supported?

Smartcards will gradually be replaced as a verification method, so look for support for NFC or Bluetooth (usually on smartphones) and/or biometrics. If the support isn’t currently there, look for a commitment to deliver it within a defined timeframe.

How many payment methods are supported?

Today, e-payment methods can include smartcards and mobile phone apps, but in future will include options such as smart watches and key fobs. Commitment to a mobile phone application is essential in the short term, but check also that your vendors plan to support emerging technologies. Then there’s the number of top-up methods: how flexible are the vendors’ solutions when it comes to the different ways in which users and parents can top up online?

Who owns your data?

Data protection is increasingly regulated and you’ll want clarity around data ownership so that you can remain compliant. Ensure you discuss data ownership and data protection with your vendors, especially if you have an open loop system, your servers are hosted off site, and/or you’re rebadging an EMV card system.

Can single & daily transaction limits be set?

The institution or users may want to set these limits to protect the individual’s finances. This may be especially important in an open loop system.

Can parents see transactions, if the student wants them to?

A more sophisticated system will provide a wide range of options at institution and user level. For example, the institution may wish to provide students with the option of whether to permit their parents to see their transaction history.

What level of support is available?

Look for a vendor who offers all the pre-sales support you need, because having absolute clarity about your project – and being ready to answer queries and concerns – will help to get all of your internal and external stakeholders on board. As for post-sales support, compare the service level agreements on offer from the vendors to assure the level of service you need within a certain number of hours or days, depending on the level of urgency in each potential situation.

25

Lack of clarity of the business case, and no strong perceived imperative to proceed

Unclear project ownership and poor branding for the scheme

Difficulty in adapting existing functional systems to operate with smart cards

Failure to get faculties, schools and administrative departments to work together

Not getting the best from suppliers or becoming ‘locked in’ to one

Introduction of new staff working practices meets resistance

Students and staff have no good reason always to carry their smart campus cards

Reputational damage due to poor planning, resulting in delayed or unsuccessful launch

Undertainty about the potential impact of Near Field Communication-based mobiles

Difficulty in handling cards for occasional visitors to campus

Difficulty in eliminating the use of cash at campus points payments

Why some [campus] smartcard systems fail

How will you handle card, balance & transaction issues?

It’s worth checking with your potential vendors how you’d handle situations such as the following:

• Automaticissuingofnewandreplacementsmartcards

• Migratinglegacyuseraccounts/balancesanduniqueidentifierswhentransitioningfromonesystemtoanother

• Transactionsdisputedbytheuser

• Refundsandrebates(suchaswhenunclaimedfundsareleftinuseraccountsaftergraduation/departure).

26

“There’s clearly an appetite for new methods of payment among students – so they will come to expect more sophisticated ways to pay as these trends gather momentum in the consumer world. Universities need to take careful consideration of this as they think about how they market themselves to the next generation of tech-savvy students.”64

— Chris Davies, Global Payments

At a glance:

27. Knowing what you’re looking for, and the questions to ask, will help you to choose the right vendor and assure a successful solution.

Why use smartcards? - HESCA63

REFERENCES

1 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society. 2012, Da Capo Press. 2 Financial Inclusion Commission — Financial Inclusion: Improving the financial health of the nation, 2015 http://www.finan cialinclusioncommission.org.uk/pdfs/fic_report_2015.pdf3 Niklas Arvidsson, Sweden’s Royal Institute of Technology — Welcome to Sweden - the most cash-free society on the planet, 2014 http://www.theguardian.com/world/2014/nov/11/welcome-sweden-electronic-money-not-so- funny4 CNBC — Cashless Africa: Kenya’s smash success with mobile money, 2013 http://www.cnbc.com/id/1011804695 Pew Research Centre — The future of money: Smartphone swiping in the mobile age, 2012 http://www.pewinternet. org/2012/04/17/the-future-of-money-in-a-mobile-age/6 David Wolman — Why America Is Going Cashless, 2012 http://www.huffingtonpost.com/david-wolman/cash-america- book_b_1353423.html7 Link — Link website homepage, 2015 http://www.link.co.uk/Pages/Home.aspx8 Financial Inclusion Commission — Financial Inclusion: Improving the financial health of the nation, 2015 http://www.finan cialinclusioncommission.org.uk/pdfs/fic_report_2015.pdf9 Nets — Digital Values, issue 1, 2014 http://www.nets.eu/SiteCollectionDocuments/Digital-Values/Nets-Digital-Values-issue- one-2014.pdf10 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society. 2012, Da Capo Press. 11 Sage Pay — The Payments Landscape, 2014 http://www.engage.sagepay.com/paymentslandscapedownload-012 Bank of England — Counterfeit Bank of England Banknotes, 2015 http://www.bankofengland.co.uk/banknotes/Pages/ about/counterfeits.aspx13 Wolman: The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society. 2012, Da Capo Press. 14 Sage Pay — The Payments Landscape, 2014 http://www.engage.sagepay.com/paymentslandscapedownload-015 Professor Kai A Olsen, University of Bergen — Exporting the cashless society in Digital Values, issue 1, 2014 http://www. nets.eu/SiteCollectionDocuments/Digital-Values/Nets-Digital-Values-issue-one-2014.pdf16 Sage Pay — Cash costs UK businesses more than £17.8bn a year, 2014 http://www.sagepay.co.uk/news/cash-costs-uk- businesses-more-than-17-8bn-a-year17 The UK Cards Association — Contactless Statistics, 2014 http://www.theukcardsassociation.org.uk/contactless_contact less_statistics18 The Guardian — London tube introduces contactless payments, 2014 http://www.theguardian.com/money/2014/sep/16/ london-tube-contactless-payments-underground-oyster19 The Economist — Unfriending Cash, 2015 http://www.economist.com/news/finance-and-economics/21646802-facebook- enters-booming-market-mobile-payments-unfriending-cash?fsrc=scn/tw/te/pe/ed/unfriendingcash20 The Economist — Unfriending Cash, 2015 http://www.economist.com/news/finance-and-economics/21646802-facebook- enters-booming-market-mobile-payments-unfriending-cash?fsrc=scn/tw/te/pe/ed/unfriendingcash21 Deloitte — Contactless Mobile Phone Payments (Finally) Gain Momentum, 2015 http://www2.deloitte.com/content/dam/ Deloitte/global/Documents/Technology-Media-Telecommunications/gx-tmt-pred15-contactless-mobile-payments.pdf, sum marised at http://www.techweekeurope.co.uk/e-marketing/deloitte-mobile-payments-rise-2015-15941722 Huff Post Money — Cash Dying as Credit Card Payments Predicted to Grow in Volume, 2012 http://www.huffingtonpost. com/2012/06/07/credit-card-payments-growth_n_1575417.html23 SUMS Consulting — Cashless Campus, 2012 http://www.sums.org.uk/images/documents/Cashless%20Campus%20Brief ing%20Paper%20-%20May%202014.pdf24 BBC News – Chip and pin security and fraud fears, 2014 http://www.bbc.co.uk/news/uk-england-28465980 25 UCAS — Eight out of ten freshers have smartphones, undated http://www.ucasmedia.com/2014/eight-out-ten-freshers-have- smartphones26 Global Payments — The Payment Industry’s ‘Perfect Storm’, 2014 https://globalpaymentsinc.co.uk/images/pdfs/ GP_Payments_Whitepaper_2014.pdf

27

27 Nils Ragnar Løvhaug: Towards the Electronic Wallet in Digital Values, issue 1, 2014 http://www.nets.eu/SiteCollectionDocu ments/Digital-Values/Nets-Digital-Values-issue-one-2014.pdf28 Sage Pay — Cash costs UK businesses more than £17.8bn a year, 2014 http://www.sagepay.co.uk/news/cash- costs-uk-businesses-more-than-17-8bn-a-year29 Accenture, quoted by VendHQ — Is Retail Ready for a Cashless Society? Evaluating Retail’s Top 5 Mobile & Digital Trends, undated http://f9e7d91e313f8622e557-24a29c251add4cb0f3d45e39c18c202f.r83.cf1.rackcdn.com/Vend_VD_WP_Cash less_Final.pdf30 Weber Shandwick Netherlands — Shopping & Payments: Evolution-Revolution, 2014 http://www.slideshare.net/wsneder land/shopping-and-payments-evolutionrevolution?qid=766a8d1f-f6d0-47af-9cf4-dec4e3aba2cd&v=default&b=&from_ search=1631 Financial Inclusion Commission — Financial Inclusion: Improving the financial health of the nation, 2015 http://www.finan cialinclusioncommission.org.uk/pdfs/fic_report_2015.pdf 32 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society, 2012, Da Capo Press33 Payments Council — The Future for Cash in the UK: The initial report of the Strategic Cash Group 2010 http://www.pay mentscouncil.org.uk/files/payments_council/future_of_cash2.pdf34 Education Technology — Are cashless campuses the future? 2014 http://edtechnology.co.uk/Article/are_cashless_cam puses_the_future35 Weber Shandwick Netherlands — Shopping & Payments: Evolution-Revolution, 2014 http://www.slideshare.net/wsneder land/shopping-and-payments-evolutionrevolution?qid=766a8d1f-f6d0-47af-9cf4-dec4e3aba2cd&v=default&b=&from_ search=1636 TechWeekEurope — Young People ‘Ready To Replace Passwords With Biometric Security’, 2015 http://www.techweek europe.co.uk/e-innovation/biometric-security-replacing-password-visa-15968037 Nils Ragnar Løvhaug: Towards the Electronic Wallet in Digital Values, issue 1, 2014 http://www.nets.eu/SiteCollectionDocu ments/Digital-Values/Nets-Digital-Values-issue-one-2014.pdf38 Financial Inclusion Commission — Financial Inclusion: Improving the financial health of the nation, 2015 http://www.finan cialinclusioncommission.org.uk/pdfs/fic_report_2015.pdf39 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society, 2012, Da Capo Press. 40 Financial Inclusion Commission — Financial Inclusion: Improving the financial health of the nation, 2015 http://www.finan cialinclusioncommission.org.uk/pdfs/fic_report_2015.pdf41 VendHQ — Is Retail Ready for a Cashless Society? Evaluating Retail’s Top 5 Mobile & Digital Trends, undated http://f9e7d91e313f8622e557-24a29c251add4cb0f3d45e39c18c202f.r83.cf1.rackcdn.com/Vend_VD_WP_Cashless_Fi nal.pdf42 CR80News — Next-gen apps merge campus ID and student life, 2015 http://www.cr80news.com/news-item/next-gen- apps-merge-campus-id-and-student-life/43 Mourad, Ennew & Kourtam — Brand Equity in Higher Education, 2010 www.emeraldinsight.com/0263-4503.htm44 Kandiko & Mawer — Student Expectations and Perceptions of Higher Education, 2013 http://www.kcl.ac.uk/study/learn ingteaching/kli/research/student-experience/QAAReport.pdf45 Times Higher Education — Student Retention, 2008 http://www.timeshighereducation.co.uk/news/student-reten tion/400728.article46 Improving the Student Experience — Why improve the student experience? undated http://www.improvingthestudentexperi ence.com/why-improve-student-experience/47 All-Party Parliamentary Group on Migration — New report warns UK at risk of losing foothold in crucial international student market, 2015 http://www.appgmigration.org.uk/post-study-work-inquiry48 Hobsons — Beyond the data: Influencing international student decision making, 2014 http://go.hobsons.com/ ISS2014/&s=wl49 Universities UK — Efficiency, effectiveness and value for money, 2015 http://www.universitiesuk.ac.uk/highereducation/ Documents/2015/EfficiencyEffectivenessValueForMoney.pdf50 Universities UK — Efficiency, effectiveness and value for money, 2015 http://www.universitiesuk.ac.uk/highereducation/ Documents/2015/EfficiencyEffectivenessValueForMoney.pdf51 The Guardian — Lifting the cap on student numbers: five lessons learned from Australia, 2014 http://www.theguardian.com/ higher-education-network/2014/aug/07/lifting-the-cap-on-student-numbers-five-lessons-learned-from-australia52 Universities UK — Efficiency, effectiveness and value for money, 2015 http://www.universitiesuk.ac.uk/highereducation/ Documents/2015/EfficiencyEffectivenessValueForMoney.pdf53 Education Technology — Are cashless campuses the future? 2014 http://edtechnology.co.uk/Article/are_cashless_cam puses_the_future54 Smartex: Use by Universities of EMV Contactless-Enabled Payment Cards on Campus, 201555 Smartex: Use by Universities of EMV Contactless-Enabled Payment Cards on Campus, 201556 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society, 2012, Da Capo Press.

28

57 Wolman — The End of Money: Counterfeiters, preachers, techies, dreamers – and the coming cashless society, 2012, Da Capo Press.58 Statista — Global mobile payment transaction volume from 2010 to 2017, 2015 http://www.statista.com/statistics/226530/ mobile-payment-transaction-volume-forecast59 Payments Council — The Future for Cash in the UK, 2010 http://www.paymentscouncil.org.uk/files/payments_council/fu ture_of_cash2.pdf60 CR80News — Student uses campus card to embezzle funds, 2015 http://www.cr80news.com/news-item/student-uses- campus-card-to-embezzle-funds/61 Smartex — Cashless Campuses in the UK, 2013 http://www.slideshare.net/RichardPoynder/cashless-campuses-in-the- uk?qid=3a3a434c-0703-4b6c-b260-7c158e74d83c&v=default&b=&from_search=162 MonitorIT — Increase Revenue from Library Fines and Fees, 2015 http://monitorit.co.uk/blog/2015/03/increase-revenue- from-library-fines-and-fees/63 HESCA — Why use smartcards? (undated) via http://www.smartex.com 64 Education Technology — Are cashless campuses the future? 2014 http://edtechnology.co.uk/Article/are_cashless_cam puses_the_future

29

Unit 2, Church Lane, Naphill, Buckinghamshire, HP14 4US, UK

T: 01494 565066

W: monitorit.co.uk