case study 3 liabilities - world banksiteresources.worldbank.org/.../liabilities_case_study.pdf ·...

TRANSCRIPT

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Case study 3 liabilities

Vienna, 4 June 2013

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

2 2

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2013 with an effective date after 1 January 2013 but not the IFRSs they will replace.

Disclaimer: The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for any loss caused by acting or refraining from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

Framework-based approach for applying IFRS

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3

• What are the economics of the phenomenon (eg

transaction or event)?

• What information about the phenomenon is

relevant for informing resource allocation

decisions by existing and potential investors and

lenders who cannot require information directly

and that can be faithfully represented etc?

• Then consider IFRS requirements

• Make judgements to develop accounting policy

• Make judgements and estimates to apply the

requirements with rigour and consistency

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter, not necessarily those of the IASB or IFRS Foundation

Forward contracts: Growem and Chipem

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

5

• Forward contract is an agreement to buy/sell an asset at a fixed price on a particular date.

• Some reasons for forward contracts

• hedge economic risks (eg price fluctuations)

• speculation

• to secure future access to a scare resource

Forward contracts

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

6

• Pricing forward contracts (rational pricing theory)

• for non-perishable commodities, securities and currencies arbitrage opportunities cause the relationship between forward and spot prices to depend mainly on interest rates (the time value of money) and counterparty credit risk

• other cash flows must be adjusted for in pricing, eg dividends and storage costs

Economics—forward contracts

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

7

• Assume that today:

• spot price of gold = $1,000 per ounce

• risk free interest rate = 10%

• holding costs = nil

• no counterparty credit risk and no margin

• Forward rate 12 months = $1,100 per ounce

Economics—rational pricing theory

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

8

• ‘Proof’: if forward rate was higher (say $1,200) then

• an arbitrager would borrow $1,000 to buy an ounce of gold and immediately enter into a 12 month forward contact to sell that gold for $1,200. Result: arbitrage profit = $100 ($1,200 income less $1,000 cost of gold sold less $100 finance cost)

• put another way, rather than using a forward to hedge the risk that gold price will rise, today borrow $1,000 from bank to buy today the gold needed in 12 months time at $1,000 and pay $100 interest on the loan (ie total cash flow $1,100).

Economics—rational pricing theory

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9

• Which elements, if any, arise from a fixed price forward contract (eg for purchase of gold):

• gross (asset and liability) accounting for the rights and obligations that arise from the contract; or

• net (asset or liability) accounting for the contract?

Conceptual Framework, elements

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10

• Executory contract = contract under which neither party has performed any of its obligations or both parties have partially performed their obligations to an equal extent (IAS 37.3)

• Onerous contract = a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

• unavoidable costs = the lower of the cost of fulfilling the contract and any compensation or penalties arising from failure to fulfil it.

(IAS 37.68)

Executory contracts

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

11

• 1/1/20X1 a paper manufacturer enters into a contract to buy 1,000 tonnes of pine wood chips for A$100 per tonne on 31/12/20X3.

• On 31/12/20X1, an identical contract with a two-year time frame would be priced at A$40 per tonne.

Example 1―forward purchase contract

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

12

• Scenario 1: must settle net in cash.

• Scenario 2: must settle by physical delivery in accordance with the entity’s expected purchase requirements (ie gross settlement).

• Scenario 3: can be settled net in cash or by physical delivery (ie gross settlement).

• Scenario 4: same as 1 but entered into forward contract to hedge the cash flow exposures of commodity price risk of highly probable forecast purchase of pine wood chips.

Example 1―forward contract continued

13 Ex 1 Scenario 1―settled net in cash

Chipem is contracted to buy at A$100 in 2 years

If contracted today, would buy at A$40 in 2 years

Which IFRS specifies accounting?

Choose 1 of: (a) a derivative—IAS 39 or, if adopted

early, IFRS 9 Financial Instruments;

(b) IAS 37 Provisions, Contingent Liabilities and

Contingent Assets irrespective of whether the contract is

onerous; (c) IAS 37, only if the contract is onerous;

(d) another IFRS; or

(e) no specific IFRS therefore apply the IAS 8 hierarchy.

13

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

13

14

Ex 1 Scenario 2―physical delivery, normal usage requirements

Chipem contracted to buy at A$100 in 2 years

If contracted today would buy at A$40 in 2 years

Which IFRS specifies accounting?

Choose 1 of: (a) a derivative—IAS 39 or, if adopted

early, IFRS 9 Financial Instruments;

(b) IAS 37 Provisions, Contingent Liabilities and

Contingent Assets irrespective of whether the contract is

onerous; (c) IAS 37, only if the contract is onerous;

(d) no specific IFRS therefore apply the IAS 8 hierarchy;

(e) if onerous IAS 37; if not onerous IAS 8 hierarchy; or

(f) another IFRS.

14

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15

Significant judgement—is the forward purchase contract onerous?

• Onerous contract = a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

• unavoidable costs = the lower of the cost of fulfilling the contract and any compensation or penalties arising from failure to fulfil it.

Ex 1 Scenario 2―physical delivery, normal usage requirements continued

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

16

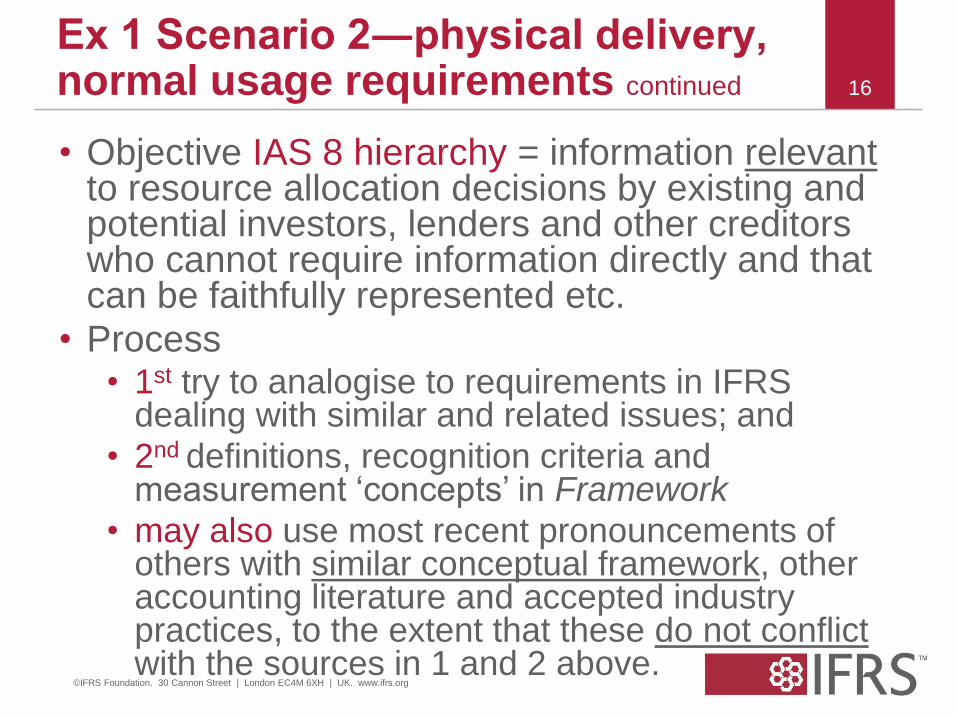

• Objective IAS 8 hierarchy = information relevant to resource allocation decisions by existing and potential investors, lenders and other creditors who cannot require information directly and that can be faithfully represented etc.

• Process • 1st try to analogise to requirements in IFRS

dealing with similar and related issues; and

• 2nd definitions, recognition criteria and measurement ‘concepts’ in Framework

• may also use most recent pronouncements of others with similar conceptual framework, other accounting literature and accepted industry practices, to the extent that these do not conflict with the sources in 1 and 2 above.

Ex 1 Scenario 2―physical delivery, normal usage requirements continued

17

Ex 1 Scenario 2―physical delivery, normal usage requirements continued

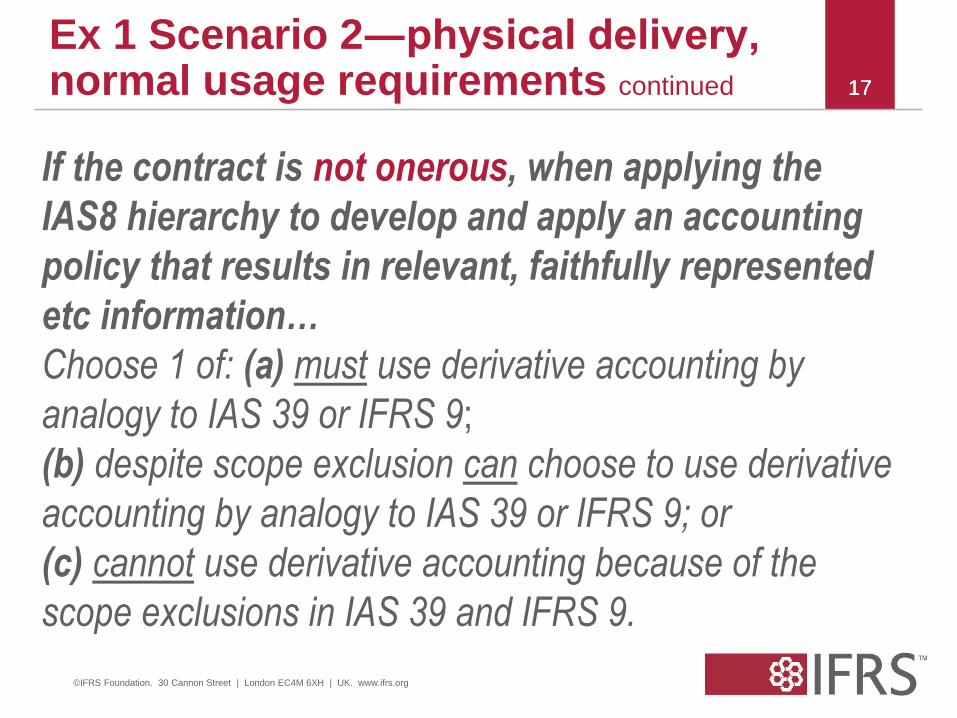

If the contract is not onerous, when applying the

IAS8 hierarchy to develop and apply an accounting

policy that results in relevant, faithfully represented

etc information…

Choose 1 of: (a) must use derivative accounting by

analogy to IAS 39 or IFRS 9;

(b) despite scope exclusion can choose to use derivative

accounting by analogy to IAS 39 or IFRS 9; or

(c) cannot use derivative accounting because of the

scope exclusions in IAS 39 and IFRS 9.

17

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

17

18

Ex 1 Scenario 2―physical delivery, normal usage requirements continued

Consistently with the objective of financial reporting,

whose information needs provide focus when

assessing the relevance of financial information?

Choose 1 of: (a) Chipem’s controlling shareholder, if any;

(b) Obligit; (c) other non-controlling interests in Chipem;

(d) lenders and other creditors of Chipem that can

require Chipem to provide information directly to them; or

(e) those existing and potential investors, lenders and

other creditors that cannot require Chipem to provide

information directly to them.

18

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18

19

Ex 1 Scenario 2―physical delivery, normal usage requirements continued

Which method of accounting for forward contracts

that are not onerous provides the most relevant

information to primary users? Choose 1 of: (a) derivative accounting (as set out in IAS39

and IFRS 9); (b) not to account for the forward contract—

observed common practice; (c) historical cost accounting

for the asset (right to receive chips) and the liability

(present obligation to pay for the chips) that arises from the

contract; (d) same as (c) but present net (ie at nil), see

IAS1.32 re offsetting; (e) same as (c) except fair value

accounting; or (f) other accounting.

19

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19

20

Ex 1 Scenario 3―choice to settled net in cash or physical delivery

Chipem is contracted to buy at A$100 in 2 years

If contracted today, would buy at A$40 in 2 years

Which IFRS specifies accounting?

Choose 1 of: (a) a derivative—IAS 39 or, if adopted

early, IFRS 9; (b) IAS 39 (or IFRS 9) unless entered into

and continues to be held for the purpose of taking

delivery of the pine bark chips in accordance with

Chipem’s expected purchase or usage requirements—in

which case; if onerous, IAS 37; if not onerous, the IAS 8

hierarchy; (c) another IFRS; or (d) no specific IFRS

therefore apply the IAS 8 hierarchy.

20

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

20

21 Ex 1 Scenario 4―cash flow hedge

Chipem is contracted to buy at A$100 in 2 years

If contracted today, would buy at A$40 in 2 years

Which IFRS specifies accounting?

Choose 1 of: (a) IAS 39 or, if adopted early, IFRS 9—a

derivative at fair value through profit or loss; (b) IAS 39

hedge accounting—at fair value through OCI; (c) IAS 39

hedge accounting—at fair value through profit and loss;

(d) (b) if Chipem chooses hedge accounting and satisfies

IAS 39’s requirements; otherwise (a); (e) no specific

IFRS therefore apply the IAS 8 hierarchy; or

(f) another IFRS;

21

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

21

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

22

• 1/1/20X5 a pine tree farmer enters into a contract to sell 1,000 tonnes of sawn pine logs to a wood chip manufacturer in exchange for A$100 per tonne on 31/12/20X9.

• On 31/12/20X5, an identical contract with a 4-year time frame would be priced at A$150 per tonne.

Example 2―forward sale contract

23 Example 2―settled net in cash

Growem is contracted to sell at A$100 in 4 years

If contracted today, would contract to sell at A$150 in 4 years

Which IFRS specifies accounting?

Choose 1 of: (a) a derivative—IAS 39 or, if adopted

early, IFRS 9 Financial Instruments;

(b) IAS 37 Provisions, Contingent Liabilities and

Contingent Assets irrespective of whether the contract is

onerous; (c) IAS 37 because the contract is onerous;

(d) another IFRS; or (e) no specific IFRS therefore apply

the IAS 8 hierarchy.

23

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

23

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

24

• IAS 41 requires growing timber to be measured at fair value less costs to sell without reference to forward sale contract, ie the increased market price is reflected in the fair value of the trees (see IAS 41.16)

• Does being contracted to sell that timber at a lower fixed price (A$100) make that contact onerous on 31/12/20X5? If so,

• at 31/12/X5 measure provision liability using IAS 37 (say A$50,000, ie ‘best estimate’)

• recognise change in provision in 20X5 as expense/income (see IAS 37)

Example 2—some explanation

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

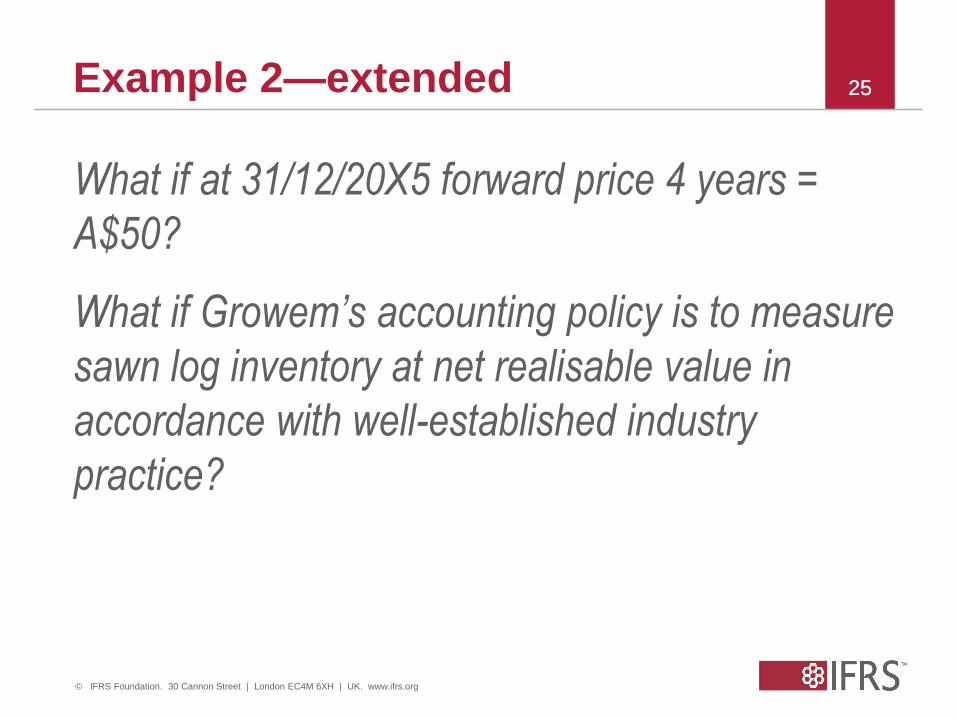

25 25 Example 2—extended

What if at 31/12/20X5 forward price 4 years =

A$50?

What if Growem’s accounting policy is to measure

sawn log inventory at net realisable value in

accordance with well-established industry

practice?

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

26

• Derivative in scope of IFRS 9

• measuring fair value of derivative

• Onerous contract in scope of IAS 37

• determining whether onerous contract

• measuring provision in accordance with IAS 37

• IAS 8 hierarchy

• developing accounting policy that provides relevant information

Forward contracts: judgement and estimates

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter, not necessarily those of the IASB or IFRS Foundation

Flymecheaply (FMC) budget airline

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

28 28 Leases—identifying elements

Using only Conceptual Framework, what elements arise for FMC at commencement of the 10 leases? Choose 1 of: (a) asset: control over resource—unconditional right to use 10 aircraft; and liability: present obligation—unconditional obligation to pay specified lease payments on 10 aircraft; (b) asset: control over resource—in substance purchase of 7 aircraft; and liability: present obligation to pay specified lease payments on 7 aircraft; and no elements for lease of other 3 aircraft (c) no assets and no liabilities for any of the 10 leases; or (d) another …

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

29 29 Lease accounting—IAS 17 Leases

How must FMC account for 7 leases under IFRS? Choose 1 of: (a) finance lease accounting—at commencement of lease recognise asset and liability. Thereafter, depreciate aircraft (IAS 16 PPE) and apportion lease payments between the finance charge (so as to produce a constant periodic rate of interest on the remaining balance of the liability) and the reduction of the outstanding liability; (b) operating lease accounting—recognise lease payments as an expense on a straight-line basis over the 10 year lease term; or (c) another…

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30 30

Lease accounting—IAS 17 Leases continued

How must FMC account for 3 leases under IFRS? Choose 1 of: (a) finance lease accounting—at commencement of lease recognise asset and liability. Thereafter, depreciate aircraft (IAS 16 PPE) and apportion lease payments between the finance charge (so as to produce a constant periodic rate of interest on the remaining balance of the liability) and the reduction of the outstanding liability; (b) operating lease accounting—recognise lease payments as an expense on a straight-line basis over the 14 year and 11 month lease term; or (c) another…

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

31 31

Lease accounting—judgements and proposals

What judgements would FMC have made in

accounting account for the 3 leases?

What disclosures would FMC make about the

judgements it made in classifying the 3 leases?

If the IASB’s current proposals for lease

accounting (Exposure Draft 2013) were to

become an IFRS, what would the accounting for

the 3 leases be at commencement of the lease?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

32 32

Contracts with customers—identifying elements

Using only the Conceptual Framework, what elements arise for FMC entering into contracts with its customers? Choose 1 of: (a) asset: cash received from customer; and liability: present obligation—unconditional obligation to provide ticket holding customer with flight booked; (b) asset: cash; and liabilities: present obligation—unconditional obligation to provide ticket holding customer with flight booked and flight reward upon redeeming loyalty points; (c) asset: cash and income: increase in cash balance; or (d) another …

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

33 33 IAS 18 Revenue

When must FMC account for income from the contracts with its customers under IFRS? Choose 1 of: (a) recognise revenue when the liability is extinguished, ie the earlier of when the customer flies or cancels a ticket; (b) recognise the portion of revenue attributed to the flight booked in accordance with (a) and the portion attributed to the loyalty award when that liability is extinguished, ie the earlier of when the customer flies on a loyalty flight or when the loyalty points expire unused; (c) same as (b) but recognise ticket change fee when the ticket is changed; or (d) another…

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34 34 IAS 18 Revenue continued

How must FMC measure income from the contracts with its customers in accordance with IAS 18? Choose 1 of: (a) the cash received from the customer is allocated between the purchased flight and the loyalty points earned by measuring the customer loyalty portion by reference to the amount required to settle it, in accordance with IAS 37; (b) allocate the cash received between the purchased flight and the loyalty points earned using the fair value of the loyalty award taking account of expected expiry using historic data; or (c) same as (b) but take account of the time value of money in measuring revenue (ie future value income received in advance; or (d) another…

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

35 35 Expected new revenue IFRS

How will FMC measure revenue if it early adopts the new IFRS revenue from contacts with customers? Choose 1 of: (a) the cash received from the customer is allocated between the purchased flight and the loyalty points earned by measuring the customer loyalty portion by reference to the amount required to settle it, in accordance with IAS 37; (b) allocated the cash received between the purchased flight and the loyalty points earned using the fair value of the loyalty award taking account of expected expiry using historic data; or (c) same as (b) but take account of the time value of money in measuring revenue (ie future value income received in advance; or (d) another…

36

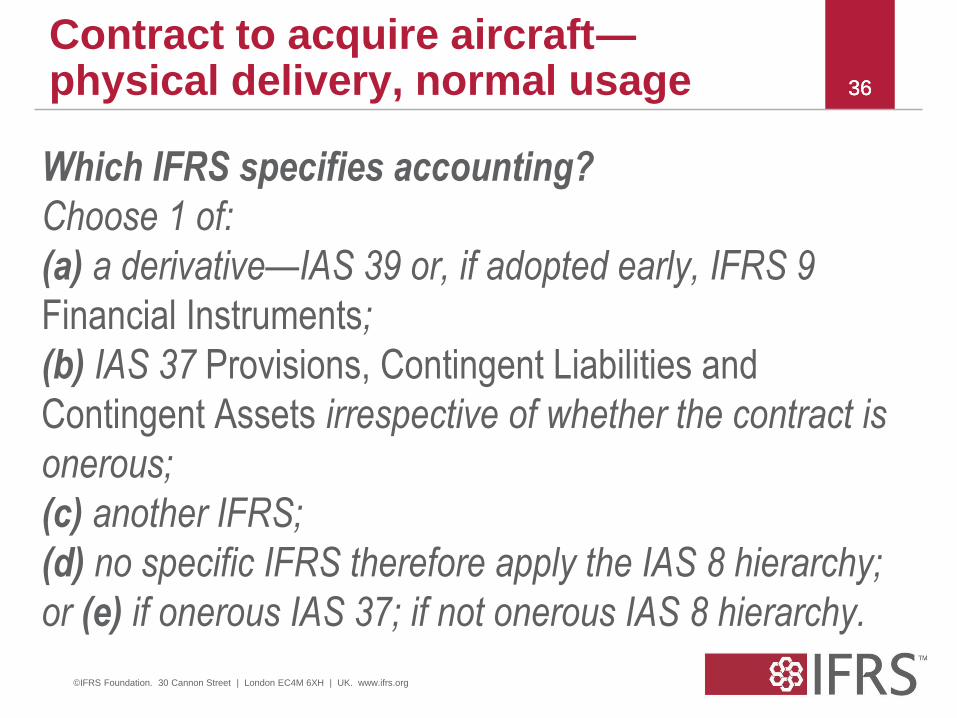

Contract to acquire aircraft― physical delivery, normal usage

Which IFRS specifies accounting?

Choose 1 of:

(a) a derivative—IAS 39 or, if adopted early, IFRS 9

Financial Instruments;

(b) IAS 37 Provisions, Contingent Liabilities and

Contingent Assets irrespective of whether the contract is

onerous;

(c) another IFRS;

(d) no specific IFRS therefore apply the IAS 8 hierarchy;

or (e) if onerous IAS 37; if not onerous IAS 8 hierarchy.

36

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

36

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

37

Significant judgement—is the forward purchase contract onerous?

• Onerous contract = a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

• unavoidable costs = the lower of the cost of fulfilling the contract and any compensation or penalties arising from failure to fulfil it.

Contract to acquire aircraft― physical delivery, normal usage cont.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

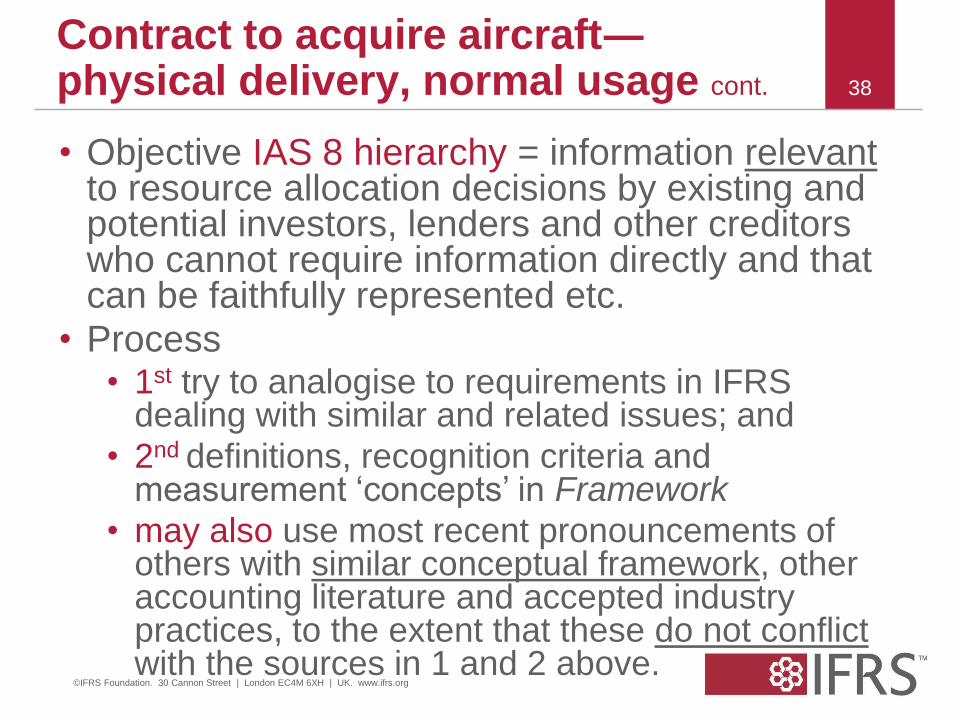

38

• Objective IAS 8 hierarchy = information relevant to resource allocation decisions by existing and potential investors, lenders and other creditors who cannot require information directly and that can be faithfully represented etc.

• Process • 1st try to analogise to requirements in IFRS

dealing with similar and related issues; and

• 2nd definitions, recognition criteria and measurement ‘concepts’ in Framework

• may also use most recent pronouncements of others with similar conceptual framework, other accounting literature and accepted industry practices, to the extent that these do not conflict with the sources in 1 and 2 above.

Contract to acquire aircraft― physical delivery, normal usage cont.

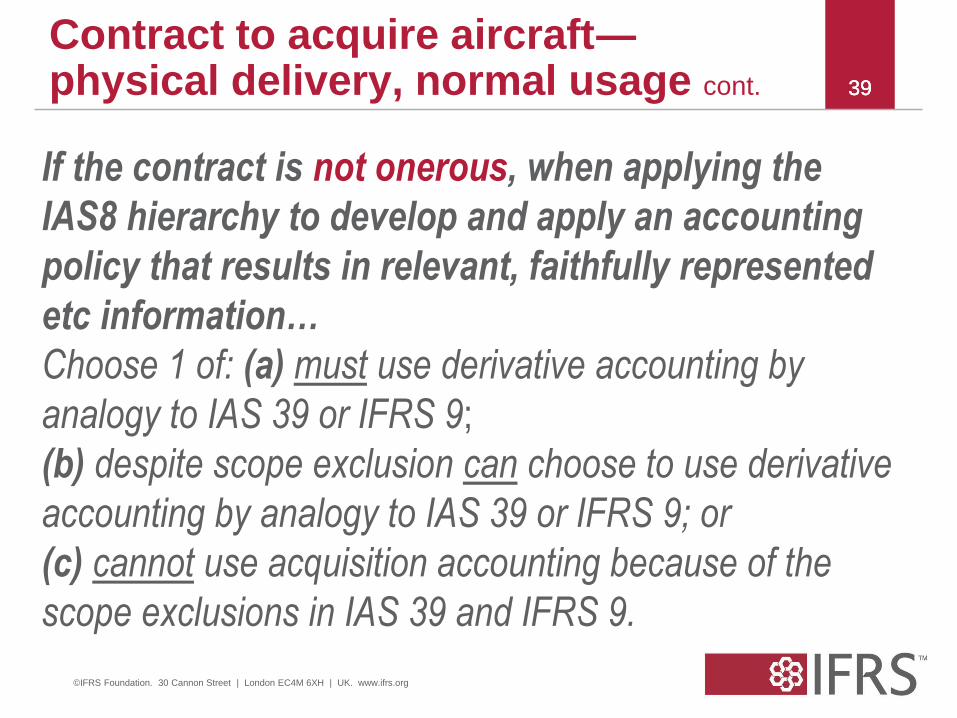

39

Contract to acquire aircraft― physical delivery, normal usage cont.

If the contract is not onerous, when applying the

IAS8 hierarchy to develop and apply an accounting

policy that results in relevant, faithfully represented

etc information…

Choose 1 of: (a) must use derivative accounting by

analogy to IAS 39 or IFRS 9;

(b) despite scope exclusion can choose to use derivative

accounting by analogy to IAS 39 or IFRS 9; or

(c) cannot use acquisition accounting because of the

scope exclusions in IAS 39 and IFRS 9.

39

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

39

40

Contract to acquire aircraft― physical delivery, normal usage cont.

Consistently with the objective of financial reporting,

whose information needs provide focus when

assessing the relevance of financial information?

Choose 1 of: (a) Mr En Trepreneur founding shareholder;

(b) Obligit; (c) other non-controlling interests in FMC;

(d) lenders and other creditors of FMC that can require

FMC to provide information directly to them; or (e) those

existing and potential investors, lenders and other

creditors that cannot require FMC to provide information

directly to them.

40

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

40

41

Contract to acquire aircraft― physical delivery, normal usage cont.

Which method of accounting for forward contracts

that are not onerous provides the most relevant

information to primary users? Choose 1 of: (a) derivative accounting (as set out in IAS39

and IFRS 9); (b) not to account for the forward contract—

observed common practice; (c) historical cost accounting

gross for the asset (right to receive 2 aircraft) and the

liability (present obligation to pay for 2 aircraft) that arises

from the contract but present net (ie at nil); (d) same as (c)

but present gross; (e) same as (d) except fair value

accounting; or (f) other accounting.

41

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

41

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

42 42

Pilot retention scheme—identifying elements

Using only Conceptual Framework, what elements arise for FMC from its pilot retention scheme with regard to Employee A at 31/12/20X1? Choose 1 of: (a) liability: present obligation—unconditional obligation to pay long-service award to A on her 40th birthday (and expense: increase in liability in 20X1); (b) liability: present obligation—unconditional obligation to pay 1% of final salary to A on her 40th birthday (and expense: increase in liability in 20X1);; (c) no element definition satisfied—the obligation is conditional on A remaining employed by FMC for another 4 years; or (d) another …

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

43 43 Pilot retention scheme—IFRS

How must FMC account for the pilot retention

scheme in accordance with IFRS? Choose 1 of:

(a) short-term employee benefit (IAS 19 Employee

Benefits);

(b) other long-term employee benefits (IAS 19);

(c) post employment benefits (IAS 19);

(d) provision (IAS 37 Provisions, Contingent Liabilities

and Contingent Assets); (e) another IFRS;

(f) no specific IFRS therefore apply the IAS 8 hierarchy

© 2012 IFRS Foundation 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

44

Pilot retention scheme—IAS 19

other long-term employee benefit

20X1 20X2 20X3 20X4 20X5

Benefit attributed to: 1,215.5 3,193.8 4,790.7 6,387.7 7,984.6

– prior years – 1,596.9 3,193.8 4,790.8 6,387.7

– current year (1% of final

salary) 1,215.5 1,596.9 1,596.9 1,596.9 1,596.9

Opening obligation

– 664.2 2,159.6 3,563.4 5,226.3

Interest at 10%

– 66.4 216 356.3 522.6

Actuarial loss – 349.2 – – 798.4

Current service cost 664.2 1,079.8 1,187.8 1,306.6 1,437.2

Closing obligation 664.2 2,159.6 3,563.4 5,226.3 7,984.5

44

© 2012 IFRS Foundation 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

45

Pilot retention scheme—IAS 19

other long-term employee benefit cont.

Calculations 20X1:

• Expected final salary: L$100,000 × (1.05)4

= CU121,551.

• Benefit for the current year: 1% ×

L$121,551 expected final salary = L$1,216.

• Adjustment for vesting condition: L$1,216 ×

80% + CU0 × 20% = CU972.

• Present value: L$973 × 1/(1.1)4 = CU973 ×

0.683013 = CU664.

45

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

46 46

Pilot retention scheme—judgements and estimates

• estimate pilots’ salary increases to 40th birthday

• estimate probability that pilots will leave

employment or die in the vesting period and

consequently forego the benefit

• determine the discount rates by reference to

market yields on high quality corporate bonds (or,

in countries where there is no deep market in

such bonds, government bonds) of a currency

and term consistent with the currency and term of

the obligation.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

47 47

Pension scheme—identifying elements

Using only Conceptual Framework, what elements

arise for FMC from its employee pension scheme?

Choose 1 of: (a) liability: present obligation only for

vested pension benefits (and expense: increase in

liability in 20X1); (b) liability: present obligation—

vested and unvested accumulating pension benefits

(and expense: increase in liability in 20X1); (c) no

element definition satisfied until the pension is paid

(payment = expense); or (d) another …

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

48 48 Pension scheme—IFRS

How must FMC account for the pension scheme in accordance with IFRS? Choose 1 of: (a) short-term employee benefit (IAS 19 Employee Benefits); (b) other long-term employee benefits (IAS 19); (c) post-employment benefits (IAS 19); (d) termination benefit (IAS 19); (e) provision (IAS 37 Provisions, Contingent Liabilities and Contingent Assets); (f) another IFRS; (g) no specific IFRS therefore apply the IAS 8 hierarchy

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

49 49

Pension scheme—examples of judgements and estimates

• estimate employees’ pensionable salary

(lower of annual salary at 65th birthday or

when leave FMC’s employment (include

salary increases)

• estimate number of continuous service

periods of 10 years employees will complete

• estimate the probabilities about paying

pensions to employees spouses etc

• determine the discount rates, see pilots above

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

50 50

Emission trading scheme—identifying elements

Using only Conceptual Framework, what elements arise for FMC from exchanging cash for carbon emissions certificates in the market on 31/12/20X6? Choose 1 of: (a) increase asset (carbon certificates held—a resource controlled by FMC) and decrease asset (cash—paid for certificates); no liability because FMC is yet to emit carbon in 20X7; (b) same as (a) but also increase liability—present obligation to deliver the certificates in 3 years and recognise expense (increase in liability); (c) decrease asset and recognise expense for the cash paid for certificates (decrease in asset); or (d) another …

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

51 51

Emission trading scheme—identifying elements

Using only Conceptual Framework, what elements arise for FMC from receiving carbon emissions certificates from the government on 31/12/20X6? Choose 1 of: (a) asset: carbon certificates held—a resource controlled by FMC; and income: increase in assets (there is no liability before FMC emits carbon in 20X7); (b) asset: carbon certificates held—a resource controlled by FMC; and liability—present obligation to return the certificates in 3 years; (c) no element definition satisfied—only incur a liability when FMC emits carbon in excess of the certificates held; or (d) another …

52 Emission trading scheme—IFRS

Which IFRS specifies accounting for emissions

trading schemes?

Choose 1 of: (a) certificates—IAS 39 or, if adopted early,

IFRS 9 Financial Instruments; obligation to return

certificates—IAS 37 Provisions, Contingent Liabilities and

Contingent Assets; (b) certificates—IAS 38 Intangible

Assets; obligation to return certificates—IAS 37; (c) (b)

for purchased certificates and IAS 20 Government

Grants for certificates direct from govt; (d) another IFRS;

or (e) no specific IFRS for emission trading schemes

therefore apply the IAS 8 hierarchy.

52

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

52

Thank You

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

53