case studies in transfer pricing - ctconline.org · principal structure . bundled tech & brand...

TRANSCRIPT

Chamber of Tax Consultants 4th International Tax Conference Case studies in Transfer Pricing December, 2012 Mumbai

www.pwc.com

PwC PwC

Agenda

1 Business Models & Transfer Pricing nuances for manufacturing

2 Business Models & Transfer Pricing nuances for selling & distribution

Chamber of Tax Consultants - International Tax Conference 2

PwC PwC

Business Models & Transfer Pricing nuances for manufacturing

Chamber of Tax Consultants - International Tax Conference 3

PwC PwC

Manufacturing models & profitability

Toll Manufacturer

Contract Manufacturer

Licensed Manufacturer

Full Fledged Manufacturer

Incr

easi

ng p

rofit

pot

entia

l

Increasing functions, risks & intangibles

Does not exploit IP on own account; service provider

Exploits IP on own account; entrepreneur

Chamber of Tax Consultants - International Tax Conference 4

PwC PwC

Manufacturing Models – FAR comparisons Functions, Assets &

Risks (FAR) Full fledged

Manufacturer Licensed Manufacturer Contract Manufacturer Toll Manufacturer

Manufactures On own behalf On own behalf For Principal For Principal

R&D Carries itself/ CSA Rarely carries out R&D No No

A&M Does itself Does itself No No

Distribution Does itself Does itself No No

Procurement Does itself Does itself Generally does itself* No

Production scheduling Does itself Does itself No No

IP Owner Licensee ; exploitation rights; pays royalty

Licensee; no exploitation rights

Licensee; no exploitation rights

Inventory Owner Owner Owner* Does not own

Market & price risk Bears Bears Does not bear Does not bear

Technology risk Bears Partially bears Does not bear Does not bear

Inventory risk Bears Bears Does not bear Does not bear

Capacity risk Bears Bears Does not bear; unless not captive Does not bear

Product/ Service risk Bears (Product) Bears (Product) Bears (Service) Bears (Service)

FAR: Functions; Assets; Risks Chamber of Tax Consultants - International Tax Conference 5

PwC PwC

Indian customers – conventional model

Plain vanilla license manufacturer

INDIA

Tech & Brand Royalty

Principal Co

Flow of legal title of goods Physical movement of goods

India Sub Co (License Mfg)

Mfg division

Sales division

Supplier Indian customer

• Commercial issues – - Insufficient repatriation of entrepreneurial profits through

routine royalty ? Cap on royalty recently withdrawn - How to achieve portability of profits, from economic & tax

perspective ? • TP Assessment issues –

- Tendency to treat India Sub Co as “tested party” - Entrepreneurial results tested against entrepreneurial

comparables third party turnover exposed to TP

Entrepreneurial results trapped in India

Chamber of Tax Consultants - International Tax Conference 6

PwC PwC

Indian customers – conventional licensed manufacturer model

• India Sub Co's turnover for manufacturing segment Rs 10000 crore

• Components imported from global AEs Rs 2000 crore [supplied at say "cost plus" margin (low/ moderate) by foreign AE suppliers] constitutes 30% of total material cost of India Sub Co

• Royalty paid by India Sub Co to Principal Sub Co @ 3% of turnover Rs 300 crore

• India Sub Co has return on sales (ROS) of 2%

• Under overall TNMM, average ROS of comparables is 6% TP adjustment works out to 4% of total turnover of India Sub Co Rs 400 crore

• Proper method test import of components under cost plus/ TNMM from foreign side; royalties under CUP from royalty databases

• Proportionate adjustments not ideal solution

Chamber of Tax Consultants - International Tax Conference 7

PwC PwC

Indian customers – major import of materials from foreign principal

INDIA

Principal Co

Flow of legal title of goods Physical movement of goods

Import of materials

Entrepreneurial profits embedded

in import price

India Sub Co (Value added Distributor)

Assembly division Say 15% of VAE [or 6% ROCE]

Sales division Say ROS 3 to 4%

VAE = value added expenses ROCE = return on capital employed

Indian customer

Chamber of Tax Consultants - International Tax Conference 8

PwC PwC

Indian customers – major localisation Indian entrepreneurial model

• Significant localisation in India; also, “significant peoples functions” for manufacturing performed in India

• Difficult to segregate manufacturing & distribution functions • India Sub Co entrepreneur, albeit licensed manufacturer • Not proper to benchmark combined results of India Sub Co against

Indian entrepreneurs • If significant intangibles not embedded in imported components,

price to be tested in hands of Principal Co on cost plus/ TNMM • If significant intangibles embedded in imported components, price

may be tested with residual profit split analysis • Royalty needs to be justified on stand alone basis, as per CUP

analysis from global royalty databases, e.g. RoyaltyStat

INDIA

Tech & Brand Royalty

Principal Co

Flow of legal title of goods Physical movement of goods

India Sub Co (License Mfg)

Mfg division

Sales division

Supplier Indian customer

Chamber of Tax Consultants - International Tax Conference 9

PwC PwC

Indian customers – major localisation non integrated principal structure

Bundled Tech & Brand Royalty and fees for other non-routine,

value added services (Residual Profits)

Capable of assuming major risks & performing major significant people functions ?

Capable of assuming minor risks & performing less significant people functions ?

INDIA

Principal Co

Flow of legal title of goods Physical movement of goods

India Sub Co (License Mfg)

Mfg division Say FCMU 5 to 6%

Sales division Say ROS 3 to 4%

Supplier Indian customer

• Liability on account of technology Principal Co • Principal Co advises on material sourcing, production scheduling • Manufacturing division limited risk manufacturer • If possible, Principal Co advises on marketing strategy,

reimburses A&M costs Sales division’s limited profile • Residual profits repatriated as “bundled royalties”/ industrial

franchise fees same economic result of principal structure • Robust drafting of license agreement necessary

Chamber of Tax Consultants - International Tax Conference 10

PwC PwC

Export of products – inbound (Foreign) MNCs

INDIA

F Co

I Co

Indian customer

Products License

of IP

• Business Model : - I Co operates as contract manufacturer for F Co for exports - For exports, I Co receives “Cost Plus” or “ROCE” - I Co operates as licensed manufacturer for domestic market

• Issues : - Revenue compares export & domestic prices/ profits of products - Makes adjustment for export segment - FAR analysis key solution two markets not comparable - FAR for domestic market entrepreneur (higher functions & risks) - FAR for export market service provider (lower functions & risks)

Products

Chamber of Tax Consultants - International Tax Conference 11

PwC PwC

Export of products – outbound (Indian) MNCs

INDIA

F Co

I Co

Indian customer

Products

• Business Model : - I Co is principal or entrepreneur, owning IP - Sells products to F Co (subsidiary) for distribution - F Co receives arm’s length distribution margin - I Co could incur loss for export for market penetration

• Issues : - Revenue tests I Co’s export margins - Compares export & domestic prices/ profits or with Indian comparables - Makes adjustment for export segment - FAR analysis only solution - I Co is entrepreneur, carrying IP, bearing risks can never be tested - F Co (distributor) as tested party - F Co’s margin to be compared with foreign regional distributors

Products

License of brand

Chamber of Tax Consultants - International Tax Conference 12

PwC PwC

Business Models & Transfer Pricing nuances for selling & distribution

Chamber of Tax Consultants - International Tax Conference 13

PwC PwC

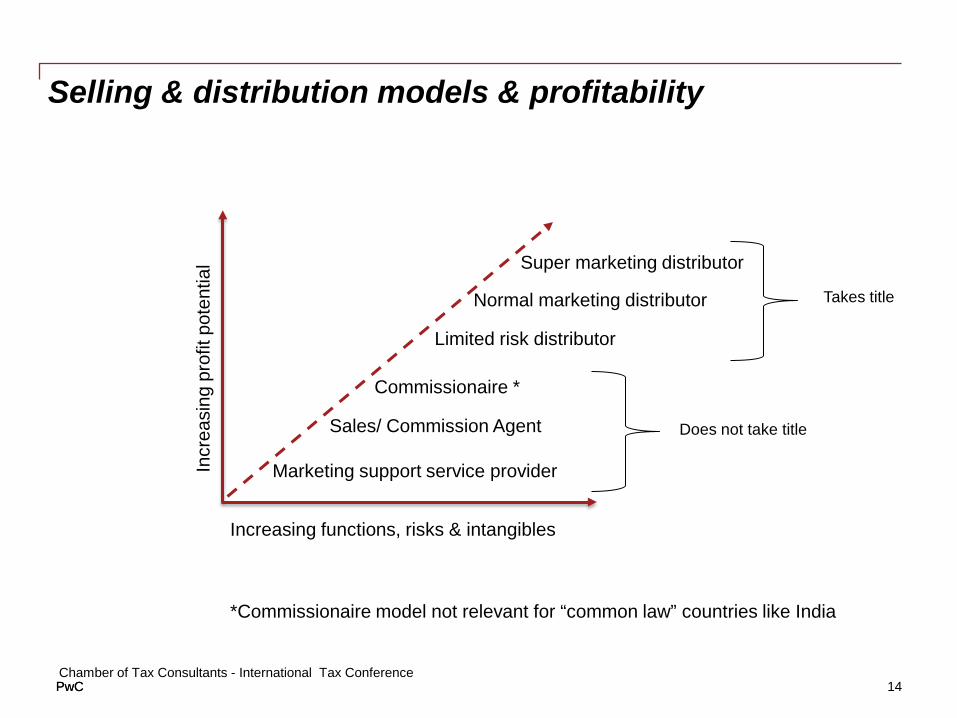

Selling & distribution models & profitability

Marketing support service provider

Sales/ Commission Agent

Commissionaire *

Limited risk distributor

Normal marketing distributor

Super marketing distributor

Does not take title

Takes title

Increasing functions, risks & intangibles

Incr

easi

ng p

rofit

pot

entia

l

*Commissionaire model not relevant for “common law” countries like India

Chamber of Tax Consultants - International Tax Conference 14

PwC PwC

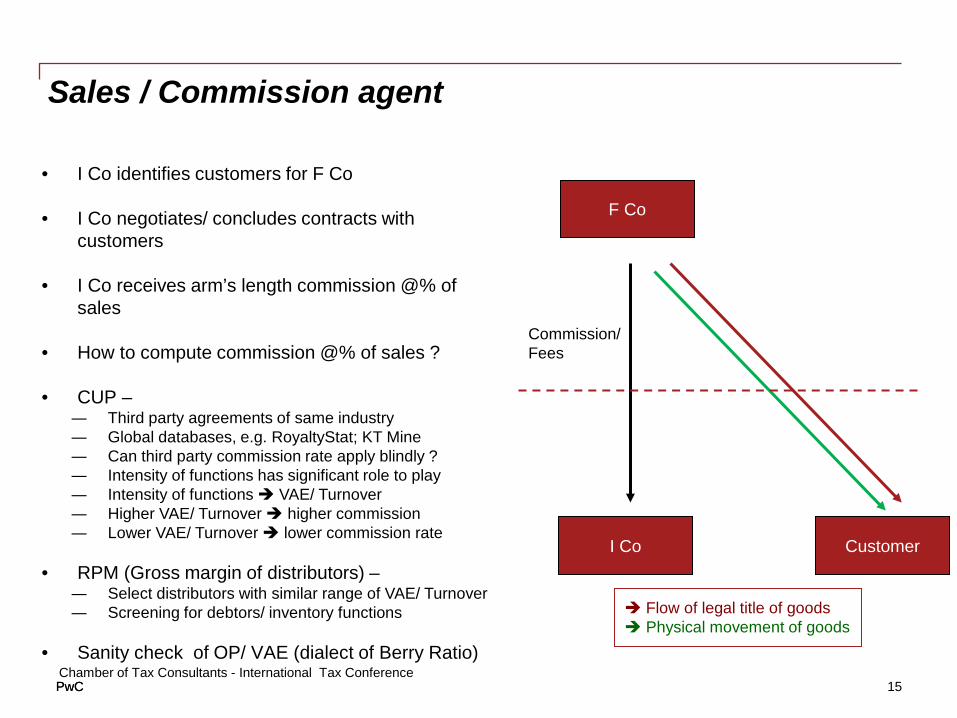

Sales / Commission agent

• I Co identifies customers for F Co

• I Co negotiates/ concludes contracts with customers

• I Co receives arm’s length commission @% of sales

• How to compute commission @% of sales ?

• CUP – ― Third party agreements of same industry ― Global databases, e.g. RoyaltyStat; KT Mine ― Can third party commission rate apply blindly ? ― Intensity of functions has significant role to play ― Intensity of functions VAE/ Turnover ― Higher VAE/ Turnover higher commission ― Lower VAE/ Turnover lower commission rate

• RPM (Gross margin of distributors) –

― Select distributors with similar range of VAE/ Turnover ― Screening for debtors/ inventory functions

• Sanity check of OP/ VAE (dialect of Berry Ratio)

F Co

I Co Customer

Commission/ Fees

Flow of legal title of goods Physical movement of goods

Chamber of Tax Consultants - International Tax Conference 15

PwC PwC

Sales / Commission agent – sanity check • I Co’s (agent) operating costs [VAE] in India Rs 50 crore

• Sales made directly by F Co to Indian customers Rs 25000 crore

• Intensity of functions [VAE/ Sales] 0.2%

• Random third party agent’s commission rate in industry 5%

• Accounts of third party agents not available no information of intensity of functions

• Market intelligence third party agents are small players, dealing in unorganised market

• F Co’s products sell predominantly on strength of IP [technology, brand, etc]

• Thirds party agents deal in unbranded products; more efforts to sell; nurture relationship, etc

• Bargaining power of I Co, vis-à-vis F Co, far less as compared to local small player agents, vis-à-vis their

principals

• Applying 5% rate Rs 1250 crore commission of I Co OP of Rs 1200 crore [1250 – 50]

• OP/ VAE of 2400% [1200/ 50 x 100] absurd result; cannot be applied

• Indian databases OP/ VAE of commission agents appx 30 to 40% (no information of commission rate)

Chamber of Tax Consultants - International Tax Conference 16

PwC PwC

Sales / Commission agent – sanity check …. contd

• Distributors with commensurate FAR profile selected Gross Margin of 1.5%; VAE/ Sales of 1%

• Applying commission rate of 1.5% on I Co Commission of Rs 375 crore; OP of Rs 325 crore

• OP/ VAE of 650% [325/ 50 x 100] exorbitant; comparable OP/ VAE 30 to 40%

• Mathematical fallacy I Co’s intensity of functions is 0.2%; while comparable distributors’ is 1%

• I Co’s intensity of functions [OP/ VAE] is 1/5th of comparable distributors

• Adjust comparable distributors’ gross margin 1/5th of 1.5% 0.3% [arm’s length commission for I Co]

• Applying commission rate of 0.3% to I Co Commission of Rs 75 crore OP of Rs 25 crore [75 – 50]

• OP/ VAE 50% [25/ 50 x 100], as against comparable commission agents’ OP/ VAE of 30 to 40%

• Still high, however best case scenario

• Else, apply commission rate w.r.t 30 to 40% of operating profits 0.08% [40% of 50/ 25000 x 100]

Chamber of Tax Consultants - International Tax Conference 17

PwC PwC

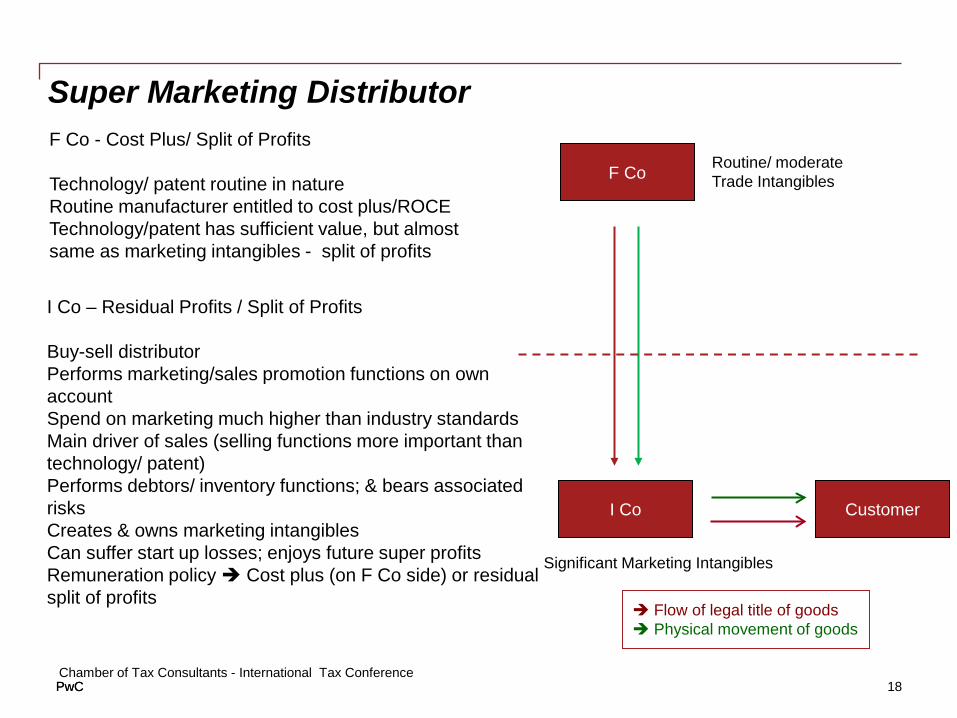

Super Marketing Distributor

I Co – Residual Profits / Split of Profits Buy-sell distributor Performs marketing/sales promotion functions on own account Spend on marketing much higher than industry standards Main driver of sales (selling functions more important than technology/ patent) Performs debtors/ inventory functions; & bears associated risks Creates & owns marketing intangibles Can suffer start up losses; enjoys future super profits Remuneration policy Cost plus (on F Co side) or residual split of profits

F Co - Cost Plus/ Split of Profits Technology/ patent routine in nature Routine manufacturer entitled to cost plus/ROCE Technology/patent has sufficient value, but almost same as marketing intangibles - split of profits

F Co

I Co Customer

Flow of legal title of goods Physical movement of goods

Routine/ moderate Trade Intangibles

Significant Marketing Intangibles

Chamber of Tax Consultants - International Tax Conference 18

PwC PwC

Marketing Intangible – General Concept

• India Sub Co has license of brand & distribution rights from Principal Co • A&M; distribution network key business drivers • Who should incur A&M, distribution expenses ? “Bright line concept” • No straight-jacket formula fact driven depends on profile of India Sub Co • Who performs significant peoples functions, key decisions on A&M ? • Revenue cannot dictate business model substance is the key

INDIA

Principal Co

Flow of legal title of goods Physical movement of goods

Indian customer India Sub Co

Distributor

Marketing intangibles trademark (brand, logo), trade name, distribution network, customer lists etc.

Chamber of Tax Consultants - International Tax Conference 19

PwC PwC

Marketing Intangible – General Concept … contd • Limited risk distributor –

― Guaranteed ROS A&M expenses borne by Principal through reimbursement or pricing ― Economic ownership of marketing intangibles vests with Principal

• Normal risk taking distributors –

― Gross Margin based return ― Intensity of functions [VAE/ Sales] key test for selecting comparables ― Comparables with commensurate VAE/ Sales, likely to have same degree of A&M spend ― No issues on account of marketing intangibles/ bright line

• Super distributors –

― If VAE/ Sales [also A&M/ Sales] of comparables < that of taxpayer distributor, then what ? ― Say, Taxpayer’s GP/ Sales is 40%; and A&M/ Sales is 10% ― Say, comparables’ GP/ Sales is 25%; and A&M / Sales is 5% ― Revenue Taxpayer to receive reimbursement from principal for excess 5% of A&M spend ― One option taxpayer outside realm of comparability apply residual profit split ― Other option if Revenue, accepts same comparables for testing pricing of products under

RPM, then logical conclusion excess 5% A&M spend compensated by excess 15% GP

Chamber of Tax Consultants - International Tax Conference 20

PwC PwC

Normal distributor – Case Study • I Co’s gross margin 45% on sales

• I Co’s VAE/ Turnover 25%

• Gross margin of comparable companies selected in TP Study 20% on sales

• VAE/Turnover of comparable companies 7% on sales

• Revenue accepts comparables in TP Study; applies “bright line” test by comparing A&M/Turnover (10%) of I Co with A&M/ Turnover (2%) of comparables

• Intensity of functions of comparable companies critical for benchmarking

• Fresh analysis conducted by applying VAE/Turnover filter (say 15 to 30%)

- Average Gross margin 40% on sales

- Average VAE/Turnover 23% on sales

- Average A&M/Turnover 9.5% on sales

• No TP adjustment

Chamber of Tax Consultants - International Tax Conference 21

PwC PwC

Marketing Intangible – Licensed Manufacturer

• India Sub Co operates as licensed manufacturer • Raw materials sourced from third parties; minimal from Principal Co • Principal Co supplies raw materials at nominal cost plus • Nil/ routine royalty for mere license of tech/ brand • India Sub Co takes all key decisions on A&M/ distribution, etc • India Sub Co bears all A&M/ distribution expenses (on own account) • Revenue Principal Co to pick-up “extra” A&M/ distribution expenses • I Co (entrepreneur) cannot be compared non-issue • Taxpayers to take first corrective steps not “test” India Sub Co

INDIA Tech & Brand Royalty

Principal Co

Flow of legal title of goods Physical movement of goods

Supplier

Indian customer India Sub Co

Distributor

Chamber of Tax Consultants - International Tax Conference 22

PwC PwC

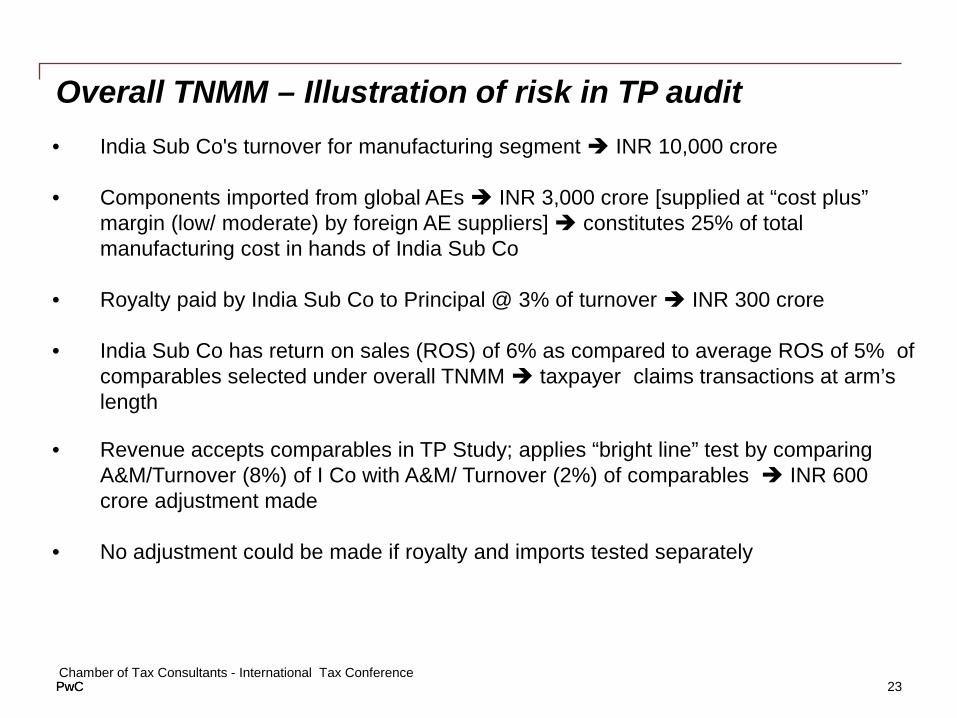

Overall TNMM – Illustration of risk in TP audit • India Sub Co's turnover for manufacturing segment INR 10,000 crore • Components imported from global AEs INR 3,000 crore [supplied at “cost plus”

margin (low/ moderate) by foreign AE suppliers] constitutes 25% of total manufacturing cost in hands of India Sub Co

• Royalty paid by India Sub Co to Principal @ 3% of turnover INR 300 crore • India Sub Co has return on sales (ROS) of 6% as compared to average ROS of 5% of

comparables selected under overall TNMM taxpayer claims transactions at arm’s length

• Revenue accepts comparables in TP Study; applies “bright line” test by comparing A&M/Turnover (8%) of I Co with A&M/ Turnover (2%) of comparables INR 600 crore adjustment made

• No adjustment could be made if royalty and imports tested separately

Chamber of Tax Consultants - International Tax Conference 23

PwC PwC

• Evaluate contribution (& related benefits) of each entity in developing marketing intangibles do efforts/ costs lead to :

- increase in value of IP owned by Principal Co; or - merely enhancing value of rights/benefits of India Sub Co [sole distributor/ seller ]

• Who undertakes key decision making activities – development of marketing strategy, authority to take decisions etc ?

• Significance of local marketing in taxpayer’s industry • Commercial expediency of marketing efforts & costs in relation to benefits/returns • Is business substance properly captured in the contracts ?

- Legal vs. economic ownership - Safeguards on license agreement long term duration of agreement;

compensation on termination of license agreement, to be highlighted

• Corroborative analysis may be undertaken to compute subsidy, if any, given to Indian licensee by foreign licensor

• Robust upfront documentation (including legal contract) covering FAR analysis & economic/ commercial realities utmost necessity

Marketing Intangibles – Key considerations

Chamber of Tax Consultants - International Tax Conference 24

PwC PwC

• Reward for additional marketing efforts of distributor can come by any of the following three options

- Enhanced gross margin - Application of profit split - Reimbursement of A&M expenses

• Position well supported by OECD discussion draft on intangibles (Example 5),

ATO Ruling (Example 3)

Marketing Intangibles – Key considerations

Chamber of Tax Consultants - International Tax Conference 25

PwC PwC

Thank You

© 2012 [PricewaterhouseCoopers Private Limited]. All rights reserved. In this document, “PwC” refers to [PricewaterhouseCoopers Private Limited] which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

26