case 4 hindalco’s acquisition of novelis.pdf

TRANSCRIPT

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 1/20

Hindalco’s Acquisition of Novelis

The case discusses the acquisition of US-Canadian aluminum

company Novelis by India-based Hindalco Industries Limited(Hindalco), a part of Aditya Vikram Birla Group ofCompanies, in May 2007. The case explains the acquisitiondeal in detail and highlights the benefits of the deal for boththe companies.

It also examines the valuation of the acquisition deal and howthe deal was financed. The case concludes by describing thechallenges that Hindalco would face in integrating the

operations of Novelis and analyzing if the deal wasovervalued as opined by some industry experts.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 2/20

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 3/20

361

Hindalco’s Acquisition of Novelis

“The acquisition will catapult the group into the Fortune 500 league, three years

ahead of the target. The combination of Hindalco and Novelis will establish a global

integrated aluminium producer.”1

- Kumar Mangalam Birla, Chairman of Hindalco, in February 2007.

“The combination of Novelis’s world -class rolling assets with Hindalco’s growing

primary aluminum operations and its downstream fabricating assets in the rapidly

growing Asian market is an exciting prospect.”2

- Ed Blechschmidt, Acting Chief Executive of Novelis, in February 2007.

Introduction

On May 16, 2007, India-based Hindalco Industries Limited (Hindalco), a subsidiary

of the AV (Aditya Vikram) Birla Group of Companies (Aditya Birla Group), acquired

the US-Canadian aluminum giant Novelis Inc. (Novelis). The acquisition was the

result of an agreement arrived at between Hindalco and Novelis on February 10, 2007.

Hindalco was to buy Novelis for US$ 6 billion in cash, making it the second biggest

acquisition3 by an Indian company till then. Novelis was to operate as a subsidiary of

Hindalco, and was to have Kumar Mangalam Birla (Kumar Mangalam) as Chairman

who was also the Chairman of Hindalco and the Aditya Birla Group. Martha Finn

Brooks would continue as Chief Operating Officer and was also appointed as the

President of the merged entity.

Hindalco was among the leading companies in the aluminum and copper industry in

the world. (Refer to Exhibit I for leading aluminum companies in the world based

on EBITDA figures). In the financial year 2006-07, Hindalco generated revenues of

US$ 14 billion and the company had a market capitalization of more than US$ 4.5

billion. It had a significant market share in all the segments in which it operated and

enjoyed a domestic market share of 42 percent in primary aluminum, 63 percent in

rolled products, 20 percent in extrusions, 44 percent in foils, and 31 percent in

wheels (Refer to Exhibit II for Hindalco‟s revenues and net income for the year

2006 and 2005).

1 Surojit Chatterjee, “Birla‟s Hindalco Buys Aluminum Giant Novelis for $6.4 billion,”

http://in.ibtimes.com, February 13, 2007.2 Heather Timmons, “Indian Metals Company to Buy Canadian Rival,” www.iht.com,

February 11, 2007.3 The biggest was Tata Steel‟s acquisition of Corus, an „all cash‟ deal which was valued at

US$ 12.1 billion.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 4/20

Mergers & Acquisitions, and Strategic Alliances

362

Exhibit I: Leading Aluminum Companies in the World

(Based on the EBITDA percent)

50

39 3934

14 16

0

10

20

30

40

50

60

H i n

d a l c o

R i o

T i n t o

V e n d a

n t a

B H P

A l c o a

A l c a n

Source: www.hindalco.com.

Exhibit IIA: Income Statement of Hindalco

(In Rs. Millions)

As on 31st March 2007 2006 2005 2004 2003

Net sales and operating

revenues

183,130 113,965 95,235 61,908 49,755

Other Income 3,701 2,439 2,700 2,400 2,330

Profit before Tax 35,046 21,057 19,042 12,457 8,994

Tax 9,841 3,341 5,707 2,606 2,520

Profit After Tax 25,643 16,555 13,233 8,389 5,821

Source: www.hindalco.com.

Exhibit IIB: Balance Sheet of Hindalco

(In Rs. Millions)

As on 31st March 2006 2005

Assets

Gross Block 103,323.21 87,119.09

Net Block 67,435.15 55,808.73

Capital WIP 8,329.17 13,229.81

Investments 11,342.20 10,477.55

Inventory 40,950.88 23,745.18

Receivables 12,484.01 23,745.18

Other Current Assets 48,086.70 39,689.30

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 5/20

Hindalco’s Acquisition of Novelis

363

As on 31st March 2006 2005

Balance Sheet Total 188,628.11 150,824.24

Liabilities

Equity Share Capital 985.66 927.77

Reserves 94,624.01 75,417.59

Total Debt 49,034.38 37,999.97

Creditors and Acceptances 19,745.30 14,573.87

Other current liab/prov 24,238.76 21,905.04

Balance Sheet Total 188,628.11 150,824.24

Source: www.myiris.com.

Novelis had a three million ton capacity for manufacturing value added aluminum

rolled products4 and was a leading producer of aluminum sheet and light gauge (thin)

rolled products for the construction and industrial markets. The company operated in

11 countries and supplied high quality aluminum sheet and foil products to various

industries including automotive, transportation, packaging, construction, industrial

products, and printing. Novelis‟customers included companies like Coca-Cola,

Kodak, Ford, General Motors, and other leading Fortune 500 companies. Novelis sold

rolled aluminum products in Asia, Europe, North America, and South America (Refer

to Exhibit III for performance of Novelis in different regions).

Exhibit III: Performance of Novelis in Different Regions

(All US$ Millions)

N.America Europe Asia S.America

Assets 1,487 2,392 1,021 814

Net sales 2,841 2,688 1,235 626

Regional

Income

64 208 70 122

Description

of Assets

10 Plants*,

2 Recycling

Facilities.

14 Plants,

1 Recycling

Facility

3 Plants 2 Plants,

2 Smelters,

1 Refinery,

2 BauxiteMine

* Plants refer to aluminum rolled product facilities.

Source: www.novelis.com.

Industry analysts opined that the acquisition would benefit Hindalco by strengthening

the company‟s global presence, as Novelis had flat rolled aluminum manufacturing

plants in different locations in the world. They considered the deal a good platform for

4 Aluminum rolled products are semi-finished aluminum products that constitute the rawmaterial for manufacturing finished goods ranging from automotive bodies to householdfoils.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 6/20

Mergers & Acquisitions, and Strategic Alliances

364

Hindalco to access global customers. Novelis had a 19 percent global market share in

foil products, 25 percent in construction and industrial products, and 43 percent in

beverage cans. After the acquisition, the merged entity would emerge as the world‟s

largest aluminum rolling company and among the world‟s top five aluminum

manufacturers. According to Shivanshu Mehta, Assistant Vice-President, NCDEX,

“The deal will catapult Hindalco‟s flat rolled product capacity from 0.2 million ton to

3.2 million ton per annum and elevate the company to a leadership position in the

business.”5

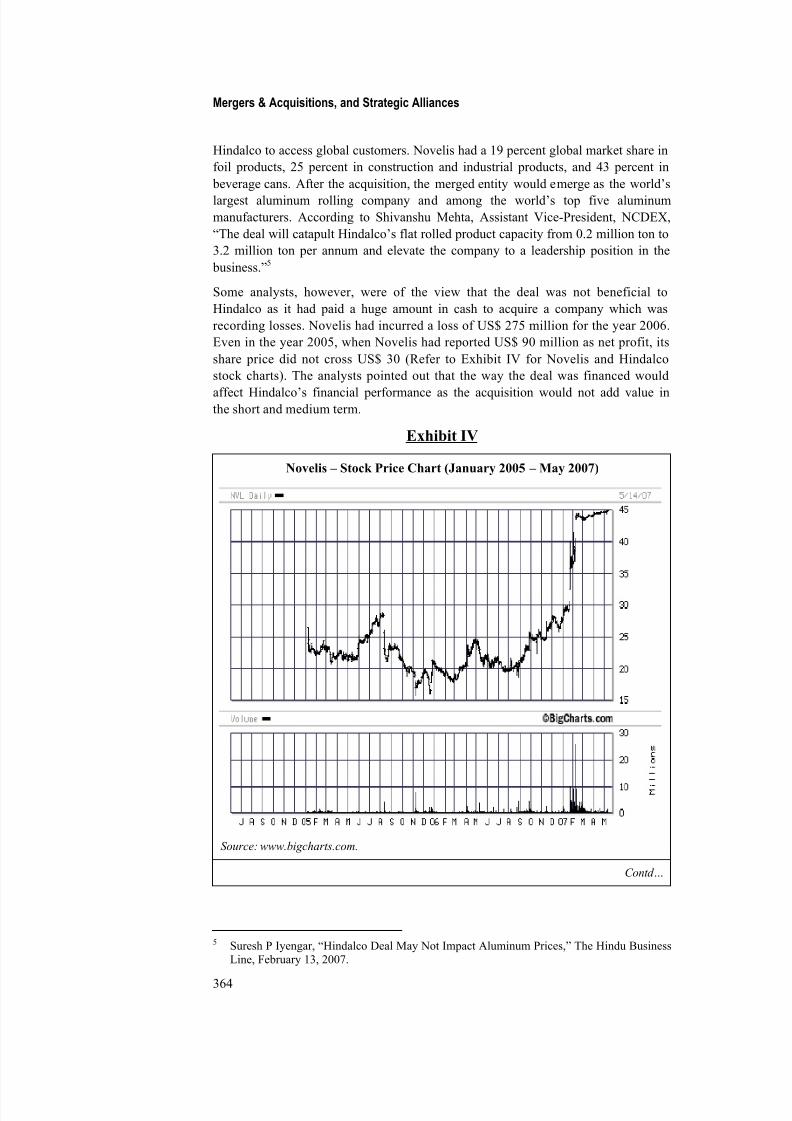

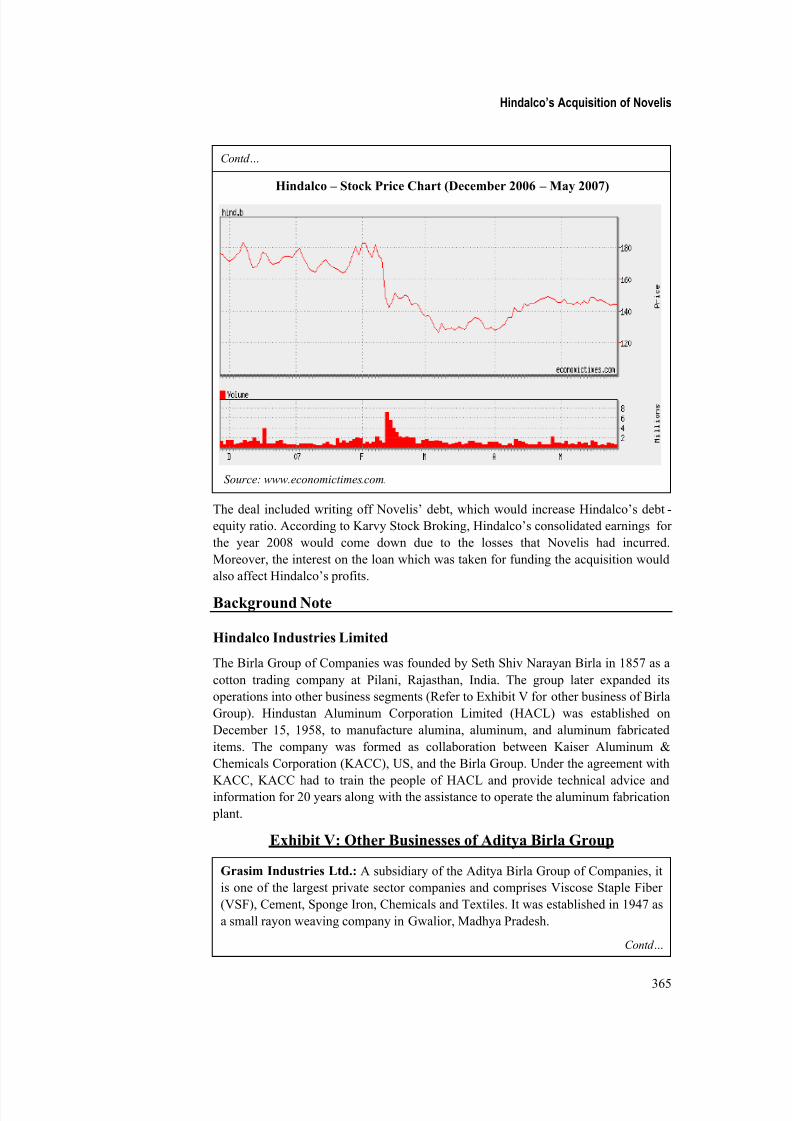

Some analysts, however, were of the view that the deal was not beneficial to

Hindalco as it had paid a huge amount in cash to acquire a company which was

recording losses. Novelis had incurred a loss of US$ 275 million for the year 2006.

Even in the year 2005, when Novelis had reported US$ 90 million as net profit, its

share price did not cross US$ 30 (Refer to Exhibit IV for Novelis and Hindalco

stock charts). The analysts pointed out that the way the deal was financed would

affect Hindalco‟s financial performance as the acquisition would not add value inthe short and medium term.

Exhibit IV

Novelis – Stock Price Chart (January 2005 – May 2007)

Source: www.bigcharts.com.

Contd…

5 Suresh P Iyengar, “Hindalco Deal May Not Impact Aluminum Prices,” The Hindu BusinessLine, February 13, 2007.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 7/20

Hindalco’s Acquisition of Novelis

365

Contd…

Hindalco – Stock Price Chart (December 2006 – May 2007)

Source: www.economictimes.com.

The deal included writing off Novelis‟ debt, which would increase Hindalco‟s debt -

equity ratio. According to Karvy Stock Broking, Hindalco‟s consolidated earnings for

the year 2008 would come down due to the losses that Novelis had incurred.

Moreover, the interest on the loan which was taken for funding the acquisition would

also affect Hindalco‟s profits.

Background Note

Hindalco Industries Limited

The Birla Group of Companies was founded by Seth Shiv Narayan Birla in 1857 as a

cotton trading company at Pilani, Rajasthan, India. The group later expanded its

operations into other business segments (Refer to Exhibit V for other business of Birla

Group). Hindustan Aluminum Corporation Limited (HACL) was established on

December 15, 1958, to manufacture alumina, aluminum, and aluminum fabricated

items. The company was formed as collaboration between Kaiser Aluminum &

Chemicals Corporation (KACC), US, and the Birla Group. Under the agreement with

KACC, KACC had to train the people of HACL and provide technical advice andinformation for 20 years along with the assistance to operate the aluminum fabrication

plant.

Exhibit V: Other Businesses of Aditya Birla Group

Grasim Industries Ltd.: A subsidiary of the Aditya Birla Group of Companies, it

is one of the largest private sector companies and comprises Viscose Staple Fiber

(VSF), Cement, Sponge Iron, Chemicals and Textiles. It was established in 1947 as

a small rayon weaving company in Gwalior, Madhya Pradesh.

Contd…

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 8/20

Mergers & Acquisitions, and Strategic Alliances

366

Contd…

Aditya Birla Nuvo: Formerly known as Indian Rayon & Industries Ltd., it is a

diversified conglomerate of the Aditya Birla Group. Its business segments includeViscose Filament Yarn (VFY), carbon black, branded garments, fertilizers, textiles,

and insulators. Aditya Birla Nuvo through its subsidiaries and joint ventures

provides services such as Life insurance, Telecom, Business Process Outsourcing

(BPO), IT services, Asset Management, and other financial services.

Ultra Tech: UltraTech Cement Limited is a Grasim subsidiary that manufactures

and markets Ordinary Portland Cement, Portland Blast Furnace Slag Cement, and

Portland Pozzolana Cement. It is the country‟s largest exporter of cement and

clinker. It exports to countries around the Indian Ocean, Africa, Europe, and The

Middle East. The Narmada Cement Company is a subsidiary of the company.

Source: www.birlagroup.com.

As a result, the HACL was set up as an integrated complex with a capacity of 20,000

MTPA (million ton per annum). It started producing aluminum metals in 1962 in

Renukoot in eastern Uttar Pradesh. Renukoot had a fully integrated plant, comprising

three main plants i.e. the Alumina, Smelter, and Fabrication Plants.

In 1965, HACL installed an extrusion press and rolling mill for the production of

aluminum sheets and rolled products with a capacity of 2,000 ton and 7,000 ton

respectively, thereby increasing the total capacity of the fabrication plant to 15,000

ton per annum. The company could produce 60,000 ton of primary metal. After

several modifications to the plant in the year 1968, the company‟s production capacity

was enhanced to 200 ton per day.

In 1967, HACL established its own power plant in Renusagar, in collaboration with

Renusagar Power Company Limited (RPCL). All of RPCL‟s assets were merged with

that of HACL. In the year 1986, the company raised its capacity from 120,000 ton to

150,000 ton of aluminum per annum. As part of a policy, the Kaiser Group divested

itself of its holdings in various corporations worldwide where it had a minority

interest and in the process it decided to disinvest its holdings in HACL also. In the

year 1988, the Kaiser Group had sold off all its shares at a premium to the

shareholders of the company and to the employees of the company.

On October 09, 1989, HACL was renamed Hindalco. In 1992, RPCL, which had been

a wholly-owned subsidiary of Hindalco, was merged with the company. In the mid-

1990s, with a view to leveraging on its core strengths, Hindalco started exploring the

possibility of setting up an integrated aluminum complex in Orissa. Subsequently, it

signed an MOU with Orissa Mining Corporation for the transfer of bauxite deposits.The project was named “Aditya Aluminum.”

In the year 1997, HACL announced a technical collaboration agreement with the

Stahlschmidt & Maiworm Gmbh6 of Germany for the establishment of an aluminum

alloy wheel plant at Silvassa Capital of Dadra and Nagar Haveli Union Territory in

western India. The company went for expansion and modernization of an aluminum

alloy wheel plant in the domestic market. After the establishment of the plant,

Hindalco became the country‟s largest integrated aluminum company, surpassing

6 It is one of the leaders in alloy wheels industry with plants in Germany, South Africa,Poland, and the US.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 9/20

Hindalco’s Acquisition of Novelis

367

Indian Aluminum company Limited (Indal)7. In the year 1999, Hindalco acquired

19,38,900 shares of a public sector major, the National Aluminum Company Limited

(Nalco)8, through one of its investment subsidiaries.

In the year 2000, Hindalco acquired a 74.6 percent equity stake in Indal, an Alcan

Canada Group Company, which had a major presence in aluminum products and was a

leader in specialty alumina chemicals. Indal became a subsidiary of Hindalco. Indal‟s

strength in alumina and downstream9 products complemented Hindalco‟s strong

presence in metal. Indal was among the world‟s lowest cost aluminum producers.

In early 2005, all Indal‟s businesses, except for the Kollur foil plant10

in the southern

Indian state of Andhra Pradesh, were merged with Hindalco. Later, in April 2005, the

company signed an MoU with the governments of Orissa and Jharkhand, states in eastern

India, for setting up a Greenfield alumina and aluminum facility in those states this helped

Hindalco to increase the alumina and aluminum capacities to much higher levels.

By 2007, Hindalco was primarily involved in production of aluminum and semi-fabricated products. The company operated in three segments: aluminum, copper and

other precious metals. Hindalco was the leading producer of aluminum in India (Refer

Exhibit VI for a note on the aluminum industry in India). The products of the group

included primary aluminum ingot, alloy ingot, billet, cast slab, wire rods, redraw rods,

alloy rod, foils, and sheet product. The copper business comprised production and sale

of copper in the form of cathodes and continuous cast rods and by-products and other

precious metals. Hindalco‟s stock was publicly traded on the Bombay Stock Exchange,

the National Stock Exchange of India Limited, and the Luxembourg Stock Exchange.

Exhibit VI: Aluminum Industry in India

The Indian aluminum sector is characterized by large players like Hindalco and

National Aluminum Company (Nalco). India has the fifth largest bauxite reserves

with deposits of about 3 billion ton or 5 percent of the world deposits while its share

in world aluminum capacity rests at about 3 percent. However, the per capita

consumption of aluminum in India is extremely low at less than 1 kg as against nearly

25-30 kg in the US and Europe, 15 kg in Japan, 10 kg in Taiwan, and 3 kg in China.

Contd…

7 Established in 1938, Indal started with India‟s first aluminum sheet rolling mill at Belur,near Kolkata, West Bengal. Indal has a nationwide spread of plants and mines, operatingthrough all stages of aluminum value chain from bauxite mining, alumina refining,

aluminum smelting with captive power to downstream sheet and foil rolling and extrusions.8 Nalco‟s activities include exploring, producing, manufacturing, and distributing aluminum

and related aluminum products. The company operates in two segments – Aluminum andChemicals. The Aluminum segment includes aluminum ingots, wire rods, billets, strips andother related products. The Chemicals segment includes calcined alumina, alumina hydrateand other related products. It also produces Bauxite and power.

9 Downstream is closer to the point of sale than to the point of production or manufacture.Companies in this case are involved in further processing the output of an upstreamcompany to produce different products and sell them in the market as end products.

10 The Indal Kollur foil plant was originally a part of Annapurna Foils Limited, the largestmanufacturer of aluminum foil in south India. The company was acquired by Indal in 2001and later merged in April 2002. The plant has the technology from the world-renowned FataHunter of Italy. It is located in Kollur village, Hyderabad, in Andhra Pradesh.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 10/20

Mergers & Acquisitions, and Strategic Alliances

368

Contd…

In the past decade, the primary aluminum producers were Bharat Aluminum

(BALCO) and NALCO in the public sector and Indian Aluminum (INDAL),Hindalco, and Madras Aluminum (MALCO) in the private sector. However, Indal

merged with Hindalco and MALCO was acquired by Sterlite industries.

Consequently, there are only three main primary metal producers in the sector.

With liberalization, the prime strategies were joint venture investments, technology

acquisition/offers, international marketing tie-ups; buy-back arrangements and

subcontracting, technical, managerial, and marketing expertise. As a part of reform,

several policy changes have been expressed to ensure hassle free entry of private

investments. Similarly, as part of moving toward privatization, the government has

withdrawn its presence from as many areas as possible, through closure and sale of

equity or disinvestments.

As a result of the process of liberalization of trade in aluminum, India has emergedas a net exporter of aluminum, on competitive terms. Government monopoly, in

terms of aluminum production and removal of price and distribution control over

aluminum has been diluted in favor of the private sector. The ownership pattern in

the private sector has undergone changes.

Compiled from various sources.

Novelis

Novelis was split from its parent company, Alcan Inc. (Alcan), the Canada-based

aluminum giant and set up as its subsidiary in January 2005. The origin of the

company can be traced back to 1902 when the Northern Aluminum Company, a

Canadian subsidiary of the Pittsburgh Reduction Company was set up. The Pittsburgh

Reduction Company was renamed as the Aluminum Company of America (ALCOA)

in the year 1907. In 1925, The Northern Aluminum Company was renamed the

Aluminum Company of Canada (ACOC) Limited. In 1928, when ALCOA started

disinvesting its funds from outside the United States, a Canadian holding company

called Aluminum Limited (AL) was formed to control the operations. This then

became the parent company of ACOC.

During the 1930s and 1940s, ACOC witnessed significant business growth as

smelting11

and hydroelectric units and fabricating plants were built in the UK and

Canada. In 1939, during the Second World War, the demand for aluminum for the

manufacture of aircraft for the military increased dramatically in Canada, the UK, and

the US. In 1945, ACOC registered the trade name „ALCAN‟. In order to meet the

demand for aluminum, the company concentrated on hydroelectric sites to increaseannual smelter production to nearly five times the existing 500,000 tons and fabricated

plants to produce sheet and other components for the aircraft. After the war, Alcan

expanded its power and smelter capacity.

In the year 1965, the company acquired Central Cable Corporation and, in 1966, the

Metals Disintegrating Corporation. After the acquisition, the Central Cable

Corporation was renamed as the Alcan Cable Corporation and the Metal

Disintegrating Corporation as the Alcan Metal Powders Inc. The acquisition brought

about an increase in the smelting capacity to almost one million tons, which was

11 To melt or fuse to separate the metallic constituents.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 11/20

Hindalco’s Acquisition of Novelis

369

nearly double the existing capacity. In the year 1966, AL was renamed as Alcan

Aluminum Limited (AAL). In the 1970s and 1980s, AAL expanded its operations

internationally by increasing the capacity of the fabricated products and smelting

operations in Australia, the UK, Brazil, and India.

In the early 1980s, taking advantage of the restructuring in the international aluminum

industry, AAL acquired The British Aluminum Company Plc12 and the Atlantic

Richfield13

company in the US. Thereby, it increased its presence in the markets for

fabricated products. In 1987, as a result of corporate restructuring, ACOC, which was

the principal subsidiary became the parent company and was also called AAL.

In the early 1990s, there was a global depression in the prices of metals due to which

the company disinvested from its downstream businesses in Argentina, Australia,

Brazil, Canada, New Zealand, the UK, the US, and Uruguay. The company also

restructured its operations in Japan, China, and Southeast Asia. In 2000, AAL

expanded its packaging business and acquired Alusuisse14

, thereby becoming the

world‟s leading supplier of aluminum-based automotive products, lightweightengineered products, and Alusuisse‟s specialty packaging. In 2001, the company was

renamed Alcan to reflect the company‟s diversified product mix and global character.

In the year 2003, Alcan acquired French aluminum company Pechiney. The merger

combined the assets of both companies, which included bauxite mines, plants to

produce primary aluminum, and rolling mills to produce flat rolled products. The

merged entity supplied products to customers like Coke and Pepsi for cans and to the

manufacturers of automotive components.

In 2004, Alcan split the major activities of Pechiney to hive off its rolled aluminum

products business into a new organization called Novelis. The company was primarily

set up for can recycling and aluminum rolling in January 2005. The rolled aluminum

was made up of a variety of alloy mixtures that were hard, thick, and of appropriatewidths with various coatings designed specially for its end users. It started operations

with 37 operating units in 12 countries with more than 13,500 employees.

Novelis inherited a debt of US$ 2.9 billion from its parent company and suffered

losses. The company bought primary aluminum from Alcan and processed it into

rolled products. In mid-2005 and in 2006, the company signed price ceiling contracts

with some soft drink manufacturers to supply aluminum products at a specified price.

Due to these contracts, the company was forced to sell at a price lower than the raw

material costs though the price of aluminum increased subsequently. This affected

Novelis‟ business. The company incurred a loss of US$ 350 million in the year 2006.

Other reasons for the loss were higher energy and transportation costs; adverse effects

of currency exchange rates; and expenses related to the company‟s restatement andreview process.

12 The aluminium producer British Aluminium Limited was originally formed as the BritishAluminium Company Limited on May 07, 1894 and when ALCAN bought it in 1982, it wasknown as British Alcan Aluminium Plc.

13 Atlantic Richfield is an American oil company that was formed by the merger of the East-coast based Atlantic Refining and the California-based RichField Petroleum, in 1966.

14 It is a Switzerland-based aluminum company that produces rolled iron products for trucksand coaches and rough ingots for the food and pharmaceuticals industry. Afteramalgamation, it was called the Alcan Aluminum Valais SA.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 12/20

Mergers & Acquisitions, and Strategic Alliances

370

In 2006, Novelis restructured its European operations and sold its aluminum rolling

mill in Annecy, France. This was considered as an important step as it helped the

company to focus on its core business and improve its competitiveness in the

European market.

Novelis marked the year 2006 as an innovation year with the introduction of Novelis

Fusion technology, a new process through which multiple alloy layers can be cast into

a single aluminum rolling ingot simultaneously. Fusion Technology increased the

formability15

of aluminum and made the metal suitable to use and to make sheet metal

that helped in building cars with more curves. It increased the use of the strong and

light metal in the automotive industry. Novelis was the first company to start

commercial production of multi-alloy aluminum ingots.

As of February 2007, Novelis operated in 11 countries with 12,900 employees. The

company was organized under four operating segments – Novelis North America,

Novelis Europe, Novelis Asia, and Novelis South America (Refer to Exhibit VII for

Novelis Operating Segments). Novelis operated six aluminum recycling units for producing aluminum sheets and foils. It recycled used aluminum such as beverage

cans; scrap from internal operations, and from customers‟ production plants. Novelis

catered to automotive, transportation, packaging, construction, industrial, and printing

markets by supplying aluminum sheets and foil products. Its shares were listed on the

New York Stock Exchange and the Toronto stock exchange.

Exhibit VII: Novelis Operating Segments

Novelis North America: This segment manufactures aluminum sheet and light

gauge products for beverage cans, containers and packaging, automotive and

transportation applications, building products, and other industrial applications.

Most of the recycled material is from used beverage cans and the material is casted

into sheet ingots for North America‟s can sheet production plants.

Novelis Europe: It provides value-added sheet and light gauge products through 14

plants. The company supplies sheets for building products such as roofing, siding,

panel walls, and shutters. Novelis Europe is a leader in the production of lithographic

sheets. It has the largest beverage can recycling plant at Latchford, UK.

Novelis Asia: It operates through Novelis Korea Limited and Aluminum Company

of Malaysia. Together, they operate three manufacturing units in the Asian region.

The Korean company provides its products to the Asia/Pacific region for

construction, industrial and beverage can markets. The Aluminum Company of

Malaysia is a publicly traded company catering to the Southeast Asian markets. It

operates a continuous casting, rolling, and coating operations.

Novelis South America: It operates two rolling plants and primary production

units in Brazil. It manufactures various aluminum rolled products, including can

stock, automotive and industrial sheets, and light gauge for the beverage & food

can, construction & industrial, and transportation. The company‟s rolling and

recycling facility in Brazil is the largest aluminum rolling and recycling unit in

South America.

Source: www.novelis.com.

15 Formability is the capacity of the material to able to bend, stamped or shaped into therequired form.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 13/20

Hindalco’s Acquisition of Novelis

371

The Deal

Hindalco acquired Novelis through its wholly owned subsidiary AV Metals16

on February

10, 2007. AV Metals purchased 100 percent of the issued and outstanding common shares

of Novelis at US$ 44.93 per share, amounting to US$ 3.6 billion. Hindalco paid a

premium of 16.6 percent on the closing price of Novelis‟ stock. Apart from equity

purchase, Hindalco also acquired Novelis‟ debts to the tune of US$ 2.4 billion.

The amount of US$ 3.6 billion was financed through borrowings, debts from group

companies, and internal cash reserves. Of the total amount, US$ 2.85 billion was financed

by AV Metals through loans taken from three financial institutions – UBS,17

ABN

Amro18, and Bank of America19. US$ 300 million was brought in by Essel Mining20, a

closely held group company, and US$ 450 million was mobilized by Hindalco.

The debt of US$ 2.4 billion was to be taken by Hindalco into its books. The company

planned to repay the debt through the cash flows of Novelis.

Hindalco had to get the approval for the deal from 66.66 percent of Novelis‟

shareholders. According to Canadian law on mergers and acquisitions, if a company

secured 66.66 percent approval, then the remaining shareholders had to sell their

shares at the price agreed upon. However, if the company did not receive the required

approval, it had to quit the deal.

Rationale for Acquisition

After the deal was signed for the acquisition of Novelis, Hindalco‟s management

issued press releases claiming that the acquisition would further internationalize its

operations and increase the company‟s global presence. By acquiring Novelis,

Hindalco aimed to achieve its long-held ambition of becoming the world‟s leading

producer of aluminum flat rolled products. Hindalco had developed long-term

strategies for expanding its operations globally and this acquisition was a part of it.

Novelis was the leader in producing rolled products in the Asia-Pacific, Europe, and

South America and was the second largest company in North America in aluminum

recycling, metal solidification and in rolling technologies worldwide. Novelis had the

most modern technology in the industry and efficiently produced high-quality

products in several countries across the world. While combining the assets of both the

16 AV Metals is the AV Birla Group‟s Canada-based SPV which is a subsidiary of Hindalcoand was created to fulfill specific or temporary objectives, primarily to isolate financial risk,usually bankruptcy but sometimes for a specific taxation or regulatory risk.

17 UBS is a global financial services firm offering wealth management, investment banking, assetmanagement, and business services to the clients. In Switzerland, UBS is the market leader inretail and commercial banking. The bank‟s net profit for the year 2006 was US$ 9097 million.

18 ABN Amro is one of the leading banks in Europe and has operations all over the world. Itwas a result of the merger of Alegemen Bank Nederland (ABN) and Amsterdamsche-Rotterndamsche Bank (AMRO). In April 2007, Barclays announced the deal to buy ABNAmro. The company recorded a profit of euro 4780 million.

19 It is the largest commercial bank in America in terms of deposits. Prior to 1993, it wascalled Nations Bank and in 1998, it merged with the San Francisco-based Bank Americaand the name was changed to Bank of America. For the year ended 2006, it recorded US$74247 million as revenues and a net income of US$ 21133 million.

20 Established in 1950, it is one of India‟s largest iron ore mining companies and part of theAditya Birla group. It is the largest producer of noble ferro alloys like molybdenum,vanadium, tungsten, and titanium with an annual mining capacity of over 5 million ton.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 14/20

Mergers & Acquisitions, and Strategic Alliances

372

companies, the merged entity could establish a global integrated aluminum producer

with low-cost alumina and aluminum production facilities along with aluminum rolled

product capabilities.

Hindalco, which had an upstream21 technology of mining bauxite and converting it

into alumina and then smelting it into aluminum, would benefit from the downstream

technology of Novelis which produced a variety of aluminum products from the raw

aluminum. Kumar Mangalam said, “In aluminum, one needs to invest in downstr eam

to go up the value chain and India does not offer suitable downstream investment

opportunities of a global scale.”22 Novelis had a downstream product capacity of 3.0

million tons while Hindalco had approximately 500 kilo tons. In this context, Debu

Bhattacharya, Managing Director of Hindalco, said, “If we earn $10 for every $100 of

aluminum we sell, we will now be able to earn another $10 for every $100 worth of

aluminum that Novelis processes into rolled products.”23

The deal was expected to fetch economies of scale to Hindalco in the long run by

reducing the costs and time spent in accessing raw materials and by catering to theglobal customers of Novelis. The most important link between them was aluminum,

which was Hindalco‟s finished product and the raw material for Novelis.

Hindalco got its revenues from the sale of its raw metal aluminum, while Novelis

added value to the raw metal aluminum to come out with rolled aluminum products.

These products were used in several high technology applications like automobiles,

beverages, building and construction, etc. This helped Hindalco to capture the total

value chain in the aluminum business. Hindalco had another advantage as the value

chain was already established; it could directly access the market at a lower freight

cost. Hindalco served one end of the value chain while Novelis served the other end.

By clubbing both, they could achieve greater economies of scale in the long run.

According to a research finding, nearly 35 million tons of aluminum was consumed

globally every year. Of that, 40 percent came from rolled products, in which Novelis

was a leading player with a 19 percent share. As Hindalco did not serve this segment,

the acquisition would help it gain access to this segment. In India, it was expected that

the aluminum rolled products market would grow from around 220,000 ton in 2006 to

1 million ton in few years. There was a huge demand for these products in Asian

regions, led by China; which contributed nearly 2.5 million ton of the total demand.

Novelis had highly sophisticated technology which would have taken Hindalco at

least ten years to develop. According to analysts, Novelis‟ assets had a replacement

value of US$ 12 billion and Hindalco would take a long period to match these assets

in the four continents at its current production of 3.3 million ton. Donlad Marleau,

Primary Credit Analyst at Standard & Poor, commented, “This deal is high -level

buying. Novelis is a strong acquisition because of the technology.”

24

In his opinion, itwas difficult to get such technology and even harder to get customer certification.

21 Upstream is closer to the point of production or manufacture than to the point of sale. Companiesin this case are involved in the procurement and production of a particular product which is not byitself the final product and which can be processed further for specific use.

22 Nandini Lakshman, “Metal Merger: India‟s Birla Thinks Big,” www.businessweek.com,February 11, 2007.

23 M.Anand, “Hindalco- Novelis The (Scary) Untold Story,” www.businessworld.com,February 26, 2007.

24 M. Anand, “Hindalco- Novelis The (Scary) Untold Story,” www.businessworld.com,February 26, 2007.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 15/20

Hindalco’s Acquisition of Novelis

373

Apart from gaining technology, Hindalco would also have access to the contracts

which Novelis had entered into for the supply of can body (material for beverage

cans). These contracts would expire in January 2010. After 2011, Novelis can pricing

issues would have been solved and the management expected that it would generatenearly 12 percent return on capital with an annual cash flow of US$ 400 million.

Hindalco would have more aluminum capacity by then and earn good returns on

investments as it planned to add new capacities in its plants which were closer to

Novelis plants in Malaysia and South Korea.

One of Hindalco‟s most important strategies in acquiring Novelis was to have an edge

over the London Metal Exchange (LME)25 prices. Although Hindalco was a low cost

producer of aluminum with good numbers on its balance sheet, it was still affected by

the fluctuations in the prices of aluminum set by the LME in the previous few years. If

the prices of aluminum came down in the near future, its profits were also likely to be

affected (Refer to Exhibit VIII for aluminum price fluctuations).

Exhibit VIII: Alumina and Aluminum Prices (2004-07)(In US$ per ton)

Year* Alumina Aluminum

2004 490 1,700

2005 440 2,000

2006 640 2,900

2007 395 2,832

* In the beginning of the year. Source: www.hindalco.com.

Hindalco‟s management believed that if it acquired a company that sold value-added

aluminum products then it might pass on the price fluctuations to the customers.Though Hindalco had a presence in this value added segment it did not have the

required technology to have an edge. Hence, it acquired Novelis, which had the

largest share in the market. Novelis would add nearly Rs.415 billion26 of sales to

Hindalco with an addition of three million ton of aluminum products to its portfolio.

The Pitfalls

Though the Hindalco-Novelis merger had many synergies, some analysts raised the

issue of valuation of the deal as Novelis was not a profit-making company and had a

debt of US$ 2.4 billion. They opined that the acquisition deal was over-valued as the

valuation was done on Novelis‟ financials for the year 2005 and not on the financials

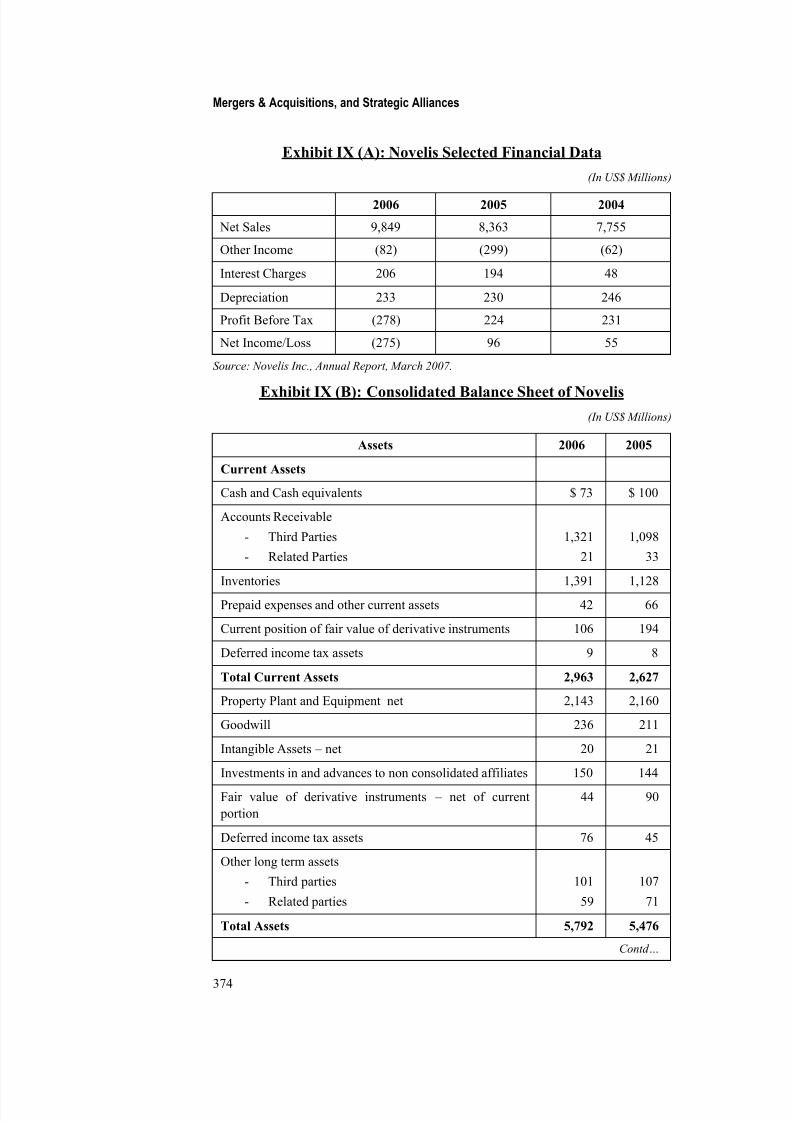

of 2006 in which the company had reported losses (Refer to Exhibit IX for Novelis

P&L statements and balance sheets). They said that Hindalco might have to collect a

huge amount of resources to revive and restructure Novelis. Stewart Spector, an

aluminum industry consultant, opined, “It seems to me that US$ 6 billion is an awful

big premium to pay for a messy operation”27

25 LME is the world‟s premier non-ferrous metal market. It offers futures and options contracts foraluminum, copper, nickel, zinc and lead. The exchange provides a forum for all trading activity.In 2006, LME achieved volumes of 87 million lots, equivalent to $8,100 billion annually.

26 1 US$ = Rupees 41.04 as of August 17, 2007.27 Surojit Chatterjee, “Birla‟s Hindalco Buys Aluminum Giant Novelis for $6.4 billion,”

http://in.ibtimes. com, February 13, 2007.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 16/20

Mergers & Acquisitions, and Strategic Alliances

374

Exhibit IX (A): Novelis Selected Financial Data

(In US$ Millions)

2006 2005 2004

Net Sales 9,849 8,363 7,755

Other Income (82) (299) (62)

Interest Charges 206 194 48

Depreciation 233 230 246

Profit Before Tax (278) 224 231

Net Income/Loss (275) 96 55

Source: Novelis Inc., Annual Report, March 2007.

Exhibit IX (B): Consolidated Balance Sheet of Novelis(In US$ Millions)

Assets 2006 2005

Current Assets

Cash and Cash equivalents $ 73 $ 100

Accounts Receivable

- Third Parties

- Related Parties

1,321

21

1,098

33

Inventories 1,391 1,128

Prepaid expenses and other current assets 42 66

Current position of fair value of derivative instruments 106 194

Deferred income tax assets 9 8

Total Current Assets 2,963 2,627

Property Plant and Equipment net 2,143 2,160

Goodwill 236 211

Intangible Assets – net 20 21

Investments in and advances to non consolidated affiliates 150 144

Fair value of derivative instruments – net of current

portion

44 90

Deferred income tax assets 76 45

Other long term assets

- Third parties

- Related parties

101

59

107

71

Total Assets 5,792 5,476

Contd…

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 17/20

Hindalco’s Acquisition of Novelis

375

Contd…

LIABILITIES AND SHARE HOLDERS EQUITY

Current Liabilities

Current portion of long term debt 144 3

Short term borrowings 133 27

Accounts Payable

-Third parties

- Related parties

1,542

44

964

38

Accrued expenses and current liabilities 508 543

Deferred income tax liabilities 61 26

Total Current liabilities 2,432 1,601

Long term debt – net of current portion 2,158 2,600

Deferred income tax liabilities 81 186

Accrued post retirement benefits 425 305

Other long term liabilities 343 192

5,439 4,884

Minority interest in equity of consolidated affiliates 158 159

Share holders equity

Preferred stock … …

Common stock … …

Additional paid in capital 398 425

Retained earnings (accumulated deficit) (198) 92

Accumulated other comprehensive losses (5) (84)

Total share holders equity 195 433

Total liability and share holders equity 5,792 5,476

Source: Novelis Inc., Annual Report 2007.

After the deal, Hindalco‟s debt– equity ratio was expected to slide down to 2:1 from

1:2. This was expected to further affect Hindalco‟s balance sheet. Analysts were

predicting a dilution in the EPS of Hindalco by 18 percent after the acquisition.

Further, the deal could reduce Hindalco‟s reserves, which were being used for fundingthe deal. The profits would also be affected due to the interest on the debt borrowed.

The analysts therefore were of the opinion that the acquisition would dilute the

earnings of the company. Due to the massive expansion plans taken up by Hindalco,

Novelis would further push Hindalco‟s high gearing level28

. It was also estimated that

Hindalco would have to improve annual free cash flow by 35 percent to US$ 540

million for the acquisition to be considered as neutral.

28 Debt gearing level is the relationship between the long term liabilities of the business andthe capital employed. The idea behind calculating the ratio is to have a balance between theshareholders‟ funds and the long term liabilities.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 18/20

Mergers & Acquisitions, and Strategic Alliances

376

According to a report by Edelweiss Research29

on Hindalco, the Novelis deal was

valued at 4.7 times EV/EBITDA30 for the financial year 2006-07 earnings. This

valuation had been done based on the debt and the earnings before accounting for all

non-cash items. It also did not take into account the price ceiling contracts. The report

stated that the deal seemed to be expensive for a non-integrated low margin business.

It also stated that the deal would dilute the 2007-08 financial years‟ earnings by 12

percent, while the debt-equity ratio was expected to increase to (2.72:1 from 0.43) for

the same year. The key assumptions made by Hindalco‟s management while entering

into the deal was an increase in aluminum and copper prices, increase in metal

production, and higher backward integration related synergies which were not

factored by Edelweiss Research into their estimates.

Industry experts pointed out that though Novelis had a leading global presence in

rolled aluminum products, it did not have much pricing power. This was because

Novelis had to face competition from strong players like Alcoa, Norsk Hydro, Alcan,

and Aleris who contributed nearly 53 percent of the global market share. In such ascenario, to gain market share, Novelis had entered into can contracts till 2010 and

sacrificed its profits. Novelis was running into losses due to the can contracts.

A research note from Merrill Lynch speculating on the possibility of such a deal said

the negatives could outweigh the positives. Merrill analyst, Vandana Luthra, pointed

out that during periods of rising aluminum prices, margins were sharply squeezed, as

selling prices for finished product did not increase commensurately.

However, Hindalco‟s management felt that the deal would be beneficial for the

company in the long term and would allow it access to global customers. Kumar

Mangalam said, “The complementary expertise of both these companies will create

and provide a strong platform for sustainable growth and ongoing success.”31

He

added that the acquisition would lead Hindalco into the Fortune 500 companies‟ list,three years ahead of the target. Hindalco was expected to double its turnover to US$

20 million after the acquisition. After the acquisition was completed in May 2007,

Novelis became a subsidiary of Hindalco.

In mid-2007, Hindalco was planning a massive expansion of its operations by

increasing the capacity to 1.5 million tons by 2011-12. This would make Hindalco one

of the world‟s fifth largest producers of aluminum, up from its position as 13 th largest

in 2007. Hindalco had formed a JV with Almex, US, to manufacture high strength

aluminum alloys for application in aerospace, sporting goods, and surface transport

industry.

29 India-based Edelweiss Capital Ltd offers investment banking, private placement of equity,convertible debt, merger and acquisition advisory, and restructuring services. The companyis also involved in stock broking, distribution of financial products, and asset managementservices. The company also provides market research services.

30 EV includes the cost of paying debt; EBITDA refers to Earnings before Interest TaxDepreciation and Amortization. EV/EBITDA compares the value of the company free ofdebt, to earnings before interest and tax. It is calculated without taking into account the costof assets or the effects of tax. EV/EBITDA is generally used to value shares, it is assumedthat debt (such as bonds) that has a verifiable market value is worth its market value. Otherdebts may be assumed to be worth its book value (the amount shown in the accounts).

31 Surojit Chatterjee, “Birla‟s Hindalco Buys Aluminum Giant Novelis for $6.4 billion,”http://in.ibtimes.com, February 13, 2007.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 19/20

Hindalco’s Acquisition of Novelis

377

Suggested Readings and References:

1. The Birth of Giants Alcan and Alcoa, http://www.alunet.net, 1999.

2. Heather Timmons, Indian Metals Company to Buy Canadian Rival,

www.iht.com, February 11, 2007.

3. Nandini Lakshman, Metals Merger: India's Birla Thinks Big, www.businessweek.com, February 11, 2007.

4. Hindalco to Buy Novelis for $6 Billion, www.forbes.com, February 11,2007.

5. Hindalco Industries Ltd. and Novelis Inc. Announce an Agreement for

Hindalco’s Acquisition of Novelis for Approximately $6.0 Billion, www.http://www.finanznachrichten.de/nachrichten, February 11, 2007.

6. Birla buys US based metal major for $6 bn, www.rediff.com, February 12,

2007.

7. Laura Mandro & Robert Daniel Novelis Shares Leap on $6 Billion Hindalco

Buyout, www.marketwatch.com, February 12, 2007.

8. Novelis to add Rs 41,500 cr in Hindalco’s Sales, www.timesofinida.indiatimes.com. February 12, 2007.

9. Hindalco to Acquire US-Based Novelis in $6-B All-Cash Deal, http://www.thehindubusinessline.com, February 12, 2007.

10. Surojit Chatterjee, Birla’s Hindalco Buys Aluminum Giant Novelis for $6.4

billion, http://in.ibtimes.com, February 13, 2007.

11. Suresh P. Iyengar, Hindalco may not Impact Aluminum Prices,

www.businessline.com, February 13, 2007.

12. Flash note by HSBC on Hindalco Industries, www.hsbcnet.com, February13, 2007.

13. Role of Royalty in Hindalco Novelis Buy, www.minesandcommunitites.org, February 14, 2007.

14. Chidanand Rajghatta, Novelis Acquisition puts Indian Stamp on Coke,

Budweiser Can, www.timesofindia.indiatimes.com, February 14, 2007.

15. Indian Economic News- Policy Update, www.indianembassy.org, February15, 2007.

16. M. Anand, Hindalco – Novelis The Untold Story,

www.businessworldindia.com, February 26, 2007.

17. 2007 Metal Industry News, www.metalcenternews.com, March 2007.

18. Andrew Corn, Indian Conglomerate Buys Novelis, www.seekingalpha.com, April19, 2007.

19. Reduce Hindalco Industries: Edelweiss, www.moneycontrol.com, May 14,2007.

20. Novelis Now a Hindalco Subsidiary Acquisition Process Completed, www.businesswireindia.com, May 15, 2007.

8/10/2019 Case 4 Hindalco’s Acquisition of Novelis.pdf

http://slidepdf.com/reader/full/case-4-hindalcos-acquisition-of-novelispdf 20/20

Mergers & Acquisitions, and Strategic Alliances

378

21. Hindalco Industries Completes Acquisition of Novelis Inc., www.canstock.com, May 15, 2007.

22. Martha Finn Brooks Named President of Novelis Inc., http://biz.yahoo.com, May 16, 2007.

23. Crisil Downgrades Hindalco’s NCDs, www.thehindubusinessline.com, June17, 2007.

24. www.bigcharts.com.

25. www.wikipedia.com.

26. www.novelis.com.

27. www.hindalco.com.

28. www.alcan.com.

29. www.aluminum.org.

30. www.economictimes.com.

31. www.birlagroup.com.

32. www.myiris.com.

33. www.novelisrecycling.com.