caribbean air transport - documents & reports - all ...€¦ · annex 4 - air transport...

TRANSCRIPT

September 25, 2006

Document of the World Bank

Report N

o. 36863-LAC

C

aribbean Air Transport

Report No. 36863-LAC

Caribbean Air Transport

Strategic Options for Improved Services and Sector Performance

Finance, Private Sector and Infrastructure Department (LCSFP)Latin America and the Caribbean Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Table of Contents

Acknowledgements .......................................................................................................................... i Technical Terms .............................................................................................................................. 11

Executive Summary ....................................................................................................................... iii

I . Introduction and Objectives ......................................................................................................... 1 I1 . Civi l Aviation, International Trade and Tourism in Caribbean Economic Development ......... 2 I11 . What Can Air Services Do For Tourism Development? .......................................................... 5 IV . Policy and Regulation o f Air Services .................................................................................... 12 V . Regional Airline Services ........................................................................................................ 24 V I . Where Do We Go From Here - and How? ............................................................................. 36 Annexes ......................................................................................................................................... 41 Annex 1 - Caribbean Air Transport Services Symposium, Barbados: June 1-2, 2006 ................ 42 Annex 2 - Caribbean Regional Organizations and their Membership. ......................................... 45 Annex 3 - Caribbean Tourism and Transport Statistics ................................................................ 46 I . Trends and composition o f tourist arrivals ............................................................................ 46 I1 . Dominican Republic - Tourism trends and air transport services ........................................ 48

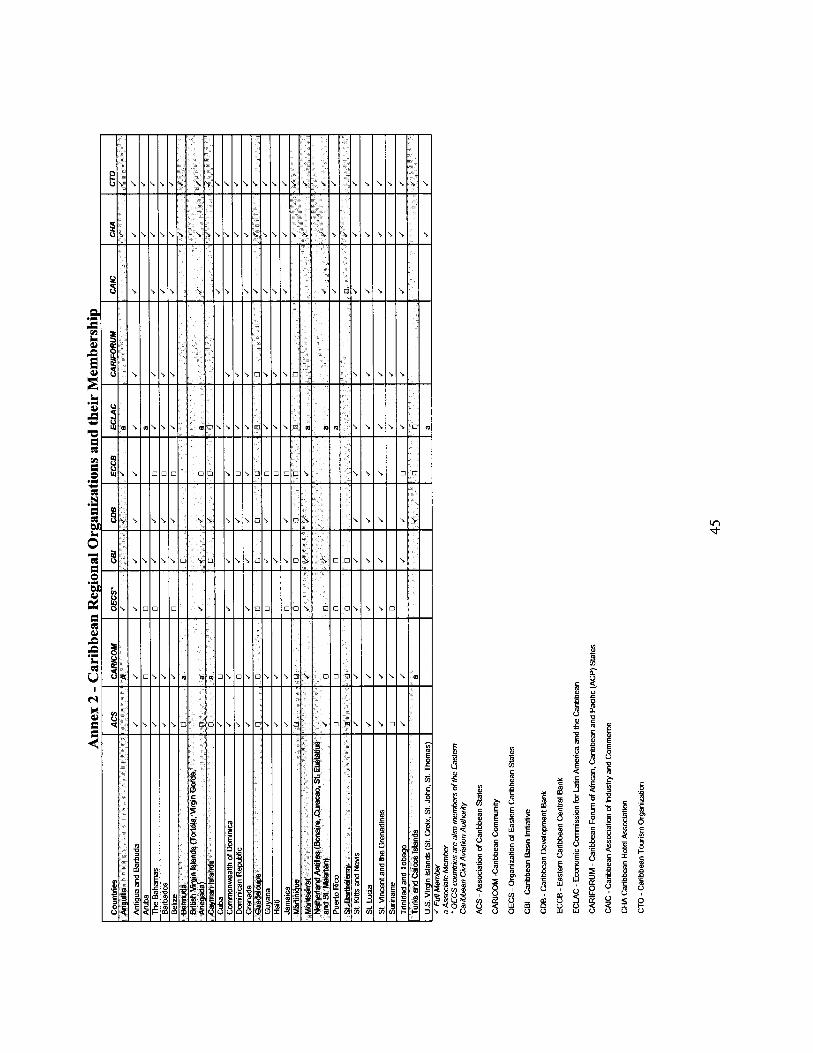

Annex 4 - Air Transport Services Case Studies ............................................................................ 50 A . Aruba .................................................................................................................................... 50 B . Barbados ............................................................................................................................... 56 C . Mauritius .............................................................................................................................. 64

Annex 5 - L i s t o f Reports and References .................................................................................... 75 Annex 6 - List o f Persons Met and/or Interviewed ....................................................................... 77 Map IBRD 34974 .......................................................................................................................... 82

.. ...

List of Tables . Main Text

Table 1 : Caribbean Arrivals by Air. 2004-2005 ............................................................................................................ 4 Table 2: Intra-Caribbean Movements by Air. 2000-2003 .............................................................................................. 4 Table 3: Aviation Safety Status in Selected Caribbean Countries ............................................................... Table 5: Caribbean Airlift Capacity - by Country ................... Table 6: OECS - Analysis of Intra-Eastem Caribbean Airlift . Table 7 : Regional Airlines Operational Performance

Table 4: Caribbean Airlift Capacity - by Airline .......

List of Boxes . Main Text

Box 1: Airport Security in OECS ...................

Box 3: Key Features o f the CARICOM MASA . Box 4: Recent International Experience in Box 5: Examples o f Subsidized Air Services .............................................................................................................. 20

Box 2: Air Services Policy in Aruba and B ............................................ 15

................................................................... 16

Box 6 : The Fiscal and Economic Impact o f LIAT Operati Box 7 : The Experience o f Mauritius ..................... Box 8: Jamaica - One Approach Towards Estimat

List o f Charts - Main Text

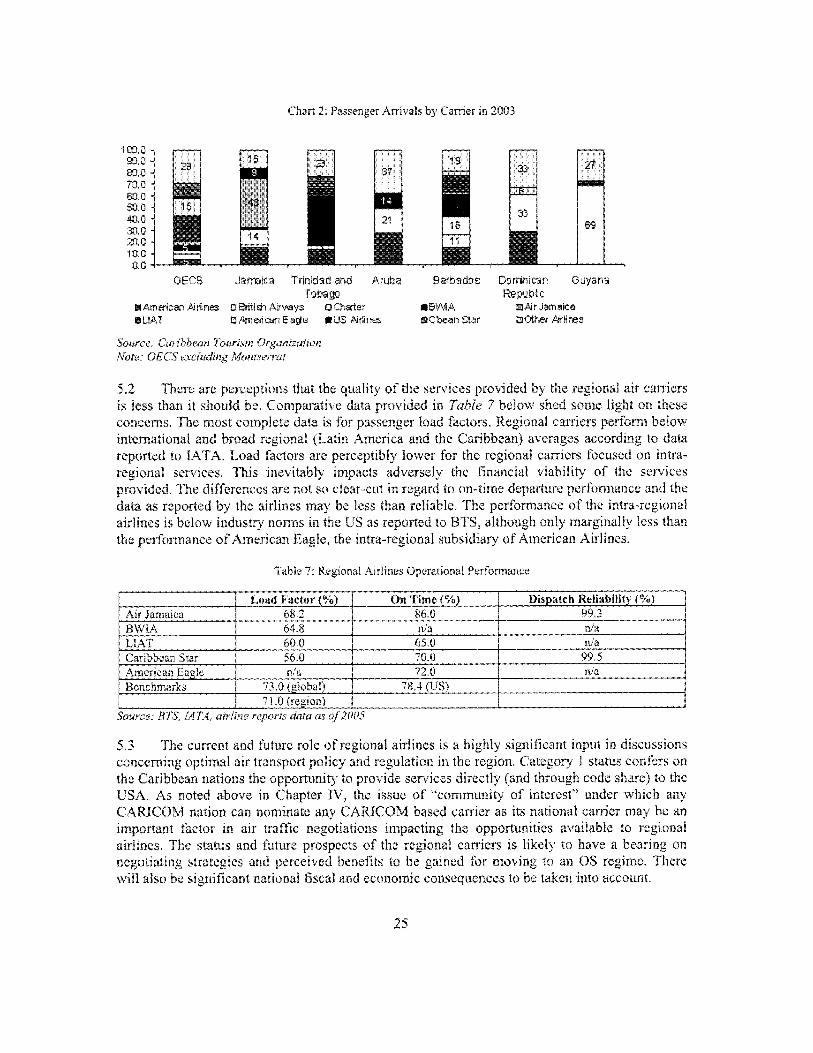

Chart 1: U.S. - Caribbean Traffic Compared to Other Regions .................................................................................... 3 Chart 2: Passenger Arrivals by Carrier in 2003 ........................................................................................................... 25

List of Tables - Annexes

Table A4- 1 : Weekly flights by Airline and Destination CountryRegion: February 13-1 9, 2006 .............................. 60 Table A4- 2: Weekly flights by Airline to USA Airports: February 13-19, 2006. ...................................................... 61 Table A4- 3: Weekly flights by Airline to European Airports: February 13-19, 2006 ................................................ 61 Table A4- 4: Tourist Arrivals in Mauritius from Country o f Origin ........................................................................... 65 Table A4- 5: Overview of key Bilateral Air Services Agreements ............................................................................. 66

List of Charts - Annexes

Chart A3- 1 : Tourists Arrivals to Selected Caribbean Chart A3- 2: Tourists Arrivals to Selected Caribbean Chart A3- 3: Tourists Arrivals per Capita in Selected Chart A3- 4: Tourists Arrivals per Capita in Selected Chart A3- 5: Tourists Arrivals by Main Market (in percentage o f total) ..................... Chart A3- 6: Dominican Republic: Tourist Arrivals by Main Market (in percent)

Chart A3- 8: Total Passenger Movement by Air (perc Chart A3- 7 : Total Passenger Movement by Air ........ Chart A3- 9: Total Scheduled Passenger (Arrivals and Departures) by Airport. Chart A3- 10: Total Charter Passenger (Arrivals and Departures) by Airport ............................................................ 49 Chart A4- 1 : Tourist (Stop-Over) Arrivals per Capita in Selected Countries, 2004 .................................................... 50

Chart A4- 3: Tourist Arrivals by Country in 2004 (in percent o f total) .................................................... Chart A4- 4: Tourist Arrivals by Country (Non-US) ................

...................................... .49

Chart A4- 2: Aruba Real GDP and Tourism Sector Performance (percent change) .................................................... 50

Chart A4- 5: Air Passenger Arrivals to Amba by Carrier ...................... Chart A4- 6: Real GDP and Long-Stay Tourist Arrival Growth Rates . Chart A4- I : Barbados: Tourist Arrivals by Country o f Residence ....... Chart A4- 8: Tourist Arrivals by Market, 2004 ...... Chart A4- 9: Passengers (EmbarkedDisembarked Chart A4- 10: Passengers (EmbarkedDisembarkedTransit) Carried by Charters in 2004 ......................................... 60 Chart A4- 1 1 : Load Factor on Selected Routes ............................................................... .68 Chart A4- 12: Destination and Share o f Cargo Chart A4- 13: Contribution to Passengers Tra Chart A4- 14: Contribution to Freight Traffic and Revenues .............................................................. Chart A4- 15: Shareholding o f Air Mauritius Ltd. (March 2005) ........................................................ Chart A4- 16: Number o f Hotel Rooms and Annual Growth Rate .......................................................... Chart A4- 17: Hotel Occupancy Rate ............................................................................. Chart A4- 18: Average Length o f Stay in Hotels ................................................................

AcknowledPements

This report was prepared by Douglas R. Andrew (Lead Infrastructure Specialist) and Stephen J. Brushett (Lead Transport Specialist).

The report takes into account the results o f a stakeholder symposium that was held in Barbados, June 1-2,2006, details o f which are provided in Annex I o f this report.

The report also takes into account the findings o f a “Caribbean Air Transport Services Study - Air Fares Yie ld Analysis and Best Practices Simulation Model” carried out by a team from Inter VISTAS Consulting Inc. led by Douglas Wilson, Director o f Transportation, Forecasting and Planning under funding provided by the Bank.

Specific contributions to the preparation o f the report were made by: Ingrida Rosa (Consultant Economist), who collected and analyzed data for this report and who prepared the Aruba and Barbados case studies and by Vickram Cuttaree (Infrastructure Economist), who prepared the Mauritius case study. Marc Forni (Consultant) provided information concerning air transport infrastructure, safety and security improvements in the OECS countries. Additional research was carried out by Julieta Abad and Nicolas Serrie. Annette Minott assisted in the organization o f the above-mentioned stakeholder symposium and o f the various country visits. Maria Constancia Mal lo provided assistance in the editing and formatting o f this report.

Peer reviewers were Charles Schlumberger (Senior Transport Specialist), Pierre Pozzo di Borgo (Senior Transport Specialist) and Jordan Schwartz (Senior Infrastructure Specialist).

Special thanks for their contributions and insights are due to McHale Andrew (Research and Development Adviser, Caribbean Tourism Organization - CTO) and Ian Bertrand (Civil Aviation Consultant, El Perial Management Services) responsible for carrying out the parallel EU funded study on air transport services under the Caribbean Regional Sustainable Tourism Development Program (CRSTDP).

Technical Terms

International air service among states i s governed by the International Air Services Transit Agreement (IASTA) and by complementary bilateral air services agreements (BASA) which cover the rights o f airlines o f one state to fly (and carry passengers and cargo) into and beyond another state. The rights permitted in terms o f airline entry, the frequency and capacity o f flights, pricing and regulation o f airline co-operation as well as other operational issues, are normally covered in these agreements which are categorized by defined "freedoms o f the air" in ascending order o f "liberalizationy', i.e.:

1" freedom - aircraft o f one state flying over another state 2"d freedom - landing for technical reasons in another state 3'd freedom - carriers from state A setting down passengers in state B 4'h freedom - carriers from state A picking up passengers from state B 5'h freedom - carriers from state A picking up passengers in state B destined for state C or setting down passengers in State B originating in State C

The 1" and 2nd freedoms are included in the IASTA. The other freedoms would normally be included in the BASA, though 5th freedom rights are rarely granted.

"Open Skies" (OS) bilateral air service agreements usually have the following characteristics:

unlimited airline designation provided the airlines have at least their principal place o f business in the designating state; an open route schedule; open traffic rights; open capacity; airline investment provisions which focus on effective control and principal place o f business, but protect against flag o f convenience carriers; third-country code-sharing; a minimal tariff filing regime; and application o f normal competition law

The Multilateral Agreement on the Liberalization of International Air Transportation (MALIAT) provides for:

an open route schedule open traffic rights open capacity designation based on effective control and principal place o f business but protection against flag o f convenience carriers multiple airline designation third country code sharing minimal tariff filing regime retention o f cabotage

11

Executive Summarv

Introduction. Safe and secure air transport services, provided cost effectively in response to demand, are key contributors to the economic development o f the Caribbean region. The present study builds on the results o f earlier analyses o f the constraints to improved air transport sector performance and seeks to provide guidance to the Caribbean governments on available strategic options centered on two specific areas: (i) improving sector policy and regulation for air services at both the national and regional level, including approaches to securing service continuity on potentially unprofitable routes; and (ii) addressing the future role o f regionally-owned and operated airlines and the contribution o f governments thereto.

Background. The report has been prepared in response to the demand init ially expressed by the countries o f the Organization o f Eastern Caribbean States (OECS) further to which the required study was included in the FY06-09 Country Assistance Strategy. The audience for this report i s however the Caribbean Community as a whole, given the broad regional interest and topicality o f the subject matter, and Jamaica, Barbados and Trinidad and Tobago in particular given their ownership interests in airlines which play a critical role in inter-island interconnectivity in the Eastern Caribbean.

The report takes into account the results o f a stakeholder symposium held in Barbados June 1-2, 2006 which was attended by 37 participants - from 7 different Caribbean countries representing governments, airport authorities and regionally- based airlines and from various regional organizations involved in c iv i l aviation, tourism, economics and development finance. The symposium notably confirmed the strategic importance o f sustaining effective regional services; making foreign based airlines want to fly to the Caribbean; and making regionally based airlines viable. Participants also noted that effective air transport services would be a critical underpinning to the successful implementation o f the Caribbean Single Market and Economy and to exploiting opportunities for regional, multi-destination tourism.

Conclusions and Recommendations. Four main sets o f conclusions and recommendations emerge from the report:

1. Evidence from international experience supports the view that a policy o f liberalization i s effective in securing cost effective, reliable and quality air transport services in most cases. Competitive forces and technological change in the industry (smaller, efficient aircraft) increase the opportunity to provide services to various markets at a profit. This holds true inter al ia in the Caribbean sub-region where recent empirical evidence suggests: lower fares f iom the United States to destinations adopting an “open skies” regime compared to those that do not; some examples o f where private sector airlines are able to profitably service small island markets. Caribbean nations would thus be advised to adopt a fully unrestrictive policy towards air services provided that: (i) local airlines have a right to compete, with the “community of interest” principle applying; and (ii) adequate arrangements are put in place to ensure fair competition. In this regard negotiated “open skies” style bilateral agreements should be complemented by a revision to the CARICOM multilateral agreement to open new competitive opportunities for the provision o f regional air services.

... 111

2. Evidence from international experience indicates that there are few cases where the public sector has been able to run an airline efficiently and profitably. For specific historical reasons, there are, however, a number o f airlines in the Caribbean sub-region which currently are part or wholly publicly owned. These airlines are undercapitalized and are generally facing serious operational and financial problems, with consequent negative impact on the quality and reliability o f regional services. Caribbean nations with ownership interests in regionally based airlines would be advised to adopt clear and appropriate policies and to take necessary actions to allow such airlines to compete, to become pro j tab le and earn appropriate returns or else go out of business. Open-ended, non-transparent and unpredictable government support for these airlines should not continue. A formal ownership agreement between each government and the airline board could be struck covering, inter alia: target rates o f return; l ines o f business; risk management policy; dividend policy; Board accountability to the government; and financial support from the government necessary to implement the policy.

3. Continuity o f inter-island air services - especially in the Eastern Caribbean - in a liberalized market i s a legitimate concern. International evidence suggests that there are many countries adopting liberal air services policies that have recognized the importance o f securing social services (public service obligation). There are a number o f working schemes in place for addressing this need, though relatively few so far in developing countries. Caribbean nations would be advised to adopt appropriate policies in regard to public service obligation which would underpin, for example, the award of subsidies to airlines for selected routes and services on the basis of a competitive process - that is to ensure “competition for the market ’’ where “competition in the market ” cannot be sustained. The policy should clearly establish inter alia: objectives; target beneficiary groups or communities; payment arrangements; and performance monitoring.

4. A liberal environment for the provision o f air transport services does not obviate the need for effective policy and regulatory capacity. Governments will need the capability and the know how to effectively manage the opportunities created by competition for services to ensure overarching policy objectives can be met and satisfactory services to the consumer can be secured. A good start, for example, has been made in this direction in the Eastern Caribbean in regard to the management o f air safety and security. Further to this, Caribbean nations would be advised to take the opportunity to now generally review and selectively strengthen public sector capacity, in order to assure effective monitoring of air transport services, to critically assess policy options and their impact on sector performance, and to develop and sustain knowledge of a i r transport best practices.

i v

I. Introduction and Obiectives

1.1 Safe and secure air transport services, provided cost effectively in response to demand, are key contributors to the economic development o f the Caribbean region. The present study builds on the results o f earlier analyses o f the constraints to improved air transport sector performance and seeks to provide guidance to the Caribbean governments on available strategic options centered on two specific areas: (i) improving sector policy and regulation for air services at both the national and regional level, including approaches to securing service continuity on potentially unprofitable routes; (ii) addressing the future role o f regionally owned and operated airlines and the contribution o f governments thereto.

1.2 T h i s report has been prepared in response to the demand init ially ex ressed by stakeholders in the countries o f the Organization o f Eastern Caribbean States (OECS) , further to which the Bank agreed to the inclusion o f an air transport rationalization study in the FY06-09 Country Assistance Strategy. The audience for the report i s however the English speaking Caribbean region as a whole, not the OECS alone. Air transport policy reform and the improvement o f Caribbean air services are matters o f broader regional concern and in fact a matter o f specific attention at this time in the Caribbean Community (CARICOM). Island interconnectivity, .especially in the Eastern Caribbean, i s impacted inter alia by the status and performance o f various regionally-based airlines, in a number o f which Caribbean governments have significant strategic and financial interests - particularly in Air Jamaica, BWIA (British West Indies Airways) and Leeward Islands Air Transport Services (LIAT). Thus, in addition to the OECS, particular attention i s paid in this report to the issues and options for Jamaica, Barbados and Trinidad and Tobago (TT).

P

' Comprising Anguilla; Antigua and Barbuda; British Virgin Islands; Dominica; Grenada; Montserrat; St. Kitts and Nevis; St. Lucia; and St. Vincent and The Grenadines.

11. Civil Aviation, International Trade and Tourism in Caribbean Economic Develonment

EfJicient demand responsive air transport services are crit ical for international trade and economic development. This applies with particular force in the Caribbean in view of its geography, its openness and its dependence on the tourism sector. While Caribbean tourism growth has lagged world average growth rates, the sector has responded well post 9/11 and is diversifLing to meet new market demands. The Eastern Caribbean may be more vulnerable however than other parts of the region to trends towards new destinations. Whereas the cruise market is an important one, air arrivals account for most of the time - and money - spent in the Caribbean market. The most signflcant sources of tourism are North America and - less so - Western Europe, but there is also a substantial amount of intra-Caribbean travel.

2.1 A well functioning air transport sector offers significant economic development benefits2. Integration o f developing nations into global and regional markets - and the concomitant benefits that come from increased trade and economic diversification - i s inconceivable without adequate air transport infrastructure (ATI) and the transport services to make use o f them. The attractiveness o f developing nation markets for new business opportunities wil l depend critically on how effectively rising demand for air travel, both passenger and freight, can be met.

2.2 The arguments for a strong, responsive air transport sector apply with particular force in the Caribbean region. This i s a region essentially comprised o f a large number o f diverse, small island economies which are highly dependent on international trade. Geographical realities thus also place serious limits on the traditional role o f land transport in meeting demands for mobility. Additionally, maritime transport has thus far had a limited economic impact and i s largely geared to meeting the demands o f niche markets for passenger travel (cruises, yachting) with a limited number o f ferry services available to the traveling public. As discussed below, the tourism sector, accounting for about 18% o f GDP and 34% o f employment, i s now, and i s likely to remain, a driving force for Caribbean economic growth and uniquely reliant on good air linkages to i t s main markets, in North America and Western Europe. Economic diversification in the region i s giving rise to additional demands for good connectivity, though both transport and telecommunications in such areas as financial and information services, and other “offshore” businesses such as in education and health3. Most nations also have important “diaspora” communities: cost-effective air services contribute to their continued linkages to home countries with the associated economic benefits.

2.3 The Caribbean region i s recognized as one o f the world’s leading tourism destinations, traditionally driven by “sand, sea and sun” opportunities packaged to suit a variety o f demands. Proximity to the USA - accounting for over one third o f a l l tourists and same day arrival to the primary destinations in the north o f the region - and recent diversification into new niche markets - adventure, nature and event based tourism - are among factors that should fuel future tourism sector growth. Tourism in the Caribbean is, however, subject to intense global competition and inevitably there i s significant price sensitivity. In this regard, it should be remembered that the USA i s simultaneously an important source o f tourist traffic as well as a

World Bank 2005e. This paragraph owes largely to World Bank 2005c.

2

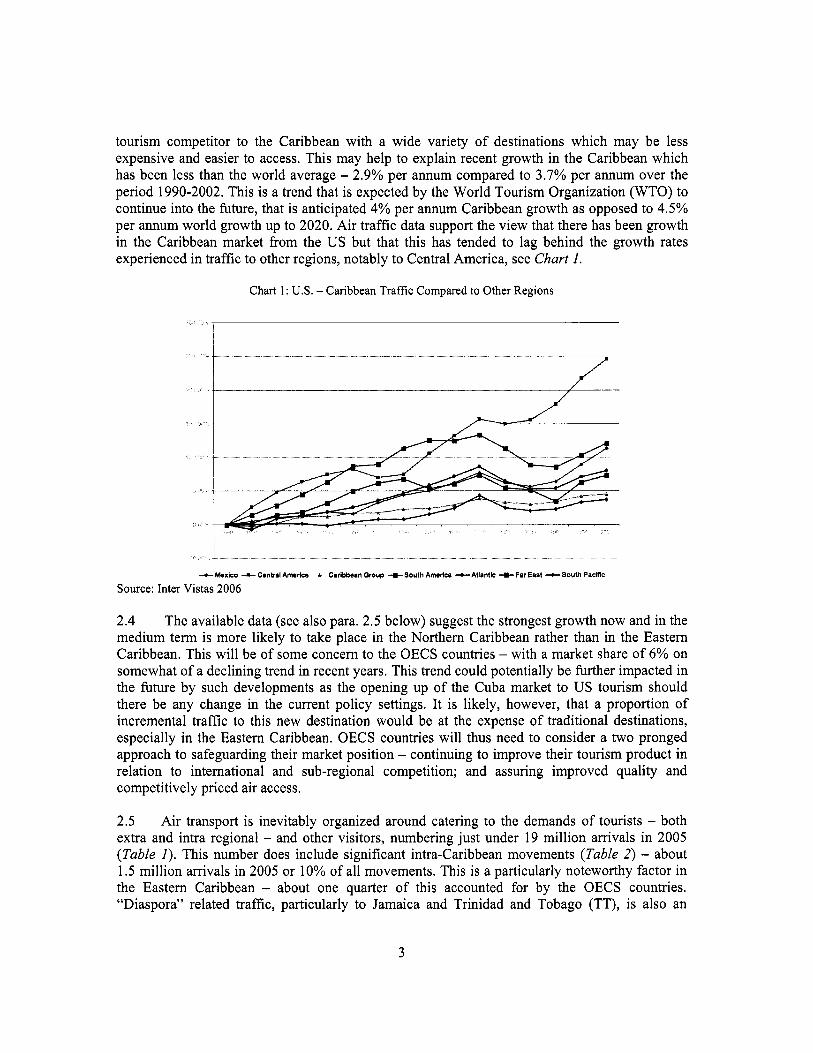

tourism competitor to the Caribbean with a wide variety o f destinations which may be less expensive and easier to access. This may help to explain recent growth in the Caribbean which has been less than the world average - 2.9% per annum compared to 3.7% per annum over the period 1990-2002. T h i s i s a trend that i s expected by the Wor ld Tourism Organization (WTO) to continue into the future, that i s anticipated 4% per annum Caribbean growth as opposed to 4.5% per annum world growth up to 2020. Air traffic data support the view that there has been growth in the Caribbean market from the U S but that this has tended to lag behind the growth rates experienced in traffic to other regions, notably to Central America, see Chart 1.

Chart 1: U.S. - Caribbean Traffic Compared to Other Regions

+Moxko + C a n t r a l h r k a * Caribbean Group +South America +Atlantk +FarEast +South Pacmc

Source: Inter Vistas 2006

2.4 The available data (see also para. 2.5 below) suggest the strongest growth now and in the medium term i s more likely to take place in the Northern Caribbean rather than in the Eastern Caribbean. This wil l be o f some concern to the OECS countries - with a market share o f 6% on somewhat o f a declining trend in recent years. This trend could potentially be further impacted in the future by such developments as the opening up o f the Cuba market to US tourism should there be any change in the current policy settings. I t i s likely, however, that a proportion o f incremental traffic to this new destination would be at the expense o f traditional destinations, especially in the Eastern Caribbean. OECS countries wil l thus need to consider a two pronged approach to safeguarding their market position - continuing to improve their tourism product in relation to international and sub-regional competition; and assuring improved quality and competitively priced air access.

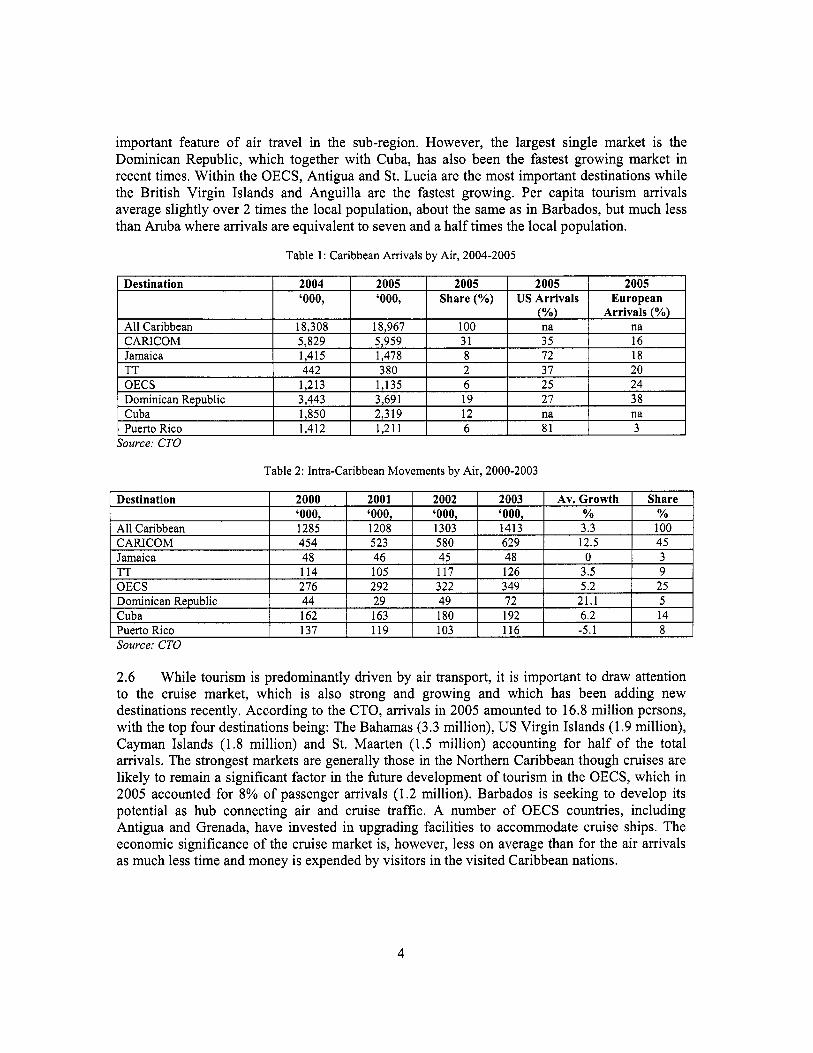

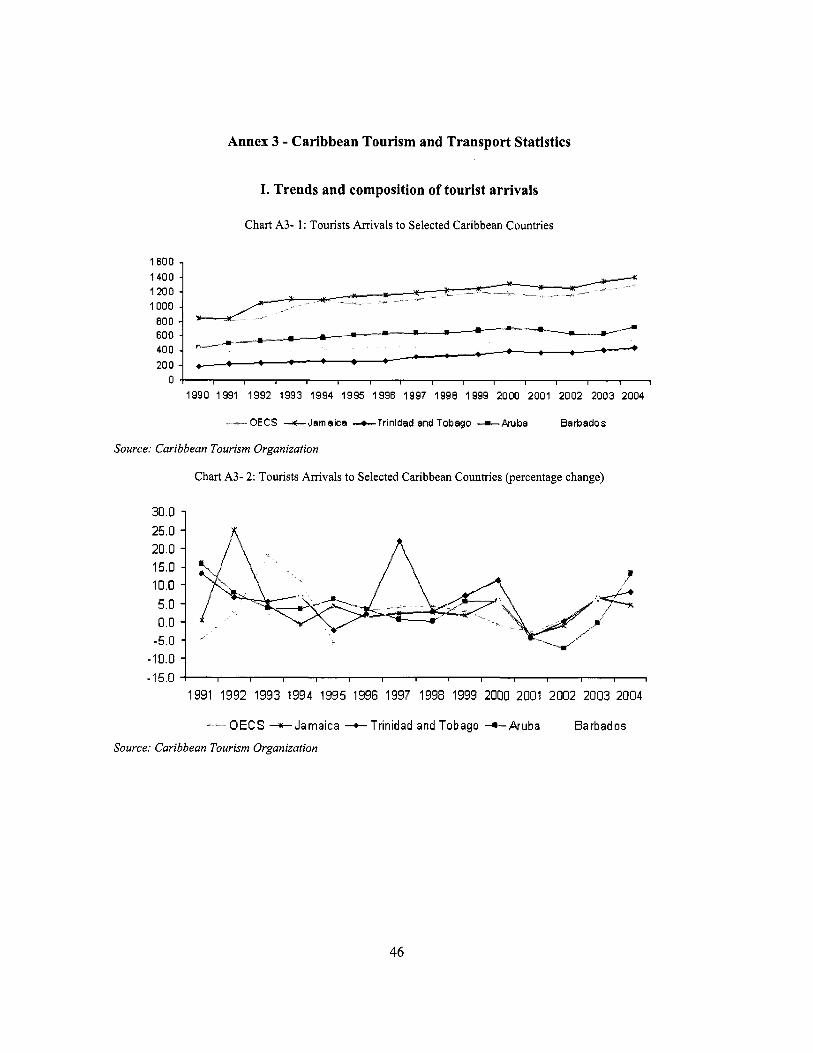

2.5 Air transport i s inevitably organized around catering to the demands o f tourists - both extra and intra regional - and other visitors, numbering just under 19 mi l l ion arrivals in 2005 (Table I). This number does include significant intra-Caribbean movements (Table 2) - about 1.5 mi l l ion arrivals in 2005 or 10% o f al l movements. This i s a particularly noteworthy factor in the Eastern Caribbean - about one quarter o f this accounted for by the OECS countries. “Diaspora” related traffic, particularly to Jamaica and Trinidad and Tobago (TT), i s also an

3

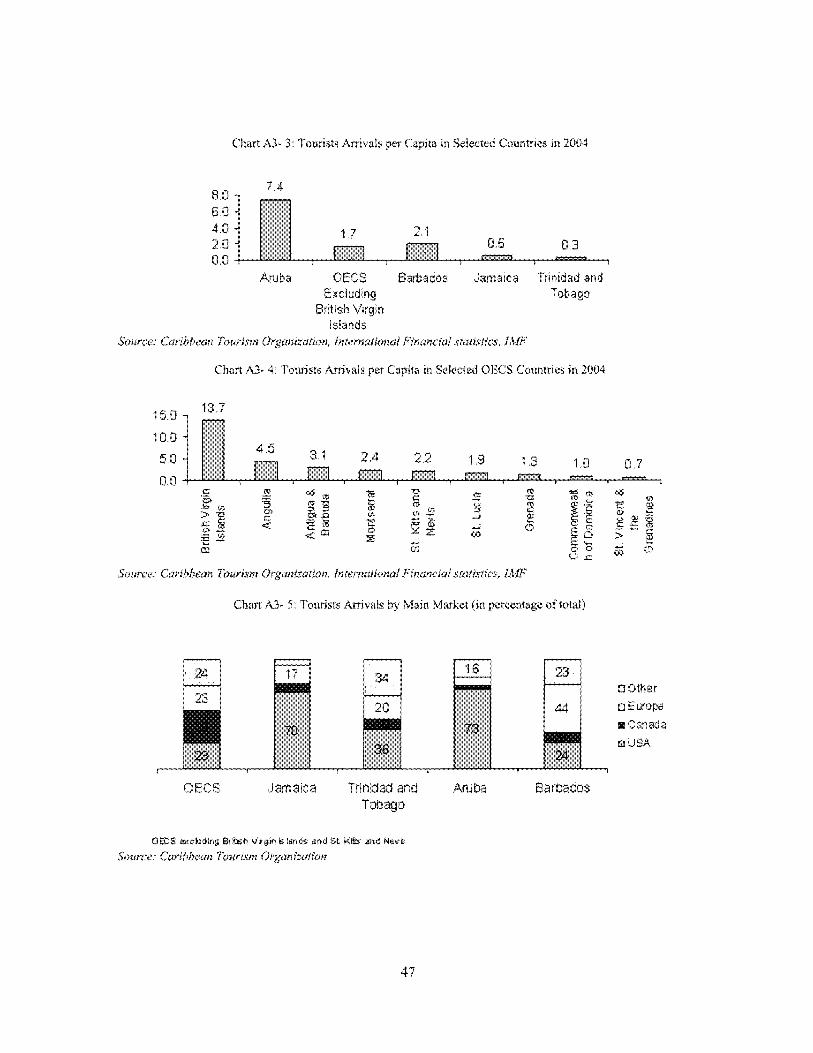

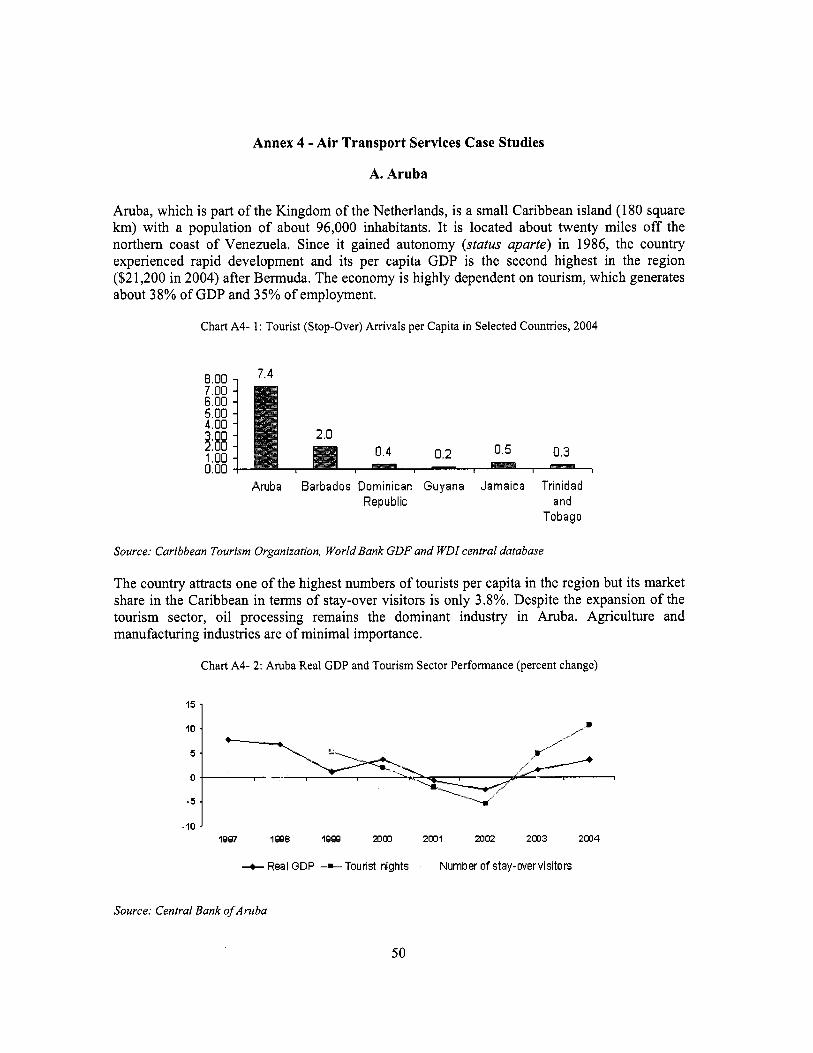

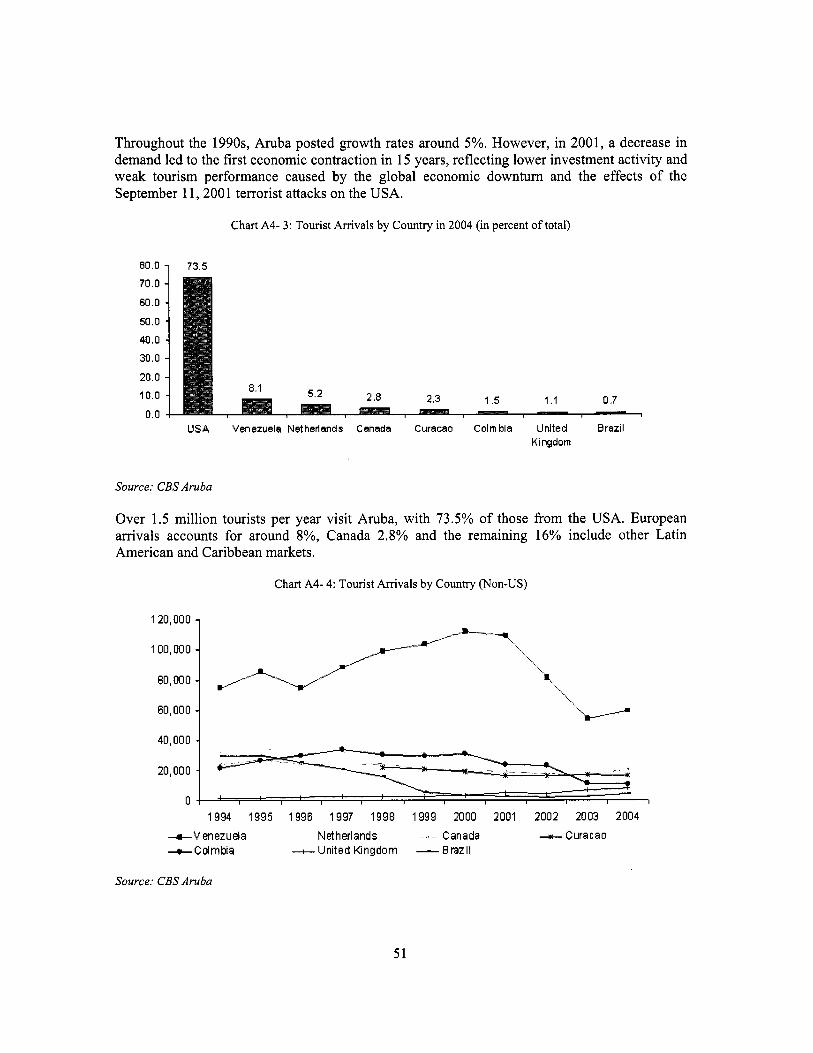

important feature o f air travel in the sub-region. However, the largest single market i s the Dominican Republic, which together with Cuba, has also been the fastest growing market in recent times. Within the OECS, Antigua and St. Lucia are the most important destinations while the British Virgin Islands and Anguilla are the fastest growing. Per capita tourism arrivals average slightly over 2 times the local population, about the same as in Barbados, but much less than Aruba where arrivals are equivalent to seven and a half times the local population.

Table 1 : Caribbean Arrivals by Air, 2004-2005

Source: CTO

Table 2: Intra-Caribbean Movements by Air, 2000-2003

Source: CTO

2.6 Whi le tourism i s predominantly driven by air transport, i t i s important to draw attention to the cruise market, which i s also strong and growing and which has been adding new destinations recently. According to the CTO, arrivals in 2005 amounted to 16.8 million persons, with the top four destinations being: The Bahamas (3.3 million), U S Virgin Islands (1.9 million), Cayman Islands (1.8 million) and St. Maarten (1.5 million) accounting for half o f the total arrivals. The strongest markets are generally those in the Northern Caribbean though cruises are likely to remain a significant factor in the future development o f tourism in the OECS, which in 2005 accounted for 8% o f passenger arrivals (1.2 million). Barbados i s seeking to develop i t s potential as hub connecting air and cruise traffic. A number o f OECS countries, including Antigua and Grenada, have invested in upgrading facilities to accommodate cruise ships. The economic significance o f the cruise market is, however, less on average than for the air arrivals as much less time and money i s expended by visitors in the visited Caribbean nations.

4

111. What Can Air Services D o For Tourism Development?

The air transport sector contributes to tourism and travel through: assuring safety and security, providing infrastructure, and providing adequate and appropriate a i r services through international and regional carriers. The Caribbean region has seen recent improvements in air safety and security, with a large number of the English-speaking countries obtaining a Category I status under the FAA IASA program, the most recent being the OECS in Apr i l 2006. Airport infrastructure is not a binding constraint to tourism development other than in a few exceptional cases. Efforts are under way - inter al ia through capacity expansion, improved management and private sector participation - to improve the arrival experience. A i r transport services are provided by a variety of carriers - with in the case of the US-Caribbean market, increasing competition f iom both legacy and low cost carriers to the dominant position of American Airlines. There are competing services on most routes, though with generally fewer alternatives on intra-Caribbean routes which are normally served by regional carriers. The proportion of airl i ft capacity allocated to intra-Caribbean traflc is much higher in the Eastern Caribbean than elsewhere. US-Caribbean fares are on average higher than comparable US domestic fares - although the difference is less marked in those markets which have adopted an “open skies” policy. The specific characteristics of the market for intra-regional services in the Eastern Caribbean has kept fares here relatively low, although this may be not be sustainable.

Air Safety and Security

3.1 One o f the most significant events affecting recent tourism development in the Caribbean has been 9/11 and i t s aftermath. Air safety and security are thus to be seen as paramount for consolidating the position o f the sector and are particularly important for securing the U S market. The Caribbean has recovered relatively well from the init ial shocks, and overall in fact better than other tourism regions, with tourism growth o f 7.1% recorded in 2003, 6.9% in 2004 and 3.6% in 2005., However there can be no cause for complacency. Growth could s t i l l fal l back again in the absence o f corrective measures being taken in regard to safety, security and ATI. Even wi th the implementation o f such measures, there i s the possibility that air travel and tourism wil l fal l o f f as the result of: renewed fears o f terrorist activity; and o f the consequent increase in security and delays and inconvenience encountered at airports in the USA and the sub-region.

3.2 In this regard, the ultimate objective for Caribbean nations i s obtaining Category 1 status under the International Air Safety Assessment (IASA) Program which i s managed by the Federal Aviation Administration (FAA). The program, first established in 1992, i s designed to determine the capacity o f foreign countries to adhere to international standards and recommended practices, including aircraft operation and maintenance, in conformity with the established norms o f the International C iv i l Aviation Organization (ICAO). This i s to ensure that any foreign carriers operating to and from the USA benefit from proper oversight in regard to safety by a competent c iv i l aviation authority. In addition, it i s a requirement that the airports from which direct flights leave for the USA comply with safety and security standards issued by the Transportation Safety Administration (TSA). Inspection programs have been carried out in conjunction with the FAA to assess which countries qualify. Category 1 status confers a range o f benefits to the countries concerned, in addition to the likely effect o f increasing marketability through a safety “seal o f

5

approval”, this including the opportunity to “code share” with U S airlines. One such benefit i s to allow the airlines o f that particular country to be eligible to fly into the USA, which may be a quite important consideration when countries assess the benefit o f entering into an “open skies” agreement as wil l be discussed in Chapter IV below. Following Table 3 below, many Caribbean countries whose c iv i l aviation arrangements do not currently enjoy Category 1 status do not currently have national airlines serving the U S A (or often any other international) market.

Country Aruba Barbados Belize Bermuda Cayman Islands Dominican Republic Haiti

Table 3: Av ia t ion Safety Status in Selected Caribbean Countries

Status Remarks 1

na na 2 Currently not serving USA 1 1 2 Currently not serving USA 2

Jamaica Netherlands Antilles OECS Suriname Trinidad & Tobago

1 1 1 Certification granted in 2006 1 1

Box 1: Airport Security in OECS

The events o f September 11,2001 (9/11) had a significant impact on the Eastern Caribbean island states on several fronts as the number o f tourist arrivals fel l . The resulting loss of tourism earnings, a key source o f government tax revenue and employment, created a liquidity crisis among OECS countries. The countries clearly recognized the potential gravity o f the economic damage and took steps to respond to these events.

Within six months of 9/11, the World Bank approved a regional program comprised o f 5 projects tailored to the individual needs o f Dominica, Grenada, St. Kitts and Nevis, St. Lucia and St. Vincent and the Grenadines. In addition to meeting the short term liquidity needs o f OECS countries through an emergency lending instrument, the Bank addressed the need to enhance security associated with the tourism industry in the countries. Prior to 911 1, ports and airports in the sub-region lacked modern security equipment and operated in an environment o f relaxed security,

To assist governments in meeting more stringent international security requirements, the Bank provided technical expertise and financial resources to enhance security at ports and airports with the aim of preventing acts o f terrorism and safeguarding the sub-region’s image as a safe tourism destination. The development objectives o f the Emergency Recovery Project were to: i) help safeguard and maintain the productive capacity o f the tourism sector by securing the industry’s energy needs; ii) enhance security at key airport and seaport facilities in line with international standards; and, iii) strengthen the country’s institutional capacity to develop and implement security plans, procedures and measures as mandated by the international civil aviation and maritime transport regulatory agencies.

As a result o f the project, international airports in the five participating countries have greatly enhanced their security arrangements, and the underlying cultwe in regard to safety, through an improvement in the regulatory framework, provision of training, installation of screening equipment, and construction of airport perimeter roads and fences. After having met all security guidelines required, all airports have been able to obtain International Civil Aviation Organization (ICAO) certification.

Key to project success was the establishment o f a cohesive capacity building program at the sub-regional level. The OECS Directorate of Civil Aviation, later the Eastern Caribbean Civil Aviation Authority (ECCAA), was involved early on in the project and effectively coordinated the institutional strengthening and training components o f the program. By coordinating various aspects of implementation, the ECCAA directly supported participating countries’ ability to address regional security issues. The authority i s now well positioned to apply regional standards and to conduct security audits in the OECS countries on behalf o f ICAO.

6

Air Transport Infrastructure

3.4 In addition to safety considerations, more efficient, customer-focused management of, and appropriate investment in, airport infrastructure are likely to improve the arrival and transit experience for passengers and increase tourism potential. Jamaica and the Dominican Republic are the only two countries which have introduced private operation and financing o f airports, using the instrument o f a long te rm concession o f airport operation to a private provider. These efforts seem to be registering some success in improving efficiency, service quality and covering costs - the concession o f Sangster Airport in Montego Bay, Jamaica for example should specifically help increase capacity for tourist arrivals, as witness the recent start up o f a new direct Virgin Atlantic service from London. In a number o f other countries, airport management i s being turned over to state owned statutory corporations (such as St. Lucia, TT, Grenada and Guyana), measures supplemented by the increased prevalence o f contracting out of airport services, Barbados, which i s the major hub for the Eastern Caribbean, i s currently undertaking - with public financing - a major renovation and capacity expansion at Grantley Adams Airport in advance o f the 2007 Wor ld Cup Cricket.

3.5 Airport infrastructure i s generally speaking not a binding physical constraint in regard to handling current and projected future demand. However, there are some countries whose principal airport runways are s t i l l unable to accommodate wide body jet aircraft (Guyana, St. Vincent and the Grenadines, and Dominica). There are other cases where further investment may shortly become necessary to improve service levels and aircraft turnaround time, where for example at peak periods there are significant numbers o f large aircraft seeking to arrive and depart (Antigua). In terms o f airfield security, most airports in the CARICOM area are compliant, though some deficiencies in relation to I C A O requirements have been noted in Jamaica, Grenada and Guyana4. The Caribbean region has an abnormally high density of international airports in close proximity, with the consequence that the volume o f services per station i s low by international standards. The Inter Vistas study indicated that most Caribbean airports have lower traffic volumes than the smallest US airports which are served by low cost carriers (LCC), and that none has a throughput o f more than 1 mi l l ion passengers per year5. There are some underexploited opportunities for the development o f sub regional “hubs” with higher capacity and service levels around which service “spokes” could be better deployed. Air traffic in the Eastern Caribbean employs Barbados and Antigua as principal hubs, with Port o f Spain, TT also providing a point through which intra-Caribbean travel can be facilitated. Future growth in traffic volumes i s thus likely to be much higher in these “hubs” than in other airports in the OECS.

3.6 Airport charges are typically much less important than passenger costs in the total cost o f services. These charges do seem to vary quite considerably between regional airports, as regional governments currently adopt different policies in regard to cost recovery and revenue generation.

World Bank 2005a. Inter Vistas Consulting 2006.

7

Air Transport Services

3.7 The Caribbean market i s currently served by a variety o f air transport services provided by a number o f international as well as by privately and state-owned regional carriers. Some, if not all, o f these carriers have been able to increase the level o f services in response to demand. I t i s a moot point as to whether the current capacity could be considered adequate in relation to demand, although there i s competition on most routes, though generally speaking less on the intra-Caribbean routes. Regional carriers have low load factors and are running at a loss as discussed further in Chapter V. There also continue to be concerns about cost, quality and reliability. Providing basic concerns on air safety and security would be addressed, this report would argue that efficiency and cost effectiveness of air transport services wil l be the major consideration in increasing the contribution o f air services to economic development o f the Caribbean region as a tourism destination. The measures that need to be taken are thus the principal subject for consideration later in this report.

3.8 Scheduled airline capacity - measured in terms o f departing seats - to the Caribbean appears to have fallen back marginally in 2005 compared to 2004, although growth in 2006 i s expected to be o f the order o f 4.7%. T h i s compares to an average global growth rate o f 5.9% for the same period6. US based airlines are the dominant players in the market (Table 4). American Airlines i s the largest service provider at over one third o f al l seats, this including i t s regional American Eagle service based in San Juan, Puerto Rico. This rather substantial degree o f concentration in one supplier i s being eroded however through increased activity o f competitors in the USA - both other “legacy” carriers attracted by higher available yields on international as opposed to domestic services and “low cost carriers” which have been expanding services from a historically l ow base figure. Services to and from the USA - and to some extent Canada - have been growing whereas those to and from Europe have on average stagnated (in fact a 1% decline i s expected in 2006 over 2005). Services from Latin America account for a very small percentage - in the range 3 to 4% o f seats and mostly to and from Venezuela - though there i s a strategic interest in the Caribbean in developing more air transport and business linkages with the region. Caribbean region based carriers are significant players, accounting for 28% o f available seats. As discussed further in Chapter V, there are significant differences in the markets and the associated challenges between those airlines competing directly with international carriers on external routes (such as Air Jamaica and BWIA) and those providing intra-Caribbean services often in competition only with each other (LIAT, Caribbean Star).

Airclaims 2006.

8

Table 4: Caribbean Airlift Capacity - by Airline (‘000, departing seats)

Air Jamaica 2,157 1,521 5 Charters 1,273 1,121 4 Source: Airclaims 2006

3.9 From the point o f view o f a country analysis, the strongest recent growth in capacity appears in regard to services to and from The Bahamas and Dominican Republic (Table 5) though in 2006, Antigua, St. Lucia and Jamaica are also expected to increase7. OECS countries account for about 10% o f airlift capacity. Puerto Rico remains the dominant market because o f the extensiveness o f air connections with the US and with San Juan as the largest hub in the Caribbean region. T h i s i s overall, however, a slower growth market, though intra-Caribbean movements have been growing at 2 to 4% per annum.

Table 5: Caribbean Airlift Capacity - by Country (‘000, departing seats)

Source: Airclaims 2006

’ Airclaims 2006.

9

3.10 The specific cases o f Aruba and Barbados - studies o f which are provided in Annex 4 o f this report - illustrate recent trends and the extent o f the diversity in the provision o f air transport capacity to Caribbean destinations which are heavily dependent on the tourism sector. Aruba had substantially expanded i t s AT1 capacity in the late 1990s to cater for growing tourist arrivals, over 70% o f which are from the USA. Aircraft movements have generally mirrored passenger arrivals with modest growth re-established in 2004 after several years o f post 9/11 decline. In a randomly chosen week in March 2006, 160 weekly flights were logged; o f which, 84 direct to or from 13 different US destinations, by 19 different carriers, Barbados’ growth in tourist arrivals has kept pace and generally slightly exceeded GDP growth in recent years, the largest portion o f arrivals coming from Europe, especially UK. In a randomly chosen week in February 2006, 455 weekly flights were logged, o f which 91 to major hubs in North America and Europe. There are 54 direct flights to 7 different destinations in the USA. Services are provided by 22 different scheduled carriers and by a number o f charter services (1 6% o f total).

Air Transport in the OECS

3.1 1 In Chapter 11, it was established that a very high proportion o f air arrivals in the OECS were from intra-Caribbean movements - in fact, as high as 30%, comparable to the figure for TT but higher than the Caribbean average o f 7% and much higher than the Jamaica’s o f 3%. Not surprisingly, the availability o f seats to the OECS follows a similar pattern, as highlighted in Table 6 below. In two cases - St. Vincent and The Grenadines and Dominica - 100% o f air traffic i s intra-Caribbean.

Table 6: OECS - Analysis o f Intra-Eastern Caribbean Airlift

Sources: World Bank 200Sd (a,b), CTO (c), Inter Vistas 2006 (d), Airclaims 2006 (e) Note: (1) non-stop flights only (2) E. Caribbean is OECSplus Barbados (3) some rounding errors

10

Air Fares

3.12 The Inter VISTAS consulting teams carried out a comparison o f fares in three markets - the U S domestic market; the US to Caribbean market (countries adopting an “open skies” (OS) policy); the U S to Caribbean markets (countries adopting a more restrictive set o f policies). On the basis on sample data drawn from 10 U S markets and 22 Caribbean destinations, the analysis concluded that on average: fares to OS Caribbean destinations were $71 higher than a US domestic comparator, whereas fares to “restricted” Caribbean destinations were $155 higher. Average fares on routes governed by a liberalized regime are 12% lower than on routes where more restricted agreements prevail. The presence o f a l ow cost carrier on a route tends to lower average fares by 16%, suggesting an effect o f liberalization that might be anything up to 28%. The averages do, however, tend to mask large variations between the data for city-pairs. The relationships have been found to be statistically significant.

3.13 The difference in actual fares between domestic routes and OS international routes could reflect higher operating costs on international services, the larger traffic volumes o f domestic routes (hence, lower costs) and the reluctance o f some U S domestic airlines to serve international destinations. Fares may tend to be higher under restrictive as opposed to liberal regimes as when fare controls are in force airlines may be unable to offer deals in response to any decline in traffic and thus make best use o f their yield management systems. Airlines may be forced to fly with empty seats, the revenue shortfall from which they must then compensate by seeking higher ticket prices.

3.14 There i s limited data available on trends in fares on intra-Caribbean services. The intra- regional air services market in the Eastern Caribbean has specific characteristics which make i t diff icult to compare to trends in international fares. Fares have tended to fal l over the recent past, perhaps by a factor o f 20-25% since 2000 and taking into account the introduction o f the services o f the privately owned Caribbean Star in direct competition to LIAT. W h i l e the traveling public has gained some benefit from this situation in the short run (subject to quality and reliability o f the service), the current fare levels may not be sustainable in view o f the financial situation o f the operators (they are losing money on a regular basis) and o f the need for LIAT to be properly capitalized in order to remain operational at all. The policy and industry specific issues are discussed in more detail in the succeeding chapters o f this report.

Inter Vistas 2006.

11

IV. Policv and Repulation of Air Services

Ai r services in the Caribbean are regulated by inter-governmental bilateral air service agreements (BASA), many of which incorporate restrictions to a greater or lesser extent, in regard to fare approval, designation of carriers, routes and capacity. I n practice however greater flexibility may be practiced, especially in regard to fares. Multi lateral A i r Service Agreements (MSA) , such as the one adopted by the Caribbean Community (CARICOW, exist but these are often also restrictive and have had limited impact to date in terms of improved a i r services. The arguments in favor of a liberal “open skies ’’ (OS) policy are persuasive and are broadly agreed in principle in the Caribbean. International experience on the benefit of a liberal, OS approach is broadly positive and not just in the relatively advanced cases of the USA and E U but in a variety of developing country settings as well. For the OS countries in the Caribbean - Aruba, Dominican Republic - the results have been largely positive - Jamaica is expected to shortly follow. This means that OECS, Barbados and TT (Trinidad and Tobago) w i l l be competing against destinations with the most liberal a i r services regimes that small countries can achieve in place.

Caribbean nations would be advised to adopt a fully unrestricted policy towards a i r services provided that both local airlines have a right to compete and that adequate arrangements are in place to ensure fair competition. The adoption of OS by individual Caribbean governments would be enhanced with a revised CARICOM M S A fully supportive of these principles. Individual member states may however not always be prepared to adopt and implement “open skies ’ I at the same pace. Key issues for the Caribbean nations concern implementation and the management of risks, in particular regard to service continuity and local state-owned airlines. National strategies and policy framework would need to speciJically address the risk of service provision shortfalls through the use of subsidies and protection of the competitive process to ensure benefits of competition are passed to consumers. Countries which have a signiJicant ownership interest in regionally based airlines w i l l need to adopt clear and appropriate policies to allow these airlines to either compete or go out of business. I n order to design and implement good policies, some countries may require selective strengthening of policy and regulatory capacity.

The existing regulatory framework

4.1 In l ine wi th international practice, air services currently are regulated in Caribbean nations via a series o f bilateral air service agreements (BASAs) entered into by each government. BASAs cover the framework under which the airlines o f one state are granted economic rights to fly into and beyond another state. BASAs, as elaborated via the result o f on-going bilateral negotiations, regulate the rights o f each country to designate one or more airlines, what routes the airlines can service, the capacity they can offer and their pricing o f the services. The details are usually covered by memoranda o f understanding that accompany each BASA. The key point i s that both nations need to agree to any changes. BASAs in the Caribbean generally contain a number o f restrictions, often more so for intra-Caribbean agreements than for others, though in practice some flexibility has been demonstrated, especially in regard to pricing.

12

4.2 Traditionally, governments can only designate airlines under BASAs that can be regarded as owned and controlled by nationals o f the designating nation. CARICOM nations have been in the forefront o f efforts to reduce the restrictiveness o f this requirement for smaller countries with small capital markets. This has resulted in I C A O adopting a “community o f interest” principle to assist developing nations in similar positions - under a 1983 non-mandatory Resolution A24-12. Under the CARICOM M A S A (CMASA) - discussed further below - there i s already enshrined the concept o f a CARICOM carrier (article l(f)) in an attempt to address this problem. However, for air services beyond the Caribbean, agreement o f the bilateral partner government remains necessary. There appears to be increasing openness on this issue e.g. the issue i s explicitly and generally favorably addressed in the Memorandum o f Consultations between the Jamaican and U S governments in the context o f the finalization o f the new OS BASA. Further practical expressions o f this intent are that BWIA i s designated by Antigua and St. Lucia in their BASAs with the UK and Air Jamaica by Barbados and St Lucia in their BASAs with the USA.

4.3 The ability o f designated foreign airlines to serve “in-between” and “beyond” markets (so-called fifth freedom rights) i s often highly restricted. This can be potentially important in thinner markets e.g. a European carrier flying to Antigua and Grenada would generally need explicit agreement to provide services between say Miami and Antigua en-route and between the two Caribbean nations. I t i s understood that there are significant “grand parented” rights for some international carriers such as British Airways in this respect. The use o f such rights - if included in a BASA - does in theory provide an option for providing additional competition on, and service options for, intra-regional traffic in the Eastern Caribbean. The practical interest o f international airlines appears, however, to be limited, as such services cannot usually be profitably provided on the wide body aircraft that they employ.

4.4 A number o f countries in the Caribbean have now either adopted, or are reviewing the advantages o f adopting, an OS policy with the USA. This represents the most liberal option with a substantial degree o f openness in regard to pricing, airline and route designation. The comparison o f the experiences o f one such country - Aruba - as opposed to a country that continues to adopt a more restrictive regime - Barbados - are illustrated in Box 2 below (with further detail in Annex 4).

13

Box 2: Air Services Policy in Aruba and Barbados

Aruba i s part o f the Netherlands but has enjoyed an autonomous status since 1986. Influenced by the experience o f the Netherlands, Aruba was an early adherent to liberal air transport policies, signing an open skies agreement with the USA in September 1997 including the granting o f 5‘h freedom rights. There are 18 bilateral service agreements in effect in total, most o f the rest o f which incorporate some degree o f restriction, such as air carrier and destination designation. Four agreements have restrictions on capacity and six on frequencies o f service.

There has been growth in the number o f airlines and the frequency o f services with the USA since 1997, albeit not al l o f that can be attributed to air services policy, The number o f U S scheduled carriers has increased from one to five and the number o f charter flights have expanded by 3.6 times. There are presently no registered national airlines providing services. There were two national airlines prior to OS, both o f which subsequently have ceased operations.

Barbados i s a Commonwealth country, which has been increasingly dependent on tourism, predominantly from Western Europe. Its airport also serves as a hub for the Eastern Caribbean with substantial intra-CARICOM air traffic. Barbados has no national airline, Two designated CARICOM carriers, BWIA and LIAT, account for 35% of traffic. Air access i s defined by 18 BASAs, none o f which are “open skies”. Eleven agreements provide for multiple airline designation, six for single designation, All agreements provide for double approval o f tariffs, which i s restrictive in principle and practice. Passenger capacity and frequency o f flights are not formally restricted but are required to be approved by the authorities.

I

Regional air service agreements

4.5 In the Caribbean region, air transport policy and regulation at the national level has to take cognizance o f the existence o f multilateral air service agreements (MASA), which may impose specific additional obligations. There are two such agreements which are relevant for the countries o f this study - the CARICOM M A S A (CMASA) which i s reviewed in more detail below and the air transport agreement o f the Association o f Caribbean States (ACS)9. The ACS agreement i s intended to support the objectives o f the 25 member grouping, in particular regard to the establishment o f a “sustainable tourism zone” in the region. The agreement was formalized in February 2004 but has yet to come into effect. I t has been signed by 15 member countries but ratified only by six. I t i s thought unlikely in any event that this agreement could be implemented in i t s current form as it contains restrictions which would conflict with the provisions of the bilateral agreements signed by some Caribbean nations, for example: the agreement limits signatories to designate two airlines and restricts the issuance o f f i f th freedom rights.

4.6 By contrast, the CMASA i s legally in effect. T h i s agreement does at this time contain a number o f restrictions and clauses that have been agreed by member countries to be in need of revision, as per Box 3 below. With the implementation o f the Caribbean Single Market and Economy (CSME) for CARICOM members it i s recognized that some o f the provisions o f the C M A S A wil l need up-dating as they are inconsistent with the Revised Treaty o f Chaguaramas. A revised C M A S A might be expected to support trade and economic development in the region through: creating an open market for air services to encourage competition and expand opportunities for regional airlines, improve services and reduce prices; facilitating (or at least not constraining) the adoption by member countries o f liberal air service arrangements with external partners. However, there i s a risk that the reform o f the C M A S A wil l fal l short and that some

See Annex 2. Membership includes 17 Caribbean countries and a number o f Latin American countries having sea borders with the Caribbean.

14

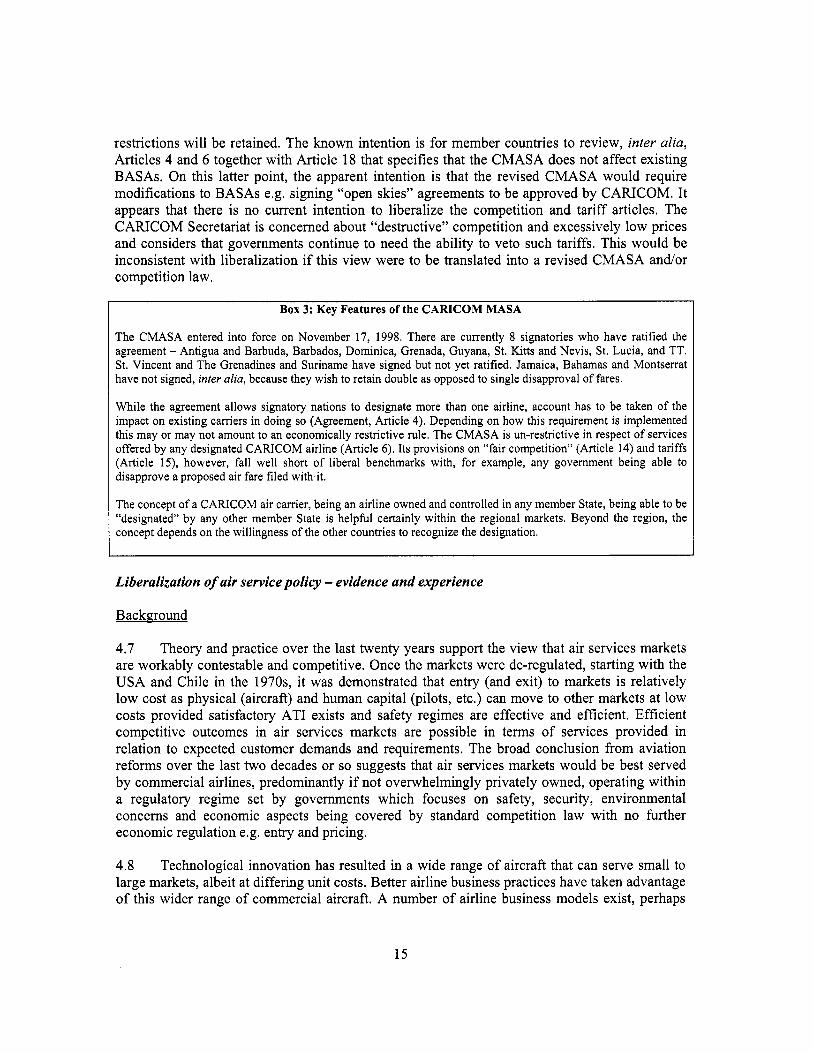

restrictions wi l l be retained. The known intention i s for member countries to review, inter alia, Articles 4 and 6 together with Article 18 that specifies that the C M A S A does not affect existing BASAs. On this latter point, the apparent intention i s that the revised CMASA would require modifications to BASAs e.g. signing “open skies” agreements to be approved by CARICOM. I t appears that there i s no current intention to liberalize the competition and tariff articles. The CARICOM Secretariat i s concerned about “destructive” competition and excessively low prices and considers that governments continue to need the ability to veto such tariffs. This would be inconsistent with liberalization if this view were to be translated into a revised C M A S A andor competition law.

Box 3: Key Features o f the CARICOM MASA

The CMASA entered into force on November 17, 1998. There are currently 8 signatories who have ratified the agreement - Antigua and Barbuda, Barbados, Dominica, Grenada, Guyana, St. K i t t s and Nevis, St. Lucia, and TT. St. Vincent and The Grenadines and Suriname have signed but not yet ratified. Jamaica, Bahamas and Montserrat have not signed, inter alia, because they wish to retain double as opposed to single disapproval o f fares.

Whi le the agreement allows signatory nations to designate more than one airline, account has to be taken o f the impact on existing carriers in doing so (Agreement, Article 4). Depending on how this requirement i s implemented this may or may not amount to an economically restrictive rule. The CMASA i s un-restrictive in respect o f services offered by any designated CARICOM airline (Article 6). Its provisions on “fair competition” (Article 14) and tariffs (Article 15), however, fa l l well short o f liberal benchmarks with, for example, any government being able to disapprove a proposed air fare filed with it.

The concept o f a CARICOM air carrier, being an airline owned and controlled in any member State, being able to be “designated” by any other member State i s helpful certainly within the regional markets. Beyond the region, the concept depends on the willingness o f the other countries to recognize the designation.

Liberalization of air service policy - evidence and experience

B ac knround

4.7 Theory and practice over the last twenty years support the view that air services markets are workably contestable and competitive. Once the markets were de-regulated, starting with the USA and Chile in the 1970s, i t was demonstrated that entry (and exit) to markets i s relatively l ow cost as physical (aircraft) and human capital (pilots, etc.) can move to other markets at low costs provided satisfactory AT1 exists and safety regimes are effective and efficient. Efficient competitive outcomes in air services markets are possible in terms o f services provided in relation to expected customer demands and requirements. The broad conclusion from aviation reforms over the last two decades or so suggests that air services markets would be best served by commercial airlines, predominantly if not overwhelmingly privately owned, operating within a regulatory regime set by governments which focuses on safety, security, environmental concerns and economic aspects being covered by standard competition law with no further economic regulation e.g. entry and pricing.

4.8 Technological innovation has resulted in a wide range o f aircraft that can serve small to large markets, albeit at differing unit costs. Better airline business practices have taken advantage o f this wider range o f commercial aircraft. A number o f airline business models exist, perhaps

15

most simply characterized by the traditional “legacy” airlines often offering “hub and spoke” or network services increasingly linked via international alliances on the one hand e.g. American Airlines and so called l ow cost carriers (LCCs) on the other, e.g. Southwest or Spirit. Analysts consider that the latter s t i l l have a significant unit cost advantage over the former because of more efficient use o f physical and human capital, although legacy carriers are moving to reduce their costs in the face o f the competition. Southwest only uses Boeing 737s for example, reducing costs o f maintenance and operations. The general expectation i s that real air fares on average wil l continue to decline with falling unit costs being passed onto to customers as a result o f competition. With lower and reducing costs it would thus become profitable for existing and new airlines to serve progressively smaller markets. This i s a factor that i s relevant for some o f the smaller Caribbean air markets.

International

4.9 Empirically, there i s evidence that liberalization has been associated with increased services and lower fares. The evidence i s stronger perhaps in the US and EU markets where more extensive analysis has been carried out - but the positive impacts are also fel t in a number o f diverse, developing country settings, see Box 4 below. The effects o f comprehensive liberalization on the air markets for markets as diverse as Latvia” and India are dramatic.

4.10 In the USA, air fares are estimated to be 24 percent lower than what they would have been if the regulated market had continued”. Studies o f the effects o f OS air service agreements on the U.S. and EU markets and smaller markets such as the Netherlands-Kenya routes and Australian markets also show benefits. Studies also highlight that there are benefits resulting from earlier rather than later liberalization which could provide a strategic advantage - such for the Netherlands versus France.

Box 4: Recent International Experience in Air Transport Policy Reform

Following the initial experience of Chile, a number of countries in different parts of the world have implemented policy reforms broadly consonant with OS.

- Chile - The government considers that the OS policy adopted in 1989 has contributed to a 10 percent per annum growth in passengers up to the present, and a 9 percent per annum growth in cargo. The number of services offered internationally has increased from 104 to 329 per week. This has not however been at the expanse of Chilean carriers, who account for 1,487 services now, compared to 47 per week before.

Lebanon - A recent analysis carried out on behalf of the EU indicates that this country’s OS policy has helped to deliver a dynamic air market as the tourism sector rebounds’*. The local airline - MEA - appears to have coped well with the new competitive environment.

Latvia - Comparing the performance of Latvia to Armenia as regards services to the EU, there i s a dramatic difference in fares, with those in the more open Latvian market being up to 40% lower. I t does, however, appear that entry into the single EU air market has created more rapid traffic growth than that obtained since the earlier introduction o f OS.

lo World Bank 2006.

’’ European Commission (2004) 74 Final February 2004. Cliff Winston and Steve Morrison, Brookings Institution, Washington DC 2003.

16

4.11 Countries interested in pursuing a liberal approach to air services have the option to participate in the Multilateral Agreement on the Liberalization o f International Air Transportation (MALIAT). The provisions are similar to those o f the U S style OS agreements, but would apply multilaterally as opposed to bilaterally. A country can request to participate provided that it has demonstrated that i t has acceded to a number o f stated international security agreements. Current signatories are Brunei, Chile, New Zealand, Singapore, Samoa, Tonga and the USA. The New Zealand government i s the depository state for the agreement.

Caribbean-Speci f ic

4.12 Aruba has signed an OS agreement with the U S A and generally appears to follow the liberal policies o f the Netherlands. I t i s noteworthy that following the signature o f the OS agreement with the USA a number o f airlines entered in direct competition with American Airlines that had previously dominated the USA-Aruba markets. The latter’s market share fe l l significantly. U S charter airlines increased output significantly also. Aruba i s less than hal f the size o f Barbados but i t s connectivity in terms o f the number o f flights into major airports such as Miami appears approximately the same. In the case o f the Dominican Republic, there has been continued growth in air traffic and passenger arrivals since the signing o f an OS agreement with the USA in December 1999. O n average, the rate o f growth is, however, not greater than in the period preceding OS though the growth o f traffic and increase in carriers i s marked to some destinations, such as Punta Cana.

4.13 The evident increases in airline services to Aruba and the Dominican Republic cannot, therefore, be attributed simply and only to the adoption o f OS policies. In both cases, the countries have benefited from the development and marketing o f an attractive tourism product and government policies that have been supportive o f private sector development in the sector. Barbados - a case study on which i s also included in Annex 4 - has tended to adopt more restrictive policies, have been relatively successful in developing air services - helped in this case by the role o f a “hub” that i t plays in the southern part o f the Eastern Caribbean. Barbados air fares have however been higher on average than some o f the neighboring islands.

4.14 Jamaica i s at an advanced stage in i ts discussions with the US on the implementation of an OS agreement. The agreement was negotiated in October 2002, providing for unrestricted capacity and frequency on al l routes, but has yet to come into effect. In addition to other benefits, the signing o f the agreement i s seen as advantageous to Air Jamaica’s prospects as i t would open up service opportunities beyond the 10 destinations in the USA included in the current more restrictive BASA. As and when this agreement i s finalized and put into effect, countries in the Caribbean operating more restrictive agreements - such as OECS and Barbados - would be faced by an increased number o f countries adopting OS policies and which are likely to be increasing the quantity o f international air services to their destinations. There is, thus, the potential for some diversion o f business to countries as a result o f increased competition from countries adopting more liberal regimes and away from the Eastern Caribbean.

4.15 Standard competition law i s generally considered to appropriately address concerns about predatory pricing, which often arise in debates over the liberalization o f air markets. This i s

17

generally absent in the focus countries o f this study, with the exception o f Jamai~a '~ . CARICOM has initiated work in this area, which should result in the establishment o f a CARICOM Competition Policy Commission. While it i s explicitly seen as a mechanism to assist the implementation o f the CSME, it i s unclear at this stage whether air services markets wil l be covered by the law and the Commission or not. Each member country would have to agree to this in any event.

Specific policy issues of concern to the Caribbean

Service continuitv

4.16 When assessing air service liberalization reform propositions, policy makers are often concerned about potentially greater risks to the continuity o f services in liberalized and more commercial markets. This i s l ikely to be particularly so in the Caribbean region for a number o f reasons: principally the need to ensure some level o f access and connectivity between the various island countries given the existence o f few, if any, modal alternatives to air transport; additionally the concern that the current air transport services to the smaller islands such as in the Eastern Caribbean might not be continued under a more liberal, market-oriented environment. The Caribbean countries would thus be advised to consider whether or not to adopt explicit policies as to the situations in which they would intervene to secure either andor: a given level o f service that would not be provided as a result o f competition in the market; a level of (subsidized) fares either generally or to specific groups that would otherwise not be attainable through competitive service provision. I t i s not evident that any such policies have been adopted. The alternative approach - where (such as with LIAT in the Eastern Caribbean) a regional state- owned airline i s implicit ly expected to cover this service requirement without, however, having the resources to do so - i s neither preferable, nor likely sustainable over the medium term.

4.17 International experience suggests that air transport services will generally be available in the absence o f restrictive economic regulation including entry and air fare controls. Prices charged will depend on a range o f factors - with average prices often being higher in smaller markets where technically available scale economies are less likely to be utilized and competition i s limited. Fixed costs, while less important than in the infrastructure services markets, s t i l l do exist. Also costs, on a passenger-kilometer basis, reduce as route length increase. Evidence also suggests that the presence o f competition, particularly from LCCs, lowers average prices14. Al lowing airlines pricing freedom within the limits o f general competition law i s likely to result in the maximum achievable level o f services. I t would thus be generally expected that more services, rather than less, would be provided under a liberal policy environment than under a restricted regime and that this should apply also in the Caribbean.

4.18 Should the Caribbean region more generally and explicitly adopt liberalized air services policies, service provision decisions would be made by airline management, including decisions to cut or vary services and raise fares. Compared to a situation where governments own airlines

l3 In principle in Caribbean international air markets redress can be sought using the partner nation's law, for example BWIA could use U S law if it considered that a US carrier was engaging in anti-competitive predatory behavior in the TT-US market. l4 See also Inter Vistas Consulting June 2006

18

can direct their operations, governments often fee l exposed to adverse polit ical consequences o f commercial decisions particularly when alternative services may not be directly comparable e.g. passenger sea ferries versus air services. Under the policy approach proposed here, loss-making airlines would reduce services. Air fares may init ially r ise because o f reduced competition but operating costs would fal l somewhat with higher load factors and more efficient competing airlines may be encouraged to enter the market, thus offsetting the ability to raise prices. In any event, remaining airline(s) would have stronger incentives to serve profitable markets and service levels would almost certainly rise. Very small markets l ike Montserrat would likely get services, however, at “high” prices reflecting the high costs, in the absence o f any explicit subsidies. I t i s likely that many customers - certainly those in the tourism and business sectors - will be willing and able to pay the prices to order to benefit from the available services.

4.19 The high price o f services - and their relatively infrequency - in relation to a government “benchmark” would, however, be o f legitimate policy concern insofar as this might adversely impact intra-Caribbean travel movements which do have broader economic and social benefits. There would be an argument for subsidizing such travel - in order to capture such benefits - if this would not otherwise take place at market service and fare levels. In the current situation, however, it i s difficult to identify and quantify the extent o f “social” air travel, given that the customer base for air services i s a heterogeneous one, e.g. even in regard to St. Vincent and The Grenadines and Dominica which are totally dependent on regional, intra-Caribbean services, a large proportion o f travelers are tourists or persons on private or government business. Nor i s information widely available on route profitability, with a likely substantial degree o f cross- subsidization o f loss-making routes practiced by both LIAT and Caribbean Star. Caribbean governments - and specifically those o f the OECS - would thus be advised to undertake further work in this area and to ensure that the capacity o f the responsible policy and regulatory authorities in their countries are strengthened to carry out andor supervise such work.

4.20 Explicit subsidies via contracts with airlines would in principle be an appropriate mechanism to address remaining air service adequacy concerns if the government considered this to be the best use o f tax revenue and value for money could be achieved e.g. through competitively awarded tenders or auctions. Sound public policy would, however, suggest that before any such policy i s adopted the proposal should pass a cost-benefit test in addition to government funds being available. In this regard, the policy - and the mode by which i t should be implemented - would also have to address the following points:

* * * *

* *

What are the objectives o f the policy? Who are the target beneficiary groups or communities? What i s subsidized and how i s the level o f subsidy determined? What are the arrangements for managing payment o f any subsidy and ensuring it i s correctly used (and targeted)? How i s the air service provided - on a competitive basis, or through allocation? How i s the performance o f the airline to be monitored and service contracts periodically renewed?

4.21 There i s some relevant international experience that could be tapped by Caribbean policy makers in designing a policy framework to underpin service continuity with some specific

19

examples provided in Box 5. Many o f the largest countries or blocs which have been in the forefront o f air service liberalization - this including the USA, EU and Australia - do have essential services policies in place as the (limited) application o f “public service obligation” i s recognized. The extent to which essential services are provided under such policies, whether with or without financial subsidy, i s quite limited, though the services are undoubtedly important for the beneficiary communities. The issue o f service continuity i s recognized in a number o f different developing country settings - including Cape Verde and Madagascar - although there are relatively few examples o f a successful scheme being launched and sustained. The Madagascar experience i s quite illustrative o f the practical difficulties that might be encountered in implementing a service support scheme in a resource-challenged environment. In the case o f Cape Verde, a policy to secure inter-island maritime service on designated unprofitable routes through competitive bidding for least cost subsidy appears to have been successful. The policy has created additional supply options at a subsidy cost much lower than had been expected.

Box 5: Examples o f Subsidized Air Services