capture insight performance attribution · n // 2 today’s agenda » webinar details »...

TRANSCRIPT

CAPTURE INSIGHT PERFORMANCE ATTRIBUTION

WHAT DOES PAST PERFORMANCE ATTRIBUTION

SAY ABOUT FUTURE ACTIVE RISK?

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

2

TODAY’S AGENDA

» Webinar details

» Introduction to Bloomberg Portfolio Risk & Analytics

» Understanding customization

» Total return attribution

» Factor based attribution

» Analysis of active forward risk and risk bets

» Attribution analysis on your proprietary data

» Introduction to multi asset class attribution

» Q&A

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

3

MULTI ASSET CLASS, PORTFOLIO RISK

AND ANALYTICS SOLUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

4

A CUSTOMIZABLE SOLUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

5

SLICE AND DICE DATA

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

6

GRAPHICAL REPRESENTATION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

7

REPORTS VIA EXCEL OR PDF

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

8

CONTRIBUTION TO RETURN - TOTAL RETURN (BRINSON) MODEL

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

9

POWERFUL GRAPHICAL SUMMARY

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

10

FACTOR BASED ATTRIBUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

11

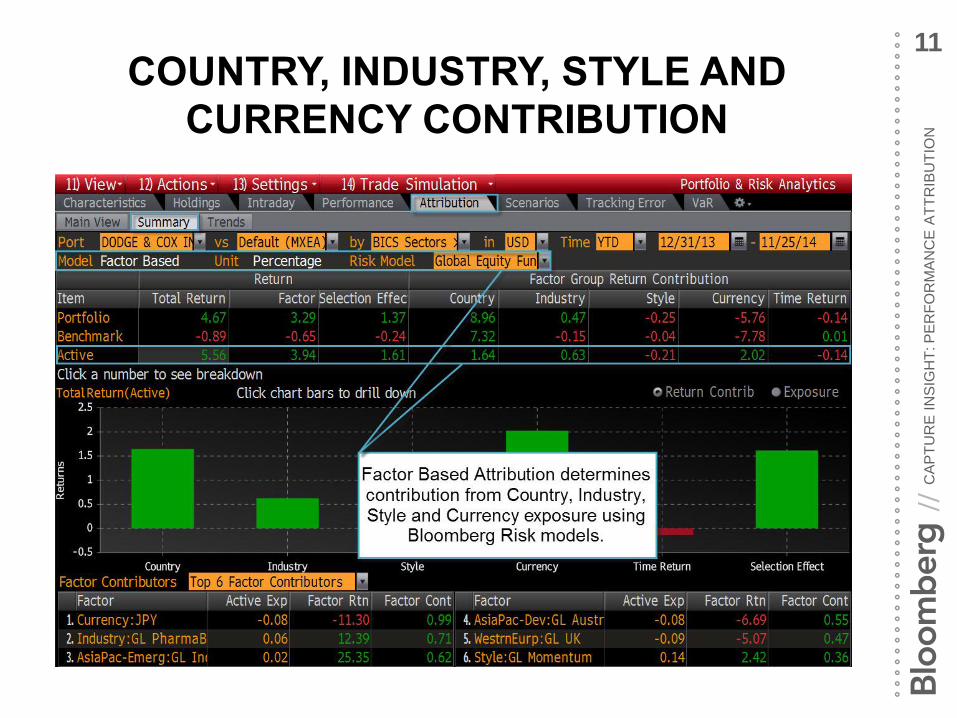

COUNTRY, INDUSTRY, STYLE AND

CURRENCY CONTRIBUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

12

BLOOMBERG OFFERS TRANSPARENCY

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

13

EXPOSURE CONSIDERED

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

14

RECAP SO FAR…

Portfolio return can be explained as contribution to

return from multiple perspectives:

• Total Return from a BICS, or Country, or

customized ‘Waterfall’ to slice and dice holdings.

• Factor Based Returns explain Industry, Style,

Country and Currency contribution.

Whether articulating performance to investors or

analyzing a potential new fund investment,

portfolio attribution explains past performance and

can inform your forward risk.

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

15

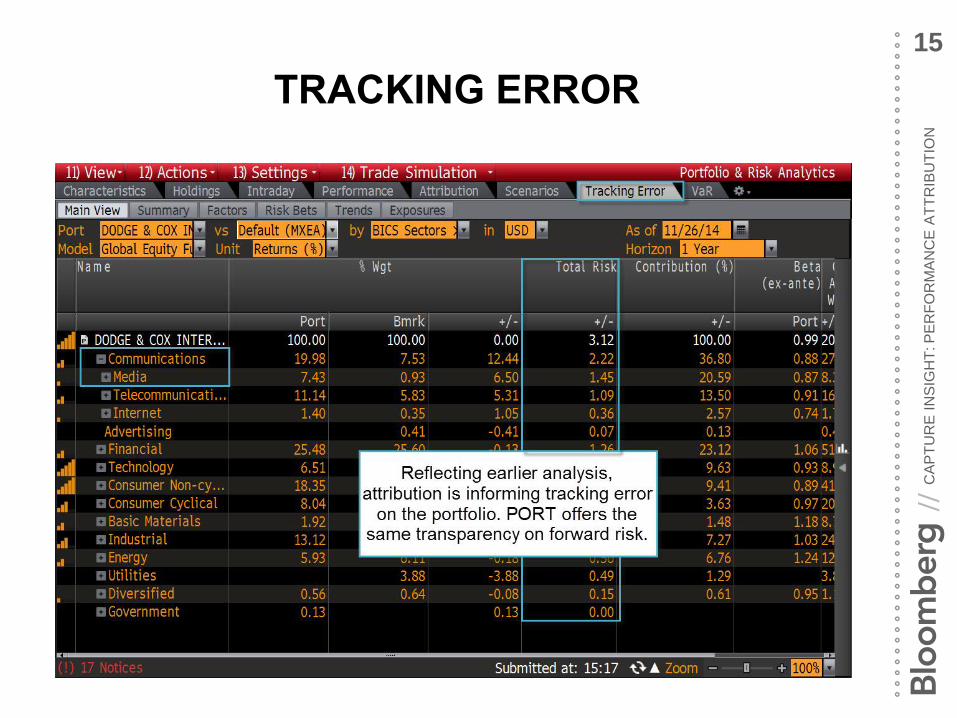

TRACKING ERROR

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

16

FACTOR TRANSPARENCY

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

17

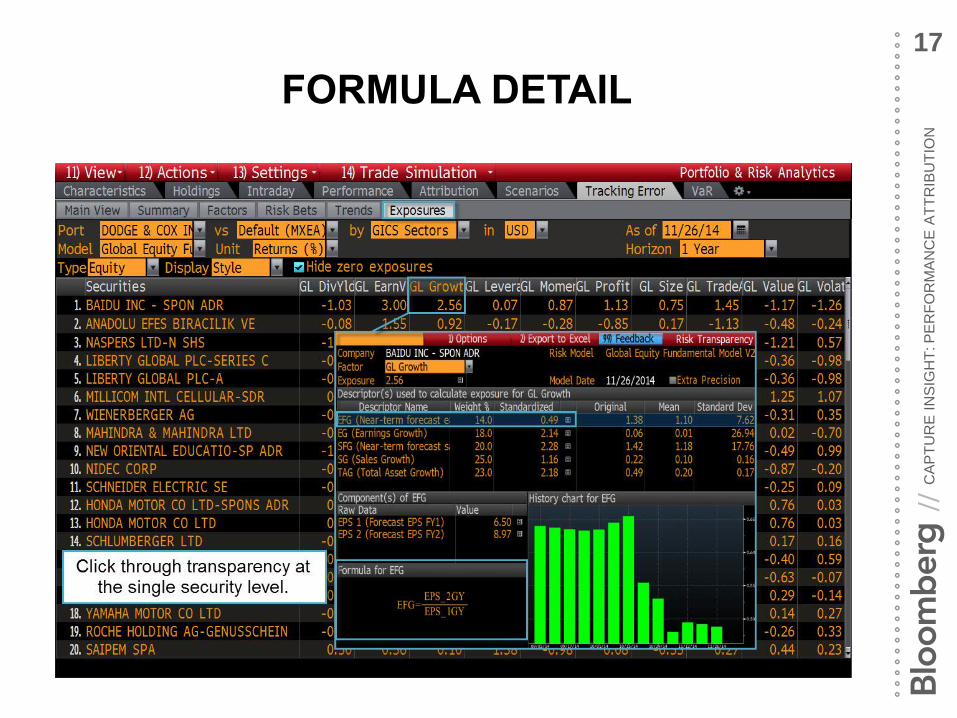

FORMULA DETAIL

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

18

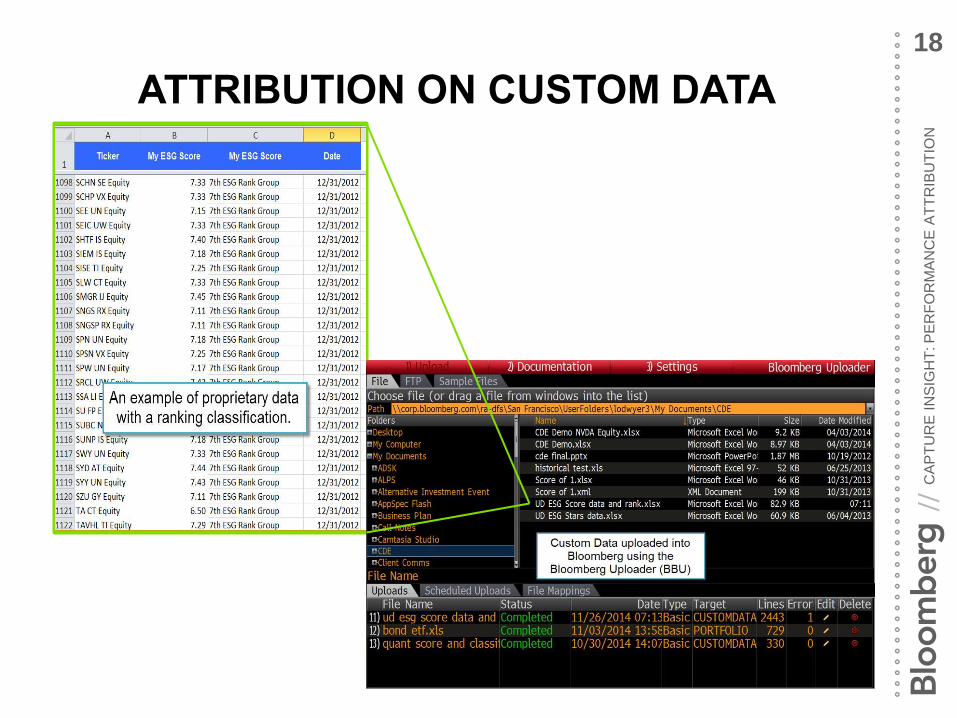

ATTRIBUTION ON CUSTOM DATA

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

19

DESCRIBE A PORTFOLIO WITH

CUSTOM CLASSIFICATIONS

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

20

UNDERSTAND YOUR CONTRIBUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

21

A MULTI ASSET CLASS SOLUTION

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

22

MULTIPLE ASSET CLASSES IN A

SINGLE PORTFOLIO OR BENCHMARK

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

23 MORE RESOURCES

• Contact your Bloomberg Rep for training, brochures and white papers

• HELP<GO> for further explanation and videos

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

WEBINAR DETAILS - RECAP

» On Demand

• This webinar will be available ON DEMAND starting on 12/12/14 and available for 90 days

» Slide availability

• The slides will be available through the ON DEMAND link to view this webinar; they will also be attached to the post webinar mailing

» Q&A

• We will attempt to answer as many questions as possible

• Additional answers to questions asked during today’s webinar will be aggregated and part of the post-mailing sent out the following week

» Inviting a colleague

• If you’d like to invite a colleague to view the ON DEMAND version of this presentation, they may register at AMER: http://www.bloomberglp.com/performanceattribution EMEA/APAC: http://www.bloomberglp.com/attribution

24

CA

PT

UR

E I

NS

IGH

T: P

ER

FO

RM

AN

CE

AT

TR

IBU

TIO

N

//

CONTACT >>>>>>>>>>>>>>>>>>>>>>>> [email protected] NEW YORK +1 212 617 7070 LONDON +44 20 7330 7099 SINGAPORE +65 6212 9798